€¦ · in-depth report aug 29, 2013. ica gruppen . food, glorious food • leading food retailer...

TRANSCRIPT

FOOD RETAIL, SWEDEN

ICA Gruppen

Initiating coverage

In-depth report Aug 29, 2013

Food, glorious food Swedish market leader with strong real estate backing

Solid earnings growth potential coupled with dividend power

Still mispriced, initiating at BUY with a SEK 235 target price

Contents Investment case summary ......................................................................... 4

Valuation and recommendation ................................................................. 6

How Hakon Invest became ICA Gruppen ................................................ 11

Financial forecasts ................................................................................... 13

Company description of ICA Gruppen ..................................................... 26

Nordic and Baltic food retail market dynamics ......................................... 33

Appendix ................................................................................................. 37

Disclosures .............................................................................................. 48

Erik Sandstedt, CFA 0046 (0)8 701 3128

3 August 29, 2013

FOOD RETAIL, SWEDEN Initiating coverage

In-depth report Aug 29, 2013

ICA Gruppen Food, glorious food • Leading food retailer with strong real estate backing

• Solid earnings growth potential coupled with dividend power

• Still mispriced, initiating at BUY with a SEK 235 target price

We see solid earnings growth, deleveraging and good dividends We see a bright future for food retailer ICA Gruppen, whose name was changed from Hakon Invest to reflect a new focus after the acquisition of 60% of the ICA shares from Ahold which gave the group full ownership. We model a solid EBIT CAGR of 9% during 2013-15 accompanied by a further boost to PTP growth thanks to gradually declining financial expenses. While we expect significant deleveraging ahead, we still see a 4% average dividend yield – with capacity to distribute much more.

Valuation multiples a lot lower than they appear The current headline valuation multiples look expensive, but looks can be deceiving. We believe the multiples fail to factor in the real estate portfolio (42% of market cap) and are also heavily inflated by the Norwegian losses. Looking behind these factors, suggests investors can still buy discounted assets: 2014e EV/EBIT of 13.9x drops to 11.7x excl. Norway and 11.9x excl. real estate. We believe ICA Gruppen deserves a premium valuation based on its rock solid Swedish operations, the significant property backing, growth opportunities in the Baltics, and recovery or exit potential in Norway.

Strong track record with a bright future We value ICA Gruppen at SEK 235 per share, based on our sum-of-the-parts approach and backed by our DCF analysis, indicating 22% potential upside to the current share price. We initiate coverage with a BUY on ICA Gruppen, the second-largest listed retailer in the Nordics, boasting a strong track record and a bright future. Company page on Handelsbanken’s REON

Web address: Link to company website IR web address: Link to IR website Next event: Nov 13, 2013: Q3 report

Source: Handelsbanken Capital Markets

Absolute and relative performance

Source: Reuters

Share price (SEK): 193Mkt cap (EURm): 4,468Mkt cap (SEKm): 38,821No of shares (m): 201.1Est. buybacks next 12m (% of MC): n.mFree float (%): 39Avg daily volume (000'): 199Avg daily value (EURm): 4Bloomberg: ICA SSReuters: ICAA.ST

Balance sheet 2012Net debt (SEKm): 12,988

Main owners Votes (%) Capital (%)ICA-handlarnas Förbund 51 51Industrivärden 10 10

90

110

130

150

170

190

95

125

155

185

A S O N D J F M A M J J A

IndexSEK

ICA Gruppen rel. DJ Stoxx 600

% -1m -3m -12mAbsolute: 7 4 89Absolute EUR: 6 3 79Relative DJStoxx: 6 3 5752w range (SEK): 198 / 99.9

SEKm 2011 2012 2013e 2014e 2015e Sales 2,498 99,535 98,780 100,095 102,063 Sales growth (%) -6.2 >900 -0.76 1.3 2.0 Gross margin (%) 44.0 15.1 14.5 14.8 14.9 EBIT adj 302 3,061 3,119 3,440 3,699 margin (%) 12.1 3.1 3.2 3.4 3.6 EBT 252 10,867 2,240 2,800 3,149 EPS reported (SEK) 0.62 42.2 7.4 10.1 11.4 EPS adj (SEK) 1.84 2.18 7.9 10.1 11.4 Y-o-y growth (%) n.m 19 265 28 12 P/E adj (x) 52.3 54.4 24.3 19.1 17.0 P/BV (x) 1.95 1.16 1.66 1.58 1.49 ROE adj (%) 6.1 3.1 7.1 8.5 9.0 EV/EBIT (x) 32.8 12.3 16.0 14.0 12.7 EV/sales (x) 4.0 0.38 0.50 0.48 0.46 FCFE adj yield (%) 2.6 31.1 -17.9 5.5 5.6 Tot DPS (SEK) 5.9 0 6.5 7.5 8.5 Tot Div yield (%) 6.1 0 3.4 3.9 4.4 Net debt/equity (%) -6.5 59.4 48.3 40.3 33.2

12m target return Target price, inc. div. (SEK): 235 Expected total return (%): 22 Expected total dividend yield (%): 3.4 DCF Value (SEK): 243

4 August 29, 2013

Investment case summary Nordic food retailer ICA Gruppen is poised for continued strong performance based on the cornerstones of Swedish market dominance and strong income from its overlooked real estate portfolio, spiced with the recovery/exit potential in ICA Norway. We forecast a 2013-15 EBIT CAGR of 9% and also see a 16% PTP CAGR, supported by gradually lowered interest rate expenses as the group significantly deleverages. The current, expensive-looking valuation multiples are inflated by the Norwegian losses and overlook the real estate portfolio (42% of market cap), suggesting to us that assets are actually priced at a discount. We initiate coverage with a BUY recommendation and target price of SEK 235 and advise investors to finance their ICA Gruppen position with Axfood (REDUCE) based on relative valuation.

How an investment company became a food retailer On February 11, 2013, Hakon Invest announced an agreement on the acquisition of the remaining 60% of the shares in ICA from Ahold for a cash consideration of SEK 20bn. With the completion of the transaction on March 27, 2013, Hakon Invest held all shares in ICA and changed its name to ICA Gruppen to reflect the new direction of the group. ICA Gruppen will be a retail company with four business areas: Food, Banking, Real Estate and Non-food. As of June 30, 2013, ICA Gruppen was owned 51% by the Association of ICA retailers and 10% by AB Industrivärden.

Figure 1: ICA Gruppen structure

Source: Company data

Sweden and Real Estate: Twin pillars of earnings support A cornerstone of ICA’s sound financial position is continued solid performance in ICA Sweden and ICA Real Estate. With a market share of 37%, twice as high as numbers two and three, ICA is the indisputable market leader in Sweden, and it seems likely to us that the business will continue to generate operating profits of at least SEK 3bn per year in the foreseeable future. At the same time, property holdings makes up 42% of market cap and offers steady cash flow generation, factors that are often overlooked in valuations of the company.

Solid EBIT growth, with PTP boosted further by drop in interest costs We model a 2% sales CAGR during 2013-15 and foresee a 9% EBIT CAGR during the same period, driven by a solid performance in ICA Sweden and somewhat lower losses in Norway. As the group is on track of rapid amortisation of debt, we see financial expenses gradually declining, explaining the strong PTP CAGR of 16% that we expect. In a scenario where Norwegian losses do not fall from the 2013 level (HCMe: SEK -769m), we calculate that the 2013e-15e EBIT CAGR would still translates into a solid 4%.

We expect the group to lower the gearing (net debt/EBITDA) to its 1-1.5x long-term target by 2016 (and below 2x 2014e) while distributing at least a 4% average dividend yield, but with a capacity to distribute much more.

ICA Gruppen owns 100% of ICA

Dominant market position in Sweden, and 42% of market cap in property

9% and 16% EBIT and PTP CAGR (2013-15e)

4.0% average dividend yield

August 29, 2013 5

We only see ICA staying in Norway if losses are gradually reduced, either through collaboration or other measures. If profits deteriorate significantly from here, we believe the group will exit the market. As such, the risk of a continued presence in the market, but with significantly accentuating losses is rather low, in our view. Based on our scenario analysis of ICA Norway, we believe the cash cost to exit Norway is SEK 2.2bn, which is also the negative value we assign to this segment in our SOTP valuation.

Figure 2: Two-year CAGR (2013e-15e)

Source: Handelsbanken Capital Markets and company data 2012 and 2013 are pro forma. 2009-2012 ICA. 2013-15 ICA Gruppen

Figure 3: EBIT delta (2013e-15e)

Source: Handelsbanken Capital Markets and company data

Valuation multiples a lot better than they seem ICA Gruppen is trading at a 2014e EV/EBIT of 13.9x. Considering our view of ICA Norway, we also look at the valuation excluding Norway and find that the 2014e EV/EBIT drops substantially to 11.7x. Further, ICA Gruppen has real estate holdings valued at SEK 16bn, or 43% of the current market cap and 33% of the EV. To gain an understanding of the multiple implied by the current share price for the non-property businesses (i.e. Food and Banking), we deduct the real estate market value and earnings from the current market cap. This would result in the share trading at a 2014e EV/ EBIT of 11.9x, in line with Axfood, and at a discount to other Swedish consumer staples.

Figure 4: EV/EBIT valuation

Source: Handelsbanken Capital Markets

A strong track record and a bright future We value ICA Gruppen at SEK 235 per share, based on our sum-of-the-parts (SOTP) approach and backed by our DCF analysis, indicating 22% potential upside to the current share price. We initiate coverage with a BUY recommendation on ICA Gruppen, the second-largest listed retailer in the Nordics with a strong track record and a bright future.

1%

8%

10%

2%

9%

16%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Sales EBIT (adj.) PTP (adj.)

2009-2012 2013e-2015e

-200-100

0100200300400500600700

15.8

13.914.7

11.912.5

11.710.7

9.5

6.07.08.09.0

10.011.012.013.014.015.016.017.018.0

2013e 2014e

Reported ex Real Estate ex Norway ex Norway & Real Estate

Simply put, ICA Norway will be turned or exited

Multiples inflated by Norway… 2014e EV/EBIT of 13.9x falls to 11.7x when excluding the loss-maker… ...and there is a significant property backing (42% of market cap)

Initiate with BUY

6 August 29, 2013

Valuation and recommendation The share is trading at a 2014e EV/EBIT of 13.9x, but 11.7x excluding Norway, backed by a significant property portfolio valued at SEK 16bn, or 42% of the current market cap. The current share price puts ICA Gruppen’s non-property assets at a 2014e EV/EBIT of 11.9x – highly attractive, in our view, as this includes losses in the Norwegian business. Excluding Real Estate and Norway, the 2014e EV/EBIT drops as low as 9.5x, suggesting assets can still be bought at a discount. We value ICA Gruppen at SEK 235 and recommend buying into the second-largest listed retailer in the Nordics with a strong track record and a bright future.

Current valuation multiples not nearly as high as they look ICA Gruppen is trading at a 2014e EV/EBIT of 13.9x, or a 15-20% premium to Swedish food retailer Axfood and a 10-15% premium to other Swedish consumer staple stocks. Considering our view that Norway will be exited unless losses are significantly reduced, we also look at the valuation excluding Norway and find that the 2014e EV/EBIT drops substantially to 11.7x, or in line with Axfood.

