india monthly markets update - july 2010

TRANSCRIPT

Monthly Markets Update - India

July 2010

Prepared by: iFAST Research Team

Monthly Markets Update - India July 2010

Key Points

International bourses made a turnaround during the month of July, with emerging markets like Brazil and Russia leading the pack, after the negative returns delivered by these markets in the previous month. The MSCI Emerging Markets index rose by a handsome 8.00% in July.

India was an underperformer during the month of July, with the benchmark Sensex index rising by only 0.95% during the month, weighed down by inflationary fears and concerns on further monetary tightening by the central bank.

Domestically, the BSE Consumer Durables index was the top performer during the month of July rising by close to 12%. Banking and realty stocks also did well during the month. The broader markets continued to outperform, with the BSE Mid Cap and BSE Small Cap indices returning 3.62% and 3.06% respectively in July compared to just 0.95% return managed by the BSE Sensex index over the same tenure.

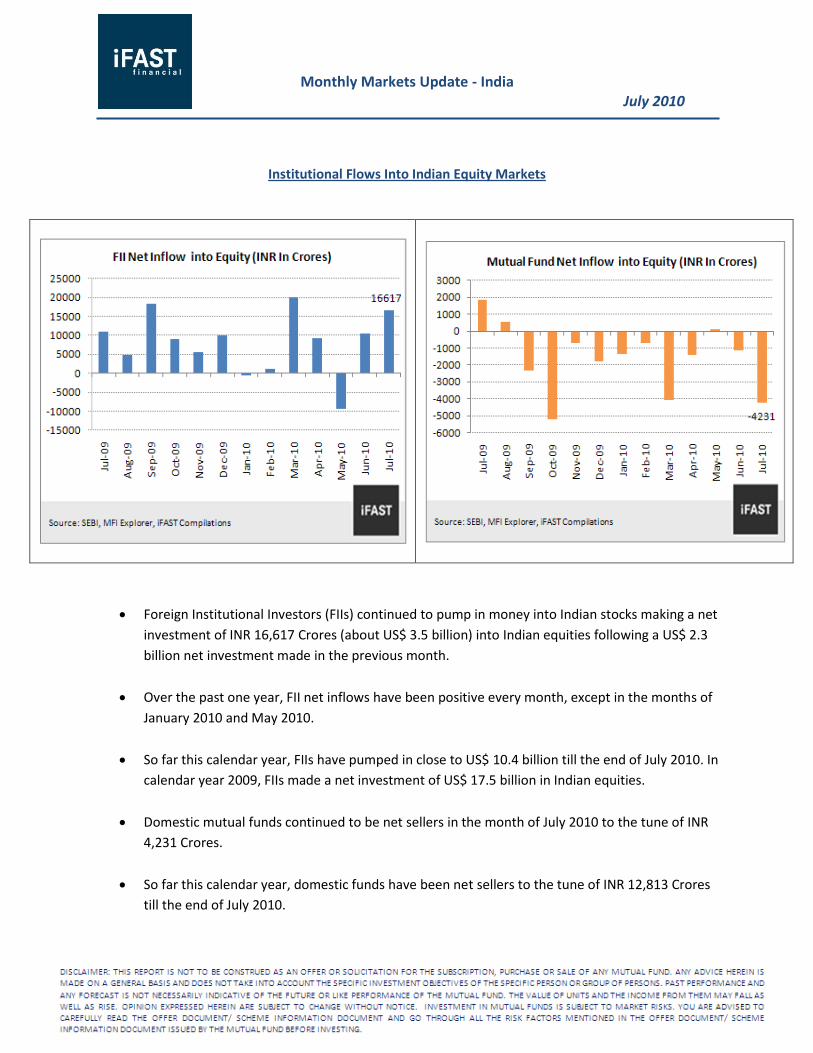

Foreign Institutional Investors (FIIs) continued to pump in money into Indian stocks making a net investment of INR 16,617 Crores (about US$ 3.5 billion) into Indian equities during the month of July. Domestic mutual funds continued to be net sellers in July.

The rupee closed the month almost flat with a minor gain of 0.03%, but the dollar weakened against most currencies during the month of July and the dollar index fell by about 5.20% during the month.

