india morning bell - rathionline.com...anand rathi shares and stock brokers limited (hereinafter...

TRANSCRIPT

Anand Rathi Shares and Stock Brokers Limited (hereinafter “ARSSBL”) is a full service brokerage and equities research firm and the views expressed therein are solely of ARSSBL and not of the companies which have been covered in the Research Report. This report is intended for the sole use of the Recipient and is to be circulated only within India and to no countries outside India. Disclosures and analyst certifications are present in Appendix. Anand Rathi Research India Equities

India I Equities Country

Daily

6 May 2014

India Morning Bell

All the latest research and data

Hindustan Unilever - Weak performance continues; Sell. We value the stock at a target price of `510, at a target PE of 27x FY16e earnings. As Hindustan Lever continues to reel from the heat of keener competition in segments such as laundry, skin care and oral care, we expect it to continue investing in these categories. We expect it to report revenue and earnings CAGRs of just 10% and 5%, respectively. Hence, we believe that, at current levels, any stock-price upside has already been capped.

Canara Bank - Core earnings modest, high slippages persist; Sell. On our higher business growth assumptions, we raise our FY15/16 PAT estimates for the bank by 5.7%/4.3%. On the better RoE, we raise our target from `225 to `275. We maintain our Sell rating, since we expect near-term profitability to be constrained by weak asset quality. While the present valuation appears to price in asset-quality concerns, persistent perceptions of default risk would restrict a valuation re-rating. Our target is based on the two-stage DDM (CoE: 18.1%; beta: 1.2; Rf: 8.5%).

Emami - Restrained revenues, better margins; Buy. We value the stock at a target price of `550, at a target PE of 22x FY16e earnings. Over the past 12 years, it has quoted at an average PE of 18x. Considering the healthy growth momentum, however, we value it near the mean PE + 1 Standard deviation. Because of the healthy margin-expansion potential due to lower menthol prices, the strong revenue-growth momentum from the Canteen Stores Department, rural sales and modern trade, we expect the company to report a 17% earnings CAGR over FY14-16. The management has indicated that it would launch about eight products over the next 3-4 quarters and this would help sustain the earnings-growth momentum ahead.

V-Guard Industries - A good quarter, but fairly valued; Hold. We have raised our FY14 and FY15 estimates as we believe that a harsh summer and truncated monsoon would generate greater demand for frontline products such as stabilisers, fans and pumps. However, we are concerned by weaker elements in distribution channels, which are experiencing liquidity problems and could impede growth. Hence, we have restricted our upward revision for the company’s PAT in FY15 and FY16 to 11% and 14%, respectively. At the ruling price of `523, the stock quotes at a P/E and an EV/EBIDTA of 15.4x and 9.1x, respectively, discounting its FY16e figures.

Sensex: 22445

Nifty: 6699

Markets 5 May ’14 1 Day YTD Sensex 22445 0.2% 6.0%Nifty 6699 0.1% 6.3%Dow Jones 16531 0.1% -0.3%S & P 500 1885 0.2% 2.0%FTSE 6822 0.2% 1.1%Nikkei* 14458 -0.2% -11.3%Hang Seng* 21976 -1.3% -5.7%

Volumes (US$m) 5 May ’14 1 Day Avg '14Cash BSE 404 5.2% 399Cash NSE 1,900 0.3% 1,988Derivatives (NSE) 11,575 13.0% 24,233

Flows (US$m) 5 May ’14* MTD YTD FII – Cash Buy 371 833 35,919Sell 325 722 31,344Net 46 111 5,374FII - Derivatives Buy 1,676 3,251 264,706Sell 1,837 3,288 260,844Net -161 -37 3,170DII – Cash Buy 177 305 6,263Sell 214 410 7,892Net -37 -105 -1,511

Others 5 May ’14 1 Day YTD Oil Brent (US$/bbl)* 107.6 -0.1% -1.8%Gold (US$/oz)* 1,309.2 -0.1% 8.6%Steel (US$/MT) 590.0 0.0% 0.9%`/US$ 60.23 0.0% 2.6%US$/Euro* 1.39 0.0% -1.0%Yen/US$* 102.13 0.0% 3.1%Call Rate 7.25% -35.bps -150.bps10-year G-Secs 8.74% .bps -8.9bpsEMBI spreads 317.32 -1.5bps -16.9bps@7:30am *Provisional Source: BSE, Bloomberg

6 May 2014 India Morning Bell

Anand Rathi Research India Equities

Market Data

Price Performance Price Performance Price Performance Top-5 gainers Top-5 gainers Top-5 gainersCompany CMP (INR) 1 wk (%) 1 Mth (%) Company CMP (INR) 1 wk (%) 1 Mth (%) Company CMP (INR) 1 wk (%) 1 Mth (%)

MARICO LTD 227 11.2 8.1 ATUL LTD 651 22.7 48.2 TATA SPONGE IRON 603 25.7 17.4

INDIAN OVERSEAS 60 8.7 15.2 TVS MOTOR CO LTD 100 15.2 9.0 HSIL LTD 182 23.3 31.8

WOCKHARDT LTD 775 7.3 27.7 SOLAR INDUSTRIES 1194 14.6 30.6 ASTRA MICROWAVE 77 22.8 41.1

TORRENT PHARMA 601 6.7 6.9 UNITED BK OF IND 35 12.3 12.1 PREMIER CAPITAL 195 20.1 80.0

ING VYSYA BANK 585 6.6 (3.6) ALSTOM INDIA LTD 463 11.4 12.9 FUTURE LIFESTYLE 94 12.9 43.2

Top-5 losers Top-5 losers Top-5 losersCompany CMP (INR) 1 wk (%) 1 Mth (%) Company CMP (INR) 1 wk (%) 1 Mth (%) Company CMP (INR) 1 wk (%) 1 Mth (%)

JUST DIAL LTD 1005 (19.5) (35.6) HEXAWARE TECHNOL 148 (13.7) (8.1) VIP INDS LTD 80 (17.6) (22.3)

RELIANCE COMMUNI 117 (11.1) (9.2) DELTA CORP LTD 88 (12.8) (13.5) KESORAM INDS LTD 62 (16.2) (17.0)

JINDAL STEEL & P 244 (10.9) (18.6) PIPAVAV DEFENCE 43 (12.7) 16.4 HCL INFOSYSTEMS 43 (13.1) 1.4

TATA COMMUNICATI 273 (10.3) (9.7) JET AIRWAYS IND 240 (12.6) (13.8) ACCELYA KALE SOL 665 (12.9) (16.5)

DLF LTD 139 (9.6) (21.0) DEWAN HOUSING 222 (12.1) (0.3) JK TYRE & IND LT 191 (12.8) 4.6

Volume Volume VolumeVolume spurts Volume spurts Volume spurtsCompany CMP (INR) 1 wk avg 1/4 wk (%) Company CMP (INR) 1 wk avg 1/4 wk (%) Company CMP (INR) 1 wk avg 1/4 wk (%)

KANSAI NEROLAC P 1,240 21,022 205.0 ALSTOM INDIA LTD 463 681,558 223.6 ASIAN STAR CO 556 11 285.5

INDIAN OVERSEAS 60 12,985,788 197.7 AJANTA PHARMA 1,061 386,814 188.8 CENTURY PLYBOARD 40 3,388,492 260.6

ALSTOM T&D INDIA 271 664,107 167.7 NATIONAL BUILDIN 207 1,542,374 185.2 TIME TECHNOPLAST 39 514,787 243.3

UPL LTD 279 14,835,853 137.8 3M INDIA LTD 3,750 3,750 177.1 CENTRUM CAP LTD 23 9,243 226.6

CENTRAL BK INDIA 54 2,614,703 114.9 HATSUN AGRO PROD 269 55,672 176.8 TATA SPONGE IRON 603 2,148,066 217.1

Technicals Technicals Technicals Above 200 DMA Above 200 DMA Above 200 DMACompany CMP (INR) 200D Avg (%) Company CMP (INR) 200D Avg (%) Company CMP (INR) 200D Avg (%)

ADANI ENTERPRISE 426 242 74.1 PRITI MERCANTILE 707 283 144.9 CHANNEL NINE ENT 502 135 258.0

AUROBINDO PHARMA 594 351 68.2 # AMTEK AUTO LTD 181 86 107.5 GREENCREST FINAN 197 58 226.6

APOLLO TYRES LTD 165 99 64.6 # SYMPHONY LTD 870 448 91.9 ECO FRIENDLY FOO 289 96 192.4

WOCKHARDT LTD 775 474 62.3 # PARAG SHILPA INV 525 273 90.7 ESTEEM BIO PROC 581 212 165.0

UPL LTD 279 175 58.7 MONSANTO INDIA 1735.4 929.0 84.8 MAA JAGDAMBE TRA 92 35 159.4

Below 200 DMA Below 200 DMA Below 200 DMACompany CMP (INR) 200D Avg (%) Company CMP (INR) 200D Avg (%) Company CMP (INR) 200D Avg (%)

IDEA CELLULAR 130 157 (16.8) STRIDES ARCOLAB 515 637 (19.1) INDIAN INFOTECH 6 26 (75.7)

NTPC LTD 114 134 (15.0) JET AIRWAYS IND 240 293 (18.3) GLOBAL INFRATECH 46 79 (41.0)

JUST DIAL LTD 1,005 1,183 (14.8) WESTLIFE DEVELOP 325 368 (11.5) LUMINAIRE TECH 25 42 (40.7)

JUBILANT FOODWOR 963 1,127 (14.3) WNS HOLDINGS-ADR 1,131 1,262 (10.5) UNNO INDUS LTD 19 29 (34.1)

RELIANCE COMMUNI 117 132 (11.0) BAJAJ CORP LTD 205 229 (10.4) JAYBHARAT TEXTIL 22 34 (33.6)

Small Caps(US$100m-250m)

Large Caps(>US$1bn)

Mid Caps(US$250m-1bn)

