individual client overview of december’s estate & income tax legislation wealthcounsel...

TRANSCRIPT

Individual Client Overview of December’s Estate & Income Tax Legislation

WealthCounsel Advisors ForumJanuary 13, 2011

Presented by:Robert S. Keebler, CPA, MST, AEP

Keebler & Associates, LLPPhone: (920) 593-1701

E-mail: [email protected]©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

• Small Business Jobs Act of 2010 (“SBJA”) Overview• Tax Relief, Unemployment Insurance Reauthorization, and Job

Creation Act of 2010 (“2010 Tax Relief Act”) Overview– 2010 Income Tax Law Overview– 2010 Estate/Gift/GST Tax Law Overview

• 2010 Modified Carryover Basis Rules• Choosing Between 2010 Estate Tax vs. Modified Carryover

Basis• Tax Planning Opportunities in 2011

2

Course Outline

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

3

Small Business Jobs Act of 2010 (“SBJA”) Overview

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

• Summary of certain key provisions (not all-inclusive) Extension of bonus depreciation Expansion of Section 179 expensing Five-year carryback of certain business credits Reduction in built-in gain (BIG) period for S-corporations 100% gain exclusion on qualified small business stock Conversion of 401(k), 403(b), and 457(b) plans to

designated Roth accounts

Small Business Jobs Act of 2010(September 27, 2010)

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved. 4

Small Business Jobs Act of 2010100% Exclusion on Qualified Small Business Stock

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved. 5

• For qualified small business stock acquired after Sept. 27, 2010, and before Jan. 1, 2011 exclusion for the gain on a sale of qualified small business stock increased from 50% to 100% The “2010 Tax Relief Act” now extends this special

provision until December 31, 2011.

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Small Business Jobs Act of 2010Conversion of Qualified Plans to Roth Accounts

6

• Allows the conversion of 401(k), 403(b), and governmental 457(b) plans to Roth accounts

• Subject to the limits of in-service distributions• No recharacterization provision• Absent an election to the contrary, income will be

recognized equally over a period of 2 years (2011 and 2012) when the conversion occurs in 2010

• Applies to distributions made after September 27, 2010

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Small Business Jobs Act of 2010Conversion of Qualified Plans to Roth Accounts

7

• Under the qualified plan rules, a contributory 401(k) plan is viewed separately from a parallel profit sharing plan. When a 401(k) plan has after-tax basis, this creates a unique advantage for the taxpayer. If a 401(k) plan with a high basis rate is rolled into a Roth 401(k) plan, taxes will only be paid on the earnings, not the basis.

Entire Account Separate Account

$184,000 of TI $120,000 of TI

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Small Business Jobs Act of 2010Conversion of Qualified Plans to Roth Accounts

8

• EXAMPLE: Tom’s 401(k) plan is valued at $200,000, and he had a basis of $80,000. Tom’s profit sharing plan is valued at $809,000; a 100 percent 401(k) to Roth 401(k) conversion will result in $120,000 of taxable income.

• If a pro rata rule applies, like in the class of IRAs, the taxable amount would be $184,000 ((80K/1MM) x 200K)

9

Tax Relief, Unemployment Insurance Reauthorization,

and Job Creation Act of 2010 (“2010 Tax Relief Act”)

Overview

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

2010 Tax Relief Act(December 17, 2010)

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved. 10

• Summary of certain key provisions (not all-inclusive) Income tax provisions

Extension of lower income tax rates until 2012 Extension of 0%/15% long-term capital gains tax rates until 2012 Extension of favorable tax treatment for qualified dividends until 2012 Extension of other income tax credits (e.g., child tax credit)

Estate tax provisions Reinstatement of estate and GST tax Higher exemption amounts Lower tax rates Portability of estate tax exemption

11

2010 Income Tax Law

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

• Lower income / capital gains tax rates– Roth IRA conversion planning– Acceleration of income to 2011 and 2012– Triggering of gains in 2011 and 2012 – Election out of installment treatment

• Extension of capital gains treatment for qualified dividends– “Strip-out” of C-Corp earnings and profits

• Extension of income tax credits– Coordination of tax credits with other education benefits (i.e., 529

plan withdrawals)

12

Prior Estate/Gift Tax Law

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

• 2010– No estate tax– No GST tax– $1,000,000 lifetime gift tax exemption amount with a flat 35% gift tax

rate on taxable gifts over the exemption amount• 2011 & Beyond

– $1,000,000 estate tax exemption amount with a maximum estate tax rate of 55%

– $1,000,000 lifetime gift tax exemption amount with a maximum gift tax rate of 55%

– GST tax reinstated• Special GST rules under EGTRRA no longer apply

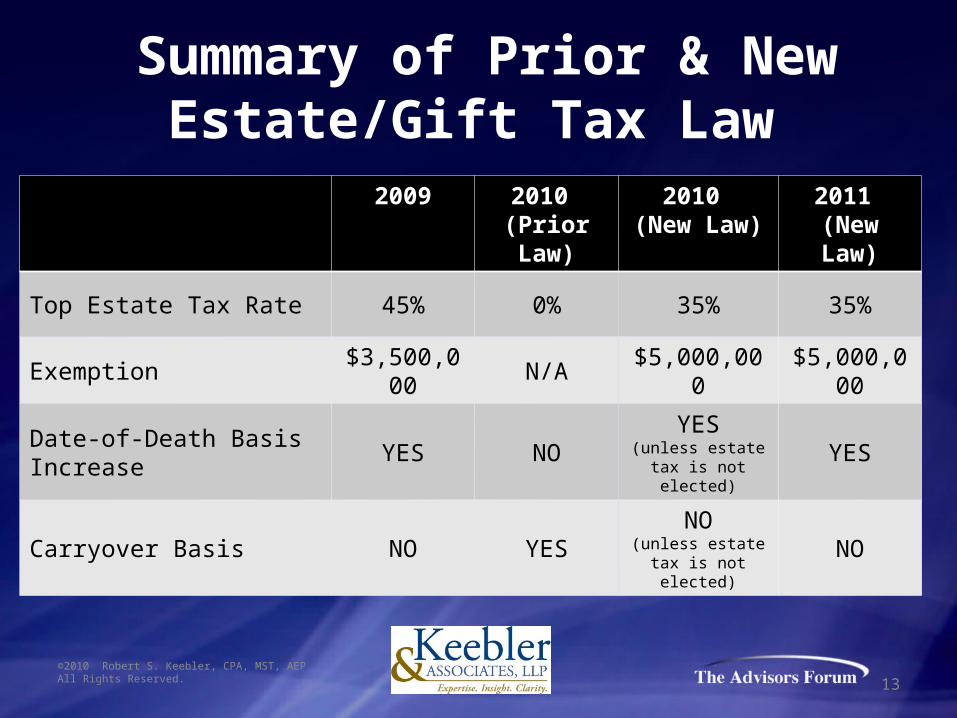

Summary of Prior & New Estate/Gift Tax Law

2009 2010 (Prior Law)

