imrb report - auto component module

TRANSCRIPT

MARKET ATTRACTIVENESS OF AUTO COMPONENT BUSINESS IN INDIA

BIRD, The Business & Industrial Research Division of IMRB International, India

Summary presentation for:

2nd – 3rd July, 2009

2

Flow of the Presentation

Scope of the study

Research Approach and Sampling Plan

Study Findings

Environment Analysis

Auto Component Market Segments in India

Market Size and Growth Rate

Import basket – Total and from ASEAN countries

Distribution channel and margins

Import duty and Government Initiatives

Conclusions and Recommendations

Attractiveness matrix and Market Entry Strategy

Annexure

3

Scope of the Study

To map the industry environment of Indian Auto Component

Industry

To understand the market dynamics1 of Auto Component

Industry in India

To gauge the attractiveness of Indian Auto Component

Market for Thai investors

1 Market Dynamics involved:-• Identification of major hubs, • Classification of auto component industry, • Analysis of component markets, • Government incentives and FDI inflows, • Growth drivers and challenges etc

4

Research Approach (Common slide for all modules)

The two pronged approach following is explained as under:

Analysis with Framework developed by BIRD@IMRB

to assess business attractiveness

QualitativeSection

Attractive Business Segments for Thai

Investors

Secondary/Database Section Qualitative

Approach Stakeholders

Unstructured Business

Interviews (UBIs)

- Industry Associations e.g.

(ACMA, SIAM)

- Auto Component Manufacturers

- Automobile Manufacturers

- OEM aftermarket channel

* 9 FGDs were conducted across 7 cities for this module

Study Findings:

6

Entry Barriers- OEMs having strategic long term vendor relationships esp. for high value items- However, OEMs open to supply meeting their quality standards at better cost- 100% FDI allowed for new player

Consumer Power- Auto OEMs have average 2 or more suppliers - Replacement marketconsumers have options for branded and cheaper spurious parts

Threat of Substitutes- Organized component players working closely with R&D teams of OEMs- Unorganized units have greater threatsas the replacement market consumers now shifting to genuine components

Industry Competitors- 450 – 500 mid to large players with around 6 to 7 thousand units- Unorganized segment : around 10,000 units- In certain segments, less competition due to lack of technology and limited players

Supplier Power- Raw material cost are 50 – 60% of total production cost- Tier structure supporting vendorrelationship

Environment Analysis of Indian Auto Component Market

Low

Moderate

HighHigh

Moderate

7

70%

30%

OEM Demand (Including Domestic & Exports)Replacement Demand

Auto Component Market in India comprise of OEM, replacement and export demand

As high as 70% of the

genuine auto component

demand in India comes

from OEMs (Domestic and

Exports)

8

Chennai (South), Delhi NCR (North) and Pune (West) are major automobile and automotive component hubs in India

9

Two wheelers contribute to 85% of the total automobile volumes in India

Passenger cars contribute 11% of the total volumes (1.32 Million) Over the past few year, automobile market is growing an average rate of 15 – 16%

Category 2002-03 2003-04 2004-05 2005-06 2006-07

Passenger Car 609 843 1018 1113 1323

Utility Vehicle 114 146 192 197 222

Commercial Vehicle 204 275 354 391 520

Two-Wheeler 5076 5623 6530 7609 9442

Three-Wheeler 277 356 374 434 556

Grand Total 6280 7244 8468 9744 11065

Growth Rate 18.13% 15.34% 16.90% 15.06% 13.55%

All Number in '000 units while Growth Rate is in percentageSource: Ministry of Heavy Industries, Government of India

