in the supreme court of belize a.d., 2006 claim no. 83 of...

TRANSCRIPT

1

IN THE SUPREME COURT OF BELIZE A.D., 2006

CLAIM NO. 83 OF 2006

BETWEEN

(FIRST CARIBBEAN INTERNATIONAL (BANK (BARBADOS) LIMITED CLAIMANT

AND

(THE BELIZE BANK LIMITED FIRST DEFENDANT (DEVELOPMENT FINANCE ( COROPORATION SECOND DEFENDANT (SOCIAL SECURITY BOARD THIRD DEFENDANT (STANLEY ERMEAV FOURTH DEFENDANT [As Receiver for BELIZE GOLD BANANAS LIMITED, TROPICAL PRODUCE COMPANY LIMITED, TOLEDO FISH FARMING COMPANY LIMITED] (BELIZE GOLD BANANAS LIMITED FIFTH DEFENDANT

(TROPICAL PRODUCE ( COMPANY LIMITED SIXTH DEFENDANT (TOLEDO FISH FARMING ( COMPANY LIMITED SEVENTH DEFENDANT (TOLEDO CITRUS COMPANY

LIMITED EIGHT DEFENDANT

Before: Honourable Justice Hafiz

Mr. Michael Young SC for Claimant Mr. Rodwell Williams SC for First Defendant Mr. Fred Lumor SC for Second and Third Defendants Mr. Eamon Courtenay SC for Fourth Defendant

2

J U D G M E N T

BACKGROUND

1. The Claimant is a banking corporation duly incorporated under the Laws

of Barbados West Indies with a branch duly registered in Belize carried on

at #21 Albert Street, Belize City. On the 14 th October 2002 they assumed

all the assets rights liabilities and obligations of the Belize branch of

Barclays Bank PLC in Belize.

2. The First Defendant, The Belize Bank Limited (BBL) is a banking

corporation operating in Belize. The Second Defendant, Development

Finance Corporation (DFC) is a finance corporation operating in Belize.

The Third Defendant, Social Security Board (SSB) is also a financial

institution in Belize.

3. The Fourth Defendant, Stanley Ermeav is Receiver of charged assets

of the Fifth Defendant, Belize Gold Bananas, the Sixth Defendant Tropical

Produce Company Limited and the Seventh Defendant Toledo Fish

Farming Company Limited. The eight Defendant is Toledo Citrus

Company Limited.

4. At the commencement of this Claim there were Second Claimants and

Third Claimants who removed themselves after hearing arguments from

the First, Second, Third and Fourth Defendants that the Claim cannot be

brought in their personal capacities as Receivers and Liquidators. The

Third Claimants were Court Appointed Liquidators of Caribbean Farming

Limited. It is necessary to give the history of Caribbean Farming Limited

(CFL) in order to get a better understanding of the Claim before the Court.

The Claimant’s submission is helpful in this respect. Caribbean Farming

Limited is a company incorporated under the Laws of the Cayman Islands.

However it is the holding company of several wholly owned subsidiary

3

companies which own property in Belize, including the Fourth, Fifth, Sixth,

Seventh and Eight Defendants. This group of companies will be referred

to as the Caribbean Farming Group (CFG).

5. The CFG has conducted the business of the growing, harvesting and sale

of bananas, citrus and shrimp for many years and in that connection has

acquired and managed farmlands in Belize. In the course of the said

business the Caribbean Farming Group (CFG) has arranged financing for

its operations and the subsidiaries of the CFG have created certain

mortgages and charges as security for the financing provided from time to

time. The financing has been provided variously by the First Claimant,

First Caribbean International Bank (Barbados) Limited, the First Defendant

the Belize Bank Limited, the Second Defendant the Development Finance

Corporation and the Third Defendant Social Security Board (hereinafter

called “the Lenders”). The various lenders separately took securities on

properties through the different subsidiary companies and this led to

complexity in the status of the securities and the respective positions of

the lenders.

6. The CFG began experiencing financial problems and from March 2003 the

First Claimant made a formal written demand on the outstanding loans.

Ultimately the First Claimant petitioned the Cayman Court for liquidation of

Caribbean Farming Limited and on the 8 th of April 2005 Provisional

Liquidators were appointed. (They are Marcus Wide and David Walker

who removed themselves as Second Claimants).

7. On 1 July 2005 BBL appointed Stanley Ermeav, the Fourth Defendant,

Receiver of the charged assets of TPCL, TFFC, Farm 1 Limited, Farm 11

Limited and D&F Limited. On 15 July 2005, DFC appointed Stanley

Ermeav, Receiver of the charged assets of BGB. The Third Defendant,

Social Security Board (SSB) on 18 July 2005 appointed Stanley Ermeav,

4

Receiver of the charged assets of BGB. The Fourth Defendant, Stanley

Ermeav is therefore the Receiver of the charged assets of Fifth

Defendant, BGB, the Sixth Defendant , TPCL and the Seventh Defendant

TFFC. On the 28 th of July 2005 the First Claimant appointed Marcus

Wide and Brian Robinson as Receivers (who were removed as the Third

Claimants) of the Fifth Defendant Belize Gold Bananas Limited. The

Receivers appointed by the First Claimant by letters dating between the

end of July and September 2005 , wrote the Fourth Defendant who is also

a Receiver requesting information and accounting in respect of the assets

of the companies of which he had taken possession. The First

Claimants were not satisfied with the response of the Fourth Defendant

and thereafter filed this Claim on the 17 th of February 2006 to protect the

assets which formed the securities for its loans to the CFG and in

pursuance of realizing proceeds from the said securities.

8. After the filing of the Claim the Claimants learnt that (i) in January 2006 a

number of properties of the subsidiary companies of the CFG had been

sold to companies named serially Gold Bananas 1, 2, 3, 6, 11 and Banana

Farms 9 & 10 and Traders Home Limited and (ii) The First Defendant had

been granted Mortgage Debentures on the assets of certain of the above

companies which had purchased the properties in January 2006.

9. Following upon the discovery of the Conveyances and the Mortgage

Debenture the Claimants amended their Statement of Claim. The

Statement of Claim was further amended after the Second Claimants and

Third Claimants were removed as parties. This significantly reduced the

dispute between the parties. The final Amendment to the Claim is labeled

“Third Amended Statement of Claim”.

5

The Claim

10. The Claimant at paragraph 8 of their Claim states that they have

caused searches to be conducted in relation to the securities

created by affiliates of the CFG and annexed to the Claim was a

listing of the charges and Mortgages and assignments. They said

that the Caribbean Farming Group has defaulted on their payment

obligations of the Lenders and as at the 5 th of February 2006 was

indebted to the Claimant in the amount of BZ$13,101.283.70 with

interest continuing to accrue at a current rate of 15 per annum. At

paragraph 12 the Claimant state that the floating portion of the

charges held by the Claimant has crystallized.

11. They claim that by letter of the 11 th of April 2006 addressed to the

Banana Growers Association, Banana Farm 9 & 10 Limited

reported that they had purchased all assets of the Fifth Defendant

from Stanley Ermeav, acting as receiver of the Fifth Defendant.

That through searches at the Land Titles Unit they learnt that

certain Conveyances have been recorded in respect of sales of

lands from the First Defendant Belize Bank and the Fourth

Defendant, Stanley Ermeav to Banana Farms 9 & 10 Ltd. The

Conveyances relate to a 200 acre parcel and 77 acre parcel of

land. See paragraph 15 of Third Amended Statement of Case.