ICA Gruppen has real estate holdings valued at SEK 16bn, or 42% of the current market cap and 33% of the enterprise value (EV). Deducting the real estate market value and earnings from the current market cap, to gain an understanding of what multiple the current share price implies for the non-property business (i.e. food and banking), the share would trade at a 2014e EV/ EBIT of 11.9x, which we find attractive.

Adjusting for Real Estate and Norway, to find the implied multiple of the healthy part of the business – ICA Sweden, Rimi Baltic and the ICA Bank – translates into a 2014e EV/EBIT of 9.5x, which we believe is far too low in light of the stability of the Swedish business and the growth opportunities in Rimi Baltic.

The high P/E ratio (24.3x in 2013e) reflects unusually high interest-rate expenses following the debt that ICA Gruppen took on in conjunction with the buyout of ICA. These costs will decrease as debt is amortised, leaving a 2015e P/E of 17.0x, or 13.9x excluding Norway. Also, the group’s current tax rate is inflated due to tax loss carry-forwards in Norway.

We argue that ICA Gruppen should trade at a premium to peers for the following reasons:

• A superior business model (store owners highly incentivised to perform)

• Best-in-class margins (7% “total” margin in Sweden vs. European peers at 4%)

• Category heavyweight in Sweden (37% market share vs. nearest peer at 15%)

• Backing from property assets (market value of SEK 16bn)

• The recovery potential in Norway (large swing factor on SEK ~700m in losses)

Multiples inflated by Norwegian losses

Significant property backing, or 42% of market cap P/E drops on reduced interest costs

ICA Gruppen deserves a premium

August 29, 2013 7

Table 1: ICA Gruppen valuation summary

Source: Handelsbanken Capital Markets

SOTP: ICA Sweden the heavyweight, ICA Real Estate the overlooked jewel We value ICA Gruppen at SEK 235 per share, offering 22% potential upside to the current share price. Our target price is based on a some-of-the-parts (SOTP) approach; below we elaborate on the constituents.

Table 2: Sum-of-the-parts valuation (SOTP)

Source: Handelsbanken Capital Markets, company data, FactSet

SOTP price target 235DCF value 243Current share price 193

Upside to SOTP target 22%Upside to DCF 26%

Valuation 2013e 2014e 2015eEV/S 0.50 0.48 0.46EV/EBIT 15.8 13.9 12.6P/E 24.3 19.1 17.0Dividend yield 3.4% 3.9% 4.4%

Valuation (excl. Real Estate) 2013e 2014e 2015eEV/S 0.50 0.48 0.46EV/EBIT 14.7 11.9 10.4P/E 31.2 18.0 14.9

Valuation (excl Norway) 2013e 2014e 2015eEV/S 0.60 0.57 0.54EV/EBIT 12.5 11.7 11.1P/E 16.0 14.5 13.9

Valuation (excl. Norway & Real Estate) 2013e 2014e 2015eEV/S 0.41 0.38 0.36EV/EBIT 10.7 9.5 8.8P/E 14.4 11.8 11.1

Holding Value SEKm Per share Methodology

ICA Sweden 100% 42,636 212 14x EBIT (2013e)ICA Norge 100% -2,173 -11 Exit cash costRimi Baltic 100% 4,533 23 0.15x sales (2013e) + real estateICA Bank 100% 1,425 7 1.5x equity (2012)ICA Real Estate 100% 13,281 66 Market valueICA Group function 100% -2,157 -11 6x EBIT (2014e)ICA 57,545 286

Forma 100% -14 0 1x book value Kjell & Co 50% 407 2 1x sales (2012)Cervera 91% 94 0 1x book value inkClub 100% 265 1 0.5x sales (2012)Hemtex 69% 245 1 Market capNon-Food 997 5

Net debt -11,281 -56 2013e

Equity value 47,261 235

2014e EV/EBIT of 13.9x… …11.9x excluding Real Estate… …11.7x excluding Norway… …9.5x “rest of ICA”

Sweden and Real Estate above current market cap No hope value attached to Norway Portfolio companies insignificant

8 August 29, 2013

SOTP constituents • ICA Sweden: We apply a multiple of 14x EBIT to our 2013 forecast, valuing ICA

Sweden at SEK 42.6bn, or SEK 212 per share. This multiple corresponds to what we believe is a well deserved 20% premium to Axfood (11.8x), which is supported by the difference in the quality of business models. ICA Sweden should trade at a high multiple as it enjoys a 37% market share, approximately twice as high as its nearest two peers, Axfood and Coop, with a 4.5% wholesale margin and an approximate 7% store margin – best-in-class in Europe. The five-year EBIT CAGR is an impressive 14% per annum and we forecast a 2012-15e CAGR of 5% per annum.

• ICA Norway: We assign a negative value to ICA Norway of SEK -2.2bn, or SEK -11 per share. After five consecutive years of losses amounting to nearly SEK 4bn (reported) and almost SEK 3bn (adjusted), we struggle to find any value in this business. Our value is based on assumed cash flow burdens from exiting the market, although this excludes SEK 1bn in deferred tax assets that the group could potentially utilise if the market is exited. In a more bullish scenario (although far from our base case), assuming the group can reach a 2% EBIT margin and these profits valued at 8x, would lift our SOTP by SEK 23 per share, or 10%.

• Rimi Baltic: We apply a multiple of 0.15x our 2013 sales forecast, and add the SEK 3bn in real estate holdings, valuing the business at SEK 4.5bn, or SEK 23 per share. The valuation multiples drop quickly in the coming years on the back of strong earnings growth, with the Baltic region a key growth and focus area of ICA Gruppen. We model a three-year EBIT CAGR of 7% per annum in 2012-15e (2007-12 was 21% per annum).

• ICA Bank: We value the bank at 1.5x reported equity (2012), translating into 8.4x our 2013 EBIT forecast. This puts the bank at a value of SEK 1.4bn, or SEK 7 per share

• ICA Real Estate: Following the transaction in which ICA Gruppen bought out Ahold’s ICA stake, the group disclosed a market value on the real estate portfolio of SEK 18.1bn. As this includes around SEK 3bn in the Baltic region, which is not part of ICA Real Estate, we assume a value of SEK 13.3bn, after also deducting SEK 1.8bn of sale and leaseback properties, translating into a yield of 7.4% on cash earnings.

• Non-food portfolio companies: We value Hemtex at the current market capitalisation, or SEK 245m adjusted for the 68.5% ownership. We see limited value in Forma and Cervera; to which we assign book values; or in essence zero value. We are more upbeat about Kjell & Company, which we value at 1x 2013e sales (2012 EBIT margin 7.5%) whereas we value inkClub to 0.5x sales (2012 EBIT margins 7.2%). In total, we value the Non-food companies at SEK 1bn, or SEK 5 per share, comprising only 1.7% of ICA Gruppen’s EV.

Figure 5: SOTP bridge

Source: Handelsbanken Capital Markets

212235

23 7

66 5

11

11

56

0

50

100

150

200

250

300

350

Best-in-class margins

Valued at a loss

Future growth area with real estate support

1.5x book

Significant property holdings

Little value

Sweden and Real Estate key value drivers, with Norway the swing factor

August 29, 2013 9

Table 3: Peer group valuation – European food retailers

Source: Handelsbanken Capital Markets and FactSet

Table 4: Peer group valuation – Swedish consumer staples

Source: Handelsbanken Capital Markets and FactSet

Valuation excluding Norway deflates multiples significantly We argue that ICA Gruppen’s valuation is substantially inflated by large losses in Norway, amounting to more than SEK 500m per year. As we believe that ICA Gruppen will exit or at least significantly restructure the business, unless performance improves, either organically or by the suggested collaboration with Norgesgruppen, we look at the valuation excluding Norway. The 2014e EV/EBIT multiple drops from 13.9x to 11.7x when Norway is excluded (or to 12.2x if estimated cash flow costs for leaving the market are added on net debt).

Figure 6: EV/EBIT valuation, with and without Norway

Source: Handelsbanken Capital Markets

ROE

2013 2014 2013 2014 2013 2014 2013 2014 2013 2014 2013 2013 2014Ahold 0.38 0.39 5.7 5.8 9.1 9.2 14.4 12.6 3.7% 4.1% 13% 4.2% 4.2%Axfood 0.42 0.41 8.2 7.8 12.5 11.8 16.3 15.5 4.4% 4.5% 25% 3.4% 3.4%Carrefour 0.27 0.26 5.5 5.1 9.3 8.6 16.8 14.4 2.7% 3.0% 12% 2.9% 3.1%Casino 0.30 0.29 4.5 4.2 6.4 5.9 13.9 12.6 4.3% 4.6% 8% 4.7% 4.8%Colruyt 0.74 0.69 8.9 8.3 12.1 11.3 17.3 16.3 2.5% 2.7% 19% 6.1% 6.2%Delhaize 0.31 0.28 4.7 4.4 8.6 7.8 11.1 10.6 3.0% 3.3% 8% 3.6% 3.7%Jeronimo 0.84 0.75 12.0 10.6 17.2 14.9 22.9 19.6 2.2% 2.5% 29% 4.9% 5.0%Kesko 0.26 0.26 6.4 6.0 10.7 9.8 15.5 13.4 5.1% 5.5% 7% 2.5% 2.6%Morrison 0.54 0.53 7.6 7.3 11.1 10.8 11.5 11.3 4.4% 4.6% 11% 4.8% 4.9%Sainsbury 0.42 0.40 7.2 6.8 11.8 10.8 12.4 11.7 4.3% 4.5% 10% 3.6% 3.7%Tesco 0.53 0.50 6.9 6.4 10.1 9.3 11.4 10.7 4.0% 4.3% 15% 5.3% 5.4%

Median 0.42 0.40 6.9 6.4 10.7 9.8 14.4 12.6 4.0% 4.3% 12% 4.2% 4.2%Average 0.46 0.43 7.1 6.6 10.8 10.0 14.9 13.5 3.7% 4.0% 14% 4.2% 4.3%

ICA Gruppen 0.50 0.48 10.2 9.2 15.8 13.9 24.3 19.1 3.4% 3.9% 7.1% 3.2% 3.4%Premium/discount to median 19% 19% 47% 42% 48% 42% 69% 51% -0.7% -0.4% -4.8% -1.0% -0.8%

EV/SALES EV/EBITDA EV/EBIT P/E EBIT marginDiv yld

ROE

2013 2014 2013 2014 2013 2014 2013 2014 2013 2014 2013 2013 2014AAK 1.01 0.91 11.5 9.8 14.9 12.4 19.7 16.7 1.6% 1.8% 17% 6.8% 7.3%Axfood 0.42 0.41 8.2 7.8 12.5 11.8 16.3 15.5 4.4% 4.5% 25% 3.4% 3.4%Cloetta 1.68 1.52 12.6 9.5 18.6 12.2 17.5 13.2 0.0% 0.0% 9% 9.0% 12.5%Oriflame 1.05 1.03 8.5 8.0 10.1 9.7 12.3 11.7 7.8% 7.8% 47% 10.4% 10.6%SCA 1.67 1.59 10.5 8.9 16.2 12.9 18.7 15.3 2.8% 3.0% 10% 10.3% 12.3%Swedish Match 4.42 4.26 14.6 14.0 15.9 15.5 17.4 16.2 3.1% 3.4% 27.7% 27.6%

