income splitting: opportunities & pitfalls - cch

TRANSCRIPT

Income Splitting: Opportunities & PitfallsJoan E. Jung, Partner, Michael A. Goldberg, Partner, Samantha A. Prasad, Partner, and Matthew D. Getzler, Associate – Minden Gross LLP

1

Personal Attribution Rulesand Kiddie Tax

Joan Jung

2

3

Attribution Rules – The Basics

• Generally applicable to the transfer and loan of property by an individual to a spouse or common-law partner (“CL partner”) and non-arm’s length minors (including nieces and nephews)

• Applicable to the period throughout which the individual (transferor) was resident in Canada

• Where applicable, the rules operate:– to prevent income splitting in respect of income from

property– to attribute income and also to attribute losses

Attribution Rules – Relevant ITA sections

• s.74.1(1) income attribution with reference to spouse and CL partner

• s.74.1(2) income attribution with reference to non-arm’s length minor; niece or nephew

• s.74.2 capital gain/loss attribution with reference to spouse or CL partner

• s.74.3 transfers to a trust for the benefit of spouse, CL partner, non-arm’s length minor, niece or nephew

4

Critical Words

• “Where an individual has lent or transferred property … either directly or indirectly, by means of a trust or by any other means whatever, to or for the benefit of …”

5

“Lent or transferred property“

• Fasken Estate 49 DTC 491 (Exch. Ct.) • “The word "transfer" is not a term of art and has not a

technical meaning. It is not necessary to a transfer of property from a husband to his wife that it should be made in any particular form or that it should be made directly. All that is required is that the husband should so deal with the property as to divest himself of it and vest it in his wife, that is to say, pass the property from himself to her. The means by which he accomplishes this result, whether direct or circuitous, may properly be called a transfer.”

6

Transfer - KieboomConcerns

• Transfer of property– s. 248(1), ITA: “… includes a right of any kind whatever

…”– Economic interest?

• See The Queen v. Kieboom 92 DTC 6382 (FCA)– Undervaluation constitutes a transfer?

• See CRA Document No. 2010-0366301I7; Interpretation Bulletin IT-511R, paragraph 1

7

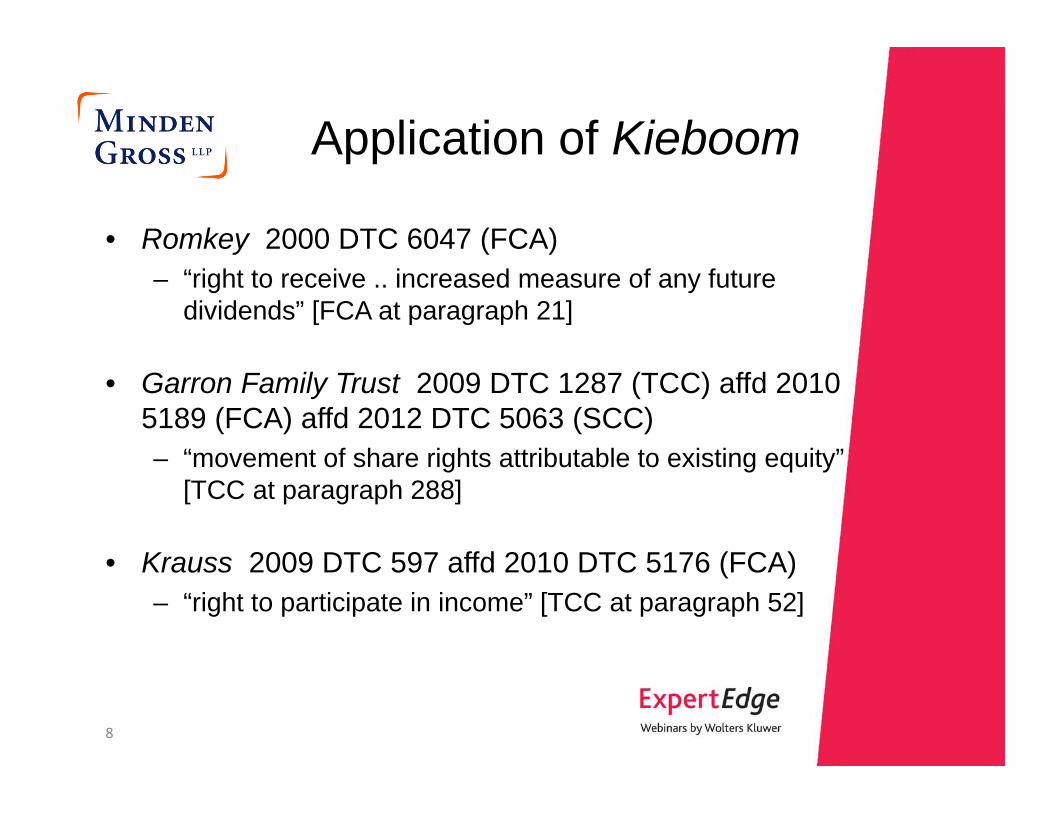

Application of Kieboom

• Romkey 2000 DTC 6047 (FCA)– “right to receive .. increased measure of any future

dividends” [FCA at paragraph 21]

• Garron Family Trust 2009 DTC 1287 (TCC) affd 2010 5189 (FCA) affd 2012 DTC 5063 (SCC)– “movement of share rights attributable to existing equity”

[TCC at paragraph 288]

• Krauss 2009 DTC 597 affd 2010 DTC 5176 (FCA)– “right to participate in income” [TCC at paragraph 52]

8

Directly or indirectly … by any other means whatever

• Garron Family Trust [FCA at paragraph 79]• “Once it is accepted that an indirect transfer of the

shares of a corporation from Shareholder A to Shareholder B can be achieved by a corporate reorganization that shifts part of the value of the corporation from the class of shares owned by Shareholder A to the class of shares owned by Shareholder B, I see no principled basis for concluding that the same transaction cannot also be an indirect transfer of property “in any manner whatever” to the person that owns Shareholder B.”

9

Directly or indirectly … by any other means whatever

• Garron Family Trust considered s. 94, ITA rather than the attribution rules, but similar wording– Implies looking through corporations– See also St – Pierre and Lafontaine v. The Queen 2008

DTC 3730 (TCC) affd 2008 DTC 6639 (FCA)

10

Extended application –subsection 74.1(3), ITA

• Where the transferred or loaned property is used to either repay borrowed money that was used to acquire property or to reduce an amount payable for that property

• s. 74.1(1) or (2) will apply to income/loss thereafter on a proportionate basis, based on FMV of loaned/transferred property to the cost of the property acquired

11

Extended application –subsection 74.1(3), ITA

12

Arm’s length lender

1. LoanTaxpayer who acquires income producing property

Taxpayer’s spouse

2. Gift3. Gift used to repay loan

Extended application –subsection 74.5(7), ITA

• Guaranteeing loans (or interest thereon) made by third party to a “specified person” as defined in s.74.5(8)– Includes spouse, CL partner, non-arm’s length minor

(including niece or nephew)– Includes a corporation (other than SBC) of which any of

the above is a “specified shareholder”• If applicable, property loaned by third party to

