imrf board rankings reserve policy fy budget · village of bannockburn employer nbr: 06601 linda...

TRANSCRIPT

VILLAGE OF BANNOCKBURN

IMRF Board Rankings Reserve Policy

FY 2015/2016 Budget

Preliminary Notice of Illinois Municipal Retirement Fund Contribution Rate for Calendar Year 2016

Date April 2015

Employer name VILLAGE OF BANNOCKBURN Employer No. 06601

The employer rate below is based on a 27 year amortization period for most employers. Overfunded employers will receive a letter outlining options available to accelerate the amortization of their overfunding (which reduces rate) If they so choose.

Your IMRF contribution rates on all earnings paid to IMRF members and employer rate in the 2016 calendar year are as follows:

Member Contributions (tax-deferred) ...

Employer Contributions Retirement Rate

Normal Cost .. .

Funding Adjustment <over> under ... .......... .

Net Retirement Rate ......

• Other Program Benefits

Death

Disability ....

Supplemental Benefit PayrnenL ... . . ..... .. ... .

Early Retirement Incentive .... ....... .... .. ..

• TOTAL EMPLOYER RATE ............ .. ................ .

IMRF Contributions

Regular

4·50%

7.29%

3.51%

10.80%

0.18%

0.14%

0.62%

0.00%

11·74%

Tile Final Notice of IMRF Contribution Rates for Calendar Year 2016 will be posted in November 2015. If you have any questions regarding this preliminary rate notice, please contact the IMRF Employer Account Analyst at i ·800-ASK-IMRF.

VILLAGE OF BANNOCKBURN LINDA MCCULLOCH, FINANCE DIRECTOR 2275 TELEGRAPH RD Ste 2 BANNOCKBURN IL 60015-1594

Oak Brook, IL 60523-2337 1-800-ASK-IMRF (275-4673)

IMRF.

2014 EMPLOYER RETIREMENT RESERVE STATEMENT REGULAR RESERVE ACCOUNT

www.imrf.org

PAGE: 1

VILLAGE OF BANNOCKBURN EMPLOYER NBR: 06601 LINDA MCCULLOCH, FINANCE DIREC 2275 TELEGRAPH RD Ste 2 BANNOCKBURN IL 60015-1594

PHONE NUMBER: 847-945-6080

FIELD REP .... : KATE SETCHELL PHONE NUMBER: 708-848-4171

NORMAL COST FUNDING ADJ OVRjUND

RETIREMENT

7.890 DISABILITY 6.880 DEATH

SUPPLEMENTAL PENSION 14.770

OPENING BALANCE, JANUARY 1, 2014 .... _ .................. . INTEREST ON OPENING BALANCE - RATE: 7.500% EMPLOYER RETIREMENT CONTRIBUTIONS (14.770% X 1,163,041.75) RESIDUAL INVESTMENT INCOME EARNINGS CREDIT ER FOR RET RESERVE CONT

ENDING BALANCE, DECEMBER 31, 2014

.110

.240

.620

1,729,949.87 129,746.24 171,781.18 17,629.18-

250,000.00

2,263,848.11

Employer # 06601

PLEASE

KEEP THIS GASB FOOTNOTE DISCLOSURE STATEMENT FOR THE AUDITORS

THIS STATEMENT CAN ALSO BE VIEWED AT IMRF.ORG EMPLOYER DOCUMENT ARCHIVE

This information is intended to provide your governmental unit with pension information required in the Notes to Financial Statements for your next annual financial report. The following information is patterned after illustration 6 shown on pages 32 and 33 of the Governmental Accounting Standards Board Statement No . 50 for an employer contributing to an agent-multiple-employer defined benefit pension plan.

Employers who have a fiscal year ending other than December 31 will have to adjust the information shown in the three - year trend information to reflect their fiscal year. IMRF has provided a template at www.IMRF.org for employers who have a fiscal year ending after December 31 , 2013 or later, and who opted to use the optional phase-in rates to assist in calculating their net pension obligation.

This information should be shared with your auditors. Questions can be directed to Corey Lockwood at (630) 706-4226 or [email protected].

