india automobiles sector - credit suisse

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

22 August 2017 Asia Pacific/India Equity Research

Automobiles & Components

India Automobiles Sector Research Analysts

Jatin Chawla

91 22 6777 3719

Vaibhav Jain

91 22 6777 3968

THEME

The distinct path towards EVs

Figure 1: Ownership cost already at par/lower for fleet vehicles

Source: Company data, Credit Suisse estimates

■ EVs will soon be relevant in India. The general view is that whilst EVs

are very relevant in the global context, India is a long way off from seeing

any wide-spread adoption of EVs. This might be true for passenger cars

(where most of the global focus is) but we believe all other segments will

see EV adoption much faster than expected, as the benefit of driving an EV

compared to ICE goes beyond 20%. The change in economics will be

driven by (1) falling battery prices, (2) economies of scale for EVs, (3) BS

VI implementation, and (4) fuel price vs electricity cost being favourable.

■ Urban public transport will be the first to move to EVs. Given the long

distances covered per day, the cost economics for public transport vehicles

will be favourable much earlier than for personal transport vehicles. The

three key issues with EVs currently are infrastructure for charging, limited

range and high upfront costs. All these issues can be addressed by moving

to swapping where the biggest constraint will be the standardisation

technology, which is not a major challenge for buses & 3W. For both,

almost 70% of sales could be EVs by 2025. Bajaj with a dominant share

and high margins in 3W is most vulnerable with ~25% of earnings at risk.

■ Personal transport needs further reduction in battery prices. The

economics for EVs is not favourable currently for both 2W and personal

cars, however, this can change in a few years if battery prices continue to

decline at their current rate of 10% p.a. We believe 2W shift will happen

faster as 2W do not need an expensive fast charging network. Moreover,

given the lower barriers to entry on EVs, we will see new competitors

emerging in 2Ws. For cars, penetration will be driven by fleet segment

where EVs already make sense. Fleets are likely to spend on their own

charging network. It might make sense for the government to bring back

incentives on plug-in hybrids as even in 2025, EVs <10% for cars.

-15% -14%

-4%

-1%

-5%-1%

1%

9% 8% 10%16% 16%

25% 18%

26%

-20%

-10%

0%

10%

20%

30%

2W Cars 3W Fleet Bus

2017 2021 2025

Cost benefit of driving an EV over ICE (total cost of ownership)

22 August 2017

India Automobiles Sector 2

Focus charts Figure 2: Decline in solar tariffs—key driver for

focus on EVs in India

Figure 3: BS-VI will result in a ~10% increase in ICE

prices; with battery price decline gap closing

Source: MNRE, Credit Suisse research Source: Credit Suisse estimates

Figure 4: Post 2020 and with battery prices at

US$130; payback period will come down to ~2 years

Figure 5: 3W, car fleet and buses to have a very

high share of EVs; 2W too will start moving

Source: Credit Suisse estimates Source: Credit Suisse estimates

Figure 6: Bajaj's 3W business—both market share

and margins at risk from EVs

Figure 7: Total cost of ownership of EV vehicles' will

be beneficial for all segments in FY25E

Source: Company data, Credit Suisse estimates Source: Credit Suisse estimates

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Dec

’10

Dec

’11

Dec

’12

Jan’

14

Feb

’15

Jun’

15

Aug

’15

Sep

’15

Oct

’15

Nov

'15

Jan'

16

Apr

'16

Jun'

16

Sep

'16

Dec

'16

Feb

'17

May

'17

Solar tariffs in India (Rs/unit)

-

2.0

4.0

6.0

8.0

10.0

12.0

2W PV CV

Increase in vehicle price due to BS VI changes (%)

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2W PV

2017 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

Cars (inc fleet) 2W 3W Buses

Share of Evs in 2025 Penetration

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3W PV share 3W gasoline/CNGshare

3W small dieselshare

3W large dieselshare

Bajaj's share in 3W Passenger vehicles

(Rs/km) ICE EV ICE EV Preferred Mode

2W 3.2 3.7 3.3 2.8 Charging

Cars 16.1 18.7 16.1 13.9 Charging

3W 2.8 2.9 2.7 2.1 Swapping

PV fleet 9.1 9.1 8.8 7.5 Charging

Bus 42.5 44.6 44.3 35.2 Charging/

Swapping

2017E 2025E

22 August 2017

India Automobiles Sector 3

The distinct path towards EVs

EVs will soon be relevant in India as well

The general view is that whilst EVs are very relevant in the global context; India is long

way off from seeing any wide-spread adoption of EVs. This might be true for passenger

cars (where most of the global focus is) but we believe all other segments will see EV

adoption much faster than expected, with economics on EVs working out to be far better

than ICE (even without incentives).

The key drivers of this improving economics in India will be (1) falling battery pack prices

which have already declined from US$1,000/KWH in 2010 to US$230/Kwh currently, and

are expected to decline 10% every year for the next few years and fall to US$130/kwh by

2025, (2) economies of scale for EV manufacturers helping them lower prices, (3)

implementation of BS-VI norms pushing ICE vehicle prices up by 10%, (4) the fuel price vs

electricity price economics is already favourable in India, and with the movement of mix

towards solar it could become even more favourable, and (5) range and performance

anxiety going away as products become better. The key challenge will be the lack of any

sort of infrastructure for charging and the willingness of the government to continue with

incentives till 2025, once EV volumes start becoming meaningful.

Urban public transport will be the first to move to EV

Given the long distances covered per day, the cost economics for public transport vehicles

will be favourable much earlier than for personal transport vehicles. The three key issues

with EVs currently are infrastructure for charging, limited range and high upfront costs. All

these issues can be addressed by moving to battery swapping where the biggest

constraint will be the standardisation of technology; which though is difficult but not

impossible for standard products like buses & 3W. The other advantages with swapping is

that the process of charging can be moved to a central location which can then tie-up with

renewable energy suppliers at a lower price. Also, given that batteries can be charged in

ideal conditions might help in increasing the life of a battery.

For both buses & 3W, almost 70% of sales in cities by 2025 is likely to be EVs. This

impending change on 3W is not lost on the OEMs and all of them are ready with their

electric vehicles. We feel the biggest negative impact of this change will be on Bajaj Auto

as it is a dominant player with a 80%+ share on small passenger 3W used in urban cities.

For buses, the cost of handling swapping of batteries is higher, and on cost terms almost

equivalent to installing fast chargers that can be used overnight for charging. Fast

charging might just be a more practical solution but that entails high upfront costs on both

the bus and the charging infrastructure.

Personal transport needs further reduction in costs

For personal transport, the cost dynamics still does not work out as payback periods

currently exceed five years, and we feel the payback period has to be <3 years for a

transition to happen; this could happen by FY21, once battery prices are lower and ICE

cost higher post BS-VI. Within personal vehicles, 2W will transition faster than cars as 2W

do not really need a high cost fast charging network. On 2W, there will be competition from

a number of startups as well since the traditional advantages of a 2W OEM—brand and

distribution are unlikely to play a big role in EVs. We expect >20% of total 2W sold to be

electric by 2025. We could see the entry of Bajaj into scooters with an electric scooter.

On cars, penetration will be driven by fleet segment where EVs already make sense.

Fleets are likely to spend on their own charging network. As such this will limit penetration

of EVs to <10% of the total PV volumes even by 2025. We believe it makes sense for the

government to bring back incentives on plug-in hybrids, once battery costs start coming

down; it will make economic sense. No major threat to Maruti as such, Mahindra will

benefit from the shift towards EVs amongst fleet, given that it has a head start.