“specified person” deemed to be loaned by the individual

13

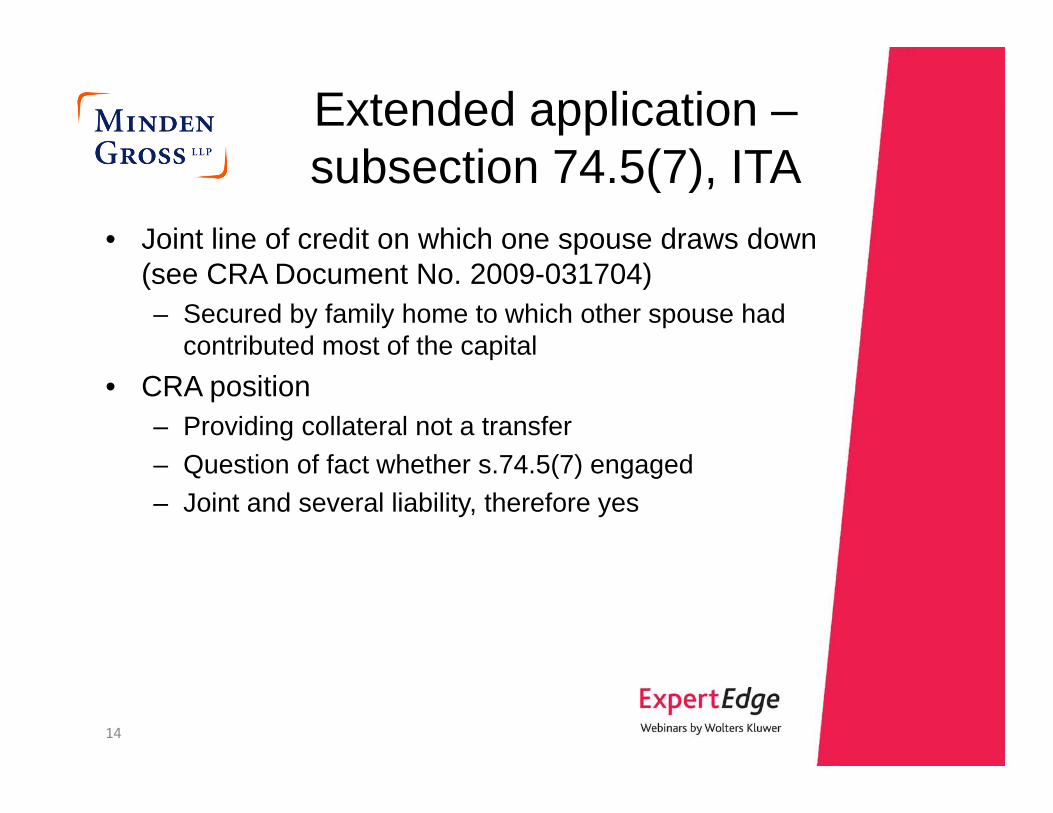

Extended application –subsection 74.5(7), ITA

• Joint line of credit on which one spouse draws down (see CRA Document No. 2009-031704)– Secured by family home to which other spouse had

contributed most of the capital• CRA position

– Providing collateral not a transfer– Question of fact whether s.74.5(7) engaged– Joint and several liability, therefore yes

14

Extended application –subsection 74.5(6), ITA

• Sometimes referred to as intermediary rule or back to back rule, but broader– No series concept (see St-Pierre and Lafontaine 2008

DTC 3730 (TCC) affed 2008 DTC 6639 (FCA)) • s. 74.5(6)(b) requires property transferred to another

person “on condition” that property (not necessarily the same property) be transferred or lent directly or indirectly to or for the benefit of a “specified person”

15

Extended application –subsection 74.5(6), ITA

• But s.74.5(6)(a) does not require a transfer “on condition”– Where an individual has transferred or lent property and

that property (or property substituted therefor) is transferred or lent by any person (not necessarily the person to whom the individual transferred or lent) directly or indirectly to or for the benefit of a “specified person”

16

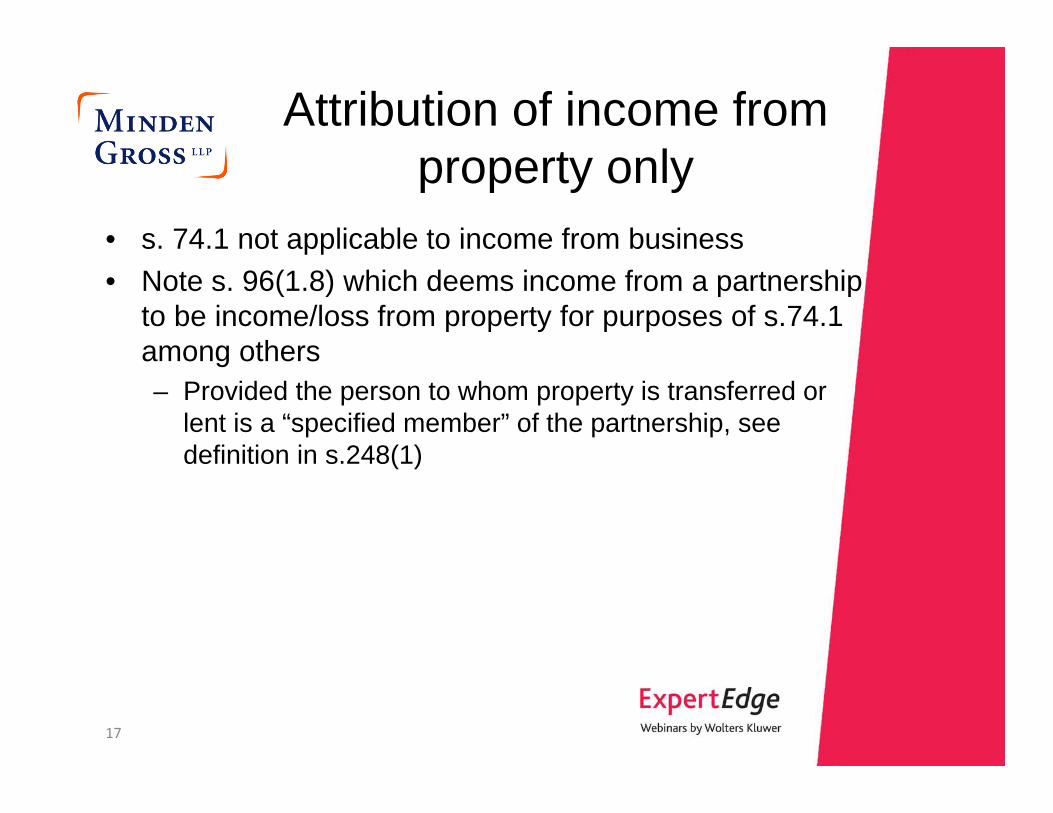

Attribution of income from property only

• s. 74.1 not applicable to income from business• Note s. 96(1.8) which deems income from a partnership

to be income/loss from property for purposes of s.74.1 among others– Provided the person to whom property is transferred or

lent is a “specified member” of the partnership, see definition in s.248(1)

17

Section 74.2 - Disposition of property?

• s. 74.2 deems an amount to be the transferor spouse’s taxable capital gain or allowable capital loss from the disposition of property

• Can transferor potentially claim capital gains exemption on the attributed taxable capital gain?– Yes, see s.74.2(2)

• Can transferor potentially claim ABIL on the attributed allowable capital loss?– No, see CRA Document Nos. 9621015 and 931818

18

When does attribution cease?

• Generally if the individual transferor ceases to be resident in Canada

• In the case of minors, s. 74.1(2) ceases to apply in the year in which the recipient (i.e., the person to whom property was loaned or transferred) attains age 18– But beware s.56(4.1) which may apply to loan

19

When does attribution cease?

• In the case of spouse or CL partner, s.74.5(3) may apply if living separate and apart– Note election required under s.74.5(3)(b) with respect to

capital gains attribution under s.74.2 • Repayment of loan to cease attribution requires

repayment with the original loaned property or property substituted therefor– See 1993 Revenue Canada Round Table, Q.36

20

Section 160 - Joint and several liability

• Assuming transfer of property• s.160(1)(d): joint and several liability for any increase

in transferor’s Part I tax liability resulting from inclusion of attributed income under s.74.1-75.1

• s.160(1)(e): joint and several liability for any tax liability of transferor for the year of transfer or preceding year to extent that FMV of transferred property exceeded FMV of consideration (if any)

21

Section 120.4 – Tax on split income

• General rule : increases to 29% rate on “split income” of a “specified individual” with no credits other than dividend tax credit and foreign tax credit, s.120.4(2) and (3)

• If applicable:– Attribution rules in s.74.1, 74.3 and 75(2) do not apply,

s.74.5(13)– Rules in s.56(2), (4) and (4.1) do not apply, s.56(5)

22

Section 120.4 – Tax on split income

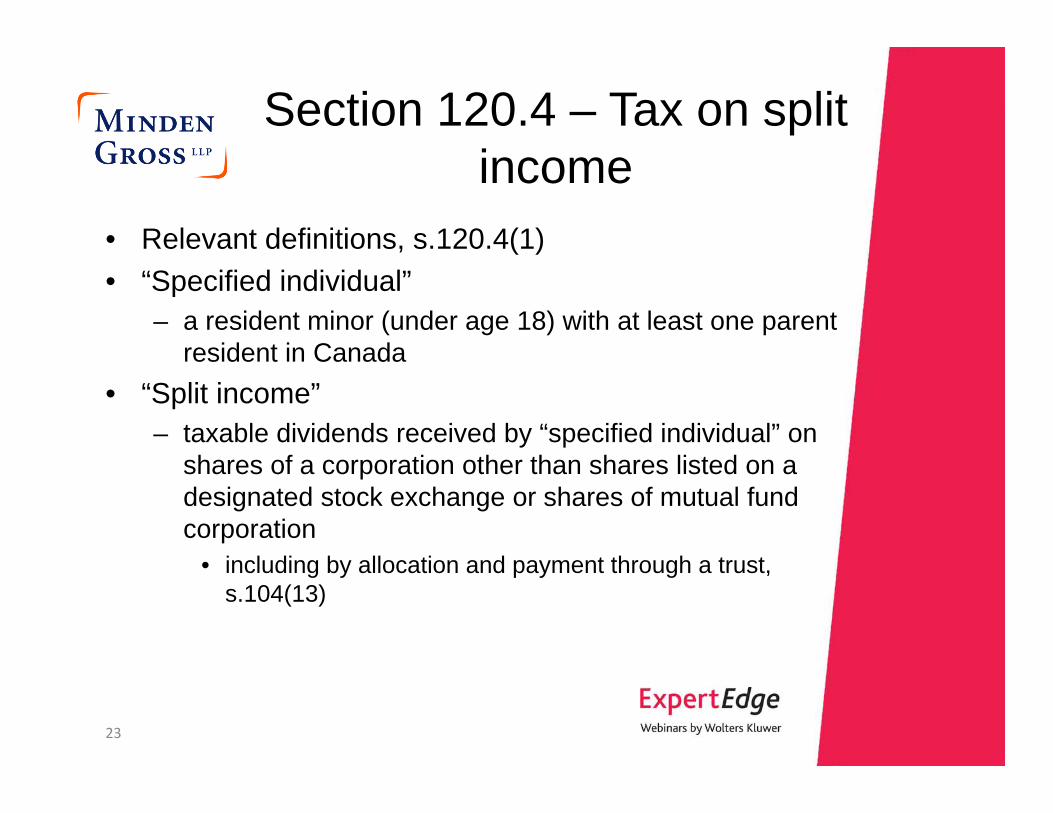

• Relevant definitions, s.120.4(1)• “Specified individual”

