ind as 7 statement of cash flows educational material on

TRANSCRIPT

IND AS – 7 _ Statement of Cash Flows

Educational material on Ind AS -7

Division II _ Schedule III

Definitions1. Cash – Comprises cash on hand and demand deposits

2. Cash Equivalents – are short term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant riskof changes in value.

3. Cash flows – are inflows and outflows of C&CE

4. Operating Activities – are principal revenue generating activities of the entity and other activities that are not investing or financing activities.

5. Investing Activities – are the acquisition and disposal of long-term assets and other investments not included in cash equivalents.

6. Financing Activities – are activities that result in changes in the size and composition of the contributed equity and borrowings of the entity.

Cash & Cash Equivalents

1. Cash equivalent means investments which can be realized easily in cash in a short period from the date of investing the same.

2. Purpose – cash equivalents are held for the purpose of meeting short term cash commitments rather than for investment or other purposes.

3. Liquidity and Risk – For an investment to qualify as a cash equivalent it must be readily convertible to a known amount of cash and be subject to an insignificantrisk of changes in value. Therefore an investment normally qualifies as a cash equivalent only when it has a short maturity of ,say, 3 months or less from the dateof acquisition

4. Cash Management – Cash flows excludes movements between items that constitute C&CE because these components are part of the cash management of thecompany rather than part of its operating, investing and financing activities.

5. Equity investments are excluded from cash equivalents unless they are, in substance, cash equivalents, For eg. in case of preference shares acquired within ashort period of their maturity and with a specified redemption date.

6. Bank borrowings are generally considered to be financing activities. However, where Bank OD which are repayable on demand form an integral part of ancompany’s cash management, Bank OD are included as a component of C&CE.

Cash & Cash Equivalents

Solution

1. Not included – long term

2. Exclude as original maturity is not less than 90 days from the date of acquisition

3. Include as due within 90 days from the date of acquisition

4. Include

5. Include

6. Include

7. Include

8. Include

Presentation of Statement of Cash Flows

Activities

Operating Investing

Financing Activities that result in theacquisition and disposal of long termassets and other investments notincluded in cash equivalentsActivities that result in changes in

size and composition of thecontributed equity and borrowingsof the entity.

Principal revenue producingactivities of the company and otheractivities that are not investing orfinancing activities

Reporting of Cash Flow from Operating Activities

1. The amount of cash flows arising from operating activities is a key indicator of the extent to which the operations of the entity have generated sufficient cash flowsto:

✓ Repay loans

✓ Maintain the operating capability of the entity

✓ Pay dividends

✓ Make new investments without recourse to external source of financing.

2. Cash flow from operating activities are primarily derived from the principal revenue producing activities of the company. Therefore they generally result fromthe transactions and other events that enter into the determination of profit or loss. Examples of cash flows from operating activities are:

✓ Cash receipts from sale of goods and rendering of services

✓ Cash receipts from royalties, fees, commissions and other revenue

✓ Cash payments to suppliers for goods and services

✓ Cash payments to and on behalf of employees

✓ Cash receipts and cash payments of an insurance entity for premiums and claims, annuities and other policy benefits

✓ Cash payments and refund of income taxes unless they can be specifically identified with financing and investing activities

✓ Cash receipts and payments from contracts held for dealing or trading purposes

Reporting of Cash Flow from Operating Activities

Example

Solution

S No Activities

1 Operating – main revenue generating activities

2 Operating – expenses related to main operations of business

3 Operating - expenses related to main operations of business

4 Operating - expenses related to main operations of business

5 Not included - Credit transactions will not be included in cash flows

6 Operating – Supplementary revenue generating activities

7 Not included – Non cash transaction

8 Operating – Cash outflow related to main operations of business

9 Not included – Non cash transaction

10 Not included – Financing activities

11 Not included – Non cash transaction

12 Operating – relating to operations of business

13 Operating – relating to operations of business

1. Cash flows from sale of an item of PPE are cash flows from investing activities. However cash payments to manufacture or acquire assets held for rental to otherand subsequently held for sale as per para 68A of Ind AS 16, are cash flows from operating activities. The cash receipts from rent and subsequent sale of suchassets are also cash flow from operating activities.

2. A Company may hold securities and loans for dealing or trading purposes, in which case they are similar to inventory acquired specifically for resale. Hence cashflows from these activities are classified under operating activities.

3. Amount of cash flows arising from operating activities is a key indicator of the extent to which the operations of the entity have generated sufficient cash flowsor not . If cash flows from operations is positive , it will be treated as positive indicator whereas negative cash flow from operations will denote that companiesability to generate the revenue from its main operations is very weak. The companies in the initial stage of their business or the companies which are facingeconomic problems will generally have the negative cash flows from the operations.

Cash flows from Operating Activities

Direct Method

Indirect Method

Major classes of gross cash receipts andgross cash payments are disclosed

Profit or loss is adjusted for the effects of:

✓ transactions of a non-cash nature

✓ any deferrals or accruals of past or future operating cash receipts orpayments✓ Items of income or expenses associated with investing or financingcash flows

Reporting of Cash Flow from Operating Activities

1. Where major classes of gross cash receipts and gross cash payments are disclosed.

2. Entities are encouraged to report cash flows from operating activities using the direct method.

3. The direct method provides information which may be useful in estimating future cash flows and which is not available under indirect method.

4. Direct method starts with cash revenue / income / receipts of the company.

5. All the cash expenses will be deducted from such cash revenue.

6. The cash profit will adjusted for the cash flows arising from investing and financing activities.

7. Non cash expenses / losses / gains will not be considered.

8. The payments to suppliers and receipt from customers are also taken into consideration.

9. The resultant figure would be cash flows from operating activity.

10. The exercise would be similar to converting to Income and Expenditure A/c (Accrual system) into receipt and payment (cash system).

