india infrastructure report.pdf

TRANSCRIPT

Q1 2012www.businessmonitor.com

infrastructure report

issn 1752-5403published by Business Monitor international Ltd.

inDia INCLUDES BMI'S FORECASTS

Business Monitor International Senator House 85 Queen Victoria Street London EC4V 4AB United Kingdom Tel: +44 (0) 20 7248 0468 Fax: +44 (0) 20 7248 0467 Email: [email protected] Web: http://www.businessmonitor.com

© 2011 Business Monitor International. All rights reserved. All information contained in this publication is copyrighted in the name of Business Monitor International, and as such no part of this publication may be reproduced, repackaged, redistributed, resold in whole or in any part, or used in any form or by any means graphic, electronic or mechanical, including photocopying, recording, taping, or by information storage or retrieval, or by any other means, without the express written consent of the publisher.

DISCLAIMER All information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time of publishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business Monitor International accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of the publication. All information is provided without warranty, and Business Monitor International makes no representation of warranty of any kind as to the accuracy or completeness of any information hereto contained.

INDIA INFRASTRUCTURE REPORT Q1 2012 INCLUDING 5-YEAR INDUSTRY FORECASTS BY BMI

Part of BMI's Industry Report & Forecasts Series

Published by: Business Monitor International

Copy deadline: November 2011

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 2

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 3

CONTENTS

Executive Summary ......................................................................................................................................... 5

SWOT Analysis ................................................................................................................................................. 6 India Infrastructure Industry SWOT ...................................................................................................................................................................... 6

Market Overview ............................................................................................................................................... 7 India............................................................................................................................................................................................................................ 7

Building Materials .......................................................................................................................................... 14 Global ....................................................................................................................................................................................................................... 14

Industry Trend Analysis - Building Materials: China To Remain Demand Driver; Developed Markets Offer Little Support .............................. 14 Asia ...................................................................................................................................................................................................................... 20 Industry Trend Analysis - Building Materials: China Still Leading The Charge As Competition Heats Up ........................................................ 20

Industry Forecast Scenario ........................................................................................................................... 26 Table: India Construction And Infrastructure Industry Data ............................................................................................................................... 26 Table: India Construction And Infrastructure Industry Data ............................................................................................................................... 28

Construction and Infrastructure Forecast Scenario .................................................................................................................................................. 30