Bond yields rose across the board, but registered a sharper increase in the shorter end of the yield

curve as liquidity remained tight throughout the month. The yield of the benchmark 10 year paper

hardened by 27 basis points during the month of July.

The RBI hiked the repo rate by 25 bps and the reverse repo rate by a higher than expected 50 bps in

its monetary policy review on 27 July 2010. We expect the RBI to continue to hike rates in a

calibrated manner, with the next hike possible in its mid quarter policy review meet scheduled for

16 September 2010.

Indian fund industry’s assets (average assets under management) dropped by a marginal 1.5% in the month of July.

Diversified equity funds outperformed the benchmark Sensex index delivering an average return of 2.44% in the month of July. Banking funds and funds having higher exposure to mid and small cap stocks outperformed during the month. With the recovery in global equity markets, global funds also fared well during the month.

In the debt segment, performance of gilt and income funds were affected due to the rise in bond yields during the month.

Monthly Markets Update - India July 2010

Equity Markets Update

International Markets (As of July 2010 end):

2010 2010 2009 P/E P/E Earnings Growth

Earnings Growth

MTD Return (%) YTD Return (%) Return (%) Yr 2010 Yr 2011 2010 (%) 2011 (%)

Asia ex Japan (MSCI Asia ex Japan) 5.38% 0.31% 68.30% 13.5 12.1 29.4 11.6

Emerging Markets (MSCI EM) 8.00% 0.20% 74.50% 12.2 10.5 37.0 16.8

Europe (DJ Stoxx 600) 4.94% 0.58% 28.00% 11.6 9.8 33.4 18.7

Japan (Nikkei 225) 1.65% -9.57% 19.00% 18.0 16.0 90.2 12.9

USA (S&P 500) 6.88% -1.21% 23.50% 13.5 11.5 35.0 17.6

Australia (S&P/ASX 200) 4.46% -7.74% 30.80% 11.1 10.4 14.5 6.6

Brazil (IBOV) 10.80% -1.56% 82.70% 12.9 10.0 27.4 29.0

China (HS Mainland 100) 3.87% -3.75% 61.30% 13.4 11.6 22.3 16.4

Hong Kong (HSI) 4.48% -3.85% 52.00% 12.6 10.7 21.5 17.5

India (SENSEX) 0.95% 2.31% 81.00% 18.4 15.3 14.7 20.3

Indonesia (JCI) 5.34% 21.11% 87.00% 15.4 12.8 103.9 19.8

Malaysia (KLCI) 3.57% 6.92% 45.20% 15.5 13.7 27.7 12.8

Russia (RTSI$) 10.48% 2.43% 128.60% 7.8 6.6 69.1 18.0

Singapore (STI) 5.37% 3.11% 64.50% 14.7 13.0 20.0 13.1

South Korea (KOSPI) 3.59% 4.55% 49.70% 9.9 9.1 63.3 9.3

Taiwan (Taiwan Weighted) 5.88% -5.22% 78.30% 13.3 11.8 83.8 13.0

NASDAQ 100 (Technology Heavy) 7.18% 0.20% 53.50% 15.3 13.3 27.3 14.9

Thailand (SET Index) 7.34% 16.51% 63.20% 12.1 10.4 14.3 16.1

Source: Bloomberg, iFAST Compilations All returns are in respective local currency terms and MSCI Index returns are in USD

International bourses made a turnaround during the month of July, with emerging markets like Brazil and Russia leading the pack, after the negative returns delivered by these markets in the previous month. The MSCI Emerging Markets index rose by a handsome 8.00% in July.

The U.S. markets recovered smartly in July, with both the benchmark S&P 500 index and the technology heavy NASDAQ index rising by close to 7% during the month. However, consumer confidence continued to drop, and the index fell to 50.4 in July 2010 from 52.9 in June 2010.

India was an underperformer during the month of July, with the benchmark Sensex index rising by only 0.95% during the month, weighed down by inflationary fears and concerns on further monetary tightening by the central bank.

European markets also recovered smartly in July, with the benchmark DJ Stoxx 600 index rising by close to 5% during the month, as the Euro appreciated significantly in July, and the findings of the European Banks stress results released on 23 July 2010, received a somewhat positive response from the markets.