11. This method will have Top down approach of presentation.

Direct Method

Example

Direct Method

Solution – Direct Method

ABC Ltd

Statement of Cash flows for the year ended March 31, 2020

Direct Method

Particulars Amount Amount

Cash sales (7000+500000-10000) 497000

Less : All cash expenses

Cash Purchases (8000+349000-12000) 345000

Overheads (7000+55000-10000) 52000

Interest Financing

Depreciation Non cash

Loss on sale of asset Non cash 397000

Cash Profit 100000

Less : Tax (30000)

Total Cash flows operating activities 70000

* Purchase = Cost of goods sold + Clo. Inventory – Op. inventory

1. The net cash flows from operating activities is determined by adjusting profit or loss for the effects of :

✓ Changes during the period in inventories

✓ Changes during the period in operating receivables

✓ Changes during the period in operating payables

✓ Non cash items like:

➢ Depreciation

➢ Provisions

➢ Deferred taxes

➢ Unrealized foreign currency gain and losses

➢ Undistributed profits of associates

✓ All other items for which the cash effects are investing or financing cash flows

2. Indirect method is reverse of direct method. It starts with accounting profit after tax as given in P&L A/c. Thereafter, the profit will be adjusted for non cash items,losses and gains on investing and financing activities, interest and dividends, collection and payments to debtors/creditors ect. This indirect method will have BottomUp approach.

Indirect Method

Solution – Indirect Method

ABC Ltd

Statement of Cash flows for the year ended March 31, 2020

Indirect Method

Particulars Amount Amount

Profit After tax 53000

Add: Depreciation 7000

Interest Paid 3000

Loss on sale of asset 2000

Decrease in inventories 1000

Increase in trade receivables (3000)

Increase in trade payables 4000

Increase in provision for expenses 3000 17000

Total cash flows from operating activities 70000

Reporting of Cash Flow from Investing Activities

1. Only expenditure that result in a recognized asset in the Balance Sheet are eligible for classification as investing activities.

2. Examples of cash flows from investing activities are:

✓ Cash payments to acquire PPE , intangibles and other long term assets. These payments include those relating to capitalized development costs and selfconstructed PPE.

✓ Cash receipts from sale of PPE , intangibles and other long term assets.

✓ Cash payments to acquire equity or debt instruments of other entities and interest in joint ventures (other than payments for those instruments considered to becash equivalents or those held for dealing or trading purposes)

✓ Cash receipts from sale of equity or debt instruments of other entities and interest in joint ventures (other than receipts for those instruments considered to becash equivalents or those held for dealing or trading purposes)

✓ Cash advances and loans made to other parties (other than advances and loans made by financial institution)

✓ Cash receipts from the repayment of advances and loans made to other parties (other than advances and loans of financial institution)

✓ Cash payments for future contracts, forward contracts, option contracts and swap contracts except when the contracts are held for dealing or trading purposes orpayments are classified as financing activities.

✓ Cash receipts from future contracts, forward contracts, option contracts and swap contracts except when the contracts are held for dealing or trading purposes orthe receipts are classified as financing activities.

✓ When a contract is accounted for as a hedge of an identifiable position the cash flows of the contract are classified in the same manner as the cash flows of theposition being hedged.

Reporting of Cash Flow from Investing Activities

Example

Solution

S No Activities

1 Operating – main revenue generating activities

2 Operating – expenses related to main operations of business

3 Operating – in case of financial institutes

4 Operating – in case of financial institutes

5 Operating – in case of financial institutes

6 Operating – in case of financial institutes

7 Operating – main revenue generating activities

8 Operating – expenses related to main operations of business

9 Operating – expenses related to main operations of business

10 Investing – Asset purchased

11 Investing – Asset purchased for long term purpose

12 Investing – Strategic investment

13 Investing – Asset purchased for cash payment

14 Operating –

15 Not included – No cash flow

Reporting of Cash Flow from Financing Activities1. During the lifetime of the entity, it needs money for long term investments as well as for working capital purpose. Company can raise the capital by way of equity

or loans. Thus cash flows related to raising of funds and redemption of funds will be covered under cash flows from financing activities.

2. Examples of cash flows arising from financing activities are :

✓ Cash proceeds from issuing shares or other equity instruments

✓ Cash payments to owners to acquire or redeem the company’s shares

✓ Cash proceeds from issuing debentures, loans, notes, bonds, mortgages and other short term or long term borrowings

✓ Cash repayments of amounts borrowed, and

✓ Cash payments by a lessee for the reduction of the outstanding liability relating to a finance lease

Reporting of Cash Flow from Financing Activities

Example

Solution

S.No. Activities

1 Financing

2 Investing

3 Investing

4 Investing

5 No Cash flow

6 Investing

7 Operating

8 Investing

9 Investing

10 Financing

11 Financing

12 Investing

13 No Cash flow

14 Financing

15 Investing

Reporting of Cash Flow on Net Basis

1. An entity is required to report separately major classes of gross cash receipts and gross cash payments arising from investing and financing activities, except tothe extent that cash flows are permitted to be reported on a net basis.

2. If nothing is specifically mentioned, then as per Ind AS 7, the cash flows will be presented on Gross basis. Gross basis means the receipts would be shownseparately and the payments will be shown separately.

3. Cash flows arising from the following Operating, investing or financing activities may be reported on net basis :

✓ Cash receipts and payments on behalf of customers when the cash flows reflect the activities of the customer rather than those of the entity. Examples :

o the acceptance and repayment of demand deposits of a bank

o Funds held for customers by an investment entity and

o Rents collected on behalf of, and paid over to, the owners of properties.

✓ Cash receipts and payments for items in which the turnover is quick, the amounts are large, and the maturities are short. Examples are advance made for, andrepayment of :

o Principal amounts relating to credit card customers

o The purchase and sale of investments and

o Other short term borrowings, for eg., those which have a maturity period of 3 months or less

Reporting of Cash Flow on Net Basis

4.Cash flows arising from each of the following activities of a financial institution may be reported on a net basis :

✓ Cash receipts and payments for the acceptance and repayment of deposits with a fixed maturity date

✓ The placement of deposits with and withdrawal of deposits from other financial institutions and

✓ Cash advances and loans made to customers and the repayment of those advances and loans

Foreign Currency Cash Flows

1. Cash flows arising from transactions in a foreign currency shall be recorded in an entity’s functional currency by applying to the foreign currency amount theexchange rate between the functional currency and the foreign currency at the date of the cash flow.

2. The cash flows of a foreign subsidiary shall be translated at the exchange rates between the functional currency and the foreign currency at the dates of the cashflows.

3. Unrealized gains and losses arising from changes in foreign currency exchange rates are not cash flows. However, the effect of exchange rate changes on cash &cash equivalent held or due in a foreign currency is reported in the statement of cash flows in order to reconcile cash & cash equivalents at the beginning and theend of the period. This amount is presented separately from cash flows from operating, investing and financing activities and includes the differences, if any, hadthose cash flows been reported at end of period exchange rates.