Lower battery prices, economies of scale,

BS-VI will drive a shift towards EVs

3W – first to move to EVs, swapping a quick

viable solution

Bajaj with a large share in passenger 3W

vulnerable to the shift

Payback period needs to come down to <3

years for shift in personal vehicles

2W will move to EVs before cars as they do not need a dense fast

charging network

22 August 2017

India Automobiles Sector 4

Valuation table Figure 8: Valuation comparison of global auto majors

Company Currency CMP Market cap P/E (x) EV/EBITDA (x) RoE P/B

(LC) (US$ bn) CY17/FY18 CY18/FY19 CY17/FY18 CY18/FY19 CY17/FY18 CY17/FY18

US

Ford Motor Company USD 11 52.0 6.8 6.4 3.6 4.5 21.4 1.3

General Motors Company USD 35 49.9 5.7 5.7 2.4 2.1 19.0 1.0

Tesla USD 338 56.4 Nm Nm 64.7 28.3 -24.0 11.2

Paccar Inc USD 63 22.0 17.2 15.0 12.7 12.1 20.4 3.1

European

BMW EUR 79 61.8 7.4 7.1 3.0 2.9 14.3 1.0

Daimler EUR 60 78.2 6.6 6.7 4.1 4.2 15.9 1.0

Volkswagen EUR 127 78.8 5.4 5.1 2.8 2.6 12.5 0.6

Volvo SEK 137 26.8 14.9 14.1 6.2 5.7 20.0 2.6

Peugeot EUR 18 18.3 7.8 7.0 1.9 1.6 14.9 1.1

Renault EUR 75 25.9 5.1 4.8 3.5 3.2 12.9 0.6

Fiat Chrysler EUR 11 19.0 5.4 4.9 1.7 1.5 15.2 0.8

Korean/ Indonesia

Hyundai Motor Company KRW 147,000 32.2 6.8 6.1 7.9 7.2 8.0 0.6

Kia Motors KRW 35,500 14.1 5.8 5.1 3.7 3.2 8.9 0.5

Astra International IDR 7,925 26.6 15.8 14.2 13.1 11.8 17.2 2.6

Japanese

Toyota Motor JPY 6,138 158.8 10.1 9.4 8.4 7.9 10.1 1.0

Honda Motor JPY 3,022 49.5 9.0 8.3 8.2 7.4 8.0 0.7

Nissan Motor JPY 1,092 37.6 7.2 6.8 6.8 6.5 11.5 0.8

Suzuki Motor JPY 5,454 20.7 15.1 14.1 4.2 3.9 13.2 1.9

Subaru Corporation JPY 3,878 26.1 9.0 8.6 3.7 3.2 20.7 1.8

Mazda Motor JPY 1,598 24.9 8.3 7.7 10.2 9.2 10.7 0.8

Chinese

SAIC Motor Corp Ltd CNY 30 50.5 9.5 8.8 7.0 6.3 17.7 1.6

BYD HKD 48 18.8 26.5 19.7 9.3 7.8 9.2 2.4

Brilliance China Automotive HKD 21 9.1 21.7 16.3 Nm Nm 18.8 3.8

Dongfeng Motor Group Company HKD 10 9.7 6.8 6.5 11.0 10.7 12.7 0.8

Weichai Power CNY 7 6.6 8.6 7.8 4.3 3.8 10.7 0.8

Great Wall Motor HKD 10 13.7 9.1 8.6 6.2 5.8 19.5 1.7

Guangzhou Automobile Group HKD 16 19.5 11.4 10.1 22.5 20.1 18.5 1.9

BAIC Motor Corporation Limited HKD 7 7.3 7.3 6.4 2.2 1.6 16.5 1.1

Geely Automobile Holdings Ltd HKD 19 13.6 22.2 17.4 7.1 6.9 27.4 5.5

Indian

Bajaj Auto INR 2,741 12.8 18.7 16.4 14.1 11.9 26.1 4.5

Hero Motocorp INR 3,885 11.9 20.4 19.0 13.6 12.5 35.6 6.9

Eicher Motors INR 30,998 12.3 38.2 30.7 23.7 18.9 39.9 12.9

TVS Motors INR 582 4.0 37.2 28.7 21.8 16.6 27.7 9.7

Maruti Suzuki INR 7,498 33.4 27.0 22.9 15.4 12.9 22.0 5.6

Mahindra & Mahindra INR 1,375 13.7 21.3 17.8 14.2 12.2 15.1 3.0

Source: IBES estimates.

22 August 2017

India Automobiles Sector 5

EVs will soon be relevant in India as well The general view is that whilst EVs are very relevant in the global context; India is a long

way off from seeing any wide-spread adoption of EVs. This might be true for passenger

cars (where most of the global focus is) but we believe all other segments will see EV

adoption much faster than expected, with economics on EVs working out to be far better

than ICE (even without incentives). The key drivers of this improving economics in India

will be (1) falling battery pack prices which have already declined from US$1,000/KWH in

2010 to US$230/Kwh currently are expected to decline 10% every year for the next few

years and fall to US$130/kwh by 2025, (2) economies of scale for EV manufacturers,

helping them lower prices, (3) implementation of BS-VI norms pushing ICE vehicle prices

up by 10%, (4) the fuel price vs electricity price economics is already favourable in India,

and with the movement of mix towards solar it could become even more favourable, and

(5) range and performance anxiety going away as products become better. The key

challenge will be the lack of any sort of infrastructure for charging, and the willingness of

the government to continue with incentives till 2025, once EV volumes start becoming

meaningful.

EV benefits to increase to ~20% by 2025

We expect the penetration of EVs to increase significantly in the next few years, as the

benefit of owning an EV compared to an ICE (Internal Combustion Engine) vehicle

increases significantly. Already for public transportation segments like 3W, buses and car

fleets; the total cost of owning an EV is comparable to the cost of an ICE vehicle. This

benefit will only increase in the coming years leading to a wide-spread adoption of EVs in

these segments. Given that cost is the most important criteria for these segments, we

would not be surprised if the share of EVs in this segments reaches ~70% levels. On

personal vehicles like 2W and cars, the cost benefit does not make sense today but here

too by FY21 EVs will be at par with ICE, and with at least some sort of infrastructure

created by the public transport segment we will start seeing some shift towards EVs in

these segments as well, especially in 2W where we believe the move towards EVs will

create a completely new category of smart vehicles.

Figure 9: The economics of EVs will be irresistible in a few years

Source: Credit Suisse estimates

-15% -14%

-4%

-1%

-5%

-1%

1%

9% 8%10%

16% 16%

25%

18%

26%

-20%

-10%

0%

10%

20%

30%

2W Cars 3W Fleet Bus

2017 2021 2025

Cost benefit of driving an EV over ICE (total cost of ownership)

22 August 2017

India Automobiles Sector 6

The shift towards EVs will be driven by a number of factors –

#1 Falling battery prices

Electric vehicles growth seems to be at an inflection stage with continuous fall in battery

prices in the last few years, and rising cost of ICE engines due to tightening norms on

emissions driven by environmental concerns. Battery prices have fallen from a level of

US$1000/kwh in 2010 to below US$250/kwh in 2016. There are market expectations of

another 10% reduction per annum in the next few years, driven by scale as well as

technological advancements. At 10% reduction p.a., prices could reach below US$ 90/kwh

in CY25E.

Figure 10: Battery packs prices have fallen +75%

over the last six years..

Figure 11: ...at 10% reduction p.a., prices will reach

below US$90/kwh in CY25E

Source: Electrek Source: Electrek, Credit Suisse estimates

Scale, technological advancement to help in reduction of battery prices

In terms of incremental capacities, China, the US and Korea will account of majority of the

capacity additions over the next few years. We expect these large-scale capacity additions

to help in reduction of battery prices.

Figure 12: China likely to account for +60% of Li-ion battery capacity by 2020

GWH 2016 capacity 2020 capacity Companies

US 1 38 Tesla, LG Chem

China 16 108 Lishen, CALB, Samsung, BYD, LG Chem, Panasonic,

Boston Power, CATL

Korea 11 23 LG Chem, Samsung

Poland - 5 LG Chem

Total 28 174

Source: Company data, Credit Suisse estimates

Future cost of batteries will be reduced on lower cost of cells (technology changes leading

to higher energy density, lower production cost) and other technological breakthroughs,

which can help reduce the cost of battery pack content. Battery cells currently account for

about 75% of the total cost. In case of cells, Lithium Nickel Manganese Cobalt oxide

(NMC) currently uses Nickel, Manganese and Cobalt in the same ratio (33% each). This

ratio could change from 1:1:1 to 6:2:2 and later to 8:1:1, thus, reducing the share of the

most expensive element, Cobalt, to just 10% from 33% now. Thus, there could be a

-

200

400

600

800

1,000

1,200

2010 2011 2012 2013 2014 2015 2016

Battery pack price (USD/kwh)

Battery pack price (USD/kwh)

-

50

100

150

200

250

2016 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Battery pack price (USD/kwh) At 5% reduction p.a.

At 10% reduction p.a.

Shift from NMC (1:1:1) to NMC (8:1:1) will help

reduce high cost of cobalt

22 August 2017

India Automobiles Sector 7

significant reduction in price of the cells as well as battery packs, which will make batteries

more affordable.

Figure 13: Battery cells account for ~75% of battery pack cost—technological

break-throughs will help in the reduction in battery prices

Source: Credit Suisse estimates

Battery technology still evolving, different chemistries being tried

As the EV market is still evolving and R&D efforts are under way, different companies

have been using different technologies in electric vehicles. Among the key ones which are

being used by leading companies are (1) Lithium Iron Phosphate (LFP), a technology

supported by Chinese OEMs as well as regulators, (2) Lithium Nickel Manganese Cobalt

Oxide (NMC), which is being used by the Japanese, European and American OEMs, and

(3) Nickel Cobalt Aluminium Oxide (NCA) which is being used by Tesla. LFP batteries

have good thermal stability but low energy density whilst NCA batteries have a very high

energy density but lower thermal stability. Increasingly, however, most OEMs are turning

towards NMC technology.