Monthly Markets Update - India July 2010

Domestic Markets (As of July 2010 end):

Domestically, the BSE Consumer Durables index was the top performer during the month of July

rising by close to 12% during the month. Over a one year period (as of July 2010), the BSE

Consumer Durables index is the top performing domestic index surging by close to 73%.

Banking and realty stocks also did well in July, with the BSE Bankex and BSE Realty indices

delivering returns of 7.19% and 5.51% during the month.

The broader markets continued to outperform, with the BSE Mid Cap and BSE Small Cap indices

returning 3.62% and 3.06% respectively in July compared to just 0.95% return managed by the

BSE Sensex index over the same tenure.

Oil & gas stocks suffered from selling pressure in July, after the smart rally registered by these

stocks in the previous month on deregulation of petrol prices and hike in diesel, LPG and

kerosene prices. The BSE Oil & Gas index fell by 6.51% in the month of July after surging by

8.59% in the month of June. The biggest damage was done by Reliance Natural Resources

(RNRL) stock, which fell by a massive 37% in the month of July, as the gas ruling went in favour

of Reliance Industries, indicating that RNRL doesn’t have much reason to exist anymore and

would be merged with Reliance Power.

Pharma stocks also witnessed some profit booking in July, with the BSE Healthcare index falling

by 2.64% during the month. The BSE Healthcare index has registered positive monthly gains for

the past five consecutive months (from February 2010 to June 2010).

Monthly Markets Update - India July 2010

Institutional Flows Into Indian Equity Markets

Foreign Institutional Investors (FIIs) continued to pump in money into Indian stocks making a net

investment of INR 16,617 Crores (about US$ 3.5 billion) into Indian equities following a US$ 2.3

billion net investment made in the previous month.

Over the past one year, FII net inflows have been positive every month, except in the months of

January 2010 and May 2010.

So far this calendar year, FIIs have pumped in close to US$ 10.4 billion till the end of July 2010. In

calendar year 2009, FIIs made a net investment of US$ 17.5 billion in Indian equities.

Domestic mutual funds continued to be net sellers in the month of July 2010 to the tune of INR

4,231 Crores.

So far this calendar year, domestic funds have been net sellers to the tune of INR 12,813 Crores

till the end of July 2010.

Monthly Markets Update - India July 2010

Currency Update

The dollar weakened against most currencies during the month of July and the dollar index fell

by about 5.20% during the month. The Euro gained the most against the greenback in July rising

by close to almost 6% during the month.

Within Asia, the Singapore dollar gained the most against the dollar in July, rising by 2.41%

during the month. The currency gained strength as its economy grew by a very strong 26% (q-o-

q annualized basis) during the April to June quarter, substantially ahead of street estimates.

The rupee closed the month almost flat with a minor gain of 0.03%, even though FIIs pumped in

about US$3.5 billion during the month.

The JP Morgan REER index fell to 109.64 level on 14 July 2010 from 111.78 level in the end of

June 2010. The index indicates how overvalued the rupee is against a basket of six currencies. So

a value more than 100 indicates the rupee’s overvaluation in real terms.

Monthly Markets Update - India July 2010

Fixed Income Markets Update

Yields rose across the board, but registered a sharper increase in the shorter end of the yield

curve as liquidity remained tight throughout the month. The yield on the benchmark 1 year

paper rose by 94 basis points during the month, while the yield of the benchmark 10 year paper

hardened by 27 basis points during the month of July.

The RBI engaged in further monetary tightening in its monetary policy review on 27 July 2010,

and increased the repo rate by 25 bps to 5.75% and the reverse repo rate by a higher than

expected 50 bps to 4.50%. The central bank also revised upwards its March 2011 inflation

forecast to 6% (from 5.5% earlier), and the GDP forecast for FY 2010-2011 to 8.5% (from 8.0%

earlier). We expect the RBI to continue to hike rates in a calibrated manner to combat inflation,

with the next hike possible in its mid quarter policy review meet scheduled for 16 September

2010.

Reverse repo volumes continued to be negative for most of the month of July, on account of the

liquidity squeeze, but turned positive towards the last few days of the month. M3 (broad

money) growth rose marginally to 15.2% on 16 July 2010. Liquidity conditions are expected to

improve a bit in August, but still remain more or less tight during the month.