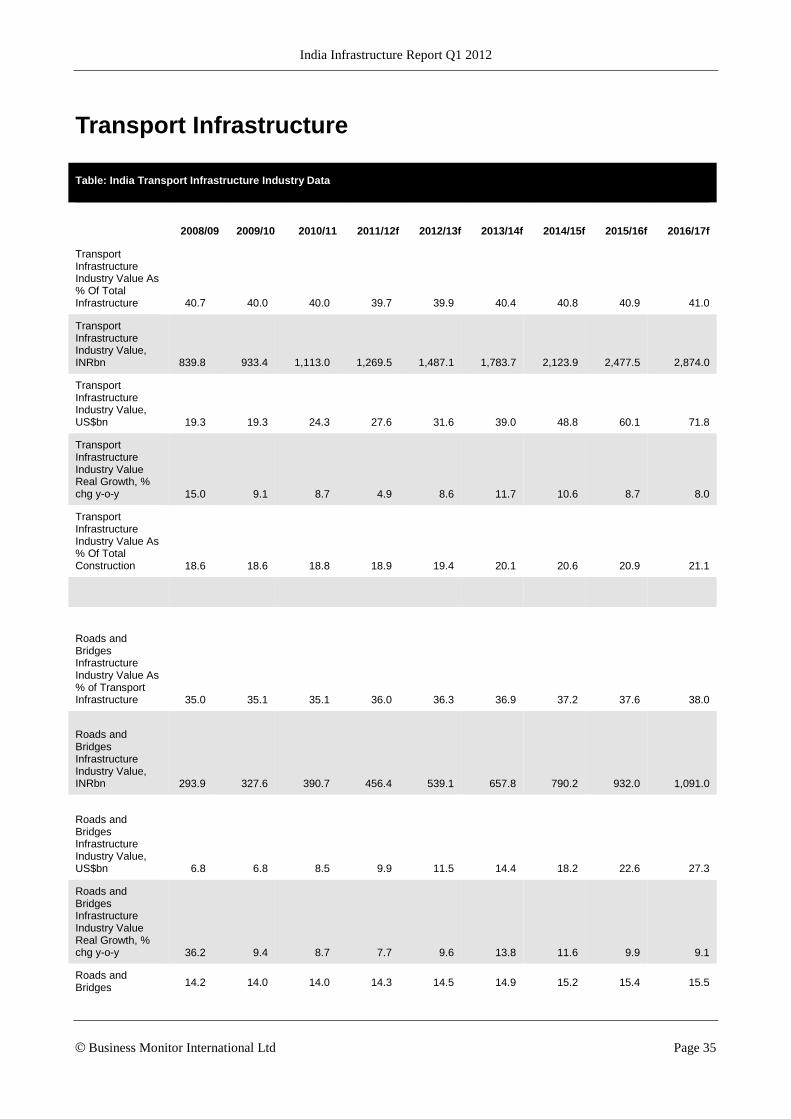

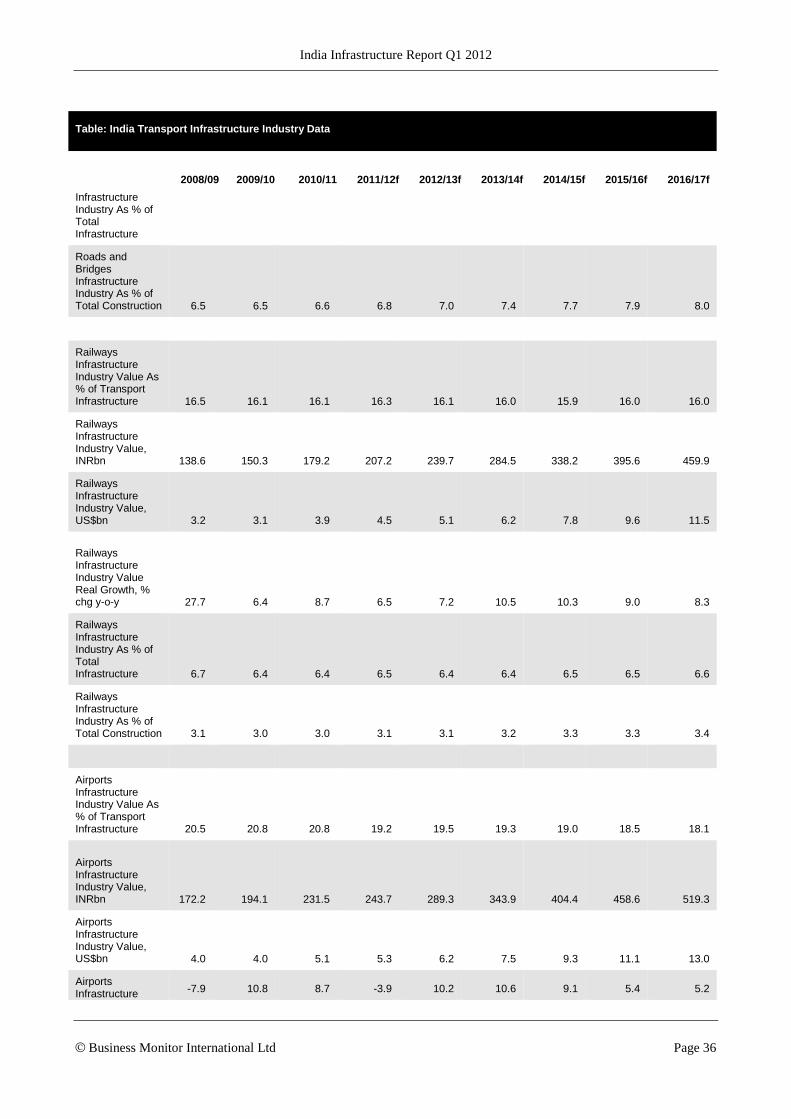

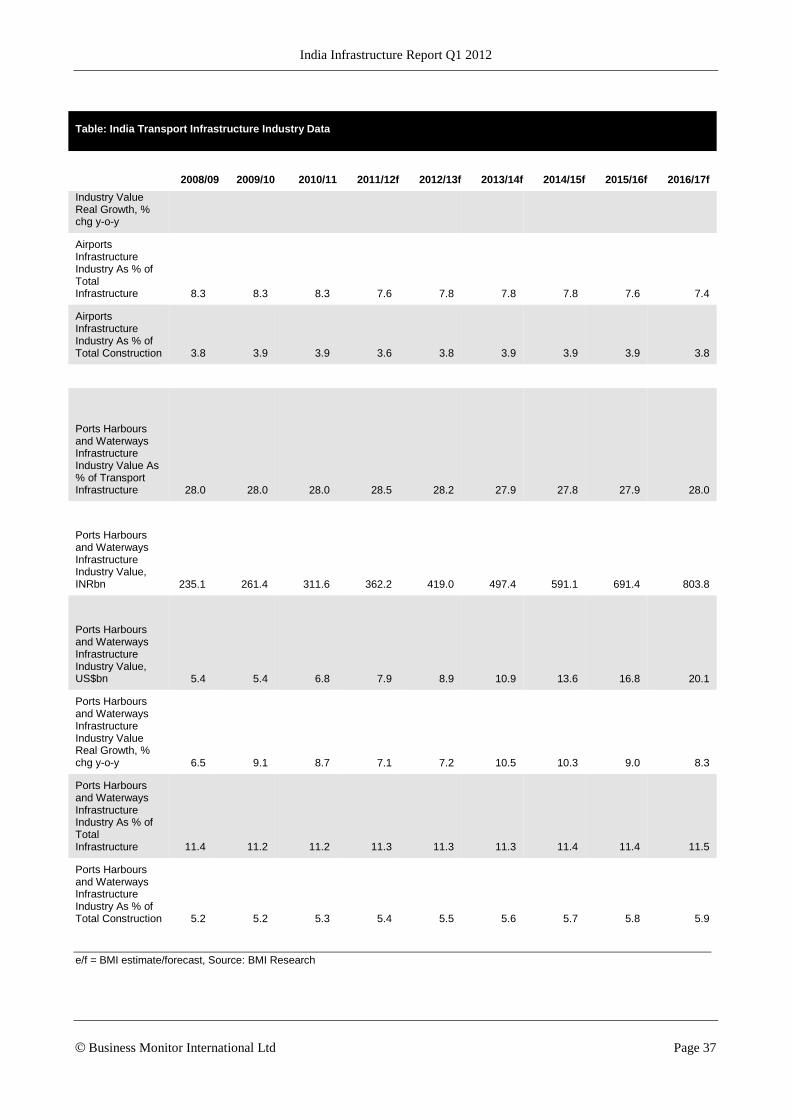

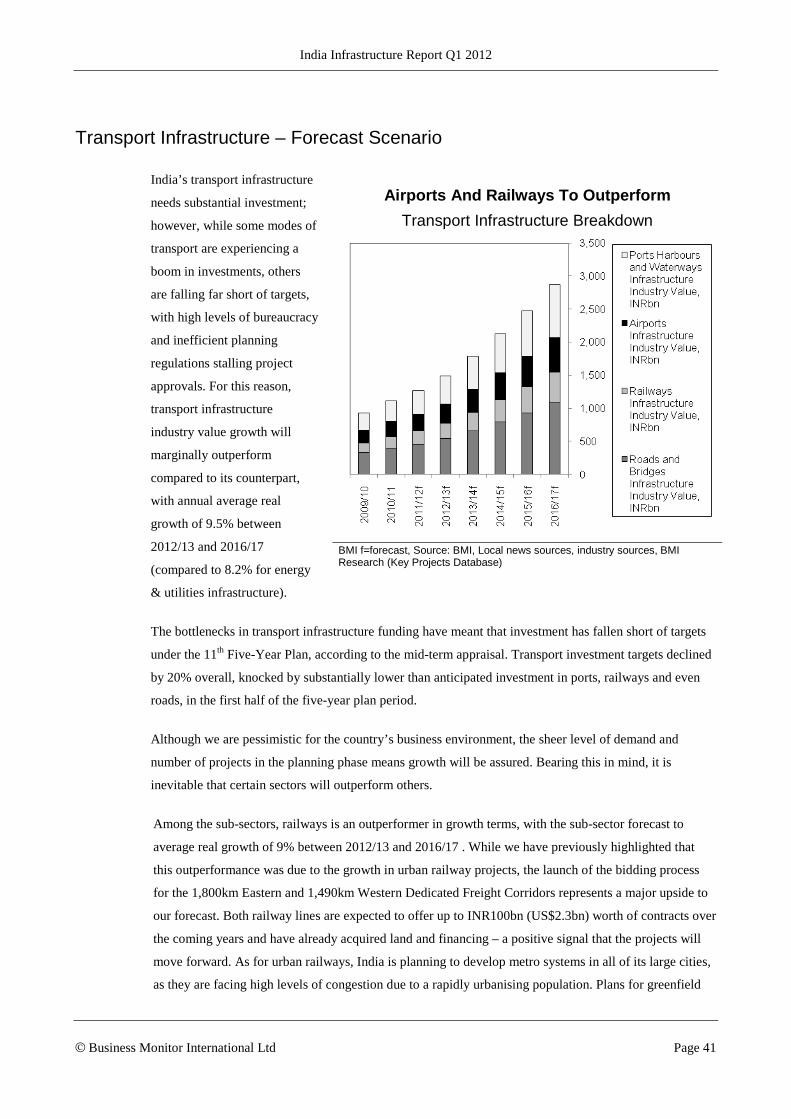

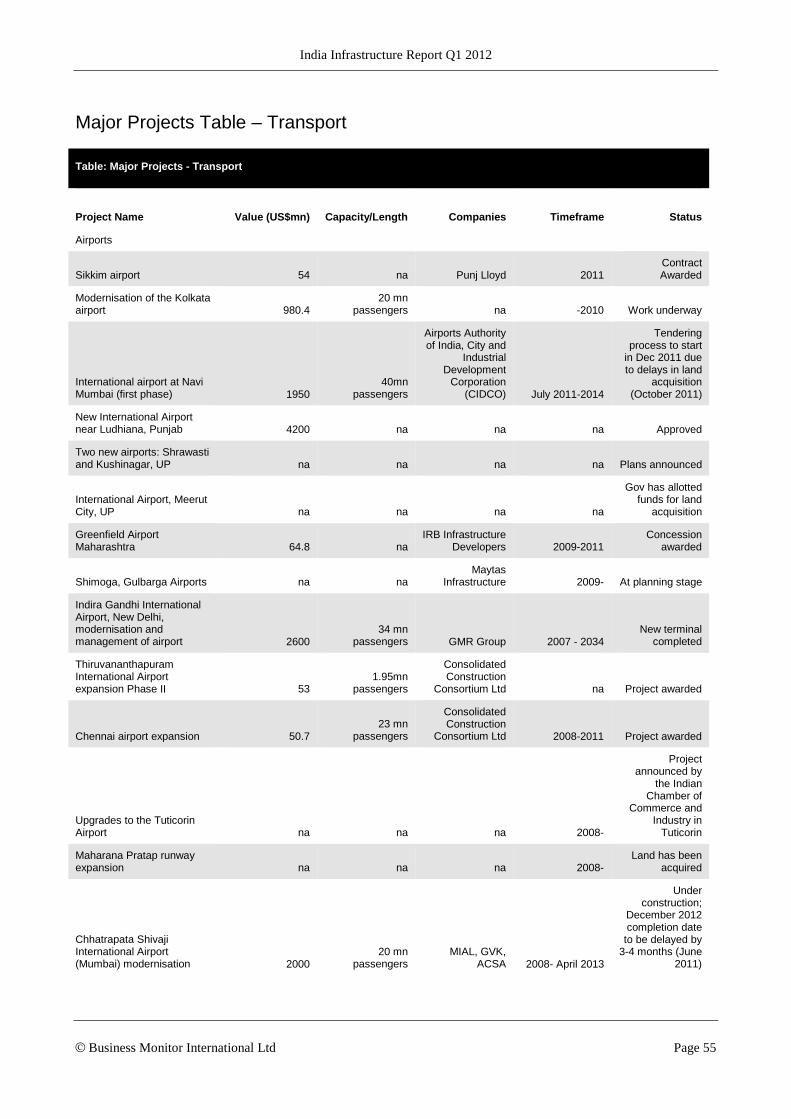

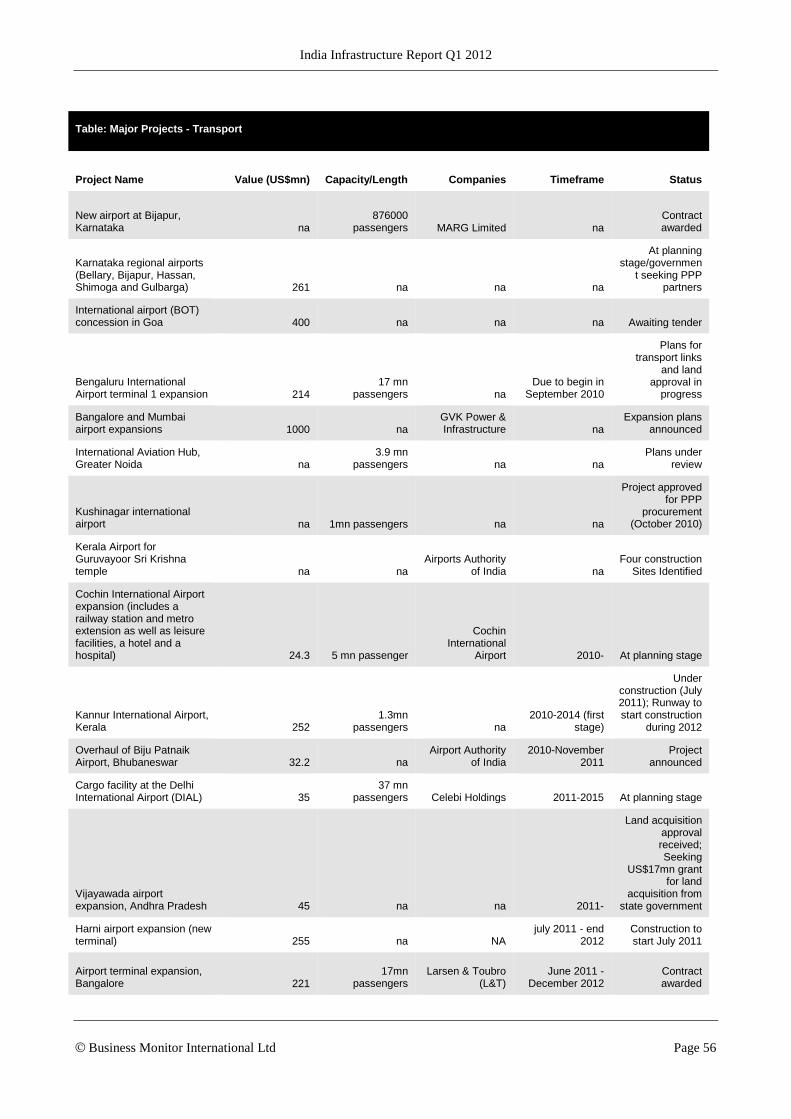

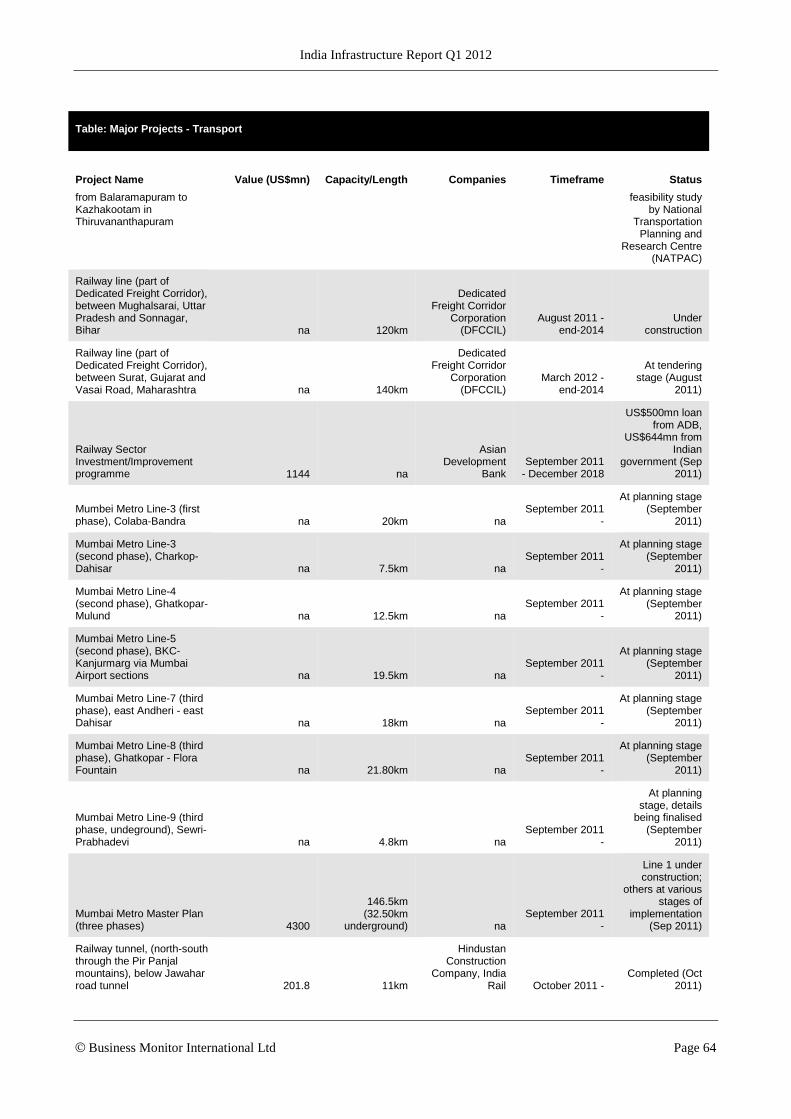

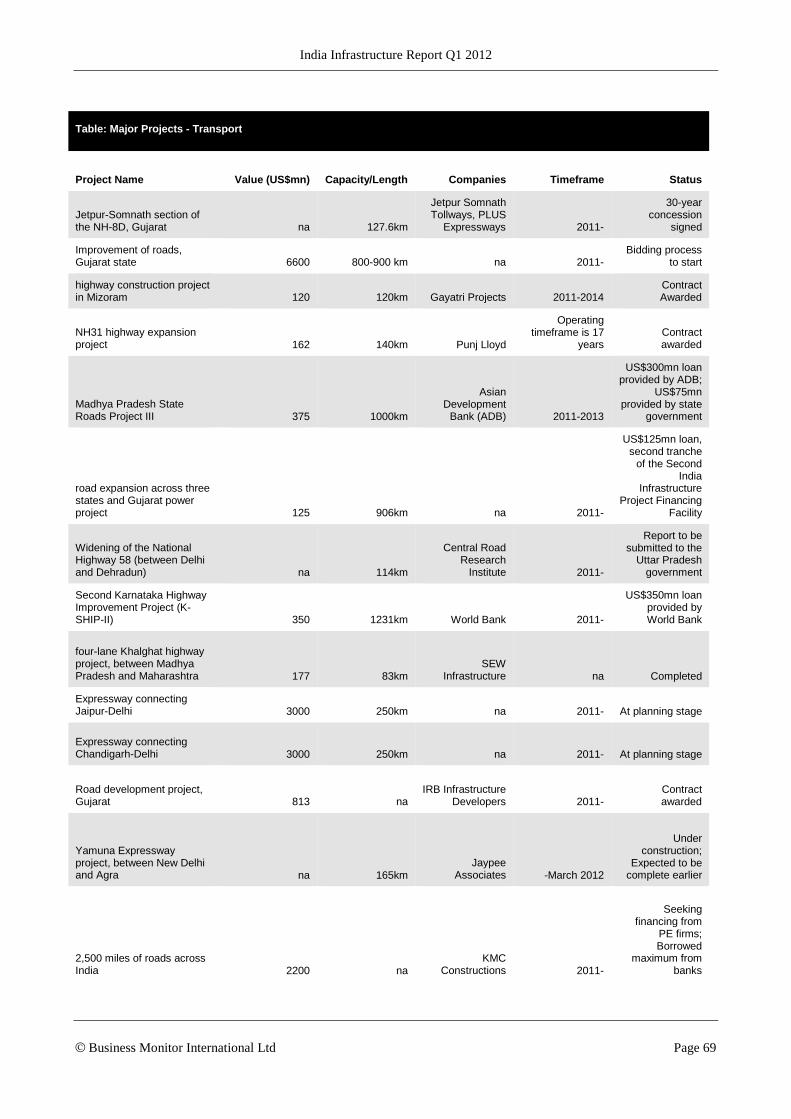

Transport Infrastructure ................................................................................................................................ 35 Table: India Transport Infrastructure Industry Data ........................................................................................................................................... 35 Table: India Transport Infrastructure Industry Data ........................................................................................................................................... 38 Transport Infrastructure – Forecast Scenario ..................................................................................................................................................... 41 Transport Infrastructure Overview ...................................................................................................................................................................... 43 Table: Competitiveness Of India's Infrastructure ................................................................................................................................................ 43 Major Projects Table – Transport ....................................................................................................................................................................... 55 Table: Major Projects - Transport ....................................................................................................................................................................... 55

Energy and Utilities Infrastructure ............................................................................................................... 72 Table: India Energy and Utilities Infrastructure Industry Data ........................................................................................................................... 72 Table: India Energy and Utilities Infrastructure Industry Data ........................................................................................................................... 74 Energy and Utilities Infrastructure Forecast Scenario ........................................................................................................................................ 78

India Electricity Generation Capacity Mix, 2011e .................................................................................................................................................. 79 Energy and Utilities Infrastructure Overview ...................................................................................................................................................... 79 Major Projects Table – Energy And Utilities ....................................................................................................................................................... 94 Table: Major Projects – Energy And Utilities...................................................................................................................................................... 94 Residential/Non-Residential Construction and Social Infrastructure .................................................................................................................114 Table: India Residential and Non-residential Building Industry Data ................................................................................................................114 Table: India Residential and Non-residential Building Industry Data ................................................................................................................114 Residential/Non-Residential Construction Forecast Scenario ............................................................................................................................116

Residential/Non-Residential Construction and Social Infrastructure Overview.......................................................................................................118 Table: World Bank ‘Doing Business’ Report: Global Rankings 2010 ................................................................................................................122 Major Projects Table – Residential/Non-Residential Construction and Social Infrastructure ............................................................................124 Table: Major Projects – Construction And Social infrastructure .......................................................................................................................124

Business Environment ................................................................................................................................ 128 India Business Environment................................................................................................................................................................................128 Rewards ..............................................................................................................................................................................................................128 Risks ...................................................................................................................................................................................................................128

Regional Overview ...................................................................................................................................................................................................130 Asia Pacific Infrastructure Business Environment Ratings ......................................................................................................................................130

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 4

Table: Regional Infrastructure Business Environment Ratings...........................................................................................................................136