Interest and Dividends

1. Cash flows from interest and dividends received and paid shall each be disclosed separately.

In case of Financial Institutions In case of other Companies

Interest Paid Operating activities Financing activities

Interest and Dividend received Operating activities Investing activities

Dividend paid Financing activities Financing activities

Taxes on Income

1. Cash flows arising from taxes on income shall be separately disclosed and shall be classified as cash flows from operating activities unless they can be specificallyidentified with financing and investing activities.

2. Taxes on income arise on transactions that give rise to cash flows that are classified as operating, investing or financing activities in a statement of cash flows.While tax expense may be readily identifiable with investing or financing activities, the related tax cash flows are often impracticable to identify and may arise ina different period from the cash flows of the underlying transaction. Therefore, taxes paid are usually classified as cash flows from operating activities. However,when it is practicable to identify the tax cash flow with an individual transaction that gives use to cash flows that are classified as investing or financing activitiesthe tax cash flows is classified as an investing or financing activity as appropriate. When tax cash flows are allocated over more than one class of activity, the totalamount of taxes paid is disclosed.

Investment in Subsidiaries, associates and joint ventures

1. When accounting for an investment in associate, a JV or a subsidiary accounted for by use of the equity or cost method, an investor restricts its reporting in thestatement of cash flows between itself and the investee, for eg., to dividends and advances.

2. An entity that reports its interest in an associate or JV using the equity method includes in its statement of cash flows the cash flows in respect of its investmentin the associate or JV, and the distributions and other payments or receipts between it and the associate or JV.

Changes in ownership interests in Subsidiaries and other businesses

1. Classification of Cash Flows as Investing Activities

✓ The aggregate cash flows arising from obtaining or losing control of subsidiaries or other businesses shall be presented separately.

✓ A Company shall disclose, in aggregate, in respect of both obtaining and losing control of subsidiaries or other businesses during the period each of the following:

a) The total consideration paid or received

b) The portion of the consideration consisting of cash and cash equivalents

c) The amount of cash and cash equivalents in the subsidiaries or other businesses over which control is obtained or lost; and

d) The amount of the assets and liabilities other than cash or cash equivalents in the subsidiaries or other businesses over which control is obtained or lost,summarized by each major category.

✓ The separate presentation of the cash flow effects of obtaining or losing control of subsidiaries or other businesses as a single line items, together with theseparate disclosure of the amounts of assets and liabilities acquired or disposed of, help to distinguish those cash flows from the cash flows arising from the otheroperating, investing and financing activities.

✓ The cash flow effects of losing control are not deducted from those of obtaining control.

✓ The aggregate amount of cash paid or received as consideration for obtaining or losing control of subsidiaries or other businesses is reported in the statement of

cash flows net of cash & cash equivalents acquired or disposed off as part of such transactions, events or changes in circumstances.

Changes in ownership interests in Subsidiaries and other businesses

1. Classification of Cash Flows as Financing Activities

✓ Cash flows arising from changes in ownership interests in subsidiary that do not result in a loss of control shall be classified as cash flows from financing activities,unless the subsidiary is held by an investment entity and is required to be measured at FVTPL.

✓ Changes in ownership interests in a subsidiary that do not result in a loss of control, such as the subsequent purchase or sale by a parent of a subsidiary’s equityinvestments, are accounted for as equity transactions (see Ind AS 110), unless the subsidiary is held by an investment entity and is required to be measured atFVTPL. Accordingly the resulting cash flows are classified in the same way as other transactions with owners.

Non Cash Transactions

1. Investing and financing transactions that do not require the use of C&CE shall be excluded from a statement of cash flows.

2. Such transactions shall be disclosed elsewhere in the financial statements in a way that provides all the relevant information about these investing and financingactivities.

3. Many investing and financing activities do not have a direct impact on current cash flows although they do affect the capital and asset structure of an entity.Such non cash items will not form part of the cash flow statement.

4. Examples of non cash transactions are :

✓ The acquisition of assets either by assuming directly related liabilities or by means of a lease.

✓ The acquisition of an entity by means of an equity issue

✓ The conversion of debt to equity

Changing in liabilities arising from financing activities1. An entity shall provide disclosures that enable users of financial statements to evaluate changes in liabilities arising from financing activities, including both

changes arising from cash flows and non cash changes.

2. To the extent necessary to satisfy the above requirement, an entity shall disclose the following changes in liabilities arising from financing activities :

a) Changes from financing cash flows

b) Changes arising from obtaining or losing control of subsidiaries or other businesses

c) The effect of changes in foreign exchange rates

d) Changes in fair values

e) Other changes

2. Liabilities arising from financing activities are liabilities for which cash flows were, or future cash flows will be, classified in the statement of cash flows as cashflow from financing activities.

3. In addition, the disclosure requirement also applies to changes in financial assets ( For eg. assets that hedge liabilities arising from financing activities) if cashflows from those financial assets were, or future cash flows will be, included in cash flows from financing activities.

4. One way to fulfill the disclosure requirement is by providing a reconciliation between the op. and clo. Balances in the BS for liabilities arising from financingactivities, including the changes identified.

5. If an entity provides the disclosure required in combination with disclosures of changes in other assets and liabilities, it shall disclose the changes in liabilitiesarising from financing activities separately from changes in those other assets and liabilities.

Components of Cash and Cash Equivalents

1. An entity shall disclose the components of C&CE and shall present a reconciliation of the amounts in its statement of cash flows with the equivalent itemsreported in the BS.

2. In view of the variety of cash management practices and banking arrangements around the world and in order to comply with Ind AS 1, Company will provide apolicy which it adopts in determining the composition of C&CE as per Ind AS 1.

3. The effect of any change in the policy for determining components of C&CE, for eg, a change in the classification of financial instruments previously consideredto be part of an entity’s investment portfolio, is reported in accordance with Ind AS - 8.

4. It has been clarified, that there should not be a difference in the amount of C&CE as per Ind AS 1 and Ind AS 7. However, as per Ind AS 7 where Bank OD whichare repayable on demand form an integral part of an entity’s cash management, Bank OD are included as a component of C&CE. Although Ind AS 7 permits BankOD to be included as C&CE, for the purpose of presentation in the BS, it would not be appropriate to include Bank OD in the line item C&CE unless netting offconditions as given in para 42 of Ind AS 32, presentation are complied with.