Monthly Markets Update - India July 2010

Economic Indicators

Economic Releases during the Month of July 2010

Event Period Consensus Actual Prior

India REPO Cutoff Yld 2-Jul-10 - - 5.50% 5.25%

Reverse Repo Rate 2-Jul-10 - - 4.00% 3.75%

India Local Car Sales JUN - - 141,184 148,481

Industrial Production YoY MAY 16.20% 11.50% 17.60%

Monthly Wholesale Prices YoY% JUN 10.80% 10.55% 10.16%

India REPO Cutoff Yld 27-Jul-10 5.75% 5.75% 5.50%

Reverse Repo Rate 27-Jul-10 4.25% 4.50% 4.00%

Exports YoY% JUN - - 30.40% 35.10%

Imports YoY% JUN - - 23.00% 38.50%

Source: Bloomberg, iFAST Compilations

Exports growth slowed down to 30.40% YoY in June from 35.10% YoY growth in the previous

month. Imports growth slowed down even more sharply to 23.00% YoY in June from 38.50% YoY

growth in the previous month.

The RBI hiked the key policy rates twice in the month of July, first by hiking both the repo and

reverse repo rate by 25 bps effective from 2 July 2010, and then by hiking the repo rate by 25

bps and the reverse repo by 50 bps effective from 27 July 2010.

The RBI also revised upwards the GDP forecast for FY 2010 – 2011 to 8.5% from 8.0% earlier.

Meanwhile the IMF increased the GDP forecast for India in 2010 to 9.5% from 8.8% earlier. The

international agency also revised upwards global economic growth for 2010 to 4.6% in its World

Economic Outlook (WEO) report released on 8 July 2010, from a 4.2% forecast earlier.

Industrial production growth dropped to 11.50% in the month of May compared to consensus

estimates of 16.20%. We expect industrial production to moderate in the second half of this

year as the base effect reduces and RBI engages in monetary tightening.

Headline inflation rose to 10.55% in the month of June, supported by rise in food prices and fuel

inflation. We expect inflation to remain in double digit territory for the next 1-2 months as the

full effect of the recent fuel price hike in June will only be felt in the month of August.

Thereafter, the inflation can start to trend lower, considering that monsoon remains as per

expectations.

Monthly Markets Update - India July 2010

Mutual Fund Industry Asset Trends

Indian fund industry’s assets (average assets under management) dropped by a marginal 1.5% in

the month of July after registering a very sharp fall of close to 16% in the previous month on

account of massive outflows from liquid plus / ultra short term funds.

In absolute terms, SBI Mutual Fund registered the largest addition in average assets, as the fund

house added on about INR 4,779 Crores of assets during the month. Newly launched IDBI

Mutual fund added on a healthy INR 940 Crores in assets through it maiden offering during the

month of July.

The largest drop in assets (in absolute terms) in the month of July was suffered by LIC Mutual

Fund, as the average assets of the fund house plunged by INR 5,624 crores during the month.

In percentage terms, JP Morgan Mutual Fund saw the largest growth in average assets

(+56.69%) in July, while LIC Mutual Fund registered the largest drop in average assets during the

month (-18.72%).

Monthly Markets Update - India July 2010

Fund Category Returns

Fund Category Returns (as of July 2010)

1 Month YTD 1 Year

Equity: Diversified 2.44 8.24 29.12

Equity: ELSS 2.37 7.97 27.99

Equity: Index 1.05 3.24 16.71

Equity: Overseas 3.76 -0.82 13.41

Balanced 1.88 7.02 21.24

Debt: MIP 0.40 3.26 7.38

Debt: Income 0.14 2.88 4.99

Debt: Gilt Short Term -0.03 2.21 2.91

Debt: Gilt Long Term -0.28 2.46 2.98

Debt: Floating Rate 0.41 2.69 4.68

Debt: Ultra Short Term 0.41 2.63 4.44

Debt: Short Term 0.21 2.00 4.79

Liquid 0.41 2.32 3.81

Fund of Funds: Overseas 5.54 -0.57 18.25 Source: MFI Explorer, iFAST Compilations

(Excludes Institutional Plans)

Diversified equity funds outperformed the benchmark Sensex index delivering an average return

of 2.44% in the month of July, while the Sensex delivered 0.95% over the same tenure. Funds

having higher exposure to mid and small cap stocks outperformed during the month. YTD,

diversified equity funds category delivered an average return of 8.24%, while the Sensex only

managed a 2.31% return over the same period. Meanwhile the BSE Mid Cap and BSE Small Cap

indices have risen 10.27% and 11.86% respectively so far this calendar year.