Source: Bloomberg

Anand Rathi Shares and Stock Brokers Limited (hereinafter “ARSSBL”) is a full service brokerage and equities research firm and the views expressed therein are solely of ARSSBL and not of the companies which have been covered in the Research Report. This report is intended for the sole use of the Recipient and is to be circulated only within India and to no countries outside India. Disclosures and analyst certifications are present in Appendix. Anand Rathi Research India Equities

Consumer

Visit NoteIndia I Equities

Key financials (YE Mar) FY12 FY13 FY14e FY15e FY16e

Sales (`m) 234,363 270,040 285,390 313,384 344,631

Net profit (`m) 26,770 32,233 37,068 38,067 40,488

EPS (`) 12.4 14.9 17.1 17.6 18.7

Growth (%) 25.3 20.4 15.0 2.7 6.4

PE (x) 45.0 37.4 32.5 31.6 29.8

PBV (x) 34.7 45.3 35.9 33.3 31.1

RoE (%) 89.6 105.2 123.3 109.1 108.0

RoCE (%) 92.7 94.3 88.8 88.8 92.8

Dividend yield (%) 1.3 3.3 2.3 2.5 2.7

Net gearing (%) (92.9) (94.9) (112.4) (115.0) (119.4)

Source: Company, Anand Rathi Research

Rating: Sell Target Price: `510 Share Price: `557

Key data HUVR IN / HLL.BO52-week high / low `725 / `536Sensex / Nifty 22445 / 66993-m average volume US$21m Market cap `1,239bn / US$20bnShares outstanding 2,163m

Shareholding pattern (%) Mar ’14 Dec ’13 Sep ’13

Promoters 67.3 67.3 67.3 - of which, Pledged - - -Free Float 32.7 32.7 32.7 - Foreign Institutions 14.1 14.8 15.3 - Domestic Institutions 4.1 3.4 3.0 - Public 14.5 14.5 14.4

6 May 2014

Hindustan Unilever

Weak performance continues; Sell

Key takeaways from call with distributor

Decline in revenues in past two months. The distributor indicated that revenue has dropped in the past two months due to the March book closure and reduction in the inventory-holding period. He down-stocked as he was expecting freebies in April.

Price hikes in the soap segments. The company hiked prices of some brands of soaps, by 5-6%. It hiked prices of Lux 5-6% and raised prices of Lifebuoy 6%. The distributor indicated that prices of most of the soap brands may be hiked in the coming months.

Delayed summer impacting revenue. Due to the delayed summer, the company’s foods segment (ice creams) was severely hit. Similarly, volumes soaps & detergents were impacted. The distributor believes that if the summer is shorter, revenues and volumes in these segments would be subdued.

Other segments flat. Other divisions, including Personal Products & Beverages, have registered flat growth rates. To counter the slowdown in the March quarter, the company has started various promotional schemes to boost demand during this quarter. In order to arrest the drop in revenue of Pepsodent, the company has started distributing Lifebuoy soap free.

Our take. We value the stock at a target price of `510, at a target PE of 27x FY16e earnings. As Hindustan Lever continues to reel from the heat of keener competition in segments such as laundry, skin care and oral care, we expect it to continue investing in these categories. We expect it to report revenue and earnings CAGRs of just 10% and 5%, respectively. Hence, we believe that, at current levels, any stock-price upside has already been capped. Risks. Lower raw-material prices and less-than expected competitive pressures.

Relative price performance

HUVR

Sensex500

550

600

650

700

750

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Source: Bloomberg

6 May 2014 Hindustan Unilever – Weak performance continues; Sell

Anand Rathi Research 2

Quick Glance – Financials and ValuationsFig 1 – Income statement (` m) Year-end: Mar FY12 FY13 FY14e FY15e FY16e

Net revenues 234,363 270,040 285,390 313,384 344,631 Revenue growth (%) 18.9 15.2 5.7 9.8 10.0 - Oper. expenses 199,528 227,987 244,916 268,272 294,727 EBIDTA 34,836 42,053 40,474 45,111 49,905 EBITDA margin (%) 14.9 15.6 14.2 14.4 14.5 - Interest expenses 17 257 407 353 353 - Depreciation 2,335 2,513 2,955 3,402 3,822 + Other income 2,596 5,320 12,653 10,235 9,140 - Tax 8,215 12,267 12,594 13,414 14,266 Effective tax rate (%) 23.4 27.5 25.3 26.0 26.0 Reported PAT 26,865 32,337 37,170 38,177 40,603 +/- Extraordinary items 1,137 6,057 2,387 - -+/- Minority interest 95 104 102 110 115 Adjusted PAT 27,907 38,290 39,456 38,067 40,488 Adj. FDEPS (`/sh) 12.4 14.9 17.1 17.6 18.7 Adj. FDEPS growth (%) 25.3 20.4 15.0 2.7 6.4 Source: Company, Anand Rathi Research

Fig 3 – Cash-flow statement (` m) Year-end: Mar FY12 FY13 FY14e FY15e FY16e

PAT 27,907 38,290 39,456 38,067 40,488 +Non-cash items 2,335 2,513 2,955 3,402 3,822 Cash profit 30,242 40,803 42,411 41,469 44,310 - Incr./(Decr.) in WC (7,545) 4,295 8,147 4,877 5,262 Operating cash-flow 22,571 39,136 50,572 46,455 49,687 -Capex (2,734) (4,407) (7,605) (7,000) (7,000) Free cash-flow 19,837 34,729 42,967 39,455 42,687 -Dividend (8,762) (41,538) (32,441) (35,425) (37,955) + Equity raised 336 73 0 - - + Debt raised - 247 (387) - - -Investments (5,794) (4,629) (3,985) (28,500) (4,800) -Misc. items 1,307 6,321 - - - Net cash-flow 6,925 (4,796) 6,153 (24,470) (68) +Op. cash & bank bal. 2,505 9,420 19,007 25,160 691 Cl. cash & bank bal. 9,430 4,625 25,160 691 622 Source: Company, Anand Rathi Research

Fig 5 – PE band

HUVR 17x

25x

33x

41x

50x

0

150

300

450

600

750

900

Jun-

00

Feb-

01

Oct

-01

Jul-0

2

Mar

-03

Nov

-03

Jul-0

4

Apr-0

5

Dec

-05

Aug-

06

May

-07

Jan-

08

Sep-

08

Jun-

09

Feb-

10

Oct

-10

Jul-1

1

Mar

-12

Nov

-12

Jul-1

3

Apr-1

4

Source: Bloomberg, Anand Rathi Research

Fig 2 – Balance sheet (` m) Year-end: Mar FY12 FY13 FY14e FY15e FY16e

Share capital 2,162 2,163 2,163 2,163 2,163 Reserves & surplus 34,649 26,485 33,210 35,852 38,385Net worth 36,811 28,648 35,373 38,015 40,548 Minority interest 183 209 223 333 448 Total debt 10,060 12,170 11,783 11,783 11,783 Def. tax liab. (net) (2,099) (2,085) (1,796) (1,796) (1,796)Capital employed 44,954 38,941 45,583 48,335 50,983 Net fixed assets 24,905 26,539 31,188 34,787 37,965 Investments 27,030 29,708 33,694 62,194 66,994 - of which, Liquid 27,030 29,708 33,694 62,194 66,994 Net working capital (26,945) (36,313) (44,460) (49,336) (54,598)Cash and bank balance 19,964 19,007 25,160 691 622 Capital deployed 44,954 38,941 45,583 48,335 50,983 Net debt (39,034) (38,631) (48,867) (52,897) (57,629)WC days (11.5) (13.4) (15.6) (15.7) (15.8)Book value (`/sh) 16.1 12.3 15.5 16.7 17.9 Source: Company, Anand Rathi Research

Fig 4 – Ratio analysis @ `557 Year-end: Mar FY12 FY13 FY14e FY15e FY16e

P/E (x) 45.0 37.4 32.5 31.6 29.8 P/B (x) 34.7 45.3 35.9 33.3 31.1 EV/Sales (x) 5.0 4.4 4.1 3.8 3.4 EV/EBITDA (x) 33.8 28.0 29.1 26.1 23.6 RoAE (%) 89.6 105.2 123.3 109.1 108.0 RoACE (%) 92.7 94.3 88.8 88.8 92.8 Dividend yield (%) 1.3 3.3 2.3 2.5 2.7 Dividend payout (%) 60.6 124.1 75.8 79.5 80.1 RM to sales (%) 53.3 52.2 52.1 51.8 51.7 Ad spend to sales (%) 11.5 12.2 12.9 13.0 13.0 EBITDA growth (%) 46.5 20.7 (3.8) 11.5 10.6 EPS growth (%) 25.3 20.4 15.0 2.7 6.4 PAT margin (%) 11.5 12.0 13.0 12.2 11.8 FCF/EPS (%) 73.8 107.4 115.6 103.3 105.1 OCF/Sales (%) 9.6 14.5 17.7 14.8 14.4 Source: Company, Anand Rathi Research

Fig 6 – Revenue break-up

Personal products

30%

Detergents21%

Soaps20%

Others12%

Tea & garden tea

11%

Canned & processed food

3%

Branded staple foods2%

Ice cream1%

Source: Company

Appendix Analyst Certification The views expressed in this Research Report accurately reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the research analyst(s) was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analyst(s) in this report. The research analysts are bound by stringent internal regulations and also legal and statutory requirements of the Securities and Exchange Board of India (hereinafter “SEBI”) and the analysts’ compensation are completely delinked from all the other companies and/or entities of Anand Rathi, and have no bearing whatsoever on any recommendation that they have given in the Research Report. Important Disclosures on subject companies Rating and Target Price History (as of 5 May 2014)

HUL

1 2 34

56

7

8

9

170

270

370

470

570

670

770

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Date Rating TP (`)

Share Price (`)

1 12-Dec-08 Sell 207 240 2 12-May-09 Sell 218 225 3 16-Jul-09 Sell 249 266 4 16-Mar-10 Sell 204 227 5 27-Jun-11 Sell 265 318 6 8-Nov-11 Sell 330 382 7 8-Oct-12 Sell 466 560 8 9-Apr-13 Sell 440 471 9 2-May-13 Sell 510 584

The research analysts, strategists, or research associates principally responsible for the preparation of Anand Rathi Research have received compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues and overall investment banking revenues.

