index, currency and futures options

DESCRIPTION

Index, Currency and Futures Options. Finance (Derivative Securities) 312 Tuesday, 24 October 2006 Readings: Chapters 13 & 14. Known Dividend Yield. Same probability distribution for stock price at time T if: Stock starts at price S 0 and provides a dividend yield = q - PowerPoint PPT PresentationTRANSCRIPT

Index, Currency Index, Currency and Futures and Futures

OptionsOptionsFinance (Derivative Securities) 312

Tuesday, 24 October 2006

Readings: Chapters 13 & 14

Known Dividend YieldKnown Dividend Yield

Same probability distribution for stock price at time T if:• Stock starts at price S0 and provides a

dividend yield = q• Stock starts at price S0e–qT and provides no

incomeReduce current stock price by dividend

yield, then value option as though stock pays no dividends

Option PricingOption Pricing

Lower Bound for Calls• c S0e–qT –Ke –rT

Lower Bound for Puts• p Ke–rT – S0e–qT

Put-call Parity• p + S0e–qT = c + Ke–rT

Black ScholesBlack Scholes

T

TqrKSd

T

TqrKSd

dNeSdNKep

dNKedNeScqTrT

rTqT

)2/2()/ln(

)2/2()/ln(

)()(

)()(

02

01

102

210

where

Binomial ModelBinomial Model

In a risk-neutral world the stock price grows at r – q rather than at r when there is a dividend yield q

The probability, p, of an up movement must therefore satisfy

pS0u + (1 – p)S0d = S0e(r-q)T

so that: pe d

u d

r q T

( )

Index OptionsIndex Options

Suppose that:• Current value of index is 930, dividend yields

of 0.2% and 0.3% expected in first and second months

• European call option with exercise price of 900 expires in two months

• Risk-free rate is 8%, volatility is 20% p.a.

What is the price of the option?

Index Options Index Options

Using Black Scholes:• d1 = 0.5444, d2 = 0.4628

• N(d1) = 0.7069, N(d2) = 0.6782

• c = 930 x 0.7069e–0.03(2/12) – 900 x 0.6782 e–0.082/12

= $51.83

Portfolio InsurancePortfolio Insurance

P

A

Suppose the value of the index is S0 and the strike price is K• If a portfolio has a of 1.0, the portfolio

insurance is obtained by buying 1 put option contract on the index for each 100S0 dollars held

• If is not 1.0, the portfolio manager buys put options for each 100S0 dollars held

K is chosen to give the appropriate insurance level

Portfolio InsurancePortfolio Insurance

Suppose that:• Portfolio has a beta of 1.0, worth $500,000• Index currently stands at 1000• Risk-free rate is 12%, dividend yield is 4%,

volatility is 22% p.a.• Option contract is 100 times the index

What trade is necessary to provide insurance against the portfolio value falling below $450,000 in the next three months?

Portfolio InsurancePortfolio Insurance

Using Black Scholes, p = $6.48• Cost of insurance = 5 x 100 x 6.48 = $3,240

If index drops to 880:• Portfolio drops to $440,000• Option payoff = 5 x (900–880) x 100 =

$10,000

Portfolio InsurancePortfolio Insurance

What if beta was 2.0?• Choose K = 960 (Table 13.2)• p = $19.21• Since beta is 2.0, two put contracts required for each

$100,000• Cost of insurance = 10 x 100 x 19.21 = $19,210

If index drops to 880:• Portfolio drops to $370,000• Option payoff = 10 x (960–880) x 100 = $80,000• Cost of hedging is higher (more put options, higher K)

Currency OptionsCurrency Options

Denote foreign interest rate by rf

When a U.S. company buys one unit of the foreign currency it has an investment of S0 dollars

Return from investing at the foreign rate is rf S0 dollars

Foreign currency provides a “dividend yield” at rate rf

Currency Option PricingCurrency Option Pricing

Lower Bound for Calls• c S0e–rf T –Ke –rT

Lower Bound for Puts• p Ke–rT – S0e–rf T

Put-Call Parity• p + S0e–rf T = c + Ke–rT

Black ScholesBlack Scholes

T

Tf

rrKSd

T

Tf

rrKSd

dNeSdNKep

dNKedNeScTrrT

rTTr

f

f

)2/2()/ln(

)2/2()/ln(

)()(

)()(

0

2

0

1

102

210

where

Black ScholesBlack Scholes

F S e r r Tf

0 0 ( )

Tdd

T

TKFd

dNFdKNep

dKNdNFecrT

rT

12

20

1

102

210

2/)/ln(

)]()([

)]()([

Futures OptionsFutures Options

Call futures option allows holder to acquire:• Long position in futures • Cash amount equal to excess of futures price over

strike price at previous settlement

Put futures option enables holder to acquire:• Short position in futures • Cash amount equal to excess of strike price over

futures price at previous settlement

PayoffsPayoffs

If futures position is closed out immediately:• Payoff from call = F0 – K

• Payoff from put = K – F0

where F0 is futures price at time of exercise

Advantages over Spot Advantages over Spot OptionsOptions

Futures contract may be easier to trade than underlying asset

Exercise of the option does not lead to delivery of the underlying asset

Futures options and futures usually trade in adjacent pits at exchange

Futures options may entail lower transaction costs

Put-Call ParityPut-Call Parity

Strategy I: buy a European call on a futures contract and invest Ke-rT of cash

FT ≤ K FT > K

Buy Call 0 FT – K

Invest Ke–rT K K

Total K FT

Put-Call ParityPut-Call Parity

Strategy II: buy a European put futures option, enter a long futures contract, and invest F0e-rT

FT ≤ K FT > K

Long Futures FT – F0 FT – F0

Buy Put K – FT 0

Invest F0e-rT F0 F0

Total K FT

Put-Call ParityPut-Call Parity

If two portfolios provide the same return, they must cost the same to set up, otherwise an opportunity for arbitrage exists

c + Ke-rT = p + F0e-rT

Binomial PricingBinomial Pricing

Suppose that:• 1-month call option on futures has a strike

price of 29• In one month the futures price will be either

$33 or $28Futures Price = $33Option Price = $4

Futures Price = $28Option Price = $0

Futures price = $30Option Price = ?