Figure 14: Various types of batteries used in Electric vehicles

Cathode Symbol Key characteristics

Lithium Cobalt oxide LiCoO2 (LCO) Highest energy density but low thermal stability

Lithium Iron phosphate LiFePO4 (LFP) High discharge rate and good thermal stability

Lithium Manganese oxide LiMn2O4 (LMO) High discharge and recharge rates; Low capacity and shorter lifetime

Lithium Nickel Manganese

Cobalt oxide

LiNiMnCoO2

(NMC)

High bursts of energy and long range

Nickel Cobalt Aluminium NCA High energy density with high specific power; Lower thermal stability

Lithium Titanate LTO Long lifecycle, ability to operate at low temperatures, high stability; Low energy

density

Source: Company data, Credit Suisse research

Battery cell74%

Other battery pack content

22%

Thermal battery management

2%

Battery management system

2%

World moving towards NMC, in India initially

LFP will prosper

22 August 2017

India Automobiles Sector 8

Figure 15: NCA, NMC and LCO provide energy density of 200-250 Wh/kg; NMC

scores best on thermal stability

Source: Industry, Battery University

China likely to drive the market given its scale

While Japanese companies were pioneers in electric vehicles, China has the advantage of

being the biggest market for vehicles, and hence, China government/regulatory bodies'

preferences are likely to have a major impact on the way EV market will evolve over the

years. For example, in case of batteries, China is supporting LFP batteries in a big way

over other technologies, as LFP batteries are considered to be safer (even at high

temperatures) but do not provide the same level of energy density (and hence,

performance for similar size/weight) as NMC batteries.

Chinese companies have set up large capacities for LFP batteries, and were earlier

pushing for their use over NMC batteries. In 2016, China government restricted the

availability of subsidies on electric vehicles (a large component) to ones which were using

LFP batteries. However, in 2017, the China government has allowed subsidies on vehicles

with NMC batteries as well. BYD, which is the leading Chinese company for EV, is

expanding its battery capacity on both LFP and NMC technologies. Chinese companies

are also looking to secure Cobalt supplies across the globe, as Cobalt is the most

expensive element in NMC batteries.

#2 Economies of scale on EVs

EV products pricing is very high in India currently

Given the lack of scale for EV manufacturers, both pricing and the specifications for EV

products in the market today are inferior compared to their ICE counterparts. The key

challenge is the significantly higher costs of a BEV powertrain compared to an ICE

powertrain. This results in very low volumes for these products, and hence, much higher

fixed costs per vehicle leading to a very high price.

0

50

100

150

200

250

300

LTO LFP LMO NMC LCO NCA

Energy density (Wh/kg)

Current EVs in India priced at a ~30% premium despite

significantly lower specs

22 August 2017

India Automobiles Sector 9

Figure 16: Current EV models provide less power, top speed and are expensive

as compared to similar ICE vehicles

Price (Rs) Power Torque Battery size Fuel/energy

cost (Rs/km)

Top speed

(kmph)

Maruti Wagon R – VXI 440,100 50kW@6200 rpm 90NM@3500 rpm NA 4.12 150

M&M E2O Plus P4 757,425 19kW@3500 rpm 70Nm@1000 rpm 11 kwh 0.75 80

Maruti Ciaz Sigma Petrol 765,879 68kW@6000 rpm 130Nm@4000 rpm NA 4.67 180

M&M E-Verito D2 ~9,500,000 ~30kW@3500 rpm 91Nm@3000 rpm 16 kwh 1.09 86

Honda Activa 4G 50,846 5.9kW@7500 rpm 9Nm @5500 rpm NA 1.46 80

Hero Electric Optima DX

Li

62,190 NA NA ~1 kwh 0.15 25

All prices are ex-showroom Delhi. Charging cost assumed at Rs 6/kwh for electric vehicles. Source: Company, CS research

With falling battery prices, these firms should be able to improve both specs and reduce

prices to a certain extent, and hence, EV volumes could rise significantly in the coming

years. To show the kind of fixed costs differential today between BEV products and ICE

products, we take an example of Mahindra Electric and Maruti Suzuki financials.

Figure 17: Fixed costs per vehicle will come down dramatically for EV players

once scale starts kicking in

Source: Company data, Credit Suisse estimates

We realise taking Reva is an extreme example since it makes a loss of almost Rs750k per

vehicle; which is higher than the ASP of a Maruti vehicle. However, it just goes to show the

extremely small scale at which the EV industry in India is operating currently. There will be

a massive fixed-cost operating leverage that will play out once volumes start scaling up.

Assuming that an EV company is broadly able to break even in FY21, fixed costs could

come down from Rs900k/vehicle to Rs 200k/vehicle; the decline helping reduce almost the

entire loss. We assume that EV companies will pass on the entire raw material cost

decline to the consumer either in form of better range/power on vehicles or in form of lower

pricing in order to improve volumes. And then by FY25, as volumes continue to scale up;

the fixed costs would come down further. Even assuming a 20% higher level than ICE

vehicles (could actually be lower); the fixed costs would come down to just broadly around

Rs100k/vehicle. This further decline will help absorb the reduction in incentives on EVs.

0

100

200

300

400

500

600

700

800

900

1000

FY17 FY21 FY25

Maruti M&M Electric (Reva)

Fixed costs (Oth exp + Emp costs) per car (Rs '000)

Reva fixed costs per car today are Rs900k

per vehicle vs Rs150k for Maruti

22 August 2017

India Automobiles Sector 10

Government trying to bring in some scale benefits with large orders

Government run firm Energy Efficiency Service Ltd (EESL) has recently floated a tender

for procuring 10,000 electric cars (total EV volumes in FY17 were a tenth of the same) and

4,000 chargers to replace government department vehicles with electric cars.

#3 Increase in costs on ICEs

BS-VI emission norms a key trigger for move towards EVs

We feel implementation of BS-VI emission norms will act as a trigger towards the shift to

EV. With BS-VI, the cost of diesel engine vehicles and 2W are likely to increase by 8-10%.

Combined with this, if battery prices also halve by 2025; the upfront price gap can come

down from almost a ~100% premium today to ~25% premium (without incentives) and

result in a payback of 2-3 year which will make EVs attractive enough for personal use as

well. We believe for fleet the price gap is already attractive if the infrastructure gaps are

addressed, and hence, all kinds of fleets—3W, buses, taxis are likely to move increasingly

towards EVs.

Figure 18: Vehicles will see a 6-10% rise in prices post BS-VI implementation

Source: Credit Suisse estimates

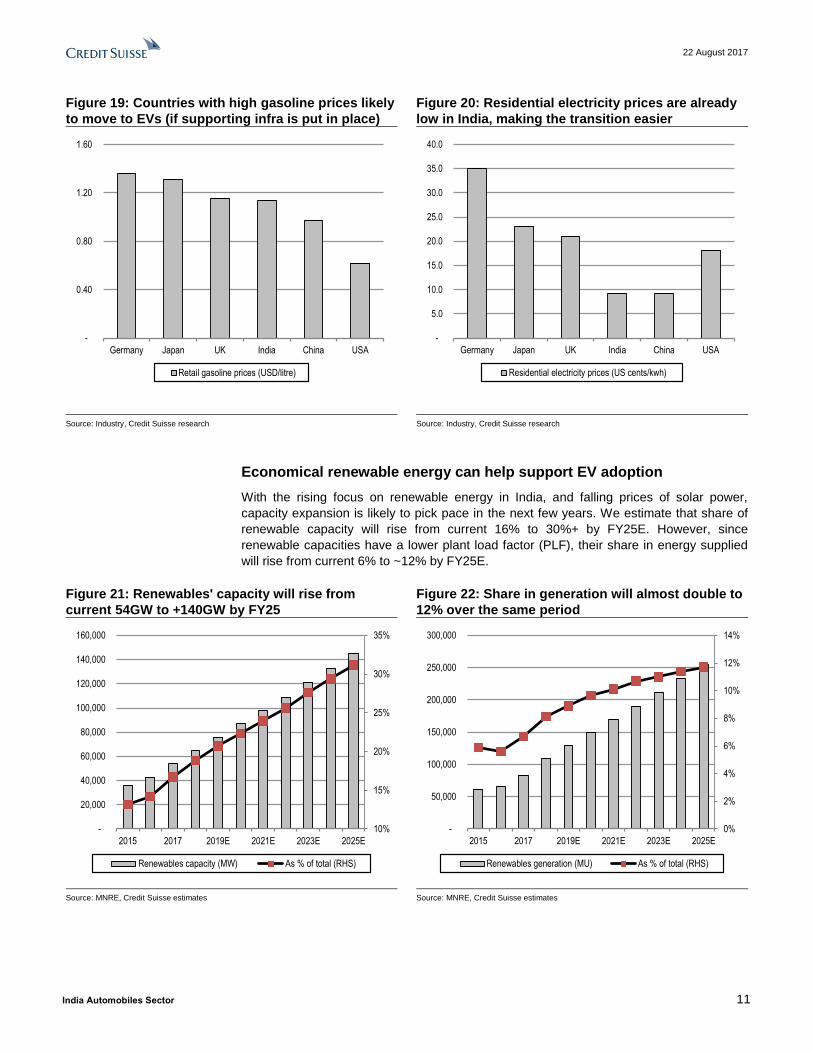

#4 Energy costs already favourable in India

Amongst the key automotive markets; the energy cost equation is favourable in India

From a consumer point of view, the key attraction of an electric vehicle is its lower

operating costs vs ICE vehicles. Hence, countries with high gasoline prices and low

electricity can possibly see an early adoption of electric vehicles, all other factors

remaining same. In India, this equation seems favourable as gasoline prices are high due

to high taxation on retail fuels. At the same time, residential electricity prices are much

lower as compared to that of developed markets, as residential electricity prices are cross-

subsidised by commercial and industrial consumers.