Anand Rathi Ratings Definitions

Analysts’ ratings and the corresponding expected returns take into account our definitions of Large Caps (>US$1bn) and Mid/Small Caps (<US$1bn) as described in the Ratings Table below:

Ratings Guide Buy Hold Sell Large Caps (>US$1bn) >15% 5-15% <5% Mid/Small Caps (<US$1bn) >25% 5-25% <5%

Anand Rathi Research Ratings Distribution (as of 4 March 2014) Buy Hold Sell Anand Rathi Research stock coverage (182) 64% 27% 9% % who are investment banking clients 4% 0% 0% Other Disclosures This report has been issued by ARSSBL which is a SEBI regulated entity, and which is in full compliance with all rules and regulations as are applicable to its functioning and governance. The investors should note that ARSSBL is one of the companies comprising within ANAND RATHI group, and ANAND RATHI as a group consists of various companies which may include (but is not limited to) its subsidiaries, its affiliates, its group companies who may hold positions, views, stakes and may service the companies covered in this report independent of ARSSBL. Investors are cautioned to be aware that there could arise a potential conflict of interest in the views held by ARSSBL and other companies of Anand Rathi who maybe affiliated, connected or catering to the companies mentioned in the Research Report; even though, ARSSBL and Anand Rathi are fully complaint with all procedural and operational regulatory requirements. Thus, investors should not use this as a sole basis for making their investment decision and should consider the recommendations mentioned in the Research Report bearing in mind the aforementioned.

Further, the information herein has been obtained from various sources which we believe is reliable, and we do not guarantee its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes an offer, or an invitation to make an offer, to buy or sell any securities or any options, futures or other derivatives related to such securities (hereinafter referred to as “Related Investments”). ARSSBL and/or Anand Rathi may trade for their own accounts as market maker / jobber and/or arbitrageur in any securities of the companies mentioned in the Research Report or in related investments, and may be on taking a different position from the ones which haven been taken by the public orders. ARSSBL and/or Anand Rathi and its affiliates, directors, officers, and employees may have a long or short position in any securities of the companies mentioned in the Research Report or in Related Investments. ARSSBL and/or Anand Rathi, may from time to time, perform investment banking, investment management, financial advisory or any other services not explicitly mentioned herein, or solicit investment banking or other business from, any entity and/or company mentioned in this Research Report; however, the same shall have no bearing whatsoever on the specific recommendations made by the analyst(s), as the recommendations made by the analyst(s) are completely independent of the views of the other companies of Anand Rathi, even though there might exist an inherent conflict of interest.

Furthermore, this Research Report is prepared for private circulation and use only. It does not have regard to the specific investment objectives, financial situation and the specific financial needs or objectives of any specific person who may receive this Research Report. Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this Research Report, and, should understand that statements regarding future prospects may or may not be realized, and we can not guarantee the same as analysis and valuation is a tool to enable investors to make investment decisions but, is not an exact and/or a precise science. Investors should note that income from such securities, if any, may fluctuate and that each security's price or value may rise or fall. Past performance is not necessarily a guide to future performance. Foreign currency rates of exchange may adversely affect the value, price or income of any security or related investments mentioned in this report.

Other Disclosures pertaining to distribution of research in the United States of America

This material was produced by ARSSBL, solely for information purposes and for the use of the recipient. It is not to be reproduced under any circumstances and is not to be copied or made available to any person other than the recipient. It is distributed in the United States of America by Enclave Capital LLC (19 West 44th Street, Suite 1700, New York, NY 10036) and elsewhere in the world by ARSSBL or an authorized affiliate of ARSSBL (such entities and any other entity, directly or indirectly, controlled by ARSSBL, the “Affiliates”). This document does not constitute an offer of, or an invitation by or on behalf of ARSSBL or its Affiliates or any other company to any person, to buy or sell any security. The information contained herein has been obtained from published information and other sources, which ARSSBL or its Affiliates consider to be reliable. None of ARSSBL or its Affiliates accepts any liability or responsibility whatsoever for the accuracy or completeness of any such information. All estimates, expressions of opinion and other subjective judgments contained herein are made as of the date of this document. Emerging securities markets may be subject to risks significantly higher than more established markets. In particular, the political and economic environment, company practices and market prices and volumes may be subject to significant variations. The ability to assess such risks may also be limited due to significantly lower information quantity and quality. By accepting this document, you agree to be bound by all the foregoing provisions.

1. ARSSBL or its Affiliates may or may not have been beneficial owners of the securities mentioned in this report.

2. ARSSBL or its affiliates may have or not managed or co-managed a public offering of the securities mentioned in the report in the past 12 months.

3. ARSSBL or its affiliates may have or not received compensation for investment banking services from the issuer of these securities in the past 12 months and do not expect to receive compensation for investment banking services from the issuer of these securities within the next three months.

4. However, one or more of ARSSBL or its Affiliates may, from time to time, have a long or short position in any of the securities mentioned herein and may buy or sell those securities or options thereon, either on their own account or on behalf of their clients.

5. As of the publication of this report, ARSSBL does not make a market in the subject securities.

6. ARSSBL or its Affiliates may or may not, to the extent permitted by law, act upon or use the above material or the conclusions stated above, or the research or analysis on which they are based before the material is published to recipients and from time to time, provide investment banking, investment management or other services for or solicit to seek to obtain investment banking, or other securities business from, any entity referred to in this report.

Enclave Capital LLC is distributing this document in the United States of America. ARSSBL accepts responsibility for its contents. Any US customer wishing to effect transactions in any securities referred to herein or options thereon should do so only by contacting a representative of Enclave Capital LLC.

© 2014 Anand Rathi Shares and Stock Brokers Limited. All rights reserved. This report or any portion thereof may not be reprinted, sold or redistributed without the prior written consent of Anand Rathi Shares and Stock Brokers Limited.

Additional information on recommended securities/instruments is available on request.

Anand Rathi Shares and Stock Brokers Limited (hereinafter “ARSSBL”) is a full service brokerage and equities research firm and the views expressed therein are solely of ARSSBL and not of the companies which have been covered in the Research Report. This report is intended for the sole use of the Recipient and is to be circulated only within India and to no countries outside India. Disclosures and analyst certifications are present in Appendix. Anand Rathi Research India Equities

India I Equities

Banks

Result Update

6 May 2014

Canara Bank

Core earnings modest, high slippages persist; Sell

Key takeaways

Aggressive credit growth, sturdy NIM, CASA share improves. While Canara Bank’s advances rose 24.3% yoy (4.6% qoq), deposits grew slower, at 18.2% yoy (2.9% qoq), increasing the credit-deposit by 350bps yoy to 71.6%. Advances growth was driven by the retail sector (45.2% yoy), farm (19.6% yoy) and SME loans (35.2% yoy). Adjusting for the interest income on income-tax refund, NIM was flat yoy, at 2.2%. CASA share increased 36bps yoy (145bps qoq) to 24.5%, led by a sharp 20% qoq rise in current deposits.

Strong fee income, weak Treasury profits, but better productivity. While fee income rose 39% yoy (52.2% qoq), trading profits fell 70% yoy to `748m and comprised 4% of pre-provisioning profits (14.8% in 4QFY13). Productivity improved, with core cost-to-income falling 38bps yoy (75bps qoq) to 48.8%, even as the bank expanded its distribution by adding 198 branches and 1,769 ATMs. With the management’s vast branch-expansion plans (6,000 branches and 10,000 ATMs by Mar’15), the operating leverage is unlikely to improve. Hence, we expect cost-to-assets at ~1.3% over FY15-16.

High slippages and loan restructuring persist, low NPA coverage. While gross NPA fell 8% qoq, fresh slippages were `21.4bn (annualised, 3.1% of loans). Total restructured loans are now `232bn (7.7% of loans), led by incremental restructuring of `14.3bn (annualised, 1.9% of loans). While NPA coverage rose 629bps qoq to 21.2%, it still is the lowest of its peers.

Our take. On our higher business growth assumptions, we raise our FY15/16 PAT estimates for the bank by 5.7%/4.3%. On the better RoE, we raise our target from `225 to `275. We maintain our Sell rating, since we expect near-term profitability to be constrained by weak asset quality. While the present valuation appears to price in asset-quality concerns, persistent perceptions of default risk would restrict a valuation re-rating. Our target is based on the two-stage DDM (CoE: 18.1%; beta: 1.2; Rf: 8.5%). Risks. Faster-than-estimated credit growth, sharp decline in defaults.

