incentivizing and rewarding employee performance ...c.ymcdn.com/sites/ and rewarding employee...

TRANSCRIPT

Click to edit Master title style

Incentivizing and Rewarding Employee Performance:Incentivizing and Rewarding Employee Performance:How to Develop Effective Incentive Compensation

Programs

Presented By:Priya J Kapila CCP SPHRPriya J. Kapila, CCP, SPHR

Delaware SHRM Chapter MeetingMay 14, 2013

Click to edit Master title styleObjectives:

• Variable Pay Overview• Types of Incentive Plans

D t i i Eli ibilit d P Mi• Determining Eligibility and Pay Mix • Identifying Performance Measures • Setting Incentive Award Amounts• Setting Incentive Award Amounts • Communicating Incentive Compensation • Evaluating Plan Effectivenessg• Recap: Do’s and Don’ts of Incentive Plan Design

2

Click to edit Master title styleVariable Pay Overview

• Variable Pay is compensation that is contingent on discretion, performance, or results achieved.

• More than 80% of U S organizations provide some form• More than 80% of U.S. organizations provide some form of short-term variable compensation, while over 50% have at least one long-term incentive plan

3

Click to edit Master title styleVariable Pay Overview

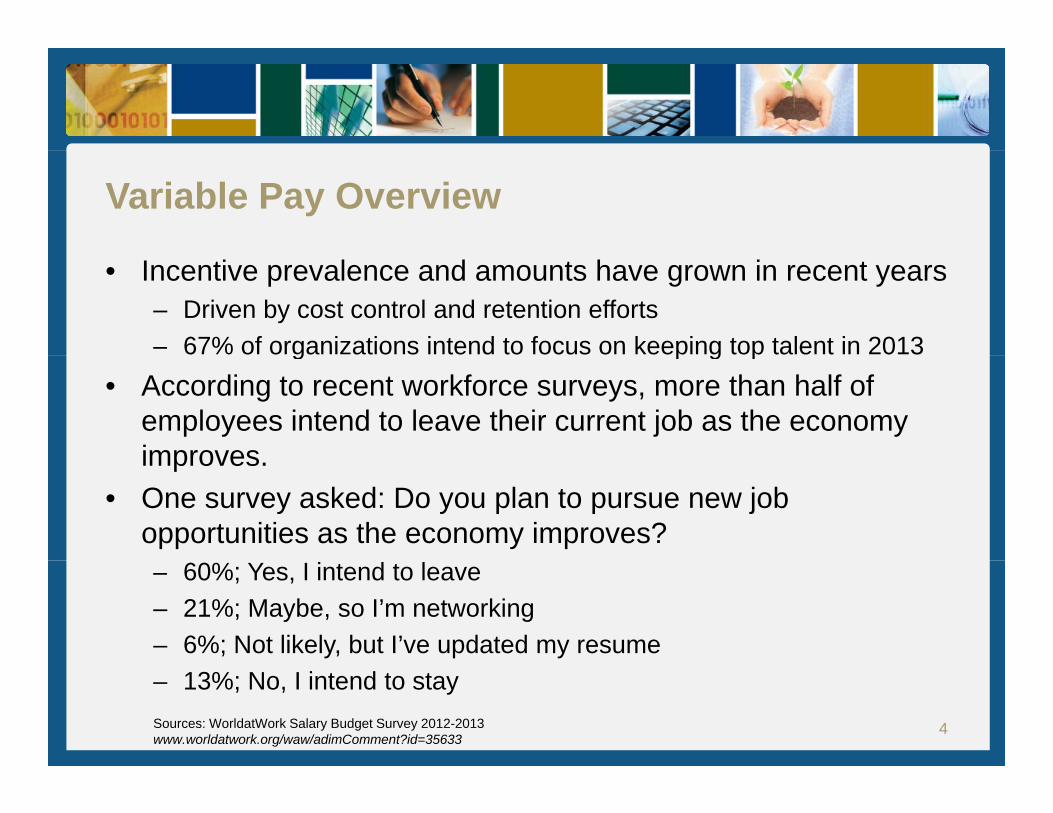

• Incentive prevalence and amounts have grown in recent years– Driven by cost control and retention efforts– 67% of organizations intend to focus on keeping top talent in 2013g p g p

• According to recent workforce surveys, more than half of employees intend to leave their current job as the economy improvesimproves.