Village of Bannockburn Linda McCuiioch 2275 Telegraph Rd Ste 2 Bannockburn IL 60015

Employer # 06601 GASB 50 Disclosures

Note X. Pension Plan

Plan Description. The employer's defined benefit pension plan for Regular employees provides retirement and disability benefits, post retirement increases, and death benefits to plan members and beneficiaries. The employer plan is affiliated with the Illinois Municipal Retirement Fund (IMRF), an agent multiple-employer plan. Benefit provisions are established by statute and may only be changed by the General Assembly of the State of Illinois. IMRF issues a publicly available fmancial report that includes financial statements and required supplementary information (RSI). That report may be obtained on-line at www.irnrf.org.

Funding Policy. As set by statute, your employer Regular plan members are required to contribute 4.50 percent of their annual covered salary. The statute requires employers to contribute the amount necessary, in addition to member contributions, to finance the retirement coverage of its own employees. The employer annual required contribution rate for calendar year 2013 was 18.66 percent. The employer also contributes for disability benefits, death benefits and supplemental retirement benefits, all of which are pooled at the IMRF level. Contribution rates for disability and death benefits are set by the IMRF Board of Trustees, while the supplemental retirement benefits rate is set by statute.

Annual Pension Cost. The required contribution for calendar year 2013 was $207,292. (If you made an additional payment toward your unfunded amount, add this payment to your monthly contributions, based on payroll and recalculate the percentage of APC contributed.)

Three-Year Trend Information for the Regular Plan

Calendar Percentage Year Annual Pension of APC Ending Cost (APC) Contributed 12/31/13 207,292 100% 12 /3 1 /12 184,902 100% 12/31/11 141,956 100%

Net Pension Obligation

$0* 0* 0*

*Ifyou utilized the phase-in contribution rate, the net pension obligation will have to be calculated.

The required contribution for 2013 was determined as part of the December 31, 2011, actuarial valuation using the entry age normal actuarial cost method. The actuarial assumptions at December 31, 2011 , included (a) 7.5 percent investment rate of return (net of administrative and direct investment expenses), (b) projected salary increases of 4.00% a year, attributable to inflation, (c) additional projected salary increases ranging from 0.4% to 10% per year depending on age and service, attributable to seniority/merit, and (d) post retirement benefit increases of 3% armually. The actuarial value of your employer Regular plan assets was determined using techniques that spread the effects of short-term volatility in the market value of investments over a five-year period with a 20% corridor between the actuarial and market value of assets. The employer Regular plan's unfunded actuarial accrued liability at December 31, 2011 is being amortized as a level percentage of projected payroll on an open 30 year basis.

Funded Status and Funding Progress. As of December 31 , 2013, the most recent actuarial valuation date, the Regular plan was 72.52 percent funded. The actuarial accrued liability for benefits was $3,112,290 and the actuarial value of assets was $2,257,147, resulting in an underfunded actuarial accrued liability (UAAL) of $855,143. The covered payroll for calendar year 2013 (annual payroll of active employees covered by the plan) was $1,110,892 and the ratio of the VAAL to the covered payroll was 77 percent.

The schedule of funding progress, presented as required supplemental information (RSI) following the notes to the fmancial statements, presents multiyear trend information about whether the actuarial value of plan assets is increasing or decreasing over time relative to the actuarial accrued liability for benefits.

Page 1

Employer # 06601 GASB 50 RSI Information for Employers

Village of Bannockburn EMPLOYER NUMBER: 06601R

REQUIRED SUPPLEMENTARY INFORMATION Schedule of Funding Progress

Actuarial Accrued UAAL as a Actuarial Liability Unfunded Percentage

Actuarial Value of (AAL) AAL Funded Covered of Covered Valuation Assets -Entry Age (UAAL) Ratio Payroll Payroll

Date (a) (b) (b-a) (a/b) (c) «b-a)/c) 12/31 /13 2,257,147 3,112,290 855,143 72.52 1,110,892 12 /3 1 /12 1,394,862 2,798,819 1,403,957 49.84 1,030,092 12/31 / 11 593,049 2,411,335 1,818,286 24.59 943,856

On a market value basis, the actuarial value of assets as of December 31, 2013 is $2,683,565. On a market basis, the funded ratio would be 86.22%.