– a resident minor (under age 18) with at least one parent resident in Canada

• “Split income”– taxable dividends received by “specified individual” on

shares of a corporation other than shares listed on a designated stock exchange or shares of mutual fund corporation

• including by allocation and payment through a trust, s.104(13)

23

Section 120.4 – Tax on split income

– Amounts included in income of a “specified individual” under s.15 as a benefit or loan, because of ownership by any person of shares of a corporation (excluding listed shares)

– Amounts included in income from a partnership or trust to extent that amounts are derived from provision of goods or services by the partnership or trust to or in support of a business carried on by:

• a person related to the specified individual at any time in the year

• a corporation of which a related person is a “specified shareholder” at any time in the year

• a professional corporation of which a related person is a shareholder at any time in the year

24

Section 120.4 – Tax on split income

• “Split income” definition proposed to be amended by Federal Budget 2014– To include income that is paid or allocated to a “specified

individual” from a partnership or trust which is derived from a business or rental of property if a related person:

• Actively engaged on a regular basis in activity of the particular partnership or trust of earning income from business or rental of property

• In the case of a partnership, has an interest in the partnership

25

Section 120.4 – Tax on split income

• “Excluded amount”– Applicable if property giving rise to the income or

capital gain which would otherwise be “split income” was acquired by the individual as a consequence of death of:

• parent• any other person, where the individual is a full time

student at a post-secondary institution or eligible for the disability tax credit in the year

26

Section 120.4 – Tax on split income

• Transmogrification rule in s.120.4(4)– Capital gain from disposition of unlisted shares to a

person non-arm’s length with the “specified individual” deemed to be a taxable dividend and not a capital gain

• Joint and several liability of “specified individual” and parent, s.160(1.2)

27

Corporate Attribution Rules

Samantha Prasad

28

Corporate Attribution RulesSection 74.4

• S.74.4: Conditions– Transfer/loan of property to company either directly or

indirectly by means of a trust or otherwise• Transfers can include corporate reorganizations where

as part of the transaction, shares are transferred or exchanged

– One of the main purposes is to reduce transferor’s income and benefit a “designated person”

• Designated person: spouse, or child, niece, nephew or other non-arm’s length person who has not reached the age of 18 in the year

• Designated person must be a “specified shareholder” of company (i.e. who owns directly or indirectly 10% of more of the issued shares of any class at any time)

29

Effect of Corporate Attribution Rules

• S. 74.4(2): Taxable benefits, based on prescribed interest rates applied to the “outstanding amount” (per s.74.4(3)) of the loan/transfer will apply for periods throughout which:– person is a “designated person” and a “specified shareholder”– Transferor is a Canadian resident– Corporation is not a small business corporation

• This deemed income inclusion can potentially result in double taxation

30

Corporate Attribution Rules

• When can the corporate attribution rules apply?– Estates freezes – Interest-free loan to corporation– “Derivative transfers” (Back to back

transfers)

31

Estate Freezes

• Typically involves a transfer of shares to a holding company or exchange of shares as part of a reorganization of the capital of a company

• Designated persons usually receive new growth shares in corporation

32

Opco

MinorKids

Parent

Opco

Holdco

Parent MinorKids

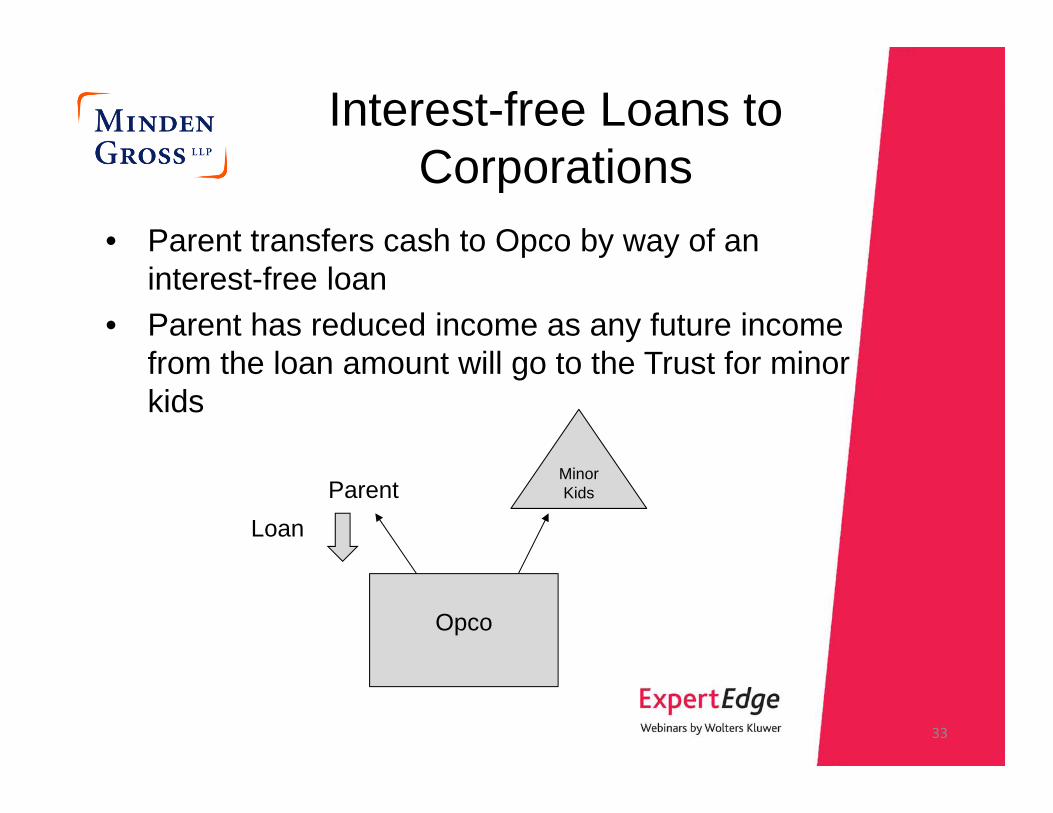

Interest-free Loans to Corporations

• Parent transfers cash to Opco by way of an interest-free loan

• Parent has reduced income as any future income from the loan amount will go to the Trust for minor kids

33

Opco

MinorKidsParent

Loan

Derivative Transfer

• Can extend the application of the corporate attribution rules

• Husband lends property to Opco 1 • Opco then lends to Opco 2 which is wholly owned

by wife

34

Opco 1

Husband Wife

loan

Opco 2

Exceptions to the Corporate Attribution Rules

• Small Business Corporation Status– CCPC, all or substantially all (90%) of the FMV of

assets of which (at any particular time) is attributable to assets that are used principally (50%) in an active business carried on primarily in Canada

– Easy to go offside the 90% test

– If offside, corporate attribution rules will apply throughout the period during which corporation is offside

35

Exceptions to the Corporate Attribution Rules

• S. 74.4 Clause inserted in Trust – Track to wording of the actual clause

– Will lose ability to distribute to the spouse during marriage

– Will restrict ability to multiply the capital gains exemption through the Trust

– Drafting tricks? CRA has said you need a blanket prohibition so cannot draft to say s.74.4 clause not applicable while Opco is a small business corporation or while transferor is non-resident

36

Avoiding the Corporate Attribution Rules

• Situations where Corporate Attribution Rules are not triggered– Start-Up situations

• Corporate attribution rules are limited to the value of the corporate at the time of the “reorganization”

