improving public debt management in the oic member countries · comcec coordination office february...

TRANSCRIPT

Improving Public Debt Management In the OIC Member Countries

COMCEC COORDINATION OFFICE March 2017

COMCEC COORDINATION OFFICE

February 2017

Improving Public Debt Management in the OIC Member Countries

COMCEC COORDINATION OFFICE March 2017

This report has been commissioned by the COMCEC Coordination Office to the IfoInstitute. The report was prepared by Martin Mosler, Prof. Dr. Niklas Potrafke, Dr. MarkusReischmann (Project Coordinator), Dr. Marina Riem, Prof. Dr. Siegfried Schönherr, Prof. Dr.Günther Schulze, Dr. Andreas Steiner (CoProject Coordinator) and Prof. Dr. TimoWollmershäuseras well as researchassisstants.Viewsand opinionsexpressed in the reportare solely those of the author(s) and do not represent the official views of the COMCECCoordinationOfficeortheMemberStatesoftheOrganizationofIslamicCooperation.Thefinalversion of the report is available at the COMCEC website.* Excerpts from the report can bemadeaslongasreferencesareprovided.AllintellectualandindustrialpropertyrightsforthereportbelongtotheCOMCECCoordinationOffice.Thisreportisforindividualuseanditshallnotbeusedforcommercialpurposes.Exceptforpurposesof individualuse,thisreportshallnotbereproducedinanyformorbyanymeans,electronicormechanical,includingprinting,photocopying, CD recording, or by any physical or electronic reproduction system, ortranslated and provided to the access of any subscriber through electronic means forcommercialpurposeswithoutthepermissionoftheCOMCECCoordinationOffice.

Forfurtherinformationpleasecontact:COMCECCoordinationOfficeNecatibeyCaddesiNo:110/A06100YücetepeAnkara/TURKEYPhone:903122945710Fax:903122945777Web:www.comcec.org*Ebook:http://ebook.comcec.org

i

Table of Contents

List of Figures ......................................................................................................................................................... iii

List of Tables ........................................................................................................................................................... vi

List of Acronyms ................................................................................................................................................... vii

Executive Summary ............................................................................................................................................... 1

1 Introduction ................................................................................................................................................... 9

1.1 DefinitionofPublicDebtManagement........................................................................................................9

1.2 PerformanceIndicatorsandBestPractices...........................................................................................10

2 Global Practices in Public Debt Management .................................................................................. 19

2.1 DescriptiveStatisticsandPerformanceIndicators.............................................................................19

2.1.1 PublicDebtDynamics.........................................................................................................................19

2.1.2 GovernmentBudgets..........................................................................................................................22

2.1.3 DebtStructures......................................................................................................................................24

2.2 InstitutionalFrameworks...............................................................................................................................33

2.3 LessonsLearnedandRelevanceforOICMemberCountries..........................................................37

2.4 SurveyResults.....................................................................................................................................................38

3 Public Debt Management in the OIC Member Countries .............................................................. 44

3.1 DescriptiveStatisticsandPerformanceIndicators.............................................................................44

3.1.1 PublicDebtDynamics.........................................................................................................................44

3.1.2 GovernmentBudgets..........................................................................................................................46

3.1.3 DebtStructures......................................................................................................................................49

3.2 InstitutionalFrameworks...............................................................................................................................56

3.3 IslamicFinanceinPublicDebtManagement.........................................................................................58

3.3.1 IslamicFinance......................................................................................................................................58

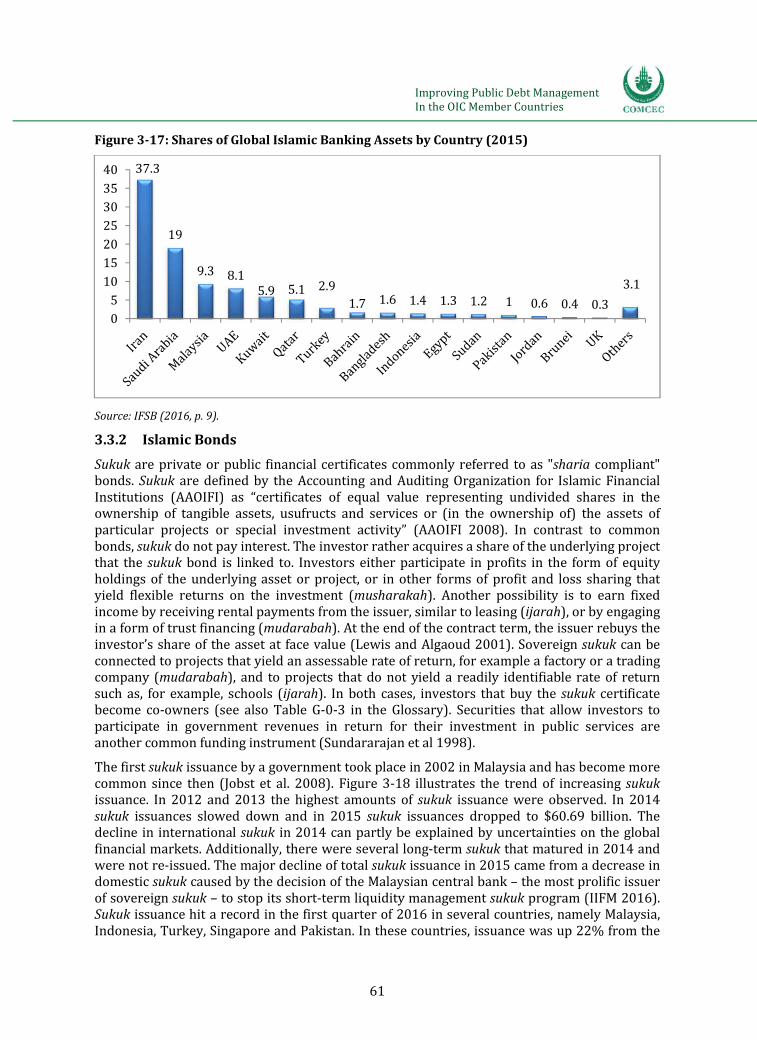

3.3.2 IslamicBonds.........................................................................................................................................61

3.4 LessonsLearned.................................................................................................................................................66

4 Public Debt Management in Individual OIC Member Countries................................................ 69

4.1 CaseStudies..........................................................................................................................................................70

4.1.1 IslamicRepublicofTheGambia.....................................................................................................70

4.1.2 RepublicofMozambique...................................................................................................................77

4.1.3 RepublicofTogo...................................................................................................................................84

ii

4.1.4 RepublicofUganda..............................................................................................................................91

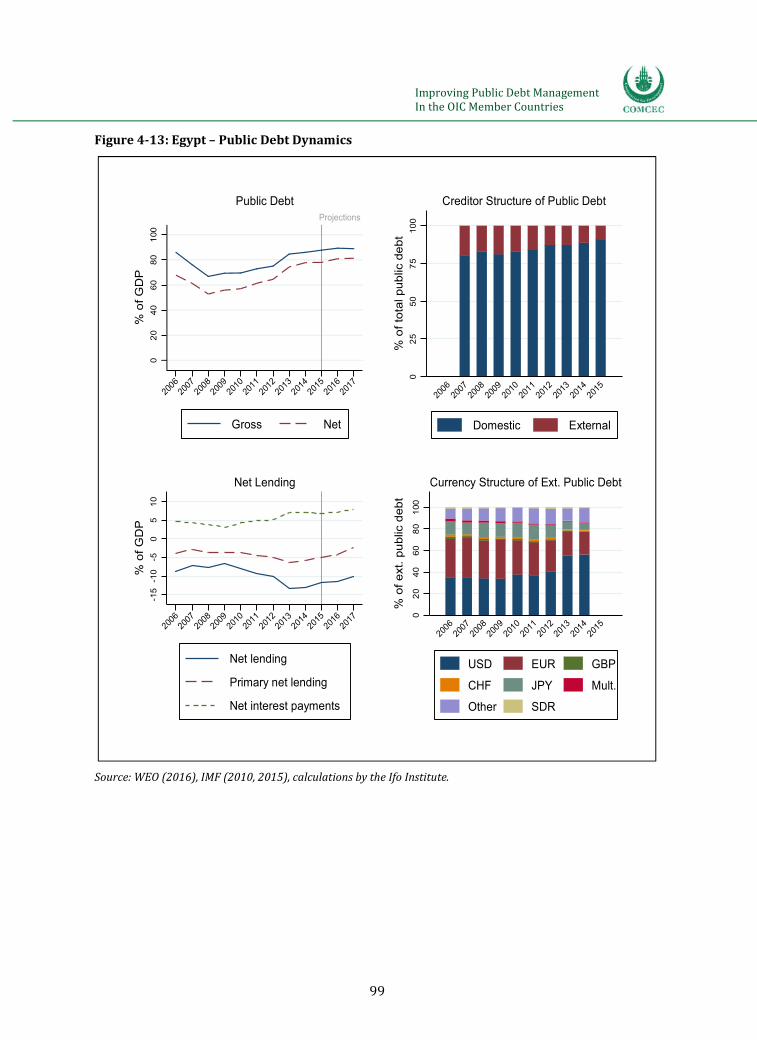

4.1.5 ArabRepublicofEgypt......................................................................................................................98

4.1.6 RepublicofIndonesia......................................................................................................................105

4.1.7 TheFederalRepublicofNigeria.................................................................................................113

4.1.8 RepublicoftheSudan......................................................................................................................120

4.1.9 RepublicofAlbania...........................................................................................................................127

4.1.10 IslamicRepublicofIran..................................................................................................................135

4.1.11 RepublicofKazakhstan...................................................................................................................141

4.1.12 LebaneseRepublic............................................................................................................................148

4.1.13 RepublicofTurkey............................................................................................................................154

4.1.14 SultanateofOman.............................................................................................................................161

4.1.15 KingdomofSaudiArabia................................................................................................................166

4.2 ComparisonofPublicDebtManagementPractices.........................................................................172

4.3 ComparisonofIslamicandConventionalFinancePractices.......................................................175

5 Policy Recommendations ..................................................................................................................... 176

5.1 MeasurestoImprovePublicDebtManagement...............................................................................176