The actuarial value of assets and accrued liability cover active and inactive members who have service credit with Village of Bannockburn. They do not include amounts for retirees . The actuarial accrued liability for retirees is 100% funded .

Page 2

76 . 98% 136.29% 192.64%

fund

general

roads

roads

roads

roads

roads

roads

roads

village hall

village hall

village hall

village hall

village hall

open space

open space

open space

open space

storm

storm

storm

storm

water

general

general

general

san sewer

san sewer

I~wer

san sewer

san sewer

san sewer

general

geReFal 201(

geReFal 30k

geReFal 3.750

tally/net

amount action

($200,000) imrf supplemental funding

($10,000) increase state income fy 15

$38,275 decrease income 25% more fy 16/ out yrs

($50,000) row plantings

$5,000 row plantings

($40,000) row removals

$20,000 row removals

($50,000) defer entry signage program

($40,000) rt 22 tree bush replantings

$24,500 rt 22 tree bush replantings

($25,000) tree replantings

($15,000) master la plan

($2,000) reduce irrigation

($20,000) tree removals

$10,000 tree removals

($20,000) tree removals

$10,000 tree removals

($25,000) tree replantings

($2,000) reduce irrigation

($35,000) 319 maintenance

$20,000 319 maintenance

($15,000) rain garden transplant/new plant pgm

$5,000 rain garden transplant/new plant pgm

($10,000) cross connection pgm

$25,000 dceo grant fy 15 not qualify

$75,000 dceo grant fy 17 moved to ss

($30,000) vh xpansion design fy 15/16

($25,000) dceo grant fy 15

($75,000) grant fy 16 - change fund and timing

2,500 dceo grant aPR related svcs fy 15

($30,000) Tele liftstn repair

($35,000) Tele liftstn assessment

$150,000 Te le liftstn rebuild

($24,500) fee in lieu of McDonalds

($393,225)

iR€F sales talE 1/2% (HR fFam 1/2% ta 1.0%)

Aatel tall Fate fram 5.0 % ta 6.5% law est

iR€F f3ermit fees 10% tAis is Ret ta VOB

pruposea auaget cnangea tv Ib/17

fund

geRefaI

general

roads

roads

village hall

police

police

open space

open space

village hall

tally/net

amOi action

(!>l80,000) '1/101 e)(f3aAsiaR project replaced

($250,000) imrf supplemental funding

($25,000) rt 22 tree bush replantings

$5,000 rt 22 tree bush replantings

($15,000) opacity/buffer replantings

($38,000) if set bi-annual squad replacement pgm - net

$11,500 net impact to repairs

($25,000) buffer / opacity replantings

($2,000) reduce irrigation watering

($2,000) reduce irrigation watering

($620,500)

more long term considerations in future fiscal years

open space

village hall

open space

village hall

roads row

rt 22

storm ditch

police

liability insc

general

general

storm

general

general

general

tally/net

($2,000) reduce irrigation watering

($2,000) reduce irrigation watering

($7,875) decr lawn maint frequency from weekly to alt weeks

($7,175) decr lawn maint frequency from weekly to alt weeks

($3,255) decr lawn maint frequency from weekly to alt weeks

($5,250) decr lawn maint frequency from weekly to alt weeks

($875) decr lawn maint frequency from weekly to alt weeks

($15,000) squad replacements to bi-annual program annual avg

($5,000) explore deductible change

($250,000) imrf supplemental funding

($5,000) garden club

($2,500) rain garden participation program 1 per year

($250,000) incr sales tax 1/2% (HR from 1/2% to 1.0%)

($30,000) hotel tax rate from 5.0 % to 6.5% low estimate

increase permit fees 10% - this is net to VOB

($585,930)

select fiscal years only

path fy 16/17 ($50,000) defer Wilmot path design

path fy 17/18 ($280,000) defer Wilmot path

village or tsannoCKDurn - Lapltal & uperatlonal KanKmgs !)ummary FY 2U15/2016 Revised 2015·03-05