2010 (New Law)

2011 (New Law)

Top Estate Tax Rate 45% 0% 35% 35%

Exemption $3,500,000 N/A $5,000,000 $5,000,000

Date-of-Death Basis Increase YES NOYES

(unless estate tax is not elected)

YES

Carryover Basis NO YESNO

(unless estate tax is not elected)

NO

13©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

• The new estate/gift tax law which passed in Congress allows an estate to elect out of the estate tax for the 2010 tax year– Effective date of law would be made retroactive to 1/1/2010– $5,000,000 estate tax exemption

• Indexed for inflation in 2012– 35% marginal estate tax rate– Election out of the estate tax would result in application of the

modified carryover basis rules

14

New Estate/Gift Tax Law

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

• The general presumption under the new estate/gift law is that the estate tax applies to all estates in 2010– Thus, one will need to affirmatively elect out of the estate

tax• Reunification of the gift and estate tax exemptions

– $5,000,000 gift tax exemption (with a 35% gift tax rate) would apply to gifts after 12/31/2010

– Thus, the gift tax exemption in 2010 would remain $1,000,000 (with a 35% gift tax rate)

15©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

New Estate/Gift Tax Law

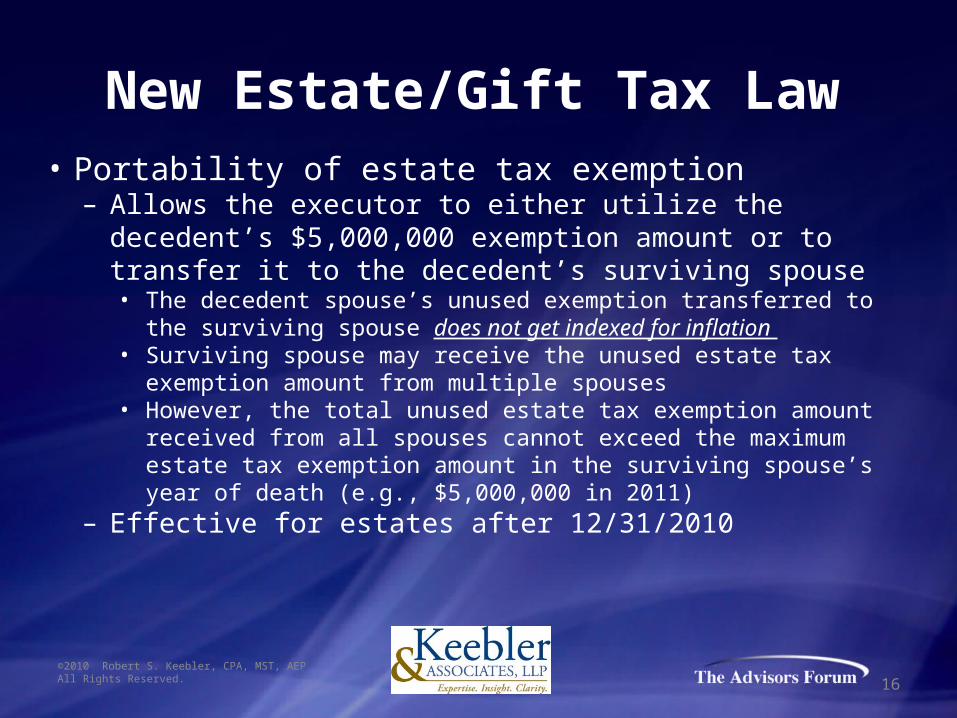

• Portability of estate tax exemption– Allows the executor to either utilize the decedent’s $5,000,000

exemption amount or to transfer it to the decedent’s surviving spouse• The decedent spouse’s unused exemption transferred to the surviving

spouse does not get indexed for inflation • Surviving spouse may receive the unused estate tax exemption amount

from multiple spouses• However, the total unused estate tax exemption amount received from

all spouses cannot exceed the maximum estate tax exemption amount in the surviving spouse’s year of death (e.g., $5,000,000 in 2011)

– Effective for estates after 12/31/2010

16©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

New Estate/Gift Tax Law

• Portability issues– Election to transfer the unused estate tax exemption amount

must be made on a timely-filed estate tax return• No election can be made on a late-filed return

– Statute of limitations remains open for the decedent spouse’s estate tax return until the statute of limitations has run on the surviving spouse’s estate tax return• The “adequate disclosure” rules (applying to post-1997 gifts) does not

apply• Thus, the IRS can audit the deceased spouse’s estate tax return (even

after the normal statute of limitations has run) and add any increase in tax to the surviving spouse’s estate tax return

17©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

New Estate/Gift Tax Law

• Portability issues– Utilizing the estate tax exemption at first spouse’s death vs.

transferring the exemption to the surviving spouse• Size of combined estate• Anticipated growth of the surviving spouse’s estate• Changes in the future estate tax law• Asset protection issues• Additional basis step-up of property in surviving spouse’s taxable

estate

18©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

New Estate/Gift Tax Law

• Portability issues – Example #1– John and Jane have a combined estate of $5,000,000. Assume that John

dies first and that, at Jane’s death, the value of the total estate is worth $6,000,000.