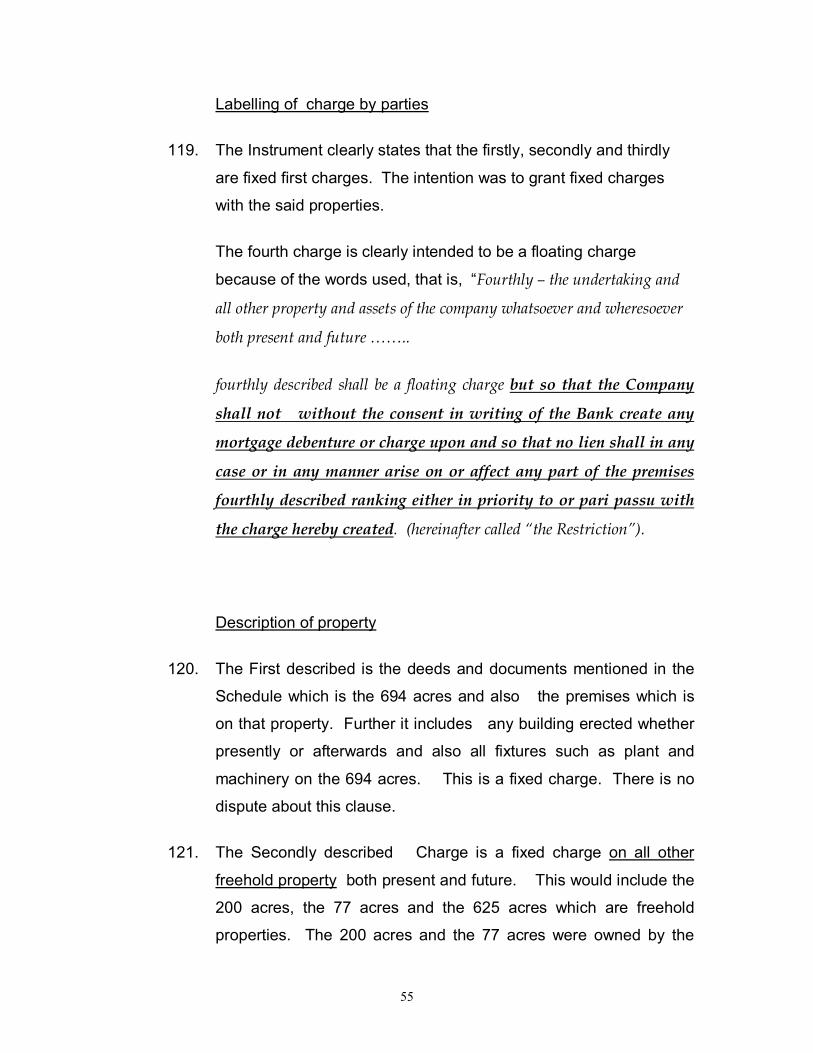

12. The Claimant states at paragraph 19 that the purchaser of the

properties conveyed by the Conveyances above are deemed in

law to have notice of the legal interests of the Claimant contained in

any mortgage instruments recorded in any public registers including

those in the Land Titles Unit and the Companies Registry and are

subject to any prior legal interests owned by the Claimant relating

to the properties subject to the Conveyances or any of them. The

6

purchaser is a company formed and registered under the

Companies Act of Belize in or around October 2005. The Claimant

state that they have also learnt through their attorneys of a

Mortgage Debenture recorded in favour of the First Defendant in

respect of the properties and assets of Farm 9 & 10. The

Mortgage Debenture is:

Mortgage Debenture of 30 th January 2006 – Mortgagor:

Banana Farm 9 & 10 Ltd. – Mortgagee: Belize Bank Ltd. –

The properties directly mortgaged are Farms 9 & 10 625

acres, 200 acres and 77 acres.

13. The Claimant say that the First Defendant as holder of the

Mortgage Debentures listed above is deemed in law to have notice

of the legal interests of the Claimant contained in any mortgage

instruments recorded in any public registers including those in the

Land Titles Unit and the Companies Registry and the Mortgage

Debenture is subject to any prior legal interests relating to the

properties subject to the Conveyances or any of them. See

paragraph 19.

14.The Claimant states that by virtue of Mortgage Debenture dated 8 th

February 1990 recorded in the Land Titles Unit Deeds Book

Volume 4 of 1990 Folios 803 to 834 the Claimant holds a first

charge on properties and assets of the Fifth Defendant, Belize Gold

Bananas in priority to all other charges and interests including

those held by any of the Defendants . See paragraph 21.

15. The Claimant states that that in the event that the Principal and

interest secured by the Mortgage of 2 nd April 1986 created by the

Sixth Defendant Tropical Produce Company Limited has been paid,

7

it holds a first mortgage on the 3225 acre parcel of land charged by

the Sixth Defendant under the Mortgage dated the 30 th of January

1987 recorded in Deeds Book Volume 1 of 1987 folios 943998.

16. The Claimant say that in any event the Mortgage of 30 th January

1987 ranks prior to any other charge by any other mortgagee

insofar as such other charge secures a debt of debts above and

beyond any balance due of the original debt to Clarence McCleary

and Anita McCleary under the Mortgage of 2 nd April 1986.

17. And the relief claimed by them which is reproduced in it entirety is:

1. “A Declaration that the Claimant First Caribbean International Bank (Barbados) Limited by virtue of Mortgage Debenture dated 8 th February 1990 recorded in the Land Titles Unit Deeds Book Volume 4 of 1990 Folios 803 to 834 holds a first charge on properties and assets of the Fifth Defendant Belize Gold Bananas in priority to all other charges and interests including those held by the first Defendant [inclusive of the Mortgage Debenture of 30 th January 2006], Second Defendant and the Third Defendant.

1B. A Declaration that any titles vested by the Conveyances listed in Paragraph 20(which is now paragraph 15 in Third Amended Statement of Claim) above relating to the 200 acre parcel, the 77 pace parcel and the 625 acre parcel formerly in the name of the Fifth Defendant are in any event subject to the Mortgage Debenture of 8 th February 1990 [including the supplemental mortgage] in favour of the Claimant.

1C. A Declaration that the Mortgage Debenture listed in Paragraph 18 above in favour of the 1 st Defendant and relating to the 200 acre parcel, the 77 acre parcel and the 625 acres parcel is in any event subject to the Mortgage Debenture of 5 th

8

February 1990 [including the supplemental mortgage].

2. A Declaration that the Claimant is entitled to take possession of and exercise its power of sale as mortgagee in relation to all properties and assets of the Fifth Defendant Belize Gold Bananas Limited [including any properties purportedly sold under any mortgages held by the First, Second or Third Defendants).

3. An Order for an accounting from the Fourth Defendant Stanley Ermeav of receipts and outgoings in relation to the properties and assets of the Fifth Defendant.

3A. An Order for an accounting from the Second Defendant Development Finance Corporation of receipts relating to the 200 acre and 77 acre parcels of land formerly owned by the Fifth Defendant [including the sale thereof].

3B. And Order for an accounting from the Third Defendant Social Security Board of receipts relating to the 625 acre parcel of land formerly owned by the Fifth Defendant [including the sale thereof].

4. An Order that the Fourth Defendant disclose and/or account for any transfers, conveyances, dealings or agreements for sale or charge or liens created or arising in relation to the properties and assets of the Fifth Defendant since the Fourth Defendant was appointed receiver in July 2005.

5. A Declaration that in any event the Mortgage of 30 th January 1987 in favour of the Claimant ranks prior to the charges in favour of the Second Defendant insofar as charge or charges in favour

9

of the Second Defendant secure a debt or debts above and beyond any balance due of the original debt to Clarence McCleary and Anita McCleary under the Mortgage of 2 nd April 1986.

6. An Order for an accounting from the Second Defendant Development Finance Corporation of receipts relating to the 3225 acre parcel of land formerly owned by the Sixth Defendant Tropical Produce Company Limited [including the sale thereof].

6A. An Order for the payment by the Defendant to the Claimant of such monies as are found to be due to the Claimant relating to the 3225 acre parcel of land formerly owned by the Sixth Defendant.

7. Directions from the Court (if and where necessary) on how proceeds of sale of management of the Fifth Defendant and Sixth Defendant are to be distributed having regard to priority including the respective priorities of the secured creditors including the Claimant as secured creditor.

8. Damages

9. Such further consequential orders and directions as the Court deems fit and just including particularly any injunctions.

10. Costs.”

18. The Defence filed by the First, Second, Third, and Fourth

Defendants were in relation to the Second Amended Statement of

Claim. Since the Third Amended Statement of Claim has reduced

the claim significantly as a result of the removal of the second and

10

third Claimants, the Defences will now be limited to the relief now

claimed.

19. The First Defendant, Belize Bank, in their Defence said that the

Claimant alleges that a mortgage debenture has been recorded in

their favour in respect of properties and assets of Banana Farm 9

and 10 Limited but the Claimant did not urge any impropriety in

respect of this mortgage debenture. Further the Claimant have not

proven interest in the properties of Banana Farm 9 and 10 and

therefore no entitlement to relief on the part of the Claimant can

arise with respect to the said mortgage debenture.

20. The Second Defendant, DFC, admitted the appointment of the

Fourth Defendant as Receiver/Manager of the Fifth Defendant,

Belize Gold Bananas Limited (BGB) under and by virtue of Deed of

Mortgage dated 29 th May, 1991 in respect of the following

properties, namely:

i) 200 acres of land situate at Swasey Branch of

Monkey River subject to Crown Grant No. 27 of 1894.

ii) 77 acres and 1 rood situate at Monkey River subject

of Crown Grant No. 12 of 1903.

Further, that the Fourth Defendant sold the 277 acres of land

sometime in January of 2006.

21. At paragraph 10 of the Defence the Second Defendant, DFC, said

that at all material times, the Claimant knew that the Mortgage

Debenture dated 8 th February, 1990, executed between the Fifth

Defendant, BGB, and the First Claimant, FCIB, does not give the

First Claimant a first charge in priority to the Second Defendant in

11

respect of the 277 acres of land. Further, that the priority of the

Second Defendant in respect of the 277 acres of land charged by a

fixed mortgage contained in a deed of mortgage dated 29 th May,

1991 made between the Second Defendant, DFC, and the Fifth

Defendant, BGB, is not postponed in favour of the First Claimant.