Balanced funds and Monthly Income Plans (MIP) categories returned 1.88% and 0.40%

respectively during the month of July.

With the recovery in global equity markets, global funds outperformed during the month of July

with the Equity: Overseas and Fund of Funds: Overseas categories returning 3.76% and 5.54%

respectively in July.

In the debt segment, performance of gilt and income funds were affected due to the rise in

bond yields during the month. Long term gilt funds delivered a negative return of 0.28% during

the month, while short term gilt funds and income funds delivered average returns of -0.03%

and 0.14% respectively in July. Returns of short term debt funds were also affected and they

delivered an average return of 0.21% in July.

Monthly Markets Update - India July 2010

Top and Bottom Five Performing Equity Funds in July

Top Five Performing Equity Funds on Our Platform during the Month of July

Sector MTD

Returns YTD

Returns

BSL COMMODITY EQUITIES FUND GLOBAL AGRI PLAN- GROWTH Overseas 13.33 -7.20

RELIANCE BANKING FUND- GROWTH Banking 8.64 25.80

EMERGING BUSINESS FUND- GROWTH Mid Cap & Small

Cap 8.36 19.43

SUNDARAM BNP PARIBAS FINANCIAL SERVICES OPPORTUNIES- GROWTH Banking 8.18 19.87

JM FINANCIAL SERVICES SECTOR FUND- GROWTH Banking 7.94 13.20

Bottom Five Performing Equity Funds on Our Platform during the Month of July

Sector MTD

Returns YTD

Returns

RELIANCE PHARMA FUND- GROWTH Pharmaceuticals -2.46 18.89

UTI PHARMA & HEALTHCARE FUND- GROWTH Pharmaceuticals -3.98 17.27

SUNDARAM BNP PARIBAS SELECT THEMATIC FUNDS- ENTERTAINMENT OPPORTUNITIES- GR Speciality -4.08 (1.00)

MAGNUM SECTOR FUND UMBRELLA-PHARMA- GROWTH Pharmaceuticals -4.30 12.09

BSL COMMODITY EQUITIES FUND GLOBAL PRECIOUS METALS PLAN- GROWTH Overseas -7.18 -2.26

Source: iFAST Compilations

Banking funds, global funds and funds having higher exposure to mid and small cap stocks

topped the charts from the equity segment in the month of July.

The top performing fund from the equity segment was a global fund focusing on stocks of agri

business companies called Birla Sun Life Equities Fund – Global Agri Plan – Growth. The fund

delivered an impressive 13.33% return during the month of July, but YTD performance is still in

the red (-7.20%).

The top performing banking fund in July was Reliance Banking Fund – Growth which delivered a

8.64% return during the month of July, and an impressive 25.80% return so far this year. The BSE

Bankex index has managed only a 15.04% return YTD. This fund is our recommended banking

fund and also has exposure in our recommended portfolios.

The bottom performing funds from the equity segment in the month of July comprised primarily

of pharma funds and media funds.

The bottom performing fund from the equity segment in July was a global fund investing in

stocks of precious metals companies called Birla Sun Life Equities Fund – Global Precious Metals

Plan – Growth (-7.18%). The poor performance could be attributed to correction in prices of

precious metals, especially gold, which fell by close to 5% during the month of July.