5. Bank OD in the BS will be included within financial liabilities. Just because the Bank OD is included in C&CE for the purpose of Ind AS 7, does not mean that thesame should be netted off against the C&CE balance in the BS. Instead Ind AS-7 requies a disclosure of the components of C&CE and reconciliation of amountspresented in the Cash Flow statement.

Components of Cash and Cash Equivalents1. Another element on account of which there could be difference between the C&CE presented in the BS and the statement of Cash Flows is unrealized gain or

losses arising from changes in foreign currency exchange rates, which are not considered to be cash flows.

If any changes in the policies take place , that will be dealt with as per the provisions of Ind AS 8.

Particulars Amount

Profit before Tax 100

Less: Unrealised exchange gain (100)

Cash flow from Operating activities Nil

Cash flow from Investing activities Nil

Cash flow from Financing activities Nil

Net increase in C&CE during the year Nil

Add : Op. balance of C&CE 4,500

C&CE as at the year end 4,500

Reconciliation of C&CE

C&CE as per Statement of Cash Flows 4,500

Add: Unrealised gain on C&CE 100

C&CE as per the Balance Sheet 4,600

Other Disclosures

1. An entity shall disclose, together with a commentary by management, the amount of significant C&CE balances held by the Company that are not available foruse by the group.

2. There are various circumstances in which C&CE balances held by an entity are not available for use by the group. Examples include :

✓ C&CE balances held by a subsidiary that operates in a country where exchange controls or other legal restrictions apply when the balances are not available forgeneral use by the parent or other subsidiaries.

3. Additional information may be relevant to users in understanding the financial position and liquidity of an entity.

4. It may include :

✓ The amount of undrawn borrowing facilities that may be available for future operating activities and to settle capital commitments, indicating any restrictions onthe use of these facilities.

✓ The aggregate amount of Cash Flows that represent increases in operating capacity separately from those cash flows that are required to maintain operatingcapacity. It will help the stake holders to know whether entity is paying proper attention for maintenance also.

✓ The amount of the cash flows arising from the operating, inventing and financing activities of each reportable segment (see Ind AS 108, Operating segments).This will provide the idea about the company as a whole as well as the various parts of the company and their efficiencies.

Illustration

Solution

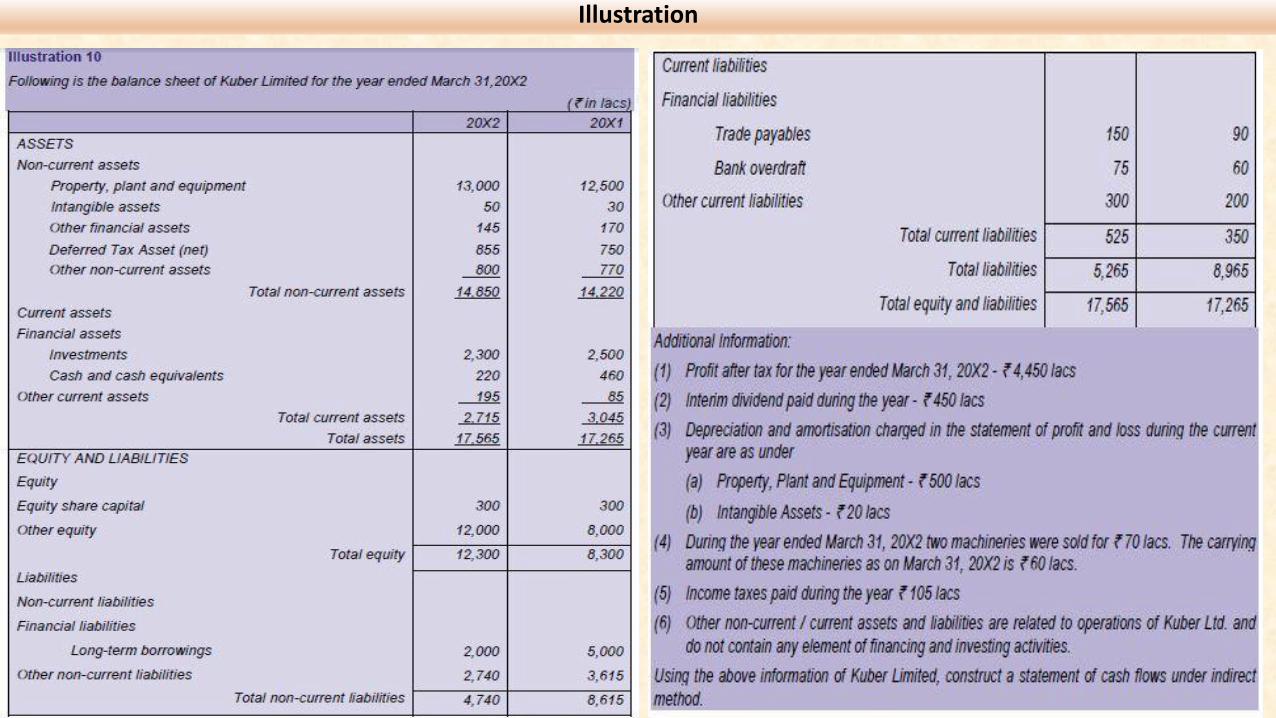

Statement of Cash Flows for the year ended March 31, 2020

Particulars Amount

Profit after tax 4,450

Add : Taxes paid 105

Profit before tax 4,555

Add : Deprecation & amortization (500+20) 520

Less: Profit on sale of PPE (10)

Less : Increase in deferred tax asset ( 855-750) (105)

4,960

Changes in operating assets and liabilities

Decrease in other financial assets (170-145) 25

Increase in other non current assets (30)

Increase in other current assets (110)

Decrease in other non current liabilities (875)

Increase in trade payables 60

Increase in other current liabilities 100

4,130

Less : Income tax paid (105)

Cash flows from operating activities 4,025

Particulars Amount

Cash flows from investing activities

Sale of machinery 70

Purchase of machinery (13000+60+500-12500) (1,060)

Purchase of intangible assets (50+20-30) (40)

Sale of financial assets (2,500-2,300) 200

Cash outflow from investing activities (830)

Cash flows from financing activities

Interim dividend paid (450)

Repayment of borrowings (3,000)

Cash outflow from financing activities (3,450)

Net increase in C&CE during the year (255)