-

2.0

4.0

6.0

8.0

10.0

12.0

2W PV CV

Increase in vehicle price due to BS VI changes (%)

BS-VI will result in a 8-10% price increase

across segments

India has high fuel costs and very low

energy costs; ideal for EV transition

22 August 2017

India Automobiles Sector 11

Figure 19: Countries with high gasoline prices likely

to move to EVs (if supporting infra is put in place)

Figure 20: Residential electricity prices are already

low in India, making the transition easier

Source: Industry, Credit Suisse research Source: Industry, Credit Suisse research

Economical renewable energy can help support EV adoption

With the rising focus on renewable energy in India, and falling prices of solar power,

capacity expansion is likely to pick pace in the next few years. We estimate that share of

renewable capacity will rise from current 16% to 30%+ by FY25E. However, since

renewable capacities have a lower plant load factor (PLF), their share in energy supplied

will rise from current 6% to ~12% by FY25E.

Figure 21: Renewables' capacity will rise from

current 54GW to +140GW by FY25

Figure 22: Share in generation will almost double to

12% over the same period

Source: MNRE, Credit Suisse estimates Source: MNRE, Credit Suisse estimates

-

0.40

0.80

1.20

1.60

Germany Japan UK India China USA

Retail gasoline prices (USD/litre)

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Germany Japan UK India China USA

Residential electricity prices (US cents/kwh)

10%

15%

20%

25%

30%

35%

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2015 2017 2019E 2021E 2023E 2025E

Renewables capacity (MW) As % of total (RHS)

0%

2%

4%

6%

8%

10%

12%

14%

-

50,000

100,000

150,000

200,000

250,000

300,000

2015 2017 2019E 2021E 2023E 2025E

Renewables generation (MU) As % of total (RHS)

22 August 2017

India Automobiles Sector 12

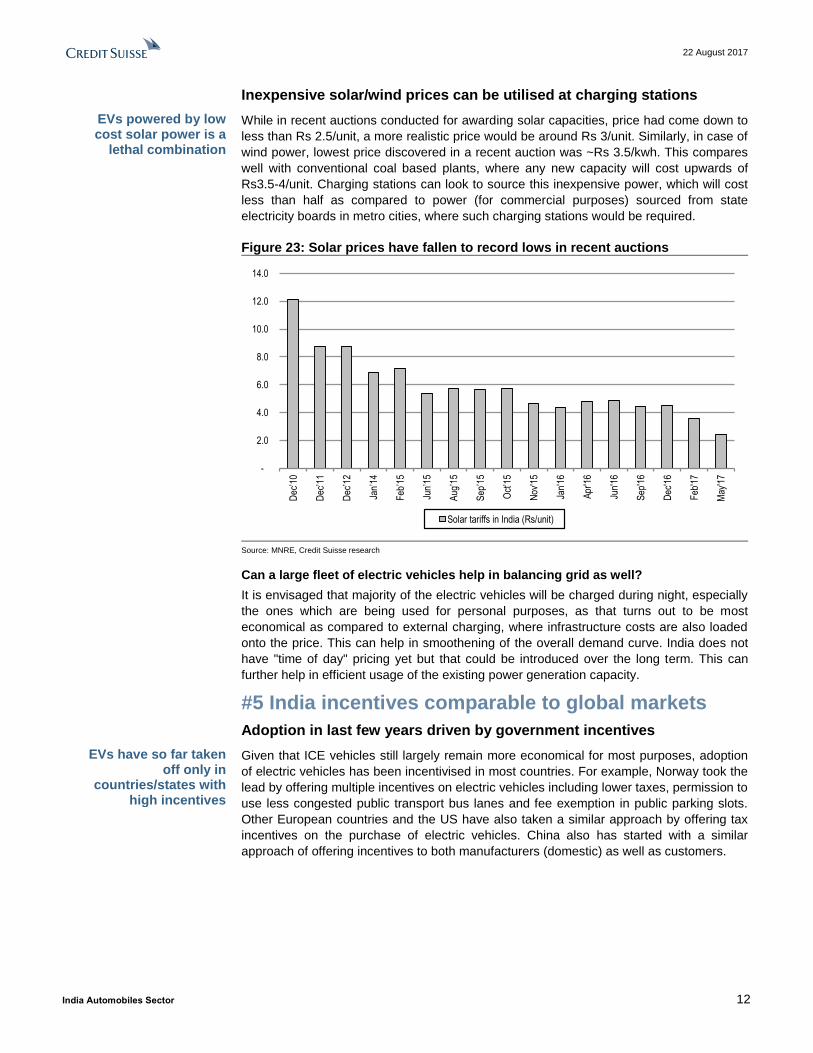

Inexpensive solar/wind prices can be utilised at charging stations

While in recent auctions conducted for awarding solar capacities, price had come down to

less than Rs 2.5/unit, a more realistic price would be around Rs 3/unit. Similarly, in case of

wind power, lowest price discovered in a recent auction was ~Rs 3.5/kwh. This compares

well with conventional coal based plants, where any new capacity will cost upwards of

Rs3.5-4/unit. Charging stations can look to source this inexpensive power, which will cost

less than half as compared to power (for commercial purposes) sourced from state

electricity boards in metro cities, where such charging stations would be required.

Figure 23: Solar prices have fallen to record lows in recent auctions

Source: MNRE, Credit Suisse research

Can a large fleet of electric vehicles help in balancing grid as well?

It is envisaged that majority of the electric vehicles will be charged during night, especially

the ones which are being used for personal purposes, as that turns out to be most

economical as compared to external charging, where infrastructure costs are also loaded

onto the price. This can help in smoothening of the overall demand curve. India does not

have "time of day" pricing yet but that could be introduced over the long term. This can

further help in efficient usage of the existing power generation capacity.

#5 India incentives comparable to global markets

Adoption in last few years driven by government incentives

Given that ICE vehicles still largely remain more economical for most purposes, adoption

of electric vehicles has been incentivised in most countries. For example, Norway took the

lead by offering multiple incentives on electric vehicles including lower taxes, permission to

use less congested public transport bus lanes and fee exemption in public parking slots.

Other European countries and the US have also taken a similar approach by offering tax

incentives on the purchase of electric vehicles. China also has started with a similar

approach of offering incentives to both manufacturers (domestic) as well as customers.

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Dec

’10

Dec

’11

Dec

’12

Jan’

14

Feb

’15

Jun’

15

Aug

’15

Sep

’15

Oct

’15

Nov

'15

Jan'

16

Apr

'16

Jun'

16

Sep

'16

Dec

'16

Feb

'17

May

'17

Solar tariffs in India (Rs/unit)

EVs powered by low cost solar power is a

lethal combination

EVs have so far taken off only in

countries/states with high incentives

22 August 2017

India Automobiles Sector 13

Figure 24: Incentives announced by various countries to support EV adoption

Country Incentives

US Tax credit of up to USD 7500

China Acquisition and excise tax benefit of up to USD 10,000

UK Grant of 35% up to GBP 4500 for cars costing up to GBP 60,000

Germany Euro 4000 for electric cars and Euro 3000 for plug-in hybrids for cars costing up to Euro 60,000

France Incentives up to Euro 6300 on electric and hybrid vehicles

Italy Waiver of ownership tax for a period of five years; 25% rate applicable beyond five years

Source: Company data, Credit Suisse research

The US: Incentives given at both federal and state level to incentivise EV adoption

In case of the US, the approach has been towards incentivising buyers on the purchase of

EVs. Certain states like California also offer attractive incentives which further reduce the

cost of ownership. Hence, it is not surprising to note that California accounted for over

50% of sales in the US.

Figure 25: California accounts for over half of EV sales in the US

Source: Company data, Credit Suisse research

Incentives in India at 30-50% of vehicle price comparable to large EV markets

There are two kinds of incentives on EVs provided by the Central government:

Demand-side incentives under FAME, might be reduced with Phase 2

Demand-side incentive under FAME (Faster Adoption and Manufacturing of (Hybrid &

Electric vehicles). This incentive was introduced in Mar-15 and provides for incentives

depending on technology. Whilst earlier the scheme included mild-hybrid, strong hybrid

(motor capable of driving vehicle), plug-in hybrid (external charging) and pure EVs

(powered by electric motor only); mild-hybrids stand excluded from this scheme from 01

April 2017. The current FAME Phase 1 scheme is valid till 30 September 2017, post which

it is expected that the government will come up with Phase 2 incentives.