Company Monitor ......................................................................................................................................... 137 Gammon India Ltd. .............................................................................................................................................................................................137 Reliance Infrastructure .......................................................................................................................................................................................139 Larsen & Toubro ................................................................................................................................................................................................142

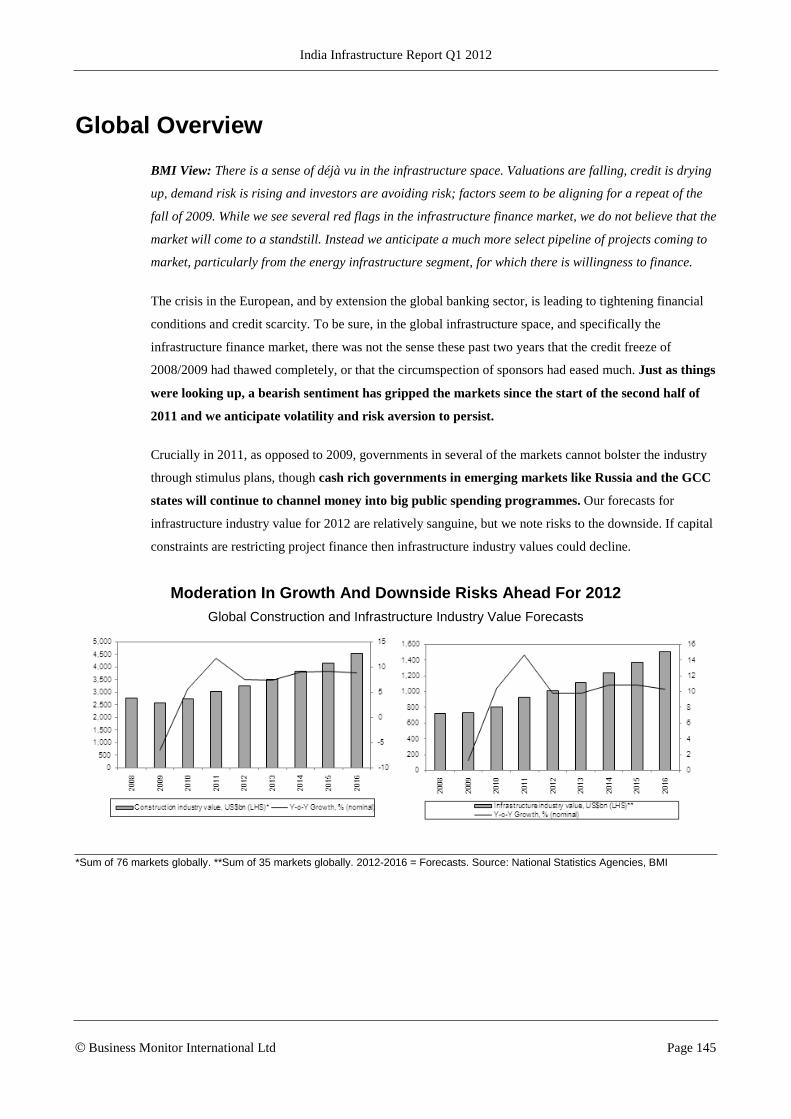

Global Overview ........................................................................................................................................... 145

Methodology ................................................................................................................................................. 152 Industry Forecasts ...................................................................................................................................................................................................152

Construction Industry .........................................................................................................................................................................................153 Data Methodology ..............................................................................................................................................................................................153 New Infrastructure Data Sub-sectors ..................................................................................................................................................................153 Construction .......................................................................................................................................................................................................154 Capital Investment ..............................................................................................................................................................................................155 Construction Sector Employment ........................................................................................................................................................................156

Infrastructure Business Environment Rating ...........................................................................................................................................................157 Table: Infrastructure Business Environment Indicators .....................................................................................................................................158

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 5

Executive Summary

BMI View: Construction activity for the first quarter of FY2011/12 (April-June) was weak, with inflation

and interest rates in India remaining at elevated levels. As such, we continue to hold fast our view of a

prolonged soft patch for the Indian construction sector in FY2011/12, with real growth forecast to reach

4.0% during the fiscal year. Looking further ahead, however, the sector's fortunes are likely to pick up in

FY2012/13, as the government is gearing up for the 12th Five-Year Plan, releasing new infrastructure

projects and addressing concerns about access to long-term financing and land acquisition.

Key drivers affecting growth include:

In October 2011, it launched an INR166bn (US$3.35bn) highways building plan under the

National Highways Development Programme, reports News Resources International. The

plan covers the construction of six-lane highways totalling 6,500km, four-lane highways

totalling 24,700km and the expansion of other highways. The programme is to be funded

through public-private partnerships (PPPs). Under the plan, four expressway construction

projects have already been given the go-ahead, while the country's PPP appraisal committee

has approved 10 roadwork projects, worth a total of US$1.1bn.

In July 2011, GMR won the contract to construct the 555.5km Ahmedabad-Udaipur-

Kishangarh expressway-widening project - the single largest highway project in the country,

both in terms of value and length. It is the first of nine similar highway projects.

In September 2011, three state-run financial institutions - the Indian Infrastructure Finance

Company Limited (IIFCL), Life Insurance Corporation of India (LIC) and India

Development Finance Corporation (IDFC) - signed a memorandum of understanding to

boost the application of takeout financing in India. The MOU would allow the three

companies to take out up to 50% of an infrastructure project's debt, potentially unlocking

about INR300bn (US$6.2bn) in bank debts, which could be used to finance other projects

and speed up the pace of India’s infrastructure development. This enhancement in takeout

financing is critical, as it could mitigate the lack of size and sophistication in India's financial

markets by boosting the liquidity and risk transfer opportunities for Indian banks.

We are forecasting Indian construction industry real growth to reach 6.0% in FY2012/13 and 7.5% in

FY2013/14. These relatively high growth figures indicate that there are still significant opportunities for

greenfield projects in India and is reflected in BMI's key projects database, which shows that there are

more than US$400bn in projects either under construction or in the pipeline in the country's infrastructure

sector.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 6

SWOT Analysis

India Infrastructure Industry SWOT

Strengths Proliferating domestic and offshore infrastructure funds target the Indian infrastructure market, driven by strong demand from the transport, power, urban infrastructure and irrigation segments.

India’s government is keen to facilitate private sector participation in infrastructure. Growing private sector investment in infrastructure – 38 infrastructure PE funds are

currently looking at assets in India, with nine more to be launched in 2011, as cited by Livemint.

Application of takeout financing boosted in India, potentially unlocking around INR300bn (US$6.2bn) in bank debts, which could be used to finance infrastructure developments in India.

Weaknesses Lack of a structured regulatory and policy framework, or well-defined operating and financing regulations – PPP framework and regulations are inconsistent and lack transparency.