Binomial PricingBinomial Pricing

Consider a portfolio:• Long futures, short 1 call futures option

Portfolio is riskless when 3– 4 = – 2 = 0.8

3– 4

–2

Binomial PricingBinomial Pricing

Riskless portfolio:• Long 0.8 futures, short 1 call futures option

Value of the portfolio in one month:• 3 x0.8 – 4 = –1.6

Value of portfolio today (r = 6%):• –1.6e–0.061/12) = –1.592

Value of futures is zero, so value of option must be $1.592

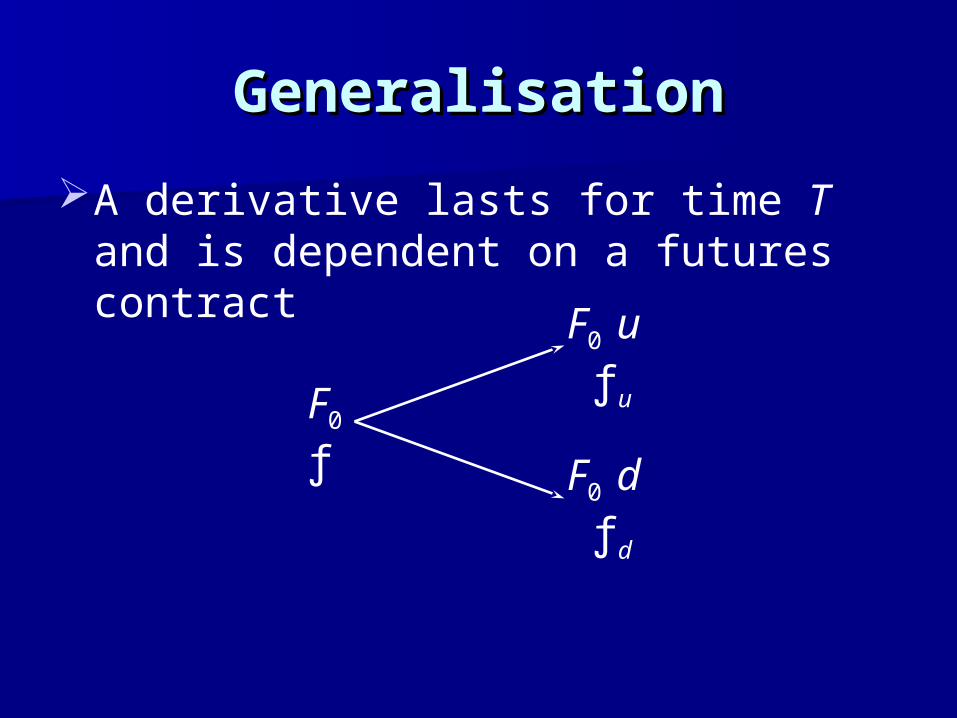

GeneralisationGeneralisation

A derivative lasts for time T and is dependent on a futures contract

F0 u ƒu

F0 d ƒd

F0

ƒ

GeneralisationGeneralisation

Consider the portfolio that is long futures

and short 1 derivative

The portfolio is riskless when:

F0u F0 – ƒu

F0d F0– ƒd

ƒu df

F u F d0 0

GeneralisationGeneralisation

Value of portfolio at time T:• F0u – F0 – ƒu

Value of portfolio today:• (F0u – F0 – ƒu)e–rT

Cost of portfolio today: • –f

Hence ƒ = – [F0u – F0 – ƒu]e–rT

GeneralisationGeneralisation

Substituting for we obtain

ƒ = [ pƒu + (1 – p)ƒd ]e–rT

where

du

dp

1

Dividend YieldDividend Yield

Valuing futures is similar to valuing an option on a stock paying a continuous dividend yield

Set S0 = current futures price (F0)

Set q = domestic risk-free rate (r )Setting q = r ensures that the expected

growth of F in a risk-neutral world is zero

Dividend YieldDividend Yield

Futures contracts require no initial investment

In a risk-neutral world the expected return should be zero

Expected growth rate of futures price is thereforezero

Futures price can therefore be treated like a stock paying a dividend yield of r

Black’s ModelBlack’s Model

TdT

TKFd

T

TKFd

dNFdNKep

dNKdNFecrT

rT

10

2

01

102

210

2/2)/ln(

2/2)/ln(

)()(

)()(

where

Futures Price v Spot Futures Price v Spot PricePrice

European Options• If a European call (put) futures option matures

before futures contract, and futures prices exceed spot prices, it is worth more (less) than the corresponding spot option

• When futures prices are lower than spot prices (inverted market) the reverse is true

Futures Price v Spot Futures Price v Spot PricePrice

American Options• If futures prices are higher than spot prices,

an American call (put) on futures is worth more (less) than a similar American call (put) on spot

• When futures prices are lower than spot prices (inverted market) the reverse is true