• One survey asked: Do you plan to pursue new job opportunities as the economy improves? – 60%; Yes, I intend to leave – 21%; Maybe, so I’m networking – 6%; Not likely, but I’ve updated my resume – 13%; No, I intend to staySources: WorldatWork Salary Budget Survey 2012-2013www.worldatwork.org/waw/adimComment?id=35633

4

Click to edit Master title styleTypes of Incentive Plans

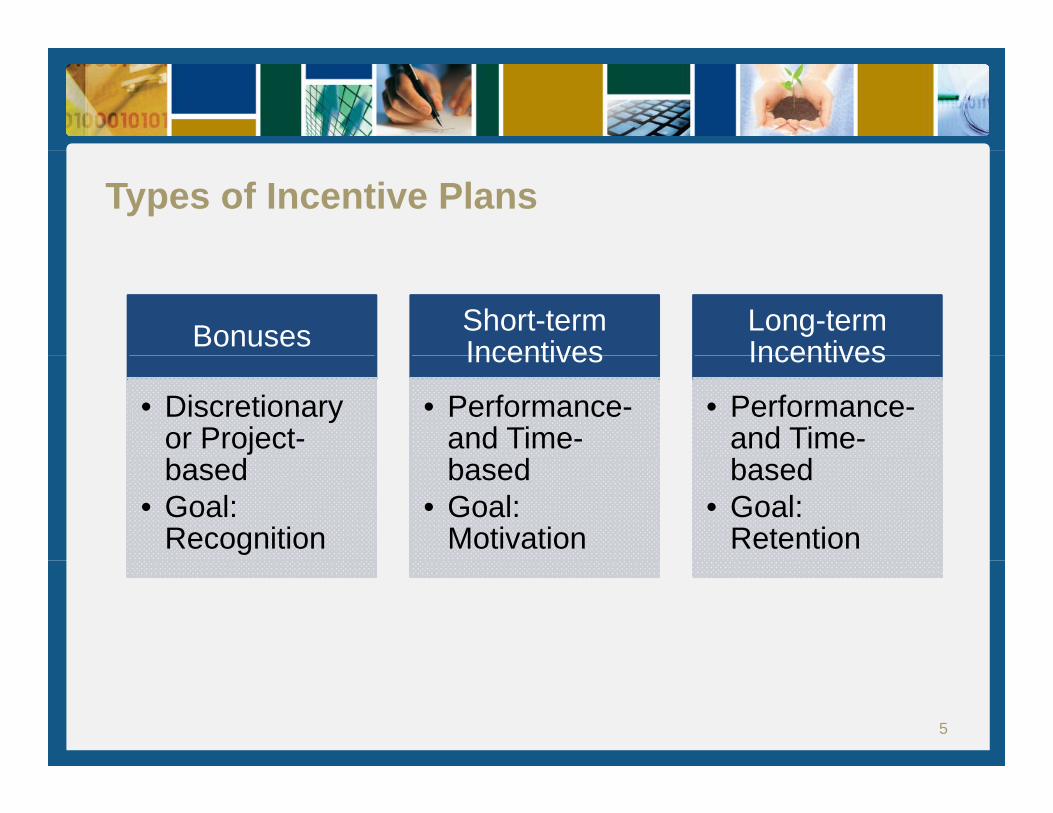

Bonuses Short-term Incentives

Long-term Incentives

• Discretionary or Project-

Incentives

• Performance-and Time-

Incentives

• Performance-and Time-

based• Goal:

Recognition

based• Goal:

Motivation

based• Goal:

Retention

5

Click to edit Master title styleIncentive Eligibility

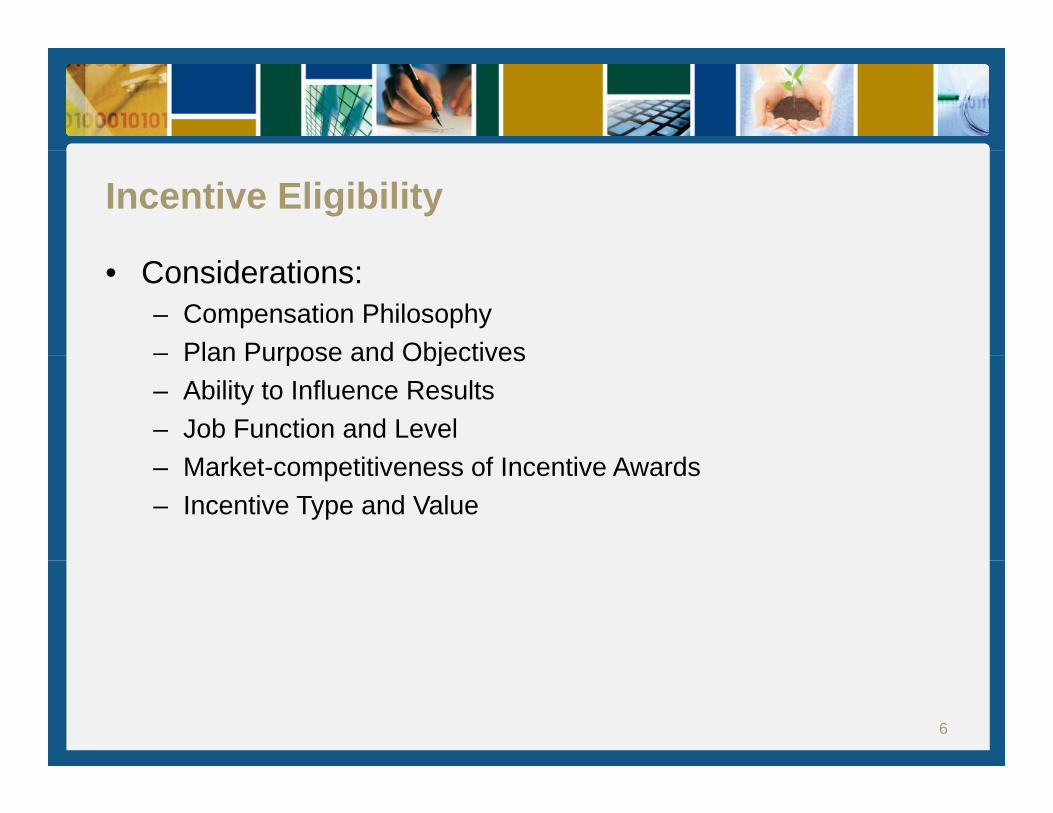

• Considerations:– Compensation Philosophy– Plan Purpose and ObjectivesPlan Purpose and Objectives– Ability to Influence Results– Job Function and Level

M k t titi f I ti A d– Market-competitiveness of Incentive Awards– Incentive Type and Value

6

Click to edit Master title styleIncentive Eligibility

• Non-exempt Employee Incentives1. Ensure employees are properly classified as exempt or

nonexemptp2. Assess appropriateness of extending bonus programs to

nonexempt employees3 If incentives are provided to non-exempt employees determine:3. If incentives are provided to non exempt employees, determine:

• Retroactive overtime or • Incentive as a percentage of total earnings

7

Click to edit Master title stylePay Mix

• Base salary: The annual fixed rate that an individual is paid for performing a job.

• Short-term/Annual incentives: At-risk cash compensation awarded to employees on an annual or more frequent basis The sum of base salary andemployees on an annual or more frequent basis. The sum of base salary and short-term incentives is typically defined as total cash compensation.

• Benefits: Non-cash compensation provided to an employee. Some benefits are required by law (e.g., payroll taxes, unemployment compensation and workers compensation) while others may be provided at the discretion of an employer (e.g., medical care, life insurance, paid time off, retirement plans, etc.).

• Perquisites: Any benefit that is offered to only a subset of the broader employee population. Prevalent perquisites include a company car,employee population. Prevalent perquisites include a company car, supplemental life and/or medical insurance and country club dues.

• Long term incentives: Compensation (cash, stock, phantom stock, etc.) typically earned as a bonus for performance which is measured over a multi-

i d (t i ll 3 5 )year period (typically 3-5 years).