Median 1.36 1.28 11.0 9.2 15.4 12.3 17.4 15.4 3.0% 3.2% 17% 9.7% 11.5%Average 1.71 1.62 11.0 9.6 14.7 12.4 17.0 14.8 3.3% 3.4% 22% 11.3% 12.3%

ICA Gruppen 0.50 0.48 10.2 9.2 15.8 13.9 24.3 19.1 3.4% 3.9% 7.1% 3.2% 3.4%Premium/discount to median -63% -63% -7% 0% 2% 13% 39% 24% 0.4% 0.7% -10.3% -6.5% -8.1%

EV/SALES EV/EBITDA EV/EBIT P/E EBIT marginDiv yld

15.8

13.913.0

12.212.511.7

6.07.08.09.0

10.011.012.013.014.015.016.017.018.0

2013e 2014e

Reported ex Norway (incl exit cash costs) ex Norway

Losses in Norway inflate multiples

10 August 29, 2013

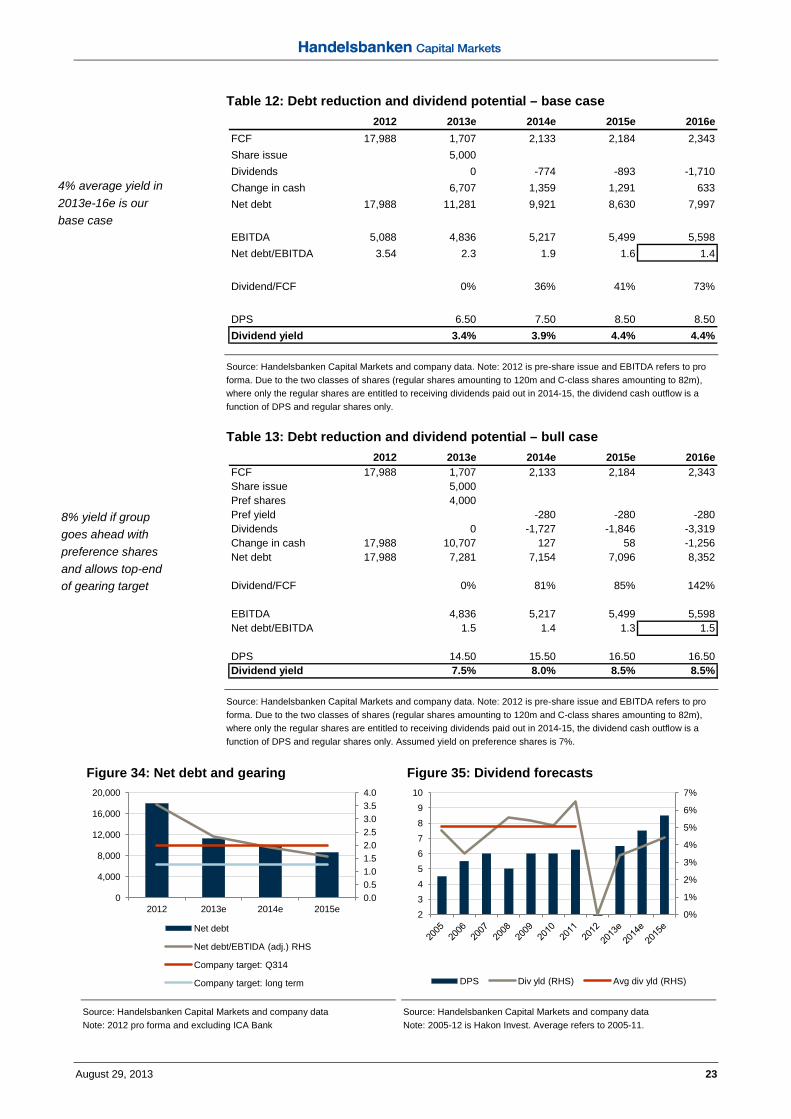

Dividend potential – 4% average yield with upside potential Following the acquisition of the remaining shares in ICA, amounting to SEK 20bn, net debt was at SEK 18bn in Q1 2013, corresponding to net debt/EBITDA of 3.7x on a pro forma basis. After a share issue in May 2013 that raised SEK 5bn and strong cash flow generation (with no dividend paid in 2013 due to the transaction), we expect the group to end 2013 with SEK 11.3bn of net debt, or 2.3x EBITDA, which compares to the group’s target of reaching 2x before Q3 2014. Despite paying out dividends of nearly SEK 1bn per year in the coming two years, we see the gearing reaching around 1.4x in 2016, which is within the company’s long-term target of 1-1.5x that the group expects to reach in 2016.

In terms of the dividend capacity, we model no issuance of preference shares in our base case, which ICA Gruppen has stated could be one option to reduce gearing (it would be treated as equity), and we also assume the group will be within the 1-1.5x target by year-end 2016. In this scenario, the average dividend yield in the period 2013 to 2016 is 4%.

For more information on our dividend scenarios, see page 23-24.

Table 5: Debt reduction and dividend potential – base case

Source: Handelsbanken Capital Markets and company data. Note: 2012 is pre-share issue and EBITDA refers to pro forma. Due to the two classes of shares (regular shares amounting to 120m and C-class shares amounting to 82m), where only the regular shares are entitled to receiving dividends paid out in 2014 and 2015, the dividend cash outflow is a function of DPS and regular shares only.

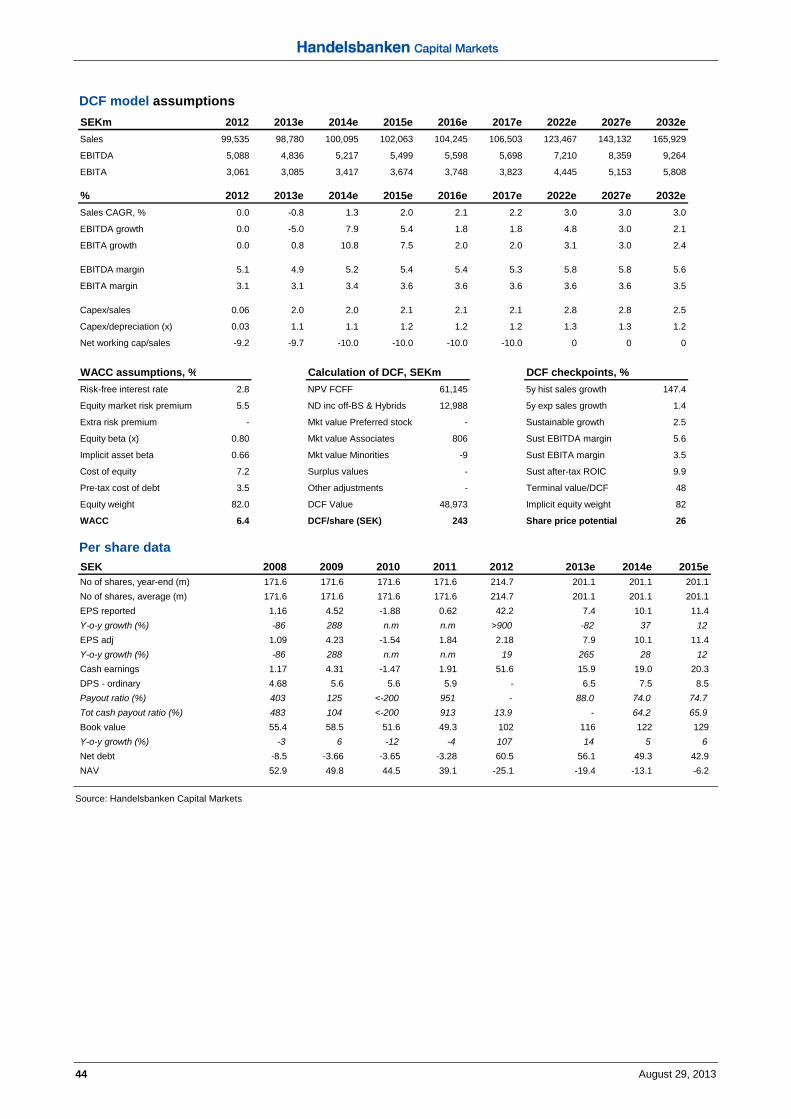

DCF valuation – cash flow nourished by defensive food and real estate Our DCF model values ICA Gruppen at SEK 243 per share, or slightly above our SOTP valuation. ICA’s cash flow has been strong and stable in the past few years, and we expect sustained healthy cash flow underpinned by the stability of food retail and wholesale, backed by the steady earnings stream from the Real Estate business. We foresee operating cash flow of around SEK 4-4.5bn per year, or SEK 2-2.5bn after capex in the coming few years. We assign a beta of 0.8x and a terminal growth rate of 2.5%, which yields a total value of SEK 243 per share, or 24% upside to the current share price. For more details, refer to our DCF on page 45.

Initiating with BUY and target price of SEK 235 We value ICA Gruppen at SEK 235 per share, based on a SOTP approach and backed by our DCF, offering 22% potential upside to the current share price. We initiate coverage with BUY and recommend buying into the second-largest listed retailer in the Nordics with a strong track record and a bright future. We also recommend that investors should finance a position in ICA with Axfood on relative valuation grounds.

2012 2013e 2014e 2015e 2016eFCF 17,988 1,707 2,133 2,184 2,343Share issue 5,000Dividends 0 -774 -893 -1,710Change in cash 6,707 1,359 1,291 633Net debt 17,988 11,281 9,921 8,630 7,997

EBITDA 5,088 4,836 5,217 5,499 5,598Net debt/EBITDA 3.5 2.3 1.9 1.6 1.4

Dividend/FCF 0% 36% 41% 73%

DPS 6.50 7.50 8.50 8.50Dividend yield 3.4% 3.9% 4.4% 4.4%

Significant deleveraging ahead

Dividend base case

4% average yield in 2013-16 is our base-case

Strong cash flow and low WACC underpin DCF DCF of SEK 243

Target price of SEK 235 BUY ICA and finance with Axfood

August 29, 2013 11

How Hakon Invest became ICA Gruppen On February 11, 2013, Hakon Invest announced an agreement on the acquisition of the remaining 60% of the shares in ICA from Ahold for a cash consideration of SEK 20bn. The transaction was completed on March 27, 2013, and, as a result, Hakon Invest holds all shares in ICA and has changed its name to ICA Gruppen to reflect the new direction of the group. As of June 30, 2013, ICA Gruppen was owned 51% by the Association of ICA retailers and 10% by AB Industrivärden.

Background on Hakon Invest’s acquisition of ICA from Ahold On February 11, 2013, Hakon Invest announced an agreement on the acquisition of the remaining 60% of the shares in ICA from Ahold for a cash consideration of SEK 20bn. The transaction was completed on March 27, 2013, and, as a result, Hakon Invest holds all shares in ICA.

The board of Hakon Invest proposed that the AGM on May 20, 2013, resolved to change the company’s name to ICA Gruppen in order to reflect the new direction of the group, having previously been more of an investment company. ICA Gruppen will be a retail company with four business areas: Food, Banking, Real Estate and Non-food. The five portfolio companies that ICA Gruppen owns in addition to ICA constitute less than 5% of the group’s assets and will be evaluated based on the group’s new direction.