Opening C&CE (460-60) 400

Closing C&CE 145

Illustration

Statement of Cash Flows for the year ended March 31, 2020

Particulars Amount

Profit 1,000

Add : Deprecation & amortization 15,000

16,000

Changes in operating assets and liabilities

Decrease in accounts receivable 7,500

Decrease in prepaid insurance 2,000

Increase in inventory (3000)

Increase in Account payables 2,000

Decrease in Wages payable (3,000)

Cash inflows from operating activities 21,500

Cash flows from investing activities

Purchase of fixed assets (46000)

Cash outflows from investing activities (46,000)

Cash flows from financing activities

Proceeds from issue of Capital 4,000

Dividend paid (2,500)

Proceeds from issue of Debentures 13,000

Cash inflows from financing activities 14,500

Net increase in C&CE during the year (10,000)

Opening C&CE 14,000

Closing C&CE 4,000

FAQ’s on Ind AS-7

Q1: Does Ind AS 7 provides any exemption with regard to its applicability like AS-3, which provides that AS-3 is not mandatory for Small and Medium sizedcompanies and non-corporate entities falling in level II and level III ?

Ans: No exemption has been provided in Ind AS -7 with regard to its applicability as provided in AS-3. Moreover, Ind AS 7 provides that statement of cash flows formsan integral part of financial statements for each period for which financial statements are prepared. Accordingly the class of companies which will be required toprepare FS as per Ind AS will be required to prepare statement of cash flows as per Ind AS-7.

Q2: Whether statement of cash flows should be prepared only for annual reporting period ?

Ans : According to para 1 of Ind AS 7, statement of cash flows is an integral part of financial statements and the same should be prepared for each period for whichfinancial statements are presented i.e. annual period as well as interim reporting period. Ind AS 34 provides that interim financial report means a financial reportcontaining either a complete set of financial statements or a set of condensed financial statements for an interim period. Accordingly statement of cash flows can bepresented in complete or condensed form.

Q3: What an item qualifies to be an cash equivalents ?

Ans: According to para 6 of Ind AS 7, Cash equivalents are short term highly liquid investments that are readily convertible to known amounts of cash and which aresubject to an insignificant risk of change in value. An investment normally qualifies to be a cash equivalent only when it has a short maturity ( not more than 3months ) from the date of acquisition.

Egs of cash equivalents

✓ Balances with banks in short term deposits say not more than 3 months

✓ Short term money market instruments, such as, 91 days treasury bills, certificate of deposit etc.

An overriding test is that cash equivalents are held to meet short term cash requirements of the entity rather than for investment or other purposes. For eg – a 3month loan or deposit given to a party to help in managing party’s short term liquidity position is not a cash equivalent because it is given for a purpose other than tomanage its own short term cash requirements.

In view of variety of cash management practices and banking arrangements, an entity is required to disclose the policy which it adopts in determining the compositionof C&CE

FAQ’s on Ind AS-7

Q4: Cash is defined as cash on hand and demand deposits. What is the meaning of the term ‘demand deposits’ ? State the treatment of demand deposits ?

Ans: Ind AS 7 does not defined the term demand deposit. In common parlance, demand deposit refers to a deposit in an account held at a bank/financial institutionwhere the amount deposited can be withdrawn at any time by the depositor without any penalty. Eg’s of such deposit are current accounts, saving accounts etc.

Q5 : What is meant by Term Deposit ? State the treatment of term deposit ?

Ans: Term deposit can be a short term or long term. For the purpose of presentation of term deposits in the statement of cash flows, short term deposits (say notmore than 3 months) are those deposits which are held with an intention to meet the short term fund requirements. Since short term deposits are highly liquidinvestments that are readily convertible into known amounts of cash and are subject to insignificant risk of changes in value, the same qualify to be a cash equivalent.

The 3 months maturity period is to be determined from the date of deposit and not from the end of the reporting period, i.e. for a term deposit to qualify to be acash equivalent, it should have original maturity of period less than 3 months.

However, term deposits placed before a specified long period (say, more than 3 months) with an intention to meet the long term fund requirements will not satisfythe definition of cash equivalents. Further there could be restrictions on withdrawal or early redemption. Accordingly cash flows from these deposits are classifiedunder investing activities.

FAQ’s on Ind AS-7

Q6: What do you mean by cash flows? Is it necessary that there should be actual cash inflow/outflow from entity’s cash/bank balances?

Ans: The dictionary meaning of the word ‘flow’ is movement. There are two types of cash flows viz. cash inflow and cash outflow. A cash flow transaction mustincrease/decrease C&CE.

Any transaction which does not have any effect on C&CE is outside the purview of statement of cash flows.

Examples:

✓ Conversion of term loan or debt into equity,

✓ Redemption of preference shares by conversion into equity,

✓ Purchase of goods on credit.

Cash flows exclude movements between items that constitute C&CE because these components are part of cash management of an entity rather than part ofoperating, investing or financing activities.

Examples :

✓ Cheques/DD’s deposited in bank

✓ Withdrawal or deposit of cash from/in bank

✓ Cash invested in short term deposit classified as cash equivalent etc.

FAQ’s on Ind AS-7Q7: What is the difference between ‘Bank overdraft’ and ‘Cash credit’ ?

Ans: Bank OD facility is granted by bank usually for a short period to accommodate short term fund requirement. It may be secured by tangible assets or may be aclean OD. OD facilities are linked with the operations in current account.

Cash credit is a fund based facility to finance working capital requirement on a continuing basis. CC is generally secured by hypothecation of inventory and debtors orpledge of goods. It may also be secured by a charge on fixed assets.

Presentation of these items in the CFS _ as per para 8 of Ind AS 7

CC from bank (a facility on a continuing basis, though contractually payable on demand on violation of t&c of sanction,) is considered as a part of financing activitiesand Bank OD forming the part of the cash management is considered as cash equivalent while preparing the CFS.

Q8: What are the examples of cash flows arising from taxes on income to be separately disclosed under cash flows from investing or financing activities ?

Ans: Taxes paid are usually classified as cash flows from operating activities.

Example – if we strictly go by classification of taxes in accordance with the nature of related transaction, tax impact of STCG should be classified as investingactivity. Suppose, entity is incurring business losses, the same gets adjusted against STCG for tax purposes. Accordingly, showing tax impact of STCG and businesslosses separately is impracticable. Therefore, tax paid is usually classified as cash flows from operating activity.