Rating: Sell Target Price: `275 Share Price: `304

Key data CBK IN / CNBK.BO52-week high / low `457 / `190 Sensex / Nifty 22445 / 66993-m average volume US$11.8m Market cap `140bn / US$2.3bn Shares outstanding 461.3m

Shareholding pattern (%) Mar ’14 Dec ’13 Sep ’13

Promoters 69.0 69.0 67.7 - of which, Pledged - - -Free Float 31.0 31.0 32.3 - Foreign Institutions 9.0 10.3 11.9 - Domestic Institutions 13.1 12.9 13.1 - Public 8.9 7.8 7.3

Quarterly results (YE: Mar) 4QFY13 4QFY14 % yoy FY13 FY14 % yoy

Net interest income (`m) 20,906 25,352 21.3 78,790 89,444 13.5

Non-interest income (`m) 10,065 10,700 6.3 31,530 39,328 24.7

Operating expenses (`m) 13,994 17,231 23.1 51,420 60,810 18.3

Cost-to-income (%) 45.2 47.8 261 bps 46.6 47.2 61 bps

Pre-provisioning profit (`m) 16,977 18,821 10.9 58,900 67,962 15.4 Provisions (`m) 7,524 10,913 45.0 22,179 37,330 68.3 PBT (`m) 9,454 7,908 (16.3) 36,721 30,632 (16.6)

Tax (`m) 2,200 1,800 (18.2) 8,000 6,250 (21.9)

PAT (`m) 7,254 6,108 (15.8) 28,721 24,382 (15.1)

EPS (`) 16.4 13.7 (16.6) 64.8 54.5 (16.0)

Source: Company, Anand Rathi Research

Financials (YE: Mar) FY15e FY16e

Net interest income (`m) 104,002 124,185 Net profit (`m) 35,381 45,412 EPS (`) 76.7 98.5 Growth (%) 45.1 28.4 PE (x) 4.0 3.1 PABV (x) 0.7 0.6 RoE (%) 11.9 14.4 RoA (%) 0.7 0.7 Dividend yield (%) 5.3 6.8 Net NPA (%) 2.0 1.9 Source: Anand Rathi Research

Change in Estimates Target Reco

Estimates revision (%) FY15e FY16e

NII 2.7 1.8PPP 3.6 3.1Provisions 5.7 4.3PAT 5.7 4.3

6 May 2014 Canara Bank – Core earnings modest, high slippages persist; Sell

Anand Rathi Research 2

Quick Glance – Financials and Valuations Fig 1 – Income statement (` m) Year-end: Mar FY12 FY13 FY14 FY15e FY16e

Net interest income 76,893 78,790 89,444 104,002 124,185 NII growth (%) (0.1) 2.5 13.5 16.3 19.4 Non-interest inc 29,276 31,530 39,328 44,423 51,804 Total income 106,169 110,320 128,772 148,425 175,990 Total Inc growth (%) 1.0 3.9 16.7 15.3 18.6 Op. expenses 46,737 51,420 60,810 71,689 84,123 Operating profit 59,432 58,900 67,962 76,736 91,867 Op profit growth (%) (2.4) (0.9) 15.4 12.9 19.7 Provisions 18,605 22,179 37,330 32,231 34,745 PBT 40,827 36,721 30,632 44,505 57,122 Tax 8,000 8,000 6,250 9,123 11,710 PAT 32,827 28,721 24,382 35,381 45,412 PAT growth (%) (18.5) (12.5) (15.1) 45.1 28.4 FDEPS (`/sh) 74.1 64.8 52.9 76.7 98.5 DPS (`/sh) 11.0 13.0 11.0 16.1 20.7 Source: Company, Anand Rathi Research

Fig 2 – Balance sheet (` m) Year-end: Mar FY12 FY13 FY14 FY15e FY16e

Share capital 4,430 4,430 4,613 4,613 4,613 Reserves & surplus 222,470 244,348 291,589 294,302 328,556 Deposits 3,270,537 3,558,560 4,207,228 5,052,881 6,004,388 Borrowings 244,165 316,088 415,789 449,600 486,403 Minority interests - - - - -Total liabilities 3,741,602 4,123,426 4,919,219 5,801,395 6,823,960 Advances 2,324,898 2,421,766 3,010,675 3,612,810 4,263,116 Investments 1,020,574 1,211,328 1,268,283 1,490,600 1,771,294 Cash & bank bal 281,794 347,147 448,287 471,731 523,415 Fixed & other assets 114,335 143,185 191,974 226,254 266,134 Total assets 3,741,602 4,123,426 4,919,219 5,801,395 6,823,960 No. of shares (m) 443 443 461 461 461 Deposits growth (%) 11.5 8.8 18.2 20.1 18.8 Advances growth (%) 10.0 4.2 24.3 20.0 18.0 Source: Company, Anand Rathi Research

Fig 3 – Key ratios Year-end: Mar FY12 FY13 FY14 FY15e FY16e

NIM (%) 2.2 2.1 2.1 2.0 2.0 Other inc / total inc (%) 27.6 28.6 30.5 29.9 29.4 Cost-income (%) 44.0 46.6 47.2 48.3 47.8 Provision coverage (%) 16.0 15.7 21.2 21.5 21.8 Dividend payout (%) 14.8 20.1 20.8 21.0 21.0 Credit-deposit (%) 71.1 68.1 71.6 71.5 71.0 Investment-deposit (%) 31.2 34.0 30.1 29.5 29.5 Gross NPA (%) 1.7 2.6 2.5 2.5 2.5 Net NPA (%) 1.5 2.2 2.0 2.0 1.9 BV (`) 465.6 515.7 598.1 604.0 678.2 Adj BV (`) 389.1 396.5 468.7 451.1 499.9 CAR (%) 13.8 12.4 10.6 10.4 9.8 - Tier 1 (%) 10.4 9.8 7.7 7.7 7.3 RoE (%) 15.4 12.1 8.9 11.9 14.4 RoA (%) 0.9 0.7 0.5 0.7 0.7 Source: Company, Anand Rathi Research

Fig 4 – PE band

CBK

2x

4x

6x

8x

0

150

300

450

600

750

900

May

-08

Nov

-08

May

-09

Nov

-09

May

-10

Nov

-10

May

-11

Nov

-11

May

-12

Nov

-12

May

-13

Nov

-13

May

-14

Source: Bloomberg, Anand Rathi Research

Fig 5 – Price-to-book band

CBK

0.4x

0.7x

1.0x

1.3x

0

150

300

450

600

750

900

May

-08

Nov

-08

May

-09

Nov

-09

May

-10

Nov

-10

May

-11

Nov

-11

May

-12

Nov

-12

May

-13

Nov

-13

May

-14

Source: Bloomberg, Anand Rathi Research

Fig 6 – Canara Bank vs. Bankex

CBK

Bankex

150

200

250

300

350

400

450

May

-13

Jun-

13

Jul-1

3

Aug-

13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr-1

4

May

-14

Source: Bloomberg

6 May 2014 Canara Bank – Core earnings modest, high slippages persist; Sell

Anand Rathi Research 3

Result Highlights Fig 7 – 4QFY14 Results vs Expectations (` m) 4QFY14 4QFY14e Var % 4QFY13 YoY % 3QFY14 QoQ %

Net interest income 25,352 21,506 17.9 20,906 21.3 22,270 13.8 Non-interest income 10,700 8,531 25.4 10,065 6.3 8,514 25.7 Pre-provisioning profits 18,821 14,324 31.4 16,977 10.9 15,909 18.3 PAT 6,108 5,003 22.1 7,254 (15.8) 4,093 49.2

Source: Company, Anand Rathi Research

Fig 8 – 3QFY14 Results (` m) 4QFY14 4QFY13 YoY 3QFY14 QoQ

Credit 3,010,675 2,421,766 24.3 2,877,001 4.6 Deposits 4,207,228 3,558,560 18.2 4,089,244 2.9 Credit-to-deposits 71.6 68.1 350 bps 70.4 120 bps CASA % 24.5 24.2 36 bps 23.1 145 bps Gross NPA 75,702 62,602 20.9 80,739 (6.2)Net NPA 59,655 52,781 13.0 68,699 (13.2)Gross NPA % 2.5 2.6 (8) bps 2.8 (30) bpsNet NPA % 2.0 2.2 (20) bps 2.4 (41) bpsNPA coverage % 21.2 15.7 551 bps 14.9 629 bps Capital adequacy % 10.6* 12.4 (177) bps 9.8* 80 bps Tier-1 % 7.7* 9.8 (209) bps 7.5* 20 bps

Source: Company, Anand Rathi Research (Note: *Basel-3)

Aggressive credit growth and sturdy NIM, but proportion of CASA declines

Canara Bank’s credit grew 24.3% yoy, much faster than the past four-quarter average of 19.3%. Deposits grew slower, at 18.2% yoy, swelling the credit-deposit by 350bps yoy to 71.6%. Adjusting for the interest income on income-tax refund, NIM was flat yoy, at 2.2%. The share of CASA increased 36bps yoy (145bps qoq) to 24.5%, led by a sharp 20% qoq rise in current deposits. In absolute terms, CASA grew 20% yoy.

Average CASA per branch, at `223m, was down 1.3% yoy; it has been on a continuous downtrend since Mar’11 due to the large number of branches added. We expect the proportion of CASA, at ~25%, to be stagnant over FY14-16. While credit-deposit is likely to rise in FY15 and FY16, the bank’s low base rate and share of CASA are likely to keep NIM over FY15-16 constrained at 2%. We expect both advances and deposits to register CAGRs over FY14-16 of 19% and 19.5%, respectively.

Fig 9 – Credit-deposit, at 71.6%, has increased qoq and yoy

1,800

1,950

2,100

2,250

2,400

2,550

2,700

2,850

3,000

3,150

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

3QFY

13

4QFY

13

1QFY

14

2QFY

14

3QFY

14

4QFY

14

63.5

64.5

65.5

66.5

67.5

68.5

69.5

70.5

71.5

72.5

Advances Credit-deposit (RHS)

(`bn) (%)

Source: Company

6 May 2014 Canara Bank – Core earnings modest, high slippages persist; Sell

Anand Rathi Research 4

Strong fee income, weak Treasury profits, better productivity

While fee income rose 39% yoy (52.2% qoq), trading profits fell 70% yoy to `748m and comprised 4% of pre-provisioning profits (14.8% in 4QFY13). Productivity improved, with core cost-to-income falling 38bps yoy (75bps qoq) to 48.8%, even as the bank expanded its distribution by adding 198 branches and 1,769 ATMs. With the management’s vast branch-expansion plans (6,000 branches and 10,000 ATMs by Mar’15), operating leverage is unlikely to improve. Hence, we expect cost-to-assets at ~1.3% over FY15-16.

Fig 12 – Fee-income grows strongly, but comprises a low share of earning assets

2,500

2,900

3,300

3,700

4,100

4,500

4,900

5,300

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

3QFY

13

4QFY

13

1QFY

14

2QFY

14

3QFY

14

4QFY

14

0.28

0.31

0.34

0.37

0.40

0.43

0.46

0.49

Fees & commissions % of avg. earning assets

(`m) (%)

Source: Company

High slippages and loan restructuring persist; low NPA coverage

While gross NPA fell 8% qoq, fresh slippages were `21.4bn (annualised, 3.1% of loans). Total restructured loans are now `232bn (7.7% of loans), led by incremental restructuring of `14.3bn (annualised, 1.9% of loans). While NPA coverage rose 629bps qoq to 21.2%, it still is the lowest of its peers. Credit costs were a high 1.18% of loans, compared to 0.58% in 4QFY13.