19©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

New Estate/Gift Tax Law

John Jane TOTAL John Jane TOTALFMV of Gross Estate 3,000,000$ 2,000,000$ 5,000,000$ 3,000,000$ 2,000,000$ 5,000,000$ Marital Deduction (3,000,000) 3,000,000 - - - - Subtotal -$ 5,000,000$ 5,000,000$ 3,000,000$ 2,000,000$ 5,000,000$ Appreciation in Gross Estate at Second Death - 1,000,000 1,000,000 - 400,000 400,000 Subtotal -$ 6,000,000$ 6,000,000$ 3,000,000$ 2,400,000$ 5,400,000$ Less: Estate Tax Exemption - (10,000,000) (10,000,000) (3,000,000) (7,000,000) (10,000,000) Net Taxable Estate -$ -$ -$ -$ -$ -$

FMV of Property at Second Death -$ 6,000,000$ 6,000,000$ 3,600,000$ 2,400,000$ 6,000,000$ Less: Cost Basis - (6,000,000) (6,000,000) (3,000,000) (2,400,000) (5,400,000) Net Capital Gain -$ -$ -$ 600,000$ -$ 600,000$

Estate Tax @ 35% -$ -$ -$ -$ -$ -$ Capital Gains Tax @ 15% - - - 90,000 - 90,000 Total Taxes -$ -$ -$ 90,000$ -$ 90,000$

OPTION 2 - Utilize Full Exemption at First Death

OPTION 1 - 100% Marital Deduction

• Portability issues – Example #2– Mike and Mary have a combined estate of $10,000,000. Assume that

Mike dies first and that, at Mary’s death, the value of the total estate is worth $12,000,000.

20©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

New Estate/Gift Tax Law

John Jane TOTAL John Jane TOTALFMV of Gross Estate 5,000,000$ 5,000,000$ 10,000,000$ 5,000,000$ 5,000,000$ 10,000,000$ Marital Deduction (5,000,000) 5,000,000 - - - - Subtotal -$ 10,000,000$ 10,000,000$ 5,000,000$ 5,000,000$ 10,000,000$ Appreciation in Gross Estate at Second Death - 2,000,000 2,000,000 - 1,000,000 1,000,000 Subtotal -$ 12,000,000$ 12,000,000$ 5,000,000$ 6,000,000$ 11,000,000$ Less: Estate Tax Exemption - (10,000,000) (10,000,000) (5,000,000) (5,000,000) (10,000,000) Net Taxable Estate -$ 2,000,000$ 2,000,000$ -$ 1,000,000$ 1,000,000$

FMV of Property at Second Death -$ 12,000,000$ 12,000,000$ 6,000,000$ 6,000,000$ 12,000,000$ Less: Cost Basis - (12,000,000) (12,000,000) (5,000,000) (6,000,000) (11,000,000) Net Capital Gain -$ -$ -$ 1,000,000$ -$ 1,000,000$

Estate Tax @ 35% -$ 700,000$ 700,000$ -$ 350,000$ 350,000$ Capital Gains Tax @ 15% - - - 150,000 - 150,000 Total Taxes -$ 700,000$ 700,000$ 150,000$ 350,000$ 500,000$

OPTION 1 - 100% Marital Deduction OPTION 2 - Utilize Full Exemption at First Death

New Generation-Skipping Transfer (GST) Tax Law

21

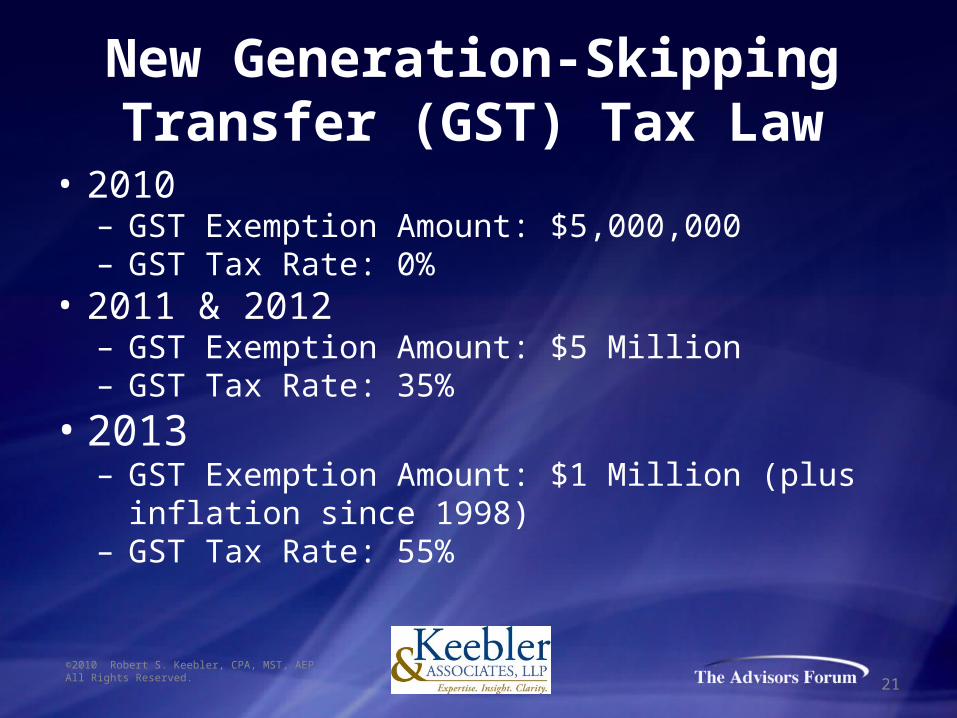

• 2010– GST Exemption Amount: $5,000,000– GST Tax Rate: 0%

• 2011 & 2012– GST Exemption Amount: $5 Million– GST Tax Rate: 35%

• 2013– GST Exemption Amount: $1 Million (plus inflation since 1998)– GST Tax Rate: 55%

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Unlike a surviving spouse’s ability to utilize a predeceased spouse’s unused unified credit, the new law does not allow a surviving spouse to use the unused GST tax exemption of a predeceased spouse.

New Generation-Skipping Transfer (GST) Tax Law

22©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

23

2010 Modified Carryover Basis Rules

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

24

In general, the basis of property in the hands of a person acquiring the property from a decedent or to whom the property passed from a decedent shall be the fair market value of the property as of the date of the decedent's death.

– However, if the “alternative valuation date” (generally six months after the decedent’s death) is used to value the property for estate tax purposes, then the basis of the property shall be the fair market value of the property as of the alternative valuation date.