• No real value at the time of a start-up

37

Avoiding the Corporate Attribution Rules

• Stock Dividend Freeze– No transfer – Freeze shares are issued by corporation

38

Opco

Parent

New freeze shares

Minor Kids

Avoiding the Corporation Attribution Rules

• Reverse Freeze – A Technical Escape? – Transfer of assets from Opco to new Subco– Issuance of freeze shares from Subco to Opco on transfer– New growth shares of Subco issued to Trust– No “transfer” by individual in respect of a designated person;

rather only a transfer between corporations– Beware of bonusing down and parent lends back to the

corporation

39

Parent

Minor Kids

Opco

Subco

Effective Use of Trusts In Income Splitting

Michael Goldberg

40

Effective Use of Trusts In Income Splitting

• Trust Basics– Income splitting– Capital gains exemption multiplication

• Specific income splitting opportunities– Prescribed rate loans– Testamentary trusts– Ontario surtax planning– Alberta trusts– S.94(1) trusts

41

Trust Basics

• It’s not all about tax– Effective management and administration of

property for a trust’s beneficiaries

• But focus today – income splitting

42

Tax Effective Use of Trusts

• Outright transfers v. transfer in trust– Generally possible to enjoy similar tax

benefits• Income splitting• Capital gains exemption (“CGE”)

multiplication– But many non-tax advantages of trusts

• Control • Flexibility

43

Outright Transfers v. Transfer in Trust

• Freeze: shares issued to spouse & kids– Tax Benefits similar to using a trust

• Income splitting • CGE multiplication

– Simple to implement and maintain but• Lose flexibility of making changes to

ownership • Incapable beneficiaries• Exposure to creditors• Expanded ownership rights

44

Trust Technical Taxation Basics

• Income splitting is possible because– Trust deed:

• Empowers trustees to make broad discretionary allocations of income and capital

• Defines income as income for ITA purposes

45

Trust Technical Taxation Basics

• If a deed does not define income then income has meaning under trust law– Does not include capital gains or “deemed”

(phantom) income for ITA purposes such as:• Deemed dividends (e.g., on redemption)• Deemed capital gains (e.g., on 21st

anniversary)• May not be able to allocate deemed income

to beneficiaries– Capital encroachment powers may assist

46

Trust Technical Taxation Basics

• Income splitting is possible because– S.104(13)

• Amounts “payable” to beneficiary taxed to beneficiary

– Payable – either paid or legally enforceable right of beneficiary in the year s. 104(24)

• Trust gets a deduction s.104(6), – Losses cannot be allocated to beneficiaries

47

Trust Technical Taxation Basics

• Income splitting is possible because– Many technical rules in s.104 ensure

income maintains character when allocated including as:

• Dividends (s.104(19))• CDA (s.104(20))• Capital gains eligible for CGE (s.104(21) &

s.(21.2))

48

Trust Technical Taxation Basics

• Multiplying the CGE– Direct share ownership

• Loss of control and flexibility– Discretionary family trust

• CGE flow-through rules (s.104(21) & s.(21.2))

49

Trust Technical Taxation Basics

• Special income splitting rules where amounts are not payable– S.104(14) – preferred beneficiary election

• Application limited to disabled beneficiaries since 1995

50

Trust Technical Taxation Basics

• Special income splitting rules where amounts are not payable– S.104(18) – Age 40 Trusts

• Income of the trust in year not made payable• Held in trust for an individual who has not

turned 21 in year• Individual’s rights vest in year not because of

exercise or failure to exercise discretion• Rights not subject to condition other than

individual survive to an age not exceeding 40

51

Trust Technical Taxation Basics

• Allocations and Distributions in Breach– Income will remain taxable in trust – Rollout under s.107(2) will be denied– Recipient may be subject to tax under

S.105(1)

52

Prescribed Rate Loan Planning

• No interest/low interest loans to benefit certain NAL persons may be subject to personal attribution rules– Exception for “Loans for Value” – s.74.5(2)

53

Prescribed Rate Loan Planning

• What is a Loan for Value?– Interest rate of at least the prescribed

rate– Interest paid on or before January 30 of

the following year– Lose exemption from attribution forever if

interest in respect of any particular year not paid on time

54

Prescribed Rate Planning

• Direct or to a Trust?• Why make a Loan for Value Now?

– Historically low prescribed rate of 1%• Long-term enhancement of income splitting

benefits– Rates may be higher in the future

55

Prescribed Rate Loan Planning

• Caution - refinancing old Prescribed Rate Loans– Cannot simply amend rate– Cannot simply refinance– Must dispose of acquired property and

repay old loan, only then can one advance a new low rate loan

56

Testamentary Trust Planning

• The estate itself and Trusts formed by will– Purposes: administration, control, tax etc.

• Some common types of trusts– Estate– Spousal– Family trusts– Insurance trusts– Spendthrift/Henson trusts– US beneficiary trusts

57

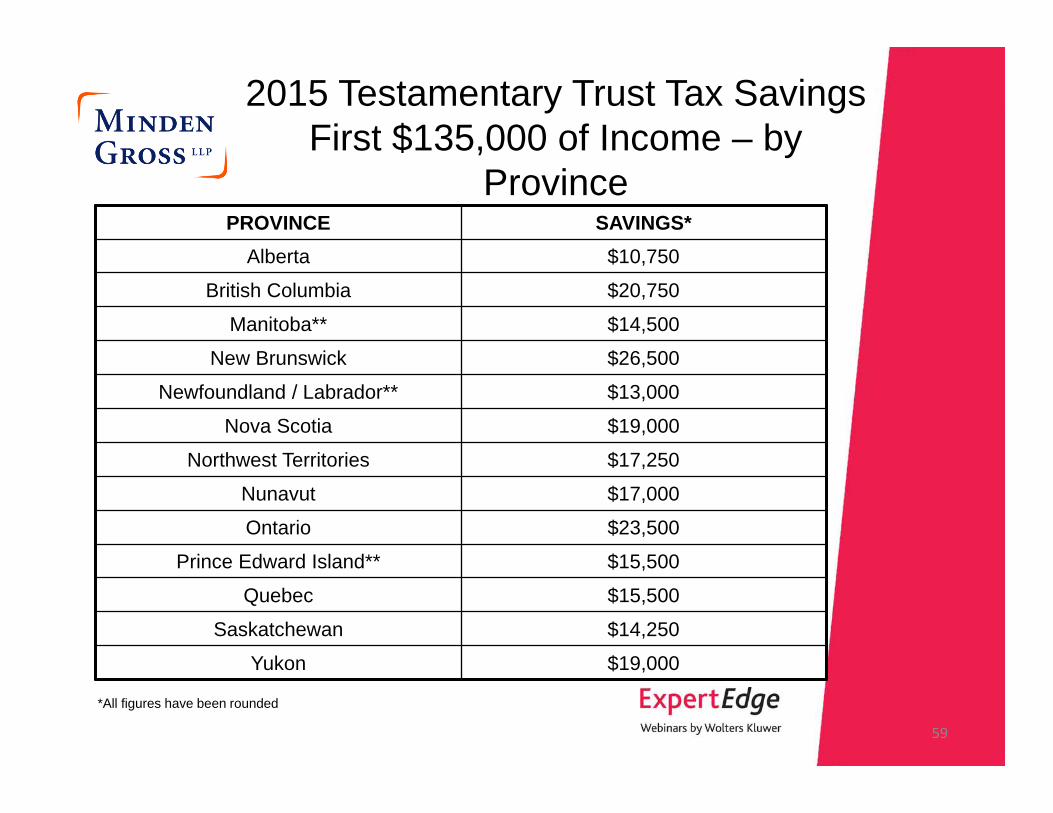

Testamentary Trust Planning

• Tax advantage of testamentary trusts– Spousal trusts – defer death taxes– Income splitting with beneficiaries– Income taxed at graduated rates

58

2015 Testamentary Trust Tax Savings First $135,000 of Income – by

Province

59

PROVINCE SAVINGS*Alberta $10,750

British Columbia $20,750

Manitoba** $14,500

New Brunswick $26,500

Newfoundland / Labrador** $13,000

Nova Scotia $19,000

Northwest Territories $17,250

Nunavut $17,000

Ontario $23,500

Prince Edward Island** $15,500

Quebec $15,500

Saskatchewan $14,250

Yukon $19,000

*All figures have been rounded

June 2013 Consultation Proposals

• Beginning in 2016 elimination of:– Graduated rates after first 36 months of estate – Exemption from income tax installment rules– Exemption from calendar taxation year– Exemption in computing AMT– Preferential treatment under Part XII.2– Ability to automatically qualify as a personal

trust– Ability to make ITCs available to beneficiaries

60

Whirlwind Legislative Process –Bill C-43 is the Law of the Land

• Final legislation extremely problematic – Nearly all original proposals enacted with

significant further restrictions and surprises that will severely impact traditional testamentary planning, spouse trust and other trust planning with no grandfathering

• Bill C-43 enacted Dec. 16, 2014 with effect as law of the land on January 1, 2016– Is this the final word?

