increasing personal retirement

TRANSCRIPT

Increasing Personal

RetirementBy JC Rhine, CLUThe Cason Group

The IssuesO Physicians who are owners of their

companies (typically organized as an LLC) face two issues that are deterrents to funding the level of retirement income they need: 1. All income is passed through and

taxed to an owner.2. Contribution restrictions are applied

to the highly compensated in qualified plans.

The SolutionO Because of the internal tax free

buildup of cash values, for more than 50 years, life insurance policies have been used as the ideal funding vehicle for executive deferred compensation benefits.

O More than 70% of Fortune 500 companies use life insurance in the funding of their executive deferred compensation plans.

The Solution (continued)

O Using pertinent IRS regulations and case law for guidance, a policy owner is allowed to receive retirement benefits from his insurance policy income tax free1.

O A life insurance policy is one of the few financial vehicles that offers this opportunity.

The Solution (continued)

O A physician should select an insurance company that offers a life insurance policy that: 1. Creates within the contract needed tax

leverage opportunities.2. Offers potential cash value growth

because of a unique allocation strategy. O ING is our recommended insurance

company because it offers a product with both features named above.

Tax LeverageO ING Life Companies’ IUL-Global Choice policy

series offers the needed leverage through policy provisions allowing the policy owner to borrow from the policy to either: 1. Be reimbursed for the taxes paid on the

premium (Select Loan Strategy).2. Increase the amount being deposited in the

policy by 35% (Net Select Loan Strategy). O In both cases the full amount of the deposited

money is in the policy and credited with the returns of the indexes used as the crediting vehicle.

Unique Allocation Strategy

O In October 2012, a U.S.A. patent was issued on the indexed crediting method outlined below deeming it to be the intellectual property of ING.

O This means that no other insurance company can use this allocation method.

Unique Allocation Strategy (continued)

O Using three stock indexes (S&P 500, EuroStoxx 50, Hang Seng) as the basis for crediting returns, the strategy offers both a both 2 year and 5 year look back at the end of each point to point investment period and policy accounts are credited:O 75% of the highest index change rateO 25% of the next highest index change rateO 0% of the lowest index change rate

Unique Allocation Strategy (continued)

O No matter what strategy or combination of strategies a policy owner may elect, he can choose with confidence knowing that all of them have a Guaranteed 0% Minimum Interest Rate.

O Meaning even if the Indexes have negative performance the resulting Index Credit Rate will never be less than 0%.

Strategy HistoryO Almost without exception, most insurance

companies use only the S&P 500 as their basis for crediting to indexed life insurance policies funding executive deferred benefits.

O To evaluate the difference in approaches, ING created the Hypothetical Index Strategy Calculator.

O This calculator shows the result of a specified index strategy applied to the historical index data used in the strategy.

Strategy History (continued)

O From January 1980 to June 30, 2013 the NYSE has been open 11,503 days.

O Because this strategy is used long term to fund retirement benefits, 20 years is an appropriate length of time to use in strategy evaluations.

O There are 4,929 rolling 20 year periods from January 1980 to June 30, 2013.

Strategy History (continued)