Section 1014 – Basis of Property Acquired from a Decedent

(For Deaths Occurring Before or After 2010)

CAVEAT: The above basis rule does not apply to property considered to be “income in respect to a decedent” (“IRD”) as defined under Section 691(a).

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

25

Section 1223 - Holding Period of Property

(For Deaths Occurring Before or After 2010)

In the case of a person acquiring property from a decedent OR to whom property passed from a decedent, if: (a) the basis of such property in the hands of such person is determined under Section 1014, and (b) such property is sold or otherwise disposed of by such person within one year after the decedent's death, then such person shall be considered to have held such property for more than one year (i.e., long-term capital gain).

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

26

In general, the basis of property in the hands of a person acquiring the property from a decedent or to whom the property passed from a decedent shall be the lesser of: (1) the adjusted basis of the decedent or (2) the fair market value of the property as of the date of the decedent's death.

Section 1022(a) – Basis of Property Acquired from a Decedent(For Deaths Occurring During 2010)

CAVEAT: The above basis rule does not apply to property considered to be “income in respect to a decedent” (“IRD”) as defined under Section 691(a).

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

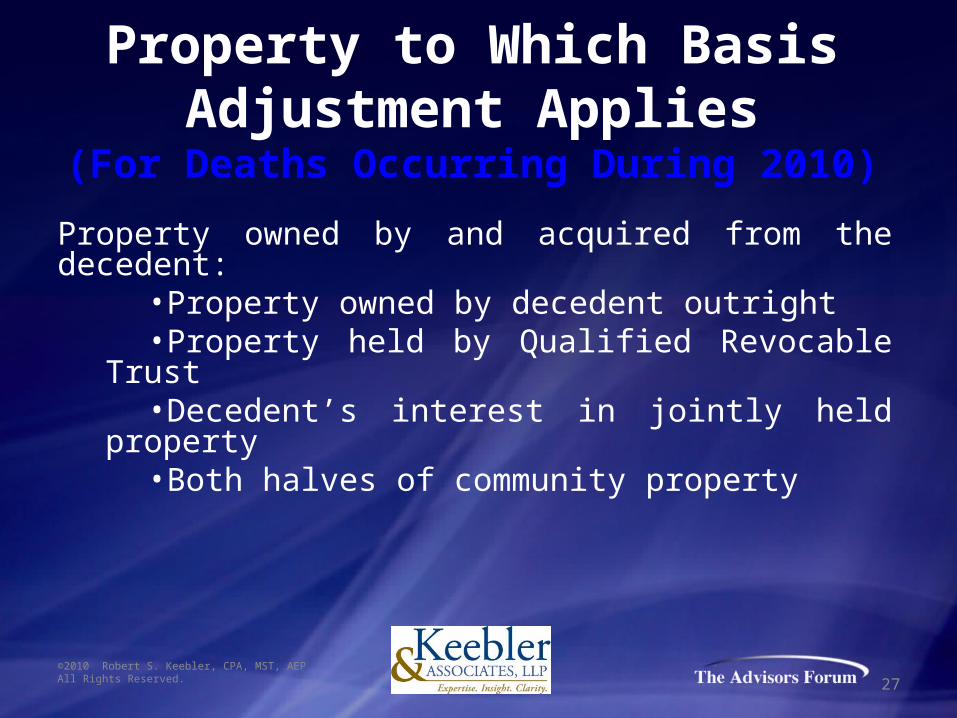

Property to Which Basis Adjustment Applies

(For Deaths Occurring During 2010)

Property owned by and acquired from the decedent:•Property owned by decedent outright•Property held by Qualified Revocable Trust•Decedent’s interest in jointly held property•Both halves of community property

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved. 27

28

In the case of a non-spouse beneficiary, there is an “aggregate basis increase” of up to $1,300,000.

– The “aggregate basis increase” of $1,300,000 is also increased by the following items that decedent had at the time of death:

• Capital loss carryovers (§ 1212(b))• Net operating loss (NOL) carryovers (§ 172)•Any losses that would have been allowed under § 165 if the property had been sold at fair market value immediately before the decedent’s death

– The executor may allocate the “aggregate basis increase” to any particular property

– The basis step-up for a particular asset cannot exceed its fair market value

Section 1022(b) – Aggregate Basis Step-Up

(Non-Spousal Beneficiaries)(For Deaths Occurring During 2010)

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

29

In the case of a spouse beneficiary, there is an “aggregate spousal property basis increase” of up to $3,000,000.

– The $3,000,000 basis step-up is in addition to the $1,300,000 general basis step-up (including any basis step-up for any capital loss carryovers, NOL carryovers and/or current year Section 165 losses the decedent had at the time of death)

– The executor may allocate the “aggregate basis increase” to qualified spousal property, defined as:

•Outright transfer property•Qualified Terminable Interest Property (QTIP)

– The basis step-up for a particular asset cannot exceed its fair market value

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Section 1022(c) – Aggregate Basis Step-Up (Spousal Beneficiaries)

(For Deaths Occurring During 2010)

30

The basis step-up provisions of Sections 1022(b) and 1022(c) do not apply to the following:

– Property which is considered “income in respect to a decedent” (“IRD”)

– Property which the decedent received by gift within three years of the decedent’s death

– Stock in any of the following entities:• Foreign personal holding companies• DISCs (or former DISCs)• Foreign investment companies• Passive foreign investment companies (unless such company is a

“qualified electing fund”)

Section 1022(d) – Basis Step-Up Exceptions

(For Deaths Occurring During 2010)