The country is overly bureaucratic – this delays the absorption of funds and deters investors.

Project delays, caused by issues with land clearance, and a nebulous bureaucratic system, continue to be a significant problem, with roughly half of planned projects running behind schedule in FY2009/10.

There are low levels of domestic expertise, stemming from a shortage of skilled project managers and engineers.

There is low mechanisation and limited use of modern technological equipment. Downgrades to investment targets under the 11th Five-Year Plan, especially in

transport infrastructure, which has been revised down by 20% in value terms. Limited long-term borrowing capability on the domestic banking sector – immature

bond market.

Opportunities Opportunities for greenfield projects across all infrastructure sub-sectors. There is the opportunity for the domestic industry to become more organised, with the

creation of more large firms through organic growth and acquisitions. This would improve overall construction quality.

Strong population growth and a growing economy is fuelling demand for infrastructure. The government is looking to attract private companies to invest in infrastructure

through public-private partnerships (PPPs). 12th Five-Year Investment plan targeting US$1trn in investment, with 50% to come

from the private sector. Significant investment in electricity generating capacity with ambitious targets,

including 470GW of nuclear power by 2050, 20GW of solar power by 2022 and 20GW of wind capacity by 2020.

Threats India may prove unable to cope with its burgeoning population, which has passed the 1bn mark, posing a major threat to the economy and political situation.

Destructive flooding affects productivity. Obstacles such as red tape, lack of transparency and bureaucratic complexities will

threaten five-year plan implementation. Land clearance issues cause major delays to infrastructure and construction projects.

An inadequate system for compensation and environmental approvals is slowing investments and, in some cases, preventing projects from progressing.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 7

Market Overview

India

Five-Year Plans Overview

Following a conference organised by India's Planning Commission, which included presenting the

findings of the Mid-Term Appraisal (MTA) of the 11th Five-Year Plan (2007/08- 20011/12), India's Prime

Minister Manmohan Singh, has revised down growth targets for the period. However, at the same time,

Singh has announced ambitious targets for the 12th Five-Year Plan, which will run from 2012/13 to

2016/17.

The 11th Five-Year Plan

India's 11th Five-Year Plan (2007/08-2011/12) originally targeted investment of INR20,562bn in

infrastructure, including utilities and transport infrastructure, as well as telecoms and irrigation. However,

based on revised estimates announced in the MTA, as detailed by Daily News & Analysis (DNA) India,

investment is likely to reach INR20,542bn (US$453,856mn) – a difference of around US$430mn.

Although this is very close to target, especially taking into account the difficult economic environment,

investments have been bolstered by better-than-expected interest in the telecoms sector, with transport

infrastructure falling far below expectations. Indeed, investment in telecoms is expected to be 1.59 times

the targeted amount, with 82% of this having come from private sector financing.

A

t

t

h

e

s

a

m

e

t

i

m

e

The 11th Five-Year Plan, Original and Revised Investment Targets, INRbn

Source: Planning Commission

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 8

At the same time, Singh has downgraded real GDP growth forecasts for the 11th Five-Year Plan Period,

stating that average growth is expected to come in at around 8% per year between 2007/08 and 2011/12.

This is down from the 9% targeted for the period and has been in response to around 7% year-on-year (y-

o-y) growth seen over the past 18-24 months. Singh attributes this to a difficult economic environment,

exacerbated by lower food production, which has been caused by below-normal rains in the 2009

monsoon. Although BMI's Asia Country Risk analysts are positive about India, especially in the context

of the global economic situation, the fiscal situation is tempering growth expectations at below 8% y-o-y.

With high levels of public debt pushing interest rates up, this will impact the price of loans within the

country. This in turn will affect private sector access to financing within India, impacting potential

investors as they attempt to raise funding for infrastructure projects.

Indeed, levels of private sector financing have fluctuated considerably over the first half of the 11th Five-

Year Plan, according to the MTA. On the whole, investment from the private sector has fallen below

expectations. Projections for private sector investment have been reduced by 50-80% in some sectors,

such as roads and railways, according DNA India.

Ports

There has been high private sector investment in ports, with 80% of the sector's total investment in the

ongoing plan coming from private sources. This is hardly surprising; the port sector has seen some of the

highest levels of private sector participation. A large number of port terminals are operated by the private

sector, meaning expansion plans are supported by private finance. At the same time, a number of

concessions for terminals have been awarded over recent years.

Airports

Airports have also seen a substantial amount of private sector investment, according to the appraisal,

accounting for around 64% of investment. Once again, this is not a shock, as a number of larger airports

in the country are being operated under concessions. Indira Gandhi International Airport in Delhi is being

run by a GMR-led consortium under a 30-year concession, for example.

Roads And Railways

Despite successes in the port and airport sectors, roads and railways have underperformed in terms of

private sector investment. According to the MTA, just 16% of investment in roads has come from the

private sector and a paltry 4% in the railways sector. In terms of railways, the entire Indian railway

network is run by state-owned Indian Railways, meaning private investors will find it very difficult to

make any gains; however, in the recent 2010/11 budget, plans were put in place to incorporate public-

private partnerships (PPPs) into investment plans.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 9

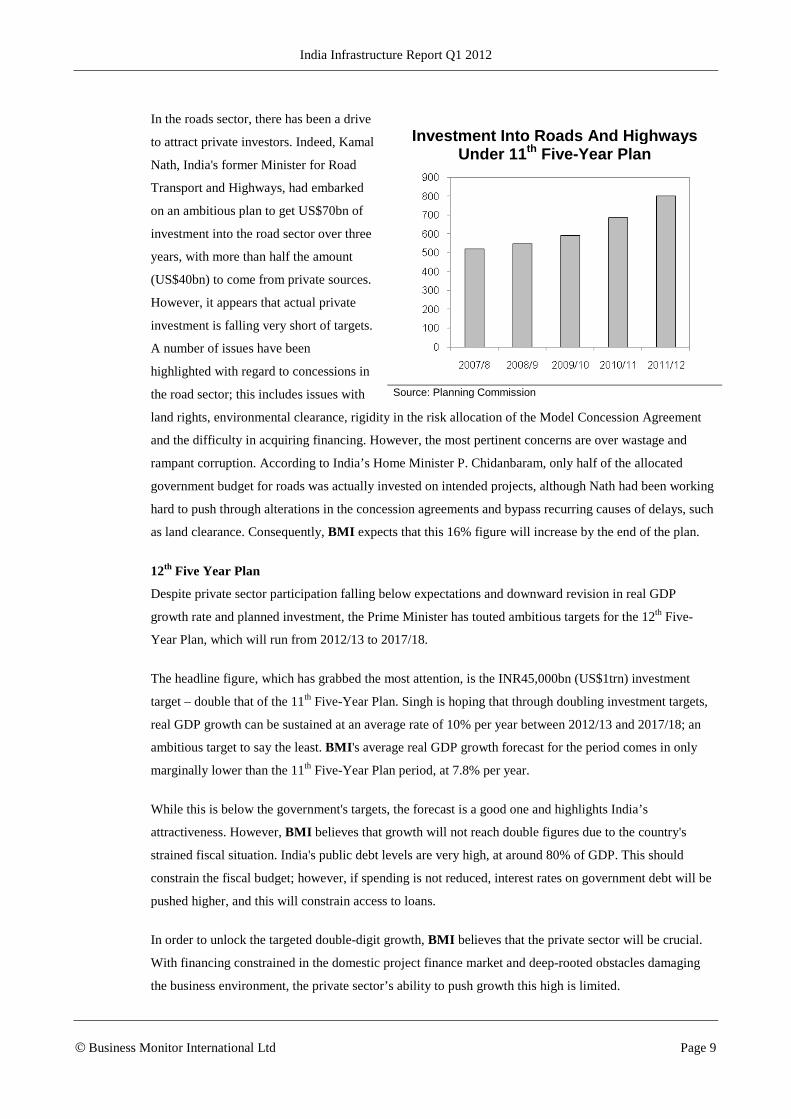

In the roads sector, there has been a drive

to attract private investors. Indeed, Kamal

Nath, India's former Minister for Road

Transport and Highways, had embarked

on an ambitious plan to get US$70bn of

investment into the road sector over three

years, with more than half the amount

(US$40bn) to come from private sources.

However, it appears that actual private

investment is falling very short of targets.

A number of issues have been

highlighted with regard to concessions in

the road sector; this includes issues with

land rights, environmental clearance, rigidity in the risk allocation of the Model Concession Agreement

and the difficulty in acquiring financing. However, the most pertinent concerns are over wastage and

rampant corruption. According to India’s Home Minister P. Chidanbaram, only half of the allocated

government budget for roads was actually invested on intended projects, although Nath had been working

hard to push through alterations in the concession agreements and bypass recurring causes of delays, such

as land clearance. Consequently, BMI expects that this 16% figure will increase by the end of the plan.

12th Five Year Plan

Despite private sector participation falling below expectations and downward revision in real GDP

growth rate and planned investment, the Prime Minister has touted ambitious targets for the 12th Five-

Year Plan, which will run from 2012/13 to 2017/18.

The headline figure, which has grabbed the most attention, is the INR45,000bn (US$1trn) investment

target – double that of the 11th Five-Year Plan. Singh is hoping that through doubling investment targets,

real GDP growth can be sustained at an average rate of 10% per year between 2012/13 and 2017/18; an

ambitious target to say the least. BMI's average real GDP growth forecast for the period comes in only

marginally lower than the 11th Five-Year Plan period, at 7.8% per year.

While this is below the government's targets, the forecast is a good one and highlights India’s

attractiveness. However, BMI believes that growth will not reach double figures due to the country's

strained fiscal situation. India's public debt levels are very high, at around 80% of GDP. This should

constrain the fiscal budget; however, if spending is not reduced, interest rates on government debt will be

pushed higher, and this will constrain access to loans.

In order to unlock the targeted double-digit growth, BMI believes that the private sector will be crucial.

With financing constrained in the domestic project finance market and deep-rooted obstacles damaging

the business environment, the private sector’s ability to push growth this high is limited.

Investment Into Roads And Highways Under 11th Five-Year Plan

Source: Planning Commission

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 10

During the 12th Five-Year Plan, the government is targeting 50% of investment to come from the private

sector, equal to US$500bn. BMI notes that while India remains an attractive market for infrastructure

investors – driven by the strong fundamentals of economic and population growth – this target is an

ambitious one.

Project Finance Concerns

The biggest concern is access to finance, with local bank capacity not really up to providing the sort of

long-term financing needed to support infrastructure projects. Due to the long-term nature of most

projects, loans need to have a term of more than 10 years. However, local banks are unable to provide this

type of financing due to the underdeveloped nature of Indian capital markets, a lack of precedent for long-

term loans, limited liquidity and the fact that banks' funds mature over the medium-term.

In order to get round this problem, in 2006, the government set up the Indian Infrastructure Finance

Company, a government-owned company which provides long-term financing for infrastructure projects.

The company has been very successful, with disbursements having reached US$2bn by the end of March

2010; these were expected to increase significantly by the end of March 2011, to US$4.4bn.