22. Further, at paragraph 11 the Second Defendant states that in the

alternative (a) the first Claimant is estopped and precluded by

acquiescence from denying that the Second Defendant has a first

charge in priority to the first Claimant in respect of the

aforementioned 277 acres of land situate at Monkey River (b) The

First Claimant is estopped by the convention or common assurance

of the parties in respect of the aforementioned 277 acres of land

situate at Monkey River and precluded from denying that the

Second Defendant has a first fixed charge in respect of the same

parcels of land in priority to the First Claimant.

( c ) It appointed the Fourth Defendant, Receiver/Manager of the

Fifth Defendant, Belize Gold Bananas Limited, under and by virtue

of a Deed of Mortgage dated 29 th May, 1991 in respect of the

aforementioned 277 acres of land with the full knowledge and

acquiescence of the First Claimant.

23. As for the Defence of the Third Defendant, SSB, they admit

appointing the Fourth Defendant, Receiver/Manager of Belize Gold

Bananas Limited, under and by virtue of a Deed of Mortgage dated

28 th February, 2000 in respect of the 625 acres of land situate

along Swasey Branch, Harvest Caye , Toledo District which he sold

and filed the notice required by section 97 of the Companies Act,

Chapter 250.

12

24. At paragraph 10 the Third Defendant, SSB states that (a) The

Mortgage Debenture dated 8 th February, 1990 executed between

the Fifth Defendant and the First Claimant does not give the First

Claimant a first charge in priority to the Third Defendant in respect

of the 625 acres of land; (b) the priority of the Third Defendant in

respect of the 625 acres of land charged by a fixed mortgage

contained in a Deed of Mortgage dated 28 th February, 2000 made

among the third Defendant, the Fifth Defendant and the Seventh

Defendant is not postponed in favour of the First Claimant.

25. In the alternative, the Third Defendant states that (a) The First

Claimant is estopped and precluded by acquiescence from denying

that the Third Defendant has a first charge in priority to the First

Claimant in respect of the 625 acres of land (b) The First Claimant

is estopped by the convention or common assurance of the parties

in respect of the said 625 acres of land and precluded from denying

that the Third Defendant has a first fixed charge in respect of the

same parcel of land in priority to the First Claimant. (c) That it

appointed the Fourth Defendant, Receiver/Manager of the Fifth

Defendant under and by virtue of a Deed of Mortgage dated 28 th

February, 2000 in respect of the said 625 acres of land with the full

knowledge and acquiescence of the First Claimant.

26.Both the Second and Third Defendants claim that the Claimants are

not entitled to the Declarations, orders and or relief sought in this

Claim.

13

The evidence

27. The evidence is this case was by way of Affidavits. The

Claimant’s affidavit evidence was from Philip Johnson and

Stephen Duncan. The Second Defendant issued affidavits from

Arsenio Burgos. The Third Defendant’s evidence is from Narda

Garcia. The Fourth Defendant Stanley Ermeav issued one

affidavit.

The Mortgage Debentures for consideration

28. There are a significant amount of mortgages but I am not

concerned with the interpretation of all of them as it is only

necessary to interpret the provisions of the Claimant’s Mortgage of

8 th February, 1990 to determine the characteristics of the charges.

After this is determined then the issue of priority of the following

mortgages will be considered:

(a) For the Claimant, FCIB

29. (i) Mortgage Debenture dated 8 th February 1990 made

between the Fifth Defendant , Belize Gold Bananas, and the

predecessor of the Claimant, Barclays Bank which is recorded in

the Land Titles Unit Deeds Book Volume 4 of 1990 Folios 803 to

834. The Mortgage is for the principal sum of $1,500,000 (as

upstamped).

(ii) Mortgage dated 24 th September 1999 on two parcels of land

comprising 200 acres and 77 acres 1 rood respectively owned by

14

Belize Gold Bananas Limited which is supplemental to the

Mortgage Debenture of 8 th February 1990 above.

(b) For the Second Defendant, DFC

30. There are several Mortgages in favour of the Second Defendant

but I am concerned only about the first Mortgage between the

Second Defendant and the Fifth Defendant, Belize Gold Bananas

Limited with respect to the 200 acres and the 77 acres. That is,

Deed of Mortgage between Belize Gold Bananas Limited and

DFC dated 29 th May, 1991 for $129,165.00 which was secured by

the said 200 acres and 77 acres. There is no dispute that this is a

specific mortgage.

(c) For the Third Defendant, SSB

31. Mortgage dated the 28 th of February 2000 between the Seventh

Defendant Toledo Fish Farming, the Fifth Defendant Belize Gold

Bananas Limited and the Third Defendant Social Security Board by

which the Fifth Defendant mortgaged 625 acre parcel of land in

favour of the Third Defendant for the sum of $2,000,000 . There is

no dispute that this is also a specific mortgage.

The Claimant’s submissions

32. Learned Counsel Mr. Young submitted that the Mortgagor, by

executing the mortgage, acknowledged and accepted the intent

and effects of the above language. That the only property which is

specifically referred to in the 1990 Mortgage Debenture is a 694.36

15

acre parcel situate south of Harvest Caye Work which is referred to

in the Schedule to the Mortgage Debenture. However, he further

submitted that the Mortgage Debenture would clearly charge

properties owned by the Fifth Defendant Company at the date of

the recording of the Mortgage. This would include the 200 acre and

77 acre parcels of land which were first mortgaged to the Second

Defendant (DFC) by a mortgage of 29 th May 1991. These

properties were vested in the Fifth Defendant by a Deed of

Conveyance dated the 24 th of March 1987. Mr. Young submitted

that the 200 acres and the 77 acres were subject to a fixed charge

and not a floating charge.

33. As for property acquired after recording of 1990 Mortgage

Debenture, Learned Counsel submitted that the 625 acre parcel

was vested in the Fifth Defendant by Minister’s Fiat Grant No. 83 of

2000. He submitted that at the very least any mortgage

subsequent to the Mortgage Debenture and covering property

acquired by the Mortgagor after the recording of the Mortgage

Debenture would in equity rank after the Mortgage Debenture. (See

P.J. 2D of Phillip Johnson’s affidavit). By the express terms of the

Mortgage Debenture, the Mortgagor was not supposed to

subsequently mortgage any property without the prior and written

consent of the mortgagor and in such event the subsequent

mortgage would not rank prior to or pari passu with the Debenture.

That any subsequent mortgagee would take a mortgage subject to

all charges recorded in the Deeds Registry and the Companies

Registry. Learned Counsel submitted that this position accords

with common sense, fairness, business efficacy, clarity and

certainty. Learned Counsel submitted that it cannot be right or

proper for a subsequent mortgagee to claim priority to the prior

16

Mortgage Debenture when such Debenture is publicly registered

and so clear in its language.

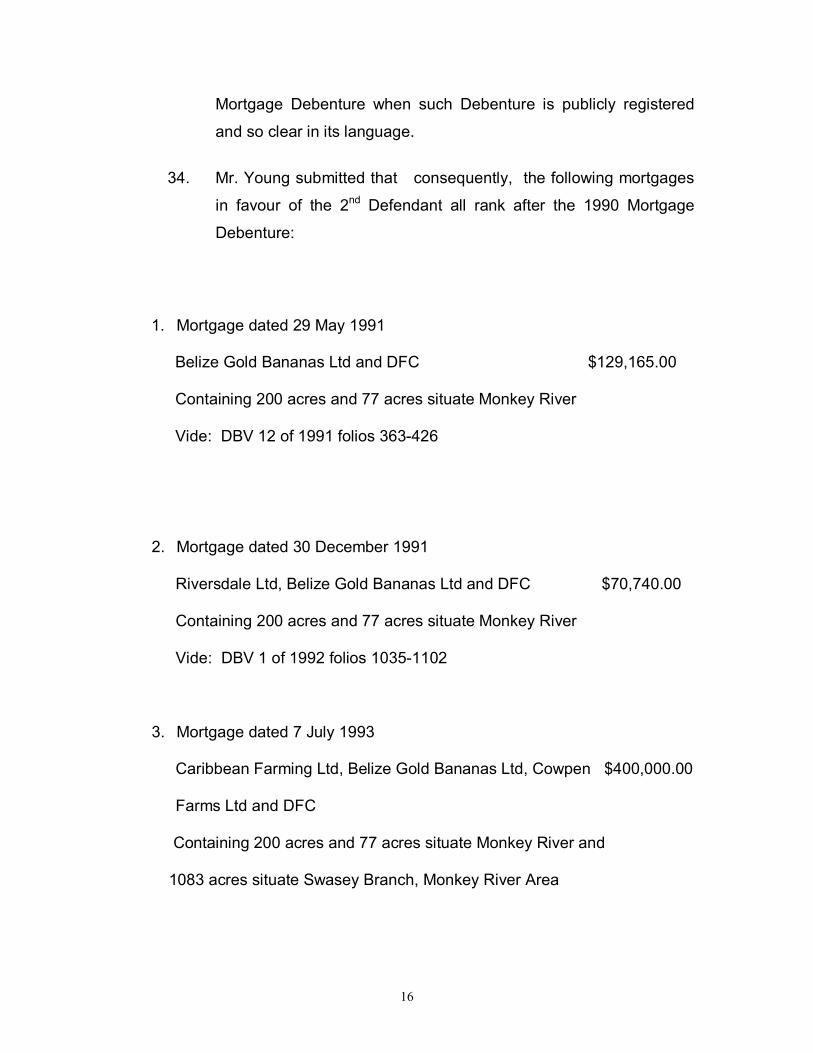

34. Mr. Young submitted that consequently, the following mortgages

in favour of the 2 nd Defendant all rank after the 1990 Mortgage

Debenture:

1. Mortgage dated 29 May 1991

Belize Gold Bananas Ltd and DFC $129,165.00

Containing 200 acres and 77 acres situate Monkey River

Vide: DBV 12 of 1991 folios 363426

2. Mortgage dated 30 December 1991

Riversdale Ltd, Belize Gold Bananas Ltd and DFC $70,740.00

Containing 200 acres and 77 acres situate Monkey River

Vide: DBV 1 of 1992 folios 10351102

3. Mortgage dated 7 July 1993

Caribbean Farming Ltd, Belize Gold Bananas Ltd, Cowpen $400,000.00

Farms Ltd and DFC

Containing 200 acres and 77 acres situate Monkey River and

1083 acres situate Swasey Branch, Monkey River Area

17

4. Deed of Mortgage dated 18 th December 2003 between $2,000.000.00

Belize Gold Bananas Limited as borrower, Tropical Produce

Company Limited as Surety and Development Finance

Corporation as Mortgagee covering 200 acre parcel, 77

acre parcel, 625 acre parcel [owned by BGB] and a 3225

acre parcel [owned by Tropical Produce].

5. Mortgage and Further Charge dated 20 March 2001 $2,000,000.00

Caribbean Farming Ltd, Belize Gold Bananas Ltd, Tropical

Produce Company Ltd, John F. Parsons Inc and DFC

Containing 200 acres situate Monkey River, 77 acres situate

Monkey River, 1083 acres situate Swasey Branch, 995 acres

situate at Potts Creek Road.

35. Mr. Young further submitted that the following mortgage in favour of

the Third Defendant rank after the 1990 Mortgage Debenture. That is:

Mortgage dated 28 th February 2000 between Toledo $2,000.000.00

Fish Farming [as borrower], Belize Gold Bananas

as surety] and Social Security Board [as mortgagee]

Charging 625 acre parcel of land along Swasey

Branch Harvest Caye.

18

36. Mr. Young then referred to the Properties conveyed in January,

2006 owned by the Fifth Defendant, that is the 625 acre parcel of land

and the 200 acre parcel and the 77 acre parcel. The conveyances

are:

(i) Conveyance of 23 rd January 2006 under Mortgage dated the 28 th of February 2000 Mortgagor Belize Gold Bananas Ltd.– Mortgagee Social Security Board – Purchaser Banana Farms 9 & 10 Ltd. This sale relates to the 625 acre parcel of land – Consideration: $960,000.

(ii) Conveyance of 23 rd January 2006 under Mortgages dated (1) 29 th May 1991 (2) 30 th December 1991 (3) 7 th July 1993 (4) 9 th

October 1996 (5) 20 th March 2001 (6) 18 th December 2003 and Deed of Substitution of Mortgage dated 13 th July 1995, Deed of Substitution dated 31 st December 1999 and Deed of Variation and Further Charge dated 5 th May 2004 Mortgagor: Belize Gold Bananas Ltd. – Mortgagee: Development Finance Corporation – Purchaser: Banana Farms 9 & 10 Ltd. This sale relates to the 200 acre parcel and 77 acre parcels of land – Consideration: $570,000.

37. These properties, the 200 acres plus the 77 acres and the 625

acres were then sold to Banana Farm 9 & 10 and have been

mortgaged to the First Defendant, Belize Bank Limited (BBL) by

way of a Mortgage Debenture on all assets of Banana Farm 9 &

10. The details are:

Mortgage Debenture of 30 th January 2006 – Mortgagor: Banana Farm 9 & 10 Ltd. – Mortgagee: Belize Bank Ltd. – (i) Properties being Farm 9 & 10 [the 200 & 77 acre parcels] with all plant, machinery and fixtures (ii) all other freehold and leasehold property present and future (iii) interests in stocks, shares debentures, bonds, book and other debts, monies and (iv) goodwill and all other property ([See exhibit “PJ2D” of Philip Johnson’s affidavit).

19

38. Learned Counsel submitted that the above Mortgage Debenture

purports to be a first fixed charge by way of legal mortgage on the

said properties. That Banana Farm 9 & 10 Limited is reported

as having purchased “all” assets of the Fifth Defendant. This is

evidenced by letter dated April 11, 2006 from Banana Farm 9 &

10 Limited to the Banana Growers Association where they

informed the Association that they purchased all the assets of

Belize Gold Bananas Limited.

39. Mr. Young submitted that the 200 and the 77 acre parcels were

sold by the Second Defendant and the Fourth Defendant in

exercise of the power of sale under the mortgages held by the

Second Defendant, which mortgages rank subsequent to the

1990 Mortgage Debenture in favour of the First Claimant. The

creation of these mortgages subsequent to the 1990 Mortgage

Debenture was in breach of the Mortgage Debenture. He

submitted that at the very least, the conveyance of the 277 acres

would not in any way discharge the legal charge on those lands

created by the Mortgage Debenture. Further, the Second

Defendant and Fourth Defendant would be accountable to the

First Claimant for any proceeds of sale received. That the

$570,000 consideration stated in the Conveyance is consideration

only for the 277 acres of land. He then posed the question as to

the position of the plant, machinery and fixtures (including trade

fixtures). He submitted that all assets were sold to Banana Farm

9 & 10 Limited and the question arises as to the consideration

paid for assets other than the land. He further submitted that no

agreement for sale has been produced and the Second

Defendant and the Fourth Defendant are liable to account for

these properties which have been sold.

20

40. With regards to the 625 acre parcel Mr. Young submitted that the

same considerations apply. That the 625 acre parcel which was

sold by the Third Defendant and Fourth Defendant in exercise of

the power of sale under a mortgage was subsequent to the

Claimant’s 1990 mortgage. Counsel submitted that the only

difference in relation to this parcel of land is that it was not owned

by the Fifth Defendant at the time of the 1990 Mortgage Debenture.

Therefore, he submitted that it may be the case that the Mortgage

Debenture, though ranking in priority to the later mortgage in favour

of the Third Defendant, created an equitable charge on the land

when it was acquired by the Third Defendant. Counsel submitted

that in any event the Third and Fourth Defendants are liable to

account for the sale of the 625 acre parcel and any plant, fixtures

and machinery thereon.

41. Learned Counsel further submitted that the assets covered by

Mortgage Debenture held by the First Defendant in respect of the

property of Banana Farm 9 & 10 Limited is subject to the 1990

Mortgage Debenture.

42. Mr. Young supported his argument on priority of mortgages on the

basis of the time of recording or registration. He referred to

sections 66 and 74 of the Law of Property Act, Chapter 190 which

states:

Section 66 – “A second mortgage or any number of mortgages may be created to affect the same land and in that case they shall, as regards taking effect, have priority in the order in which they are registered in the Land Charges Register or recorded under Part V of the General Registry Act as the case may be

Section 74 – “Every mortgage affecting a legal estate in land made after the commencement of this Act shall rank according to its date of registration as a land charge

21

pursuant to Part IV or recording pursuant to Part VI of the General Registry Act”

43. Mr. Young submitted that the Mortgage Debenture charging the

assets of the Fifth Defendant was lodged for registration on the 8 th

of February 1990 – prior to the recording of any of the mortgages of

the other lenders.