8

Click to edit Master title stylePay Mix – Illustration

Non-Executive Executive

Base SalaryAnnual IncentivesIncentivesBenefits & PerquisitesLong-term gIncentives

9

Click to edit Master title stylePerformance Measures

• Corporate vs. Individual• Qualitative vs. Quantitative

• Corporate and individual performance measures should be weighted by the relative ability to impact performanceg y y p p

Recommended Target Bonus Payout

Job Level (% of Base Salary) Corporate IndividualC-Suite 40.0% 100% 0%

% Based On Goals

C Suite 40.0% 100% 0%Vice Presidents 25.0% 80% 20%Middle Management 18.0% 60% 40%Supervisors 12.0% 40% 60%Professional Staff 10.0% 20% 80%Hourly Staff 5.0% 0% 100%

10

Click to edit Master title stylePerformance Measures

• Corporate Measures– Financial

• Examples: Sales growth, Profitability, Stock PriceExamples: Sales growth, Profitability, Stock Price– Customer Satisfaction

• Examples: Product Development and Promotion, Customer FeedbackFeedback

– Process Improvement• Examples: Quality Enhancement and Controls, Productivity

Corporate measures are generally limited to 3 5• Corporate measures are generally limited to 3-5

11

Click to edit Master title stylePerformance Measures

• Financial

Revenue Growth Revenue Growth Profitability Cash Flow-Revenue Growth

-Raising Capital

-Revenue Growth

-Profitability

-Cash Flow

-Return Measures

-Profitability

-ROC

-Cash Flow

-Cost Control

-Cash Flow

-ROC

-Cost Control

12

Click to edit Master title stylePerformance Measures

• Customer Satisfaction

Brand Awareness Market Share Maintain Market Customer-Brand Awareness

-Market Penetration

-Customer Satisfaction

-Market Share Growth

-Production Ramp-up

-Maintain Market Share

-Customer Perceptions

-Customer Retention

-Product Revitalization

13

Click to edit Master title stylePerformance Measures

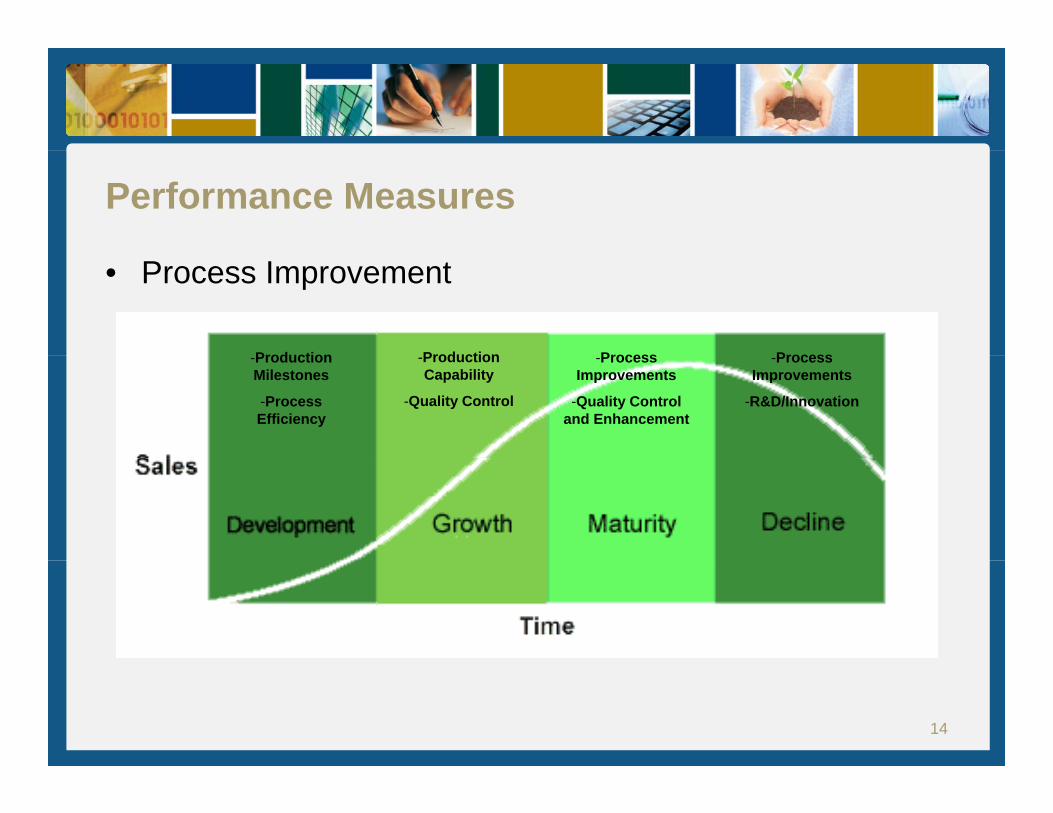

• Process Improvement

Production Production Process Process-Production Milestones

-Process Efficiency

-Production Capability

-Quality Control

-Process Improvements

-Quality Control and Enhancement

-Process Improvements

-R&D/Innovation

14

Click to edit Master title stylePerformance Measures

• Individual Measures– Production– QualityQuality– Customer Service– Competencies