Other ways of increasing financing options have been pursued. The FY2011/12 union budget saw the

Indian government reaffirm its commitment to financing infrastructure, and outlined plans to release

23.3% more funding to the sector than in FY2010/11 – reaching INR2,140bn (US$48bn) in FY2011/12;

this is equal to 17% of total budgetary expenditure. Meanwhile, government authorities involved in

infrastructure development have been allowed to issue tax free bonds, amounting to a total of INR300bn

(US$6.7bn). This includes: the Indian Railway Finance Corporation – INR100bn (US$2.2bn); the

National Highway Authority of India – INR100bn (US$2.2bn); the Housing and Urban Development

Corporation – INR50bn (US$1.1bn); and Ports – INR50bn (US$1.1bn).

In addition, the FY2011/12 budget will provide the government-owned India Infrastructure Finance

Company Limited (IIFCL) with an additional INR5bn (US$1.1bn) for its takeout financing scheme. In

takeout financing, a long-term financing institution such as IIFCL will agree to take an existing loan

(possibly short- to medium-term) off a bank's balance sheet for a price, thus boosting the liquidity and

risk transfer opportunities for Indian banks. This scheme, along with the refinancing services provided by

IIFCL, are essential for the successful implementation of India's 12th Five-Year Plan (2012/13- 2016/17)

due to the lack of size and sophistication in India's financial markets. In August 2011, it was reported that

the IIFCL will take over the management of more than US$131.1bn in loans from the IDBI Bank.

The Indian government has recognised the effectiveness of takeout financing for infrastructure

development and has boosted the scope of the scheme. In September 2011, three state-run financial

institutions - the Indian Infrastructure Finance Company Limited (IIFCL), Life Insurance Corporation of

India (LIC) and India Development Finance Corporation (IDFC) - signed a memorandum of

understanding to boost the application of takeout financing in India. The MOU would allow the three

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 11

companies to take out up to 50% of an infrastructure project's debt, in the ratio of 20:20:10 respectively.

According to Indian Finance Minister Pranab Mukherjee, this takeout financing agreement is expected to

unlock around INR300bn (US$6.2bn) in bank debts, allowing banks to finance other projects and speed

up the pace of infrastructure development in India. Originally, the takeout financing scheme is only

carried out by IIFCL for up to 20% of a project's total cost.

Restrictions on foreign institutions and investors (FIIs), which previously hindered investment in

infrastructure-related bonds, have also been relaxed – another positive move to improve long-term

financing given FIIs' access to deeper and more varied pools of funding. FIIs are now able to invest up to

US$25bn on bonds issued by infrastructure companies, an increase from an original US$5bn. FIIs are also

allowed to invest in unlisted bonds from special purpose vehicles (SPVs) belonging to infrastructure

companies, while new infrastructure debt funds that are exempt from taxes will be created to attract

foreign funds for financing of infrastructure.

In June 2011, the Indian government indicated that the structure for the SPVs for infrastructure financing

– commonly known as infrastructure debt funds (IDFs) – is now in place. The newly-designed IDFs,

which were proposed by Finance Minister Pranab Mukherjee in the Union Budget for 2011/12 (April-

March) and are expected to have a combined value of INR500bn (US$11bn), are aimed at accelerating

and enhancing the flow of long-term debt for infrastructure financing. The government hopes that these

IDFs will entice domestic and overseas institutional investors to commit long-term funding to

infrastructure projects across the country. These investors would most likely include insurance and

pension funds, as their long-term financial obligations make them well suited for financing infrastructure.

As of October 2011, Indian officials are already promoting these IDFs to overseas investors. Economic

Affairs Secretary R Gopalan was in discussion with investors in Singapore and had announced that the

first IDF is set to be launched in the coming two months. The fund is expected to attract US$3bn in

investment, and is currently undergoing the initial process of establishment.

To date, insurance and pension funds have so far played a limited role in India's infrastructure sector. To

boost the investment grade rating of these SPVs and IDFs, the government has launched a new financing

tool known as credit enhancement. According to the Economic Times, the proposal, which was reviewed

by the finance ministry in August 2011, envisages a guarantee by the IIFCL which will subscribe to 25-50

% of the bonds being issued by the infrastructure company. This will be backed by insurance cover from

the Asian Development Bank (ADB) to the tune of 50% of IIFCL's exposure, which in any case enjoys

sovereign guarantee. For example, if a SPV floated by a company for infrastructure development is

raising INR40bn debt through bond issuance, and is approved for credit enhancement, IIFCL will

subscribe to the bonds amounting to INR10bn, with half of these purchased bonds insured by ADB and

the other half enjoying a government guarantee provided by IIFCL. This would boost the SPV’s rating

from BBB to AA, making it investment grade for long-term players such as pension and infrastructure

companies, who are required to invest in bonds with a minimum rating of AA. Credit enhancement will

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 12

therefore help long-term lenders to finance infrastructure projects, while freeing up banks to make

investment that will match their liabilities, which are typically short-term deposits.

The initial phase for credit enhancement is expected to provide funding support for around INR150bn and

has since been expected to direct and indirect equity holders. In Sep 20111, it was reported by Reuters

that the Reserve Bank of India further eased external commercial borrowing policy for the infrastructure

sector by allowing direct and indirect equity holders to provide credit enhancement for domestic debt

raised by Indian infrastructure companies and infrastructure finance companies. The direct foreign equity

holder should have a minimum of 25% of paid-up capital in the debt issuing firm while the in direct

foreign equity holder needs to have at 51%%..

These measures are meant to boost foreign investment – particularly from private equity funds – into

India’s infrastructure sector, and they appear to be proving successful. Over recent years, the private

equity (PE) funds focusing on India's infrastructure sector have increased in number. Perhaps the biggest

is the Macquarie-SBI fund, which is currently in the process of raising US$1.5bn following its first close

in April 2009. Other funds include the US$1.2bn 3i India Infrastructure Fund (the international private

equity company plans to launch a second infrastructure fund of US$1.5bn) and ICICI Venture's US$1bn

India Infrastructure Advantage Fund. More recently, in March 2011, Nomura Securities, Japan's leading

securities company and subsidiary of financial conglomerate Nomura Group, announced plans to raise

US$500mn from Japanese investors for an Indian infrastructure fund. These funds have made an impact

on India’s infrastructure development. Between May and September 2011, six notable PE groups - 3i

Infrastructure , Morgan Stanley , Kohlberg Kravis Roberts , Blackstone Group and JP Morgan

Chase - invested a total of US$1.05bn into Indian companies or infrastructure projects.

According to PE research house Preqin, there are 38 infrastructure PE funds currently looking at assets in

India, with nine more to be launched in 2011, according to Livemint. In total, Preqin notes that the funds

have raised US$9.5bn for investment in India's infrastructure sector and are seeking a further US$7.3bn.

During 2010, 28 deals worth a combined US$2bn were made in India's infrastructure sector, compared to

just 18 deals worth US$333mn in 2009, according to VCCircle research, also cited by Livemint.

PE funds have seen some success, typically investing in a company or an established infrastructure asset.

Indeed, brownfield opportunities are the most popular amongst the PE infrastructure funds, as the level of

risk inherent in existing assets is significantly reduced.

Reform Momentum Can Only Improve

Policy reform, while still sluggish, is starting to move forward, following a virtual standstill in the last

two parliamentary sessions. A key reform is the introduction of a new land bill to repeal the obsolete

Land Acquisition Act of 1894 and replace it with a fresh National Land Acquisition and Rehabilitation &

Resettlement Bill 2011. With the 2012 elections looming large, the land reform bill remains a hot political

topic, with the Indian public still very much against the bill. This is in spite of the unfavourable terms for

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 13

investors, as the financial cost of land purchases is expected to rise significantly under the current

proposals. Construction companies would need to pay twice the market value for urban land and six times

for rural development. In addition, 80% of the families involved will have to give approval for

acquisitions to take place, and the bill would be implemented retrospectively.

Nevertheless, if approved in FY2011/12, as we believe it will be, the legislation could bring much-needed

speed and clarity in a process that has long been cumbersome and incoherent. Indeed, the savings on

approval/litigation/execution cost factors are likely to make the bill a net positive for investors. Project

delays have been a considerable drawback for India's business climate, and any improvements on this

front will certainly help to re-ignite investor enthusiasm.

In Conclusion...

All of these moves and announcements show that the government is moving in the right direction, and is

looking at innovative ways of increasing access to financing for private investors looking to invest in

India's infrastructure market. In order to capitalise on India’s potential, these plans need to be

implemented in a timely manner. At the same time, the issue of transparency and an over-intrusive

bureaucracy needs to be addressed in order to attract investors into the market. The government appears

serious about addressing these issues, and, in order to achieve its ambitious targets in the 12th Five-Year

Plan, it needs to be.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 14

Building Materials

Global

Industry Trend Analysis - Building Materials: China To Remain Demand Driver; Developed Markets Offer Little Support

BMI View: The recent downturn in investor sentiment sparked by growing uncertainty over the US

economic recovery and the ongoing fiscal situation in the eurozone reinforces our core view that demand

for building materials will remain broadly muted in developed economies s through 2011 and into 2012.

With persistent weakness in developed markets and political headwinds still weighing on growth in the

Middle East and North Africa (MENA), demand in China will remain the key factor in determining the

levels of growth in the global consumption of cement and steel over the coming quarters. Meanwhile,

elevated raw material and energy prices will continue to weigh on producer margins across the globe.

Key views for 2011:

• Asia and Latin America to outperform globally: emerging Markets (EM) demand for building materials

to hit new highs in 2011 driven by robust economic growth.

• Europe/North America: cement production to remain depressed but stable; still below pre-crisis levels -

persistent market weakness driving asset sell-offs and increasing EM focus.

• The impact of the crisis in Middle East and North Africa (MENA) will lead to muted consumption

growth in 2011, but this will rebound in 2012.

• Saudi Arabia and Indonesia to be global outperformers in terms of cement consumption growth.

• Steel prices to trend steadily higher through 2011 and 2012; Chinese overcapacity to alleviate some

upside pressure.

Risks:

• Elevated energy and raw materials costs represent a continued threat to producer margins and

consumers.

• China to remain the key growth driver of cement and steel demand; though monetary tightening

measures present downside risk to the demand outlook.