However where it is practicable to identify the tax cash flow with an individual transaction that give rise to cash flows, tax cash flows are classified as investing orfinancing activities.

Examples

✓ Tax payment by way of LTCG on sale of land which was used as PPE

✓ Tax payment on dividend received from a foreign Company shall be classified as investing activity.

✓ DDT u/s 115-O of Income Tax Act, 1961 (Equity and Preference dividend distribution tax) is considered as an integral part of financing activities.

FAQ’s on Ind AS-7

Q8: What are the examples of cash flows which can be reported on a net basis ?

Ans: Generally, all cash flows are reported gross. Cash flows are offset and reported net only in limited circumstances. Cash flows arising from the following Operating,Investing and Financing activities may be reported on a net basis :

❑ Cash receipts and payments on behalf of customers when the cash flow reflect the activities of the customer rather than those of the entity.

❑ Cash receipts and payments for items in which the turnover is quick , the amounts are large, and the maturities are short.

Examples :

✓ Receipt of insurance premium from policy holders and refund of premium on cancellation of general insurance policy to policy holders ( under direct method ofpresenting cash flows from operating activities)

✓ Investment and sale of securities by wealth management companies on behalf of customers ( under direct method of presenting cash flows from operatingactivities)

✓ Receipts and payment by an agent on behalf of principal

✓ Acceptance and repayment of deposits with short maturities

✓ Withdrawal and deposits from/in CC account with bank

Cash flows arising from the following activities of a financial institution may be reported on a net basis :

✓ Cash receipts and payments for the acceptance and repayment of deposits with fixed maturity date

✓ The placement of deposits with and withdrawal of deposits from other financial institutions

✓ Cash advances and loans made to customers and repayment of those advances and loans

FAQ’s on Ind AS-7

Q9: What is the preferred method to report cash flows from operating activities ?

Ans: An entity shall report cash flows from operating activities using either the ‘direct method’ or the ‘indirect method’.

As per Ind AS 7, entities are encouraged to report the cash flows from operating activities using ‘direct method’.

Under direct method, major classes of gross cash receipts and payments are disclosed. However, under indirect method, profit or loss is adjusted for the effects oftransactions of :

a) a non cash nature

b) Deferrals or accruals of past or future operating cash receipts and payments

c) Items of income or expenses associated with investing or financing cash flows

Principally, final reporting conclusions under both methods are same.

Considering voluminous operating transactions of commercial entities, it is difficult to prepare statement of cash flows under direct method as both cash as well asnon cash transactions are recorded in the books of account under accrual system of accounting.

Existing AS 3 “Cash Flow Statement”, permits to report cash flows from operating activities using either direct method or indirect method. With regard to AS-3, IRDAin its master circular on preparation of financial statements of general and life insurance business has specified that all insurers are required to present the statementof cash flows as per Direct Method.

Further as per clause 32 of listing agreement of SEBI, all listed companies are required to present the statement of cash flows as per indirect method principles of AS-3

FAQ’s on Ind AS-7

Q10: Which rate should be used in translating the cash flows denominated in a foreign currency? What is the treatment of unrealized gains and losses arising from

changes in foreign currency exchange rate ?

Ans: Cash flows arising from the transactions in a foreign currency shall be recorded in an entity’s functional currency by applying to the foreign currency amount theexchange rate between the functional currency and the foreign currency at the date of cash flows.

Cash flows denominated in a foreign currency are reported in a manner consistent with Ind AS 21 “The Effects of Changes in Foreign Exchange Rates”

Unrealized gains and losses arising from changes in foreign exchange rates do not give rise to actual inflow or outflow of C&CE. However, the effect of such exchangerate changes on C&CE held or due in a foreign currency is reported separately from cash flows from operating, investing and financing activities in order to reconcileC&CE as per the statement of cash flows with C&CE as per BS.

Q11: What are the examples of C&CE balances held by the entity that are not available for use ?

Ans: Ind AS – 7 requires an entity to disclose together with management commentary, the amount of significant C&CE balances held by the entity that are notavailable for use. Following are the examples :

a) Balances in Unpaid dividend account

b) Balances in bank account for share for share application money, pending allotment of shares

c) Earmarked bank balances for specific purpose. For example – Bank A/c for debenture redemption, dividend payment etc.

d) Balance in Bank A/c subject to legal restrictions

FAQ’s on Ind AS-7

Q12: What is the classification for interest and dividend paid and received in the statement of cash flows ? How are lease payments under finance lease and

payment towards acquiring a fixed asset on deferred payment basis presented in the statement of cash flows?

Ans: An entity presents cash flows from operating, investing and financing activities in a manner which is most appropriate to its business. The classification byactivity provides information that allows users to assess the impact of those activities on the financial position of the entity and the amounts of its C&CE.

Examples

S.No. Particulars Banks and Financial institutions

Other Entities

1 Interest received on loans and advances given Operating activities Investing activities

2 Interest paid on deposits and other borrowings Operating activities Financing activities

3 Interest and dividend received on investments in subsidiaries, associates and in other entities Investing activities Investing activities

4 Dividend paid on preference and equity shares, including tax on dividend paid on preference and equity shares by other entities

Financing activities Financing activities

5 Finance charges paid by lessee under finance lease Financing activities Financing activities

6 Payment towards reduction of outstanding finance lease liability Financing activities Financing activities

7 Interest paid to vendor for acquiring fixed asset under deferred payment basis Financing activities Financing activities

8 Principal sum payment under deferred payment basis for acquisition of fixed asset Investing activities Investing activities

9 Penal interest received from customers for late payments Operating activities Operating activities

10 Penal interest paid to suppliers for late payments Operating activities Operating activities

11 Interest paid on delayed tax payments Operating activities Operating activities

12 Interest received on tax refunds Operating activities Operating activities

FAQ’s on Ind AS-7

Q13: Provide illustrative examples where reconciliation statement is required to be disclosed between the amounts in the statement of cash flows with the

equivalent items reported in the BS ?

Ans: As per para 45, the amounts should be reconciled with the equivalent items reported in the BS. Reconciliation may be required for certain items :

a) Bank OD which are repayable on demand form an integral part of an entity’s cash management, are included as a component of C&CE in the statement of cashflows. However Bank OD will be included in financial liabilities in BS.

b) Where reporting entity holds foreign currency C&CE balances, these are monetary items that will be restated at the reporting date as per Ind AS 21. Anyexchange differences arising on translation will increase or decrease these balances but will not give rise to cash flows. Accordingly, such unrealized gains orlosses arising from changes in foreign currency exchange rates.