The acquisition of the remaining shares in ICA was financed by existing cash and cash equivalents and by secured bridge financing. The share issue of SEK 5bn conducted in May 2013 has replaced part of the bridge financing used for the acquisition. On June 30, 2013, net debt amounted to around SEK 13.2bn.

ICA’s Chief Executive Officer, Per Strömberg, has replaced Claes-Göran Sylvén as Chief Executive Officer of the parent company ICA Gruppen. Claes-Göran Sylvén will remain the President of the Association of ICA retailers (“ICA-handlarnas Förbund”). The members of ICA Gruppen’s new executive management team took their positions on May 20, 2013.

Figure 7: Simplified group structure, before and after transaction

Before transaction After transaction

Source: Handelsbanken Capital Markets and company data

Hakon Invest acquired remaining ICA stake… ...and changed name to ICA Gruppen Financing measures in place

Per Strömberg CEO of ICA Gruppen

ICA Gruppen owns 100% of ICA No longer an investment company

12 August 29, 2013

Figure 8: Transaction financing (SEKbn)

Source: Handelsbanken Capital Markets and company data. *Preference shares issue not yet conducted or decided

Ownership structure post the transaction As of June 30, 2013, ICA Gruppen was owned 51% by the Association of ICA retailers and 10% by AB Industrivärden, with both of the main owners acquiring their respective pro rata allotments in the issue of new shares completed during Q2 2013.

There are two classes of shares: regular shares and C-class shares. They have equal voting rights, but the C shares lack the right to dividends. However, this will change in 2016, as the Association of ICA retailers has exercised an option to convert its C shares to regular shares.

The Association of ICA retailers is a non-profit organisation, comprising all ICA store owners in Sweden, and it does not pay dividends to its members. According to the Association’s charter, it must retain at least 51% of the ownership in ICA Gruppen. While it is possible to change the charter with 75% of the votes, we see it as highly likely that the Association will remain majority owner of ICA Gruppen for the foreseeable future. The arrangement, in essence, restricts ICA Gruppen’s access to a significant amount of new equity, especially for the next few years, as the Association of ICA retailers would have to vote against a share issue were it unable to subscribe for its part (as it would then dilute its ownership to below 50%). We expect this constraint to gradually loosen, as the conversion of C shares in 2016 will increase the dividend received, which we expect the Association to use for building a financial buffer.

Table 6: Shareholder structure

Source: Euroclear. As of June 30, 2013.

Figure 9: Free float

Source: Handelsbanken Capital Markets and SIS

1

20

5

14

0

3

6

9

12

15

18

21

24

Cas

h

Rig

hts

issu

e

Deb

t +

pote

ntia

l pre

f sh

are

Aqu

isiti

on

pric

e

Shareholder Common C Cap %ICA-handlarnas Förbund 21,095,707 82,067,892 51.3%Industrivärden 20,125,000 0 10.0%AMF 3,686,185 0 1.8%Handelsbanken Funds 2,625,895 0 1.3%Lannebo Funds 2,442,638 0 1.2%SEB 1,989,785 0 1.0%Swedbank Robur 1,894,154 0 0.9%JPM Chase 1,865,354 0 0.9%Leif Jönsson 1,254,651 0 0.6%Robur Insurance 1,209,807 0 0.6%Total 119,078,903 82,067,892 100%

ICA-handlarnas

Förbund51.3%

Industrivärden

10.0%

Free float38.7%

Mix of financing

Two asset classes until 2016

Association of ICA retailers the main shareholder

August 29, 2013 13

Financial forecasts The cornerstone of ICA’s sound financial position is continued solid performance in ICA Sweden and ICA Real Estate, while the largest swing factor would be reduced losses in Norway, either through collaboration with Norgesgruppen or an exit of the Norwegian market. Combined, we see these factors making for an impressive 9% EBIT CAGR in 2013-15, and a 16% PTP CAGR as interest expenses are lowered on debt amortisation. We expect the group to extend its track record of sustainably generating significant positive cash flow, and despite our expectation of a reinstated dividend in 2013 and distribution of around a 4% yield, we see the gearing dropping markedly to below 2x EBITDA in 2014. If the group went ahead with its preference share issuance and levered the balance sheet to the high-end of its gearing target, the dividend yield could more than double.

Summary of forecasts We model 2% sales CAGR during 2013-15 and foresee a 9% EBIT CAGR during 2013-15, driven by continued solid performance in ICA Sweden and somewhat reduced losses in Norway. As debt is rapidly amortised, we see financial expenses being gradually lowered, explaining the strong PTP CAGR of 16%. In a scenario where Norwegian losses are not reduced from the 2013e level (HCMe SEK -769m), the 2013e-15e EBIT CAGR still translates into a solid 4% per annum.

We expect the group to lower the gearing (net debt/EBITDA) to within its 1-1.5x medium target by 2016 whilst during this period distributing a 4% average dividend yield, at the current share price. We expect the group to deliver on some, but not all, of its financial medium-term objectives.

Figure 10: Two-year CAGR (2013-15e)

Source: Handelsbanken Capital Markets and company data Note: 2012 and 2013 are pro forma numbers. 2009-12 is ICA. 2013-15 is ICA Gruppen.

Figure 11: EBIT delta (2013e-15e)

Source: Handelsbanken Capital Markets and company data

1%

8%

10%

2%

9%

16%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Sales EBIT (adj.) PTP (adj.)

2009-2012 2013e-2015e

-200-100

0100200300400500600700

Reduced interest expenses explains stronger PTP growth

4.0% average dividend growth

14 August 29, 2013

Table 7: Summary of key financials

Source: Handelsbanken Capital Markets and company data. 2012 and 2013 pro forma numbers. 2008-11 is Hakon Invest. 2012-15 is ICA Gruppen.

ICA Sweden: category heavyweight With a market share of 37%, twice as high as numbers two and three, ICA is the indisputable market leader in Sweden. On the back of its strong position in Sweden, ICA generates predictably stable margins, with an average EBIT margin of 4% in the past five years, never falling being below 3%. It should be noted that ICA’s margin is essentially a wholesale margin and that the store owners on average make another 2-3%, leaving the “total” margin well in line with best-in-class peers in Europe. ICA’s strong position in an attractive, concentrated market translates into what we see as resilient, sustainable earnings capacity. It seems likely to us that ICA Sweden will continue to generate operating profits of at least SEK 3bn per year in the foreseeable future. The ability to generate such positive earnings is a cornerstone of our positive view of the ICA share.

Figure 12: ICA Sweden, sales (SEKbn) and LFL

Source: Handelsbanken Capital Markets and company data LFL refers to stores

Figure 13: ICA Sweden, EBIT (SEKm)

Source: Handelsbanken Capital Markets and company data

2008 2009 2010 2011 2012 2013e 2014e 2015eSales 1,184 2,392 2,663 2,498 99,535 98,780 100,095 102,063Gross profit 423 988 1,201 1,099 15,069 14,309 14,795 15,207EBIT (adj.) 612 423 -387 302 3,061 3,119 3,440 3,699PTP 163 671 -341 252 10,867 2,240 2,800 3,149Net income 187 726 -303 99 9,058 1,486 2,037 2,289EPS adj. 1.09 4.23 -1.54 1.84 2.18 7.94 10.13 11.38DPS 5.00 6.00 6.00 6.25 0.00 6.50 7.50 8.50

Growth -879 -640 -550Sales 10% 102% 11% -6% n.a. -1% 1% 2%EBIT (adj.) n.a. n.a. n.a. n.a. n.a. 2% 10% 8%

Margins 1,717 1,777 1,800Gross margin 35.7% 41.3% 45.1% 44.0% 15.1% 14.5% 14.8% 14.9%EBIT margin 51.7% 17.7% -14.5% 12.1% 3.1% 3.2% 3.4% 3.6%

Balance sheetNet debt/(cash) -1,456 -628 -627 -563 12,988 11,281 9,921 8,630Net debt/EBITDA -2.3 -1.4 1.7 -1.8 2.6 2.3 1.9 1.6

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

40

45

50

55

60

65

70

75

Sales LFL (RHS)

2.5%

2.8%

3.1%

3.4%

3.7%

4.0%

4.3%

4.6%

4.9%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

EBIT Adj. EBIT Adj. EBIT margin (RHS)

EBIT growth on margin improvement EPS boosted further by reduced financial expenses on debt amortisation

Undisputed market leader, with high and stable margins

August 29, 2013 15

Figure 14: ICA Sweden, market share

Source: Handelsbanken Capital Markets and company data

Figure 15: Key peers’ market share, Sweden

Source: SCB/HUI and Magazine Markets, 2011. Other channels include petrol stations, kiosks, mail order, online, outdoor markets and pharmacy

Drivers of continued strong profits in Sweden: • ICA’s market share has been very high and stable, in recent years at around 37%. We

expect the group to sustain its market share, underpinned by superior scale advantage, and even see further scope for ICA to increase its market share in metropolitan areas, where it is somewhat below that of other parts of Sweden

• Management is targeting to increase private label sales (i.e. sales of ICA’s own brands) by around 1 p.p. per year from the current level of 20%. As margins on private labels are approximately twice as high those on external brands, any such increase yields a positive margin impact. We estimate a 3bp positive impact on every percentage point of higher private label sales, suggesting a 20bp boost to margins if ICA reaches a 25% private label share, which we find highly feasible given that key competitor Axfood is already at 25%.

• We foresee further efficiency and leverage potential on continued strong sales, where we note that ICA has a sales density (revenues/sqm) around 50% higher than that of its nearest peers. Revenues per employee have improved by 2% in the past three years and by 11% in the past five years. In addition, ICA has invested considerably in the supply chain in recent years, where we expect efficiency gains to materialise.

• ICA’s small-scale entry into the pharmacy business in 2010 under its Cura brand (52 stores as of March 31, 2013) has burdened profitably since inception, as the operations have been in the investment phase. With the business maturing, we expect the recent trend of reduced operating losses to continue.

Figure 16: Sales density (SEK ‘000/sqm)

Source: Handelsbanken Capital Markets, company data and DLF. *Sales density defined as sales/sqm in SEK (‘000) in the Stockholm region

Figure 17: ICA Sweden, private labels share

Source: Handelsbanken Capital Markets and company data

35%

36%

37%

38%

2006 2007 2008 2009 2010 2011

37%

15% 13%

5% 4%9%

17%

0%5%

10%15%20%25%30%35%40%45%

96

66 6352

0

20

40

60

80

100

120

ICA Coop Axfood Bergendahls

15%17% 17%

16% 17%18% 19% 20%

21%22%

23%

9%11%13%15%17%19%21%23%25%

Scale advantage

Private labels to boost margins Superior sales density + efficient operations

Leverage on pharmacy business

16 August 29, 2013

ICA Norway: problem child with swing factor ICA Norway has been loss-making for the past five years, with an average negative EBIT margin of 4% and accumulated losses of nearly SEK 4bn on a reported basis and SEK 3bn in adjusted terms. While the fact that Norway is one of the most penetrated markets in the world as measured by food retail stores per capita and that ICA’s brand equity is not particularly strong does not help, we believe the two main reasons behind the high losses are rather significant market share losses in the recent decade and high purchasing prices.