5 = Most important 3 = Good thing to have in the budget 1= Do not need to spend these funds

Average Budgeted Dollars by Fiscal Ranked $$ Shaded = Total Changed

Capital FY 14/15 FY 15/16 FY 16/17 notes • - overall increase from original -5 5 4 4 5 4 General 4.50 $40,000 $40,000 Financial software

3 5 3 3 4 5 4 General 3.86 $5,000 $39,000 $280,000 ext lites & design $325,000 V/H expand, roof, $10k li tes, amenities

4 5 3 3 4 3 41General 3.71 $17,500 $17,500 Network server, expand capacity

3 3 1 1 5 5 Path 3.00 $50,000 $50,000 Wilmot design engineering

3 3 1 1 5 51 Path 3.00 »» push out $280,000 Wilmot construction

4 5 3 3 3 3 41 Police 3.57 $37,500 $37,500 Police SUV

4 5 5 5 5 5 5 Roads 4.86 $3,500 $141,500 $145,000 Bridle restoration

4 5 5 5 5 5 5 Roads 4.86 $35,000 $35,000 Dunsinane const ba lance

4 5 5 5 5 5 5 Roads 4.86 $5,000 $195,000 $200,000 Lakewood restoration

4 5 5 5 5 5 5 Roads 4.86 $10,000 $40,000 $50,000 North Ave design engineering

4 5 5 5 5 5 5 1Roads 4.86 $300,000 $300,000 North Ave Village share

$23,500 $545,500 $630,000 Net ($281,000) $1 480 000

Operational items Shaded = Total Changed

3 5 5 5 4 5 5 Genera l 4.57 $10,000 $10,000 Update building code - with Lake Forest

3 5 3 3 3 5 5 Genera l 3.86 $13,500 BD at $12,000 I $25,00~l Bannockburn Day; add Special Events

3 5 3 3 3 5 5 General 3.86 $25,000 donations $30,000 Continue BBCl, $5,000 budget increase

3 3 5 5 4 5 2 General 3.86 $200,000 reduced $250,000 IMRF supplementa l funding

4 3 1 1 4 5 2 General 2.86 $0 omitted $10,000 Cont inue tri-annual deer program

3 5 1 3 3 3 11General 2.71 $0 omitted I $2,500 Village Hall - kitchen f loor and amenities

3 5 4 5 4 5 5 Open Space 4.43 $25,000 $25,000 Continue tree replantings

4 5 3 3 5 5 5 Open Space 4.29 $500 $500 Prai rie burn

3 5 5 5 4 5 3 Open Space 4.29 $20,000 reduced $2~Conti nue tree removals

3 5 3 3 4 5 5 Open Space 4.00 $25,000 $25,000 Opacity/buffer replant ings

3 5 1 1 3 5 4 Open Space 3.14 $6,500 double only L ~Doub le path screening mat eri al/labor

4 5 5 5 5 5 51Police 4.86 $2,500 $2,500 Cont inue rad io replacement program

4 5 5 5 5 5 5 Po lice 4.79 $1,200 $1,200 Continue armor vest program

3 5 2 3 4 5 5 Po lice 3.86 $7,500 . $ cross FY ~ Continue canine grant program

2 5 3 3 3 5 51Police 3.71 $3,000 $3,000 Community Safety Day - fo rmal budget

3 5 5 5 4 5 4 Roads 4.43 $50,000 $50,000 Continue ROW tree rep lantings

3 5 5 5 4 5 3 Roads 4.29 $40,000 reduced $50,000 Continue ROW tree removals

3 5 3 3 3 31Roads 3.33 $40,000 $25,000 • 2-year spread $50,000 Rt 22 tree/bush replacements

3 5 5 5 5 5 3 Sanitary Sewer 4.43 $30,000 $30,000 Tele liftstation repairs/televising

3 5 3 5 4 5 31Sanitary Sewer 4.00 $35,000 $35,000 Tele Iftstn - infiltration assessment