Q14: How should the sale proceeds from a sale and leaseback transaction be reported in the statement of cash flows ?

Ans: A sale and leaseback transaction involves the sale of an asset and the leasing back of the same asset. The accounting treatment of cash flows arising from thesale proceeds of a sale and leaseback transaction depends upon the type of lease involved.

a) If the leaseback is finance lease, then the transaction is a financial arrangement between the lessor and the lessee in substance, whereby the lessor providesfinance to the lessee with the asset as security. – In such a case sale proceeds of the asset should be classified as financing activities in the CFS. Lease financecharges and repayment of lease principal in the future are also required to be reported in the CFS as financing activities.

b) If the leaseback is an operating lease, cash flows arising from sale proceeds of the fixed assets should be recorded as investing activities. The lease payments tobe made in future would be classified as cash flows from operating activities.

FAQ’s on Ind AS-7

Q15: How debt securities purchased at a discount/premium are classified in the statement of cash flows ?

Ans: Cash flows from investing activities represent the extent to which expenditure has been made for resources intended to generate future income and cash flows.Thus actual cash outflow irrespective of discount or premium will be presented as investing activity.

Example – Bonds of face value of INR 5,25,000 are purchased in the market at a discount for INR 5,21,500. In this case, cash outflow of INR 5,21,500 will be presentedin the statement of cash flows under investing activities.

Q16: What is the presentation of cash flows arising out of payments for manufacture or acquisition of assets held for rental to others and subsequently held for

sale in the ordinary course of business ?

Ans: There are certain types of entities whose ordinary activities include routinely renting out assets to others and selling the assets subsequently in the ordinarycourse of business. The proceeds from the sale of such assets are recognized as revenue as per Ind AS 18. The derecognition principles of such assets are described inpara 68A of Ind AS 16.

Para 14 states that cash payments to manufacture or acquire assets held for rental to others and subsequently held for sale as described in para 68A of Ind AS 16 arecash flows from operating activities.

This is in contrast with the normal classification where cash payments made to acquire or manufacture PPE and cash receipts from sale of such assets are classified asinvesting activities.

Q17: Whether comparative figures are required to be presented in the statements of cash flows ?

Ans: Yes. For the purpose of analysis.

Q18: How do you classify purchase and sale of securities in the statement of cash flows ?

Ans : An entity may hold securities for dealing or trading purposes as they relate to the main revenue generating activity of the entity. In this scenario, cash flowsarising from the purchase and sale of such securities are classified as operating activities.

FAQ’s on Ind AS-7

Q19: How do you classify cash receipts and payments arising out of future contracts, forward contracts, Option contracts and Swap contracts ?

Ans: Para 16 amongst other examples of cash flows arising from investing activities, provides as follows :

g) cash payments for future contracts, forward contracts, Option contracts and Swap contracts except when contracts are held for dealing or trading purposes or the payments are classified asfinancing activities.

h) cash receipts from future contracts, forward contracts, Option contracts and Swap contracts except when contracts are held for dealing or trading purposes or the receipts are classified asfinancing activities.

When a contract is accounted for as a hedge of an identifiable position the cash flows of the contract are classified in the same manner as the cash flows of the position being hedged. (Whensuch a contract is accounted for as a hedge, cash flows arising from hedging instruments are classified as operating, investing or financing activities, on the basis of the classification of the cashflows arising from the hedged item. For Eg. When a forward contract is taken for payments of a foreign currency loan and hedge accounting is followed, cash payments and receipts of theaforesaid forward contract is classified as financing activities.

From the above para, it is clear that classification of cash flows from future contracts, forward contracts, Option contracts and Swap contracts depends on whether a contract is accounted for as ahedging instrument for hedged item or not.

Q20: An entity invests in a 10 year bond with a face value of INR 6 lakhs paying INR 2.32 lakhs. The effective ROI is 10%. An entity recognizes proportionate interest income in its statement ofprofit & loss over the period of bond. How the interest income will be treated in the statement of cash flows during the period of bond ? How the maturity proceeds of INR 6 lakhs will betreated in the statement of cash flows ? The entity is not in the business of dealing in securities.

Ans: In the given case, since the entity is not in the business of dealing in securities, INR 2.32 lakhs invested in a bond will be classified as investing activities. There is no cash flow of interestduring bond period, as there is no cash receipt. On Maturity, proceeds of INR 6 lakhs will be classified as investing activity with a bifurcation of INR 3.68 lakhs as interest and INR 2.32 asproceeds towards redemption of bond.

FAQ’s on Ind AS-7

Q21: Ind AS 7 requires disclosure of non cash transactions in the financial statements. Give examples of non-cash transactions ?

Ans: Investing and financing transactions that do not require the use of C&CE are excluded from the statement of cash flows. The disclosure of these significant non-cash transactions is made byway of notes to the financial statements. Examples of non cash transactions :

a) Acquisition of an enterprise by means of issue of equity shares

b) Conversion of debentures or preference shares into equity shares

c) Conversion of term loan into equity shares

d) Issue of bonus shares

e) Reduction of capital under restructuring or reduction of capital

f) Exchange of assets

Q22: What is the meaning of ‘contributed equity’ used in the definition of financing activities ?

Ans: In accounting and finance terms, equity is the residual interest of shareholders in assets after deducting all liabilities (Equity = Shareholder’s fund – liabilities)

Shareholder’s fund = Share Capital + Reserve & Surplus + Money received against share warrants

Thus equity is built up by 2 ways :

Contributed Equity

Retained Earnings

Thus, contributed equity is paid up capital contributed by shareholders. Cash flows arising from changes in contributed equity on account of

a) issue of additional capital,

b) buy back of shares etc are classified as financing activities.

The changes in retained earnings is primarily on a/c of profit or loss earned by the entity.

FAQ’s on Ind AS-7

Q23: Explain how securitization of receivables is presented in the statement of cash flows in the books of originator ?

Ans: No guidance in Ind AS -7. However it may be noted that derecognition of receivables in the books of originator as per Ind AS 109, ‘Financial Instruments’ implies that in substance it is similarto sale of receivables. Amount received from such securitization as early collection of amounts due from customers.

Accordingly, cash flows arising from proceeds from securitization activities derecognized in accordance with Ind AS 109 should be classified as part of operating activities even if entity does notenter into such transactions regularly.