Management has indicated that the restructuring pipeline is likely to be `30bn in FY15, spread across 12 accounts. Of these accounts, a single exposure comprises half of the restructuring pipeline. With likely weak asset quality, higher levels of restructured assets and low NPA coverage,

Fig 10 – Net interest income growth accelerated in 4QFY14

17

18

19

20

21

22

23

24

2526

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

3QFY

13

4QFY

13

1QFY

14

2QFY

14

3QFY

14

4QFY

14

(10)

(6)

(2)

2

6

10

14

18

2226

NII NII growth (RHS)

(`bn) (%)

Source: Company

Fig 11 – CASA share improves qoq to 24.5%

700

750

800

850

900

950

1,000

1,050

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

3QFY

13

4QFY

13

1QFY

14

2QFY

14

3QFY

14

4QFY

14

22

23

24

25

26

27

28

29

CASA CASA share (RHS)

(`bn) (%)

Source: Company

6 May 2014 Canara Bank – Core earnings modest, high slippages persist; Sell

Anand Rathi Research 5

credit costs are likely to constrain earnings growth over FY14-16. We expect NPA coverage (excl. technical write-offs) to be low (~21%) over FY14-16, led by the frail asset quality and a 16.3% CAGR in pre-provisioning profits over the same period. Perceptions of default risk would persist until the economic environment improves, restricting a sharp short-term valuation re-rating.

Fig 13 – Core cost-income falls yoy, but average profit per branch also declines

1.2

1.5

1.8

2.1

2.4

2.7

3.0

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

3QFY

13

4QFY

13

1QFY

14

2QFY

14

3QFY

14

4QFY

14

41.3

43.3

45.3

47.3

49.3

51.3

53.3

Avg. profit per branch Core cost-income (RHS)

(`m) (%)

Source: Company

Fig 14 – Gross NPA declines, NPA coverage has improved qoq

26

34

42

50

58

66

74

82

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

3QFY

13

4QFY

13

1QFY

14

2QFY

14

3QFY

14

4QFY

14

12

14

16

18

20

22

24

26

Gross NPAs NPA coverage (RHS)

(`bn) (%)

Source: Company

Fig 15 – High slippages and restructuring persisted in 4QFY14 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14Restructuring (` m) 28,770 16,830 9,990 34,540 14,320% of loans (annualised) 4.8 2.7 1.4 4.8 1.9Slippages (` m) 10,860 26,880 15,200 21,000 21,350% of avg. loans (annualised) 1.8 4.5 2.4 3.3 3.1

Source: Companies, Anand Rathi Research

6 May 2014 Canara Bank – Core earnings modest, high slippages persist; Sell

Anand Rathi Research 6

Valuations On our higher business growth assumptions, we raise our FY15/16 PAT estimates for the bank by 5.7%/4.3%. On the better RoE, we raise our target from `225 to `275. We maintain our Sell rating since we expect near-term profitability to be constrained by weak asset quality. While the present valuation appears to price in asset-quality concerns, persistent perceptions of default risk would restrict a valuation re-rating. At our Sep’15 target, the stock would quote at PABV of 0.5x FY15e and 0.4x FY16e. Our target is based on the two-stage DDM (CoE: 18.1%; beta: 1.2; Rf: 8.5%).

Fig 16 – Past one-year-forward P/BV

CBK

Mean

+1SD

-1SD

+2SD

-2SD0.1

0.4

0.7

1.0

1.3

1.6

1.9

May

-08

Nov

-08

May

-09

Nov

-09

May

-10

Nov

-10

May

-11

Nov

-11

May

-12

Nov

-12

May

-13

Nov

-13

May

-14

Source: Bloomberg, Anand Rathi Research

Risks

Faster credit growth may improve profitability and, consequently, lead to us increasing our earnings estimates.

Less dependence on bulk deposits and faster accretion in low-cost deposits could lead to NIM coming better than we estimate.

A more-than-expected increase in restructured bad loans.

6 May 2014 Canara Bank – Core earnings modest, high slippages persist; Sell

Anand Rathi Research 7

Financials We expect the bank to register a 19.3% CAGR in business over FY14-16, with advances and deposit CAGRs of 19% and 19.5%, respectively. We expect a 36.5% CAGR in net profit over the same period.

Fig 17 – Income Statement Year-end: Mar (` m) FY12 FY13 FY14 FY15e FY16e

Interest Income 308,506 340,779 395,476 482,448 586,787

Interest Expended 231,613 261,989 306,032 378,445 462,602

Net Interest Income 76,893 78,790 89,444 104,002 124,185

Growth (%) (0.1) 2.5 13.5 16.3 19.4

Non-interest Income 29,276 31,530 39,328 44,423 51,804

Total Income 106,169 110,320 128,772 148,425 175,990

Non-interest income / Total Inc (%) 27.6 28.6 30.5 29.9 29.4

Operating Expenses 46,737 51,420 60,810 71,689 84,123

Employee Expenses 29,731 32,536 36,724 45,164 52,998

Other Expenses 17,007 18,884 24,086 26,525 31,126

Pre-provisioning profit 59,432 58,900 67,962 76,736 91,867

Growth (%) (2.4) (0.9) 15.4 12.9 19.7

Provisions 18,605 22,179 37,330 32,231 34,745

Profit Before Tax 40,827 36,721 30,632 44,505 57,122

Taxes 8,000 8,000 6,250 9,123 11,710

Tax Rate (%) 19.6 21.8 20.4 20.5 20.5

Profit After Tax 32,827 28,721 24,382 35,381 45,412

Growth (%) (18.5) (12.5) (15.1) 45.1 28.4

Number of Shares (m) 443 443 461 461 461

Earnings Per Share (`) 74.1 64.8 52.9 76.7 98.5

Source : Company, Anand Rathi Research

Fig 18 – Balance Sheet Year-end: Mar (` m) FY12 FY13 FY14 FY15e FY16e

Share Capital 4,430 4,430 4,613 4,613 4,613

Reserves and Surplus 222,470 244,348 291,589 294,302 328,556

Net Worth 226,900 248,778 296,201 298,914 333,169

Deposits 3,270,537 3,558,560 4,207,228 5,052,881 6,004,388

Other Liabilities & Provisions 244,165 316,088 415,789 449,600 486,403

Total Loans 3,514,702 3,874,648 4,623,017 5,502,481 6,490,791

Total Liabilities 3,741,602 4,123,426 4,919,219 5,801,395 6,823,960

Advances 2,324,898 2,421,766 3,010,675 3,612,810 4,263,116

Investments 1,020,574 1,211,328 1,268,283 1,490,600 1,771,294

Cash & Bank Balances 281,794 347,147 448,287 471,731 523,415

Fixed & Other Assets 114,335 143,185 191,974 226,254 266,134

Total Assets 3,741,602 4,123,426 4,919,219 5,801,395 6,823,960

Source : Company, Anand Rathi Research

Appendix Analyst Certification The views expressed in this Research Report accurately reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the research analyst(s) was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analyst(s) in this report. The research analysts are bound by stringent internal regulations and also legal and statutory requirements of the Securities and Exchange Board of India (hereinafter “SEBI”) and the analysts’ compensation are completely delinked from all the other companies and/or entities of Anand Rathi, and have no bearing whatsoever on any recommendation that they have given in the Research Report. Important Disclosures on subject companies Rating and Target Price History (as of 5 May 2014)

Canara Bank

131

2

3

45

6

7

89

10

11

12

0

100

200

300

400

500

600

700

800

900

Jan-

08Ap

r-08

Jul-0

8

Oct

-08

Jan-

09Ap

r-09

Jul-0

9

Oct

-09

Jan-

10Ap

r-10

Jul-1

0

Oct

-10

Jan-

11Ap

r-11

Jul-1

1

Oct

-11

Jan-

12Ap

r-12

Jul-1

2O

ct-1

2Ja

n-13

Apr-1

3

Jul-1

3O

ct-1

3Ja

n-14

Apr-1

4

Date Rating TP (`)

Share Price (`)

1 24-Mar-09 Sell 115 151 2 4-May-09 Sell 163 208 3 8-Jul-09 Sell 171 265 4 2-Feb-10 Sell 379 404 5 19-Jul-10 Hold 537 479 6 25-Oct-10 Buy 863 732 7 6-May-11 Buy 776 559 8 28-Jul-11 Buy 625 479 9 14-Dec-11 Buy 559 415

10 7-Nov-12 Sell 405 420 11 5-Aug-13 Sell 239 242 12 16-Dec-13 Sell 260 262 13 3-Feb-14 Sell 225 222

The research analysts, strategists, or research associates principally responsible for the preparation of Anand Rathi Research have received compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues and overall investment banking revenues.

Anand Rathi Ratings Definitions

Analysts’ ratings and the corresponding expected returns take into account our definitions of Large Caps (>US$1bn) and Mid/Small Caps (<US$1bn) as described in the Ratings Table below:

Ratings Guide Buy Hold Sell Large Caps (>US$1bn) >15% 5-15% <5% Mid/Small Caps (<US$1bn) >25% 5-25% <5%

Anand Rathi Research Ratings Distribution (as of 4 March 2014) Buy Hold Sell Anand Rathi Research stock coverage (182) 64% 27% 9% % who are investment banking clients 4% 0% 0% Other Disclosures This report has been issued by ARSSBL which is a SEBI regulated entity, and which is in full compliance with all rules and regulations as are applicable to its functioning and governance. The investors should note that ARSSBL is one of the companies comprising within ANAND RATHI group, and ANAND RATHI as a group consists of various companies which may include (but is not limited to) its subsidiaries, its affiliates, its group companies who may hold positions, views, stakes and may service the companies covered in this report independent of ARSSBL. Investors are cautioned to be aware that there could arise a potential conflict of interest in the views held by ARSSBL and other companies of Anand Rathi who maybe affiliated, connected or catering to the companies mentioned in the Research Report; even though, ARSSBL and Anand Rathi are fully complaint with all procedural and operational regulatory requirements. Thus, investors should not use this as a sole basis for making their investment decision and should consider the recommendations mentioned in the Research Report bearing in mind the aforementioned.