61

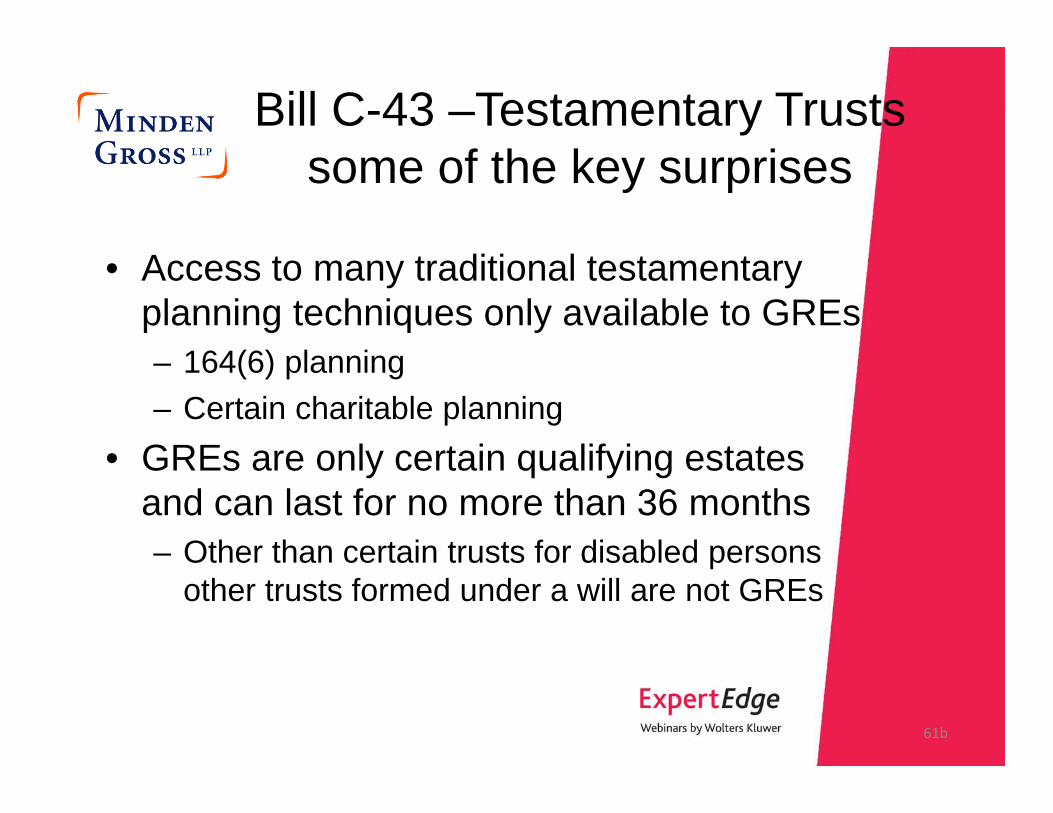

Bill C-43 –Testamentary Trusts some of the key surprises

• Income of a testamentary spousal trust in year of death of spouse beneficiary taxed to spouse beneficiary not the trust– Inequitable results– Technical drafting issues

• Is spouse beneficiary taxed on capital or income account?

61a

Bill C-43 –Testamentary Trusts some of the key surprises

• Access to many traditional testamentary planning techniques only available to GREs– 164(6) planning– Certain charitable planning

• GREs are only certain qualifying estates and can last for no more than 36 months– Other than certain trusts for disabled persons

other trusts formed under a will are not GREs

61b

Bill C-43 – Practice Points

• Consider revisiting– Not only pure tax planned testamentary trusts

but all testamentary trusts and, in particular, spousal trusts

– Self-Benefit, Alter-ego and Joint Spousal Trusts• But what are the solutions? What if the law

changes?• Non-tax planned testamentary trusts and

lifetime trusts will likely continue to be in use

61c

Ontario Surtax Planning

• Planning Point - Ontario– Ontario surtaxes do not apply when

determining tax rate• Surtaxes will apply when minor’s Ontario

tax liability exceeds surtax thresholds• Annual savings for top rate Ontario

taxpayer per minor beneficiary about $2,860 on just over $42,000 of ordinary investment income “split income”

62

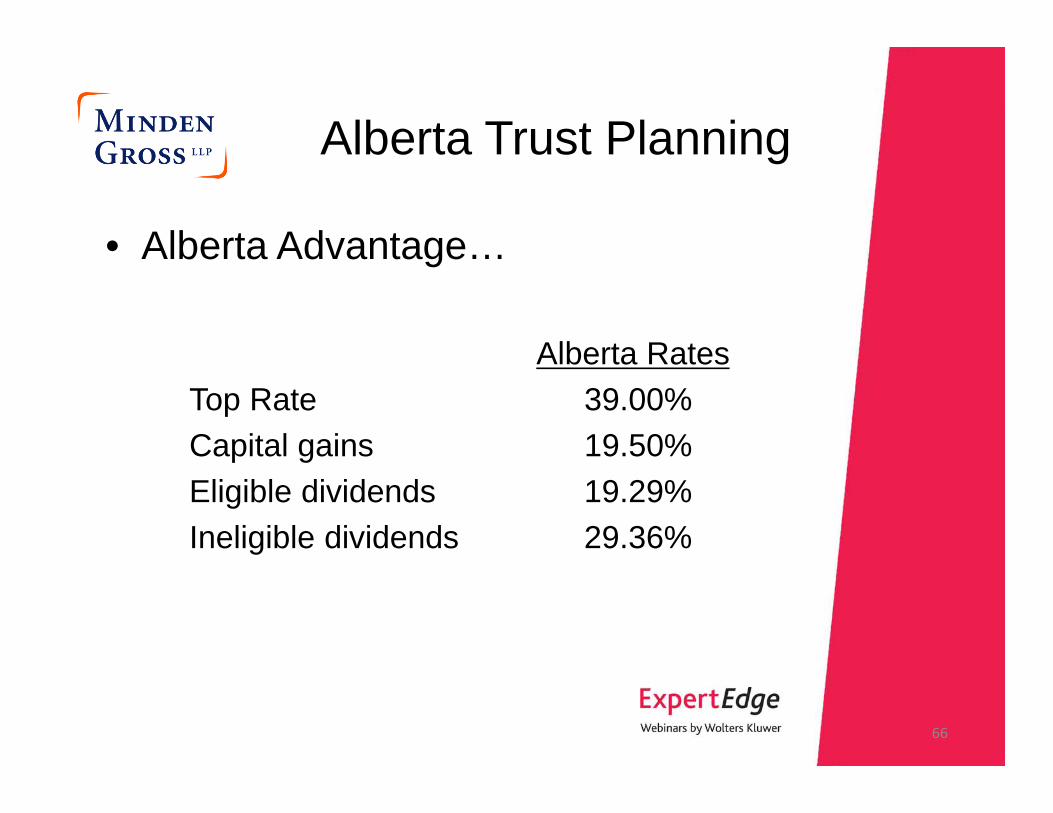

Alberta Trust Planning

• Alberta Advantage…

Alberta RatesTop Rate 39.00%Capital gains 19.50%Eligible dividends 19.29%Ineligible dividends 29.36%

63

Alberta Trust Planning

…gives rise to the Alberta Trust– Trust resident in Alberta with non-Alberta

resident beneficiaries– Income taxed in Alberta Trust– Capital distributed tax-free to beneficiaries

64

Alberta Trust Planning

…gives rise to unhappy other provinces– Anti-avoidance rules (including prov. GAAR)

• Eliminate benefits• Double tax?

– Case-law – Garron*– BEPS Etc.?