10

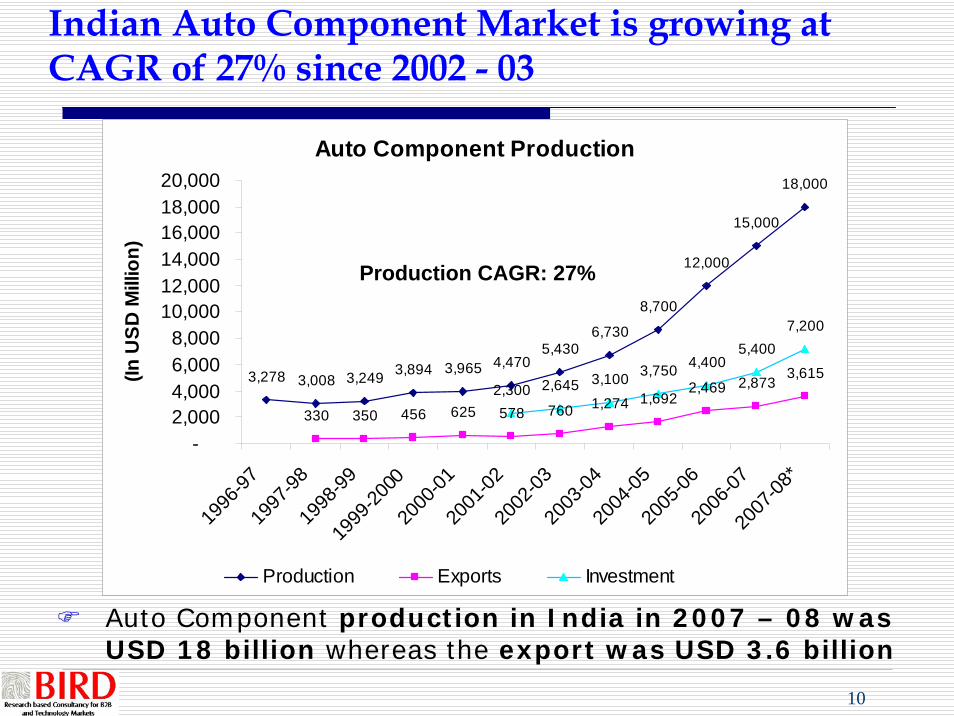

Auto Component Production

3,249 3,894 3,965 4,4705,430

6,730

8,700

12,000

15,000

18,000

330 350 456 625 578 760 1,274 1,6922,469 2,873

3,6152,300 2,645 3,100 3,750 4,400

5,4007,200

3,0083,278

-2,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

1996

-9719

97-98

1998

-9919

99-20

0020

00-01

2001

-0220

02-03

2003

-0420

04-05

2005

-0620

06-07

2007

-08*

(In U

SD M

illio

n)

Production Exports Investment

Indian Auto Component Market is growing at CAGR of 27% since 2002 - 03

Production CAGR: 27%

Auto Component production in India in 2007 – 08 was USD 18 billion whereas the export was USD 3.6 billion

11

31%19%

12%

12%10%9%

7%

Engine parts Drive transmission & steering parts Body & chassis Suspension & braking parts Equipment Electrical parts Others

Engine parts forms 31% of total Indian Auto Component Market in Value terms

In Value Terms

In value terms, engine and drive transmission & steering parts form half of the total market for auto components

12

Motor Vehicle and Engine parts formed major auto component import basked from ASEAN countries in 2004 - 05

Auto component import (OEM + Replacement) Total Import – 2004-05 (US $ Million) Growth Rate (2001-05)

Components detail All Imports

Imports from China

Imports from ASEAN

Share of China & ASEAN

All Imports

Imports from China

Imports from ASEAN

Parts and accessory of motor vehicles 543.38 3.98 61.16 12% 28% 28% 58%

Engine parts 203.19 8.99 3.09 6% 15% 113% 24%Electrical parts and accessories 29.80 0.68 0.1 3% 26% 63% -50%Bumpers and parts 23.09 0.23 1.59 8% 69% 74% 288%Injection pumps, oil pumps,

water pumps 22.67 0.73 0.01 3% 39% 111% -29%

Drive axles with differential 18.63 0.01 0.87 5% 50% -

Lighting equipment 17.46 1.8 2.01 22% 24% 14% 107%Other Brakes/Servo brakes 17.20 0.9 0.23 7% 46% 63% -17%Starter motors 11.16 0.3 1.44 16% 33% 166% 5%Clutches 9.17 0.2 0.74 10% 25% 26% 147%Wheels 7.86 0.75 0.29 13% 80% 127% 14%Steering wheels and columns 7.06 0.01 0.45 7% 45% 21% 208%Rear view mirror 4.23 0.74 0.6 32% 37% 104% 97%Laminated safety glass 1.84 0.63 0.29 50% 87% 281% 313%