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

CY11 CY12 CY13 CY14 CY15 CY16

EV sales in US Sales in California

22 August 2017

India Automobiles Sector 14

Figure 26: Incentives on various vehicles in India

Type of vehicle Technology Incentive (Rs) Product in market

2W Level 1 (<250W), typically lead acid 7500 Hero Electric Opltima DX

2W Level 2 (>250W, typically lead acid) 9400 Hero Electric e-Sprint

2W Adv battery (typically lithium ion) 17000 Hero Electric Opltima DX Li

3W Plug in Hybrid EV 25000 Electrotherm ET Yuvraj

Cars Mild Hybrid (Lead Acid) 13000 Maruti Ciaz

Cars Strong Hybrid (Lithium ion) 70000 Toyota Camry

Cars Electric vehicle (<4m length) (Lithium ion) 124000 Mahindra e20 plus

Cars Electric vehicle (>4m length) (Lithium ion) 138000 Mahindra e-Verito

LCV Electric vehicle (Lithium ion) 187000 Mahindra e-Supro

Source: Company data, Credit Suisse research

Supply-side incentive with a lower GST rate on EVs

Prior to GST, both hybrids and EVs that were taxed had a lower excise duty of 12% earlier

vs comparable vehicles that were either taxed at 12% (if length <4m) or at 24%

(length>4m). Additionally, VAT was levied by States varying from 12.5% to 14%. With the

introduction of GST (whereby State and Central government taxes have been combined)

from 01 July 2017; the incentive on all kinds of hybrids has been removed and pure EVs

are taxed at a GST rate of 12% compared to 28% for cars>4m and 43% for cars>4m.

Additionally, various state governments have their own incentives as well, where they

exempt electric vehicles from road tax, registration charges, etc.

Government also aiming at shared mobility to expedite use of electric vehicles

There is a lot of excitement around EVs currently in the country since the government has

set itself a target of 100% EVs by 2030 both on personal and commercial vehicles. This is

clearly a stretched target, and hence, unlikely to be achieved. The Niti Aayog along with

Rocky Mountain Institute conducted a charrette in Feb-17, and a report was published

which broadly hints at the direction the Niti Aayog might want the government to take on

this.

The charrette came up with an action plan proposed to be taken up by central

government, state governments and city level authorities. The proposed action plans are

trying to tackle the issues of environment and transport infrastructure in one go.

GST prioritises only EVs, no subsidies on

hybrids

EVs – a key element in Niti Aayog's plans for

urban mobility

22 August 2017

India Automobiles Sector 15

Figure 27: Various action items proposed by the charrette organised by NITI Aayog

Action Remarks

Interoperable transport data Sharing of data across various entities including private sector, which can help stakeholders develop optimal mobility

solutions

Metropolitan planning councils City government could combine transit, transport and land use agencies into integrated Metropolitan Council (MPCs)

which can address all modes of transport

Networked city-level innovation and incubation centres Launch of innovation and incubation centres within cities, which can develop new solutions

Feebates Incentives to OEMs and consumers for adoption of clean fuel vehicles; Fee on inefficient vehicles

Zero Emission Vehicle (ZEV) credits Regulation requiring OEMs to sell a minimum percentage of clean fuel vehicles and earn ZEV credits. ZEV credits to be

made tradable.

Policies that encourage Mobility as a Service (MaaS) Additional incentives for electric ridesharing vehicles

Regulations that enable EVSE deployment and

Vehicle-Grid Integration (VGI)

Using power demand from EVs to balance electricity grid and promote use of renewable energy

Manufacturer consortium for batteries, common

components and platforms

Launch a 250MWh battery plant by 2018, and scale up to 1GW production capability by 2020. Develop E-powertrain

systems and other components

Integrated transport hubs Efficiently planned transport hubs with options of last mile connectivity

Enhanced fiscal incentives Revamp FAME to target EV adoption

Non-fiscal incentives Lower registration costs & tariffs, permit exemption, free parking. Establishment of charging infrastructure at key

locations

Standardized, smart, swappable batteries for 2- and 3-

wheelers

Extensive battery swapping infrastructure and integrated payment and tracking system for 2W and 3Ws

EVSE - Electric Vehicle Supply Equipment. Source: NITI Aayog, Credit Suisse research

#6 Better products coming to market

A quick look at the EV products available in the market makes it clear that the current

products in the market are compromised solutions; no wonder EVs have not really tasted

any success. We believe we will soon see much better products coming in the market with

better top speed (comparable to ICE vehicles) and a much better range. Once the market

starts picking up, global OEMs too will start introducing EV solutions for the market. On the

2W side, we believe startups will have a big role to play in coming up with exciting

products and solutions like we have seen in other markets like Taiwan and China.

Figure 28: Most EVs available today do not provide adequate range, speed

OEM Model Battery type Battery size Top speed (kmph) Max range (km)

Passenger vehicles

M&M E2O Plus P2 Li ion 11kwh 80 140

M&M E2O Plus P8 Li ion 16kwh 85 140

M&M E-Verito D2/D6 Li ion 16kwh 86 110

Two wheelers

Hero Electric E Sprint Lead Acid 1.6 kwh 45 80

Hero Electric Optima DX Li Li ion ~1kwh 25 70

Hero Electric Cruz Lithium Ion Li ion ~1kwh 25 70

YoBykes Yo Electron Lead Acid 1.25 kwh 25 70

YoBykes Yo Xplor Lead Acid 1.25 kwh 25 70

Lohia Auto Omastar Lithium Li ion ~1kwh 25 60

Lohia Auto Genius Lead Acid ~1kwh 25 60

Three wheelers

Lohia Auto Humrahi Lead Acid 3.8 kwh 25 80

Lohia Auto Narain Lead Acid 5 kwh 25 100

Kinetic Green Safar Lead Acid 4.8 kwh 25 100

Terra Motors Y4 Alfa Lead Acid 4.8 kwh 25 100

Source: Company data, Credit Suisse research

For EVs to work in India, we need much

better products

22 August 2017

India Automobiles Sector 16

Lack of charging infrastructure though is a challenge

India has around 100,000 km of national highways and another 150,000 km of state

highways. From a fuel pump perspective there are a total of 60,000 fuel pumps in the

country with around 50% of those on highways, 27% in urban and 22% in rural. So broadly

for 250,000 km of highways there are around 30,000 fuel pumps; broadly confirming to the

global averages of a fuel station every 10 km. If we use this same benchmark for EVs and

assume that fast charging stations will be needed at least on highways and urban cities, it

would mean that India should need around ~50,000 charging stations. With the ones in

highways being DC fast charging stations and 10% of those in cities also being fast

charging stations and the remaining 90% being AC stations. With an investment of around

US$30k for each DC station and US$10k for each Level 2 AC charging station, the total

investment in charging infrastructure will be around US$1.5 bn for EVs (excluding land) to

take off in a big way.

Charging infrastructure standardisation can help

We envisage that passenger vehicles will have slow charging infrastructure at home/office

locations. In terms of public charging infrastructure, those will necessarily have to be fast

charging ones. Such stations would be required in the cities for emergency/back-up

purposes, and on the highways for regular usage. Different countries/groups of countries

have come up with their standards for fast charging infrastructure and are advocating use

of the same. Ideally, like fuel for ICE vehicles, charging standards should also be common

across various vehicles, as it reduces the infrastructure cost for the system.

Figure 29: DC charging standards adopted by various OEMs

Origin country Standard OEMs Communication protocol

Japan CHAdeMO Nissan, Mitsubishi, Kia CAN

European SAE Combo Charging System BMW, GM, VW, Ford, Daimler, others PLC

US Tesla supercharger Tesla NA

China GB/T Chinese OEMs, Tesla CAN BUS

Source: Company data, Credit Suisse research

We expect batteries to be sourced from China

China has caught up with Japan and the US, and is now leading the way in electric

vehicles both in terms of setting up large Li-ion capacities as well as faster adoption of

electric vehicles. On one hand, this will help the country address the issue of pollution

which has impacted the quality of life in many large cities. At the same time, this will also

establish China's dominance in both batteries as well as vehicles.

Figure 30: World sales of electric PVs have crossed 700 thousand.. could reach

1 mn mark in CY18

Source: Company data, Credit Suisse research

0

100

200

300

400

500

600

700

800

2011 2012 2013 2014 2015 2016

EV sales in US ('000) Western Europe China Japan

22 August 2017

India Automobiles Sector 17

Urban public transport will be the first to move to EV Given the long distances covered per day, the cost economics for public transport vehicles

will be favourable much earlier than personal transport vehicles. The three key issues with

EVs currently are infrastructure for charging, limited range and high upfront costs. All

these issues can be addressed by moving to battery swapping where the biggest

constraint will be the standardisation of technology; which though difficult is not impossible

for standard products like buses & 3W. The other advantages with swapping is that the

process of charging can be moved to a central location with tie-ups with renewable energy

suppliers at a lower price. Also, given that batteries can be charged in ideal conditions

might help in increasing the life of a battery.