*Fundy Settlement v. The Queen, 2012 DTC 5063 (SCC)

65

Alberta Trust Planning

• Alberta Advantage…

Alberta RatesTop Rate 39.00%Capital gains 19.50%Eligible dividends 19.29%Ineligible dividends 29.36%

66

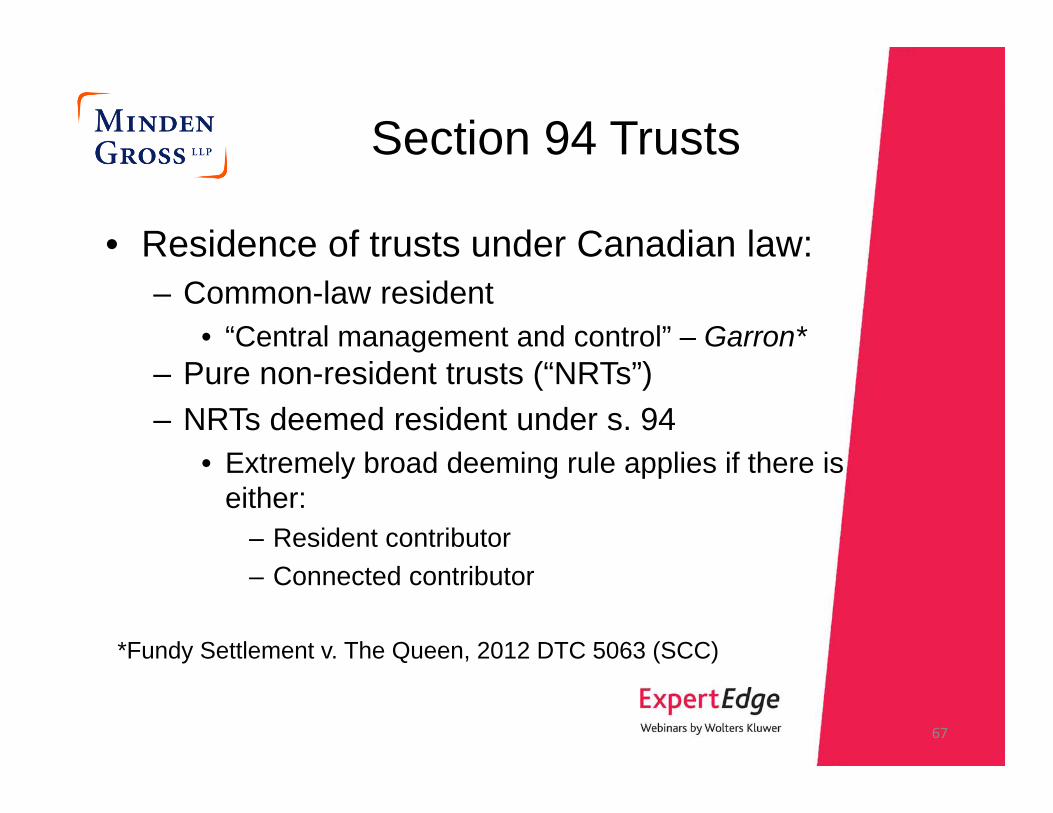

Section 94 Trusts

• Residence of trusts under Canadian law:– Common-law resident

• “Central management and control” – Garron*– Pure non-resident trusts (“NRTs”) – NRTs deemed resident under s. 94

• Extremely broad deeming rule applies if there is either:

– Resident contributor– Connected contributor

*Fundy Settlement v. The Queen, 2012 DTC 5063 (SCC)

67

Section 94 Trusts

• Some reasons to use Pure NRTs and s.94 NRTs instead of onshore trusts include:– To benefit non-residents– For privacy– Access to a wider range of investments– Access more favourable, trust, insolvency

and other legislation

68

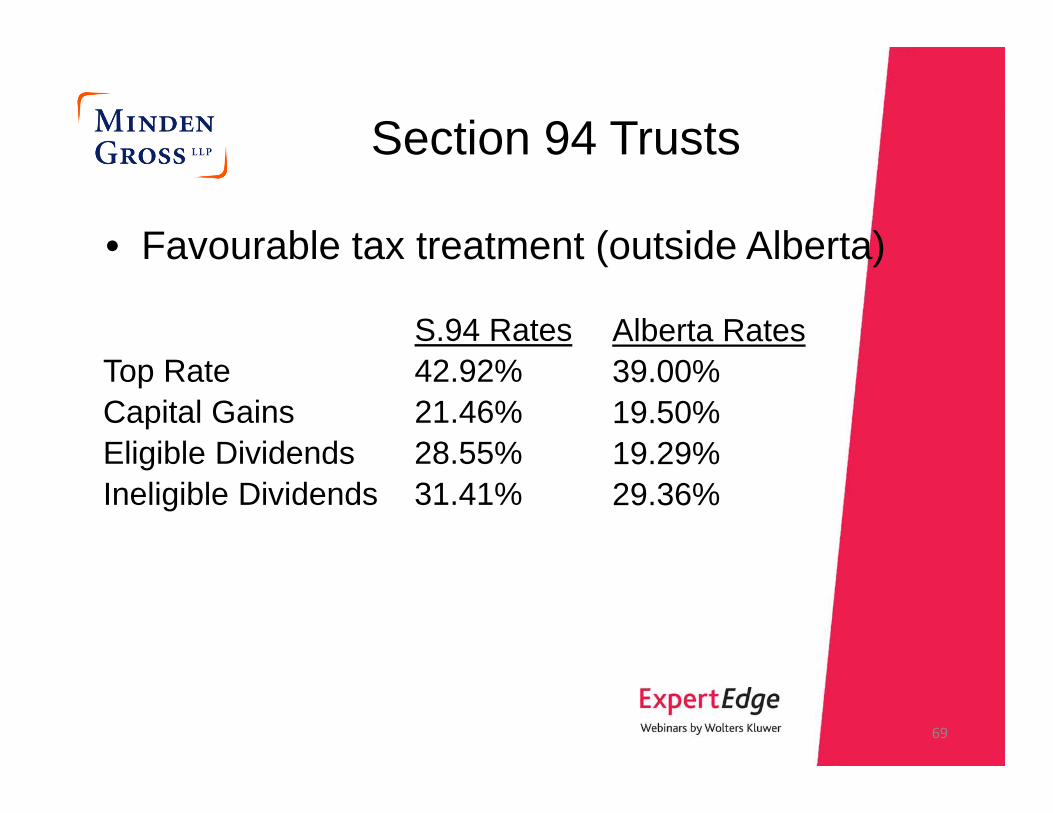

Section 94 Trusts

• Favourable tax treatment (outside Alberta)

69

Alberta Rates39.00%19.50%19.29%29.36%

S.94 RatesTop Rate 42.92%Capital Gains 21.46%Eligible Dividends 28.55%Ineligible Dividends 31.41%

Various Income Splitting Strategies

Matthew Getzler

70

Various Income Splitting Strategies

• Discretionary Dividend Shares• Stock Dividend Freezes• Downstream Freezes• Start-Up Freezes• Spousal Swaps

74

Discretionary Dividend Shares

• What are they?– Shares with nominal value that can receive

unlimited dividends at the directors’ discretion

• How are they used to split income?– Issue to spouse, issue or others and have

dividends from the corporation be taxed in their hands instead of an individual in a higher tax bracket

75

Value of Discretionary Dividend Shares

• Share attributes that support lack of value: – Non-voting– Non-participating on dissolution other return

of “redemption amount”– Redeemable by corporation at nominal

redemption amount– Discretionary dividends have no reference

to priority

76

Value of Discretionary Dividend Shares

• Share attributes (cont.): – Constating documents should provide that

dividends may be declared on one or more classes of shares to the exclusion of any one or more other classes of shares

• Corporate Steps– Valid subscription and payment– Payment of dividends to registered holders– Respect non-impairment clauses

77

Value of Discretionary Dividend Shares

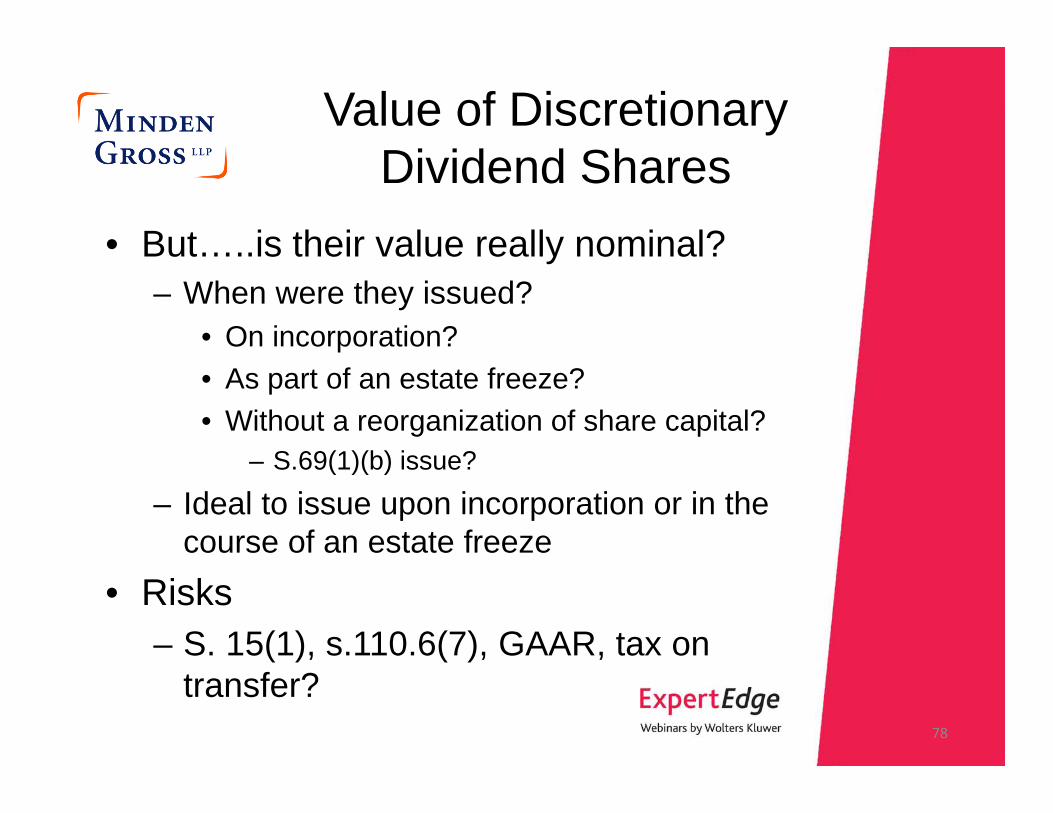

• But…..is their value really nominal? – When were they issued?