Further, the information herein has been obtained from various sources which we believe is reliable, and we do not guarantee its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes an offer, or an invitation to make an offer, to buy or sell any securities or any options, futures or other derivatives related to such securities (hereinafter referred to as “Related Investments”). ARSSBL and/or Anand Rathi may trade for their own accounts as market maker / jobber and/or arbitrageur in any securities of the companies mentioned in the Research Report or in related investments, and may be on taking a different position from the ones which haven been taken by the public orders. ARSSBL and/or Anand Rathi and its affiliates, directors, officers, and employees may have a long or short position in any securities of the companies mentioned in the Research Report or in Related Investments. ARSSBL and/or Anand Rathi, may from time to time, perform investment banking, investment management, financial advisory or any other services not explicitly mentioned herein, or solicit investment banking or other business from, any entity and/or company mentioned in this Research Report; however, the same shall have no bearing whatsoever on the specific recommendations made by the analyst(s), as the recommendations made by the analyst(s) are completely independent of the views of the other companies of Anand Rathi, even though there might exist an inherent conflict of interest.

Furthermore, this Research Report is prepared for private circulation and use only. It does not have regard to the specific investment objectives, financial situation and the specific financial needs or objectives of any specific person who may receive this Research Report. Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this Research Report, and, should understand that statements regarding future prospects may or may not be realized, and we can not guarantee the same as analysis and valuation is a tool to enable investors to make investment decisions but, is not an exact and/or a precise science. Investors should note that income from such securities, if any, may fluctuate and that each security's price or value may rise or fall. Past performance is not necessarily a guide to future performance. Foreign currency rates of exchange may adversely affect the value, price or income of any security or related investments mentioned in this report.

Other Disclosures pertaining to distribution of research in the United States of America

This material was produced by ARSSBL, solely for information purposes and for the use of the recipient. It is not to be reproduced under any circumstances and is not to be copied or made available to any person other than the recipient. It is distributed in the United States of America by Enclave Capital LLC (19 West 44th Street, Suite 1700, New York, NY 10036) and elsewhere in the world by ARSSBL or an authorized affiliate of ARSSBL (such entities and any other entity, directly or indirectly, controlled by ARSSBL, the “Affiliates”). This document does not constitute an offer of, or an invitation by or on behalf of ARSSBL or its Affiliates or any other company to any person, to buy or sell any security. The information contained herein has been obtained from published information and other sources, which ARSSBL or its Affiliates consider to be reliable. None of ARSSBL or its Affiliates accepts any liability or responsibility whatsoever for the accuracy or completeness of any such information. All estimates, expressions of opinion and other subjective judgments contained herein are made as of the date of this document. Emerging securities markets may be subject to risks significantly higher than more established markets. In particular, the political and economic environment, company practices and market prices and volumes may be subject to significant variations. The ability to assess such risks may also be limited due to significantly lower information quantity and quality. By accepting this document, you agree to be bound by all the foregoing provisions.

1. ARSSBL or its Affiliates may or may not have been beneficial owners of the securities mentioned in this report.

2. ARSSBL or its affiliates may have or not managed or co-managed a public offering of the securities mentioned in the report in the past 12 months.

3. ARSSBL or its affiliates may have or not received compensation for investment banking services from the issuer of these securities in the past 12 months and do not expect to receive compensation for investment banking services from the issuer of these securities within the next three months.

4. However, one or more of ARSSBL or its Affiliates may, from time to time, have a long or short position in any of the securities mentioned herein and may buy or sell those securities or options thereon, either on their own account or on behalf of their clients.

5. As of the publication of this report, ARSSBL does not make a market in the subject securities.

6. ARSSBL or its Affiliates may or may not, to the extent permitted by law, act upon or use the above material or the conclusions stated above, or the research or analysis on which they are based before the material is published to recipients and from time to time, provide investment banking, investment management or other services for or solicit to seek to obtain investment banking, or other securities business from, any entity referred to in this report.

Enclave Capital LLC is distributing this document in the United States of America. ARSSBL accepts responsibility for its contents. Any US customer wishing to effect transactions in any securities referred to herein or options thereon should do so only by contacting a representative of Enclave Capital LLC.

© 2014 Anand Rathi Shares and Stock Brokers Limited. All rights reserved. This report or any portion thereof may not be reprinted, sold or redistributed without the prior written consent of Anand Rathi Shares and Stock Brokers Limited.

Additional information on recommended securities/instruments is available on request.

Anand Rathi Shares and Stock Brokers Limited (hereinafter “ARSSBL”) is a full service brokerage and equities research firm and the views expressed therein are solely of ARSSBL and not of the companies which have been covered in the Research Report. This report is intended for the sole use of the Recipient and is to be circulated only within India and to no countries outside India. Disclosures and analyst certifications are present in Appendix. Anand Rathi Research India Equities

Consumer

Result UpdateIndia I Equities

`

Rating: Buy Target Price: `550 Share Price: `467

Key data HMN IN / EMAM.BO52-week high / low `539 / `393Sensex / Nifty 22445 / 66993-m average volume US$1.5m Market cap `106bn / US$1.8bnShares outstanding 227m

Shareholding pattern (%) Mar ’14 Dec ’13 Sep ’13

Promoters 72.7 72.7 72.7 - of which, Pledged - - -Free Float 27.3 27.3 27.3 - Foreign Institutions 16.0 16.7 16.7 - Domestic Institutions 1.8 2.0 2.2 - Public 9.5 8.6 8.4

6 May 2014

Emami

Restrained revenues, better margins; Buy

Key takeaways

Healthy revenue growth. Emami reported a 1% yoy drop in revenue. It indicated that it had raised prices 4% but volumes were down 5% yoy. Domestic revenues were down 4.4% whereas revenues from the Canteen Stores Department were up 41.8% yoy. Revenue of the international division was up 8.9% yoy. The management also indicated that revenue from modern trade was up 21%. Brand-wise, revenue decline/growth came as follows: Navratna Cool Oil (6)%, Navratna Cool Talc (10)%, Zandu & Mentho Plus Balm (5)%, Zandu Healthcare range 52%, Zandu Pancharishta 190%. Fair & Handsome (2)%, Boroplus Antiseptic Cream (2)%. Boroplus Prickly Heat Powder (20)%. The company has reduced the inventory with the trade from 27 days to 17 days, which has resulted in revenues dropping by `250m.

EBITDA margin improves. The drop in menthol prices has helped the company report a 790-bp yoy gross-margin expansion. Slightly higher staff costs because of the increase in number of employees and in other expenditure led to the 430-bp yoy EBITDA-margin expansion. The adjusted effective income-tax rate was up 350bps yoy. The net profit has expanded 19% yoy.

Our take. We value the stock at a target price of `550, at a target PE of 22x FY16e earnings. Over the past 12 years, it has quoted at an average PE of 18x. Considering the healthy growth momentum, however, we value it near the mean PE + 1 Standard deviation. Because of the healthy margin-expansion potential due to lower menthol prices, the strong revenue-growth momentum from the Canteen Stores Department, rural sales and modern trade, we expect the company to report a 17% earnings CAGR over FY14-16. The management has indicated that it would launch about eight products over the next 3-4 quarters and this would help sustain the earnings-growth momentum ahead. Risks. Rise in prices of raw materials, keener-than-expected competition and delay in rollout of products.

Financials (YE Mar) FY15e FY16e

Sales (`m) 21,308 24,945

Net profit (`m) 4,638 5,552

EPS (`) 20.4 24.5

Growth (%) 13.6 19.7

PE (x) 22.9 19.1

PBV (x) 8.9 7.0

RoE (%) 43.6 41.2

RoCE (%) 44.3 41.5

Dividend yield (%) 1.7 1.9

Net gearing (%) (61.4) (66.7)

Source: Anand Rathi Research

Quarterly results (YE Mar) 4QFY13 4QFY14 % yoy FY13 FY14 % yoy

Sales (`m) 4,510 4,457 (1.2) 15,954 18,208 14.1

EBITDA (`m) 1,000 1,180 18.0 3,473 4,413 27.1

EBITDA margin (%) 22.2 26.5 430 bps 21.8 24.2 300 bps

Interest (`m) 8 16 105.1 66 54 (18.1)

Depreciation (`m) 59 65 8.9 220 352 60.1

Other income (`m) 194 184 (5.2) 557 622 11.7

PBT (`m) 1,127 1,283 13.9 3,744 4,629 23.6

Tax (`m) 181 160 (11.3) 540 547 1.3

Tax rate (%) 16.0 12.5 (350) bps 14.4 11.8 680 bps

PAT (`m)* 947 1,123 18.7 3,205 4,083 27.4

Source: Company *Adjusted for extra ordinary items

Change in Estimates Target Reco

Estimates revision (%) FY15e FY16e

Revenues (6.1) (7.8)EBITDA 3.5 1.6PAT (2.3) (3.8)

6 May 2014 Emami – Restrained revenues, better margins; Buy

Anand Rathi Research 2

Quick Glance – Financials and ValuationsFig 1 – Income statement (` m) Year-end: Mar FY12 FY13 FY14e FY15e FY16e

Net revenues 13,704 15,954 18,208 21,308 24,945 Revenue growth (%) 14.0 16.4 14.1 17.0 17.1 - Oper. expenses 10,737 12,482 13,795 16,011 18,743 EBIDTA 2,968 3,473 4,413 5,298 6,202 EBITDA margin (%) 21.7 21.8 24.2 24.9 24.9 - Interest expenses 152 66 54 36 36 - Depreciation 188 220 352 371 403 + Other income 541 557 622 764 1,007 - Tax 401 540 547 1,018 1,219 Effective tax rate (%) 12.7 14.4 11.8 18.0 18.0 Reported PAT 2,768 3,204 4,082 4,638 5,552 +/- Extraordinary items (179) (57) (58) - -+/- Minority interest (0) (1) (0) - -Adjusted PAT 2,588 3,147 4,025 4,638 5,552 Adj. FDEPS (`/sh) 12.2 14.1 18.0 20.4 24.5 Adj. FDEPS growth (%) 27.6 15.8 27.4 13.6 19.7 Source: Company, Anand Rathi Research