5.2 MacroeconomicRiskManagement.........................................................................................................182

References ........................................................................................................................................................... 185

Glossary ................................................................................................................................................................ 208

Appendix A: Surveys ........................................................................................................................................ 211

Appendix B: Country Samples ...................................................................................................................... 213

iii

List of Figures

Figure11:PublicDebtManagementGovernanceStructure...............................................................................13

Figure21:GrossPublicDebtWorldwide....................................................................................................................20

Figure22:GrossPublicDebtWorldwideSince2008............................................................................................21

Figure23:DistributionofGrossPublicDebttoGDPRatiosWorldwide.......................................................22

Figure24:GovernmentNetLendingWorldwide.....................................................................................................23

Figure25:CreditorStructureofPublicDebtWorldwide....................................................................................24

Figure26:GrantElementWorldwide...........................................................................................................................25

Figure27:ShareofShortTerminTotalPublicDebtWorldwide....................................................................26

Figure28:LongTermandShortTermPublicDebtWorldwide......................................................................27

Figure29:MaturityofNewExternalPublicDebtCommitmentsWorldwide.............................................28

Figure210:InterestRateTypesWorldwide..............................................................................................................29

Figure211:InterestRatesonPublicDebtWorldwide..........................................................................................30

Figure212:CurrencyCompositionofPublicDebtWorldwide.........................................................................31

Figure213:CurrencyCompositionofPublicDebtbyIncomeGroupsWorldwide..................................32

Figure214:CurrencyCompositionofPublicDebtbyRegionalGroupsWorldwide...............................32

Figure215:UseofStrategicTargetsbyTypeofRiskWorldwide....................................................................38

Figure216:AssessmentofPublicDebtManagement............................................................................................40

Figure217:ImportanceofRiskCategoriesinPublicDebtManagement.....................................................41

Figure218:FunctioningofDomesticPublicDebtMarket...................................................................................42

Figure219:ProblemsFacedbytheDomesticPublicDebtMarket..................................................................43

Figure31:GrossPublicDebtinOICMemberCountries.......................................................................................45

Figure32:GrossPublicDebtinOICMemberCountries(2015).......................................................................46

Figure33:GovernmentNetLendinginOICMemberCountries.......................................................................47

Figure34:OilPriceDevelopmentsandNetLending.............................................................................................48

Figure35:NetDebtinOICMemberCountries.........................................................................................................49

Figure36:CreditorStructureofPublicDebtinOICMemberCountries.......................................................50

Figure37:CreditorStructureofPublicDebtbyCountry(2015).....................................................................51

Figure38:GrantElementinOICMemberCountries..............................................................................................52

Figure39:MaturityofNewExternalDebtCommitmentsinOICMemberCountries.............................53

Figure310:InterestRatesonPublicDebtinOICMemberCountries............................................................54

Figure311:CurrencyCompositionofExternalPublicDebtinOICMemberCountries.........................55

Figure312:CurrencyCompositionofExternalPublicDebtbyCountry(2014).......................................56

Figure313:DeMStrategiesinOICMemberCountries..........................................................................................57

iv

Figure314:UseofStrategicTargetsbyTypeofRisk............................................................................................58

Figure315:GlobalAssetsofIslamicFinance............................................................................................................59

Figure316:IslamicBankingShareinTotalBankingAssetsbyCountry(2015H1).................................60

Figure317:SharesofGlobalIslamicBankingAssetsbyCountry(2015).....................................................61

Figure318:GlobalSukukIssuancesandOutstanding...........................................................................................63

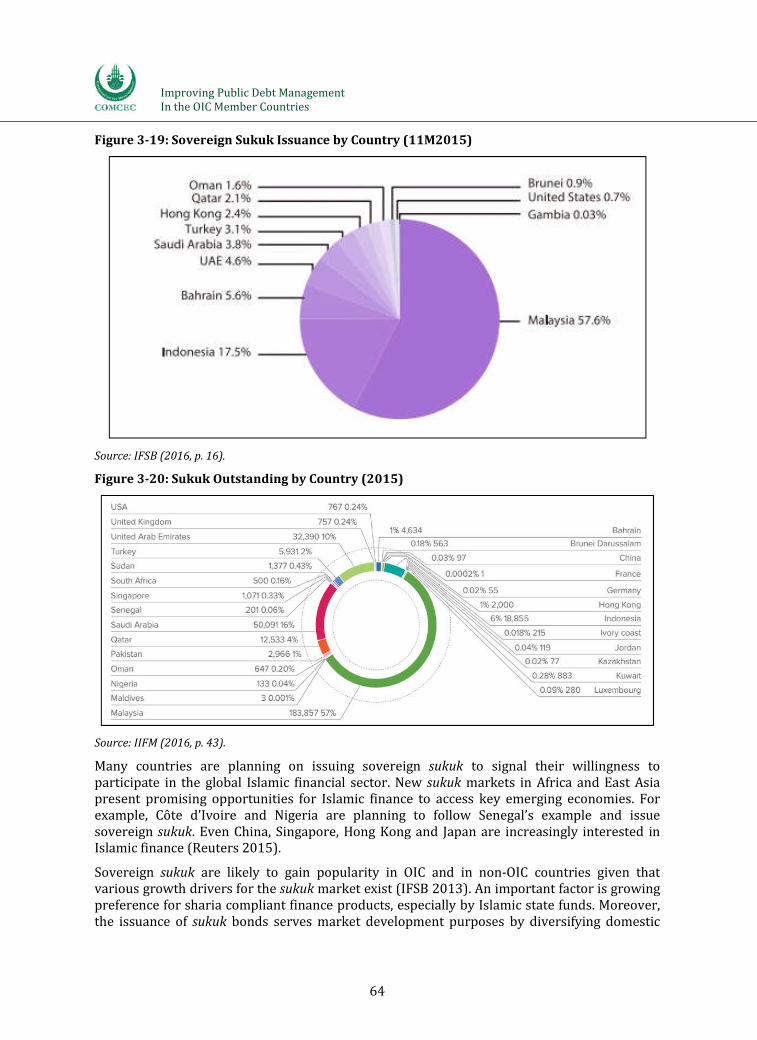

Figure319:SovereignSukukIssuancebyCountry(11M2015).......................................................................64

Figure320:SukukOutstandingbyCountry(2015)...............................................................................................64

Figure321:SelectedUSDSukukYieldsvs.U.S.GovernmentSecuritiesYield............................................66

Figure41:Gambia–PublicDebtDynamics................................................................................................................71

Figure42:GambiaYieldCurvesofTBillsandSukuk(2016).........................................................................75

Figure43:Mozambique–PublicDebtDynamics....................................................................................................78

Figure44:MozambiqueCreditorStructureofPublicDebt(2014)..............................................................81

Figure45:MozambiqueAverageMaturityofPublicDebt................................................................................82

Figure46:MozambiqueInterestRatesandInflation..........................................................................................83

Figure47:Togo–PublicDebtDynamics.....................................................................................................................85

Figure48:TogoInterestRatesandInflation..........................................................................................................88

Figure49:TogoCreditorStructureofExternalPublicDebt............................................................................89

Figure410:Uganda–PublicDebtDynamics.............................................................................................................92

Figure411:UgandaYieldsonTBondsandTBills..............................................................................................96

Figure412:UgandaYieldCurvesofTBondsandTBills(2016)..................................................................96

Figure413:Egypt–PublicDebtDynamics.................................................................................................................99

Figure414:EgyptInterestRatesonGovernmentSecurities........................................................................102

Figure415:EgyptCredittotheEconomy.............................................................................................................103

Figure416:Indonesia–PublicDebtDynamics.....................................................................................................106

Figure417:IndonesiaStructureofCentralGovernmentDebtbyInstrument.....................................110

Figure418:IndonesiaCurrencyCompositionofCentralGovernmentDebt.........................................111

Figure419:NigeriaPublicDebtDynamics...........................................................................................................114

Figure420:NigeriaPublicDebtCompositionbyInstruments(June2016)..........................................117

Figure421:NigeriaYieldCurveofFGNs................................................................................................................118

Figure422:Nigeria–CreditorStructureofExternalPublicDebt(2015).................................................119

Figure423:Sudan–PublicDebtDynamics.............................................................................................................121

Figure424:SudanRatesofReturnandInflation...............................................................................................124

Figure425:Sudan–CreditorStructureofExternalPublicDebt(2013)...................................................125

Figure426:Albania–PublicDebtDynamics..........................................................................................................128

v

Figure427:Albania–PublicDebtCompositionbyInstrumentMaturity.................................................132

Figure428:Albania–CreditorStructureofDomesticPublicDebt..............................................................133

Figure429:Iran–PublicDebtDynamics.................................................................................................................136

Figure430:Kazakhstan–PublicDebtDynamics.................................................................................................142

Figure431:KazakhstanYieldsonGovernmentSecurities............................................................................145

Figure432:Kazakhstan–CreditorStructureofExternalPublicDebt(2016)........................................146