In other cases, where the receivables are not derecognized in the books of the originator in accordance with the requirements of Ind AS 109, the proceeds from securitization arrangement arerecognized as a liability. Therefore, cash flows arising from such transactions should be classified as part of financing activities

Case StudiesCase Study 1 – Foreign Currency Cash Flows

Entity A, whose functional currency is Indian Rupee, had a balance of cash and cash equivalents of Rs. 2,00,000, but no trade receivables or trade payables on January 1, 20X2. During 20X2, theentity entered into the following foreign currency transactions:

▪ Entity A purchased goods for resale from Europe for €1,00,000 when the exchange rate was €1 = Rs. 50. This balance is still unpaid at December 31, 20X2 when the exchange rate is €1 = Rs.45. An exchange gain on retranslation of the trade payable of Rs. 5,00,000 is recorded in profit or loss [€1,00,000 x (50 – 45) = Rs. 5,00,000].

▪ Entity A sold the goods to an American client for $ 1,50,000 when the exchange rate was $1 = Rs. 40. This amount was settled when the exchange rate was $1 = Rs. 42. A further exchangegain of Rs. 3,00,000 regarding the trade receivable is recorded in the statement of profit or loss [$ 1,50,000 x (42 – 40) = Rs. 3,00,000].

▪ Entity A also borrowed €1,00,000 under a long-term loan agreement when the exchange rate was €1 = Rs. 50 and immediately converted it to Rs. 50,00,000. The loan was retranslated atDecember 31, 20X2 @ Rs. 45 = Rs. 45,00,000, with a further exchange gain of Rs. 5,00,000 recorded in the statement of profit or loss.

▪ Entity A therefore records a cumulative exchange gain of Rs. 13,00,000 (5,00,000 + 3,00,000 + 5,00,000) in arriving at its profit for the year.

▪ In addition, Entity A records a gross profit of Rs. 10,00,000 (Rs. 60,00,000 – Rs. 50,00,000) on the sale of the goods.

How cash flows arising from above transactions would be reported in the statement of cash flows under indirect method?

Ans : Particulars Amount

Profit before tax ( 10 lakhs + 13 lakhs) 23 lakhs

Adjustment for unrealized exchange gains/losses

Foreign exchange gain on long term loan (5 lakhs)

Decrease in trade payables (5 lakhs)

Operating cash flow before working capital changes 13 lakhs

Increase in trade payables 50 lakhs

Net cash flow from operating activities 63 lakhs

Cash flow from financing activities 50 lakhs

Net increase in cash & cash equivalents 113 lakhs

Cash & cash equivalent at the beginning of the year 2 lakhs

Cash & cash equivalent at the end of the year 115 lakhs

Case StudiesCase Study 2 – Subsidiary acquired in the year

Solution

Particulars Amount

Profit before tax 70000

Adjustment for non cash items

Depreciation 30000

Operating cash flow before changes in working capital 100000

Decrease in inventory (30000-4000 -35000) 9000

Decrease in trade receivables (54000-8000-50000) 4000

Decrease in trade payables (24000)

Expenditure/income to reported as investing/financing activities

Interest paid 4000

Taxes paid (11000+15000-12000) (14000)

Net cash flow from operating activities 79000

Cash flow from investing activities

Cash paid to acquire subsidiary (74000-2000) (72000)

Net cash flow from investing activities (72000)

Cash flow from financing activities

Interest paid (4000)

Net cash flow from financing activities (4000)

Net increase in cash & cash equivalents 3000

Cash & Cash equivalents at the beginning of the year 5000

Cash & Cash equivalents at the end of the year 8000

Disclosure in Balance SheetClassification of Cash & Bank balances in the Balance Sheet _ as per Ind AS-7

i. Cash & Cash equivalent shall be classified as

a) Balance with Banks (of the nature of cash & cash equivalents)

b) Cheques, drafts on hand

c) Cash of hand

d) Others (Specify nature)

ii. Bank balances other than cash & cash equivalents as above, shall be disclosed below cash & cash equivalents on the face of the BS.

iii. Earmarked balances with Banks (like – Unpaid dividend) shall be disclosed separately.

iv. Balances with banks to the extent held as margin money or security against the borrowings, guarantees, other commitments shall be disclosed separately.

v. Repatriation restrictions (if any) in respect of cash & bank balances shall be separately stated.

The disclosure regarding “Bank balances other than cash & cash equivalents” should include items such as :

1. Balances with banks to the extent of held as margin money or security against borrowings, guarantee etc.

2. Bank deposits with original maturity of more than 3 months but less than 12 months

Note: The non current portion of above balances will have to be classified under the head “Other Non-Current Assets” with separate disclosure thereof. Like Bankdeposits with more than 12 months remaining maturity shall be disclosed under “Other non current financial assets”.

Disclosure in Balance SheetClassification of Cash & Cash equivalents in the Balance Sheet _ as per AS-3

i. Cash & Cash equivalent shall be classified as

a) Balance with Banks (of the nature of cash & cash equivalents)

b) Cheques, drafts on hand

c) Cash of hand

d) Others (Specify nature)

ii. Earmarked balances with Banks (like – Unpaid dividend) shall be disclosed separately.

iii. Balances with banks to the extent held as margin money or security against the borrowings, guarantees, other commitments shall be disclosed separately.

iv. Repatriation restrictions (if any) in respect of cash & bank balances shall be separately stated.

v. Bank deposits with more than 12 months maturity shall be disclosed separately.

“Other Bank balances” would comprise of items such as 1. Balances with banks to the extent of held as margin money or security against borrowings etc

2. Bank deposits with more than 3 months maturity.

3. Bank deposits with more than 12 months maturity will also need to be separately disclosed under the sub

head “Other Bank balances”

The non current portion of above balances will have to be classified under the head “Other Non-Current Assets” with separate disclosure thereof.

Disclosure in Balance Sheet

0

50

100

150

200

250

300

350

Cash Flow from OperatingActivities

Cash Flow from InvestingActivities

Cash Flow from FinancingActivities

Cash & Cash Equivalents

Chart Title

F.Y. 2008-09 F.Y. 2009-10 F.Y. 2010-11 F.Y. 2011-12 F.Y. 2012-13 F.Y. 2013-14

F.Y. 2014-15 F.Y. 2015-16 F.Y. 2016-17 F.Y. 2017-18 F.Y. 2018-19