For both buses & 3W, almost 70% of sales in cities by 2025 is likely to be EVs. This

impending change on 3W is not lost on the OEMs, and all of them are ready with their

electric vehicles. We feel the biggest negative impact of this change will be on Bajaj Auto

as it is a dominant player with a 80%+ share on small passenger 3W used in urban cities.

For buses, the cost of handling swapping of batteries is higher and in cost terms almost

equivalent to installing fast chargers to be used overnight for charging. Fast charging

might just be a more practical solution there but that entails a high upfront costs on both

the bus and the charging infrastructure.

Public transportation to first move to EVs given cost economics

The main advantage of EVs over conventional ICE vehicles is the significantly lower

running cost despite the higher upfront cost. The benefit of this lower running costs is thus

best realised by public transport vehicles which run almost 5-7x the number of km that a

personal vehicle would run on an average per day, and that is where the transition to EVs

will happen first.

In the case of public transportation the maintenance cost economics also becomes

significantly meaningful as diesel engines (typically used in public transportation vehicles)

start needing maintenance after 100,000 km; a distance that typically takes around 8-10

years for a private vehicle but a commercial vehicle is likely to reach the same in 2-3 years

itself. Earlier there were concerns on a battery vehicle also needing a battery replacement

after 100-150k km but the modern day BEVs hardly lose any potency (range decline <

10%) even after reaching 100-150k km, and might actually be good for the life of the

vehicle (which is around 250k km).

Figure 31: ICE vehicles have large number of

moving parts…

Figure 32: ... hence, maintenance costs are higher

as compared to EV models

Source: Company data, Credit Suisse estimates Maintenance cost mentioned as % of cost of ICE vehicle. Source: CS estimates

ICE EV

Number of moving parts per vehicle

Less than 20

Over 100

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Public vehicles -ICE

Public vehicles -EVs

Personal vehicles -ICE

Personal vehicles -EVs

Maintenance cost as % of total vehicle cost

22 August 2017

India Automobiles Sector 18

The key challenges for adoption of EVs by public transportation are high upfront costs. At

current battery prices, BEV products are 60-80% more expensive than their ICE

counterparts. Whilst the low running costs still justify going the EV way, funding of the

higher upfront costs is a challenge. Given that there is practically no ecosystem for battery

charging in the country today, public transportation sector will have to set it up and each

segment of public transportation is likely to go with the solution most favourable for it.

Swapping as a possible lower cost solution for India

Swapping can help lower upfront costs and replicate fuel experience

The MNRE under Prof Jhunjhunwala is keen on promoting swapping of batteries as a

possible solution to higher upfront costs. The idea is to sell EVs without batteries and treat

battery like a fuel. This takes care of the upfront cost issue and with a reasonable network

of swapping stations can take care of the range anxiety issue as well. Since batteries can

be swapped within five minutes, in terms of consumer experience also it is very similar to

ICE where it takes 5-10 minutes to get a vehicle refueling done at a pump.

Figure 33: Total running cost for a 3W in a swapping model

Per km model Autos Remarks

Battery life (cycles) 1200 20% higher possible on swapping than normal level of 1000 cycles

Energy requirement (WH/km) 54

Landed cost of battery (USD/kwh) 300 Includes GST and import duties

Range (km) 63 Range dependent on number of swaps (assumed to be two)

Running cost per km (Rs) (A) 0.33

Infra cost per km (Rs) (B) 0.08 Assumed to be 25% of running cost

Kms travelled per day 100

Battery exchanged with utilisation 80% Assumed that users swap the battery at ~80% utilisation

Total km done every year 30,000

Battery cycles consumed in a year 600

Size of battery needed (KWh) 3.40

Capital cost of battery 66,300

Total capital cost incl. interest 83,167 Assumed interest cost of 12%

Total capital cost per km (Rs) (C) 1.39

Total cost per km (Rs) (A+B+C) 1.79

Source: Company data, Credit Suisse estimates

… but swapping has its own challenges

Standardisation of technology not feasible in many segments

The main challenge with swapping even where the cost argument works is the

standardisation of technology so that the same battery can be put in different vehicles.

Standardisation of technology at such an early stage of development of the industry might

not be the right thing to do; it is fine once the technology has matured. Also, OEMs might

not be too keen on sharing technology with competitors.

Economics works only for consistent usage and high asset turnover

The economics of swapping, however, work only for vehicles which run a certain number

of kilometres per day and have a certain consistency around their usage. Since swapping

solves the range anxiety issues, the key with swapping is to use a battery as small as

possible to reduce the upfront capital cost. This will allow for faster utilisation of the total

cycles provided by a battery, and hence, reduce the interest costs on the upfront capital

investment.

22 August 2017

India Automobiles Sector 19

On personal vehicles like 2W and cars, however, the ideal scenario for consumers would

be to swap once a day or once in two days. Since there will be an inconsistency in the

usage patterns for personal vehicles, the range expectations will be 2x the normal daily

usage, thereby, leading to a bigger battery which is swapped only in 2-3 days, leading to

lower asset utilisation. Also unlike a charging station, a swapping station will need

deployment of human resources to conduct the process of swapping as well as to

safeguard the batteries.

These extra costs mean that for 2W and 4W whilst the upfront cost can be brought in line

with ICE with the help of swapping; the total cost per km including electricity, capital cost

of battery including interest, the infrastructure cost of swapping is far higher than the cost

per km on ICE, and hence, users are unlikely to opt for such a solution.

However, in the case of auto-rickshaws (3W) and buses which largely remain within city

limits and also run a consistently high number of kms on a daily basis; swapping model is

definitely workable. The total cost per km on EV 3W and buses with swapping is already

within a 10% band of what the cost is with ICE. The pace at which battery costs are falling;

the costs will be soon comparable and in a few years the costs on EVs will be far lower

than comparable ICE vehicles. Thus in our view, these are the first segments where the

government needs to focus on.

Swapping can also help increase battery life

Without swapping, even for 3W and buses, one will have to move to fast charging. Fast

charging has an impact on the life of the battery. With swapping, the battery can be taken

to a central location and charged under ideal conditions. This can lead to an increase in

the battery life and make the swapping economics even better. Our checks with industry

suppliers suggest that battery life can be increased by more than 50% from the normal

1,000 cycles to 1,500 cycles when batteries are charged under ideal conditions.

Swapping can help take advantage of lower electricity prices and promote

renewables

With on-board charging of batteries, the batteries have to be charged when the customer

brings them to a charging station. However, with swapping, batteries can be charged at an

appropriate time when demand for electricity is lower, and hence, prices are lower than

normal.

However, the real big advantage of a battery swapping network is that the battery network

can be used as a storage of energy. The big problem with renewable energy like solar and

wind is that they do not produce energy consistently but sporadically and at times when it

might not really be needed. Also, the electric grid is designed to deliver electricity rather

than store it, and hence, it is difficult to align supply with demand. However, with a battery

network it can be charged when there is surplus energy. This could imply that this surplus

power can be available at much cheaper rates rather than at peak energy power rates. It

can also give power back to the grid when power demand is high, and thereby, make

money on the difference in power costs between demand and surplus scenarios. In our

calculations above, we have not used this economics that can further reduce gap between

ICE and electric vehicles with swapping.

Cost of fast charging infrastructure is quite high

AC to DC conversion needed to charge vehicles

There are two options of charging an electric vehicle, one is at home and other one is at

an external charging station. The batteries in an electric vehicle require direct current (DC)

for charging. On the other hand, power supplied from electricity grid is AC. In order to use

AC supply to charge the battery, the vehicle needs to have an on-board charger which

increases the cost of the vehicle depending on the size of charger. In the Indian context,

vehicles are unlikely to have "on-board" chargers beyond 2.5-3kW in order to keep cost of

For personal vehicles, the low asset turnover

means that the economics of swapping

does not work out

With swapping, batteries can be charged in ideal

conditions rather than on-board

A battery bank can make some money by

buying cheap electricity and selling it

when expensive

22 August 2017

India Automobiles Sector 20

the vehicle low. These chargers will be used at home/office locations where vehicles can

get charged for few hours.

Fast chargers will be needed outside home/office environment; government trying

to standardise chargers to maximise utilisation

In addition to home chargers, consumers will require external charging stations. These

charging stations can either have an AC output (which will be supplied to on-board

charger) or have DC output using an off-board DC charger installed at the charging

station.

Department of Heavy Industries in India has issued specifications on both AC and DC

chargers. AC chargers or Public metered AC outlets (PMAO) will have a maximum output

power of 3.3kW implying about 40 min of usage to charge a 2W with battery size of

2.2kwh). On the other hand, DC chargers will have a higher output and will be useful for

charging PVs.