J b P f– Job Performance– Personal Goals

• Team or Department Measuresp

15

Click to edit Master title styleAward Amounts

• Incentive awards should be competitive and meaningful• Award type and payout timing may impact amounts

P f h ld tli diff t i ti• Performance measures should outline different incentive payout amounts– Threshold Stretch

– Target– Stretch/Maximum

Targetwar

d Le

vel

Threshold

No Incentive Paid

Ince

ntiv

e A

w

16Target StretchThreshold

Performance Level

Click to edit Master title styleAward Amounts

• Incentive award amounts should reflect the total compensation philosophy– Who does the organization attract employees from and loseWho does the organization attract employees from and lose

employees to? (i.e., “the market”)– How should the organization compare to the market?

V i b d t d t i t• Various resources may be used to determine amounts– Published compensation surveys– Competitive peer data– Historical incentive awards

17

Click to edit Master title styleAward Amounts

• Determining competitive incentive amounts begins with a market assessment of each job or job group

Job Documentation

Market Matches

18

Click to edit Master title styleAward Amounts

• Market Pricing is the valuation of pay for jobs in the external labor markets

– Key considerations when determining labor markets:Key considerations when determining labor markets: • Location

o Localo Regiono Nation

• Industryo Industry specifico Broad spectrum of employerso Broad spectrum of employers

• Organization Sizeo Revenues/Operating Budgeto Full-time Equivalent Employees or Headcounto Full time Equivalent Employees or Headcount

19

Click to edit Master title styleAward Amounts

• Reliable Data– Published survey data

• Major consulting and surveying firmsj g y g• Statistically validated• Standard deviation analysis of data

• Unreliable data examples:Unreliable data examples:– Self-reported– DOL

Data from one or two competitors– Data from one or two competitors

20

Click to edit Master title styleAward Amounts – Annual Incentives

• Incentive Plan Funding– Budgeted– Self-fundedSelf funded

• Funding Considerations:– Hurdles– Payout Scenarios

(Worst Case and Windfalls)

