improving valuations and unlocking sector capacity

DESCRIPTION

Improving valuations and unlocking sector capacity. NHF Treasury Management Conference, 30 Euston Square, London Andy Smith, Director, Valuations – Savills 8 th October 2014. UK Housing Tenure – More Market Renting? More intermediate tenures?. Social housing stagnant - PowerPoint PPT PresentationTRANSCRIPT

savills.com

Improving valuations and unlocking sector capacityNHF Treasury Management Conference, 30 Euston Square, London

Andy Smith, Director, Valuations – Savills

8th October 2014

UK Housing Tenure – More Market Renting? More intermediate tenures?

1918

1931

1932

1933

1934

1935

1936

1937

1938

1939

1940

1941

1942

1943

1944

1945

1946

1947

1948

1949

1950

1951

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

0%

10%

20%

30%

40%

50%

60%

70%

80%

Home ownership Social housing Market renting

Pro

po

rtio

n o

f d

we

llin

g s

tock in

En

gla

nd

(%

)

Opportunity?

Source: Savills, CLG, Survey of English Housing

Social housing stagnant

Home ownership in decline

In-betweeners

Market renting expected to increase

Policy flexibility

Opportunity for social landlords and institutions

Quality product

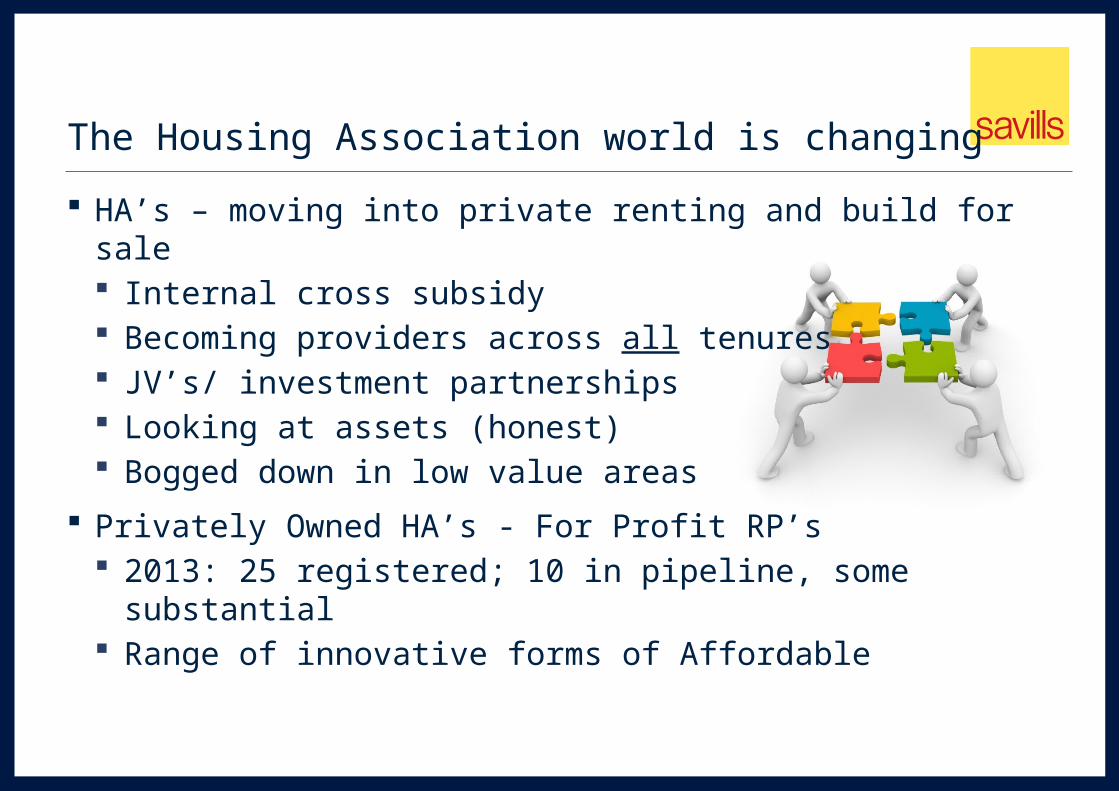

The Housing Association world is changing

HA’s – moving into private renting and build for sale Internal cross subsidy Becoming providers across all tenures JV’s/ investment partnerships Looking at assets (honest) Bogged down in low value areas

Privately Owned HA’s - For Profit RP’s 2013: 25 registered; 10 in pipeline, some substantial Range of innovative forms of Affordable

Change Drivers: Political

Government messages to RPs – build additional homes, and value for money– or merge and let someone else use the asset base

HCA wants a smaller number of larger partners and delivery of the agenda

More Welfare Reform

Additional uncertainty in HA capital and revenue income stream despite CPI plus 1% rent settlement – Univ Credit cap not helpful so make max use of resources