• Inflationary pressures a key concern for the sector across much of Asia.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 15

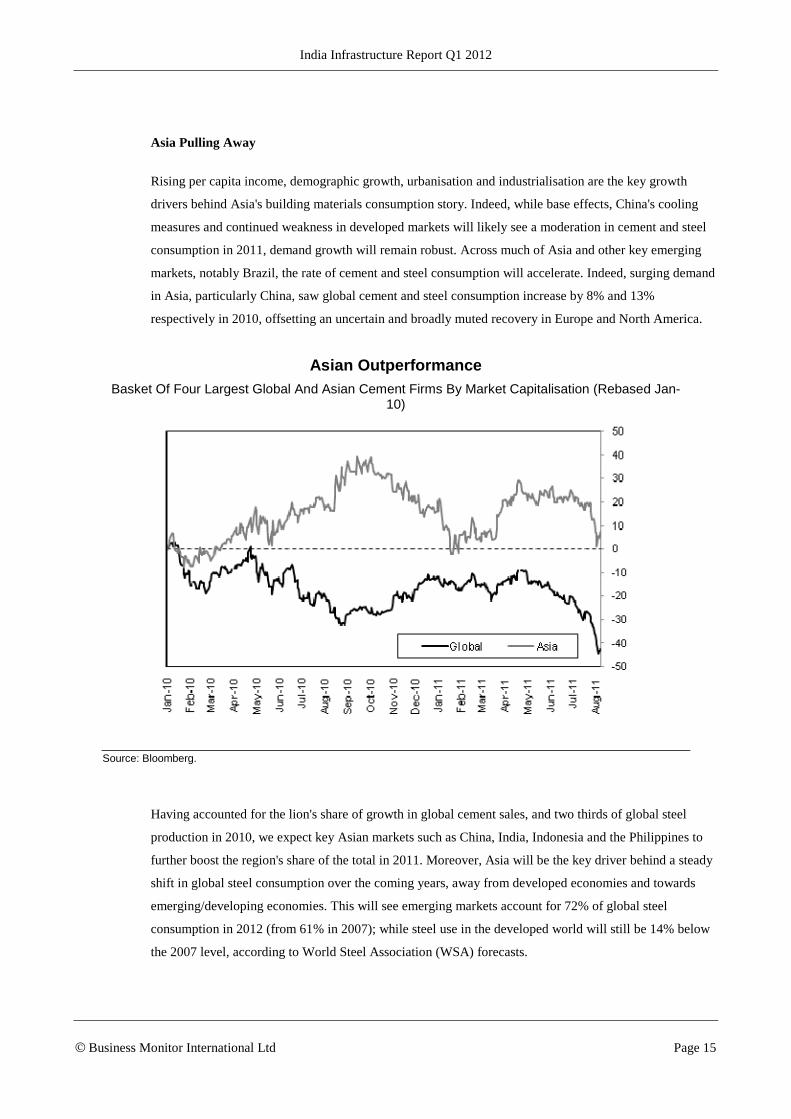

Asia Pulling Away

Rising per capita income, demographic growth, urbanisation and industrialisation are the key growth

drivers behind Asia's building materials consumption story. Indeed, while base effects, China's cooling

measures and continued weakness in developed markets will likely see a moderation in cement and steel

consumption in 2011, demand growth will remain robust. Across much of Asia and other key emerging

markets, notably Brazil, the rate of cement and steel consumption will accelerate. Indeed, surging demand

in Asia, particularly China, saw global cement and steel consumption increase by 8% and 13%

respectively in 2010, offsetting an uncertain and broadly muted recovery in Europe and North America.

Asian Outperformance Basket Of Four Largest Global And Asian Cement Firms By Market Capitalisation (Rebased Jan-

10)

Source: Bloomberg.

Having accounted for the lion's share of growth in global cement sales, and two thirds of global steel

production in 2010, we expect key Asian markets such as China, India, Indonesia and the Philippines to

further boost the region's share of the total in 2011. Moreover, Asia will be the key driver behind a steady

shift in global steel consumption over the coming years, away from developed economies and towards

emerging/developing economies. This will see emerging markets account for 72% of global steel

consumption in 2012 (from 61% in 2007); while steel use in the developed world will still be 14% below

the 2007 level, according to World Steel Association (WSA) forecasts.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 16

Of these markets, Indonesia, Asia's third most populous country, alongside the Philippines, Thailand and

Vietnam, continue to drive the rampant consumption of building materials in the region, with residential

construction, in particular, continuing to exert strong upward pressure on cement prices. We expect

Indonesia to be a regional outperformer over the next couple of years, having recorded a 14.8% rise in

cement sales in H111. Given its size and positive demographic and macroeconomic fundamentals, there is

huge growth potential within the market, particularly in the cement sector where sales are soaring and

capacity is still insufficient.

India To Outperform China

Although we expect demand to remain relatively robust in China, the raft of monetary tightening

measures introduced over the last 12 months should see the growth in consumption of cement and steel in

India outpace that of its fellow giant. However, despite the anticipated moderation in construction activity

in China, we expect demand for building materials to be relatively well supported due to China's huge

affordable housing programme, as well as extensive infrastructure projects.

India, Asia's other giant, will see demand for building materials accelerate in 2011. Indeed, according to

the WSA, demand for steel in the country is expected to grow by 13.6% year-on-year (y-o-y) in 2011 and

14.3% in 2012, as the country's insatiable demand for housing and infrastructure projects drives

consumption of the metal.

Demand for cement will also rise, although whether this will exert any upward pressure on prices is

uncertain, as capacity is high and India's cement producers are able to absorb rising costs. However, there

are significant risks to this outlook, notably those arising from the well- publicised shortcomings within

India's business environment.

Rising Input Costs And Inflation To Squeeze Margins

Over the last 12 months inflationary pressures and the high cost of key raw materials (notably fuel and

iron ore) have been, and remain, a key concern for the construction industry. Driven by strong demand in

Asia and perpetuated by the ongoing unrest in the Middle East, rising input costs have put pressure on

companies' operating margins and in many cases served to offset improving sales growth. These effects

have weighed particularly heavily on the building materials industry given its energy and resource-

intensive nature. Moreover, with input costs likely to remain elevated over the coming months, margins

will be squeezed further, as well as the increased likelihood that these costs will be passed on to the

consumer.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 17

Still Eroding Profits Brent Crude, Newcastle Coal And Chinese Iron Import Price Index (Rebased Jan-2010)

Source: Bloomberg.

However, the decidedly negative turn in investor sentiment through recent weeks has seen the price of a

barrel of oil fall significantly. This is broadly in line with BMI's view that there will be a correction in oil

prices in H211 and should help alleviate operating cost pressures for cement and steel producers.

In South East Asia, such issues regarding negative turns in investor sentiment are accentuated by the

constant threat of inflation, which remains a key concern for a number of countries in the region in 2011,

particularly Indonesia and Vietnam. Although local supply-demand dynamics can drive up prices in a

particular market on a short-term basis; factors such as transport and distribution costs, as well as

uncertain electricity supply, also remain notable constraints for the building materials sector in many

emerging markets. These heightened operating costs can serve to substantially erode positive sales

growth.

This latter issue is an especially pertinent one in sub-Saharan Africa (SSA), where the biggest obstacle

facing large cement producers is the huge infrastructure deficit. This often makes the manufacturing and

transport of building materials from country to country - a highly energy-intensive process at the best of

times - often impossible. While encouraging efforts to ramp up capacity in countries such as Nigeria,

Kenya, Angola and Zimbabwe have been seen over recent quarters, the price of key materials such as

cement will remain highly vulnerable to price volatility for the foreseeable future.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 18

Developed Markets Trailing

With weak economic data from the US continuing to erode confidence in the country's fragile recovery

and the ongoing eurozone debt crisis, the outlook for the global cement majors with heavy exposure to

these regions remains a subdued one. Indeed, high debt burdens and economic uncertainty led to a string

of asset sell offs in the first half of 2011 as firms sought to reduce exposure to these struggling markets.

Lafarge is a case in point, having sold off 'non-core' assets in the US and Europe as it bids to reduce its

substantial debt pile. While uncertainty persists, the worst appears to be over for the European building

materials market and we anticipate volumes and prices of building materials to stabilise in 2012. Even in

the US, the latest figures support our view that residential construction has bottomed (adding 0.08% to

overall GDP growth in Q211) which is positive news for the sector as a whole.

Developed Economies With Declining Share Cement Production (thousand tonnes), 2010

Source: USGS.

Steel: Demand To Grow, With Moderate Price Rises

Following a contraction of 6.6% in 2009, apparent steel use (i.e. steel consumption) increased by 13.1%

in 2010 to 1,272 million metric tonnes (mmt), according to WSA estimates. It is forecast by the WSA that

growth will moderate in 2011, but still rise by 5.3% to reach an all time high of 1,340mmt. This

moderation in growth is due to factors such as base effects as well as China's raft of measures aimed at

curbing its rampant property and construction sectors. Moreover, much of the growth seen in developed

markets in H110 reflected inventory restocking and stimulus measures that have now unwound.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 19

Global Steel Growth Outlook Steel Consumption Growth Forecast (%)

Source: WSA.

Although 2011 will likely see a relative slowdown in Chinese demand for the metal, global steel

consumption will continue to be driven by the Asian giant. Indeed, China's construction and automobiles

industries - two major steel consuming sectors - are forecast to expand by 9% and 15.8% respectively.

China Steel The Driving Force Asia And China Steel Production (Thousand Metric Tonnes)

Source: WSA.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 20

Over the next two years we expect steel prices to rise steadily. Three-month LME steel billet prices will

average US$580/tonne in 2011 and US$620/tonne in 2012, according to BMI's commodities team,

though this is still a long way off pre-crisis peak levels. Over the coming quarter we expect the metal to

trade between US$500/tonne and US$600/tonne, with a number of factors combining to prevent any

potential price surge. One notable issue is that of significant overcapacity in China, which, along with the

Chinese government's concerted efforts to cool industrial production,; reduce the likelihood of any

supply-side constraints.

While we believe that overcapacity will play a key role in curbing potential gains in steel prices there are

a number of dynamics that could precipitate upward price pressure over the coming months. Indeed, cost

pressures arising from the high cost of raw materials have continued to mount in recent months, forcing

steel producers to increase prices as margins came under pressure.

Asia

Industry Trend Analysis - Building Materials: China Still Leading The Charge As Competition Heats Up

BMI View: Attractive macroeconomic and demographic fundamentals across key Asian markets continue

to underpin our positive outlook for global building materials consumption in 2011 and 2012, as well as

over the longer-term. While China's belt tightening measures may conceivably see some softening in the

region's cement and steel consumption growth over the coming quarters, heavy investment in

infrastructure and social housing should ensure that demand levels are well-supported. Indeed, across

the region, rising demand is driving robust sales growth which, in turn, is fuelling capacity expansion

and increasing overseas investment.

Key views:

• Inflationary pressures to remain a concern until end-2011, particularly in Indonesia and Vietnam -

high costs to continue to erode profit and drive market consolidation

• Strong domestic sales driving overseas expansion for a number of large regional cement producers -

competition intensifying in Indonesia

• Robust economic growth across region to drive global consumption of building materials in 2011/2012

and beyond - driven by demand for infrastructure and housing

• High cost of energy and raw materials to continue to weigh on the industry over the short-term, at

least - squeezing margins and exerting upward price pressure

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 21

• China's cooling measures present demand side risk through 2011 and 2012

• ...but sizeable social housing and infrastructure projects to provide significant respite - steel output

proved to be robust through H111

Robust Fundamentals Drive Growth in 2011 and Beyond

Rising per capita income, demographic growth, urbanisation and industrialisation are the key drivers of

growth behind Asia's building materials consumption story. Indeed, we expect the strong demand for

housing and infrastructure in large dynamic Asian markets, such as India, China, Indonesia and

Philippines, to underpin robust growth in the sector over the medium- to long-term. This trend is

highlighted in the outperformance of Asian cement companies relative to their global, Western-based

competitors.

In contrast to global cement majors such as Lafarge and Holcim who, despite a growing presence in

emerging markets, have faced substantial headwinds over the last 18 months, Asian cement majors, such

as China-based Anhui Conch, Thailand's Siam Cement and Indonesian firm Indocement, have

performed strongly. Indeed, with Asia accounting for an expanding slice of the world's cement output -

China and India are the world's largest and second largest consumers of the building material by some

distance - there is huge potential growth and consolidation within these markets over the coming years.