Figure 34: Specifications issued by Department of Heavy Industries for charging infrastructure in India

Type Code Max power Max current Output Remarks

Bharat EV AC Charger BEVC-AC001 3.3 kW 15A 230V single phase AC AC input to the vehicle which has on-board chargers

Bharat EV DC Charger 1 BEVC-DC001 10/15 kW 200A 48/72V 2W to have max output of 3.3kwh; Higher power for 4Ws

Bharat EV DC Charger 2 BEVC-DC002 30/150 kW NA NA Current and output details to be provided later

Source: Department of Heavy Industries, Credit Suisse research

However, the cost of fast chargers is likely to be high as it would include (1) cost of

equipment, (2) civil works, (3) cost of land (rentals), (4) manpower costs (5)

operating/maintenance expenses on the equipment, and (6) return on capital. This is in

addition to electricity costs, which may or may not be cheaper than residential electricity

prices depending on sourcing strategy and government regulations.

For personal vehicles like cars & PVs, fast charging needed only once in a while

Our analysis of charging infrastructure indicates that different types of vehicles will have

different options based on the usage pattern as well as viability. For both 2W and cars, we

believe that majority of the charging will be done at either home or office locations as

those will prove to most economical. Since, cost differential is pretty sizeable as compared

to external charging stations, consumers will prefer to use external charging option just as

a back-up in case of emergency. Also, since usage level of personal vehicles will require

charging at an interval of 2-3 days, range anxiety will mostly not be there.

The usage of city based charging stations will be done only in case of emergency

situations and to the extent, that the charge allows the vehicle to reach its nearest

destination. However, in the case of cars, consumers will expect to have the option to take

them out of town and also charge them in a relatively shorter period of time, implying fast

charging option will be needed. For 2W, given the relatively smaller battery size, charging

from a normal AC charging station could also be done in less than an hour. However, for

cars, we will need to have a DC charging station which will increase the cost of the same.

Public vehicles will need fast charging stations due to higher usage

In case of public transportation vehicles like 3W, buses and fleet due to higher utilisation

per day, charging infrastructure requirement will be much higher, as a full charge (done at

night) will not be sufficient to run the vehicle for an entire day. Also, some 3W, fleet

owners/drivers may not have necessary infrastructure at their residential premises. For

buses, bus depots could be used to install fast charging infrastructure.

Given the higher costs, utilisation of fast

charging infrastructure will be low; further pushing up costs

22 August 2017

India Automobiles Sector 21

Figure 35: Effective cost of external charging for a PV fleet

Particulars Amount Units Remarks

(A) Capital cost of charging infra

Charging points 5.0

Life of charging station 15 years

Capability of charging per hour 10 kwh

Capex per charging point 1,000 Rs '000

Interest rate 12%

Amount to be charged per year (EMI) 720.1 Rs '000

Charging duration 2.20 hours For a 22 kwh battery vehicle

Hours of operation 24.0

Utilisation 30% Takes into account low usage during

night, off peak hours and weekends

Total vehicles charged per year per point 5,973

Capital cost - amount charged per vehicle 120.6 Rs

(B) Maintenance cost

Maintenance cost per year 500 Rs '000 At 10% of capex

Maint. cost - Amount charged per vehicle 83.7 Rs

(C) Electricity cost

Units charged in one charging cycle 22.0 kwh

Cost of electricity per unit 6.00 Rs/kwh Can be lower for renewable

Electricity cost - Amt. charged per vehicle 132.0 Rs Assuming full charge

(D) Rental cost

Land required per vehicle 155.0 sq. ft Used Swift Dzire area, and 100%

loading on that

Total area required 775.0 sq. ft

Real estate rental rate p.m. 50.0 Rs/sqft

Real estate rental cost per year 465,000 Rs

Rental cost to be charged per vehicle 77.9 Rs

(E) Manpower cost

Number of attendants 2 Two shifts of 12 hours each

Monthly salary 10,000

Total cost per year 240 Rs '000 Cost calculated assuming 5 charging

stations attended per person

Manpower cost to be charged per vehicle 40.2 Rs

Source: Company data, Credit Suisse estimates

Figure 36: Key components of cost of external charging for a PV fleet

Particulars Cost (Rs) Cost per unit (Rs/kwh) Cost per km (Rs/km) As % of total

Capital cost (A) 120.6 5.5 0.80 27%

Maintenance cost (B) 83.7 3.8 0.56 18%

Electricity cost (C) 132.0 6.0 0.88 29%

Total cost pre-rental,

manpower(A+B+C)

336.3 15.3 2.24 74%

Rental cost (D) 77.9 3.5 0.52 17%

Manpower cost (E) 40.2 1.8 0.27 9%

Total (A+B+C+D+E) 454.3 20.7 3.03 100%

Source: Company data, Credit Suisse estimates

22 August 2017

India Automobiles Sector 22

Figure 37: Operating cost of charging per km for a

2W (external charging station); even running costs

higher than ICE

Figure 38: Cost of charging per km for PV fleet

(external fast charging station); despite higher

capital costs for a fleet EVs already make sense

Source: Company data, Credit Suisse estimates PV assumed to be diesel vehicle. Source: Company, Credit Suisse estimates

3W – fastest adoption likely; swapping both cost

effective & implementable

Despite some concerns on their safety owing to the fact that they can topple easily given

that they run on three wheels, the 3W is a very important part of the urban mobility

ecosystem in the country, given its easy maneuverability on narrow Indian streets clogged

with traffic. There are two kinds of three-wheelers in the Indian market currently—autos

running on CNG, gasoline, diesel and e-rickshaws running on lead acid batteries. Whilst

autos have been around for decades; e-rickshaws have started proliferating in the last few

years as a replacement of the manual cycle rickshaws. We reckon both of these can

swiftly move to lithium ion batteries, as for both of them the swapping model would work

very effectively and unlike the charging network model it would need very low upfront

costs from either the government or the 3W users. There are a number of private

companies (largely battery suppliers) who are interested in setting up the same.

Swapping model already being tried for e-rickshaws and e-autos both

Swapping model is already being tried on e-rickshaws on both lead-acid and lithium ion

batteries. On lead-acid batteries, it is working as a tie-up between the e-rickshaw

manufacturer, the battery supplier (Amara Raja) and the dealer. Dealer premises are

being used to store the batteries for swapping. Given the smaller size of the battery, the

process of swapping is also not very difficult. Even for its pilot project in Nagpur, Ola is

using the swapping model only, with Acme as the provider of batteries & swapping station.

Helps improve availability of finance

One of the biggest advantage of the swapping model on e-rickshaws is that it improves the

availability of financing for the e-rickshaw operator. Given the income level of a typical e-

rickshaw operator it is considered as a very risky loan by most financiers with very high

default rates. However, with the swapping model, the cost of the battery swap also

includes the EDI (Equated Daily Installment) of the vehicle. The OEM is then able to pay

the EMIs in time to the financier. Since these loans get backed by the OEM, the financiers

are more willing to lend, and also willing to lend at a lower interest rate.

0.3

0.2

0.2

0.1

0.2

1.2

0.9

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Capital Maint. Electricity Rental Manpower Total cost ICE - fuelcost

(Rs/km)

0.8

0.6

0.9

0.5

0.3

3.0

5.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Capital Maint. Electricity Rental Manpower Total cost ICE - fuelcost

(Rs/km)

The point of swapping can also be used to

connect EMI on vehicle

22 August 2017

India Automobiles Sector 23

Solves the charging issue as customer has no place to charge vehicle overnight

For 3W particularly, swapping might be an attractive solution as the end customer might

not have a proper place to charge to the vehicle. A quick ride through any of the Indian

cities in the night would suggest that 3W are parked on the road side, and it will be difficult

for the government to provide charging infrastructure for these vehicles to be charged in

the night. Also, these customers might not be willing to spend a lot of time in the day to

charge these vehicles as that is the time they actually make money. Moreover, given the

profile of these customers, they will be really happy if the upfront cost of the vehicle can be

reduced; which can be done by selling the vehicle initially without a battery.

Figure 39: Battery swapping station provided by Acme in Nagpur for Ola 3W

Source: Ola

All major players are ready with their EV products—FY19 could be the EV year

Kinetic has already launched its e-Auto in Nagpur called Safar. The largest player Bajaj

Auto has also claimed that it is ready with its product and will launch it in CY18. Similarly,

M&M which is the largest EV manufacturer in the country is also planning to launch its

electric three-wheeler in the next few months.

We believe electric three-wheelers will start seeing decent traction in FY19 itself. And once

BS-6 norms kick in from FY21, the share of electric three-wheelers will accelerate

dramatically. We expect the share of electric 3W to increase to 25% in FY21 and then to

70% by FY25; by which time we believe ~40% of the existing population of three-wheelers

would be electric. This is one segment where we will not be surprised if the entire

population turned electric by 2030.

ICE 3W account for ~25% of Bajaj's profits; will be negatively impacted

Amongst listed players, Bajaj Auto has the largest exposure to the three-wheeler segment.