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

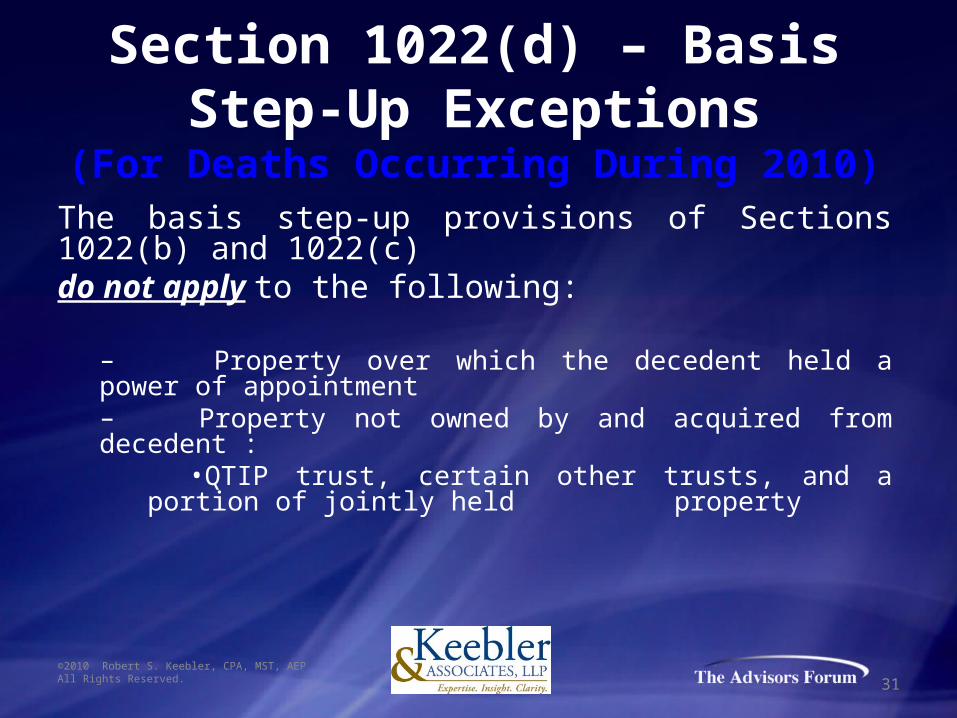

Section 1022(d) – Basis Step-Up Exceptions

(For Deaths Occurring During 2010)The basis step-up provisions of Sections 1022(b) and 1022(c) do not apply to the following:

– Property over which the decedent held a power of appointment– Property not owned by and acquired from decedent :

•QTIP trust, certain other trusts, and a portion of jointly held property

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved. 31

Income in Respect of a Decedent (IRD)

32

Income in respect of a decedent (IRD) – is all items of gross income in respect of a decedent which were not properly included as taxable income in a tax period falling on or before a taxpayer’s death and are payable to his/her estate and/or another beneficiary

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

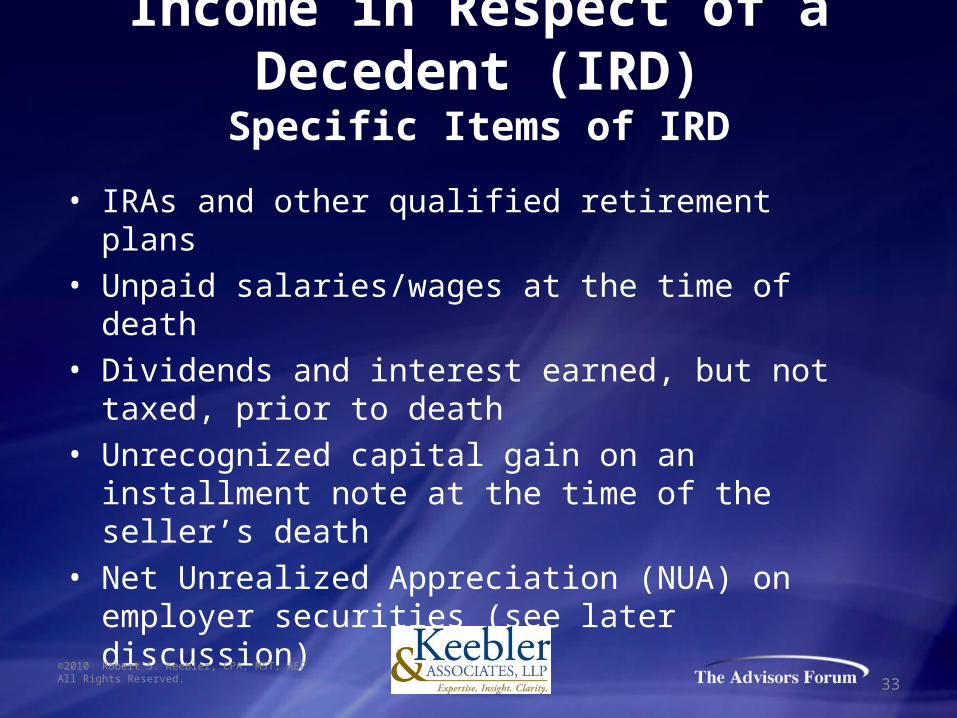

Income in Respect of a Decedent (IRD)Specific Items of IRD

• IRAs and other qualified retirement plans• Unpaid salaries/wages at the time of death• Dividends and interest earned, but not taxed, prior to

death• Unrecognized capital gain on an installment note at the

time of the seller’s death• Net Unrealized Appreciation (NUA) on employer securities

(see later discussion)