Strong Sales Growth, But Costs Weigh On Margins

Asian Cement Firms (Rebased As Of 02/08/2010)

Source: Bloomberg

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 22

Steel production in the region grew by 11.8% year-on-year (y-o-y) in 2010, increasing its proportion of

the global total from 63.5% to 65.5%, according to the World Steel Association (WSA). Indeed, the

region's insatiable demand for the metal has seen the price of iron ore soar over the last 18 months,

symptomatic of the steady shift in steel consumption away from developed economies and towards

emerging/developing economies. Moreover, despite the Chinese government's efforts to cool the

economy, steel production reached a record high in June 2011, with apparent steel consumption for the

period January to June up by nearly 9% compared to the same period in 2010. Furthermore, with steel

rebar - most commonly used in building construction - the single largest product in the country's steel

mix, the construction sector, remains a key driver behind this resilient growth.

BMI notes that, while our expectation that fixed-asset investment in China will moderate significantly

from 2011 onwards, in line with monetary tightening measures, the sheer size of the planned investments

in social housing and infrastructure should help sustain solid growth levels and capacity utilisation rates.

Meanwhile, over the short-term, we expect elevated input costs to continue to squeeze the margins of

cement and steel producers over the coming months.

Ramping Up Capacity

As China's consumption growth moderates over the next couple of years, India, Asia's other giant, will

see the demand for building materials accelerate in 2011 and beyond. According to the WSA, demand for

steel in the country is expected to grow by 13.6% y-o-y in 2011 and 14.3% in 2012, as the country's

insatiable demand for housing and infrastructure projects drives consumption of the metal. Demand for

cement will also rise, although whether this will exert any upward pressure on prices is uncertain, as

capacity is high and India's cement producers are able to absorb rising costs. There are significant risks to

this outlook; however, it is noted that these arise from the well-publicised shortcomings within India's

business environment.

These shortcomings have manifested themselves in costly delays to major planned steel and mining

projects in the country, inhibiting production levels and leaving investors wary. However, the Indian

building materials industry received a major boost in May 2011, when the Environment Ministry finally

granted final approval for a US$12bn steel mill to be operated by South Korea's POSCO, following years

of delays. While this does little to paper over the major fissures still present within India's business

environment, it is nonetheless a positive development for the sector.

Dynamic and Increasingly Competitive

Indonesia - the continent's third most populous country -, the Philippines, Thailand and Vietnam will be

key growth markets for the consumption of building materials in the region over the coming years.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 23

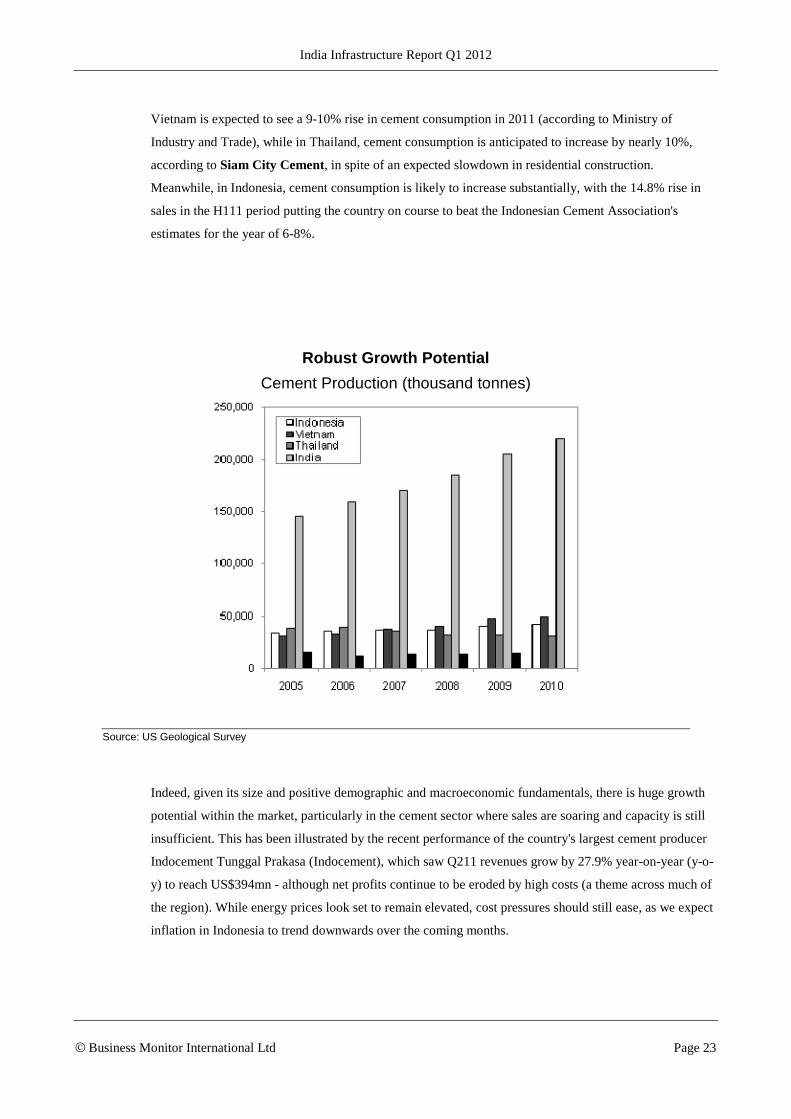

Vietnam is expected to see a 9-10% rise in cement consumption in 2011 (according to Ministry of

Industry and Trade), while in Thailand, cement consumption is anticipated to increase by nearly 10%,

according to Siam City Cement, in spite of an expected slowdown in residential construction.

Meanwhile, in Indonesia, cement consumption is likely to increase substantially, with the 14.8% rise in

sales in the H111 period putting the country on course to beat the Indonesian Cement Association's

estimates for the year of 6-8%.

Robust Growth Potential

Cement Production (thousand tonnes)

Source: US Geological Survey

Indeed, given its size and positive demographic and macroeconomic fundamentals, there is huge growth

potential within the market, particularly in the cement sector where sales are soaring and capacity is still

insufficient. This has been illustrated by the recent performance of the country's largest cement producer

Indocement Tunggal Prakasa (Indocement), which saw Q211 revenues grow by 27.9% year-on-year (y-o-

y) to reach US$394mn - although net profits continue to be eroded by high costs (a theme across much of

the region). While energy prices look set to remain elevated, cost pressures should still ease, as we expect

inflation in Indonesia to trend downwards over the coming months.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 24

Riding High With The Komodo Dragon

Indocement Q2 Revenues, Net Profits And Operating Margin

Source: Indocement, Bloomberg

This robust growth potential has not gone unnoticed and is attracting the attention of foreign cement

companies from within the region. In July 2011, Thailand cement maker Siam Cement announced plans

to spend US$219mn on developing its ceramic and construction material businesses in Indonesia, while

China's Anhui Conch is also planning to invest US$2.35bn in the construction of four new cement plants

in the country. These investments will bring welcome new capacity online for the country, as well as

stimulating increased competition within a market which holds significant potential for consolidation over

the coming years. Vietnam is another market that looks set for increasing consolidation. Indeed, despite

our positive long-term outlook for the sector, over-supply and high energy and transport costs will put

increasing pressure on less-competitive companies.

China Cools Regional Outlook, But Risks Remain Upside

Apparent steel consumption in China for the period January to June 2011 grew by nearly 9% compared to

2010, despite indicators that the government's monetary tightening measures are beginning to take an

effect on manufacturing and other industries, including residential construction. Indeed, steel production

in the country averaged a record high of approximately 2mn tonnes in June 2011, according to the WSA,

driven by strong demand from China's mass affordable housing programme and infrastructure projects.

The key role of the construction sector in this resilient growth is reflected in the sizeable contribution -

16% - of steel rebar (used primarily in building construction) in the country's steel mix.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 25

China Steel The Driving Force

Asia And China Steel Production (Thousand Metric Tonnes)

Source: WSA

With a greater number of affordable homes due to be built over the second half of 2011, and in the years

to follow, we expect steel and cement output in the country to be well-supported in the face of a wider

softening in demand, as tightening measures take effect.

A breakdown of WSA estimates shows that they expect China's apparent steel use in 2011 to increase by

5.0% to 605mnt, following 5.1% growth in 2010. Moreover, the given the pace of steel production in the

first half of 2011, Chinese steel use could be even higher than expectations. However, given that

utilisation rates remain below pre-crisis levels, we see few immediate risks from supply side constraints.

Overcapacity therefore remains an issue in the country, coupled with high input costs, which are

squeezing the margins of some of the country's main producers.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 26

Industry Forecast Scenario

Table: India Construction And Infrastructure Industry Data

2008/09 2009/10 2010/11 2011/12f 2012/13f 2013/14f 2014/15f 2015/16f 2016/17f

Construction Industry Value, INRbn 4,514.1 5,017.1 5,918.6 6,699.4 7,667.9 8,874.7 10,316.3 11,859.8 13,590.3

Construction Industry Value, US$bn 103.7 103.6 129.5 145.6 163.1 194.0 237.2 287.5 339.8

Construction Industry Real Growth, % chg y-o-y 5.4 7.0 8.1 4.0 6.0 7.5 7.7 7.0 6.6

Construction Industry, % of GDP 8.1 7.7 7.5 7.3 7.4 7.5 7.6 7.7 7.8

Total Capital Investment, INRbn 19,735.3 23,441.8 27,383.1 31,143.0 35,338.0 40,904.5 47,145.1 53,731.8 61,039.2

Total Capital Investment, US$bn 428.4 496.3 601.5 673.4 821.8 997.7 1,193.5 1,395.6 1,606.3

Total Capital Investment, % of GDP 35.4 35.8 34.8 34.1 34.0 34.4 34.7 34.9 34.9

Capital Investment Per Capita, US$ 359.8 410.9 491.2 542.4 653.1 782.4 924.0 1,066.8 1,212.8

Real Capital Investment Growth, % y-o-y 1.5 7.3 9.0 6.5 7.5 11.0 10.0 9.0 8.5

Construction Industry Employment, '000 #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A

Construction Industry Employment, % y-o-y #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A

Total Workforce, '000 759,958.6 774,780.9 789,749.6 803,769.7 818,273.7 832,851.9 847,141.0 860,948.4 873,803.4

Construction Industry Employees as % of total labour force #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 27

Table: India Construction And Infrastructure Industry Data

2008/09 2009/10 2010/11 2011/12f 2012/13f 2013/14f 2014/15f 2015/16f 2016/17f

Infrastructure Industry Value As % of Total Construction 45.7 46.5 47.0 47.8 48.5 49.7 50.4 51.1 51.6

Infrastructure Industry Value, INRbn 2,063.3 2,332.9 2,781.8 3,200.3 3,722.7 4,413.3 5,204.3 6,059.4 7,016.8

Infrastructure Industry Value, US$bn 47.4 48.2 60.8 69.6 79.2 96.5 119.6 146.9 175.4

Infrastructure Industry Value Real Growth, % chg y-o-y 12.8 11.1 8.7 5.9 7.8 10.3 9.4 8.4 7.8

Infrastructure Industry Value as % of GDP 3.7 3.6 3.5 3.5 3.6 3.7 3.8 3.9 4.0

Residential and Non-Residential Building Industry Value As % of Total Construction 54.3 53.5 53.0 52.2 51.5 50.3 49.6 48.9 48.4

Residential and Non-Residential Building Industry Value, INRbn 2,450.9 2,684.1 3,136.9 3,499.1 3,945.2 4,461.4 5,112.0 5,800.4 6,573.6

Residential and Non-Residential Building Industry Value, US$bn 56.3 55.4 68.6 76.1 83.9 97.5 117.5 140.6 164.3