Total 916.7 20.0 72.9 30% 55% 49%

Source: ACMA (Automotive Component Manufacturers Association, DGFT (Directorate General of Foreign Trade)

13

Auto Components in India generally pass from 2 – 3 nodes before reaching the end consumers

Imports are happening largely because of “pull” factor whereby OEMs and importers reaching out for cost effective procurement for desired quality products

14

Net Margin for the genuine auto components ranges from 8 – 10% for the retailers

For auto component distributors, the net margins vary between 4 – 6%

Gross Margins Net Margins

Ranges between 12 –15% based on type of part and type of manufacturer

Ranges between 4 – 6%based on type of part and type of manufacturer

Distribution Margin

Ranges between 15 –20% based on type of part and type of manufacturer

Ranges between 8 – 10%based on type of part and type of manufacturer

Retail Margin

15

Customs duty on imported auto components currently vary from 5% to 10%

However, in certain cases CVD (Countervailing Duty) and Special Additional Duty are levied

that takes the duty cover 30% to 35% of the component landing cost

100 per cent FDI inflow under automatic approval for foreign equity investment – both

automobile and auto component

Technology import on royalty payment of 5% without any duration limit and lump sum

payment of USD 2 million allowed under automatic route

Imports of automotive components is free from licensing and approvals

Initiatives taken by Indian Government

Auto component duty reduction to 5 - 7.5 % from the earlier 10 %

Setting up of the National Automotive Testing and R&D Infrastructure Project (NATRIP)

at a total cost of € 290.85 million for enabling global standards of vehicular safety, emission and

performance standards

Finalization of the Automotive Mission Plan (AMP) 2006-2016 for making India a preferred

destination for design and manufacture of automobile and automotive components

16

Quality & Price parameters play key role in purchasing auto components in the replacement market

Customers prefer to purchase replacement parts largely either from Branded shops or from OEMs / authorized service stations

Key Purchase Criteria (Replacement Market)Individual Customer

2.8

3.1

2.4

3.2

4.5

0 1 2 3 4 5

Reliability

Brand

Availability

Price

Quality

Fleet Customer

2.7

3.4

2

3.4

4.4

0 1 2 3 4 5

Reliability

Brand

Availability

Price

Quality

1 = Least Important 5 = Most Important

Source of Purchase (Replacement Parts)

35%

34%

38%

33%

42%

52%

51%

41%

51%

47%

13%

15%

21%

16%

11%

0% 20% 40% 60% 80% 100%

Equipment Parts

Suspension / Braking Parts

Transmission Parts

Electrical Parts

Engine Parts

OEM Branded Others

Source: ACMA

3.2 Conclusions and Recommendations

18

Market segments for High grade plastics and Parts for evolving technology aggregate would be attractive for Thai investors

“Thai auto component industry can supply tyres to Indian OEMs at cost effective price.”

- Sourcing Manager, one of leading passenger car manufacturers

Attractiveness Matrix for Thai Investors

Relative Degree of Technical Expertise

Abi

lity

inco

ste f

fec t

ive

sup p

l y

Low High

High

Low

- Rubber Intensive parts e.g. tyres, Accessories- Skill intensive parts

High grade plastic, IC based electronic parts /

assemblies

Labour Intensive parts, - casting, forging etc

Parts for evolving technology aggregates

19

Thai Investors should initially focus on entering plastics, silicon intensive electronics parts, rubber intensive parts auto components