44. Counsel then made submissions on the law on Floating Securities.

He referred to the text Fisher & Lightwood’s Law of Mortgage, 10 th

Edition – 1988 at page 132 to 133 where there is the following

passage describing “Floating Charge”

“Mortgage Debentures almost invariably create a floating security. Such a security is an immediate equitable charge on the assets of the company for the time being, but it remains unattached to any particular property, and leaves the company at liberty to deal with its property in the ordinary course of its business, as it thinks fit, until stopped, either by the appointment of a receiver, or by a winding up, or the company ceasing business, or the happening of some agreed event, when the charge becomes fixed to the assets and effective or as it is said, crystallizes – and gives the debenture holder priority over the general creditors. So long as the security remains a floating security, the property of the company may be dealt with, and even a part thereof sold in the ordinary course of business, as if the security had not been given and any such dealing with a particular property will be binding on debenture holders, provided that the dealing is completed before the charge ceases to be a floating security. A purchaser or other mortgagee from the company will require evidence of noncrystallization. This is generally supplied by a letter to this effect from some officer of the company or the company’s solicitor. Unless prohibited by the conditions of the debentures, this power of disposition extends to the creation of fixed charges, but not the creation of further general floating securities so as to give these priority. In fact, it is usual to provide in the deed that no

22

mortgage or charge ranking pari passu with or in priority to the debenture shall be created by the company. The registration of the charge in the Companies Register will constitute constructive notice of the floating charge to a subsequent mortgagee. The restriction may be noted amongst the filed particulars of the charge in the Companies Register (though there is no express sanction for this practice under the Companies Act – of [compare] the position in Scotland), but while this may give someone who searches the Register actual notice of the restriction, it is generally accepted that such noting is not sufficient to give constructive notice of the restriction . In the case of registered land, if the floating charge is noted on the register, the entry will usually refer to the restriction and a subsequent mortgagee will take subject to the noted rights”

45. Learned Counsel then referred to Lingus in the text Bank Security Documents which states as follows:

“Subsequent Charges

9.6 Because the floating charge is ‘incomplete’ and ‘dormant’ until it crystallizes, subsequent fixed charges (whether legal or equitable) in the ordinary course of business even with notice of the floating charge will take priority over it, subject to para 9.7 below (Re Hamilton’s Windsor Ironworks, ex p Pitman and Edwards (1879) 12 Ch D 707)……

9.7 The above rules do not apply if the floating charge contains a restriction against the creation of charges ranking in priority provided the subsequent Chargee has notice of the restriction. Such a restriction is therefore an essential part of any floating charge.”

46. Learned Counsel then referred to the case of Ferrier v Bottomer 1972 HCA 11 to bolster his argument. Here a floating

charge on the assets of a company, Australian Factors

(Queensland) Ltd. was created to secure moneys owed to

23

stockholders. On the 13 th of March 1964 a receiver was

appointed under the charge. The issue was the treatment [in

terms of priority] of two sums of money which were paid in

settlement of debts to the Company owed from outside of the

State of Queensland. The debts in favour of the Company arose

from the State of New South Wales. The approach of the High

Court was principally to examine the language of the charge

instrument itself.

“If a company borrows money and gives a charge in favour of the lenders, it is not, I think, for the Court to be astute to limit the operation of the deed creating the charge to reduce, in favour of the company, the security of the lenders. An assignment of future assets, such as this deed makes, does not in the absence of clear language so providing, lose its efficacy as an assignment when the deed has the character of a fixed charge” (See p.6)

Justice Menzies quoted the following from a prior Court of Appeal case:

“Reliance was placed on condition no. 1 as showing that property of the company first coming into existence after the appointment of the receiver and manager – in this case the chose in action consisting of the debt now sued upon – was not made subject to any charge: put shortly it was argued that since the phrase used is ‘as regards all other property and assets of the company a floating security’ and since no security on any assets could be described as floating once the receiver and manager was appointed, therefore the phrase ‘all other property and assets’ must be construed as excluding any asset thereafter first coming into existence. This argument seems to me to be as invalid as it is subtle.

…..

The fact that there was a floating charge cannot, it seems to me operate to exclude assets from the agreement to charge. That particular quality of the charge (or the agreement to charge) only means that its full operation is, so to speak, in suspense until certain events occur, and when such an event occurs the charge (or agreement to charge) loses that

24

suspended quality. That in no way justifies the conclusion that the field of the charge is in any way restricted; it only means that after this particular quality disappears equity will fasten the charge directly upon all assets thereafter coming into existence as soon as they do so.” (See pp. 6 7 ).

Later Justice Menzies at page 8 said:

“Here I feel no compulsion to limit the words of the deed which we are considering” (See p. 8).

The Effect of Recording

47. Learned Counsel Mr. Young referred to the following extracts from “Elements of Land Law” by Kevin Gray, Second Edition 1993 on the effect of recording.

“Legal Rights Bind the world

The force of the first axiom is simply explained. If B owns a legal right in or over land belonging to A, and C later acquires any interest in that land, B’s right is binding on and effective against C. This result follows irrespective of whether C previously knew of B’s right. The outcome rarely works injustice since almost all legal rights in or over land are evidence on the face of the documents relating to title, and are therefore open to perusal by an intending purchaser (See page .75 of text)

Equitable rights are governed by the doctrine of notice

Constructive Notice. Constructive notice relates to matters of which the purchaser would have been consciously aware if he had taken reasonable care to inspect ……… unconscionably, on the rights of such third parties in the property” (See pp.80 to 81 of text).

25

48. Learned Counsel submitted that in Belize, notwithstanding

the introduction of the Torrens system of Land Title

registration under the General Registry Act and the gradual

change to the system established under the Registered Land

Act, the “Deeds Registry” remains a major part of our land

titles system and the properties subject of this claim fall

under that system. He referred to paragraph 1024 of

Volume 14 of Halsbury (3rd Edition) – 156 where the

following is stated;

“Constructive notice where title not investigated. A purchaser is bound, at the risk of being affected with constructive notice, to make the usual full investigation of title, notwithstanding that he is debarred by agreement from doing so; and he is bound to follow up any inquiries suggested by matters of which he has actual notice; so that notice of a deed, which affects the land, being a deed within the period for which the title should be investigated, is notice of both its contents and of the facts which would have been disclosed if its production was insisted on.”.

49. Next, Learned Counsel referred to the case of Overseas Chinese Banking Corporation v Malaysian Kuwaiti Investment Co. Sdn Bhd [2003] and submitted that this case is instructive on the

underlying principles relating to notice, priority and the failure to

make proper inquiries. Counsel referred to Paragraphs 168, 169.

At Paragraph 173 Judge Redlich states:

“conduct which falls short of subjective dishonesty but involves failure to make the inquiries which a hypothetical, reasonable and honest person would make in the light of known facts is sufficient to affect the conscience and result in equitable intervention. A stranger will be liable for breach of trust in such circumstances. Such conduct is a form of

26

constructive or equitable fraud which stands outside subjective dishonesty.”

Mr. Young submitted that the First, Second, Third and Fourth

Defendants in law had constructive notice of the Mortgage

Debenture of 8 th February 1990 in favour of the First Claimant. He

said that when one looks at the language of the 1990 Mortgage

Debenture, it is complete and manifest in declaring the intent and

effect of the mortgage.

Submissions of the First Defendant

50. Mr. Williams SC Submitted that the Encumbered Properties are the

200 acres and 77 acres formerly owned by BGB and was sold and

conveyed by DFC to Banana Farm 9 and 10 Limited. That the 625

acres formerly owned by BGB was sold and conveyed by SSB to

Banana Farm 9 and 10 Limited. Then Banana Farm 9 and 10 Limited

mortgaged the said 200 acres, the 77 acres and the 625 acres to

BBL, the first Defendant. He correctly stated that this is not in

dispute. What is in dispute is who has the priority.

51. Mr. Williams who helpfully prepared a chart of the Mortgages in

relation to this Claim submitted that the chart clearly shows that DFC

held a specific first priority legal mortgage over the 200 acres and the

77 acres and that SSB, the Third Defendant held a specific first

priority legal mortgage over the 625 acres. This chart shows specific

property and the date of registration of the mortgage. Learned

Counsel submitted that FCIB is shown to have a Debenture with a

specific first priority legal charge on 694 acres only and what

purports to be a legal charge, but can be no more than an equitable

charge over “all other (if any) freehold property” then owned by BGB.

27

He submitted that nine years later and after the DFC specific legal

mortgages on the 200 acres and the 77 acres, the Claimant

converted to a specific legal mortgage on the 200 acres and 77

acres only, and not on the 625 acres.

52. Mr. Williams in response to the Claimant’s submission on the fixed

or specific charge on the 200 acres and the 77 acres parcels of land

which they say was notice to all the world and which therefore ranks

in priority to DFC’s later mortgages referred to The Law of Corporate Receivers and ReceiverManagers by Andrew D. Burgess at page page 34 where fixed charge is described thus:

“. . . as a charge that attaches to a particular piece of

property which is identified when the charge is created and

whose identity does not change during the subsistence of

the charge. This is because, immediately a fixed charge,

other than a legal mortgage, is granted, then by virtue of the

debenture, a proprietory interest is absolutely and

irrevocably transferred by way of specific equitable

assignment to the debenture holder. In the case of a legal

mortgage, the transfer is of both the proprietary as well as

the legal interest. The transfer of the proprietary interest and

in the case of the legal mortgage, the property in the secured

asset, means that the company cannot deal with the charged

assets without the consent of the debenture holder.