Fig 3 – Cash-flow statement (` m) Year-end: Mar FY12 FY13 FY14e FY15e FY16e

PAT 2,768 3,205 4,083 4,638 5,552 + Non-cash items 188 220 352 371 403 Cash profit 2,776 3,367 4,376 5,008 5,955 - Incr./(Decr.) in WC 700 138 (21) 126 165 Operating cash-flow 3,957 3,552 4,355 5,134 6,120 - Capex (1,156) (852) (26) (800) (1,000)Free cash-flow 2,801 2,700 4,329 4,334 5,120 - Dividend (615) (1,405) (2,567) (2,125) (2,390)+ Equity raised - - - - -+ Debt raised (683) (411) (511) - -- Investments (699) (776) (1,369) (2,700) (2,700)- Misc. items (174) (59) - - -Net cash-flow 654 58 (118) (491) 30 + Op. cash & bank bal. 2,105 2,759 2,817 2,700 2,209 Cl. cash & bank bal. 2,759 2,817 2,700 2,209 2,239 Source: Company, Anand Rathi Research

Fig 5 – PE band

3x

10x

17x

24x

30x

0

150

300

450

600

750

Jun-

02

Jan-

03

Aug-

03

Mar

-04

Oct

-04

Jun-

05

Jan-

06

Aug-

06

Mar

-07

Oct

-07

May

-08

Dec

-08

Jul-0

9

Mar

-10

Oct

-10

May

-11

Dec

-11

Jul-1

2

Feb-

13

Sep-

13

Apr-1

4

Source: Bloomberg, Anand Rathi Research

Fig 2 – Balance sheet (` m) Year-end: Mar FY12 FY13 FY14e FY15e FY16e

Share capital 151 151 227 227 227 Reserves & surplus 6,915 7,623 9,094 11,607 14,769 Net worth 7,066 7,775 9,321 11,834 14,996 Minority interest 1 1 0 0 0 Total debt 1,673 1,019 508 508 508 Def. tax liab. (net) 145 137 48 48 48 Capital employed 8,885 8,931 9,877 12,390 15,552 Net fixed assets 4,803 4,396 4,071 4,500 5,097 Investments 1,125 2,019 3,387 6,087 8,787 - of which, Liquid 1,125 2,019 3,387 6,087 8,787 Net working capital 197 (301) (280) (406) (571)Cash and bank balance 2,759 2,817 2,700 2,209 2,239 Capital deployed 8,885 8,931 9,877 12,390 15,552 Net debt (2,067) (3,680) (5,531) (7,740) (10,470)WC days 1.4 (1.9) (1.5) (1.9) (2.3)Book value (`/sh) 31.8 34.9 41.3 52.3 66.3 Source: Company, Anand Rathi Research

Fig 4 – Ratio analysis @ `467 Year-end: Mar FY12 FY13 FY14e FY15e FY16e

P/E (x) 38.3 33.1 26.0 22.9 19.1 P/B (x) 14.7 13.4 11.3 8.9 7.0 EV/Sales (x) 7.6 6.5 5.7 4.9 4.2 EV/EBITDA (x) 35.1 30.0 23.6 19.7 16.8 RoAE (%) 36.3 41.6 46.6 43.6 41.2 RoACE (%) 30.5 36.5 43.2 44.3 41.5 Dividend yield (%) 1.1 1.1 1.5 1.7 1.9 Dividend payout (%) 43.7 37.8 38.9 39.2 36.8 RM to sales (%) 45.7 44.8 37.4 36.1 36.1 Ad spend to sales (%) 16.7 17.5 15.2 16.0 16.0 EBITDA growth (%) 17.1 17.0 27.1 20.0 17.1 EPS growth (%) 27.6 15.8 27.4 13.6 19.7 PAT margin (%) 20.2 20.1 22.4 21.8 22.3 FCF/EPS (%) 102.1 84.5 106.1 93.5 92.2 OCF /Sales (%) 28.9 22.3 23.9 24.1 24.5 Source: Company, Anand Rathi Research

Fig 6 – Revenue break-up

Navratna oil25%

Zandu 18%

Boroplus antiseptic cream

14%

Exports13%

Other products12%

Fair & Handsome8%

Mentho plus balm5%

Prickly heat powder

2% Fast Relief2%

Chyawanprash1%

Source: Company

6 May 2014 Emami – Restrained revenues, better margins; Buy

Anand Rathi Research 3

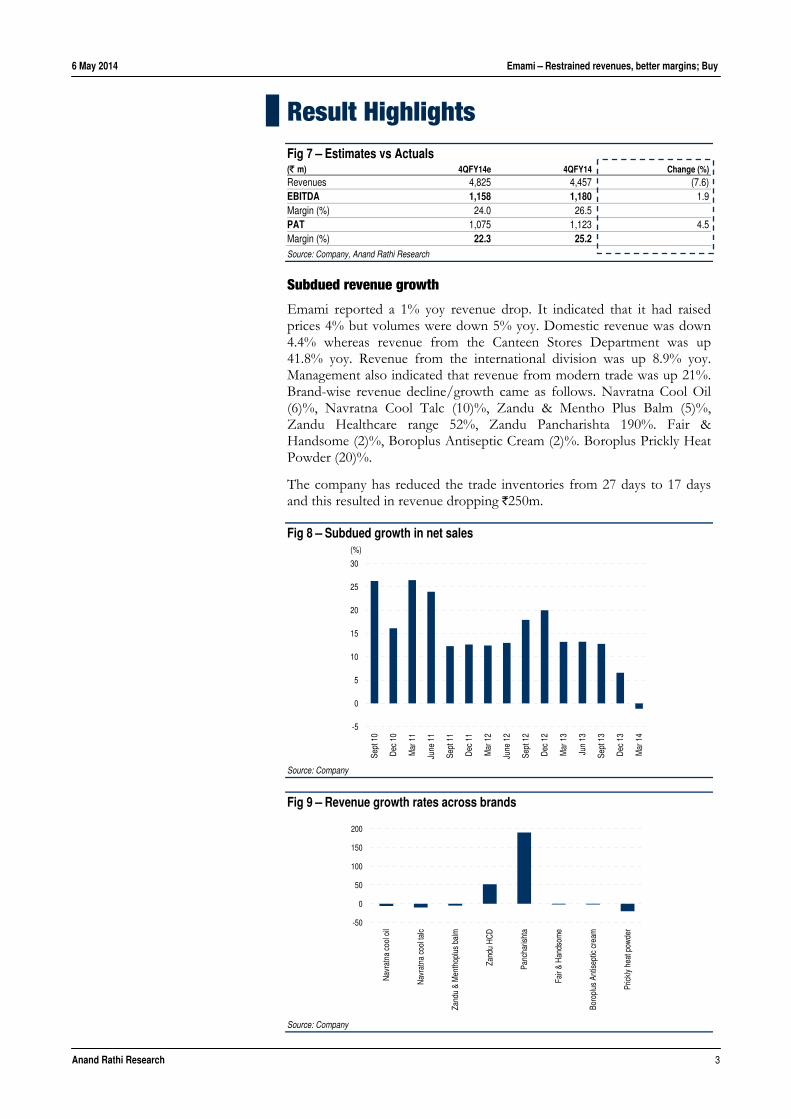

Result Highlights Fig 7 – Estimates vs Actuals (` m) 4QFY14e 4QFY14 Change (%)Revenues 4,825 4,457 (7.6)EBITDA 1,158 1,180 1.9 Margin (%) 24.0 26.5 PAT 1,075 1,123 4.5 Margin (%) 22.3 25.2 Source: Company, Anand Rathi Research

Subdued revenue growth

Emami reported a 1% yoy revenue drop. It indicated that it had raised prices 4% but volumes were down 5% yoy. Domestic revenue was down 4.4% whereas revenue from the Canteen Stores Department was up 41.8% yoy. Revenue from the international division was up 8.9% yoy. Management also indicated that revenue from modern trade was up 21%. Brand-wise revenue decline/growth came as follows. Navratna Cool Oil (6)%, Navratna Cool Talc (10)%, Zandu & Mentho Plus Balm (5)%, Zandu Healthcare range 52%, Zandu Pancharishta 190%. Fair & Handsome (2)%, Boroplus Antiseptic Cream (2)%. Boroplus Prickly Heat Powder (20)%.

The company has reduced the trade inventories from 27 days to 17 days and this resulted in revenue dropping `250m.

Fig 8 – Subdued growth in net sales

-5

0

5

10

15

20

25

30

Sept

10

Dec

10

Mar

11

June

11

Sept

11

Dec

11

Mar

12

June

12

Sept

12

Dec

12

Mar

13

Jun

13

Sept

13

Dec

13

Mar

14

(%)

Source: Company

Fig 9 – Revenue growth rates across brands

-50

0

50

100

150

200

Nav

ratn

a co

ol o

il

Nav

ratn

a co

ol ta

lc

Zand

u &

Men

thop

lus

balm

Zand

u H

CD

Panc

haris

hta

Fair

& H

ands

ome

Boro

plus

Ant

isep

tic c

ream

Pric

kly

heat

pow

der

Source: Company

6 May 2014 Emami – Restrained revenues, better margins; Buy

Anand Rathi Research 4

EBITDA margin improves

The drop in menthol prices has helped the company report a 790-bp yoy gross-margin expansion. Slightly higher staff costs because of the increase in number of employees and in other expenditure led to the 430-bp yoy EBITDA-margin expansion. The adjusted effective income-tax rate was up 350bps yoy. The net profit has expanded 19% yoy.

