improving the relationship between directors and shareholders part a: the context of shareholding in...

TRANSCRIPT

Improving the relationship between directors and

shareholders

Part A: The Context of Shareholding in Europe

Dr. Roger BarkerDirector of Corporate Governance, Institute of Directors (UK)

Senior Advisor to the Board of [email protected]

2

The structure of company ownership in Europe

The Berle and Means vision of dispersed shareholdings offers a good description of listed corporations in the United States and the UK

It was assumed that it was a common feature of economic development in all countries…but new evidence emerged in the 1990s

Initial work on ownership structure of listed European companies undertaken by Franks and Mayer (1995)…it turns out that shareholdings in continental Europe are often not widely dispersed!

These results confirmed by more detailed studies: e.g. La Porta et al (1997; 1999); Barca and Becht (2001); Faccio and Lang (2002)

Ownership structure has significant implications for the relationship between shareholders and directors – foreign ownership is also expanding rapidly in most European markets

3

Implications of concentrated ownership for board-shareholder relations

The presence of controlling shareholders may reduce the willingness of institutional investors, foreign investors and other minority shareholders to invest or engage with companies

Minority shareholders may feel vulnerable when investing alongside a controlling shareholder – even with investor protections, there is a significant asymmetry of power

The board of directors may have little effective power May be less emphasis on corporate transparency

However: Controlling shareholders may be more willing to adopt a longer-term

outlook than institutional investors – they can insulate the management from stock price fluctuations and economic cycles

Management is directly monitored by the owner of the company. Less scope for CEOs to pursue private agendas, e.g. in terms of executive remuneration, takeovers, empire-building, etc. In contrast, institutional investors may be less engaged.

4

Data on European Share Ownership

5

Typical widely-held UK companies and their largest shareholders

Royal Dutch Shell (Blackrock: 6.6%; Legal & General: 4.2%). Market Cap - $228 bn.

GlaxoSmithKline (Blackrock: 5.6%; Legal & General: 3.7%). Market cap - $98.6 bn.

Vodafone (Blackrock: 6.0%; Legal & General: 3.6%). Market cap - $145.9 bn.

BP (Blackrock: 5.9%; Legal & General: 4.2%). Market cap - $ 136.8 bn.

HSBC (Blackrock: 6.6%; Legal & General: 4.0%). Market cap - $181.9 bn.

All other shareholders own less than 3%

6

Typical European companies with significant shareholders

• Roche Holdings (just over 50% owned by descendents of Hoffmann and Oeri families. Novartis owns a further one third.) Market cap - $226 bn.

• VW (Piëch and Porsche families control more than 53%, State of Lower Saxony 20%, Qatar Holding 17%). Market cap - €78.3 bn

• BMW (Quandt family own around 47%). Market cap - €53 bn.• L’Oréal (Bettencourt family and Nestlé each control around a quarter of the

company and vote as a block). Market cap - €77.3 bn• Inditex (controlled by Amancio Ortega). Market cap – €70.0 bn• Investor AB has major stakes in ABB (7%), Electrolux (29.9%), Ericsson (19.3%),

Saab (39.5%) and SEB (20.9%), and is controlled by the Wallenberg family• ENI (Italian state has 30.3% golden share). Market cap - €65 bn• ArcelorMittal (Mittal family owns 40%). Market cap - $23.2 bn.• Sanofi (L’Oréal: 15.6%; Total: 8.9%). Market cap - €100.6 bn• Hennes & Mauritz (Controlled by Persson family). Market cap - $59.7 bn• Gazprom (50.002% owned by Russian state). Market cap - $108.1 bn

Source of market cap data: FT website, as of September 2013

7

Company ownership in Europe

Ownership concentration:mid/late-1990sPercentage of listed companies with blockholder (>20%)

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0

Telecom ItaliaSource: Enriques and Volpin (2007: 121)

Source: Federation of European Securities Exchanges (2008:16)

Percentage of listed companies owned by institutional investors, (i.e. domestic pension funds, insurance companies, mutual funds and other collective financial investment companies)

Source: Federation of European Securities Exchanges (2008:20)

Percentage of listed companies owned through cross-shareholdings of other non-financial companies

Source: Federation of European Securities Exchanges (2008:18)