53. Mr. Williams also cited the case of Re Yorkshire Woolcombers Association [1903] 2 Ch 284 at page 294.

He submitted that with regards the law on floating charges “It is

now well settled that a floating charge is an immediate equitable

28

charge on the assets of the company for the time being, which,

unlike a fixed charge, remains unattached to any specific property

until crystallization, when it settles and becomes a fixed equitable

charge.”

54. He further submitted that the law as to whether a fixed charge or a

floating charge is created is now made absolutely clear by the Privy

Council decision in the case of: Agnew v. Commissioner of

Inland Revenue [2001] 2 A.C. 710 at page 716 where it was held

that the critical feature which distinguished a floating from a fixed

charge lay in the chargor’s ability, freely and without the chargee’s

consent, to control and manage the charged assets and withdraw

them from the security.

55. He further referred to the House of Lords decision in

National Westminister Bank v. Spectrum Plus Ltd [2005] UKHL 41 where it was held that it was the courts duty to characterize the

document according to the true legal effect of its terms. That the

real question was whether the rights and obligations conferred and

imposed by the debenture disclosed an intention that the company

should be free to deal with the assets and withdraw them from the

security without the consent of the debenture holder, then the

inevitable consequence would be to reject the description as a fixed

charge.

56. Mr. Williams submitted that even though the FCIB Debenture claim

to create a fixed charge on “all other (if any) the freehold property

of the company both present and future …” the charge actually

created was not a fixed charge it was a floating charge because: (a)

although the company already owned the 200 acres and the 77

acres and had title thereto the Bank allowed it to retain the titles

29

and to be able to deal with these lands in the ordinary course of

business without the consent of the Bank; (b) by clause 6 the

company was to deposit all titles to real property with the Bank

during the continuance of the security, but this never happen and if

it did happen the mere deposit of title deed does not create a fixed

legal mortgage.

57. Counsel submitted that this is consistent with intention to create a

mere equitable charge; (c) by clause 7 the company was required

to, if the Bank requested it, to give it further legal or other

mortgages or charges on the premises constituted in the deposited

titles and deeds, or which may be later acquired by the Bank; By

clause 13 (11) the company again covenants with the Bank to

deposit all titles to land that it may own and at the request of the

Bank to execute to a legal mortgage, but if the Bank does not

require anything of it the company was free to deal with those

assets as it sees fit without the consent of the Bank. (d) it was not

until nine years later that the Bank did call on the company to do a

fixed mortgage on these lands for the purpose of perfecting the

charge created by the Debenture, (see Mortgage between BGBL

and FCIB of September 24 th , 1999 see clause 4) of the aforesaid

mortgage. He submitted that this is a clear indication that the

company was free to deal with these lands otherwise and so the

charge on them by the Debenture was not fixed. The charge was

only a floating charge.

58. Mr. Williams submitted that as the subject of a floating charge the

company BGBL was free to deal therewith until the Debenture

crystallize and that such crystallization occurred not when the

demand letter was written in 1993 by FCIB, as there followed a

forbearance, and in any event the DFC mortgage was already

30

created in 1991. He further submitted that the crystallization

occurred when the receivers was appointed in July 2005, after the

creation of the DFC mortgages, and so the floating charge

crystallize to create an equitable charge in favour of FCIB only

then, and such a charge therefore ranks after DFC’s charge.

59. Learned Counsel submitted that as to the 625 acres of parcel of

land BGBL became the owner in 2000, well after the creation of

the Debenture and it is admitted that it could not have a fixed

charge thereon and so it could be held under the floating charge, so

the creation of SSB mortgage in 2000 means that it ranked in

priority to FCIB earlier equitable charge.

60. Mr. Williams submitted that DFC and SSB appointed the Fourth

Defendant receiver of BGB before FCIB appointed Receivers of

BGB. He said that FCIB by virtue of its equitable charge under

the Debenture first in time does not have priority over DFC as to

the 200 acres and the 77 acres and over SSB as to the 625

acres. He submitted that the equities are not equal, as a legal

charge later in time does rank in priority over an earlier equitable

charge, and that the equitable charge only attaches on

crystallization of the floating charge, which occurred after the

creation of DFC legal mortgage. Counsel submitted that DFC first

legal mortgage on the 200 acres and 77 acres and SSB first legal

mortgage on the 625 acres ranks prior to FCIB equitable charge

under its Debenture. That the later perfection of First Caribbean

equitable charge to a specific legal charge some nine years later

over the 200 acres and 77 acres ranked after the DFC first

specific legal mortgage. Further, FCIB at no time perfected its

equitable charge over the 625 acres on which SSB held a first

priority legal mortgage.

31

61. Learned Counsel submitted that nine years later, on 24

September 1999, BGB and FCIB purported to perfect FCIB’s

security over 277 acres of land by executing a Deed of Mortgage

in favour of FCIB and recording it in Deeds Book Volume 30 of

1999 at folios 525 and 536.

62. Mr. Williams submitted that preamble 2 of the Deed of Mortgage

dated 24 September 1999 in which Belize Gold Bananas (BGB)

and FCIB purported to perfect FCIB security over 277 acres of

land it was acknowledged that the said 277 acres of land are also

mortgaged in favour of DFC by virtue of four separate deeds of

mortgage dated 29 May 1991, 30 December 1991, 7 July 1993

and 9 October 1996, respectively.

That in preamble 1 of the said Deed of Mortgage, the 1990

Debenture is referred to and in preamble 4, the deeds says that

“For the purpose of perfecting the Charge created by the

Debenture upon the property described in the Schedule hereto

FCIB, “in pursuance of the power in that behalf contained in the

Debenture has called upon the company to execute such specific

Charge by way of legal mortgage thereon as is hereinafter

contained which the company has agreed to do.”

The specific properties charged are described in the Schedule as

first, 200 acres and second 77 acres.

63. Mr. Williams further submitted that even if First Caribbean

Debenture created a first legal charge on the Encumbered

Properties, but which he said is denied, in priority to DFC and SSB

specific legal mortgages the sale and conveyance by DFC and SSB

32

as second priority mortgages is still valid and effective in passing a

good title for the Encumbered Properties to the purchaser Banana

Farm 9 and 10 Limited and First Caribbean may as first priority

mortgagee look to the proceeds of sale only in priority to DFC and

SSB. Then Banana Farm 9 and 10 Limited as purchasers took free

and clear of First Caribbean charge and its mortgage to BBL is

likewise free of any interest in the Encumbered Properties in favor

of First Caribbean.

64. Mr. Williams further submitted that by Section 69 of the Law of Property Act, Chapter 190 of the Laws of Belize, Revised

Edition 2000 2003 where an estate in fee simple has been

mortgaged by creation of a charge by way of legal mortgage and

the mortgagee sells under power of sale conferred by that

instrument the conveyance or transfer by him operate to vest the

fee simple in the purchaser subject to any legal mortgage having

priority to the mortgage in right of which the sale is made and any

money thereby secured and thereupon the charge by way of legal

mortgage and any subsequent charges shall merge or be

extinguished as respects the land conveyed. Hence FCIB had no

specific legal mortgage or charge on SSB’s 625 acres in any event.

65. Mr. Williams further submitted that First Caribbean is estopped by

acquiescence, convention or common assurance and waiver of

rights as against DFC’s legal charge on the 200 acres and 77

acres. Therefore, the Encumbered Properties sold and conveyed

by DFC and SSB to Banana Farm 9 and 10 Limited extinguished

the subsequent legal charge of FCIB on the 200 acres and the 77

acres, there being no legal charge of FCIB on the 625 acres sold

and conveyed by SSB, the purchaser Banana Farm 9 and 10

Limited took free and clear and its later mortgage of the

33

Encumbered Properties to BBL was free of any interest of FCIB in

the Encumbered Properties.

Submissions by Mr. Lumor for Second Defendant, DFC

66. Learned Counsel Mr. Lumor in his written submissions stated that

the Debenture made between the Fifth Defendant and the

predecessor of the Claimant, Barclays Bank created (a) a floating

charge over the present and future assets of the Fifth Defendant

and (b) A first legal charge over 694.36 acres of land situate South

of Harvest Caye Works in the Toledo District owned by the Fifth

Defendant by virtue of Minister’s Fiat (Grant) No. 6 of 1990 dated

22 nd January, 1990.

67. Learned Counsel stated in his written submissions that when the

Second Defendant by a Deed of Mortgage dated 29 th May, 1991

took a first legal charge over the 200 acres and the 77 acres of land

owned by the Fifth Defendant the Debenture of the Claimant did

not crystallize.

68. Mr. Lumor submitted that when the Claimant made a further

advance of BZ$1.5 million to the Fifth Defendant by virtue of Deed

of Mortgage dated 24 th September, 1999 the said Mortgage

recited DFC’s Mortgage at Recital Clause 3. Learned Counsel

also referred to the recital in Clause 4 of the Claimant’s 1999 Deed

of Mortgage which include the following:

“4. for the purpose of perfecting the charge created by the

Debenture upon the property described in the Schedule hereto the

Bank in pursuance of the power in that behalf contained in the

34

Debenture has called upon the Company to execute such specific

charge by way of legal mortgage thereon as is hereinafter

contained which the Company has agreed to do.