Market share losses... Five years ago, ICA had market share in Norway of 19% vs. its 14% today, meaning the group has lost around 1 unit every year, on average. Revenue growth in the past five years has been zero, which compares highly unfavourably to the 30% growth reported in ICA Sweden during the same period. In an industry with razor-thin margins and opex usually growing in line with inflation (rents, wages etc) the group, simply put, has a revenue problem.

...and sourcing problems On top of the unfavourable market share evolution, the group has a COGS problem. ICA’s purchasing prices are approximately 4-5% higher than that of peers on diseconomies of scale, as purchasing prices generally reflect volume size. Very statically and simplistic, ICA Norway would be breakeven at the same purchasing prices as peers.

Similar to ICA Sweden, the group owns significant real estate assets relating to ICA Norway that are held outside of the business unit, in ICA Real Estate, which means that the combined Norwegian operations are not quite as loss-making as the divisional reporting suggests. However, all in all, we view ICA Norway as the main weakness in the group’s business.

Figure 18: ICA Norway, revenue trend, SEKbn

Source: Handelsbanken Capital Markets and company data

Figure 19: ICA Norway, EBIT losses, SEKm

Source: Handelsbanken Capital Markets and company data

Figure 20: ICA Norway, market share trend

Source: Handelsbanken Capital Markets and company data

Figure 21: ICA, private label share markets

Source: Handelsbanken Capital Markets and company data, 2012

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

10

12

14

16

18

20

22

24

Sales LFL (RHS)

-5.0%

-4.5%

-4.0%

-3.5%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-1,400

-1,200

-1,000

-800

-600

-400

-200

0

EBIT Adj. EBIT Adj. EBIT margin (RHS)

19.0%

17.5%

16.5%15.7%

14.8%14.1%

10%

11%

12%

13%

14%

15%

16%

17%

18%

19%

20%

2006 2007 2008 2009 2010 2011

20%

13%

10%

0%

5%

10%

15%

20%

25%

Sweden Baltic Norway

ICA Norway has been loss-making for the past five years

5% market share loss last five years

Sourcing costs 4-5% higher than peers

Significant real estate backing

August 29, 2013 17

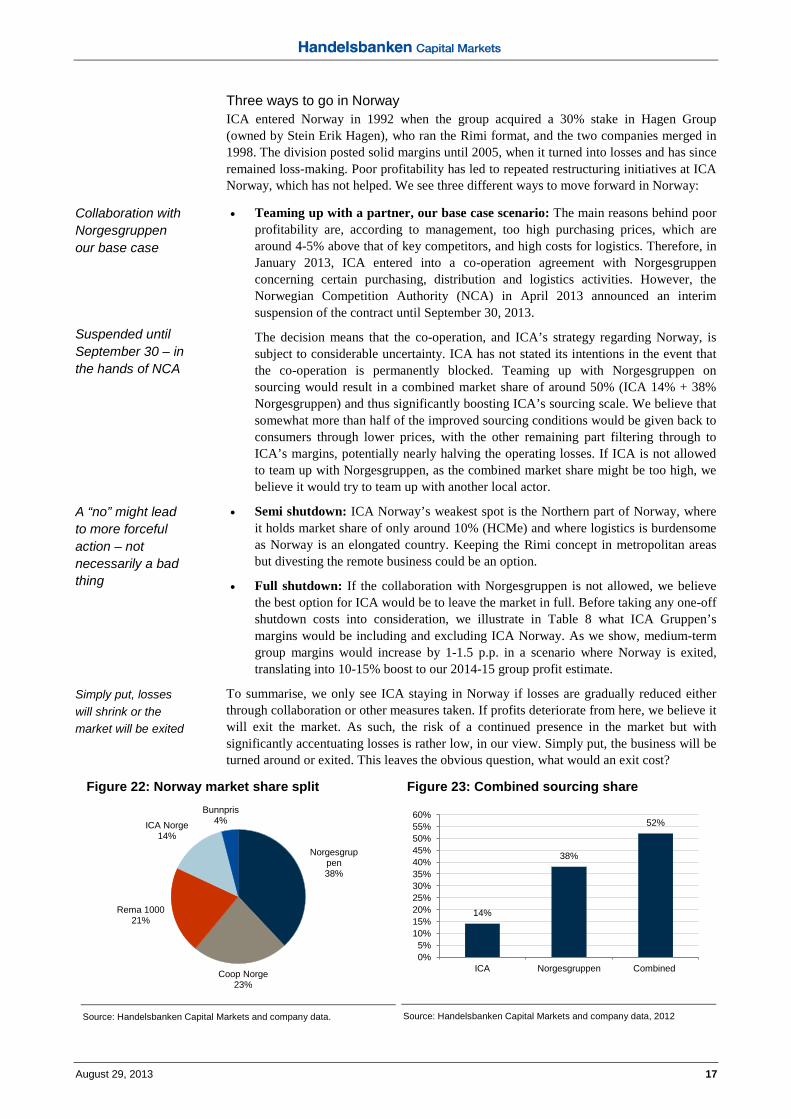

Three ways to go in Norway ICA entered Norway in 1992 when the group acquired a 30% stake in Hagen Group (owned by Stein Erik Hagen), who ran the Rimi format, and the two companies merged in 1998. The division posted solid margins until 2005, when it turned into losses and has since remained loss-making. Poor profitability has led to repeated restructuring initiatives at ICA Norway, which has not helped. We see three different ways to move forward in Norway:

• Teaming up with a partner, our base case scenario: The main reasons behind poor profitability are, according to management, too high purchasing prices, which are around 4-5% above that of key competitors, and high costs for logistics. Therefore, in January 2013, ICA entered into a co-operation agreement with Norgesgruppen concerning certain purchasing, distribution and logistics activities. However, the Norwegian Competition Authority (NCA) in April 2013 announced an interim suspension of the contract until September 30, 2013.

The decision means that the co-operation, and ICA’s strategy regarding Norway, is subject to considerable uncertainty. ICA has not stated its intentions in the event that the co-operation is permanently blocked. Teaming up with Norgesgruppen on sourcing would result in a combined market share of around 50% (ICA 14% + 38% Norgesgruppen) and thus significantly boosting ICA’s sourcing scale. We believe that somewhat more than half of the improved sourcing conditions would be given back to consumers through lower prices, with the other remaining part filtering through to ICA’s margins, potentially nearly halving the operating losses. If ICA is not allowed to team up with Norgesgruppen, as the combined market share might be too high, we believe it would try to team up with another local actor.

• Semi shutdown: ICA Norway’s weakest spot is the Northern part of Norway, where it holds market share of only around 10% (HCMe) and where logistics is burdensome as Norway is an elongated country. Keeping the Rimi concept in metropolitan areas but divesting the remote business could be an option.

• Full shutdown: If the collaboration with Norgesgruppen is not allowed, we believe the best option for ICA would be to leave the market in full. Before taking any one-off shutdown costs into consideration, we illustrate in Table 8 what ICA Gruppen’s margins would be including and excluding ICA Norway. As we show, medium-term group margins would increase by 1-1.5 p.p. in a scenario where Norway is exited, translating into 10-15% boost to our 2014-15 group profit estimate.

To summarise, we only see ICA staying in Norway if losses are gradually reduced either through collaboration or other measures taken. If profits deteriorate from here, we believe it will exit the market. As such, the risk of a continued presence in the market but with significantly accentuating losses is rather low, in our view. Simply put, the business will be turned around or exited. This leaves the obvious question, what would an exit cost?

Figure 22: Norway market share split

Source: Handelsbanken Capital Markets and company data.

Figure 23: Combined sourcing share

Source: Handelsbanken Capital Markets and company data, 2012

Norgesgruppen38%

Coop Norge23%

Rema 100021%

ICA Norge14%

Bunnpris4%

14%

38%

52%

0%5%

10%15%20%25%30%35%40%45%50%55%60%

ICA Norgesgruppen Combined

Collaboration with Norgesgruppen our base case Suspended until September 30 – in the hands of NCA

A “no” might lead to more forceful action – not necessarily a bad thing

Simply put, losses will shrink or the market will be exited

18 August 29, 2013

Table 8: ICA Gruppen comparison excl. Norway

Source: Handelsbanken Capital Markets and company data. SEKm

Figure 24: ICA Gruppen comparison excl. Norway

Source: Handelsbanken Capital Markets and company data. SEKm

An exit cost scenario on ICA Norway When ICA Norway divested its Maxi concept in 2012, it booked a cost of SEK 367m in Q2 2012. From the 2012 annual report, we conclude that the cash cost was slightly less than 50% of the amount with the remainder being impairment and write-downs.

In general, costs attached for leaving a leased store normally are:

• Payment to landlord for early exit (subject to landlord giving consent in the first place)

• Write-downs of store equipment

• Impairment of goodwill

• Operating loss during time of closure

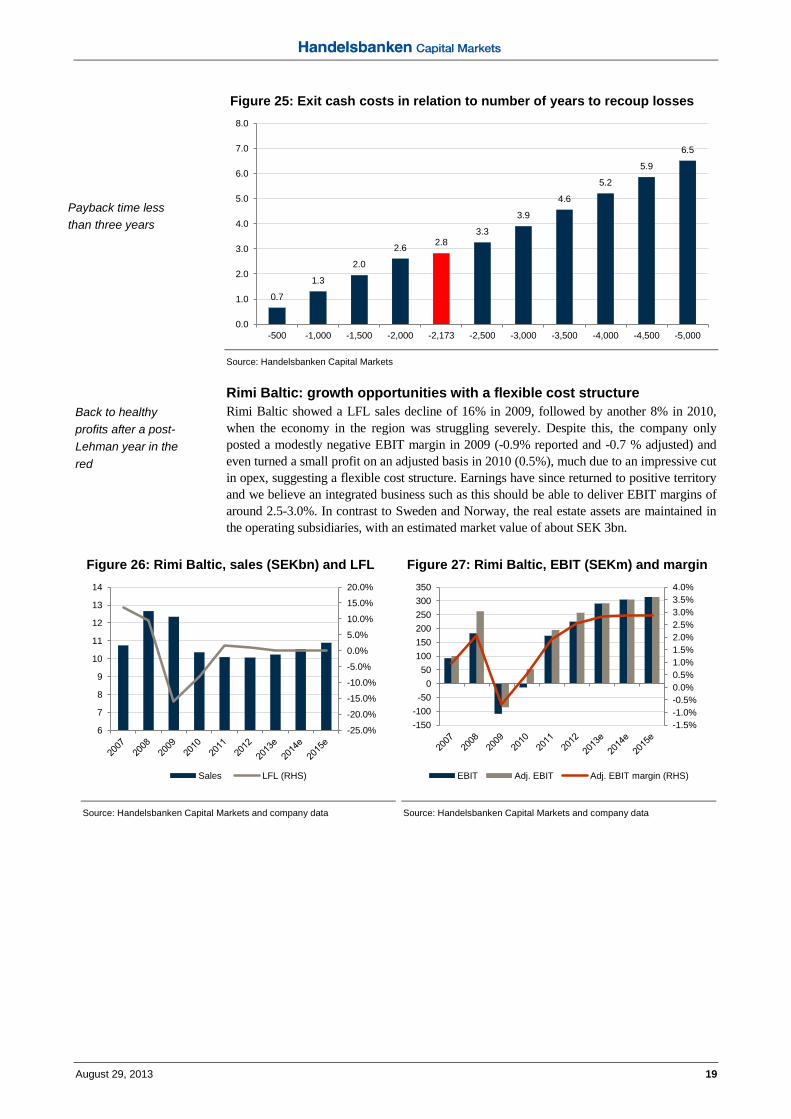

In analysing the costs for exiting the whole of Norway we use the Maxi divestment as a proxy. Maxi comprised 15% of ICA Norway revenues, suggesting the pro-rata cash cost would be nearly SEK 1.2bn to exit the remaining 85%. In addition, one would have to add costs for closing central operations such as distribution centres and severance payments to HQ staff as well as factoring in the fact that the Maxi stores were newer than the other formats, which we estimate to SEK 1bn. We thus assume total cash costs of SEK 2.2bn (stores + central costs) and use this as our negative value of ICA Norway in our SOTP valuation. Considering annual losses of around SEK 600 would suggest a payback time of 2.8x years, which we find attractive.