Residential and Non-Residential Building Industry Value Real Growth, % chg y-o-y -2.5 7.5 6.3 2.4 4.2 4.8 6.1 5.5 5.3

Residential and Non-Residential Building Industry Value as % of GDP 4.4 4.1 4.0 3.8 3.8 3.8 3.8 3.8 3.8

f = BMI forecasts. Sources: Census and Statistics Department/ILO

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 28

Table: India Construction And Infrastructure Industry Data

2013/14f 2014/15f 2015/16f 2016/17f 2017/18f 2018/19f 2019/20f 2020/21f 2021/22f

Construction Industry Value, INRbn 8,874.7 10,316.3 11,859.8 13,590.3 15,472.0 17,565.5 19,917.4 22,500.2 25,425.3

Construction Industry Value, US$bn 194.0 237.2 287.5 339.8 396.7 462.2 524.1 592.1 669.1

Construction Industry Real Growth, % chg y-o-y 7.5 7.7 7.0 6.6 5.8 5.5 5.4 5.0 5.0

Construction Industry, % of GDP 7.5 7.6 7.7 7.8 7.8 7.8 7.8 7.8 7.8

Total Capital Investment, INRbn 40,904.5 47,145.1 53,731.8 61,039.2 68,884.0 77,519.9 87,128.3 97,559.2 109,270.3

Total Capital Investment, US$bn 997.7 1,193.5 1,395.6 1,606.3 1,812.7 2,040.0 2,292.9 2,567.3 2,875.5

Total Capital Investment, % of GDP 34.4 34.7 34.9 34.9 34.7 34.5 34.2 33.8 33.5

Capital Investment Per Capita, US$ 782.4 924.0 1,066.8 1,212.8 1,352.4 1,504.2 1,671.6 1,851.1 2,051.2

Real Capital Investment Growth, % chg y-o-y 11.0 10.0 9.0 8.5 7.6 7.2 7.0 6.5 6.5

Construction Industry Employment, '000 #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A

Construction Industry Employment, % y-o-y #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A

Total Workforce, '000 832,851.9 847,141.0 860,948.4 873,803.4 886,229.8 898,389.5 910,552.4 922,846.1 934,482.0

Construction Industry Employees as % of total labour force #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A #N/A

Infrastructure Industry Value As % of Total Construction 49.7 50.4 51.1 51.6 52.1 52.4 52.7 53.0 53.2

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 29

Table: India Construction And Infrastructure Industry Data

2013/14f 2014/15f 2015/16f 2016/17f 2017/18f 2018/19f 2019/20f 2020/21f 2021/22f

Infrastructure Industry Value, INRbn 4,413.3 5,204.3 6,059.4 7,016.8 8,055.7 9,210.0 10,504.9 11,924.6 13,530.5

Infrastructure Industry Value, US$bn 96.5 119.6 146.9 175.4 206.6 242.4 276.4 313.8 356.1

Infrastructure Industry Value Real Growth, % chg y-o-y 10.3 9.4 8.4 7.8 6.8 6.3 6.1 5.5 5.5

Infrastructure Industry Value as % of GDP 3.7 3.8 3.9 4.0 4.1 4.1 4.1 4.1 4.1

Residential and Non-Residential Building Industry Value As % of Total Construction 50.3 49.6 48.9 48.4 47.9 47.6 47.3 47.0 46.8

Residential and Non-Residential Building Industry Value, INRbn 4,461.4 5,112.0 5,800.4 6,573.6 7,416.2 8,355.5 9,412.5 10,575.6 11,894.7

Residential and Non-Residential Building Industry Value, US$bn 97.5 117.5 140.6 164.3 190.2 219.9 247.7 278.3 313.0

Residential and Non-Residential Building Industry Value Real Growth, % chg y-o-y 4.8 6.1 5.5 5.3 4.8 4.7 4.7 4.4 4.5

Residential and Non-Residential Building Industry Value as % of GDP 3.8 3.8 3.8 3.8 3.7 3.7 3.7 3.7 3.6

f = BMI forecasts. Sources: Census and Statistics Department/ILO

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 30

Construction and Infrastructure Forecast Scenario

A slowdown in India's

infrastructure sector continues

to unfold in FY2011/12 (April-

March). The latest statistical

data from India's Ministry of

Statistics and Programme

Implementation (MOSPI)

showed that real growth for the

Indian construction industry

came in at just 1.2% year-on-

year (y-o-y) for the first quarter

of FY2011/12 (April-June),

compared to 7.7% y-o-y in the

same period in FY2010/11.

For the rest of FY11/12, we

remain bearish towards India's

construction sector due to

adverse monetary conditions. Inflation persists at an elevated 9.7% y-o-y in September 2011, despite 11

rate hikes since March 2010. This is placing pressure on the Indian central bank, the Reserve Bank of

India (RBI), to initiate further rate hikes to cut inflation. The RBI raised the policy repo rate by 25 basis

points to 8.50% on October 25 2011.

Meanwhile, global external conditions are turning for the worse in recent months, and we believe this

further sets the stage for weak construction growth throughout the remainder of FY2011/12. The

combination of costly debt levels and high raw material prices will deter or prevent construction

companies operating in India from carrying out large-scale projects, due to a lack of adequate financing.

We do, however, believe that this cyclical downtrend in construction has bottomed out, with inflation

already at its peak. Although rate cuts are unlikely to take place until mid-2012, the RBI has expressed a

clear desire to pause monetary tightening, and this should provide a measure of certainty to infrastructure

investors in search of financing. As such, we believe that construction activity could improve at the tail-

end of FY2011/12, and we have only revised down our real growth forecast for the Indian construction

industry for FY2011/12 to 4.0% (previously 7.3%).

Infrastructure Moving Centre Stage

Construction Industry Value And Infrastructure Share

BMI f=forecast, Source: BMI, BMI Calculation

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 31

Activity To Bound Back In 2012/13

Looking further ahead, we are confident that the sector's fortunes will start to improve in FY2012/13. The

Indian government is making serious attempts to kick-start infrastructure development for the 12th Five-

Year Plan (FY2012/13-FY2016/17), approving major infrastructure projects and pushing forward plans to

accelerate and enhance the flow of long-term financing.

In June 2011, India's Ministry of Railways announced that it will conduct the sale of INR100bn

(US$2.2bn) of tax-free bonds in India by September 2011, while other ministries involved in roads, ports

and urban development will also be conducting their bond issuances during FY11/12.

In September 2011, three state-run financial institutions - the Indian Infrastructure Finance Company

Limited (IIFCL), Life Insurance Corporation of India (LIC) and India Development Finance Corporation

(IDFC) - signed a memorandum of understanding to boost the application of takeout financing in India.

The MOU would allow the three companies to take out up to 50% of an infrastructure project's debt,

potentially unlocking around INR300bn (US$6.2bn) in bank debts, which could be used to finance other

projects and speed up the pace of infrastructure development in India. This enhancement in takeout

financing is critical, as it could mitigate the lack of size and sophistication in India's financial markets by

boosting the liquidity and risk transfer opportunities for Indian banks.

Meanwhile, special purpose vehicles developed by India for infrastructure financing - commonly known

as infrastructure debt funds (IDFs) - are being promoted by Indian officials to overseas investors. In

October 2011, India's Economic Affairs Secretary R Gopalan was in discussion with investors in

Singapore and had announced that the first IDF is set to be launched in the coming two months. The fund

is expected to attract US$3bn in investments and is currently undergoing the initial process of

establishment.

Investments from foreign sources also accelerated at the start of FY2011/12, as the high cost of domestic

financing has made Indian infrastructure companies more receptive to capital investments from overseas

companies. Between May and September 2011, six notable private equity groups - 3i Infrastructure ,

Morgan Stanley , Kohlberg Kravis Roberts , Blackstone Group and JP Morgan Chase - invested a

total of US$1.05bn into Indian companies or infrastructure projects.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 32

Boosting The Pipeline

Besides greater access to financing, another indication of a rebound in construction activity is the growing

number of infrastructure projects being implemented and announced by the Indian government. BMI 's

Key Projects Database has once again seen an increase in project backlogs for several infrastructure

sectors over the past quarter, with the value of total projects (particularly power projects) under

construction or in the pipeline in India's infrastructure sector growing from US$400bn as of August 2011

to around US$430bn as of October 2011. This does not include projects that have not provided cost

estimates, which would make the actual value of infrastructure projects available in India even higher.

Value Of Key Infrastructure Projects in India*

Source: WSA

The road sector is a key example of this increase in pipeline projects. In October 2011, the Indian

government launched an INR166bn (US$3.35bn) highways building plan under the National Highways

Development Programme, covering the construction of six-lane highways totalling 6,500km, four-lane

highways totalling 24,700km and the expansion of other highways. Under the plan, the government has

already approved four expressway construction projects, while the country's public-private partnership

appraisal committee has approved 10 roadworks projects, worth a total of US$1.1bn.

Therefore, we expected several infrastructure projects to be awarded at the start of FY2012/13 and begin

construction in late-2012 or 2013. This view is reflected in our forecasts, with real growth for India's

construction sector to reach 6.0% in FY2012/13 and 7.5% in FY2013/14. This also supports our view that

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 33

infrastructure (one of the two sub-sectors which form the construction industry value, according to BMI 's

definition) will continue to be the main driver of construction industry value, substantially outperforming

its counterpart - the residential and non-residential building sector.

However, these growth rates are still lower than the double-digit figures seen in the early 2000s, and far

below potential growth levels. Our forecast is motivated by a number of factors:

India's business environment continues to be plagued by a convoluted and incoherent legal

framework, rampant corruption and an environmental ministry that is over-zealous in

prosecuting infringements, but slow in implementing policies. Unclear and ineffective land

clearance regulations are delaying projects, and complex and convoluted bureaucracy is slowing

down planning and tendering processes These issues have led to lengthy delays, with the latest

figures from the Ministry of Statistics and Programme Installation (MOSPI) showing that 284

out of 496 construction projects in India were delayed as of December 2010.

A downgrade of investment targets in the 11th Five-Year Plan (2007/07-2011/12), announced in

March 2010 – due to lower than expected investment in the transport infrastructure sector – was

the first sign that investment targets were not eventuating at the rate anticipated.

Foreign Direct Investment (FDI) is being thwarted by the need to partner with a local player,

meaning only those who are able to form local partnerships can follow through on intentions to

invest.

Risks In Reforms

We believe that the success of the 12th Five-Year Plan is still dependent on the level of regulatory

reforms carried out by the government to facilitate infrastructure development. Structural weaknesses in

India's business environment remain considerable and could still significantly delay projects that have

reached financial closure. At present, it remains to be seen if reforms that are conducive for construction

companies will be carried out.

A key reform is the introduction of a new land bill to repeal the obsolete Land Acquisition Act of 1894

and replace it with a fresh National Land Acquisition and Rehabilitation & Resettlement Bill for 2011.

With the 2012 elections looming large, the land reform bill remains a hot political topic, with the Indian

public still very much against the bill. This is in spite of the unfavourable terms for investors, as the

financial cost of land purchases is expected to rise significantly under current proposals. Construction

companies would need to pay twice the market value for urban land and six times for rural development.

In addition, 80% of the families involved will have to give approval for acquisitions to take place, and the

bill would be implemented retrospectively.

India Infrastructure Report Q1 2012

© Business Monitor International Ltd Page 34