indonesia - home · financial inclusion insights by …finclusion.org/uploads/file/reports/2016 data...

TRANSCRIPT

INDONESIA

December 2016

QUICKSIGHTS REPORT

FII TRACKER SURVEY WAVE 3Fieldwork Conducted September through November 2016

INDONESIA

Access – Access to a bank account or mobile money account means an

individual can use bank/mobile money services either via their own

account or via an account of another person.

Active account holder – An individual who has a registered account and

has used it in the last 90 days.

Active user – An individual who has used any financial services account

for any type of transaction in the past 90 days via his/her own account or

somebody else’s account.

Adults with DFS access – Adults (15+) who either own a DFS account

or have access to someone else’s account.

Advanced use of DFS – Advanced use of DFS includes activities beyond

basic cash-in/cash-out and person-to-person transfers (e.g., savings, bill

pay, investment, insurance, etc.).

Arisan – Informal, rotating credit savings group.

Bank Perkreditan Rakyat (BPR) – Rural credit bank.

Below the poverty line – In this particular study, adults living on less than

$2.50 per day, as classified by the Grameen PPI.

Cooperative – Typically, a business or other professional organization that

is owned and run jointly by its members, who share the profits or benefits.

Cooperatives can release some of the profits/funds as loans to its

members.

Digital financial services (DFS) – Financial services provided through

an electronic platform (mobile phones, electronic cards, the internet, etc.).

Dormant accounts –Registered accounts that have never been used or

that have not been active (e.g., used in the past 90 days).

Financially included –Included individuals are those who have an

account with an institution that provides a full suite of financial services

and comes under some form of government regulation. Services include

savings, money transfers, insurance or investment. Institutions that only

offer loans to consumers, such as some MFIs, are not considered to be

full-service institutions.

Full-service nonbank financial institutions – Financial institutions that

offer their customers at least one of the following services: savings, money

transfers, insurance, or investment.

Grameen Progress out of Poverty Index (PPI) – A poverty

measurement tool from the Grameen Foundation wherein a set of

country-specific questions are used to compute the likelihood that a

household is living below the poverty line.

Microfinance institution (MFI) – An organization that offers financial

services to low-income populations. Almost all give loans to their

members, and many offer insurance, deposit and other services.

Mobile money (MM) – A service in which a mobile phone is used to

access financial services.

Nonbank financial institution (NBFI) – A financial organization that is

not formally licensed as a bank or a mobile money provider, but whose

activities are regulated, at least to some extent, by the central bank within

the country. Such financial institutions include rural credit banks,

cooperatives, Post Office Banks, and savings and credit cooperatives.

Non-full-service financial institution – Institution that offers a limited

range of financial products or services, often in an informal setting. These

institutions are not included in the financial rate calculation and include

arisans, money lenders, money guards and other savings groups.

Registered active user – Individual who holds a registered financial

services account and has used it in the last 90 days.

Services beyond basic wallet – DFS transactions that go beyond simple

deposits, withdrawals or money transfers.

Unregistered/over-the-counter (OTC) user – An individual who has

used a financial service through someone else’s account, including an

agent’s account or the account of a family member or a neighbor.

Urban/rural – Urban and rural persons are defined according to their

residence in urban or rural areas as prescribed by the national bureau of

statistics.

Key definitions

2

INDONESIA

Country context

• In November 2016, the Indonesian government announced the creation of a National Strategy for Financial Inclusion (SNKI) to expand bank

account ownership to 75 percent of the adult population by 2019, among other goals.* While Indonesia is a bank-led financial services market,

this goal is nonetheless very ambitious, given that less than 25 percent of adult Indonesians currently hold a bank account.

– Achieving the SNKI objective is complicated by the concentration of bank account ownership in specific demographic groups – men, residents

of urban areas, and households with incomes above the poverty line. Bank account ownership is rising among underserved groups – women,

residents of rural areas, and those below the poverty line – at a rate that outpaces their counterparts; however, the gap remains significant.