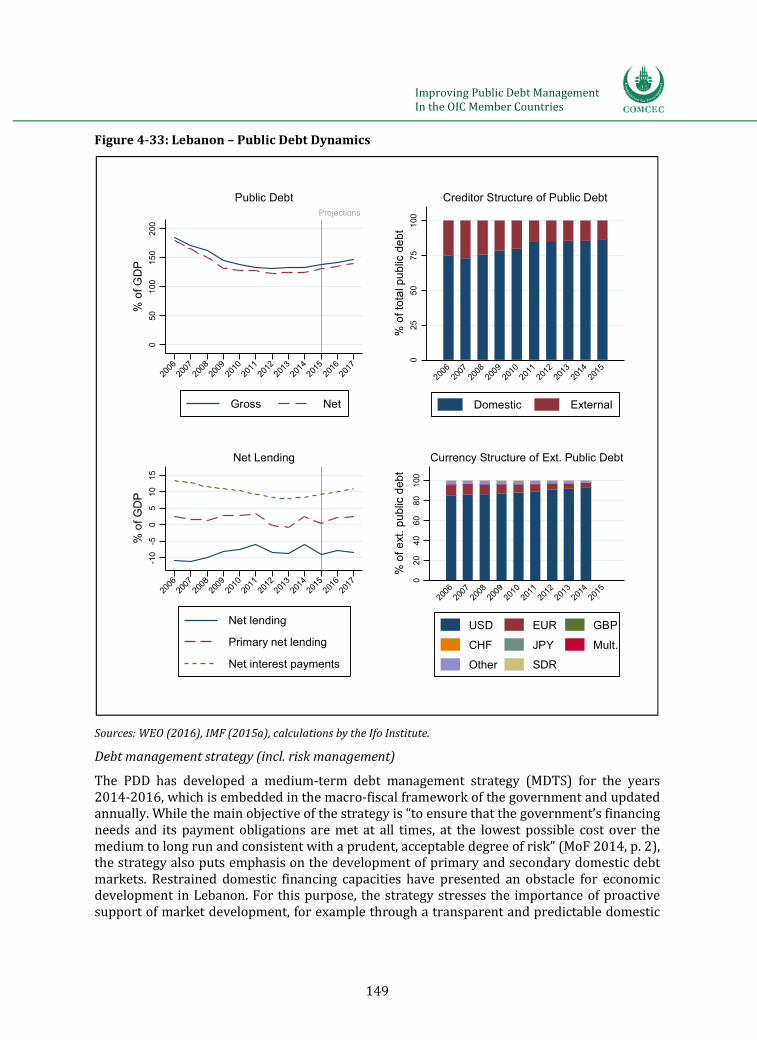

Figure433:Lebanon–PublicDebtDynamics.......................................................................................................149

Figure434:LebanonYieldsonTBills....................................................................................................................151

Figure435:Turkey–GeneralGovernmentDebtDynamics............................................................................155

Figure436:TurkeyOrganizationofPublicDebtManagement...................................................................156

Figure437:TurkeyDomesticBorrowingbyInstruments(2015).............................................................158

Figure438:Turkey10yearBondsYields.............................................................................................................159

Figure439:OmanPublicDebtDynamics..............................................................................................................162

Figure440:OmanOutstandingPublicDebtbyInstruments........................................................................164

Figure441:SaudiArabia–PublicDebtDynamics...............................................................................................166

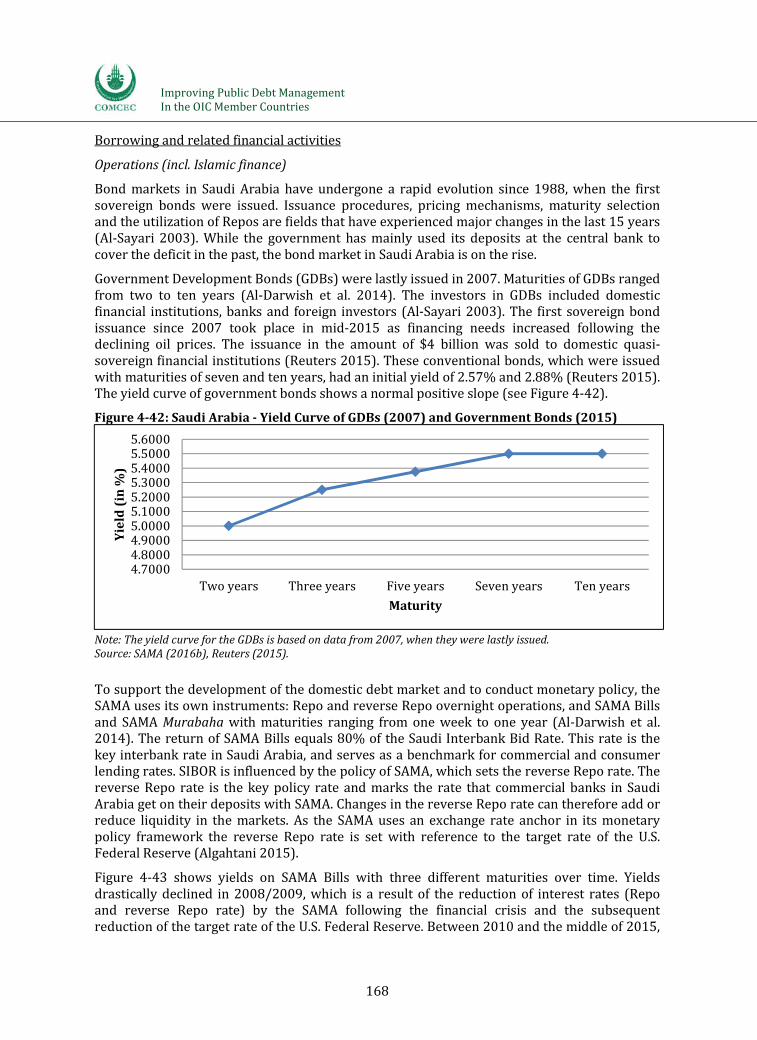

Figure442:SaudiArabiaYieldCurveofGDBs(2007)andGovernmentBonds(2015)..................168

Figure443:SaudiArabiaYieldsonSAMABills...................................................................................................169

Figure444:SaudArabiaYieldCurvesofSAMABills........................................................................................169

FigureA01:CESifoWorldEconomicSurveyOctober2016...........................................................................211

FigureA02:IfoPublicDebtManagementSurvey2016...................................................................................212

vi

List of Tables

Table11:WorldBankDeMPAPerformanceIndicators.......................................................................................10

Table12:RisksRelevantforPublicDebtManagement........................................................................................14

Table13:InterdependenciesofPublicDebtManagement,FiscalPolicyandMonetaryPolicy..........16

Table41:Gambia–CostandRiskIndicatorsfortheGovernment'sDebtPortfolio(2014).................73

Table42:MozambiqueCostandRiskIndicatorsfortheGovt.'sDebtPortfolio(2014)......................80

Table43:TogoCostandRiskIndicatorsfortheGovernment’sDebtPortfolio(2015).......................87

Table44:UgandaCostandRiskIndicatorsoftheGovernment’sDebtPortfolio...................................94

Table45:Egypt–CostandRiskIndicatorsfortheGovernment'sDebtPortfolio(Mid2015)........101

Table46:IndonesiaTargetindicatorsfordebtportfoliorisk......................................................................108

Table47:IndonesiaCostandRiskIndicatorsoftheGovernment’sDebtPortfolio............................109

Table48:IndonesiaOutstandingCentralGovernmentDebt20112016(intrillionIDR)..............110

Table49:NigeriaRiskIndicatorsfortheGovernment'sDebtPortfolio(2015)..................................116

Table410:Albania–CostandRiskIndicatorsfortheGovernment’sDebtPortfolio(2015)...........131

Table411:Lebanon–CostandRiskindicatorsfortheGovernment'sDebtPortfolio(2013).........150

Table412:ComparisonofDebtLevelsandStructuresinCaseStudyCountries(2015)....................173

Table413:ComparisonofDebtManagementObjectivesinCaseStudyCountries...............................174

Table51:ChallengesandObstaclestoPublicDebtManagement.................................................................177

Table52:SummaryofPolicyRecommendations.................................................................................................183

TableG01:GeneralPublicDebtTerms....................................................................................................................208

TableG02:GeneralIslamicFinanceTerms............................................................................................................209

TableG03:TypesofSukuk............................................................................................................................................210

vii

List of Acronyms

$ U.S.Dollar

AAOIFI AccountingandAuditingOrganizationforIslamicFinancialInstitutions

ADF AfricanDevelopmentFund

AfDB AfricanDevelopmentBank

ATM AverageTimetoMaturity

ATR AverageTimetoRefixing

BADEA ArabBankforEconomicDevelopmentinAfrica

BCEAO BanqueCentraledesEtatsdel'Afriquedel'Ouest

BIS BankforInternationalSettlements

BOAD BanqueOuestAfricainedeDeveloppement

BoU BankofUganda

BRVM BourseRégionaledesValeursMobilières

CBI CentralBankofIran

CBE CentralBankofEgypt

CBG CentralBankofGambia

CBoS CentralBankofSudan

CCA CaucasianandCentralAsian

CESEE Central,EasternandSoutheasternEurope

CFAFranc FrancdelaCommunautéFinancièred’Afrique

CHF SwissFranc

CMA CapitalMarketAuthority

CNDP ComitéNationaldelaDettePublique

COMCEC StandingCommitteeforEconomicandCommercialCooperationoftheOIC

DDP DirectiondelaDettePublique

DeM DebtManagement

DeMPA DebtManagementPerformanceAssessment

DLDM DirectorateofLoansandDebtManagement

DMO DebtManagementOffice

DMU DebtManagementUnit

DVP DeliveryVersusPayment

EFF ExtendedFundFacility

EIB EuropeanInvestmentBank

viii

EPG EgyptianPound

EUR Euro

FRN FloatingRateNotes

FX ForeignExchange

GBP UnitedKingdomPound

GDB GovernmentDevelopmentBond

GDP GrossDomesticProduct

GCC GulfCooperationCouncil

GMD GambianDalasi

GNI GrossNationalIncome

HIPC HeavilyIndebtedPoorCountries

IBRD InternationalBankforReconstructionandDevelopment

IDA InternationalDevelopmentAssociation

IDB IslamicDevelopmentBank

IIFM InternationalIslamicFinancialMarket

IFAD InternationalFundforAgriculturalDevelopment

IFSB IslamicFinancialServicesBoard

IMF InternationalMonetaryFund

ITB IslamicTreasuryBill

JPY JapaneseYen

MDRI MultilateralDebtReliefInitiative

MDTS MediumTermDebtManagementStrategy

MEAF MinistryofEconomicAffairsandFinance

MEFMI Macroeconomic and Financial Management Institute of Eastern and SouthernAfrica

MENA MiddleEastandNorthAfrica

MIFC MalaysiaInternationalIslamicFinanceCentre

MoEF Ministèredel’ÉconomieetdesFinances

MoF MinistryofFinance

MoFEA MinistryofFinanceandEconomicAffairs

MoFNE MinistryofFinanceandNationalEconomy

MoFPED MinistryofFinance,PlanningandEconomicDevelopment

NDB NetDomesticBorrowing

ix

NDT NationalDirectorateofTreasury

NPV NetPresentValue

OECD OrganisationforEconomicCooperationandDevelopment

OFID OPECFundforInternationalDevelopment

OIC OrganizationofIslamicCooperation

OPEC OrganizationofthePetroleumExportingCountries

OTC Overthecounter

OTR OfficeofTogoleseRevenue

PDMS PublicDebtManagementStrategy

PDU PublicDebtUnit

PPP PublicPrivatePartnership

RO OmaniRial

SAI SupremeAuditInstitution

SAMA SaudiArabianMonetaryAgency

SAS Sukukalsalam

SDR SpecialDrawingRight

SDMO SeparateDebtManagementOffice

SOE StateOwnedEnterprise

ST ShortTerm

TBill TreasuryBill

TBond TreasuryBond

TL TurkishLira

UAE UnitedArabEmirates

UK UnitedKingdom

UN UnitedNations

US UnitedStates

USD U.S.Dollar

VAT ValueAddedTax

WAEMU WestAfricanEconomicandMonetaryUnion

WAIR WeightedAverageInterestRate

WEO WorldEconomicOutlook

WES CESifoWorldEconomicSurvey

ImprovingPublicDebtManagementIntheOICMemberCountries

1

Executive Summary

1 Definition and Performance Indicators of Public Debt Management

Public debt managementisintendedtodesignthegovernment’sdebtportfolioinatargetedand efficient way. Public debt management strategies aim at raising the required amount offunding at the lowest possible costs, consistent with a prudent degree of risk. Additionalobjectivesincludedevelopingandmaintaininganefficientmarketforgovernmentsecurities.