21

Click to edit Master title styleAward Amounts – Annual Incentives

• Market Pricing Example

Job: Branch ManagerJob: Branch Manager

Compensation Element

Median Published Survey Data Average Market DataSurvey #1 Survey #2 Survey #3

Base Salary $101,000 $108,000 $105,000 $104,667y $ , $ , $ , $ ,

Total Cash Compensation $119,000 $123,500 $125,750 $122,750

Annual Incentive $18,000 $15,500 $20,750 $12,834

Annual Incentive (% of Base Salary) 17.8% 14.4% 19.8% 17.3%

22

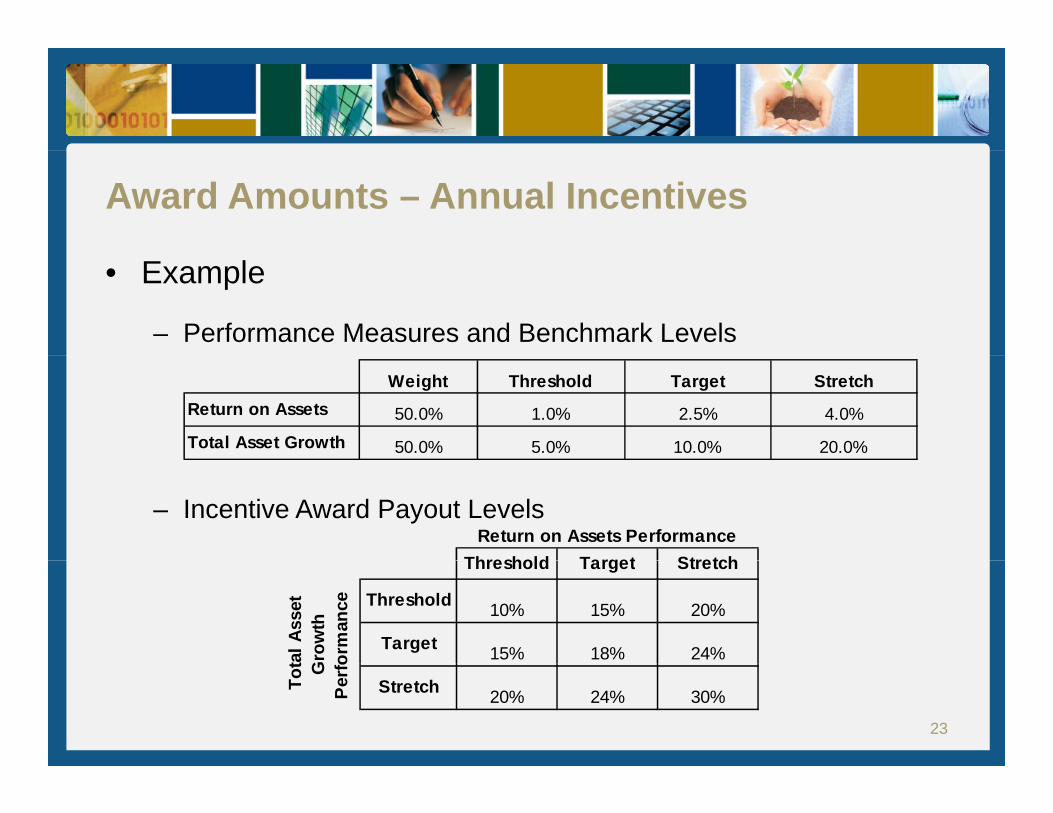

Click to edit Master title styleAward Amounts – Annual Incentives

• Example

– Performance Measures and Benchmark Levels

Weight Threshold Target StretchReturn on Assets 50.0% 1.0% 2.5% 4.0%Total Asset Growth 50.0% 5.0% 10.0% 20.0%