In a worst case scenario, where we pro-rate the Maxi cash cost on stores (Maxi was 4% of the store base) rather than on sales (15% of sales) would mean a cash cost of SEK 4bn, or SEK 5bn including central operations. We find this scenario too pessimistic as the Maxi stores are significantly larger than the remaining stores, making a pro-rata analysis on the number of stores misleading.

Table 9: Costs to exit Norway (SEKm) – base case

Source: Handelsbanken Capital Markets

Table 10: Costs to exit Norway (SEKm) – worst case

Source: Handelsbanken Capital Markets

2012 2013e 2014e 2015eIncluding NorwaySales 96,862 98,780 100,095 102,063EBIT (adj.) 3,427 3,119 3,440 3,699EBIT margin (adj.) 3.5% 3.2% 3.4% 3.6%

Excluding NorwaySales 77,812 82,373 84,490 86,614EBIT (adj.) 4,021 3,888 4,040 4,149EBIT margin (adj.) 5.2% 4.7% 4.8% 4.8%

DifferenceEBIT margin 1.6% 1.6% 1.3% 1.2%EBIT 17% 25% 17% 12%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Including Norway Excluding Norway

Group EBIT Group EBIT margin (RHS)

Maxi closure Maxi sales % of Norway Rest of Norway P&L cost -367 15% -1,565Cash cost -176 15% -1,173

Maxi closure Maxi stores % of Norway Rest of Norway P&L cost -367 4% -7,528Cash cost -176 4% -4,033

Normal shutdown costs

Using Maxi shut-down as a proxy for the remaining stores

SEK 2bn in cash costs assumed for a Norwegian exit SEK 5bn worse case but unlikely

August 29, 2013 19

Figure 25: Exit cash costs in relation to number of years to recoup losses

Source: Handelsbanken Capital Markets

Rimi Baltic: growth opportunities with a flexible cost structure Rimi Baltic showed a LFL sales decline of 16% in 2009, followed by another 8% in 2010, when the economy in the region was struggling severely. Despite this, the company only posted a modestly negative EBIT margin in 2009 (-0.9% reported and -0.7 % adjusted) and even turned a small profit on an adjusted basis in 2010 (0.5%), much due to an impressive cut in opex, suggesting a flexible cost structure. Earnings have since returned to positive territory and we believe an integrated business such as this should be able to deliver EBIT margins of around 2.5-3.0%. In contrast to Sweden and Norway, the real estate assets are maintained in the operating subsidiaries, with an estimated market value of about SEK 3bn.

Figure 26: Rimi Baltic, sales (SEKbn) and LFL

Source: Handelsbanken Capital Markets and company data

Figure 27: Rimi Baltic, EBIT (SEKm) and margin

Source: Handelsbanken Capital Markets and company data

0.7

1.3

2.0

2.6 2.83.3

3.9

4.6

5.2

5.9

6.5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

-500 -1,000 -1,500 -2,000 -2,173 -2,500 -3,000 -3,500 -4,000 -4,500 -5,000

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

6

7

8

9

10

11

12

13

14

Sales LFL (RHS)

-1.5%-1.0%-0.5%0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%

-150-100-50

050

100150200250300350

EBIT Adj. EBIT Adj. EBIT margin (RHS)

Payback time less than three years

Back to healthy profits after a post-Lehman year in the red

20 August 29, 2013

Figure 28: Rimi Baltic, market share

Source: Handelsbanken Capital Markets and company data

Figure 29: Rimi Baltic, nr of personnel, y-o-y

Source: Handelsbanken Capital Markets and company data

ICA Real Estate: the oft-overlooked jewel EBIT excluding capital gains in ICA Real Estate is around SEK 0.8-1bn on revenues of SEK 1.9-2.3bn (of which around SEK 1bn internal), and has been consistently in this range over the past few years. Considering the underlying stability of the business, we expect the past couple of years to be a good proxy for the coming years, with the exception that the SEK 8.5bn revaluation of the property portfolio that occurred in conjunction with the transactions from Ahold will be depreciated by around SEK 200m per year. This deprecation was booked in group central costs in Q2 2013, but we expect it to be relocated to ICA Real Estate in due course and model this with effect from Q3 2013 (some of it could end up in Rimi Baltic). We also note that the divesture of Norwegian ICA Maxi properties will lower EBIT somewhat. We model EBIT around SEK 800m per year in the coming years. Earnings in ICA Real Estate relate mainly to owned properties, as sub-lease arrangements are principally designed with no margin.

Figure 30: ICA Real Estate, sales and EBIT (SEKm)

Source: Handelsbanken and company data. *Adjusted is clean of capital gain/losses

ICA Bank: a growth segment Despite investments in a broader product offering, profitability continues to be healthy in ICA Banken. In 2012, the RoE was 14.3%, with the key to profitability being wide lending margins due to inexpensive deposit funding. In 2011-12, credit losses were just above 50bp, which is high compared to the larger Swedish banks, but the ratio has come down over time. We model EBIT of around SEK 200m per year in the coming three years, or a margin slightly above 20%.

23.8%

22.1%22.8%

22.4%21.8%

16%

17%

18%

19%

20%

21%

22%

23%

24%

25%

26%

2007 2008 2009 2010 2011

-10%

20%

-20%

-3%

2%4%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2007 2008 2009 2010 2011 2012

0

200

400

600

800

1,000

1,200

1,400

1,600

2007 2008 2009 2010 2011 2012 2013e 2014e 2015e

EBIT Adj. EBIT

Defensive income stream

SEK 800m in annual EBIT seen (includes additional SEK 200m of depreciations from market value revaluation)

~20% margins

August 29, 2013 21

Figure 31: ICA Bank, sales and EBIT (SEKm)

Source: Handelsbanken Capital Markets and company data

Non-food portfolio companies: small in the bigger scheme The performance among the five Non-food portfolio companies in ICA Gruppen varies, but on aggregate the portfolio has been loss-making for the past three years. Ongoing restructuring might yield performance better than that seen recently, but we still factor in cautious assumptions on the back of the weak track record. In total, these companies comprise less than 3% of group sales and value (based on our SOTP).

Table 11: Sales and EBIT, Non-food portfolio companies

Source: Handelsbanken Capital Markets and company data

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0

100

200

300

400

500

600

700

800

900

1,000

2007 2008 2009 2010 2011 2012 2013e 2014e 2015e

Sales EBIT Adj. EBIT Adj. EBIT margin (RHS)

2008 2009 2010 2011 2012 2013e 2014e 2015eFormaSales 880 870 875 847 533 386 366 348Sales growth 11% -1% 1% -3% -37% -28% -5% -5%EBIT 13 -21 15 -12 -124 -50 -50 -50EBIT margin 1% -2% 2% -1% -23% -13% -14% -14%

CerveraSales 341 544 707 722 723 717 717 717Sales growth -10% 60% 30% 2% 0% -1% 0% 0%EBIT -24 -25 -33 -12 -7 -28 -20 -20EBIT margin -7.0% -4.6% -4.7% -1.7% -1.0% -3.9% -2.8% -2.8%

HemtexSales 1391 1295 1081 929 941 948 976 976Sales growth -14% -7% -17% -14% 1% 1% 3% 0%EBIT -33 -221 -233 -116 -46 -24 -12 -10EBIT margin -2.3% -17.0% -21.5% -12.5% -4.9% -2.6% -1.3% -1.0%

inkClubSales 394 452 497 504 529 532 532 532Sales growth 8% 15% 10% 1% 5% 1% 0% 0%EBIT 53 64 39 34 38 26 26 21EBIT margin 13.5% 14.2% 7.8% 6.7% 7.2% 5.0% 5.0% 4.0%

Kjell & CoSales 441 550 644 684 814 909 954 1,002Sales growth 28% 25% 17% 6% 19% 12% 5% 5%EBIT 13 22 23 38 61 59 59 65EBIT margin 2.9% 3.9% 3.6% 5.6% 7.5% 6.5% 6.2% 6.5%

TotalSales 3,447 3,711 3,804 3,686 3,540 3,492 3,546 3,576Sales growth -1% 8% 2% -3% -4% -1% 2% 1%EBIT 22 -181 -189 -68 -78 -17 3 6EBIT margin 1% -5% -5% -2% -2% 0% 0% 0%

Small but solid profit

Less than 3% of group sales

Forma: changing industry dynamics Cervera: highly competitive market Hemtex: losses being reduced after a few tough years inklClub: online retailer with good margins but slowing sales growth Kjell & Co: portfolio star!

22 August 29, 2013

Cash flow and balance sheet: reduced gearing whilst healthy dividends ICA’s cash flow generation has been very stable in the past few years, underpinned by its solid Swedish operations, as well as by the healthy and low-volatility cash flow from the Real Estate business. Despite the Norwegian problems, cash flow from operations grew by 4% per annum in 2007-12 and we expect the group to sustainably generate significant positive cash flow.

Figure 32: Cash flow from operations

Source: Handelsbanken Capital Markets and company data Note: 2005-12 is ICA, 2013e-15e is ICA Gruppen

Figure 33: Free cash flow

Source: Handelsbanken Capital Markets and company data Note: 2005-12 is ICA, 2013e-15e is ICA Gruppen. CFO after capex

Dividend scenarios Following the acquisition of the remaining shares in ICA, amounting to SEK 20bn, net debt was SEK 18bn in Q1 2013, corresponding to net debt/EBITDA of 3.7x on a pro forma basis. After a share issue in May 2013, raising SEK 5bn and strong cash flow generation (with no dividend paid in 2013 due to the transaction), we expect the group to end 2013 with SEK 11.3bn of net debt, or 2.3 EBITDA, which compares to the group’s target of reaching 2x before Q3 2014. Despite paying out dividends of nearly SEK 1bn per year in the coming two years, we see the gearing reaching around 1.4x in 2016, which is within the company’s long-term target of 1-1.5x that the group expects to reach in 2016.

In our base case, we model no issuance of preference shares, which ICA Gruppen has stated could be one option to reduce gearing (as it would be treated as equity), and also assume it will be within the 1-1.5x target by year-end 2016. In this scenario, the average dividend yield in 2013e-16e is 4%.