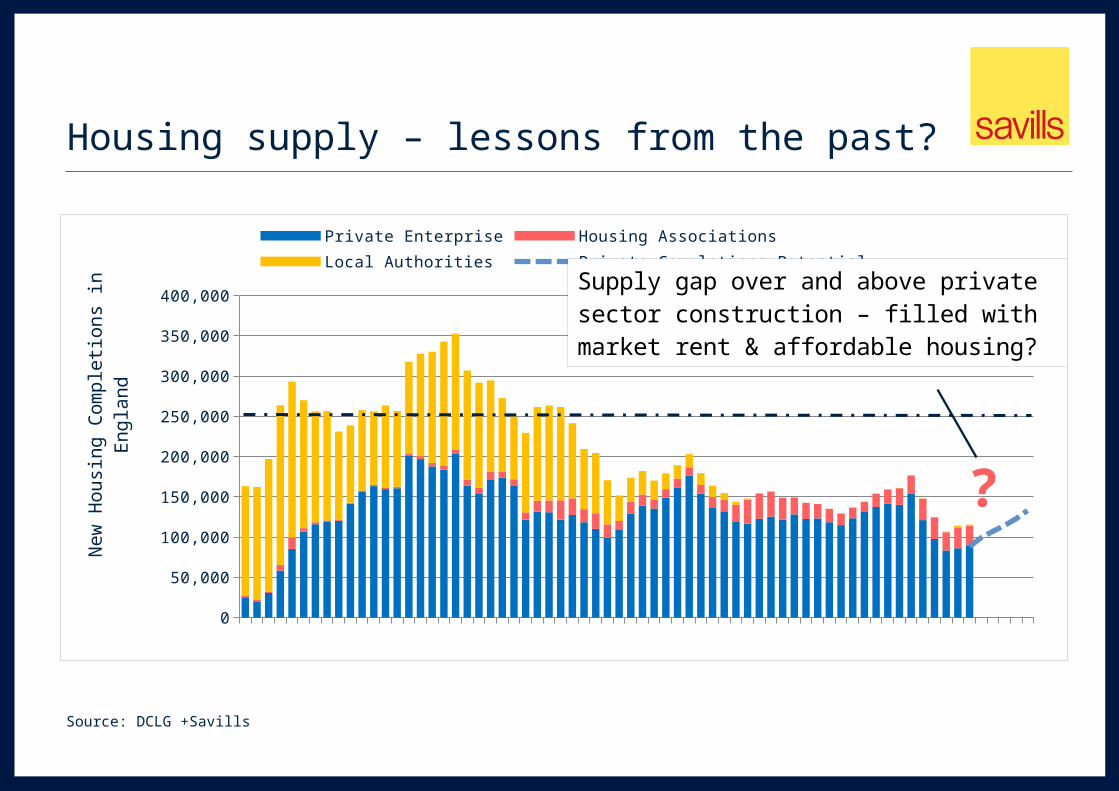

Housing supply – lessons from the past?

Source: DCLG +Savills

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Private Enterprise Housing AssociationsLocal Authorities Private Completions Potential

Ne

w H

ou

sin

g C

om

ple

tion

s in

En

gla

nd Supply gap over and above private sector

construction – filled with market rent & af-fordable housing?

?

Government plans to deliver 165,000 affordable homes between 2015 and 2018

Affordable Homes Programme - HCA Funding for new homes at 80% market rents. Up to 2015 allocated. £1.7bn 2015 -18 To hopefully fund 165,000 new homes 75% of grant if on site pre March 2015

Affordable Homes Guarantee Programme - HCA Government debt guarantee to bring down the cost of borrowing for new homes. Approximately £220m has so far been allocated out of a £350m fund to be spent by

2017.

But Starts down by 5,650 in 2014 Enthusiasm of HA players? Level of grant? Regulatory burden? Affordable Rents = more risky

than Target Rents?

Are we clear about our objectives?

Low and affordable rents

Good quality well managed homes

House maximum number of people

Build more Housing

Community initiatives

Ok - let’s use the profit approach to help us meet our objectives

Why is the profit motive good for Housing?

Higher surpluses

Greater financial capacity

More money to spend on meeting objectives

Make the right compromises

Use finite resources more effectively

The key is what you do with the profits

EUV-SH or MV-STTHow do they differ?

£0

£50,000

£100,000

£150,000

£200,000

£250,000

£300,000

New House New Flat 1930s House 1970s Flat

VP

MV-STT

EUV-SH

What does that mean in terms of £££s?

EUV-SH MV-STT VP

Asset Value £1m £2m £3m

Loan to Value 1.10 1.25 N/A

Amount Borrowed £909,000 £1,600,000

Existing Use Value for Social Housing Key Factors Affecting Valuation

Assumes sale to another RP only

Social / target / affordable rent levels

Rental growth

Condition – costs to repair / maintain

Discount Rate (All Risks Yield)

Market Value subject to TenanciesKey Factors Affecting Valuation

Assumes Mortgagee in possession

Move from Social/Affordable to Market rent levels

Active Asset Management

Opportunistic sale of voids/break up

Yield required by investor

Does location matter?

YES!

In some parts of the Country, MV-STT and EUV-SH will be the same

It’s all in the Rents!

Does location matter?

£0

£20,000

£40,000

£60,000

£80,000

£100,000

£120,000

£140,000

£160,000 Average Max Bid by Local Authority

Price movements for VP’s, MVSTTs and EUVSH - illustration

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

1 2 3 4 5 6 7 8 9 10

MV-VP

MV-STT

EUV-SH

Uplift above Base EUVSH by type

Tenure % EUV-SHExtra Care 81%General Needs 137%Mixed Lots 130%

Housing for Older People 138%

Intermediate Rent 100%

Shared Ownership 81%Sheltered 128%Supported 165% 127%

£15k per unit released for new development

So what does this tell us?

What are we being asked to value?

Its all in the lotting!

Market Evidence points to latent headroom in EUV-SH values

MV-STT is a higher value – but LTV?

Funders Attitudes

Thank you

Andy Smith

Director, Valuations

Savills, 33 Margaret Street

London, W1G 0JD

+44 (0) 20 7409 5993

+44 (0) 7967 555 480