69. It is Mr. Lumor’s submission that by the aforementioned term

included in the 1999 Charge the Claimant has acknowledged that

DFC has a first legal charge on the 277 acres of land owned by the

Fifth Defendant and sought to ‘neutralize’ the effect of the first

charge of DFC. Mr. Lumor said that the attempt to perfect the

1990 Debenture of the Claimant by the 1999 Deed is a futile act

which gave no priority in ranking to the Claimant.

70. Learned Counsel in his written submissions on the law of Floating

Mortgage referred to the text Law of Mortgage, 10 th edn., by

Fisher & Lightwood at page 132 to 133. This passage is also

quoted above in the Claimant’s submission.

71. Mr. Lumor also referred to Barnsley’s Conveyancing Law and Practice, 3 rd Editon., by D.G. Barnsley at page 365 which states:

“3. Floating Charges. A floating charge has been judicially explained as one which presently affects all the items

expressed to be included in it but not specifically affecting any

item until the happening of an event which causes the

security to crystallize as regards all the items. It floats over

the company’s assets, enabling the company to deal with

them in the ordinary course of business. It becomes a fixed

charge on the occurrence of an event causing it to crystallize,

eg liquidation, or the appointment of a receiver.”

35

72. Mr. Lumor submitted that the charge given to DFC on the 277 acres

was given by the Fifth Defendant in the “ordinary course of

business”. He referred to the case of Countrywide Banking

Corporation Ltd. Vs. Brian Norman Dean (1988) AC 338 at 349

where the Privy Council stated that the transaction must be such

that it would be viewed by an objective observer as having taken

place in the ordinary course of business.

73. Mr. Lumor then referred to the Conveyances referred to by the

Claimant in their Claim in which they said that the purchasers of

the properties are deemed in law to have notice of the legal interest

of the Claimant contained in any mortgage instrument recorded in

any public registers including those in Land Titles Unit and the

Companies Registry. Learned Counsel submitted that this

statement cannot be sustained in law as the averment did not

identify the mortgages and the particular public register meant.

Further, he submitted that it was not mentioned whether the floating

charge of the Claimant crystallized before DFC took the charge on

the 277 acres of land.

74. In support of his argument on Floating charge over present and

future assets, learned counsel referred to the case of T. Niall

Welch vs, Bowmaker (Ireland) Limited and Others (1980) I.R. 251 at 255 to 256 per Henchy J. who gave his views on a

debenture that charged properties present and future and also

specific charge. Henchy J. said:

“ I am fortified in this conclusion as to the extent of the

specific charge by the fact that, when the particulars of the

charge created by the debenture were lodged with the

registrar of companies for registration, the “short particulars

of the property” charged were given …as “the company’s

36

undertaking and all its property and assets present and

future including its uncalled capital for the time being

goodwill and as a specific charge the following premises …”

The words after “the following premises” described the

properties specified in the schedule to the debenture. It

would seem that Bowmaker did not consider (or intend

anyone consulting the statutory register of charges to

consider) that the debenture had created a specific charge

over the Ivy Lawn property. Bowmaker represented to the

registrar of Companies, and to the public at large, that the

charge over the Ivy Lawn property created by the debenture

was only a floating charge. In my view, that was a correct

representation of the effect of the debenture.”

75. With regards to the Notice of the Particulars of the Mortgage, Mr.

Lumor referred to the above case as Per Hency J. at page 255 to

256 who said that there is no duty on the bank to seek out the

precise terms of the debenture and that actual or express notice of

the prohibition must be shown before the subsequent mortgagee

can be said to be deprived of priority.

76. Learned Counsel, Mr. Lumor also referred to Legal Problems of Credit and Security, 3 rd ed., by Roy Goode para. 224 where it is

said that:

“It is well established that registration of a charge, though notice

of the existence of the charge, is not notice of the contents of the

instrument of charge, despite the fact that a party searching the

register and obtaining details of a registered charge is then

entitled to inspect a copy of the charge instrument at the

37

company’s registered office….. As the law now stands, the rule is

clear: registration is not notice of the terms of the security

agreement.”

77. And he further referred to para 226 where it is said that:

“Where a floating charge creates restrictions on the debtor’s

power of disposal …. The absence of such restrictions in the

filed particulars entitles a third party acquiring an interest in the

asset without notice of the restrictions to ignore them.”

78. Mr. Lumor referred to the Affidavit of Arsenio Burgos, Chairman of

the Board of Directors of the Second Defendant , DFC sworn to on

6 th May, 2006 at paragraph 6 and 7. At paragraph 6 Mr. Burgos

deposed that the Claimant took a Mortgage Debenture dated 8 th

February, 1990 as a floating charge on the assets. See Exhibit

“AB–1” for the Mortgage. Then at paragraph 7 he deposed that

the particulars of Mortgage or Charge filed in the Companies

Register by the First Claimant in relation to the aforementioned

Debenture pursuant to Section 93 of the Companies Act, Cap. 250

is also produced. See Exhibit “AB2”.

79. Mr. Lumor submitted that the shorts particulars of the property

mortgaged, that is Mortgage dated February, 1990 filed by the

Claimant evidenced an intention or gave notice of only 694.36

acres of Land as being the subject of a fixed charge whilst all the

other assets including “present or future” were subject to the

floating charge. He submitted that the Fifth Defendant was

therefore entitled to deal with the other assets in the ordinary

course of business including charging the same by fix charge.

Further, he submitted that the DFC cannot be imputed with notice

38

of any restrictions contained in the Mortgage Debenture of the

Claimant dated 8 th February, 1990.

80. Mr. Lumor in further support of this argument referred to the case

of Siebe Gorman & Co. Ltd. Vs. Barclays Bank Ltd. (1979) 2 Lloyd’s Report 142 at 160. Though this case is now overruled he

submitted that parts of it are not overruled. Here it is said that while

the registration of particulars of a charge at the Companies Registry

may by itself serve to give subsequent mortgagees constructive

notice of a charge affecting the company’s property, it will not be

deemed by itself to give them constructive notice of the special

provisions contained in that charge restricting the company from

dealing with its property in the usual manner, at least when the

subsisting charge is a floating security.

Submissions for the 3 rd Defendant, SSB

81. For the Third Defendant, Mr. Lumor applied the same principles of

law as in his submissions for DFC. He submitted that the

particulars of the property mortgaged by the Fifth Defendant to the

Claimant filed in the Companies Registry pursuant to section 95 of

the Companies Act, Chapter 250 recites the 694.36 acres of land

and the present and future assets of the mortgagor, the Fifth

Defendant. The Notice is dated 8 th February, 1990. The amount

secured by the mortgage was BZ$1 million and not

BZ$13,101,283.70.

82. Learned Counsel submitted that the Third Defendant, SSB, took a

first legal charge of the 625 acres of land owned by the Fifth

Defendant by a Deed of Mortgage dated 28 th February, 2000 for

a loan of BZ$2,000,000.00.

39

83. He further submitted that when the SSB took the 625 acres of land

as security, the Debenture of the Claimant did not crystallize. The

Fifth and Seventh Defendant defaulted on the loan and the fourth

defendant was appointed Receiver/Manager of the assets of the

Fifth Defendant with knowledge and notice to the Claimants. He

further submitted that the Fourth Defendant was appointed

because its Deed of Mortgage dated 28 th February, 2000 ranked

superior to that of the First Claimant.

84. Mr. Lumor also relied on the cases of National Westminister Bank

v. Spectrum Plus Ltd [2005] UKHL 41 and Agnew v. Commissioner of Inland Revenue [2001] 2 A.C. 710 at page 716 in support of his arguments. Learned Counsel in oral arguments also referred to the text ‘Principles of Modern Company Law, by Gower and Davies, 7 th Edition in support of his arguments at

pages 818 – 825. This was in relation to the nature of the floating

charge, the vulnerability of the floating charge and crystallization.

Response from Mr. Michael Young

85. Mr. Young in his response to the arguments by Mr. Lumor and Mr.

Williams said that the Agnew case supra and Spectrum case

supra actually support the position of the Claimant. In the Agnew’s case Mr. Young drew the Court’s attention to page 716

at paragraphs 3 and 4 where the Court looked at the question of

whether the Company’s right to collect book debts and deal with

their proceeds free from their security means that the charge on

the uncollected book debts, though described in the debenture as

fixed, was nevertheless a floating charge until it crystallized by the

appointment of the receivers. The Court said that this is a question

40

of characterization and to answer it the Court must examine the

nature of the floating charge and ascertain the features which

distinguish it from a fixed charge.