Performance indicators for public debt management are grouped into the categories (1)governance and strategy development (e.g. the legal or managerial framework); (2)coordinationwithmacroeconomicpolicies(e.g.coordinationwithfiscalormonetarypolicies);(3)borrowingandrelated financialactivities (e.g.domesticorexternal borrowing); (4)cashflowforecastingandcashbalancemanagement(e.g.effectivenessofcashflowforecasts);and(5)debtrecordingandoperationalriskmanagement(e.g.debtadministrationandsecurity).

Apublic debt management strategyhelps(1)makingprudentborrowingdecisionsbasedonan analysis of cost and risks; (2) facilitating intragovernmental and creditoraddressedcommunication and coordination to reduce uncertainty; (3) giving debt managers a clearmandate, thereby ensuring good governance and accountability; and (4) fostering thedevelopmentofadomesticdebtmarketbymakingthegovernment’sdebtgoalstransparenttomarketparticipants.

Risks for the government’s debt portfolio arise from the structure of outstanding debt,includingbutnotlimitedtorefinancing risk,interest rate riskandexchange rate risk.

2 Global Practices in Public Debt Management

Inaglobalsampleovertheperiod19802015,theaverage public debt levelassumedvaluesbetween40%and80%ofGDPwithatendencytoincrease.Inmostyears,averagepublicdebtrelativetoGDPinthegroupofhighincomecountriesislargerthaninmiddleincomeandlowincomecountries.

Theaverage public budget deficitwas7.2%ofGDPduringtheperiod19801995.Since1995budgetdeficitshavedecreasedto2.0%onaverage(1.4%ofGDPfortheperiod19962006).Theglobalfinancialcrisis,however,marksastructuralbreakandpushedbalancesdeeperintodeficit, where they will remain in coming years according to projections. Compared to the1980sand1990s,publicbudgetbalancesoflowincomecountrieshaveimprovedremarkably.

Theshorterthematurity of debt,thehighertheamountofdebttoberolledoverinagivenyearandthehighertherefinancing risk.Theaverageshareofshorttermintotalpublicdebtinaglobalsampledecreasedfrom24%in1995to11%in2015.Whileprivatecreditorsextendtheircreditforanaverageperiodofapproximatelyfiveyears,officialcreditorssigncontractswithmaturitiesexceeding20yearsonaverage.

Debtdenotedinforeign currency issubjecttoexchange rate riskbecauseadevaluationofthedomesticcurrencyincreasesthevalueofforeigncurrencydenominateddebtexpressedindomestic currency. Public debt denominated in foreign currency has increased slightly overthe past 20 years. Itmakes up about 36%of total public debt across all income groups; theshareishighestinlowincomecountriesandlowestinhighincomecountries.

Foreigndenominated public debt is mostly contracted in U.S. Dollars, whoseshare has beenrisingovertimeandequaled59%in2014.OtherdominantcurrenciesaretheEuro(13%)andSpecialDrawingRights(SDRs)withtheIMF(6%).Whilehighincomecountriesmostlyrelyon

ImprovingPublicDebtManagementIntheOICMemberCountries

2

domestic creditors (76.2% in 2015), middleincome countries divide their financing needsalmostequallybetweenbothtypesofinvestorsandlowincomecountries’debtismostlyheldbyexternalcreditors.

Interest rate riskarises forcontractswithshortmaturitiesorvariable interestrates.Whilehighestinhighincomecountries,theshareofvariableratecontractsisgenerallysmall.

Governmentsmayreceivecredits on concessional terms,inparticularfromofficialcreditorsasaformofdevelopmentaidorinsupportoflocalreforms.Thisgrantelementinpublicdebthasbeenrisingovertimeandamountedto50%in2014.Theaverageinterestrateofpublicdebtisoftenlowerthanthelendingratetotheprivatesector,whichmightbeexplainedbytheimportanceofconcessionallendingtogovernments.

Debt Management Offices (DMOs) are typically responsible for funding operations, foranalyzing and monitoring risks, for the settlement of transactions and for keeping financialrecordsuptodate.Theexistenceofaprincipaldebtmanagemententitywithclearobjectives,amediumtermstrategyandtherequirementtoreporttoparliamentorgovernmentisgenerallyconsideredasbestpracticeinpublicdebtmanagement.

TheDMOaspartoftheoverallinstitutional structuremaybeadepartmentoftheMinistryofFinance, an office within the central bank or an independent agency. A clear separation ofassignedresponsibilities formonetarypolicyandfordebtmanagement isapreconditionforaccountable institutions; this suggests separating the DMO from the central bank. If therecruitment of trained portfolio managers from the private sector has priority, independentagencies outside of other official institutions, socalled separate debt management offices(SDMOs),mightbeestablished.

If public debt management is located within the central bank, it faces conflicts of interest between monetary policy and public debt management. A clear allocation of theresponsibilities for monetary policy and debt management, which is a precondition foraccountableinstitutions,thereforesuggestsdividingthesepoliciesbetweentwoinstitutions.

An efficient governance structure requires that DMOs follow a clear mandate with welldefinedobjectives.Potentialtargetsaretheallocationofpublicdebtindomesticandexternalcurrencydebt,thedivisionbetweenfixedandfloatinginterestratedebtandthepercentageoftotaldebtthathastoberefinancedwithintwelvemonths.Thishelpstoimproveaccountabilityandtolimitprincipalagentproblems.Activetradingbasedonbenchmarksisratherabsentinglobalbestpractices.

Therearecompetingviewsontheaims of public debt management:asaformofportfoliomanagement, costs are minimized for given risks (narrow view). Alternatively, when takingrevenues into account, public budget management has to prevent mismatches betweenrevenuesanddebtpayments(broadview).Thisstrategyfocusesonbudgetaryrisksandaimsat reducing financial risks by guaranteeing that government can meet its obligations at anypointintime.Assuch,itcoordinatespublicdebtmanagementwith otherpublic policies.

AWorldBanksurveyconducted in2013showsthat60%of therespondingcountrieshadaformal debt management strategy in place. 77% of those with formal strategy published it,76%aimedatstrategictargets,71%usedquantitativeanalysisandonlyaminoritygroundedthestrategyonalegalframework.

ImprovingPublicDebtManagementIntheOICMemberCountries

3

ResultsfromtheCESifoWorld Economic Survey(WES)suggestthattheefficiency of public debt management is highest in highincome countries and lowest in lowincome countries.While foreign currency risk is least important in highincome countries, it is the mostimportantriskcategoryforpublicdebtmanagementintheotherincomegroupsandintheOICcountries.

PublicdebtmarketsinhighincomecountriesreceivedthebestassessmentfromWESexperts,inlowincomecountriestheworst.PublicdebtmarketsinthegroupofOICcountriesperformonaveragerelativelyunsatisfactoryininternationalcomparison.Accordingtotheexperts,themostimportantproblems faced bydomesticpublicdebtmarketsinOICcountriesareapoor market infrastructure,thelimited size of the economiesandamissing investor base.

Global best practiceinOECDcountriesrevealsfourimportantissuesforthesuccessofpublicdebt management. First, public debt management needs to be based on a sound longtermstrategy.Second,itisimportantthatthisstrategyisimplementedbyaninstitutioncapabletodealwithpublicportfoliomanagement.Third,moderninstrumentsandtechniqueshavetobeused in public debt management. Finally, suitable mechanisms to ensure accountability andsuccessfuldelegationhavetobedesigned.Appliedtoemerginganddevelopingcountries,theircharacteristics (e.g. limited access to financial resources, less developed institutions, largervulnerability)havetobetakenintoaccount.

3 Public Debt Management Practices in the OIC Member Countries

Average public debt relative to GDPintheOICmembercountrieshasincreasedfrom36.7%in2012to46.1%in2015andisexpectedtoriseto51.1%in2017.Theamountofoutstandinggross public debt relative to GDP is, however, very heterogeneous among OIC membercountries,rangingbetween3%and139%.

ThehighestaveragedebttoGDPratiosareexpectedinlowincomeOICcountriesinthenextyears. Highincome OIC countries are expected to experience the largest increases in theaveragedebttoGDPratios.Differentdebtdynamicsalsoariseamongregionalgroups.SeveralAfrican countries have been granted debt relief or restructuring in the last decade.Consequently,debtratioshavesubstantiallydecreasedbetween2006and2009intheAfricangroupbuthaveslightlyrisenafterwards.TheaveragedebttoGDPratiointheAsiangrouphasbeenonarelativestablepath.TheaveragedebttoGDPratiointheArabgrouphasincreasedsince2014asthedeclineinoilpriceshadnegativeeffectsontheeconomiesofoilproducingcountries.WhilethefiscalbuffersofsomeOICmembercountriesareexpectedtobecapableofabsorbingthepredictedbudgetdeficitsfollowingloweroilrevenuesforsomeyears,otherOICmembercountrieshavetoissuesubstantialamountsofdebt.