In a scenario where the group issues SEK 4bn in preference shares (SEK 3-5bn was mentioned in conjunction with the Ahold transaction) and also assuming it will allow the gearing to be in the high end of its 1-1.5x target translates into an average dividend yield of 8% during 2013e-16e. Now, we see it highly unlikely that the group would issue preference shares and allow a top-of-the-range gearing with continued uncertainties as the Norwegian turnaround just to be able to distribute an 8% dividend yield, but it nonetheless highlights the dividend capacity in ICA Gruppen.

0

1,000

2,000

3,000

4,000

5,000

6,000

CFO Average

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

FCF Average

Sustained strong cash flow

Significant deleveraging ahead

Base... ...and bull case

August 29, 2013 23

Table 12: Debt reduction and dividend potential – base case

Source: Handelsbanken Capital Markets and company data. Note: 2012 is pre-share issue and EBITDA refers to pro forma. Due to the two classes of shares (regular shares amounting to 120m and C-class shares amounting to 82m), where only the regular shares are entitled to receiving dividends paid out in 2014-15, the dividend cash outflow is a function of DPS and regular shares only.

Table 13: Debt reduction and dividend potential – bull case

Source: Handelsbanken Capital Markets and company data. Note: 2012 is pre-share issue and EBITDA refers to pro forma. Due to the two classes of shares (regular shares amounting to 120m and C-class shares amounting to 82m), where only the regular shares are entitled to receiving dividends paid out in 2014-15, the dividend cash outflow is a function of DPS and regular shares only. Assumed yield on preference shares is 7%.

Figure 34: Net debt and gearing

Source: Handelsbanken Capital Markets and company data Note: 2012 pro forma and excluding ICA Bank

Figure 35: Dividend forecasts

Source: Handelsbanken Capital Markets and company data Note: 2005-12 is Hakon Invest. Average refers to 2005-11.

2012 2013e 2014e 2015e 2016eFCF 17,988 1,707 2,133 2,184 2,343Share issue 5,000Dividends 0 -774 -893 -1,710Change in cash 6,707 1,359 1,291 633Net debt 17,988 11,281 9,921 8,630 7,997

EBITDA 5,088 4,836 5,217 5,499 5,598Net debt/EBITDA 3.54 2.3 1.9 1.6 1.4

Dividend/FCF 0% 36% 41% 73%

DPS 6.50 7.50 8.50 8.50Dividend yield 3.4% 3.9% 4.4% 4.4%

2012 2013e 2014e 2015e 2016eFCF 17,988 1,707 2,133 2,184 2,343Share issue 5,000Pref shares 4,000Pref yield -280 -280 -280Dividends 0 -1,727 -1,846 -3,319Change in cash 17,988 10,707 127 58 -1,256Net debt 17,988 7,281 7,154 7,096 8,352

Dividend/FCF 0% 81% 85% 142%

EBITDA 4,836 5,217 5,499 5,598Net debt/EBITDA 1.5 1.4 1.3 1.5

DPS 14.50 15.50 16.50 16.50Dividend yield 7.5% 8.0% 8.5% 8.5%

0.00.51.01.52.02.53.03.54.0

0

4,000

8,000

12,000

16,000

20,000

2012 2013e 2014e 2015e

Net debt

Net debt/EBTIDA (adj.) RHS

Company target: Q314

Company target: long term

0%

1%

2%

3%

4%

5%

6%

7%

23456789

10

DPS Div yld (RHS) Avg div yld (RHS)

4% average yield in 2013e-16e is our base case

8% yield if group goes ahead with preference shares and allows top-end of gearing target

24 August 29, 2013

ICA Gruppen’s financial objectives The current financial goals will be reviewed in 2013 by the new board of directors and management, as the underlying conditions for the existing goals have changed due to the transaction. This could require existing financial goals to be replaced with new ones or for figures in the existing goals to be changed. Our understanding is that the focus of the basic strategy will, however, remain the same.

Table 14: Financial objectives vs. HCM expectations

Source: Handelsbanken Capital Markets and company data

Table 15: Forecasts by division, yearly

Source: Handelsbanken Capital Markets and company data. Note: 2008-12 is ICA. 2013-15 is ICA Gruppen. 2013 is pro forma.

Financial objectives 2013e 2014e 2015eOutgrow the market in each market -0.8% 1.3% 2.0%EBIT margin 3.5-4.0% 3.2% 3.4% 3.6%ROE 14-16% over a business cycle 7.1% 8.5% 9.0%Equity ratio 30–35% 33% 33% 34%Dividend payout ratio above 40% 88% 74% 75%Strong and stable dividend yield 3.4% 3.9% 4.4%Net debt of 1.0–1.5x EBITDA long term 2.3 1.9 1.6

Sales 2008 2009 2010 2011 2012 2013e 2014e 2015eICA Sweden 55,969 59,003 60,596 62,500 65,751 67,576 69,265 70,997ICA Norway 20,164 21,666 21,225 20,679 19,050 16,408 15,605 15,449RIMI Baltic 12,661 12,329 10,352 10,089 10,050 10,217 10,542 10,877ICA Bank 582 634 612 764 814 822 880 924ICA Real Estate 1,969 2,095 2,135 2,202 2,252 2,204 2,249 2,294ICA Group functions 1,221 467 452 348 102 91 100 100Intra group sales -1,603 -1,543 -1,512 -1,403 -1,155 -1,124 -1,138 -1,151Non-Food portfolio 2,587 2,592 2,574Total 90,963 94,651 93,860 95,179 96,864 98,780 100,095 102,063

EBIT 2008 2009 2010 2011 2012 2013e 2014e 2015eICA Sweden 1,709 2,320 2,750 2,617 2,869 3,045 3,174 3,275ICA Norway -719 -506 -588 -1,255 -1,020 -962 -600 -450RIMI Baltic 182 -109 -13 173 224 290 304 314ICA Bank 111 132 91 171 181 170 198 208ICA Real Estate 1,134 1,025 917 1,005 1,298 949 779 780ICA Group functions -300 -149 -233 -206 -244 -410 -359 -369Non-Food portfolio -73 -56 -59Total 2,117 2,713 2,924 2,505 3,309 3,008 3,440 3,699

EBIT (adj.) 2008 2009 2010 2011 2012 2013e 2014e 2015eICA Sweden 1,709 2,408 2,750 2,617 2,869 3,045 3,174 3,275ICA Norway -679 -466 -588 -646 -594 -769 -600 -450RIMI Baltic 262 -85 52 194 256 291 304 314ICA Bank 111 132 91 171 181 170 198 208ICA Real Estate 802 882 893 1,005 986 867 779 780ICA Group functions -300 -159 -233 -206 -244 -411 -359 -369Non-Food portfolio 0 -73 -56 -59Total 1,923 2,711 2,960 3,101 3,454 3,119 3,440 3,699

EBIT margin (adj.) 2008 2009 2010 2011 2012 2013e 2014e 2015eICA Sweden 3.1% 4.1% 4.5% 4.2% 4.4% 4.5% 4.6% 4.6%ICA Norway -3.4% -2.2% -2.8% -3.1% -3.1% -4.7% -3.8% -2.9%RIMI Baltic 2.1% -0.7% 0.5% 1.9% 2.5% 2.8% 2.9% 2.9%ICA Bank 19.1% 20.8% 14.9% 22.4% 22.2% 20.7% 22.5% 22.5%ICA Real Estate 40.7% 42.1% 41.8% 45.6% 43.8% 39.3% 34.6% 34.0%Total 2.1% 2.9% 3.2% 3.3% 3.6% 3.2% 3.4% 3.6%

Ticking some but not all boxes

August 29, 2013 25

Table 16: Forecasts by division, quarterly

Source: Handelsbanken Capital Markets and company data. Note: 2008-12 is ICA. 2013-15 is ICA Gruppen. 2013 is pro forma

Q112 Q212 Q312 Q412 Q113 Q213 Q313e Q413e Q114e Q214e Q314e Q414eICA Sweden 15,371 16,698 16,498 17,184 16,043 17,177 16,828 17,528 16,444 17,606 17,249 17,966ICA Norway 5,017 4,957 4,395 4,681 4,138 4,151 3,999 4,119 3,848 3,860 3,859 4,037RIMI Baltic 2,418 2,589 2,418 2,625 2,367 2,581 2,539 2,730 2,485 2,684 2,615 2,757ICA Bank 198 210 199 207 219 203 200 200 220 220 220 220ICA Real Estate 25 26 23 28 30 11 25 25 25 25 25 25ICA Group functions -292 -298 -276 -289 -280 -268 -282 -295 -283 -271 -285 -298Intra group sales 572 577 548 555 561 557 537 549 572 568 548 560Non-Food portfolio 563 613 570 841 561 613 572 846Total 23,309 24,758 23,805 24,990 23,641 25,025 24,417 25,697 23,872 25,306 24,803 26,113

EBIT ICA Sweden 540 673 858 798 629 719 883 814 645 755 923 852ICA Norway -120 -606 -130 -164 -439 -193 -170 -160 -160 -170 -140 -130RIMI Baltic 29 60 36 99 40 72 71 106 44 76 75 109ICA Bank 39 58 58 26 54 32 42 42 50 50 50 50ICA Real Estate -62 -85 -45 -52 -100 -147 -81 -83 -89 -89 -88 -94ICA Group functions 262 532 274 230 313 246 195 195 195 195 195 195Non-Food portfolio -60 -35 -44 66 -58 -30 -39 71Total 690 631 1,051 937 437 694 897 980 627 786 974 1,053

EBIT (adj.)ICA Sweden 540 673 858 798 629 719 883 814 645 755 923 852ICA Norway -120 -180 -130 -164 -246 -193 -170 -160 -160 -170 -140 -130RIMI Baltic 29 60 68 99 40 73 71 106 44 76 75 109ICA Bank 39 58 58 26 54 32 42 42 50 50 50 50ICA Real Estate -62 -85 -45 -52 -100 -148 -81 -83 -89 -89 -88 -94ICA Group functions 257 264 246 219 247 230 195 195 195 195 195 195Non-Food portfolio -60 -35 -44 66 -58 -30 -39 71Total 684 751 1,055 937 564 678 897 980 627 786 974 1,053

EBIT margin (adj.)ICA Sweden 3.5% 4.0% 5.2% 4.6% 3.9% 4.2% 5.3% 4.6% 3.9% 4.3% 5.4% 4.7%ICA Norway -2.4% -3.6% -3.0% -3.5% -5.9% -4.6% -4.3% -3.9% -4.2% -4.4% -3.6% -3.2%RIMI Baltic 1.2% 2.3% 2.8% 3.8% 1.7% 2.8% 2.8% 3.9% 1.8% 2.8% 2.9% 4.0%ICA Bank 19.7% 27.6% 29.1% 12.6% 24.7% 15.8% 21.0% 21.0% 22.5% 22.5% 22.5% 22.5%ICA Real Estate 44.9% 45.8% 44.9% 39.5% 44.0% 41.3% 36.3% 35.4% 34.0% 34.3% 35.6% 34.7%Total 2.9% 3.0% 4.4% 3.7% 2.4% 2.7% 3.7% 3.8% 2.6% 3.1% 3.9% 4.0%

26 August 29, 2013

Company description of ICA Gruppen On March 27, 2013, ICA Gruppen acquired the remaining 60% stake in food retailer ICA from Royal Ahold for SEK 20bn. ICA Gruppen is dominated by ICA, the largest food retailer in Sweden, but it also has substantial operations in Norway and the Baltic countries. The group also includes significant real estate activities, a bank and a portfolio of non-food companies.