– Incentive Award Payout Levels

Threshold Target StretchReturn on Assets Performance

Threshold Target Stretch

Threshold 10% 15% 20%

Target 15% 18% 24%tal A

sset

G

row

th

orm

ance

23

Stretch 20% 24% 30%

Tot G

Perfo

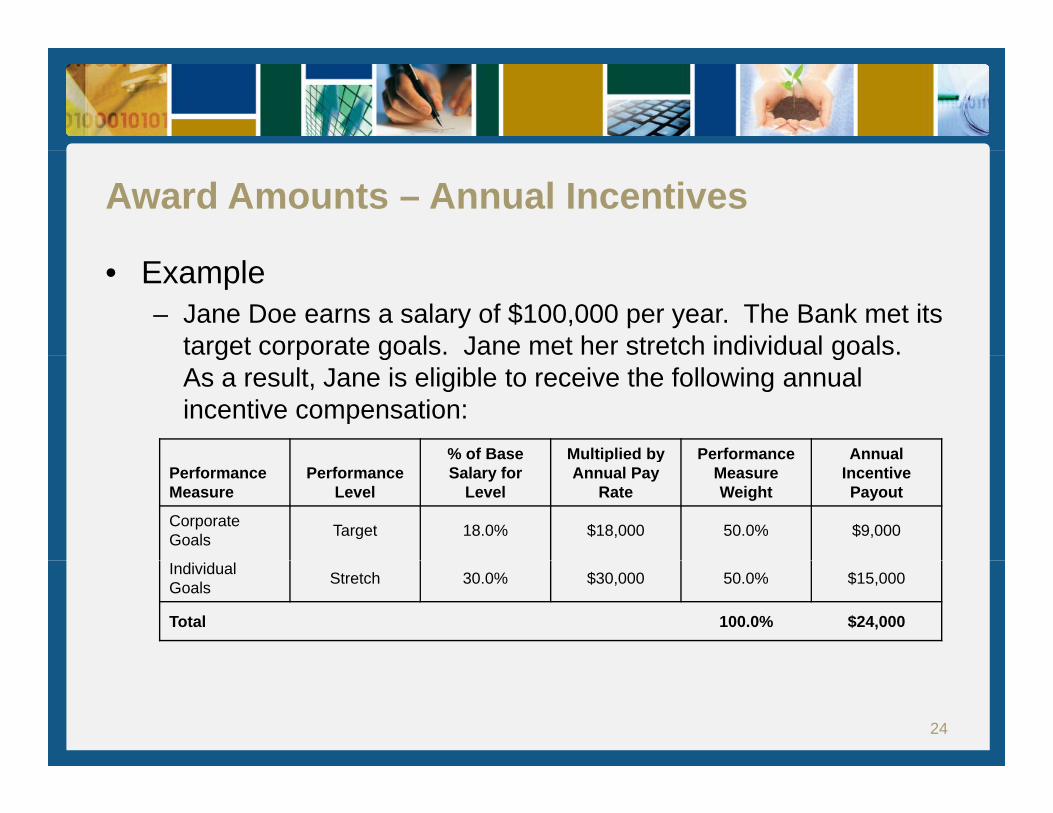

Click to edit Master title styleAward Amounts – Annual Incentives

• Example– Jane Doe earns a salary of $100,000 per year. The Bank met its

target corporate goals. Jane met her stretch individual goals. g p g gAs a result, Jane is eligible to receive the following annual incentive compensation:

% of Base Multiplied by Performance AnnualPerformance Measure

Performance Level

% of Base Salary for

Level

Multiplied by Annual Pay

Rate

Performance Measure Weight

AnnualIncentive Payout

Corporate Goals Target 18.0% $18,000 50.0% $9,000

Individual Goals Stretch 30.0% $30,000 50.0% $15,000

Total 100.0% $24,000

24

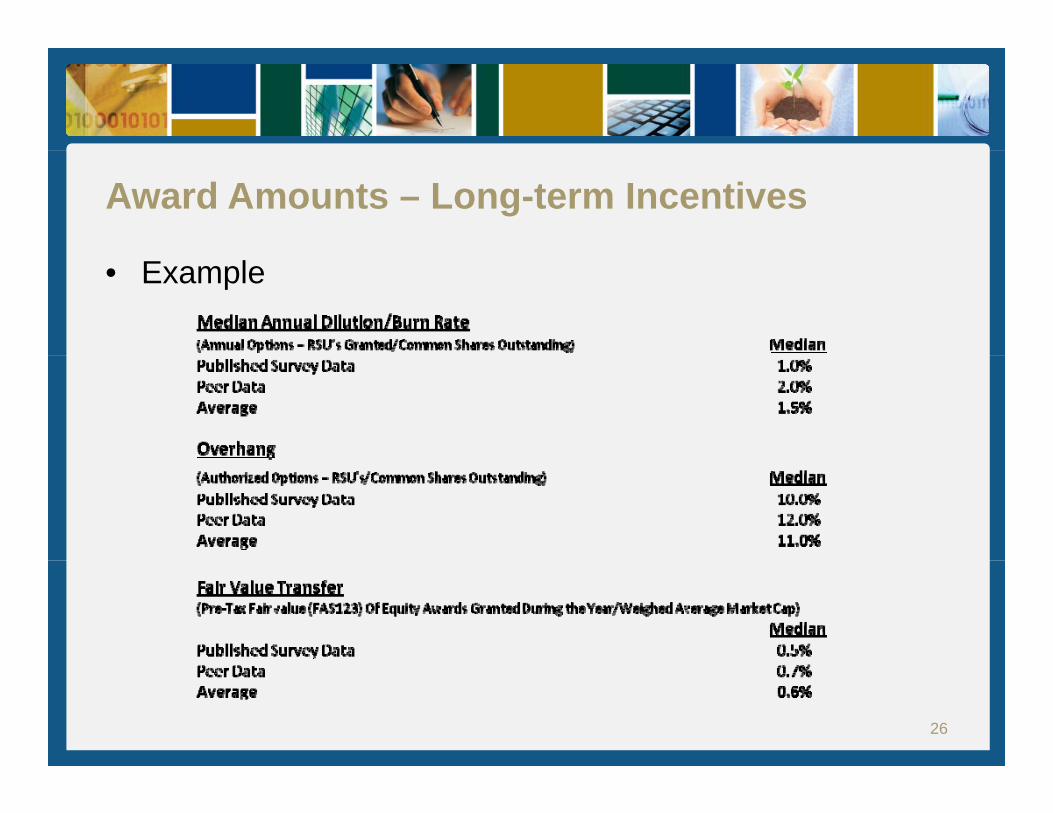

Click to edit Master title styleAward Amounts – Long-term Incentives

• Annual Dilution/Burn Rate: A snapshot of the relative use of shares within the greater scope of shares outstanding. It is calculated by dividing the annual shares granted (net of

ll ti ) b th t t l b f h t t dicancellations) by the total number of shares outstanding. • Overhang: The decrease in ownership percentage of current

owners when additional shares of stock are issued calculated th b f t t di t k t ( i d/as the number of outstanding stock grants (unexercised/

granted options, unvested stock awards, etc.) plus the number set aside for future grants, expressed as a percentage of the total shares outstandingpercentage of the total shares outstanding.