The averagegrant element inOIC countrieshas beenabout50%since2006, similar to theworldwide average. Grants are primarily extended by official creditors, i.e. internationalorganizations and governments, while private credit contracts rarely have a grant element.Grantstolowincomecountriesaremoregenerousthantomiddleincomecountries.ThegrantelementisparticularlyhighintheAfricangroup.

Theshareofshort-term debtintotalpublicdebtintheOICmembercountrieshasdecreasedfrom68.1%in2006to54.5%in2015(slightlyabovetheworldwideaverageof52%).Officialcreditorssigncontractswithmaturitiessimilartotheworldwideaverageataround21yearson average. Private creditors extend their credit for an average period of approximately 4years (below the worldwide average of 5 years). The maturity of new debt contracts issignificantlylargerinlowincomecountriesthaninmiddleincomecountries,whichmightbe

ImprovingPublicDebtManagementIntheOICMemberCountries

4

explainedbythe largershareofofficialcreditors inlowincomecountries.Consequently, theaveragematurityofnewcontractsislargestintheAfricangroup.

The average share of domestic debt in total public debt in OIC member states has slightlyincreased since 2006 and stands at around 41.5% in 2015 (a share above the worldwideaverage).Lowincomecountrieshavealowershareofdomesticdebt(31%)thanmiddleandhighincomecountries(41.9%).Inhighincomecountries,theshareofdomesticcreditorshasincreased since 2008 and stands at about 77.7% in 2015. However, OIC member countriesdifferconsiderablyintheirsharesofexternaldebt.

The largest share of external public debt inOIC countries was denominated inU.S. Dollars(51.3%),followedbyEuro(15.4%),SpecialDrawingRights(6.6%)andJapaneseYen(3.2%)in2014.TheshareofexternalpublicdebtdenominatedinU.S.DollarandSpecialDrawingRights(SDR) has increased between 2006 and 2014 while the share of external public debtdenominated in Euro has been relatively constant. The share of external public debtdenominatedinJapaneseYenhasdecreased.

Theaverageinterest rate on public debthasbeenrelativelystableandlowinOICmembercountriesoverthelastdecade(theaverageinterestratewasabout1.9%in2014).ManyOICmembercountriesborrowfromofficialcreditorsatpreferentialrates(onaverageabout1.2%in2014). The average interest rate forprivatecredits was about3.9% in2014,a ratebeinghigher than the worldwide average. Lowincome countries face lower interest rates thanmiddleincome ones presumably because they have access to concessional lending. Averageinterestrates intheArabandAsiangrouphavedecreasedoverthe lastyears,whileaverageinterestratesintheAfricangrouphaveincreasedsince2006.

IslamicfinancehasbecomeanimportantpartofthefinancialsystemsinseveralOICmembercountries.GovernmentsinOICcountriesuseIslamic sovereign bonds (sukuk)inpublicdebtmanagement. Sukuk are financial certificates commonly referred to as "sharia compliant"bonds, which do not pay interest. The investor rather acquires a share of the underlyingproject that the sukuk bond is linked to. Several OIC member countries plan to increase theshareofIslamicfinanceinstrumentsinthenextfewyears.

InmostOICmembercountriesaPublic Debt Management Office (DMO)at theMinistryofFinance is responsible for public debt management. In some countries, a department at thecentral bank also carries out debt management operations. Only few OIC member countrieshaveestablishedindependentdebtmanagementoffices.Inseveralcountries,thereisnotonesingleentityresponsibleforpublicdebtmanagementbutseveraldepartmentsattheMinistryofFinanceandthecentralbankandinsomecasesalsoinotherinstitutions.

Among the OIC member countries, 62% countries have established a formal debt management strategy (similar to the worldwide average of60%).Among the OIC membercountrieswithaformalpublicdebtmanagementstrategy,78%havepublishedthisdocument.AmongtheOIC membercountries with a formalpublicdebt managementstrategy,68%usestrategictargetsandbenchmarks(asharebeinglowerthantheworldwideaverageof77%).

AmongtheOICmembercountrieswithaformalpublicdebtmanagementstrategy,63%haveset strategic targets for currency risk, 58% have set targets for refinancing risk, and 53%haveset targets for interestraterisk.Incontrast,onaglobalview, it ismostcommontosetstrategictargetsforrefinancingrisk(66%),followedbyinterestraterisk(56%)andcurrencyrisk(50%).Targetsusedforcurrencyriskincludetheshareofforeigncurrencydebtintotaldebt;targetsusedforinterestrateriskincludetheshareoffixedinterestdebtintotaldebtand

ImprovingPublicDebtManagementIntheOICMemberCountries

5

theaveragetimetorefixing;andtargetsusedforrefinancingriskincludeaceilingonmaturingdebtwithinoneyear(in%oftotaloutstandingdebt)andtheaveragetimetomaturity.

4 Public Debt Management Practices in Individual OIC Member Countries

The low and lowermiddle income African countries Gambia,Mozambique, Togo, Uganda,aswell asSudanhave sharesofexternal publicdebt in total publicdebtofaboutorover50%.These figures indicate an underdeveloped domestic debt market. The high share of debtdenominatedinforeigncurrenciesexposesthesecountriestoexchangeraterisk.NigeriaisanexceptionamongtheAfricancountrieswithexternalpublicdebtamountingtoonlyabout18%oftotalpublicdebt.

The external public debt of low and lowermiddle income countries with high shares ofexternalpublicdebtislargelyheldbyofficialcreditorssuchasinternationalorganizationsandgovernments. Low and lowermiddle income countries often face difficulties in financingthemselves on international capital markets. Official creditors lend at preferential interestratesandat longermaturities thanprivatecreditors.Consequently, thecasestudycountrieswith a high share of external public debt have lower interest rates and longer averagematuritiesintheirgovernmentdebtportfolio.

Other case study countries such as Egypt and Lebanon strongly rely on the domestic debt market.Highinterestratesongovernmentdebtandpreferencesforsafe lendingreducetheincentives of banks to provide credit to the private sector in these countries, leading to acrowding-out of bank loans to the private sector. Banks tend to invest in shortterminstruments toavoidassetand liabilitymismatcheswithshorttermbankdeposits. Lebanonhas recently made progress in reducing the reliance on the domestic debt market especiallythroughaswapofdomesticcurrencydebttoEurobonds.

Giventhedifferentdebtlevelsandstructures,debt management strategiesvaryamongthecasestudycountries.Outof the15 case studycountries, elevenhave developed formal debtmanagement strategies. Uganda, Egypt, Indonesia, Nigeria, Albania and Lebanon havepublished numerical targets for risks in the public debt portfolio. Turkey has set numericaltargetsbutdoesnotdisclosethesenumbers.Gambia,MozambiqueandTogohavesetgeneralobjectivesbutdonotformulatespecifictargets.SaudiArabia,Sudan,KazakhstanandOmandonothaveordonotdisclosetargets.

Iran and Sudan all local banks operate under Islamic finance rules, while in SaudiArabiaonethird of all local banks can beconsidered as fully Islamic.Consequently, Islamic financeinstrumentsalsoplayanimportantroleforpublicdebtmanagementinthesecountries.DebttoGDPratios in IranandSaudiArabiaarevery low,amountingto17.1%and5.8%in2015.PublicdebtinSaudiArabiaiscompletelydomestic,whiletheshareofdomesticpublicdebtinIran accounts for more than 90%. Declining oil revenues give rise to additional borrowingneeds and these countries plan to also tap international debt markets. To prepareinternational bond issuances, legal and organizational structures for debt management arebeing established at the moment. In contrast, Sudan has a relatively high public debt ratio(68.9%)andabout90%ofpublicdebtisexternal.

The central bank of Saudi Arabia (SAMA) issues SAMA Bills and the government has issuedGovernment Development Bonds (GDBs). Although GDBs are not defined as Islamic bonds,they are “zakah (compulsory alms) deductible” for domestic investors. The general rise inpopularity of corporate and quasisovereign sukuk and other Islamic finance instruments inSaudi Arabia indicate that Islamic bonds will play also a bigger role in the future of thecountry’spublicdebtmanagement.

ImprovingPublicDebtManagementIntheOICMemberCountries

6

The government of Iran has mainly borrowed from domestic Islamic banks by taking loanswith fixed rates of return in the past. In 2015, Iran has started to expand its Islamic bondmarket. There are various types of instruments such as murabaha, musharakah, ijarah, anddifferent types of sukuk. Sovereign sukuk, ijarah, and Sovereign Settlement Bills were issuedforthefirsttimein2016.IslamicTreasuryBills(ITBs)werealso introduceddescribingzerocouponbondssoldatadiscounttotheirfacevalues.

The government and the central bank of Sudan use various short and longterm Islamicfinance instruments for debt and liquidity management. The central bank uses Central BankijarahCertificates(shihab)foropenmarketoperationswhosereturnsarefixedanddistributedmonthly. The central bank also uses sukuk bonds for the management of liquidity. Thegovernment employs two types of sukuk: shortterm Government Musharaka Certificates(GMCs),whicharemainlyusedforliquidityandcashmanagement,andlongtermGovernmentInvestment Certificates (GIC). The nominal value of the instrument is distributed in profitsquarterlyorbiannually.ComparedtothemarketforGMCs,whichhasbeengrowingsteadilysince 1999 because of the specific characteristics of these instruments such as highprofitability, low risk, shortterm maturity and high liquidity, the market for GICs has beenstagnatingsinceitsintroductionin2003.

Some case study countries with conventional finance systems have also introduced Islamicfinance instruments in public debt management. Countries such as Gambia, Togo and Omanhave already issued sukuk. Indonesia has established a rapidly growing market for publicsukukandhasalsoissuedGlobal Sukuk denominatedinforeigncurrency.OthercountriessuchasEgypt,Kazakhstan,Mozambique,NigeriaandUgandahavecreatedlegalprerequisitestouseIslamicfinanceinstrumentsand/orareplanningtoissuesukukinthenextyears.