Monthly Markets Update - India July 2010

Top and Bottom Five Performing Debt Funds in July

Top Five Performing Debt Funds on Our Platform during the Month of July

Sector MTD

Returns YTD

Returns

RELIGARE GILT FUND LONG DURATION PLAN- GROWTH GILT - Long Term 3.37 11.90

MAGNUM MONTHLY INCOME PLAN FLOATER- GROWTH MIP 2.39 5.73

HDFC MULTIPLE YIELD FUND- GROWTH MIP 1.00 6.87

BSL MIP II WEALTH 25- GROWTH MIP 0.94 3.56

HSBC MIP SAVINGS PLAN- GROWTH MIP 0.92 3.16

Bottom Five Performing Debt Funds on Our Platform during the Month of July

Sector MTD

Returns YTD

Returns

TEMPLETON INDIA GOVERNMENT SECURITIES FUND COMPOSITE PLAN- GROWTH GILT - Long Term -0.78 -0.07

IDFC DYNAMIC BOND FUND PLAN A- GROWTH Income -0.81 1.51

CANARA ROBECO DYNAMIC BOND FUND- GROWTH Income -0.85 1.46

TEMPLETON INDIA GOVERNMENT SECURITIES FUND LONG TERM PLAN- GROWTH GILT - Long Term -0.87 -0.02

IDFC GOVERNMENT SECURITIES FUND INVESTMENT PLAN A- GROWTH GILT - Long Term -1.15 0.96

Source: iFAST Compilations (Excludes Liquid funds and close ended debt funds)

The top performers from the debt segment during the month of July were Monthly Income

Plans (MIP), with them picking up four of the top five spots. Most of these top performing MIPS

in July were aggressive MIPs, with higher exposure to equities ranging between 15-25% of the

portfolios.

The top performing fund from the bond segment in July was surprisingly a long term gilt fund

called Religare Gilt Fund – Long Duration Plan – Growth, which delivered an impressive return of

3.37% during the month, even as most other long term gilt funds closed the month with

negative returns. The fund is a very small fund with a corpus of only INR 0.07 Crores (as of June

2010), with the entire portfolio in cash. YTD (as of July 2010) the fund has managed a handsome

return of 11.90%, making it the best performing gilt fund so far this year.

The bottom performing debt funds during the month of July were long term Gilt funds and some

Income funds, as their performance was impacted due to hardening in long term bond yields

during the month.

The bottom performing gilt fund in July was a long term gilt fund called IDFC Government

Securities Fund – Investment Plan A – Growth, which is a long term gilt fund and delivered a

negative return of 0.27% during the month.

Monthly Markets Update - India July 2010

Recommended Portfolios Update

1. Conservative Portfolio:

Portfolio Objective:

The portfolio aims to achieve long term capital appreciation by investing 90% into bond funds and 10% into equity funds. The target allocation may change depending upon our views on financial markets. Currently we have an overweight position in equities and we target to have an exposure of 80% to bond funds and 20% to equity funds.

Total Investment: INR 1,00,000 Portfolio Absolute Return since inception:

(Inception Date: 26 Feb 2010) 4.63%

Portfolio Value:

INR 1,04,633

July 2010 Portfolio Return:

0.60%

Portfolio Commentary:

The portfolio gave a return 0.60% in the month of July. Being overweight on Equity contributed to better returns in the portfolio, and the two equity funds accounted for 74% of the total portfolio returns during the month. In the debt portfolio, returns from the debt funds were muted as the RBI chose to hike the key policy rates twice in July. Liquid funds gave an annualized return of 4.0% to 5.0% in July, due to short term liquidity crunch. The call rates for July were mostly above 5.4% but during the last few days of the month the call rates fell below 5% as the liquidity in the system picked up. All debt funds gave positive returns except for ICICI Prudential Long Term Plan, which gave a negative performance during the month. The debt funds gave returns in the range of -0.43% to 0.45%. The debt funds in total contributed 26% of the overall portfolio return in July.

2. Moderately Conservative Portfolio:

Portfolio Objective:

The portfolio aims to achieve long term capital appreciation by investing 70% into bond funds and 30%

into equity funds. The target allocation may change depending upon our views on financial markets.

Currently we have an overweight position in equities and we target to have an exposure of 60% to bond

funds and 40% to equity funds.

Total Investment: INR 1,00,000 Portfolio Absolute Return since inception:

(Inception Date: 26 Feb 2010)

6.34%

Portfolio Value:

INR 1,06,342

July 2010 Portfolio Returns:

0.73%

Portfolio Commentary:

Monthly Markets Update - India July 2010

The portfolio gave a return 0.73% in the month of July. Overweight position on Equity contributed to better performance of the portfolio. All Equity funds in the portfolio except DSP Blackrock Top 100 Fund outperformed the Sensex. HDFC Top 200 fund contributed the most to the portfolio, accounting for almost 33% of the overall portfolio returns, which was followed by ICICI Prudential Discovery fund, which accounted for almost 23% of the overall portfolio return in July. In the debt portfolio, all debt funds gave positive returns except for ICICI Prudential Long Term Plan, which gave a negative performance during the month. The debt funds contributed 15% of the overall portfolio return in July.