33©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

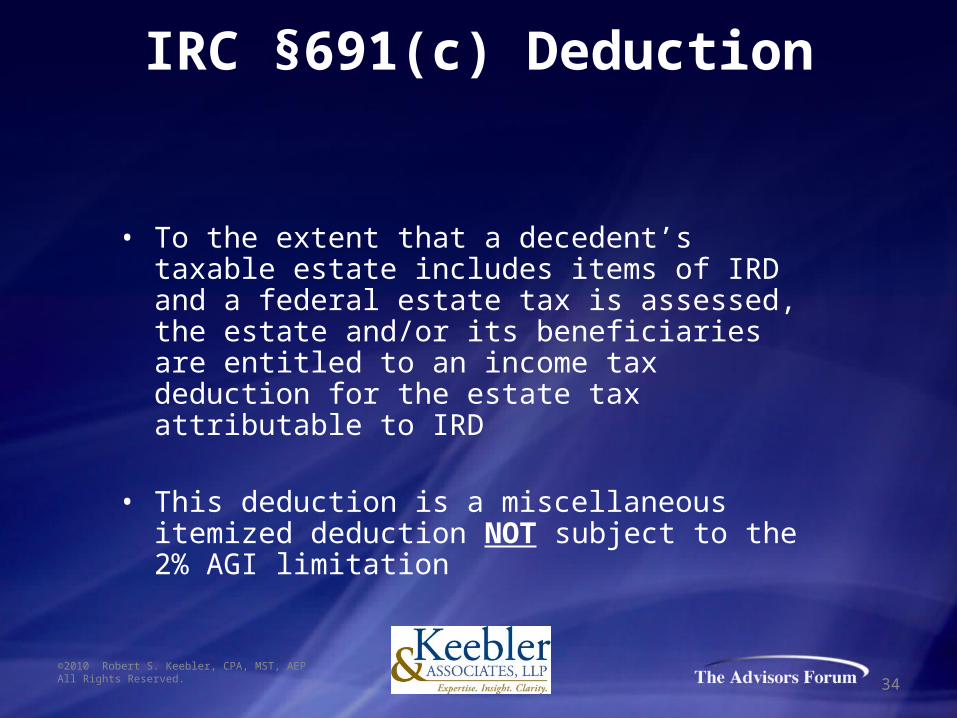

• To the extent that a decedent’s taxable estate includes items of IRD and a federal estate tax is assessed, the estate and/or its beneficiaries are entitled to an income tax deduction for the estate tax attributable to IRD

• This deduction is a miscellaneous itemized deduction NOT subject to the 2% AGI limitation

IRC §691(c) Deduction

34©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

• The income tax deduction computation for estate taxes paid on IRD is determined on a “with and without” basis

• In essence, the total deduction allowed is the difference between: (a) the estate tax liability with all items of IRD included in the taxable estate and (b) the estate tax liability without the IRD included in the taxable estate

IRC §691(c) Deduction

35©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

• Executor’s filing requirement– Carryover basis property in excess of $1.3 million

• Property acquired by decedent within three years of death not treated as carryover basis property and not reported on a 709

• Required information (i.e., recipient, property description, adjusted basis in hands of decedent, whether any gain on sale would be treated as ordinary income, decedent’s holding period, allocation of basis increase)

• $10,000 penalty for failure to file on time

– Executor also required to furnish information to persons named in the return

36

Reporting Requirements Under Section 6018

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

37

Choosing Between 2010 Estate Tax vs. Modified

Carryover Basis

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

38©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Summary of Prior & New Estate/Gift Tax Law

2009 2010 (Prior Law)

2010 (New Law)

2011 (New Law)

Top Estate Tax Rate 45% 0% 35% 35%

Exemption $3,500,000 N/A $5,000,000 $5,000,000

Date-of-Death Basis Increase YES NOYES

(unless estate tax is not elected)

YES

Carryover Basis NO YESNO

(unless estate tax is not elected)

NO

Gross estate ≤ $5,000,000($10,000,000 for married couples)

Elect into estate tax

Gross estate between $5,000,000 and $30,000,000($10,000,000 and $30,000,000 for married couples)

Need to analyze

Gross estate > $30,000,000 Elect out of estate tax

Comparison of Estate Tax Options in 2010

CAVEAT: The above table discusses the estate tax decision in a general context. Depending on the specific attributes of the estate, more analysis may need to be done to determine whether or not the estate tax should be elected.

39©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

• Perhaps the single most important issue in determining whether or not to elect into the estate tax will be the total tax incurred under each scenario

– Need to compare estate tax rate vs. future ordinary income/capital gains tax rates

– If estate tax elected out of, then the future ordinary income/capital gains tax to be incurred will need to be reduced to its present value

• In most cases, the decision to elect into the estate tax can be made according to the following simple algebraic formula

– Current estate tax liability = Present value of future income tax liability

40

Electing Into or Out of the Estate Tax

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

• In more complex estates (i.e., ones with multiple tax bases, tax characteristics, and/or IRD), a thorough quantitative analysis will need to be performed

• In this situation, the decision to elect into the estate tax will usually be reached according to the following algebraic formula:

41

Electing Into or Out of the Estate Tax

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

FactorsX = Gross estateXb = Cost basis of gross estateY = Estate tax exemptionZ = Modified carryover basis increaseRy = Estate tax rateRz = Income tax/capital gains tax rate

Formula(X – Y) x Ry = ([X – Xb] – Z) x Rz

John dies in 2010 with a $5,000,000 gross estate. John’s gross estate consists of a variety of assets with an aggregate cost basis of $2,800,000. Given these facts, John’s estate would elect into the estate tax because the estate will likely not have an estate tax and likely will get a full cost basis step-up to the date-of-death value.

OPTION 1 (Elect Into Estate Tax): Total tax liability = $0OPTION 2 (Elect Out Of Estate Tax): Total tax liability = $330,000

* Assumes all assets are capital assets (with no depreciation recapture) and contain no IRD. Further it is assumed that the future capital gain tax rate is 15%.