5 Policy Recommendations

Most OIC countries have established legal and organizational public debt managementframeworksandhavecreatedDebt Management Officesorareintheprocessofdoingso.Insome countries, the delineation of responsibilities for public debt management remains,however,vague.Publicdebtmanagementfunctionsoftenarenotfullycentralizedatthedebtmanagement office but additional ministerial departments, the central bank and committeespursue debt management functions. A large number of institutions involved in public debtmanagement hampers coordination and makes it difficult to evaluate the degree ofaccountability of the individual institutions. As long as all debt management responsibilitiesare not centralized at a debt management unit, adequate and systematic communicationbetween the various embedded institutions is important. All OIC member countries areadvised to setup DebtManagementOffices if theyhavenot doneso,and to give theseDMOclearlydefinedauthoritytomanagepublicdebt.

About 38% of the OIC member countries have not yet developed a medium-term debt management strategy (MTDS) following international standards. Among the OIC membercountries with formal public debt management strategies, 32% have not yet set numericalstrategic targets. All OIC countries are recommended to create MTDS including numericalstrategic targets.Aclearcommitment to thepublicdebtmanagementstrategy is likely tobehelpful in attracting foreign investors and improving domestic debt markets. Countries thathave not yet published their debt management strategies are advised to do so to facilitatecommunicationwithinternationalinvestors.Itisimportanttostrengthenpublicdisclosureoflegal and organizational structures of public debt management, operations and strategies intheOICmembercountries.

ImprovingPublicDebtManagementIntheOICMemberCountries

7

OIC member countries that already have established professional public debt managementpracticesmightadviseothercountriesinestablishinginstitutionalframeworksforpublicdebtmanagement.Existinginstitutionalsettingsandpublicdebtmanagementdocumentsmightbetaken as models by countries that take the first steps in implementing formal public debtmanagement. Often countries have gained various experiences regarding public debtmanagement such as longterm strategy development, risk management, monitoring orinstitutional coordination. Countries may be able to offer good examples within one area ofdebtmanagementand/ornegativeexperiencefromwhichlessonscanbelearned.OICmembercountries are also advised to cooperate. Tasks such as the training of specialized staff, thedevelopmentofcapacitiesof themiddleofficeandthecreationofriskquantificationmodelsmightbecentralized.Giventheircommonalities,thisopenstheroomforcooperationamongthe OIC member countries. Therefore, it might be useful to bring OIC member countriestogetherfordevelopingsolutionsofpublicdebtmanagementproblems.Itisrecommendedtocoordinate cooperation within COMCEC for instance by setting up workshops or jointtrainingcoursesonpublicdebtmanagement.

Central bank independence might be strengthened in the OIC member countries. In somecountries,thecentralbankhaspurchasedsubstantialamountsofsovereignbonds.Thisposestheriskthatmonetaryandfinancialpoliciesarenotclearlyseparatedandthatthecentralbankcannotimplementanindependentmonetarypolicy.Publicdebtmanagementiswelladvisedtofurtherdiversifytheinvestorbase.

Islamic sovereign bonds (sukuk)arelikelytogainpopularityinOICandnonOICcountries.An important factor is growing preference for sharia compliant finance products. Moreover,the issuance of sukuk bonds might serve market development purposes by diversifyingdomestic capital markets and attracting new investors from Islamic countries. Investors canbenefit from new sovereign sukuk issuances because of the opportunity to diversify theirportfolios. Several OIC member countries are planning on issuing sovereign sukuk or havealready done so. Infrastructure projects are especially suitable as underlying structure forsovereign sukuk given the assetbacked nature of these bonds. In several Islamic marketsfunding gaps and infrastructure requirements exist. As investments in infrastructure areexpected to increase in developing and emerging countries with Islamic banking playing animportantroleinmanyofthesemarkets,sukuk issuancerelatedtoinfrastructureisexpectedtoincrease.

However, Islamic finance instruments do not always minimize financing costs as they mayentail additional administrative expenses and greater legal and accounting challenges. Theprohibitionofinterestandthelimitedprimaryandsecondarymarketforsukukmaygiveriseto concerns regarding an efficient price system and tradability. The limited tradability, thecomparativelyhigh issuance costs, and the rather limited volume ofsukuk constrain marketliquidityandhenceagovernment’sflexibilityinfiscalpolicyandacentralbank’sflexibilityinmonetarypolicy.

As a result of underdeveloped domestic debt markets, several low and lowermiddleincomeOICmembercountriesstronglydependonexternalborrowing.Domesticdebtmarketsare potentially an important source of financial funding for governments. A wellfunctioningdomestic market for public debt helps to reduce the risks linked to public debt because itprovides additional diversification opportunities and reduces the exchange rate risk. Fordomesticcreditorsitiseasierandlessexpensivetobuysovereignbondsiftheyaretradedonthedomesticratherthanontheinternationalmarket.Domesticcreditors,inturn,areasourceoffundsthatreactslesstoglobalmarketconditionsandasaresultislessvolatileandinstable

ImprovingPublicDebtManagementIntheOICMemberCountries

8

thanexternalsources.Thedomesticdebtmarketcanbestrengthenedbyavarietyofmeasuressuch as improving legal and regulatory frameworks, market infrastructure, political stabilityanddevelopingareliablepublicdebtmanagement.Weakpublicdebtmanagementcapacitiesdecreasethegovernment’scredibilityresultinginhigherriskpremiumsespeciallywithregardto longtermbonds.Disseminating informationondebtoperations,adoptingtransparency inprimary auctions and developing secondary markets strengthen the functioning of domesticdebtmarkets.

Some OIC member countries are heavily indebted to the domestic banking sector. Highinterest rates on government debt and preferences for safe lending reduce the incentivesofbankstoprovidecredittotheprivatesectorinthesecountries,leadingtoacrowding-out of bank loans to the private sector.Bankstendtoinvestinshorterterminstrumentstoavoidassetand liabilitymismatcheswithshorttermbankdeposits givingrise to interest rateriskandrefinancingriskforthegovernment’sdebtportfolio.Whenasubstantialpartofpublicdebtis held by domestic banks, a potentially dangerous link between public finances and thebankingsectorexists:publicdefaultwoulddamagethebankingsectoranddifficulties inthebankingsectorendangergovernment’sabilityinplacingitsbondsonthedomesticmarket.Adiversified domestic creditor base with a large share of nonbanking investors is favorable.The investors’ base can be broadened by reforming the legal framework to grant pensionfunds,insurancecompaniesandforeigninvestors’accesstothedomesticdebtmarket.

OIC member countries may well use sukuk in public debt management in addition toconventional bonds to diversify the government’s debt portfolio and attract new investors,domesticallyand from other (Islamic) countries. In particular, countries that rely heavilyonthe domestic banking sector may benefit from these instruments, including retail sukuk.Countries that mainly rely on concessional lending may also use Islamic finance products toattractprivateinvestors.

Governments often issue shortterm bonds rather than longterm bonds. Interest rates ofshortterm bonds are usually lower than longterm ones when the markets have concernsabout political and macroeconomic risks. This also prevents the establishment anddevelopment of a domestic debt market which is supposed to satisfy the investors’ andgovernments’financingneedsinthelongrun.Countrieswithshortaveragematurityofpublicdebt are exposed to refinancing risk and may lengthen maturities of public debt bypreferring longerterm TBonds over shortterm TBills. In countries with low shares offoreign currency debt, this objective might be achieved, for example, by using swaps ofdomestic currency debt to foreign currency debt which generally longer maturity. Publicbudget management might also benefit from the current low interest rate environment tolengthen the average maturity of debt to reduce refinancing risk and reduce the number ofbondsissuedannually.Animportantindicatorforthequalityofthedomesticdebtmarketisinhowmuchthebondmaturitystructuremirrorsthegovernmentexpenditurestructure.

Macroeconomic risk managementisanimportantcomplementtopublicdebtmanagement.The main tools in macroeconomic risk management are information and analytical systemsbasedonadequatefrequencydataprovidingearlywarningindicators.Theseindicatorsenablepolicy makers to react to crises with adequate control measures. Several best practices areusedinternationallythatOICmembercountriesarerecommendedtoconsider.

ImprovingPublicDebtManagementIntheOICMemberCountries

9

1 Introduction

1.1 Definition of Public Debt Management

Publicdebt management is intendedtodesign thegovernment’sdebt portfolio ina targetedandefficientway.TheIMF(2014,p.5)describespublicdebtmanagementas“theprocessofestablishing a strategy for managing the government’s debt in order to raise the requiredamountoffundingatthelowestpossiblecovercostoverthemediumtolongrun,consistentwith a prudent degree of risk.” Public debt management is an everyday business that is notonlyrelevantwhenabudgetdeficithastobefinancedormaturingdebthastoberepaid.Debtmanagement relates to the total stock of outstanding debt, whose structure (e.g. currencydenomination, creditor base, maturity structure and interest rates) can be changed throughoperations on the moneyand capital markets. While debt management in the privatesectorprimarilyaimstominimizecostsandrisks,debtmanagementinthepublicsector(DeM)canpursue additional goals, such as macroeconomic stabilization (Tobin 1963), tax burdensmoothing(Barro1995)orastabilizationofthepublicbudget(Missale2000).

Historicalexperienceswithsovereigndebtcrises(e.g.Mexicoin1994,Turkeyin1994,Russiain1998andArgentinain2001)andtherecentsovereigndebtcrisisinEurope,triggeredbytheU.S.financialcrisisstartingin2007,haveshownthatpublicdebtmanagementisrelevantforboth high and lowerincome countries. As the IMF (2014, p. 6) pointed out, public debtmanagement is closely linked with a country's financial stability and crisis vulnerability:“Sound risk management practices are essential given that a government’s debt portfolio isusually the largest financial portfolio in the country and can contain complex and riskyfinancialstructures,whichhavethepotentialtogeneratesubstantialriskstothegovernment’sbalance sheet and overall financial stability. Sound risk management by the public sector isalsoessentialforriskmanagementbytheprivatesector.“

Governments regularly borrow to finance public expenditures. Overall, the decision on theamounttobeborrowedshouldbebasedonasustainabilityanalysisofpublicdebt.Suchfiscalsustainability typically relates to the solvency of the government, i.e. the ability to continueservicingitsdebtwithoutanunrealisticallylargefuturecorrectionofthebudgetbalanceoranexplicitdefault(see,e.g.,Burnside2005, IMF2007).Toraisethe intendedfunds,publicdebtmanagers have to choose suitable finance instruments and seek for the best borrowingconditions, i.e. to raise the funds at the lowest cost. Additionally, they have to structure thedebtportfolioinawaysuchthatnegativeeffectsofeconomicorfinancialshocksonthepublicbudget are minimized (see, e.g., Melecky 2007). Thus, financing public debt in an efficientmannerrequiresacomplexmultiperspectiveapproach.