4 5 3 3 5 5 5 Storm Sewer 4.29 $35,000 $35,000 319 maintenance LakeSide/Waukegan

3 5 3 3 4 5 51storm Sewer 4.00 $15,000 $15,000 Transplant ing & new planting program . 5 5 3 5 5 5 Vi llage Hall 4.57 $40/000 $9,000 VH ext $49,2Q9j interior lighting - $45,000 grant offset ~

3 5 3 3 5 3 5 Vi llage Ha ll 3.86 $2,000 $2,000 Prairie burn

3 5 3 3 4 3 5 Village Hall 3.71 $15,000 reduced ! $25,000 Opacity/buffer replantings

3 5 3 3 3 5 4 Village Hall 3.71 $25,000 $25,000 Continue tree replant ings

3 5 3 3 3 5 3 Village Hall 3.57 $20,000 reduced $25,000 Continue t ree removals

2 5 3 3 4 3 4 Village Hall 3.43 $15,000 $15,000 Master landscape and rep lanting design

3 3 3 3 3 5 21village Hall 3.14 $0 omitted , $10,000 Furnace, 2 a/c, and refrigerator

3 5 5 3 5 5 5 Water 4.43 $20,000 $20,000 Leak detection - eng & consultant

3 5 5 3 3 5 5 Water 4.14 $10,000 $10,000 $20,000 Cross connection program

3 5 3 3 3 5 51water 3.86 $18,750 $18,750 Sandblast and repaint hydrants

$0 $710,450 $75,000 Net ($115,000) $900,450

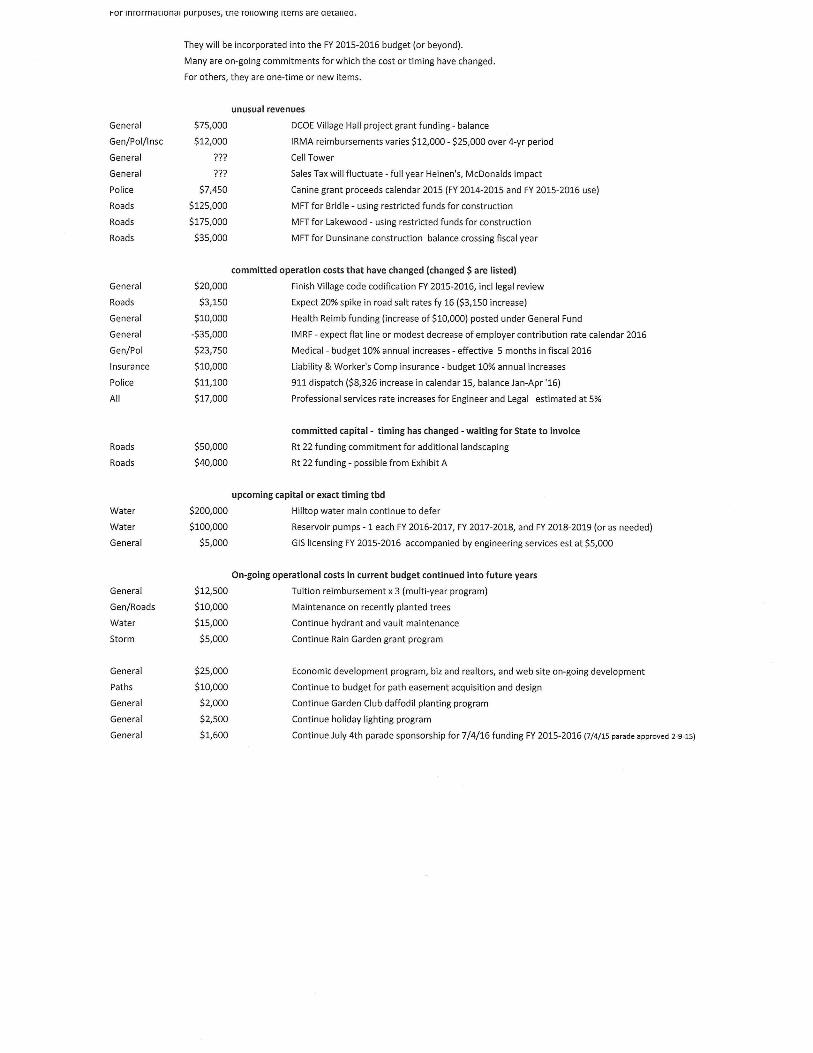

~or InTOrmanOnal purposes, me TOIIOWlng I(ems are ae(allea.