Within domestic 3W PVs, it has a 60% share and in the small urban 3W it has a dominant

80% share. We reckon both its share as well as the ~30% profitability that it enjoys in this

business will come under threat from the transition to EVs. The domestic 3W and exports

3W business each account for roughly ~10% each of Bajaj's revenues. Whilst the

domestic 3W business will be challenged first; we would not be surprised if competitors try

to replicate the success in India, in the export markets as well.

22 August 2017

India Automobiles Sector 24

Figure 40: We expect EVs to have a 70% share in

total 3W passenger sales

Figure 41: Bajaj has a dominant share on passenger

vehicles and will be most impacted

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Brief profiles of 3W EV OEMs in India

Kinetic Green Energy and Power Solutions

Kinetic Green is part of Pune-based Kinetic group (which also owns listed company Kinetic

Engineering). The company is present in Electric three wheelers segment. Kinetic has a

manufacturing plant in Ahmednagar, Maharashtra. The company won a large order from

the UP government in early 2016 to supply 27,000 autos at a total value of Rs 4bn. These

products were sold with Lead-acid batteries. In April 2017, Kinetic Green launched an

electric three wheeler with Lithium Ion battery. Kinetic group was earlier present in 2W

business, which was sold to M&M in 2008. The company has a non-compete clause with

M&M on 2W business till 2018.

Lohia Auto

Lohia Auto, founded in 2009, has three major product ranges—electric two wheelers,

electric commercial vehicles and conventional lightweight commercial vehicles (passenger

& carriage). The company has over 100 dealers and is present in over 40 cities in the

country. Among electric 2Ws, while earlier models were equipped with Lead-Acid

batteries, the company has also launched Lithium Ion version of one of the products.

Among electric three wheelers, the products come with Lead Acid batteries only. Lohia

Auto has its manufacturing base in Kashipur, Uttarakhand. The company formed a JV with

US based UM Motorcycles in September 2014, which sells "Renegade" motorcycles in

India.

Buses – difficult choice between creating swapping

infrastructure & creating charging infrastructure

For buses, the cost of swapping and fast charging is almost similar and already marginally

within a 10% range in terms of costs of an ICE bus running intra-city. Intra-city buses are

largely run by government agencies and they would find it difficult to justify the huge

upfront costs associated with an electric bus. Thus, here too swapping should be a

solution that could work but the logistical issues here are not as simple as a three-wheeler.

Given the huge size of the battery, it will need robotic arms to replace the batteries. The

fact that an electric bus typically has batteries in 2-3 different places unlike a three-wheeler

where there is just one stack of batteries, it would make it even more complex. Also, the

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

FY17 FY21 FY25

Total 3W sales Total EV sales

0%

20%

40%

60%

80%

100%

3W PV share 3W gasoline/CNGshare

3W small dieselshare

3W large dieselshare

Bajaj's share in 3W Passenger vehicles

22 August 2017

India Automobiles Sector 25

best benefits of swapping are utilised when batteries are charged at a central location as

that can provide ideal charging conditions to improve battery life. Sun Mobility, a company

headed by Reva founder Mr Chetan Maini is looking to develop a swapping solution for

buses. They have recently tied up with Ashok Leyland for the same.

Figure 42: On buses, the cost of swapping and fast charging is almost similar; fast

charging has higher upfront costs but might be easier to implement

Units ICE Electric with fast

charging

Electric with swapping

Battery cost (landed in India) USD/kwh 300

Capital cost Rs '000 3,000 6,240 3,315

Battery size kwh 150

Cost of the battery Rs '000 2,925

Life of the vehicle years 12 12 12

Annual usage km 50,000 50,000 50,000

Range of the vehicle km 150 150

Battery cycles 1,000 1,000

Life of battery km NA 150,000 150,000

Interest rate 12% 12% 12%

NPV capital cost of vehicle (incl.

battery replacements)

Rs '000 3,000 9,529 3,315

Per month EMI Rs '000 39 125 44

Capital cost per km (A) Rs/km 9.5 30.0 10.4

Maintenance cost

Annual cost Rs '000 450 112.5 112.5

Maintenance cost per km (B) Rs km 9.0 2.3 2.3

Operating cost per km (C) Rs/km 24.0 12.3 31.1

Total cost per km (A+B+C) 42.5 44.6 43.8

Source: Company data, Credit Suisse estimates

22 August 2017

India Automobiles Sector 26

Personal transport needs further reduction in costs For personal transport, the cost dynamics still do not work out as payback periods

currently exceed five years, and we feel the payback period has to be <3 years for a

transition to happen; this could happen by FY21 once battery prices are lower and ICE

cost higher post BS-VI. Within personal vehicles, 2W will transition faster than cars as 2W

do not really need a high cost fast charging network. On 2W, there will be competition from

a number of startups as well since the traditional advantages of a 2W OEM—brand and

distribution are unlikely to play a big role in EVs. We expect >20% of the total 2W sold to

be electric by 2025. We could see the entry of Bajaj into scooters with an electric scooter.

On cars, penetration will be driven by fleet segment where EVs already make sense. Fleet

are likely to spend on their own charging network. As such this will limit penetration of EVs

to <10% of the total PV volumes even by 2025. We believe it makes sense for the

government to bring back incentives for plug-in hybrids, once battery costs start coming

down; it will make economic sense. No major threat to Maruti as such, Mahindra will

benefit to a certain extent from the shift towards EVs amongst fleet, given that it has a

head start.

Growth will take off only when payback period falls to < 3 years

As mentioned earlier, one of the big triggers for the mass adoption for EVs in India will be

the implementation of BS-VI norms in 2020. A 40% fall in battery prices would result in the

payback period on a 2W coming down to just two years from over six years currently.

Figure 43: By 2025, the payback period on ICE could be down to just two years

ICE Battery prices at USD 220 Battery prices at USD 130

Expected distance driven (km) 7,500 7,500 7,500

Capital cost (Rs) 55,000 90,000 72,000

Out of which Battery cost (Rs) 42,900 25,740

Battery cost per kwh (USD) 220 130

Battery cost per kwh including import duty &

GST (USD)

300 180

Battery size (kwh) 2.2 2.2

Electricity cost per kwh (Rs) 6.00 6.00

Range (km) 65 65

Mileage on gasoline (km/litre) 60

Gasoline price (Rs/litre) 70

Running cost per annum (Rs) 8,750 1,523 1,523

Maintenance costs (3% on ICE, half on EV)

(Rs)

1,650 825 825

Total cost per annum (Rs) 10,400 2,348 2,348

Payback (years) 6.3 1.6

Source: Company data, Credit Suisse estimates

Two-wheelers – disruption likely once EVs take off

Existing products are compromise vehicles

The existing electric vehicles in the market are compromise vehicles as the manufacturers,

in order to price them in line with ICE vehicles, have put very low size batteries resulting in

a very poor performance. Most of the existing electric scooters on the road have a top

speed of 25kmph which is much lower than the minimum of 60kmph that a consumer

would want. Thus, the usage of electric scooters today is limited with annual sales of

22 August 2017

India Automobiles Sector 27

around 30k p.a.; only 0.2% of the overall domestic 2W volumes of 17.6 mn units. Clearly,

the current economics is not supportive of a wide-scale adoption until battery prices come

down.

Initial focus on premium products

However, we believe there exists a space for an electric vehicle where the main

positioning is not a lower running costs but positioning it as a smart vehicle. Since an

electric vehicle is amenable to a lot more sensors, and thus, can be made much more

feature rich. This will further increase the cost of the vehicle but it can be positioned as a

premium vehicle and sold in the market. It will still need setting up of a charging network,

and hence, if a startup is going to launch the same, the launch will initially will be restricted

to a few top two-wheeler cities. We reckon the target cities could be the cities which are

the top IT centres in the country as youth in such organisations will be more attracted to a

smart vehicle. Given the large size of the market, even with a 1% ratio of early adopters

there is enough scale for people to get into EVs.

Figure 44: EVs will start gaining traction in FY21;

will continue to scale up thereafter

Figure 45: Premium EV scooters can be relevant for

almost ~45% of the 2W market

Source: Company data, Credit Suisse estimates Source: SIAM, Credit Suisse research

2W – even low cost AC chargers can act as fast charging stations

As highlighted in the section above, the cost of swapping is significantly higher than an

ICE engine since on the 2W side. Moreover, in this early stage of the industry, we do not

expect OEMs to collaborate and work with each other closely towards standardisation.

Standardisation of battery and BMS (Battery Management System) is a must for

swapping. Hence, even if battery costs come down significantly we do not expect 2W to

move towards swapping as in a fiercely competitive industry, it is only fair to expect OEMs

to try and create differentiation, and hence, not share technology with each other. Whilst

swapping does not work; what works for 2W is that given the smaller size of the battery

even an AC charging station (not too expensive) is good enough for fast charging of the

battery.

Different models globally

The two most successful 2W electric vehicle companies in the world are Gogoro from