• On incorporation?• As part of an estate freeze?• Without a reorganization of share capital?

– S.69(1)(b) issue?

– Ideal to issue upon incorporation or in the course of an estate freeze

• Risks– S. 15(1), s.110.6(7), GAAR, tax on

transfer?78

Stock Dividend Freezes

• Alternative method of effecting an estate freeze

• May not run afoul of the corporate attribution rules– a stock dividend does not in itself constitute

a transfer directly or indirectly … to a company by an individual

79

How are they done?

• Articles of amendment filed, if necessary, creating a new class of freeze shares

• Stock dividend on the common shares consisting of freeze shares in amount sufficient to reduce the common shares to a nominal value

• New common shares acquired by the beneficiaries of the freeze – Personal attribution rules should be

considered80

Before

Opco

Parent

acb = $1fmv = $1M

100 common shares

81

After

Opco

ParentTrust

10,000 Class A Shares

acb = $1fmv = $1M

100 common shares

acb = $1fmv = $1

82

Characteristics of Freeze Shares Issued on Stock Dividend

• low stated capital– minimize the deemed dividend, based on an

increase to the stated capital• CRA unwilling to recognize a PAC

– stock dividend freeze does not involve a transfer of property in a non-arm’s length transaction

– Must be pretty certain of shares’ FMV or could be adverse unintended tax consequences

83

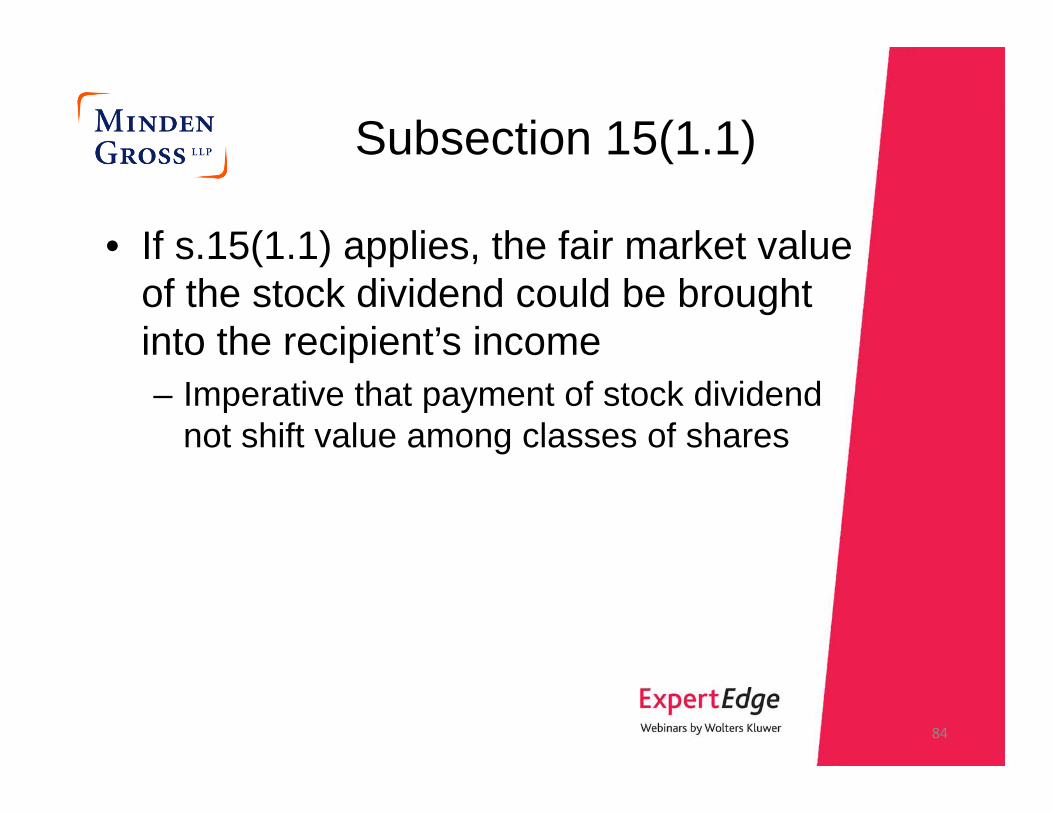

Subsection 15(1.1)

• If s.15(1.1) applies, the fair market value of the stock dividend could be brought into the recipient’s income– Imperative that payment of stock dividend

not shift value among classes of shares

84

Subsection 15(1.1) cont.

• S. 15(1.1) applies where:– it can reasonably be considered that one of

the purposes of the payment of the stock dividend was to significantly alter the value of an interest in the corporation of any “specified shareholder” of the corporation

85

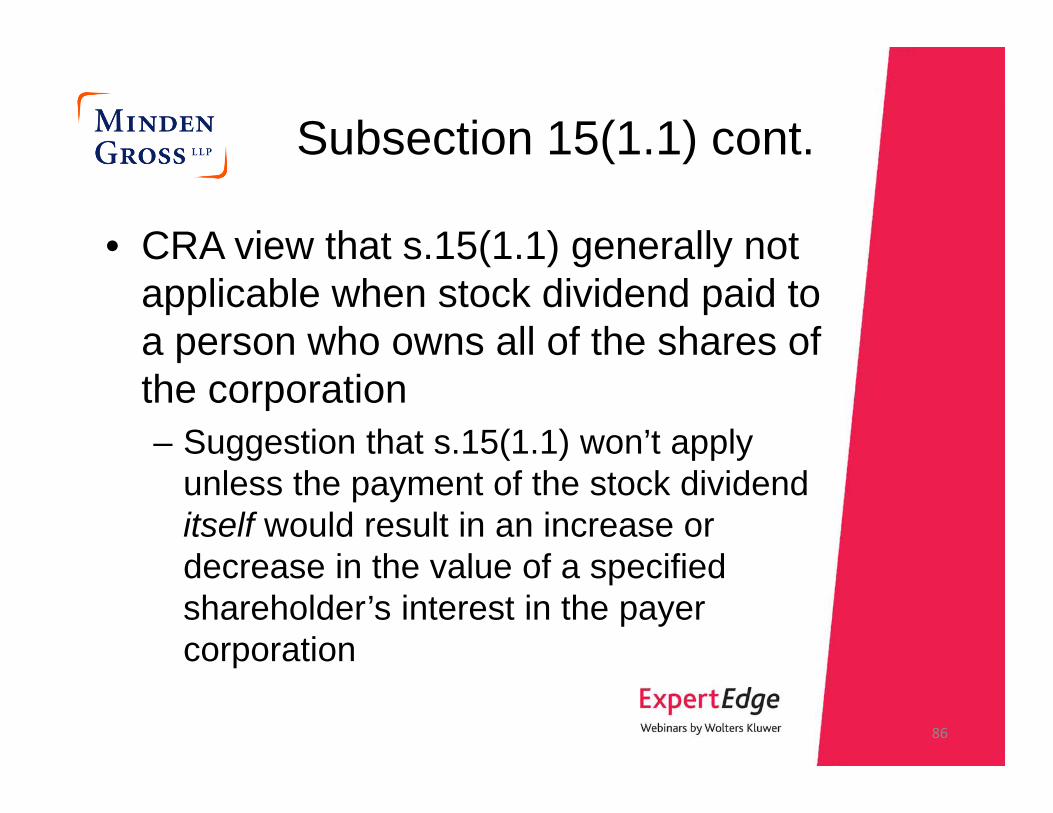

Subsection 15(1.1) cont.