86. Mr. Young then drew the Court’s attention to page 730 of the said

case at para 49 where the Court said that the Company was in

control of the process by which charged assets were extinguished

and replaced by different assets and this is inconsistent with a fixed

charge. Mr. Young then referred to the same case at pages 725

726 para 3132 where the Court stated that in deciding the

question of whether a charge is a fixed charge or a floating charge,

the Court must be engaged in a twostage process. The first stage

is to construe the instrument of the charge and seek to gather the

intentions of the parties from the language they have used. The

second stage is the categorization stage. The Court also said that

“This is a matter of law. It does not depend on the intention of the

parties. If their intention, properly gathered from the language of

the instrument is to grant the company rights in respect of the

charged assets which are inconsistent with the nature of a fixed

charge, then the charge cannot be a fixed charge however they

may have chosen to describe it. A similar process is involved in

construing a document to see whether it creates a licence or

tenancy. The Court must construe the grant to ascertain the

intention of the parties: but the only intention which is relevant is the

intention to grant exclusive possession……. in construing a

debenture to see whether it creates a fixed or a floating charge, the

only intention which is relevant is the intention that the Company

should be free to deal with the charged assets and withdraw them

from security without the consent of the holder of the charge; or to

put the question another way whether the charged assets were

41

intended to be under the control of the company or of the charge

holder.”

87. Mr. Young thereafter referred to the Spectrum case at

paragraphs 83, 99, 104, and para 111. Paragraph 99 dealt with

the classic and frequently cited definition of a floating charge given

by Romer J in the Yorkshire case. Mr. Young in referring to this

definition said that the Debenture in question had a fixed charge on

unfixed things because the property is capable of being ascertained

and defined. The property here is land, that is, the 200 acres, 77

acres and the 625 acres.

88. In referring to paragraph 104, Mr. Young submitted that this is in

contrast with Mr. Williams’ submission. At para 104 the Court said

that the debenture could fortify the apparently fixed character of the

charge by including a provision entitling the chargee to call for a

formal written assignment by the chargor of the debts as they

accrued. Mr. Young submitted that by having a provision which

fortifies the fixed charge does not mitigate the idea of fixed charge.

89. Para 111 refers to the essential characteristic of a floating charge

which distinguishes it from a fixed charge which is the chargor is

left free to deal with the asset.

90. Mr. Young then referred to the case of Welsh and Bowmaker supra cited by Mr. Lumor. He drew the Court’s attention to the

judgment of Henchy J. at page 253, para 3 where the Court said

that that because there was a qualifying condition in the debenture

a conflict has arisen between Bowmaker and the bank as to their

priorities in regard to the Ivy Lawn Property. He then went on to

look at the complicating condition in the debenture. Mr. Young

42

submitted that there was an internal conflict in charging document

which determined the result. He then referred to Kenny J.

dissenting judgment where the learned Judge found that the

debenture created a specific charge on the Ivy Lawn Property

although it was not mentioned in the particulars.

91. Mr. Young further submitted that he disagrees with Mr. Lumor that

the charge in the Debenture in question is a floating charge and

that all the property, all the land charged is a fixed charge. Mr.

Young further submitted that the language of the 1990 Mortgage

Debenture is clear unlike the situation of the Welch and Bowmaker Debenture.

92. He then looked at the Clauses in the 1990 Debenture and

submitted that by Clause 6 all land is charge with fixed charge.

Clauses 7 and 8 are confirmation clauses. Clause 13(11) is

consistent with legal charge.

93. Mr. Young submitted that the 1999 Debenture seek to perfect the

charge. It does not mean it was not specific. He said that when

one say that he is perfecting does not mean that you do not have a

legal charge and that the clear intent is that the charge is really

retroactive back to the 1990 Debenture. That the said Debenture

of 1990 created a first legal charge on the 277 acres.

94. With regard to the 625 acre parcel Mr. Young submitted that there

was no fixed charge on the 625 acres. But in terms of equity, FCIB

ranks first. When the subsequent legal mortgagee exercised its

power of sale, the ranking would apply to the proceeds of sale and

FCIB would rank first.

43

Determination

95. The first issue for determination is whether the security in

Mortgage Debenture dated 8 th February 1990 in favour of the First

Claimant in respect of the 200 acres and 77 acres is a fixed charge

or a floating charge. To answer this question the court has to

look at the distinction between a fixed charge and a floating charge.

To do this the Court will examine the nature of the floating charge

and ascertain the features which distinguish it from a fixed charge.

It is therefore necessary to touch on the history of the floating

charge though not in any detail. See the Agnew case supra for

the history of the floating charge from its inception to 2001 when Agnew was decided. The cases adjudicated upon by the Courts

with regards to floating charge/fixed charge paid particular attention

to charges over book debts. In the Spectrum case supra the

House of Lords finally resolved the controversial legal issue

concerning the distinction between a fixed charge and a floating

charge. I say controversial because of the previous position of the

law.

96. The floating charge originated in England in a series of cases in the

Chancery Division in the 1870s. The reason for this development

was because of the possibility of two things. (1) The possibility of

assigning future property in equity which was confirmed in Holroyd v. Marshall (1862) 10 HL Cas 191. This principle

made it possible for future book debts to be assigned by way of

security. See the case of Tailby v Official Receiver (1888) 13

App Cas 523. (2) The Companies Clauses Consolidation Act,

1845 sanctioned a form of mortgage for use by statutory

companies by which the company assigned “its undertaking”.

44

97. Before moving on I will touch on what is meant by the word

“undertaking”. In Re Panama New Zealand and Australian Royal Mail Co. (1870) 5 Ch App 318 the Company charged its

“undertaking and all sums of money arising therefrom”. Gifford LJ

held, at p. 322, that “undertaking” meant “…all the property of the

company, not only which existed at the date of the debenture, but

which might afterwards become the property of the company.” He

also said that the word “undertaking” “..necessarily infers that the

company will go on, and that the debenture holder could not

interfere until either the interest which was due was unpaid, or until

the period had arrived for the payment of his principal , and the

principal was unpaid.” See also paragraph 96 of Spectrum case

supra.

98. Now, on the reason for the development of the floating charge was

that compliance with the terms of the fixed charge on the

company’s circulating capital would paralyse its business. This is

because the fixed charge gives the holder of the charge an

immediate proprietary interest in the assets subject to the charge

which binds all those into whose hands the assets may come and

who has notice of the charge. Unless the consent of the holder of

the charge is obtained the Company would be unable to deal with

its assets without committing a breach of the terms of the charge.

In other words a fixed charge on all the property of the Company

would deprive the company of access to its cash flow, which is the

life blood of a business.

99. A floating charge on the other hand contemplates that the

Company will continue to carry on the business despite the

existence of the charge. The charge is upon the entire

undertaking of the debtor company and its assets from time to time

and at the same time the Company is able to freely deal with its

45

assets and pay its trade creditors in the ordinary course of business

without any consent from the holder of the charge. This form of

security was very attractive to banks and it acquired great

importance in the English commercial life.

100. The floating charge however was criticized because it enabled the

holder of the charge to withdraw all or most of the assets of an

insolvent company and leave the liquidator with little or nothing and

as a consequence they were unable to pay preferential creditors.

This led to the provision of laws which made the preferential debts

payable out of proceeds of a floating charge in priority to the debt

secured by the charge.

101. But then there was a second mischief which arose because of the

nature of the floating charge which put ordinary trade creditors of

the company at risk even though they would not know of the

existence of the charge. The reason being is that the holder of the

charge can at any time step in and obtain priority over them. This

normally leave many supplier of goods unpaid. This was seen as a

great injustice and more than 80 years later the remedy adopted

by Parliament was to require floating charges to be registered so

that proposed creditors of the company could discover the

existence of the floating charge. This requirement was introduced

in England by the Companies Act 1900. See section 14 of that

Act. Later by the Companies Act 1907, section 10 (1) (e) it was

extended to include all charges on book debts whether floating or

fixed.

102. The Act did not provide any definition for “floating charge” and

before the introduction of any legislation the term did not have any

distinct meaning. It therefore, became necessary to distinguish

46

between fixed charges and floating charges within the meaning of

the Act.

The previous position under the law

103. A number of judicial decisions gave conflicting interpretations over

the characteristics that were definitive of a fixed charge, particularly

with references to charges over book debts, commencing with the

decision of Slade J. in Siebe Gorman v Barclays Bank (1972) 2 Lloyd’s Rep. 142. For clarity ‘book debts’ of a Company is

money outstanding to the company from its customers. In Sieb Gorman case it was held that where the debenture required the

charged book debts not to be disposed of prior to their collection

and the proceeds to be paid into a specific bank account upon their

collection, such restrictions would be sufficient for the purpose of

constituting a fixed charge. As a result, under this case the charge

was fixed even if the debenture did not prohibit the debtor from

withdrawing money from the account into which the proceeds were

deposited without the bank’s consent, so long as the other

restrictions were present.

104. The problem with this decision was highlighted in Spectrum case