3. Balanced Portfolio

Portfolio Objective:

The portfolio aims to achieve long term capital appreciation by investing 50% into bond funds and 50%

into equity funds. The target allocation may change depending upon our views on financial markets.

Currently we have an overweight position in equities and we target to have an exposure of 40% to bond

funds and 60% to equity funds.

Total Investment: INR 1,00,000 Portfolio Absolute Return since inception:

(Inception Date: 26 Feb 2010) 8.31%

Portfolio Value:

INR 1,08,311

July 2010 Portfolio Returns:

1.17%

Portfolio Commentary:

As we were positive on Indian Equities, we are overweight equities, and the portfolio gave a return of 1.17% in the month of July. Equity funds contributed close to 93% of the portfolio return and 7% of the overall portfolio return was from the Debt portfolio. Midcap index outperformed the Large cap index during the month. Sundaram Select Midcap Fund was the best performing fund during the month with an absolute return of 3.99%. The worst performing fund in portfolio the month was DSP Blackrock Top 100 fund, which gave a return of -0.28%. However, HDFC Top 200 fund has contributed the most to the portfolio, accounting for close to 31% of the overall portfolio’s return.

4. Moderately Aggressive Portfolio:

Portfolio Objective:

The portfolio aims to achieve long term capital appreciation by investing 30% into bond funds and 70%

into equity funds. The target allocation may change depending upon our views on financial markets.

Currently we have an overweight position in equities and we target to have an exposure of 20% to bond

funds and 80% to equity funds.

Monthly Markets Update - India July 2010

Total Investment: INR 1,00,000 Portfolio Absolute Return since inception:

(Inception Date: 26 Feb 2010)

11.27%

Portfolio Value:

INR 1,11,274

July 2010 Portfolio Returns:

2.09%

Portfolio Commentary:

The portfolio gave a return of 2.09% in the month of July. Overweight position in Equity helped to post

better performance during the month. The banking sector was one of the best performers in this

month. Reliance Banking fund was the best performing fund during the month with absolute return of

8.64%, accounting for close to 21% of the total portfolio’s return, despite having a low weightage in the

portfolio.

All of the equity funds have outperformed the Sensex except for DSP Blackrock Top 100 fund. Most of

the equity funds in the portfolio have been able to deliver more than 2% returns in July. Reliance

Growth fund, although it is a midcap oriented fund, its performance has lagged that of the BSE Midcap

Index, mainly due to its higher holding of cash to the tune of over 8% of the portfolio in June.

5. Aggressive Portfolio:

Portfolio Objective:

The portfolio aims to achieve long term capital appreciation by investing 10% into bond funds and 90%

into equity funds. The target allocation may change depending upon our views on financial markets.

Currently we have an overweight position in equities and we target to have an exposure of 0% to bond

funds and 100% to equity funds.

Total Investment: INR 1,00,000 Portfolio Absolute Return since inception:

(Inception Date: 26 Feb 2010)

14.64%

Portfolio Value:

INR 1,14,642

July 2010 Portfolio Returns:

2.92%

Portfolio Commentary:

The portfolio gave a return of 2.92% in the month of July. All the funds in the portfolio were equity funds and except for DSP Blackrock Top 100 Fund, the others outperformed the Sensex by a huge margin. Most of the sectoral and midcap funds have delivered returns in excess of 3% in July. Reliance Banking fund has given an absolute return of 8.64% followed by Sundaram BNP Paribas Select Midcap Fund, which has given an absolute performance of 3.99% for July. Meanwhile Reliance Growth Fund, which is a midcap fund in the portfolio, underperformed because of huge idle cash lying in the portfolio to the tune of over 8%. Reliance Banking fund, despite have only 10% weightage in the portfolio has accounted for 30% of the portfolio’s return for the month of July.

------------------ END ------------------