• CRA view that s.15(1.1) generally not applicable when stock dividend paid to a person who owns all of the shares of the corporation– Suggestion that s.15(1.1) won’t apply

unless the payment of the stock dividend itself would result in an increase or decrease in the value of a specified shareholder’s interest in the payer corporation

86

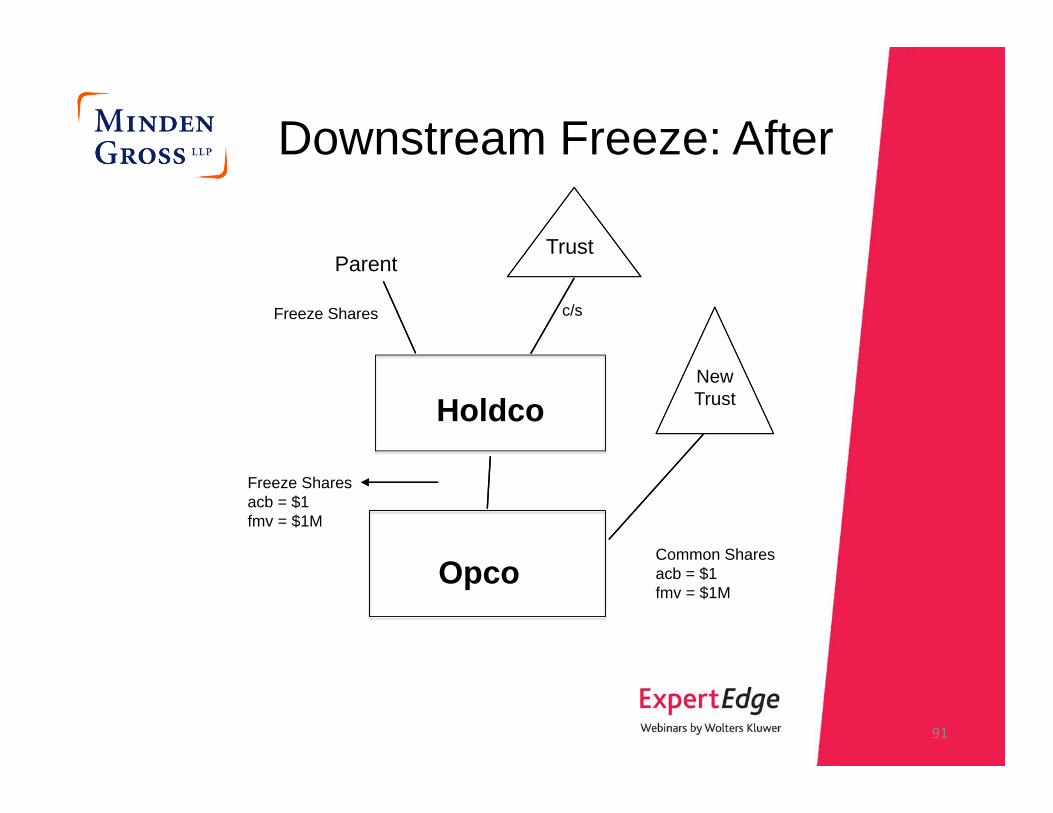

Downstream Freezes

• A freeze of a subsidiary or other downstream corporation

• Implemented in a number of circumstances, for example: – when growth shares are to be distributed

out of a family trust and new freeze desired – where a refreeze is undesirable

87

Implementation of Downstream Freeze

• Exchange by Holdco of common shares held in Opco for freeze shares

• Common shares of Opco ultimately to be held in the hands of the beneficiary of the freeze

88

Structure: Before

Opco

Holdco

TrustParent

Freeze Shares c/s

c/sacb = $1fmv = $1M

89

Traditional Freeze

90

Opco

Holdco

NewTrustParent

Original Freeze Shares

New Freeze Shares

c/s

c/s

Trust

Downstream Freeze: After

Opco

Holdco

TrustParent

Freeze Shares c/s

Freeze Sharesacb = $1fmv = $1M

NewTrust

Common Sharesacb = $1fmv = $1M

91

Benefits of Downstream Freeze

• Retraction rights• Trustee/director liability• Valuation

92

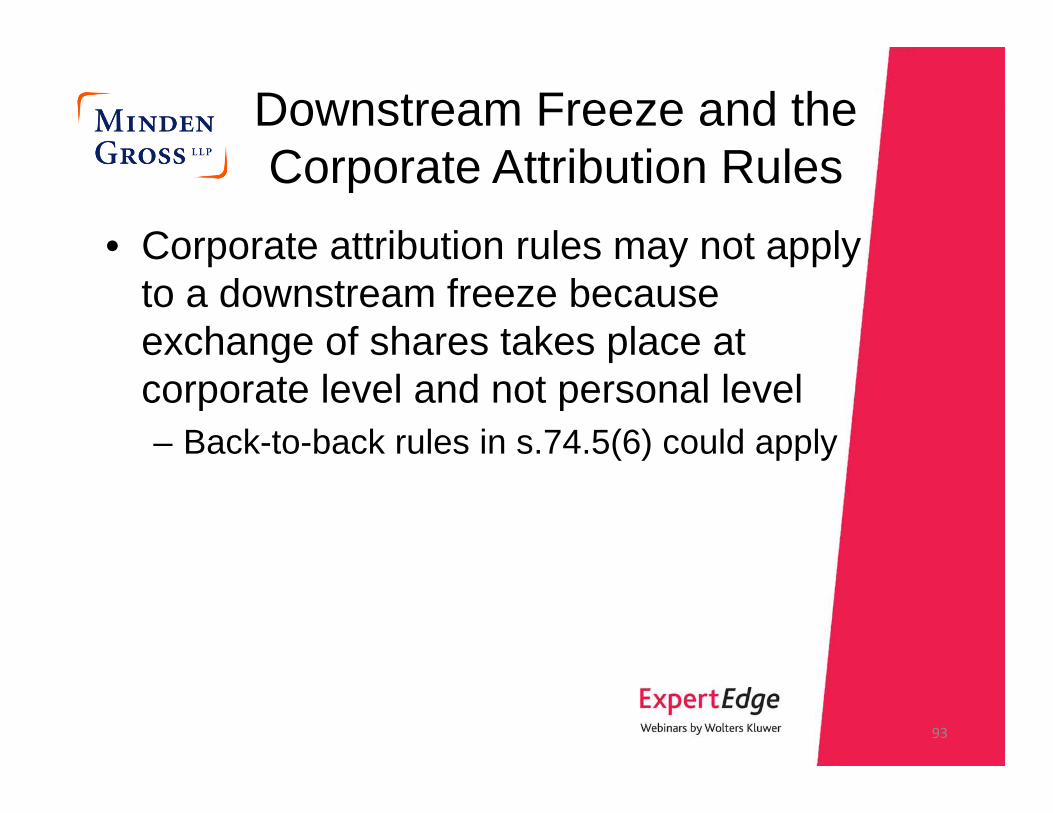

Downstream Freeze and the Corporate Attribution Rules

• Corporate attribution rules may not apply to a downstream freeze because exchange of shares takes place at corporate level and not personal level– Back-to-back rules in s.74.5(6) could apply

93

Back-to-Back Rules

• First part of provision applies where:– individual has transferred or lent property

(i.e., the shares of Opco originally transferred by Parent to Holdco)

– to another person (i.e., Holdco) – and that property or substituted property

(i.e., the Opco shares) – is in turn transferred (i.e., exchanged by

Holdco for freeze shares of Opco) – to or for the benefit of a “specified person

(i.e., Opco) with respect to the individual

94

Back-to-Back Rules cont.

• The “individual”– Generally includes corporations with family

members who are designated persons as significant shareholders

• If applicable:– individual who made the first transfer (i.e.,

Parent) deemed to have made the second transfer (i.e., the downstream freeze), thus causing corporate attribution rules to apply

• When applicable??95

Start-up Freezes

• Ideal time to get a desired structure in place at the outset

• Implementation of freeze or even just using a discretionary trust from the outset provides flexibility and reduces costs at a later date

• Limits application of certain tax provisions

96

Benefit of Start-Up Freeze

• Can start income splitting immediately, if possible

• May allow income splitting when income does start coming

• May be important to have structure in place in order to multiply lifetime capital gains exemption– Increase in value attributable to shares– 2-year holding period

97

Spousal Swaps

• Allows spouse to pay tax on income or capital gains with respect to property transferred between spouses– Transfer must be at fair market value

• Potentially subject to capital gains on assets transferred

• Use of losses to shelter gains– If for anything less, attribution rules will

apply• All income attributed to transferor

98

Spousal Swaps cont.

• Transfer interest in principal residence?– Typically asset with significant value– Typically non-income earning– Disposition typically exempt from capital

gains tax on account of principal residence exemption

– Must consider land transfer tax

• Other real estate (i.e., rental or business)– Land transfer tax and recapture

considerations99

This webinar is brought to you by Wolters Kluwer and in partnership with Minden Gross LLP.

For more information please contact customer service at 1-800-268-4522.

Visit www.cch.ca/ExpertEdge for a full list of our webinars.

Joan E. Jung(416) 369-4306

Michael A. Goldberg(416) 369-4317

Samantha A. Prasad(416) 369-4155

Matthew Getzler(416) 369-4316

100