ICA Gruppen is primarily active in food retailing in Sweden, Norway and the Baltic countries through its ICA subsidiaries, which also include banking and real estate operations. Besides ICA-related activities, the group also includes holdings in mainly non-food retailers. Our understanding is that each holding will be reviewed, as they must be regarded as core to ICA to remain within the business ahead.

Figure 36: Business areas

Source: Company data

ICA's revenue generation There are four cornerstones that generate ICA’s revenues: the stores (retail), the supply chain (wholesale), real estate development and financial services.

• Supply chain (53.9% of revenue in 2012): ICA buys products and sells them at a mark-up to retailer-owned stores in Sweden and franchised stores in Norway. ICA also sells services to these stores, such as marketing communications, logistics, training and retail technology.

• Stores (42.5% of revenue): ICA generates retail revenue in several ways. In Sweden, it comes from royalties and/or profit distributions from the stores. It also comes from end-customers through Maxi Special, the wholly-owned company that sells houseware and leisure products at Maxi ICA Hypermarkets. In Norway, revenue comes from wholly-owned stores and franchise fees. In the Baltic countries, it comes from wholly-owned stores.

• Properties (2.8% of revenue): It is strategically important for ICA to obtain and develop the right retail locations and shopping centres. It therefore owns many of its retail properties. Tenants can include other retailers too. The operations generate revenue in the form of rent. If the properties have appreciated in value when they are sold, they generate a capital gain (and vice versa).

• Financial services (0.8% of revenue): Offering financial services is one of many ways ICA is trying to build customer loyalty. In Sweden, ICA Bank’s customers can save, borrow and obtain insurance. Net interest income and commissions contribute to earnings, while the use of ICA Bank’s cards reduces fees paid to other card issuers. The bank also offers services such as payment terminals and ATMs to other companies for a fee.

August 29, 2013 27

The group has organised its operations into five business divisions, which we elaborate on in detail below. ICA’s profit generation is mainly concentrated to ICA Sweden and ICA Real Estate, while ICA Norway weighs on group profitability. Rimi Baltic and the ICA Bank contribute small, but positive, earnings.

Figure 37: ICA revenue split by activity

Source: Handelsbanken Capital Markets and company data *Data refers to 2012

Figure 38: ICA revenue split by division

Source: Handelsbanken Capital Markets and company data *Data refers to 2012

Figure 39: ICA EBIT by division

Source: Handelsbanken Capital Markets and company data *EBIT is adjusted for one-offs and refers to 2012

Figure 40: ICA number of employees

Source: Handelsbanken Capital Markets and company data *Excluding franchise and independent stores

Store structure ICA manages its stores in the following way:

• Independent retailers working in cooperation: The retailers own and manage their stores but have central agreements with ICA covering a number of areas. This is called the “ICA idea” and is used only in Sweden. The number of stores using this concept is 1,330.

• Wholly-owned stores: ICA owns and manages the stores as an integrated chain. It is the only store format used in the Baltic countries and is the dominant format in Norway. The number of stores using this format is 577.

• Franchising: These stores are managed by franchisee, used only in Norway. The number of stores using this format is 155.

• Combination: The above models can be combined, depending on the situation. Maxi ICA Hypermarkets in Sweden is a combination solution where retailers manage the food departments while ICA manages non-food goods. 75 stores use this format.

54%

43%

3% 1%0%

10%

20%

30%

40%

50%

60%

Wholesale Retail Real estate Financial services

67%

20%

10%

1% 2%0%

10%

20%

30%

40%

50%

60%

70%

80%

ICA Sweden ICA Norway Rimi Baltic ICA Bank ICA Real Estate

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

ICA Sweden

ICA Real Estate

RIMI Baltic

ICA Bank ICA Group

functions

ICA Norway

76

4,667

8,078 8,199

21,020

0

3,000

6,000

9,000

12,000

15,000

18,000

21,000

24,000

Other Norway Baltics Sweden Total

The “ICA idea” in Sweden only

Baltics and part of Norway

Norway also franchise

28 29 August 2013

ICA Sweden In 2012, ICA Sweden generated revenue of SEK 65.7bn and an operating profit of SEK 2.8bn. For Sweden, revenue mainly relates to ICA’s wholesale activities, which accounted for SEK 52.2bn, but revenue also derives from non-food sales at the 75 ICA Maxi stores, store rentals, royalties (we estimate that around one-third of ICA Sweden’s EBIT stems from royalties) and various services. Consolidated revenue of SEK 65.7bn can be compared to total store sales of SEK 98.8bn (which is the number used in market share analysis, for example).

The ICA idea: unique to Sweden ICA Sweden operates a food retail business in cooperation with independent ICA retailers based on the ICA concept, which is unique to ICA Sweden. Each retailer owns and operates their own store and can therefore meet customers’ needs through locally-adapted concept offerings. ICA originated from this concept, which also involves individual retailers working together in, for example, procurement, logistics and market communications to achieve the same economies of scale as a wholly-owned retail chain. The ICA retailers are able to use ICA’s purchasing organisation to deliver goods to the stores but are not obliged to purchase products through ICA. Today, around 75% of ICA retailers’ purchasing goes through the ICA system, with the balance generally being dairy products, where industry praxis is to buy goods from third-party vendors and locally-produced products.

The percentage of products bought centrally from ICA has proven to be stable over time, as it is normally cheaper and more efficient for the store owners to purchase from ICA. The ICA concept is owned by the Association of ICA retailers, whose main mission is to preserve and develop the ICA concept. The ICA agreement contains a pre-emption clause that applies if the ICA retailer wants to sell its company or operations (the selling price is 1x net income). New stores are normally established by ICA Sweden, which provides financing to the retailers to establish their stores. In this way, the retailer initially only owns a small percentage of the shares (9%) in the company that operates the store, but when enough profit has been accumulated the retailer’s ownership rises to 99% as they control all the shares apart from one “golden share”, which is held centrally at ICA.

In addition to independent stores, about 75 ICA Maxi stores operate in a mixed format, with the ICA retailer responsible for food items and ICA responsible for non-food items.

Table 17: ICA Sweden store format

Source: Handelsbanken Capital Markets and company data. Excludes Cure (52 pharmacy stores) and ICA To Go (four stores). Revenues refer to 2012.

Table 18: ICA Sweden store trends

Source: Handelsbanken Capital Markets and company data. Excludes Cura (the pharmacy stores)

Name Format Nr of stores Sales Store itemsICA Nära Convinience 700 15,041 5,000ICA Supermarket Supermaket 430 30,919 7,000-11,000ICA Kvantum Large supermarket 121 23,577 10,000-30,000ICA Maxi Hypermarket 75 28,735 35,000

2005 2006 2007 2008 2009 2010 2011 2012Maxi ICA Stormarknad 45 52 60 66 69 72 75 75ICA Kvantum 126 122 119 117 118 116 117 121ICA Supermarket 488 477 460 454 444 443 435 430ICA Nära 758 746 743 732 728 716 704 700ICA To Go 2 3 4Sweden total 1,417 1,397 1,382 1,369 1,359 1,349 1,334 1,330

SEK 100bn business when measured on store sales to end-customer

Independent store owners manage the stores but are closely linked to ICA 75% of goods bought from ICA ICA always keeps a “golden” share

Supermarket format the largest

Negative store growth but positive space growth

August 29, 2013 29

Figure 41: ICA Maxi store layout

Source: Company data

ICA Norway ICA entered Norway in 1992, when the group acquired a 30% stake in Hagen Group (owned by Stein Erik Hagen), who ran the Rimi format, and the two companies merged in 1998. The division posted solid margins until 2005, when it turned into losses and has since remained loss-making.

At the end of 2012, ICA had 497 outlets in Norway, down by 53 from the year before, the result of the divestment of ICA Maxi in Norway. The majority of the outlets are wholly-owned (69%) while the remainder (31%) are franchised. Total revenue in 2012 was SEK 19bn and an operating loss of SEK 597m was posted, excluding non-recurring items (SEK 1,023m on a reported basis).

At the start of 2013, ICA operated four formats in Norway, of which one (ICA Naer) will be discontinued during the year.

Poor profitability has led to repeated restructuring initiatives at ICA Norway. The main reasons behind poor profitability are, according to management, too high purchasing prices, which are around 4-5% above that of key competitors, and high costs for logistics. Therefore, in January 2013 ICA entered into a co-operation agreement with Norgesgruppen concerning certain purchasing, distribution and logistics activities. However, the Norwegian Competition Authority (NCA) announced in April 2013 an interim suspension of the contract until September 30, 2013. The decision means that the co-operation—and ICA’s strategy regarding Norway—is subject to considerable uncertainty. ICA has not stated its intentions in the event that the co-operation is permanently blocked. In addition to unfavourable purchasing prices, we note that ICA lacks the scale, market share and strong brand equity that it enjoys in Sweden.

Table 19: ICA Norway store format

Source: Handelsbanken Capital Markets and company data

Name Format Nr of stores Sales Store itemsRimi Discount 315 9,701 3.500-4.000ICA Supermarked Supermarket 78 4,750 12.000-13.000ICA Naer Convenience 68 2,149 10,000-30,000Matkroken Convenience 36 n.a 3.000-5.000

ICA’s hypermarket format

Long history in Norway

Large losses

Teaming up with Norgesgruppen on sourcing? Collaboration currently suspended by NCA

Shifting portfolio towards Rimi and Supermarket

30 29 August 2013

Figure 42: ICA Norway, store count

Source: Handelsbanken Capital Markets and company data

Figure 43: ICA Norway, store structure

Source: Handelsbanken Capital Markets and company data

Figure 44: Rimi store layout

Source: Company data

Rimi Baltic ICA has operated indirectly in the Baltic region since 1996, through its Norwegian business which expanded the Rimi concept into the Baltic region. ICA Baltic was established in 1999 and in 2004, the group agreed with Finnish retailer Kesko on a joint venture in the Baltic region, creating Rimi Baltic. Two years thereafter, ICA acquired Kesko’s interest in Rimi Baltic and consolidated the business.

Rimi Baltic is a wholly-owned subsidiary with 235 outlets in Estonia (83), Latvia (114) and Lithuania (38). Total revenue was SEK 10bn and operating profit was SEK 224m in 2012.

Table 20: Rimi Baltic store format

Source: Handelsbanken Capital Markets and company data

200

300

400

500

600

700

800

2006 2007 2008 2009 2010 2011 2012

Owned69%

Franchise31%

Name Format Nr of stores Store itemsRimi Hypermarket Hypermarket 48 30.000-40.000Rimi Supermarket Supermarket 72 12.000-18.000Supernetto and Säästumarket Discount 115 2,500

Rimi store entrance

In the Baltic region since 1996

Discount and hypermarket focus

August 29, 2013 31

Table 21: Number of stores in Baltic countries

Source: Handelsbanken Capital Markets and company data

Figure 45: Rimi store layout

Source: Company data