Electing Into or Out of the Estate TaxSimple Example #1*

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved. 42

43

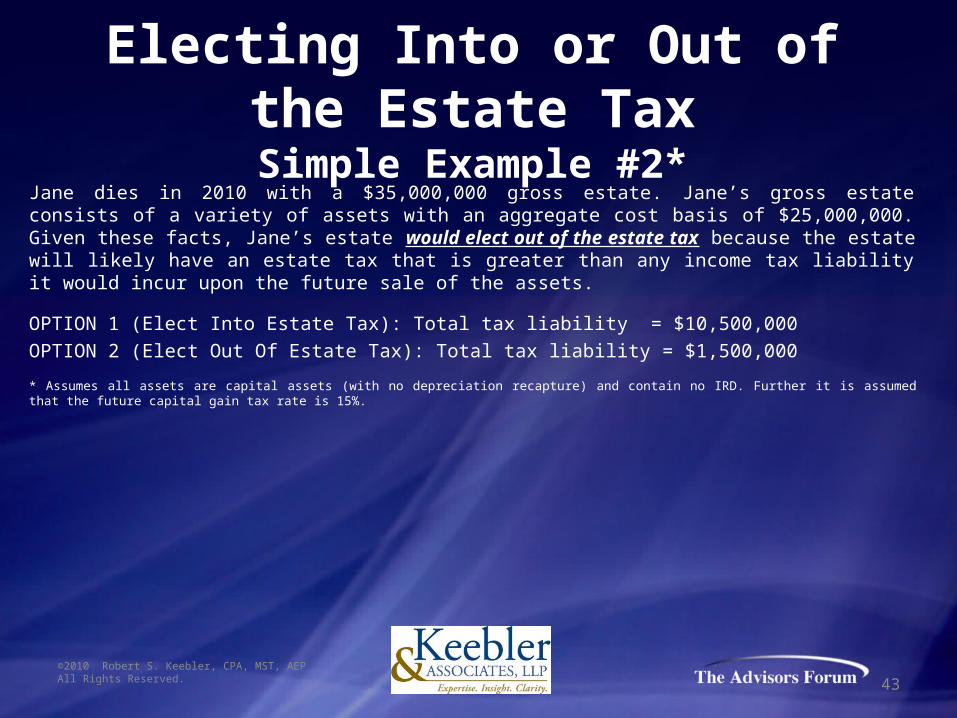

Electing Into or Out of the Estate TaxSimple Example #2*

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Jane dies in 2010 with a $35,000,000 gross estate. Jane’s gross estate consists of a variety of assets with an aggregate cost basis of $25,000,000. Given these facts, Jane’s estate would elect out of the estate tax because the estate will likely have an estate tax that is greater than any income tax liability it would incur upon the future sale of the assets.

OPTION 1 (Elect Into Estate Tax): Total tax liability = $10,500,000OPTION 2 (Elect Out Of Estate Tax): Total tax liability = $1,500,000

* Assumes all assets are capital assets (with no depreciation recapture) and contain no IRD. Further it is assumed that the future capital gain tax rate is 15%.

• Future depreciation “tax shield”– Need to present value future benefit of income tax deductions

• Depreciation recapture– IRC §1245 recapture – ordinary income tax rates– IRC §1250 recapture – 25% tax rate

• IRC §754 election impact– Impact of potential IRC §743(b) step-down

• State/local income taxes

44

Other Considerations

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

45

Electing Into or Out of the Estate TaxComprehensive Example

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

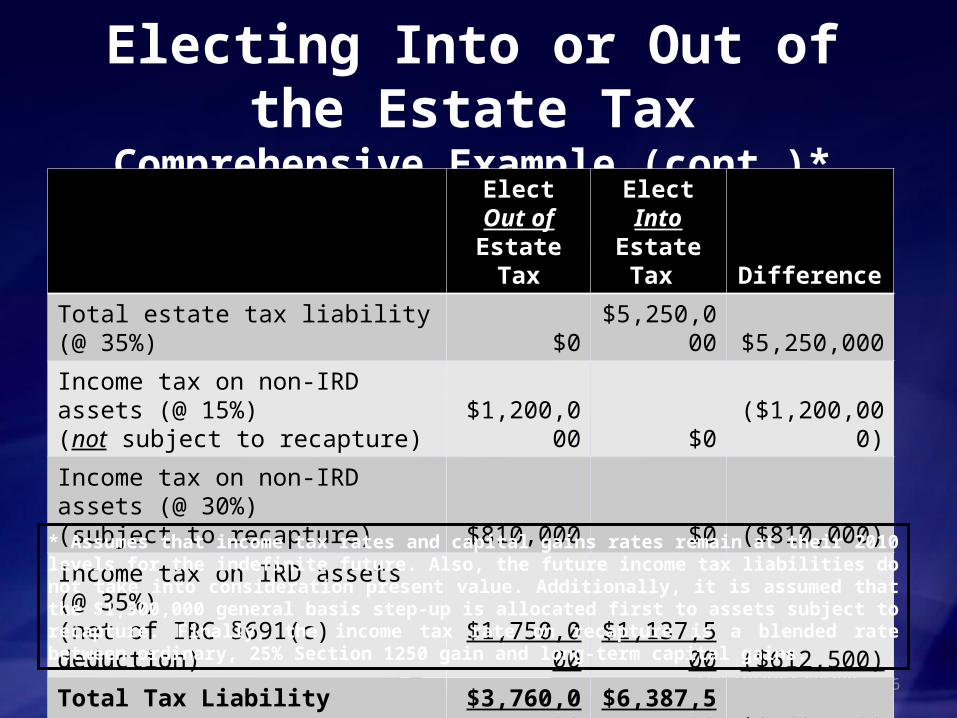

Martha dies in 2010 with a $20,000,000 gross estate. Martha’s gross estate consists of the following assets:

DOD FMV Cost Basis Built-In Gain

Non-IRD assets (not subject to recapture) $10,000,000 $2,000,000 $8,000,000

Non-IRD assets (subject to recapture) $5,000,000 $1,000,000 $4,000,000

IRD assets $5,000,000 $0 $5,000,000

Gross Estate $20,000,000 $3,000,000 $17,000,000

46

Electing Into or Out of the Estate TaxComprehensive Example (cont.)*

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Elect Out of Estate Tax

Elect Into Estate Tax Difference

Total estate tax liability (@ 35%) $0 $5,250,000 $5,250,000

Income tax on non-IRD assets (@ 15%)(not subject to recapture) $1,200,000 $0 ($1,200,000)

Income tax on non-IRD assets (@ 30%)(subject to recapture) $810,000 $0 ($810,000)

Income tax on IRD assets (@ 35%)(net of IRC §691(c) deduction) $1,750,000 $1,137,500 ($612,500)

Total Tax Liability $3,760,000 $6,387,500 $2,627,500

* Assumes that income tax rates and capital gains rates remain at their 2010 levels for the indefinite future. Also, the future income tax liabilities do not take into consideration present value. Additionally, it is assumed that the $1,300,000 general basis step-up is allocated first to assets subject to recapture. Finally, the income tax rate on recapture is a blended rate between ordinary, 25% Section 1250 gain and long-term capital gains.