20

Phase wise entry strategy for attractive auto component segments

Phase I – Supply from plants located in Thailand or other countries

• Form vendor relationship with Indian OEMs• Export parts from Thailand / other countries• Set up warehouse at port of entry for efficient distribution management• Target replacement market for auto accessories like alloy wheels, music systems, car perfumes, decorative stickers etc

• Set up assembly unit in India• Assembly unit to be set up at one of the auto clusters, nearer to OEMs• Consolidate business with old OEMs and target new OEMs and Tier – 1 suppliers• Use raw material procured from India or from Thailand / other countries

• Focus on replacement market for core components once the products is established among OEMs• To be targeted after establishing credibility among OEMs• Acceptance by OEMs initially provide necessary push to these components in replacement market

Phase II – Bring manufacturing

closer to marketplace

Phase III – Target servicing

replacement market

Thank You

Annexure

23

Major OEM players in India

Passenger Cars Commercial Vehicles Two-Wheelers Three-WheelersMaruti Suzuki Ashok Leyland Hero Honda Bajaj AutoHyundai Tata Motors Bajaj Auto PiaggioTata Motors Eicher Motors TVS Motors Mahindra & MahindraHonda Swaraj Mazda Royal Enfield Motors TVS MotorsMahindra & Mahindra Volvo Kinetic Motors Tata MotorsToyota MAN-Force Suzuki Motors Force MotorsFiat Yamaha Motors

Hindustan Motors Honda

General Motors LML India

Ford

Volkswagen

Renault

Mercedes Benz

Skoda

BMW

Volvo

24

Auto Components Sub-segments and Key Players

Sub-segments Auto Component ManufacturersTata Autocomp Systems Ltd, PuneDenso IndiaMotherson Sumi, Delhi NCRMacro Precision Components, Bangaluru

Appollo Tyres, Delhi NCRCeat Tyres, MumbaiMRF Tyres, ChennaiSundaram Clayton Ltd, Chennai

Lucas TVS, Chennai

Parts for evolving technology aggregates

Delphi TVS, Chennai

Skill intensive engine parts

Clutch AutoMunjal Showa, Delhi NCRSona Koyo, Delhi NCRRane TRW Steering Systems LimitedAmtek AutoLucas TVS, Chennai

Bosch India, BangaluruUcal Fuel Systems LtdPrecision Sintered Products, Gujarat

Rubber intensive parts and accessories

Plastics, Silicon intensive and electronics parts

25

Auto Components Sub-segments and Key Players

Sub-segments Auto Component ManufacturersBharat Forge, PuneAutomotive axles, MysoreUnitech Texmech Pvt. Ltd., PuneProgressive Gears Industries (P) Ltd, Delhi

Labour intensive - casting, forging parts

26

Auto Components Sub-segments and Key Players

Product Segment Key Sub-Segments Major PlayersGears & Drive Rico Auto IndsClutches Automotive AxlesAxles Wheels India Ltd.Others Sona Koyo Steer.

GKN Driveline (India)Starter Motors, Generator, DensoDistributor, Spark Plugs, Motherson SumiIgnition Coil, Flywheel MICOMagnet, Voltage Regulator, Minda IndustriesElectrical Ignition India Nippon

Lucas TVS

Engine Parts

Pistons Piston Rings Engine Valves CarburettorsFuel Delivery System

EscortsIndia PistonsGoetze (India)India PistonsRane Engine ValvesShriram Pistons & RingsSpaco CarburettorsUcal FuelLucas TVSMICO Germany

Electrical Parts

Transmission and Steering

27

Major Players for Auto Components – Key sub-segment wise (contd…)

Product Segment Key Sub-Segments Major Players

Headlight Lumax, Autolite, Phoenix Lamps

Dashboard Premiere Instruments & Controls

Sheet Metal Jay Bharat Maruti, OmaxAuto, JBM tools

Suspension and BrakingBrake SystemBrake LiningsShock Absorbers

Automotive AxlesBrakes IndiaKalyani BrakesAllied NipponRane Brake LiningSundaram BrakeGabriel IndiaMunjal Showa

Fan Belts Rico AutoSheet Metal Rico AutoOthers

Equipment