Generally,publicdebtmanagementdescribestheprocessofestablishingandimplementingaprudent strategy for raising the required amount of funding, while considering thegovernment’scostandriskpreferences.Inanyevent,thegovernmentmaysetadditionalgoals,suchasdevelopingandmaintaininganefficientmarketforgovernmentsecurities.Inpractice,publicdebtmanagementusuallyinvolvesthefollowingtasks(Wheeler2004):

Establishingclearpublicdebtmanagementobjectiveswithinasoundgovernanceframework,includingaprudentcostandriskmanagementstrategyandaccompanyingportfoliomanagementpolicies;

Establishinganefficientorganizationalstructureandappropriatemanagementinformationsystems;

Ensuringthatallportfoliorelatedtransactionsareconsistentwiththegovernment’sdebtmanagementstrategywhilebeingefficientlyexecuted;

ImprovingPublicDebtManagementIntheOICMemberCountries

10

Establishingreportingprocedurestoensurethatthegovernment’sdebtmanagersareaccountablefortheirassigneddebtmanagementresponsibilitiesandassignments.

Themainpurposeofthisstudyistoexaminepublicdebtmanagementpracticesinthemembercountriesof theOrganizationofIslamicCooperation(OIC)andtoproposerecommendationsfor improving public debt management in the OIC member countries. The study explicitlyconsiders the institutional framework of public debt management and the debt structure.Otherimportantissuesregardingthesustainabilityofpublicdebt,suchasthelevelsofpublicbudgetdeficitsanddebt,andwhetherdebtisissuedforfinancinginvestmentorconsumptionarebeyondthescopeofthisstudy.Thedecisionontheamounttobeborrowedismadebythegovernmentbeforetheprocessofpublicdebtmanagementsetsin.

1.2 Performance Indicators and Best Practices

The World Bank (2015) has developed the Debt Management Performance Assessment(DeMPA) methodology to assist countries in improving their public debt management. TheDeMPAperformanceindicatorscoverfivedimensionsofpublicdebtmanagement,namely:(1)governance and strategy development, (2) coordination with macroeconomic policies, (3)borrowing and related financial activities, (4) cash flow forecasting and cash balancemanagement, and (5) debt recording and operational risk management (see Table 11 forfurtherdetails).

Table 1-1: World Bank DeMPA Performance Indicators

Performance Indicator Description

1. Governance and Strategy Development

LegalFramework The existence, coverage and content of the legal framework onauthorization to borrow (in both domestic and foreign markets),undertake debtrelated transactions (e.g. debt exchanges as well ascurrencyandinterestswaps)andissueloanguarantees

ManagerialStructure (1)Managerialstructureforcentralgovernmentborrowinganddebtrelatedtransactions

(2) Managerial structure for preparation and issuance of centralgovernmentloanguarantees

DebtManagementStrategy

(1) Quality of the DeM strategy document (guidelines and targetrangesofindicatorsforinterestrate,refinancing,andforeigncurrencyrisks)

(2)DecisionmakingprocessandpublicationoftheDeMstrategy

DebtReportingandEvaluation

(1) Publication of a statistical bulletin on debt, loan guarantees anddebtrelatedoperations

(2)Reportingtoparliamentorcongress

Audit (1) Frequency and comprehensiveness of financial, compliance, andperformanceaudits(oftheeffectivenessandefficiencyofgovernmentDeM operations, including the internal control system), andpublicationofexternalauditreports

(2)Degreeofcommitmenttoaddresstheoutcomesfromtheaudits

ImprovingPublicDebtManagementIntheOICMemberCountries

11

Performance Indicator Description

2. Coordination with Macroeconomic Policies

CoordinationwithFiscalPolicy

(1)Supportingfiscalpolicymakersthroughtheprovisionofaccurateand timely forecasts on total central government debt service underdifferentscenarios

(2) Availability of information on key macroeconomic variables, aswellasthequalityandfrequencyofdebtsustainabilityanalyses

CoordinationwithMonetaryPolicy

(1) Clarity of separation between monetary policy operations andDeMtransactions

(2) Coordination with the central bank through regular informationsharing on current and future debt transactions and the centralgovernment’scashflows

(3)Extentofthelimitofdirectaccesstofinancialresourcesfromthecentralbank

3. Borrowing and Related Financial Activities

DomesticBorrowing (1)The extent to which marketbasedmechanismsareused to issuedebt; the preparation of an annual plan for the aggregate amount ofborrowinginthedomesticmarket,dividedbetweenthewholesaleandretail markets; and the publication of a borrowing calendar forwholesalesecurities

(2) Availability and quality of (documented) procedures forborrowing in the domestic market and interactions with marketparticipants

ExternalBorrowing (1) Documented assessment of the most beneficial or costeffectiveborrowingtermsandconditions(includinglenderorsourceoffunds,currency,interestrateandmaturity)andaborrowingplan

(2) Availability and quality of documented procedures for externalborrowings

(3) Availability and degree of involvement of legal advisers beforesigningoftheloancontract

LoanGuarantees,Onlendingandderivatives

(1)Availabilityandqualityofdocumentedpoliciesandproceduresfor

approvalandissuanceofcentralgovernmentloanguarantees

(2)Availabilityandqualityofdocumentedpoliciesandproceduresforapprovalandissuanceofcentralgovernmentonlending

4. Cash Flow Forecasting and Cash Balance Management

(1)Effectivenessofforecastingtheaggregatelevelofcashbalancesin

governmentbankaccounts

(2) Decision of a proper cash balance (‘liquidity buffer’) andeffectiveness of managing the intended cash balance in governmentbank accounts (including the integration with any domestic debtborrowingprogram,ifrequired)

ImprovingPublicDebtManagementIntheOICMemberCountries

12

Performance Indicator Description

5. Debt Recording and Operational Risk Management

DebtAdministrationandSecurity

(1) Availability and quality of documented procedures for theprocessingofdebtrelatedpayments

(2) Availability and quality of documented procedures for debt andtransaction data recording and validation, as well as storage ofagreementsanddebtadministrationrecords

(3)Availabilityandqualityofdocumentedproceduresforcontrollingaccess to the central government’s debt data recording andmanagementsystemandaudittrail

(4) Availability and frequency of offsite, securely stored debtrecordingandmanagementsystembackups

SegregationofDuties,StaffCapacityandBusinessContinuity

(1)Segregationofduties forkeyfunctionsandthepresenceofariskmonitoringandcompliancefunction

(2)Sufficientstaffcapacityandhumanresourcemanagement

(3) Presence of an operational risk management plan, includingbusinesscontinuityanddisasterrecoverystrategies

DebtandDebtRelatedRecords

(1)Completenessandtimelinessofcentralgovernmentrecordsonitsdebt,loanguaranteesanddebtrelatedtransactions

(2)Completeanduptodaterecordsofgovernmentsecuritiesholdersinasecureregistrysystem,ifapplicable

Source: World Bank (2015)

(1)GovernanceandStrategyDevelopment

Legal framework and managerial structure

Public debt management requires a legal framework defining the authority for public debtmanagement operations such as borrowing and issuing new debt, undertaking debtrelatedtransactions andproviding loan guarantees. Themanagerial structure should includea cleardefinition of roles and responsibilities. Generally, it is recommended to have a divisionbetweenthepolitical level,i.e.thepresident,ministeroffinance,thecabinet,theparliamentorcongress, or any other responsible political authority at the executive level who sets theoverall government debt management objectives and decides on the risk level that thegovernment is willing to tolerate, and the executive level, i.e. the entities responsible forimplementingsuchpolicydecisions(seeFigure11).

ImprovingPublicDebtManagementIntheOICMemberCountries

13

Figure 1-1: Public Debt Management Governance Structure

Note: DeM = Public Debt Management, SAI = Supreme Audit Institution Source: World Bank (2015, p. 6).

It is advisable that public debt management operations are undertaken by one integratedprincipal entity, such as a debt management office (DMO). Only as an alternative if suchintegration is not feasible, multiple entities may execute specialized tasks. In that case, allentities should ensure a regular exchange of information and a clear coordination of theiractivitiesthroughformalinstitutionalmechanisms.Inprincipal,itprovestobebeneficialifthetask of public debt management is assigned to either the national central bank or to theMinistry of Finance. On one hand, concerns over price stability and a smooth transmissionchannel of monetary policy may speak in favor of the central bank. On the other hand, thepursuit of macroeconomic goals and, in practice most importantly, the minimization offinancingcostsforthebudgetmaymaketheMinistryofFinancetheadequateinstitutionforsupervising and conducting debt managementoperations. Moreover, locating a consolidateddebt management entity within the Ministry of Finance facilitates coordination andinformation sharing. For a separate debt management office outside the mentionedinstitutions,formalagencyarrangementsaswellasstrongeraccountabilityandtransparencyframeworksarerequired(Togoetal.2003).Finally,debtmanagementtasksmaybeassignedtoaninteragencybody.However,giventhattheMinistryofFinanceisthenaturalauthorityresponsibleforacountry’sfinancialstability,suchabodyshouldbechairedbytheMinistryofFinance(Banguraetal.2000).