Fig 10 – Improving EBITDA margin

0

7

14

21

28

35

Sept

10

Dec

10

Mar

11

June

11

Sept

11

Dec

11

Mar

12

June

12

Sept

12

Dec

12

Mar

13

Jun

13

Sept

13

Dec

13

Mar

14

(%)

Source: Company

Fig 11 – Healthy net profit growth

0

10

20

30

40

50

Sept

10

Dec

10

Mar

11

June

11

Sept

11

Dec

11

Mar

12

June

12

Sept

12

Dec

12

Mar

13

Jun

13

Sept

13

Dec

13

Mar

14

(%)

Source: Company

Key takeaways from the conference call

Reduction of inventory in trade (with distributors) from 27 days to 17 days resulted in loss of revenues of `250m. Over the next six months, the company plans to reduce inventory days from 17 to 10.

Management expects 16-17% revenue growth in FY15. It expects its international division to grow 25% and the CSD to grow 10%.

It expects a 4% price hike and has already raised prices of summer products (in Feb’14).

It also indicated a 100-bp EBITDA margin expansion in FY15 due to lower raw material (mentha) prices.

For the next 2-3 years, it would continue at MAT levels, i.e., 20%.

Due to the weaker market sentiment, the company added only 34,000 retail outlets in FY14. It plans to add 100,000 in FY15.

6 May 2014 Emami – Restrained revenues, better margins; Buy

Anand Rathi Research 5

As most of the launches were in the March quarter, ad-spend has not increased in FY14, but management expects it to increase in coming quarters.

The company plans to launch eight products in FY15. These would constitute a mix of new brands and brand extensions.

As the company is already obtaining 27% of its revenue from low-unit packs (LUPs), it does not see any material increase in the proportion of revenue from LUPs ahead.

It indicated capex of `800m in FY15 and `1bn in FY16.

Valuation

We value the stock at a target price of `550, at a target PE of 22x FY16e earnings. Over the past 12 years it has traded at an average PE of 18x. Considering the healthy growth momentum, however, we value it near the mean PE + 1 Standard deviation. On the healthy margin-expansion potential due to the lower menthol prices, the strong revenue-growth momentum from the Canteen Stores Department, rural sales and modern trade, we expect a 17% earnings CAGR over FY14-16. Management has indicated that it would launch around eight products over the next 3-4 quarters and this would help sustain the earnings-growth momentum ahead.

Fig 12 – Mean PE and Standard deviation

Mean

+1SD

+2SD

-1SD

-2SD

0

6

12

18

24

30

Apr-0

2O

ct-0

2M

ay-0

3N

ov-0

3Ju

n-04

Jan-

05Ju

l-05

Feb-

06Au

g-06

Mar

-07

Sep-

07Ap

r-08

Oct

-08

May

-09

Nov

-09

Jun-

10D

ec-1

0Ju

l-11

Feb-

12Au

g-12

Mar

-13

Sep-

13Ap

r-14

Source: Bloomberg, Company, Anand Rathi Research

Risks

Higher raw-material prices

Delay in rollout of new products

Keener-than-expected competitive pressures.

Appendix Analyst Certification The views expressed in this Research Report accurately reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the research analyst(s) was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analyst(s) in this report. The research analysts are bound by stringent internal regulations and also legal and statutory requirements of the Securities and Exchange Board of India (hereinafter “SEBI”) and the analysts’ compensation are completely delinked from all the other companies and/or entities of Anand Rathi, and have no bearing whatsoever on any recommendation that they have given in the Research Report. Important Disclosures on subject companies Rating and Target Price History (as of 5 May 2014)

Emami 14

12 3

4 56

7 89

10

11

1213

50

150

250

350

450

550

Jan-

08Ap

r-08

Jul-0

8O

ct-0

8

Jan-

09Ap

r-09

Jul-0

9O

ct-0

9

Jan-

10Ap

r-10

Jul-1

0

Oct

-10

Jan-

11Ap

r-11

Jul-1

1O

ct-1

1Ja

n-12

Apr-1

2Ju

l-12

Oct

-12

Jan-

13Ap

r-13

Jul-1

3

Oct

-13

Jan-

14Ap

r-14

Date Rating TP (`)

Share Price (`)

1 27-May-08 Buy 133 94 2 2-Sep-09 Buy 157 132 3 3-Nov-09 Buy 200 138 4 2-Feb-10 Buy 221 186 5 1-Jun-10 Buy 283 224 6 9-Jul-10 Buy 336 280 7 27-Jun-11 Buy 369 301 8 8-Nov-11 Buy 335 281 9 8-Oct-12 Buy 425 337

10 9-Nov-12 Buy 456 400 11 9-Apr-13 Buy 464 404 12 7-May-13 Buy 518 446 13 8-Jul-13 Buy 490 484 14 24-Oct-13 Buy 550 478

The research analysts, strategists, or research associates principally responsible for the preparation of Anand Rathi Research have received compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues and overall investment banking revenues.

Anand Rathi Ratings Definitions

Analysts’ ratings and the corresponding expected returns take into account our definitions of Large Caps (>US$1bn) and Mid/Small Caps (<US$1bn) as described in the Ratings Table below:

Ratings Guide Buy Hold Sell Large Caps (>US$1bn) >15% 5-15% <5% Mid/Small Caps (<US$1bn) >25% 5-25% <5%

Anand Rathi Research Ratings Distribution (as of 4 March 2014) Buy Hold Sell Anand Rathi Research stock coverage (182) 64% 27% 9% % who are investment banking clients 4% 0% 0% Other Disclosures This report has been issued by ARSSBL which is a SEBI regulated entity, and which is in full compliance with all rules and regulations as are applicable to its functioning and governance. The investors should note that ARSSBL is one of the companies comprising within ANAND RATHI group, and ANAND RATHI as a group consists of various companies which may include (but is not limited to) its subsidiaries, its affiliates, its group companies who may hold positions, views, stakes and may service the companies covered in this report independent of ARSSBL. Investors are cautioned to be aware that there could arise a potential conflict of interest in the views held by ARSSBL and other companies of Anand Rathi who maybe affiliated, connected or catering to the companies mentioned in the Research Report; even though, ARSSBL and Anand Rathi are fully complaint with all procedural and operational regulatory requirements. Thus, investors should not use this as a sole basis for making their investment decision and should consider the recommendations mentioned in the Research Report bearing in mind the aforementioned.

Further, the information herein has been obtained from various sources which we believe is reliable, and we do not guarantee its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes an offer, or an invitation to make an offer, to buy or sell any securities or any options, futures or other derivatives related to such securities (hereinafter referred to as “Related Investments”). ARSSBL and/or Anand Rathi may trade for their own accounts as market maker / jobber and/or arbitrageur in any securities of the companies mentioned in the Research Report or in related investments, and may be on taking a different position from the ones which haven been taken by the public orders. ARSSBL and/or Anand Rathi and its affiliates, directors, officers, and employees may have a long or short position in any securities of the companies mentioned in the Research Report or in Related Investments. ARSSBL and/or Anand Rathi, may from time to time, perform investment banking, investment management, financial advisory or any other services not explicitly mentioned herein, or solicit investment banking or other business from, any entity and/or company mentioned in this Research Report; however, the same shall have no bearing whatsoever on the specific recommendations made by the analyst(s), as the recommendations made by the analyst(s) are completely independent of the views of the other companies of Anand Rathi, even though there might exist an inherent conflict of interest.

Furthermore, this Research Report is prepared for private circulation and use only. It does not have regard to the specific investment objectives, financial situation and the specific financial needs or objectives of any specific person who may receive this Research Report. Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this Research Report, and, should understand that statements regarding future prospects may or may not be realized, and we can not guarantee the same as analysis and valuation is a tool to enable investors to make investment decisions but, is not an exact and/or a precise science. Investors should note that income from such securities, if any, may fluctuate and that each security's price or value may rise or fall. Past performance is not necessarily a guide to future performance. Foreign currency rates of exchange may adversely affect the value, price or income of any security or related investments mentioned in this report.

Other Disclosures pertaining to distribution of research in the United States of America

This material was produced by ARSSBL, solely for information purposes and for the use of the recipient. It is not to be reproduced under any circumstances and is not to be copied or made available to any person other than the recipient. It is distributed in the United States of America by Enclave Capital LLC (19 West 44th Street, Suite 1700, New York, NY 10036) and elsewhere in the world by ARSSBL or an authorized affiliate of ARSSBL (such entities and any other entity, directly or indirectly, controlled by ARSSBL, the “Affiliates”). This document does not constitute an offer of, or an invitation by or on behalf of ARSSBL or its Affiliates or any other company to any person, to buy or sell any security. The information contained herein has been obtained from published information and other sources, which ARSSBL or its Affiliates consider to be reliable. None of ARSSBL or its Affiliates accepts any liability or responsibility whatsoever for the accuracy or completeness of any such information. All estimates, expressions of opinion and other subjective judgments contained herein are made as of the date of this document. Emerging securities markets may be subject to risks significantly higher than more established markets. In particular, the political and economic environment, company practices and market prices and volumes may be subject to significant variations. The ability to assess such risks may also be limited due to significantly lower information quantity and quality. By accepting this document, you agree to be bound by all the foregoing provisions.

1. ARSSBL or its Affiliates may or may not have been beneficial owners of the securities mentioned in this report.

2. ARSSBL or its affiliates may have or not managed or co-managed a public offering of the securities mentioned in the report in the past 12 months.

3. ARSSBL or its affiliates may have or not received compensation for investment banking services from the issuer of these securities in the past 12 months and do not expect to receive compensation for investment banking services from the issuer of these securities within the next three months.

4. However, one or more of ARSSBL or its Affiliates may, from time to time, have a long or short position in any of the securities mentioned herein and may buy or sell those securities or options thereon, either on their own account or on behalf of their clients.

5. As of the publication of this report, ARSSBL does not make a market in the subject securities.

6. ARSSBL or its Affiliates may or may not, to the extent permitted by law, act upon or use the above material or the conclusions stated above, or the research or analysis on which they are based before the material is published to recipients and from time to time, provide investment banking, investment management or other services for or solicit to seek to obtain investment banking, or other securities business from, any entity referred to in this report.