General

Gen/Pol/lnsc

General

General

Police

Roads

Roads

Roads

General

Roads

General

General

Gen/Pol

Insurance

Police

All

Roads

Roads

Water

Water

General

General

Gen/Roads

Water

Storm

General

Paths

General

General

General

They will be incorporated into the FY 2015-2016 budget (or beyond).

Many are on-going commitments for which the cost or timing have changed.

For others, they are one-time or new items.

$75,000

$12,000

???

???

$7,450

$125,000

$175,000

$35,000

unusual revenues

DCOE Village Hall project grant funding - balance

IRMA reimbursements varies $12,000 - $25,000 over 4-yr period

Cell Tower

Sales Tax will fluctuate - full year Heinen's, McDonalds impact

Canine grant proceeds calendar 2015 (FY 2014-2015 and FY 2015-2016 use)

MFT for Bridle - using restricted funds for construction

MFT for Lakewood - using restricted funds for construction

MFT for Dunsinane construction balance crossing fiscal year

committed operation costs that have changed (changed $ are listed)

$20,000 Finish Village code codification FY 2015-2016, incllegal review

$3,150 Expect 20% spike in road salt rates fy 16 ($3,150 increase)

$10,000 Health Reimb funding (increase of $10,000) posted under General Fund

-$35,000 IMRF - expect flat line or modest decrease of employer contribution rate calendar 2016

$23,750

$10,000

$11,100

$17,000

$50,000

$40,000

Medical - budget 10% annual increases - effective 5 months in fiscal 2016

Liability & Worker's Comp insurance - budget 10% annual increases

911 dispatch ($8,326 increase in calendar 15, balance Jan-Apr '16)

Professional services rate increases for Engineer and Legal estimated at 5%

committed capital - timing has changed - waiting for State to invoice

Rt 22 funding commitment for additional landscaping

Rt 22 funding - possible from Exhibit A

upcoming capital or exact timing tbd

$200,000 Hilltop water main continue to defer

$100,000 Reservoir pumps -1 each FY 2016-2017, FY 2017-2018, and FY 2018-2019 (or as needed)

$5,000 GIS licensing FY 2015-2016 accompanied by engineering services est at $5,000

On-going operational costs in current budget continued into future years

$12,500 Tuition reimbursement x 3 (multi-year program)

$10,000

$15,000

$5,000

$25,000

$10,000

$2,000

$2,500

$1,600

Maintenance on recently planted trees

Continue hydrant and vault maintenance

Continue Rain Garden grant program

Economic development program, biz and realtors, and web site on-going development

Continue to budget for path easement acquisition and design

Continue Garden Club daffodil planting program

Continue holiday lighting program

Continue July 4th parade sponsorship for 7/4/16 funding FY 2015-2016 (7/4/15 parade approved 2-9-15)

~LLAGEOFBANNOCKBURN

AN ORDINANCE ESTABLISHING FUND BALANCE POLICY AND DEFINITIONS

ORDINANCE NO.2011-18

WHEREAS, the Board of Trustees of the Village of Bannockbum approved a General Fund Minimum Reserve Policy ("Policy") September 8, 1997 to insure that the Village maintains adequate cash reserve levels necessary to fund the Village's normal recurring obligations while providing sufficient reserve funds for any unexpected expense(s) or loss in revenue(s) (emergency); and

WHEREAS, while the Policy provided that the "reserve balance shall be equal to 100% of the projected and actual total annual revenues (excluding Enterprise Fund revenues)", this calculated requisite amount could readily exceed two fiscal years of operational costs and unintentionally hamper efficient operations; and

WHEREAS, the practice has been to benchmark the required reserve at the current years operating budget total, with the intent to allow sufficient time and funding for the Village Board to evaluate and implement modifying actions to maintain a sufficient reserve threshold; and