Debt management strategy

The legislation should stipulate the debt management entity to develop a debt managementstrategy. The strategy defines the objectives for the management of domestic and externalpublic debt, other financial (contingent) liabilities and related assets. In particular, the debtmanagementstrategyreferstoadocumentthatdefinestargetvaluesandbenchmarksforriskindicatorsof the debt structure.Developinga debtmanagement strategymayprovide manyadvantages(Cabral2015),includingbutnotlimitedto:

ImprovingPublicDebtManagementIntheOICMemberCountries

14

Makingprudentborrowingdecisionsbasedonananalysisofcostsandrisks Facilitatingintragovernmentalandcreditoraddressedcommunicationandcoordination

toreduceuncertainty Givingdebtmanagersaclearmandate,therebyensuringgoodgovernanceand

accountability Fosteringthedevelopmentofadomesticdebtmarketbymakingthegovernment’sdebt

goalstransparenttomarketparticipants

Overall, a sound risk management is essential for fiscal sustainability. The most importantriskstobetakenintoaccountarethefollowing:

Refinancingriskorrolloverrisk,i.e.theriskthatthegovernmentisunabletorefinancematuringdebt.Theshorterthematurityofdebtis,thehigheristheamountofdebttoberolledoverinagivenyearandthehighertherefinancingrisk.

Interestrateriskorrefixingrisk,i.e.theriskthatborrowingcostsincreasedueofunfavorabledevelopmentsininterestrates.Interestrateriskishigherifcontractsarebasedonvariableinterestrates.Withfixedinterestrates,itcoverstheriskthatrefinancingofmaturingdebtisrealizedathigherinterestrates.

Exchangeraterisk,i.e.theriskthatadevaluationoftheexchangerateincreasesthevalueofdebtexpressedindomesticcurrency.Hence,exchangerateriskisrelevantfordebtdenotedinforeigncurrency.

Additionally, debt managers face operational risks that should be managed throughgovernance and control functions (see Table 12). Indicators to be assessed in the debtmanagement strategy also include projections of the total debt service and the maturitystructureunderdifferentscenarios.

Table 1-2: Risks Relevant for Public Debt Management

Risk Description

Refinancingriskorrolloverrisk

Referstotheriskthatdebtwillhavetoberefinancedatahighercostorcannotberefinancedatall.Totheextentthatrefinancingriskislimitedtotheriskthatdebt might have to be financed at higher interest rates, including changes increditspreads,itmaybeconsideredatypeofinterestraterisk.However,itisoften treated separately, because the inability to refinance maturing debtand/orexceptionallylargeincreasesingovernmentfundingcostsarelikelytogiverisetoadebtcrisis.Additionally,bondswithembeddedputoptionsmaypotentiallyexacerbaterefinancingrisk.

Measures of refinancing risk include the share of debt maturing within one,twoandthreeyearstototaldebttheaveragetimetomaturity(ATM),theshareofshorttermtolongtermdebt,ortheredemptionprofile.

Interestrateriskorrefixingrisk

Refers to the risk of increases in the cost of debt arising from changes ininterestrates.Forbothdomesticandforeigncurrencydebtchangesininterestrates influencedebtservicingcostson newissuances when fixed ratedebt isrefinanced,andonexistingandnewfloatingratedebtat therateresetdates.Generally,shorttermandfloatingratedebtisconsideredtobethesubjecttoahigherriskthanlongterm,fixedratedebt.

Measuresofinterestrateriskincludetheaveragetimetomaturity(ATM),theshare of fixedrate to floatingrate debt and the average time to interest raterefixing(ATR).

ImprovingPublicDebtManagementIntheOICMemberCountries

15

Risk Description

Exchangeraterisk

Refers to the risk of increases in the value of debt arising from changes inexchangerates.Debtdenominatedinorindexedtoforeigncurrenciesmayaddvolatility to debt servicing costs as measured in domestic currency due toexchangeratemovements.

Measures of exchange rate risk include the share of foreign currency todomestic currency debt, the currency composition of foreign currency debt,andtheshareofshorttermexternaldebttointernationalreserves.

Liquidityrisk Referstotheriskthatthevolumeof liquidassets,especiallycash,diminishesquickly as a result of unanticipated cashflow obligations and/or possibledifficultiesinraisingfundsthroughshorttermborrowing.

Creditrisk Theriskofnonperformancebyborrowerson loans orother financialassets,orbyacounterpartyonfinancialcontracts.Thisriskisparticularlyrelevantincases where debt management includes the management of liquid assets. Itmay also be relevant with regard to the acceptance of bids in auctions ofsecuritiesissuedbythegovernmentandcreditguarantees,andwithrespecttoderivativecontractsenteredintobythedebtmanager.

Settlementrisk Referstotheriskthatcounterpartydoesnotdeliverasecurityasagreedinacontract,afterthecountry(othercounterparty)hasalreadymadethepaymentaccordingtotheagreement.

Operationalrisk

Refers to a range of different types of risks, including but not limited totransaction errors in the various stages of executing and recordingtransactions; inadequacies or failures in internal controls, or in systems andservices;reputationrisk;legalrisk;securitybreaches;ornaturaldisastersthataffect the debt manager’s ability to pursue activities required to meet debtmanagementobjectives.

Sources: IMF (2014, pp. 12-13), World Bank (2015)

Debt reporting and evaluation

To ensure a transparent disclosure of the debt portfolio, it is recommended that a statisticbulletin is published regularly, including information on domestic and external public debtstocks and ratios (by creditor, residency classification, instruments, currency, interest ratebasis and original and residual maturity), debt flows (especially principal and interestpayments)andloanguaranteesdecomposedbytypeofloanandclarifyingtheamountthathasalreadybeenamortized.

(2)CoordinationwithMacroeconomicPolicies

Publicdebtmanagement interactswith fiscal andmonetarypolicy.Fiscal policy involves theusage of public spending, taxes and other sources of revenue which determine the primarybudgetbalanceandinfluenceeconomicoutcomes.Objectivespursuedbyfiscalpolicyincludestabilizing the economy, improving resource allocation and providing public goods andservicesandinfluencingtheincomedistribution.Monetarypolicyprimarilyaimsatachievingprice stability.Bydoingso, it inevitablyaffects both interest rates and exchange rates whilepossibly trying to stabilize output. Instruments available to monetary policy include openmarket operations and regulatory tools, e.g. reserve requirements. The objectives and the

ImprovingPublicDebtManagementIntheOICMemberCountries

16

implementation of public debt management, fiscal policy and monetary policy areinterdependentandinvolvetradeoffs(seeTable13).However,itisadvisedthatpublicdebtmanagement should be pursued independently (Togo 2007). Nevertheless, fiscal policymakers, monetary policy makers and debt managers should coordinate their actions, e.g. byestablishing an internal public debt committee, and agree on common objectives such astargetsorceilingsonthedeficitandonthestockofpublicdebt(Allenetal.2013).

Table 1-3: Interdependencies of Public Debt Management, Fiscal Policy and Monetary Policy

Source: Togo (2007)

Debtmanagementtransactionsshallbeformallyseparatedfrommonetarypolicyoperationsifthe central bank conducts debt management transactions as an agent of the centralgovernment.Itisrecommendedthatthecentralbankprovidesinformationtothegovernmentandmarkets,clearlystatingwhetheritperformstransactionsundertheobjectiveofmonetarypolicy or debt management on behalf of the government. A steady exchange of informationbetween the debt management entity and the central bank on current and future debttransactionsandoncentralgovernmentcashflowsisadvisable,especiallyifthosetransactionsare important for monetary policy. Moreover, a formal limitation concerning public funding

Public Debt Management

Objective:raisingtherequiredamountofgovernmentfundingatthelowestpossiblecost,consistentwithaprudentdegreeofrisk

Target:debtstructuring

Instruments:operationsonthecapitalmarkets

Fiscal Policy

Objective:achievingtheleastdistortingbudgetarypolicythatstabilizesoutput,improvestheresourceallocationandmanagesdistributiveeffects

Target:primarybudgetbalance

Instruments:governmentspending,taxes

Debt management actions are likely to influence thegovernment’s debt service costs, and can thus forcegovernmentstoreduceexpenditurestodecreasedebtlevelsandmeettheirdebtobligations.

Fiscalpolicymeasures(inparticularspendingandtaxation)arelikely to influence the risk premium of government debt whichaffects debt managers’ ability to issuing debt instruments andbuildasounddebtportfolio.

Monetary Policy

Objective:achievingpricestabilitywhilepossiblystabilizingorincreasingoutput

Targets:inflation,interestrates,monetaryaggregates,exchangerate

Instruments:openmarketoperations,regulatorytools.

Thedebtstructure,includingmaturity,floatinginterestratesorcurrencydenomination,are likelytorestrainthecentralbank’spolicyoptions,e.g.inincreasinginterestratesordevaluatingthedomestic currency, given that these measures may potentiallytriggeradebtcrisis.

Exchangerateandinterestratepoliciesarelikelytorestricttheissuanceofforeigncurrencydebtandfloatingratedebt.Aloosemonetary policy may increase the inflation expectations ofinvestors,andhencerequiredebtmanagerstoissueshorttermdebt,ordebtthatisindexedtoinflationrates.

ImprovingPublicDebtManagementIntheOICMemberCountries

17

through the central bank may be put in place, restricting direct financing to exceptionalemergencysituationsandalimitedtimeperiod.

(3)BorrowingandRelatedFinancialActivities

To fulfill theprojectedborrowingrequirements,marketbased instrumentssuchasauctions,syndication, tap issuance or retail issuance might be used. Moreover, it is recommended topublishanannualborrowingplanfordomesticandexternalborrowing.Thisborrowingplanshall distinguish between wholesale and retail markets, and other sources of funding. Aborrowingcalendarincludingdebtinstruments,issuedatesandindicativeborrowingamountsfor wholesale securities may be released regularly. It is usually advisable that the generalpublicshallhaveaccesstoinformationonproceduresfordomesticandexternalborrowing,aswellastheterms,conditionsandcriteriaforaccessingprimarywholesaleandretailmarkets.Thedebtmanagemententitymayregularlydiscussitsassessmentonborrowingplansandthedevelopmentof(domestic)marketswithmarketparticipants.Similarly,anassessmentofthemost advantageous and costeffective terms and conditions for external borrowing may beprepared. Internal documented procedures for all external borrowing should be easilyaccessibleandregularlyreviewed.Allrelevantfinancialtermsoftheloantransactionshallberegisteredintoadebtrecordingsystem,preferablyinatimelymanner.Legaladvisersmaybeconsultedduringthenegotiationprocessandmayauthorizethelegalarrangements.