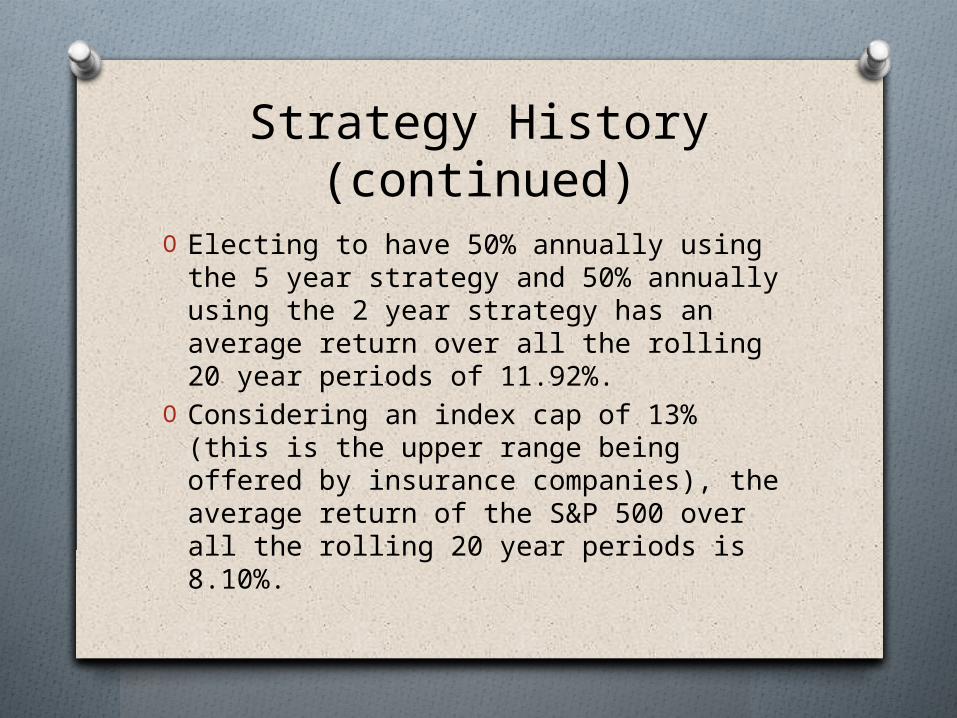

O Electing to have 50% annually using the 5 year strategy and 50% annually using the 2 year strategy has an average return over all the rolling 20 year periods of 11.92%.

O Considering an index cap of 13% (this is the upper range being offered by insurance companies), the average return of the S&P 500 over all the rolling 20 year periods is 8.10%.

Strategy History (continued)

O Twenty Year Examples: O $100,000 invested annually earning 11.92% has a future value in

20 years of $7,989,717.O A $7,989,717 account earning 11.92% can produce a 20 year

annual income of $950,942.

O $100,000 invested annually earning 8.10% has a future value in 20 years of $5,002,006.

O A $5,002,006 account earning 8.10%% can produce 20 year annual income of 474,803.

O The numbers above do not include any insurance company mortality charges and expenses.

O This is not a comparison of two insurance companies; it is a targeted evaluation of the two crediting strategies under consideration.

Benefit ExampleO The illustration shown is for a 45-year-old

male electing to contribute $50,000 annually into the ING IUL-Global Choice insurance policy using the Net Select Loan Strategy.

O Using this strategy, he would contribute $50,000 annually but would actually have $67,500 allocated in the policy.

O The illustration assumes he will make these contributions for 20 years and delay taking benefits until age 70.

Benefit Example (continued)

O The illustrated numbers are based on 50% of each annual premium being deposited in the 2 & 5 year strategies. Hypothetical illustrated earnings are 8.08% on both strategies.

O Initial Face Amount of insurance: $1,369,000 (Non MEC Limit)

O Death Benefit Option: 2 (Increasing)O Annual Premium: $67,500O Premium Election:

1. 100% Indexed Strategy 2. Loan Type: Net Select Loans3. Personal income tax rate is assumed to be 35%

Year

YearEnd Age

OwnerLLC

Income

Owner Taxes

Owner Net

Income

OwnerPremiu

m

Net Select Loan

Total to Policy

Retirement

BenefitsReceived

Net Surrender

ValueNet Death

Benefit

1 45 50,000 17,500 32,500 50,000 17,500 67,500 0 17,134 1,462,605

6 50 50,000 87,500 162,500 50,000 17,500 67,500 0 227,057 1,729,300

16 60 50,000 262,500 487,500 50,000 17,500 67,500 0 1108,257 2,546,275

21 65 50,000 367,500 682,500 50,000 17,500 67,500 1,913,144 2,539,257

27 71 0 0 0 0 0 -365,463

365,463 2,759,556 3,389,451

36 80 0 0 0 0 0 -365,463

3,654,630

1,505,128 1,924,586

46 90 0 0 0 0 0 -365,463

7,511,920

227,322 964,798

Insurance Policy Excerpts

Owner LLC Distributions

Owner Premiums Owner Benefits

Highlights of Projected Net Select Loan Strategy

1. $50,000 contribution, policy owner borrows to leverage investment.

2. $67,500 is invested each year in the Global Index Strategy.

3. $17,500 tax cost per year to policy owner for 20 years = $350,000 (he is paying this already).

4. $32,500 income per year for 20 years that policy owner could spend otherwise = $650,000

5. Annual tax free income of $326,228 for 20 years = $6,624,560

6. It would require $440,407 of taxable income (35% bracket) to net $326,228.

Policy RiderO The ING Global Choice policy has a

rider that will provide you valuable wealth protection if you are disabled.

O The Accelerated Benefit Rider is a feature of the policy offered at no charge.

O If you are you are disabled, the benefit is the lesser of 50% of the face of the policy or $1,000,000.