• Spousal bequests• Charitable bequests• Bequests subject to GST tax

47

Impact on Formula Clauses

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

48

Tax Planning Opportunities in 2011

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

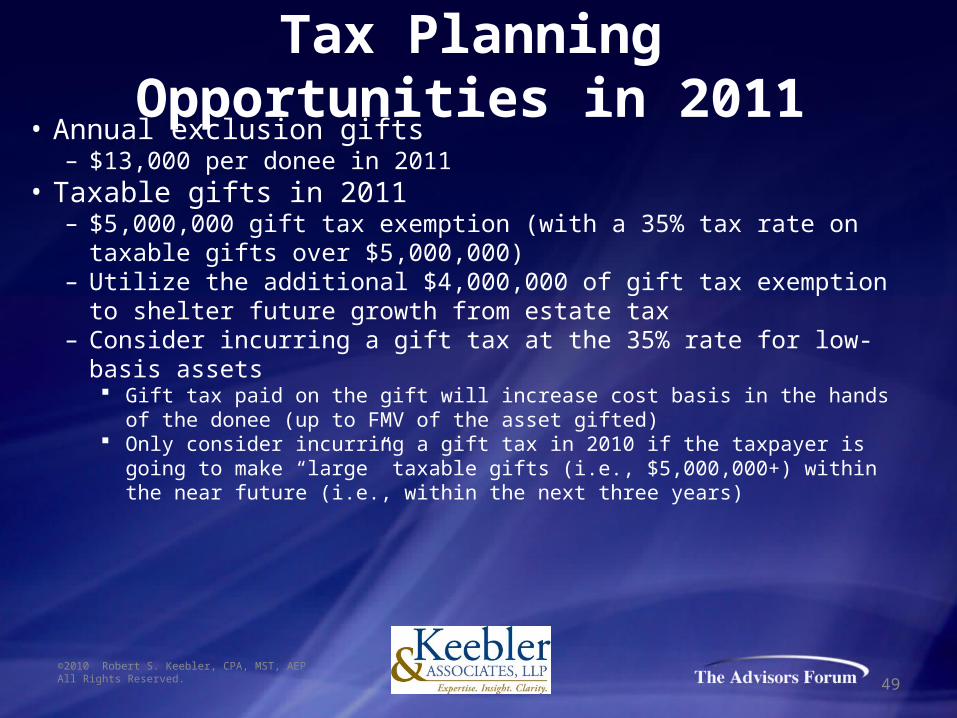

• Annual exclusion gifts– $13,000 per donee in 2011

• Taxable gifts in 2011– $5,000,000 gift tax exemption (with a 35% tax rate on taxable gifts over

$5,000,000)– Utilize the additional $4,000,000 of gift tax exemption to shelter future

growth from estate tax– Consider incurring a gift tax at the 35% rate for low-basis assets

Gift tax paid on the gift will increase cost basis in the hands of the donee (up to FMV of the asset gifted)

Only consider incurring a gift tax in 2010 if the taxpayer is going to make “large” taxable gifts (i.e., $5,000,000+) within the near future (i.e., within the next three years)

49

Tax Planning Opportunities in 2011

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

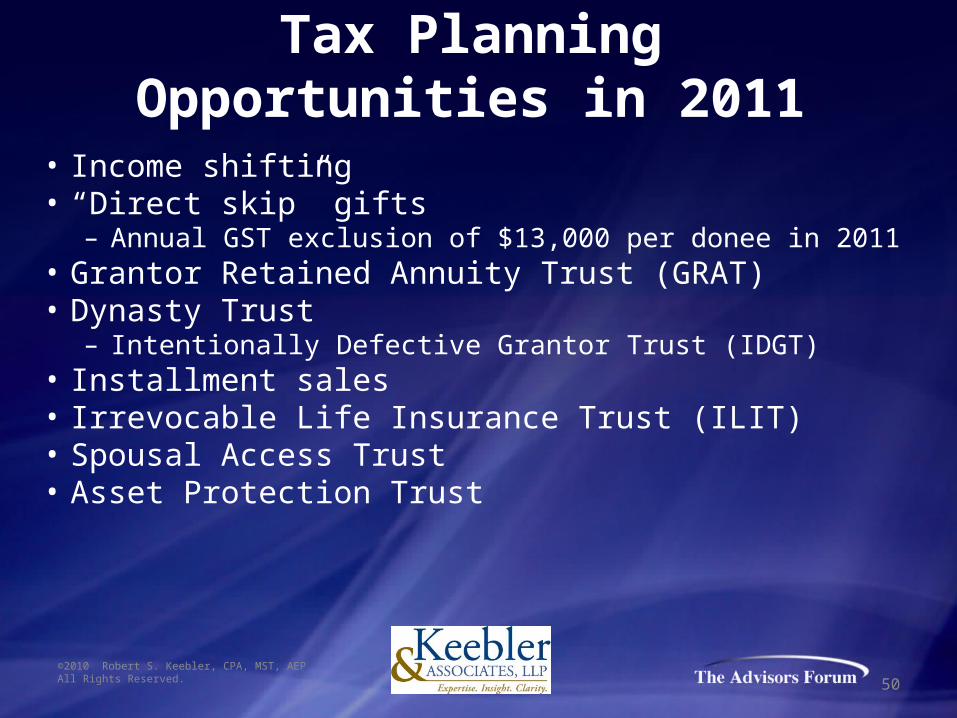

• Income shifting• “Direct skip” gifts

– Annual GST exclusion of $13,000 per donee in 2011• Grantor Retained Annuity Trust (GRAT)• Dynasty Trust

– Intentionally Defective Grantor Trust (IDGT)• Installment sales• Irrevocable Life Insurance Trust (ILIT)• Spousal Access Trust• Asset Protection Trust

50

Tax Planning Opportunities in 2011

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Concept Shift income to younger family members to reduce income taxes

Considerations•Asset protection•Kiddie tax•Potential $10,000,000 gift•Children use income to invest or purchase insurance

51©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Income Shifting

• Estate tax-free• Income tax-free• Utilize the $5,000,000 gift and GST exemption amounts

Strategic Issues• Dynasty trusts• Alternative asset classes

Funding strategies• Gifts• Loans• Split-dollar arrangement

52©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Irrevocable Life Insurance Trust (ILIT)

ConceptOne spouse transfers up to $5,000,000, in trust, to their spouse

Benefits•Asset protection•Estate tax•Direct decedent protection•Income shifting

53©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.

Spousal Access Trust

Circular 230 Disclosure

Pursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of the Treasury, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax advice in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party.

For discussion purposes only. This work is intended to provide general information about the tax and other laws applicable to retirement benefits. The author, his firm or anyone forwarding or reproducing this work shall have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to be caused, directly or indirectly by the information contained in this work. This work does not represent tax, accounting, or legal advice. The individual taxpayer is advised to and should rely on their own advisors.

©2010 Robert S. Keebler, CPA, MST, AEPAll Rights Reserved.