WHEREAS, the implementation of Government Standards Accounting Board Statement 54 ("GASB 54") v.rill utilize fund balance classifications for govenunental funds to establish a hierarchy for use of funds as presented in Exhibit A; and

WHEREAS, GASB 54 requires that the governing board establish a Reserve Policy; and

WHEREAS, the Village's historical practice has been to maintain 12-months of budgeted operational expenditures as a reserve regardless of fund classification, it is recognized that the GASB 54 Reserve Policy excludes Proprietary Funds (Water and Sanitary Sewer) and a Reserve Policy is only applicable for Governmental Ftmds; and

WHEREAS, maintaining a formal 12-month reserve may challenge future Board actions, it is deemed prudent to continue the Village's long-standing practice and maintain a 12-month reserve, with that reserve clearly based upon the preceding fiscal year's cash-basis activity; and

WHEREAS, a reduced formal reserve threshold v.rill continue to adequately serve the residents of the Village of Bannockburn and will provide desired flexibility for future Village Boards; and

WHEREAS, GASB 54 requires that the governmg board establish the person(s) authorized to make fund balance assignments.

NOW THEREFORE IT IS HEREBY ORDAINED by the President and Board of Trustees of the Village of Bannockburn County of Lake, State of Illinois, as follows:

SECTION ONE: Recitals. The foregoing recitals are incorporated into and made a part of this Ordinance by this reference.

SECTION TWO: Fund Balance Definitions. The Fund Balance Definitions as depicted in Exhibit A are hereby established for the Village of Bannock bum.

SECTION THREE: General Fund Reserve Policy. The General Fund Reserve goal will continue to be 12-months of operational expenditures from all funds, with the formal Reserve Policy being calculated from the 12-months total of Governmental Funds actual cashbasis operational costs from the immediately preceding fiscal year.

SECTION FOUR: Order of Resource Use. The Village of Bannockbum will spend the most restricted dollars before less restricted, in the following order:

1. Nonspendable (if the funds become spendable) 2. Restricted 3. Committed 4. Assigned 5. Unassigned

SECTION FIVE: Fund Balance Designations. The Village Board of Trustees hereby appoints the Village Finance Director with the authority to make fund balance determinations.

SECTION SIX: Effective Date. This ordinance shall be in full force and effect upon its passage and approval in the manner provided by law.

PASSED THIS d5 DAY OF ~,-:-\ ,2011.

Q . \ / N · d 1 . ' D,-\\r-, ~~-\"'- \. V'c;) AYES: '2:;\'/.- (IJ-,,\\~ \~~ , W{€-'(" \ I 0( ~ \ \ . ->

NAYS: No'~

ABSENT: N.O't'lll..

APPROVED THIS ';;:25 DAY OF Ap-;\\ 2011.

ATTEST:

Village Clerk Procedure stmllreserve\gasb54 & lb ord

EXHIBIT A (examples follow in parentheses)

Fund Balance - the difference between assets and liabilities in a Governmental Fund

N onspendable Fund Balance - the portion of a Governmental Funds net assets that are not available to be spent, either short term or long term, in either form or through legal restrictions. (inventory, prepaid items, long term receivables, endowment principal)

Restricted Fund Balance - the portion of a Governmental Fund's net assets that are subject to external enforceable legal restrictions (unspent bond proceeds, grants earned but not spent, debt covenants, taxes dedicated to a specific purpose, restricted by state statute, revenues restricted by enabling legislation)

Committed Fund Balance - the portion of a Governmental Fund's net assets with self-imposed constraints or limitations that have been placed at the highest level of decision making (governing board determined specific set aside, tax levy for specific purpose via ordinance or resolution)

Assigned Fund Balance - the portion of a Govemmental Fund's net assets to denote an intended use of resources (appropriated fund balance for subsequent year expenditures, positive residual balances in governmental funds other than general fund, delegated authority to assign)

Unassigned Fund Balance - available expendable financial resources in a governmental fund that are not the object of tentative management plan (residual fund balance in general fund)