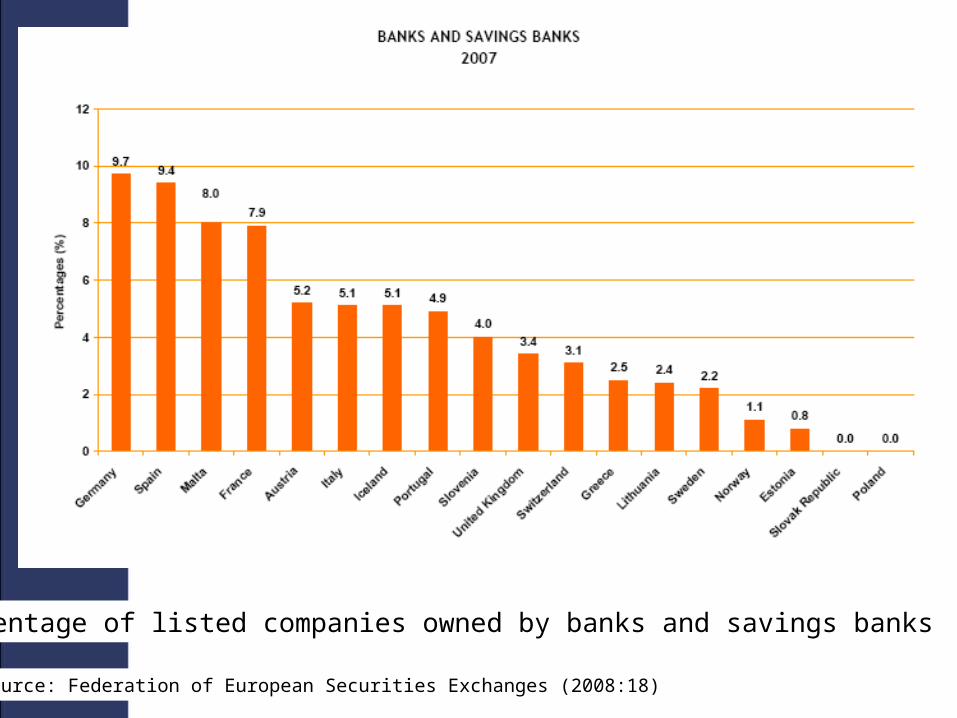

Percentage of listed companies owned by banks and savings banks

Source: Federation of European Securities Exchanges (2008:23)

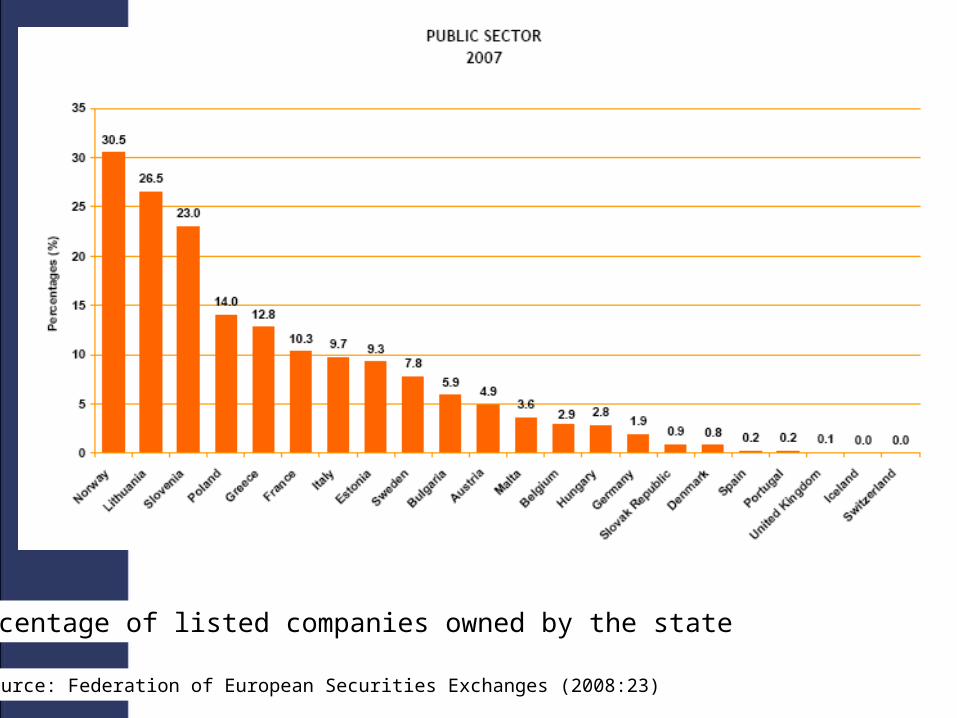

Percentage of listed companies owned by the state

Source: Federation of European Securities Exchanges (2008:13)

Percentage of listed companies owned by foreign shareholders

Sovereign Wealth Funds – increasing stakes in European companies

• Rio Tinto (12% stake from the Aluminium Corporation of China)• Lagardère (Qatar Holding took 10.1% stake in 2011; Arnaud

Lagardère holds 14% of voting shares)• Barclays (Qatar Holding took 6.8% stake in 2008, and holds

warrants for a further 3.2%; Nexus Capital Investing (Abu Dhabi) holds 6.3%)

• UBS (Government of Singapore: 6.45%)• Crédit Suisse (Olayan Group (Saudi Arabia) holds 6.6% and State of

Qatar holds 6.2%)• Volkswagen (State of Qatar: 17%)