• Fair Value Transfer: A measurement of the pre-tax “fair value” of equity awards granted during the year expressed as a percentage of weighted-average market capitalizationa percentage of weighted-average market capitalization.

25

Click to edit Master title styleAward Amounts – Long-term Incentives

• Example

26

Click to edit Master title styleAward Amounts – Long-term Incentives

• Burn rate and overhang progression are becoming less meaningful as the market shifts away from options and toward whole-share LTI vehicles (e g restricted stock ortoward whole share LTI vehicles (e.g., restricted stock or performance shares)

• As a result, the Fair Value Transfer methodology of evaluating market-competitive long-term incentive levels is growing in popularity

• Once the long-term incentive pool is determined aOnce the long term incentive pool is determined, a distribution schedule must be developed

27

Click to edit Master title styleAward Amounts – Long-term Incentives

• Vesting period:– Cliff – For example, 100% vested three years after the grant– Installment – For example 25% vested each year after grantInstallment For example, 25% vested each year after grant– Typical vesting period is 3-5 years

Y 1 52 3 64 7 8 9 10Year 1 52 3 64 7

Annual

1-32-4

3 5

8 9 10

Annual Overlapping

3-54-6

5-76-8

7-9

28

7 98-10

Click to edit Master title styleIncentive Plan Communication

Communication is critical!• Performance measures should be established prior to or

at the beginning of the periodat the beginning of the period• Distribute plan document to employees• Share progress frequentlyShare progress frequently• Provide periodic feedback on individual performance• Announce results in advance of awards

29

Click to edit Master title styleIncentive Plan Effectiveness

• Evaluating the incentive plan’s effectiveness should begin several months before the next performance periodperiod

• Consider all stakeholder perspectives• Possible Results of Evaluation:

– Continuance– Refinement– Termination– Termination

30

Click to edit Master title styleIncentive Plan Do’s and Don’ts

Don’t: Charge HR with full responsibility for the incentive plan.

Do: Gain top management support and promotion of the plan.p

Leadership Team

Middle Management Supervisors Employees

31

Click to edit Master title styleIncentive Plan Do’s and Don’ts

Don’t: Establish complex performance measures that are difficult to calculate and understand.

Do: Set performance measures that are “SMART.”

• Specific – Measures are clearly defined• Measurable – Able to assess via quantitative or qualitative metrics• Accountable – Employee can impact the resultp y p• Realistic – Based on appropriate goal and benchmark setting• Timely – Measure monthly, quarterly, annually

32

Click to edit Master title styleIncentive Plan Do’s and Don’ts

Don’t: Use corporate performance measures that do notreinforce business goals.

Do: Focus on metrics that are relevant to organizationalstrategies and objectives.g j

33

Click to edit Master title styleIncentive Plan Do’s and Don’ts

Don’t: Reward activity with incentive compensation.

Do: Adhere to incentive plan goals that are results-basedDo: Adhere to incentive plan goals that are results-based.

A ti it BaseActivity Base Pay

Activity Successful Outcomes

Incentive Pay

34

y Outcomes Pay

Click to edit Master title styleIncentive Plan Do’s and Don’ts

Don’t: Payout incentives that are too high or too low.

Do: Pay incentives that are market-competitive andDo: Pay incentives that are market-competitive and well-aligned with performance.

Above Market

Below M k t

35

Market

Click to edit Master title styleIncentive Plan Do’s and Don’ts

Don’t: Fail to communicate the incentive plan terms and criteria.

Do: Communicate the plan early and often.

36

Click to edit Master title styleAdditional Considerations

B S l P• Base Salary Program– Foundation of compensation administration– Importance of external competitiveness and internal equity

• Sales Compensation• Sales Compensation– Pay the winners like winners and the losers like losers– Commissions and sales incentives are used to reward performance

• Performance Management• Performance Management– Administer pay for performance– Calibration of scores– Data driven decisions

• Fair Pay– Recent legislation– Varying statistical recommendations for analysis– Ensures pay system has been administered fairly

37

Click to edit Master title style

Questions?Priya J. Kapila, CCP, SPHR

CBIZ Human Capital Services(800) 844 4510(800) 844-4510