– Unbanked or otherwise underserved individuals use financial products and services, including digital ones, but these offerings tend to be

informal and/or not full-service in nature. For example, 20 percent of Indonesian adults who do not hold a formal, full-service financial

account instead use arisans, or other types of informal rotating savings groups. Successful implementation of the SNKI, therefore, requires

competing with a widespread set of non-full-service institutions that are already catering to the needs of the unbanked.

• In August 2016, the Indonesian Financial Services Authority (OJK) announced that more progressive financial technology (fintech)

regulations were under development.

– Current regulations are structured such that fintech does not fall under a single regulatory authority. This structure inhibits growth in the

fintech sector, as a commercial entity dealing in fintech has to be compliant with multiple and occasionally competing or contradictory sets of

regulations.

– These new regulations will consolidate regulatory authority while also creating a regulatory environment that actively encourages fintech

expansion. For example, the new regulations will establish a “regulatory sandbox,” or the ability for companies to test new products without

establishing full compliance with existing regulations. This change would lower barriers to market entry and provide regulators with an

opportunity to adapt regulations to new technologies and consumption patterns.**

• Over 25 percent of Indonesians have used digital financial services (DFS) and products (full and non-full service), including 6 percent of the

financially excluded population. OJK has signaled support for expanding use of DFS by promoting fintech through various means including:

– Hosting the first Indonesia Fintech Festival and Conference in August 2016. The event featured talks by both established institutions (e.g.,

Bank Indonesia) and start-up corporations (e.g., Go-Jek) on how to apply fintech to businesses, as well as by Indonesian and international

government representatives, including Queen Maxima of the Netherlands.

– Launching a Fintech Innovation Hub, a “one-stop contact center” where fintech companies can network and collaborate.**

* Parlina, I. (2016, November 18). Indonesia promotes financial inclusion with new strategy. Retrieved from

http://www.thejakartapost.com/news/2016/11/18/indonesia-promotes-financial-inclusion-with-new-strategy.html.

**OJK. (2016, October 6). Press Release: OJK Drafts Regulations on Fintech Development3

INDONESIA

26%have

financial

accounts

3% have a

nonbank financial

institution account

24% have a

bank account

0.7% have a

registered mobile

money account

2016: Registered full-service financial

account holders*(Shown: Percentage of Indonesian adults,

N=6,044)

.

Notable statistics

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.

*Overlap representing those who have multiple kinds of financial accounts is not shown.

4

• Banks remain the driver of Indonesian financial inclusion; 93 percent of Indonesian adults who

are financially included hold a full-service bank account.

– Thirty percent of Indonesian adults have ever used a full-service bank account (either their

own or one belonging to someone else).

– Of those Indonesians who have accessed a full-service bank account, 81 percent (24 percent

of all adults) hold an account.

– Indonesian bank account holders tend to be active users. Ninety-four percent of all

Indonesian full-service bank account holders had used their accounts in the 90 days preceding

the survey.

• Less than 1 percent of Indonesian adults have used mobile money. Awareness of mobile money

services, however, rose substantially, from 8 percent in 2015 to 15 percent of the adult population

in 2016.

– The conversion rate from awareness to use increased compared to 2015; now a greater share

of Indonesian adults who are aware of mobile money are also mobile money users.

– The increase in the conversion rate suggests that market conditions are facilitating growth in

the use of mobile money.

• Arisans are the preferred non-full-service provider of financial services for the unbanked or

otherwise underserved members of society – women, those living in rural areas or those living

below the poverty line.

– Arisans/similar institutions are excluded from the financial inclusion calculation because they

do not offer a full suite of financial services.

– Twenty-two percent of Indonesian adults have used an arisan, compared to 11 percent who

have used a multifinance institution (MFI), and 2 percent who have used Bank Perkreditan

Rakyat (BPR).

– Twenty percent of all Indonesian adults without formal accounts have used an arisan.

INDONESIA

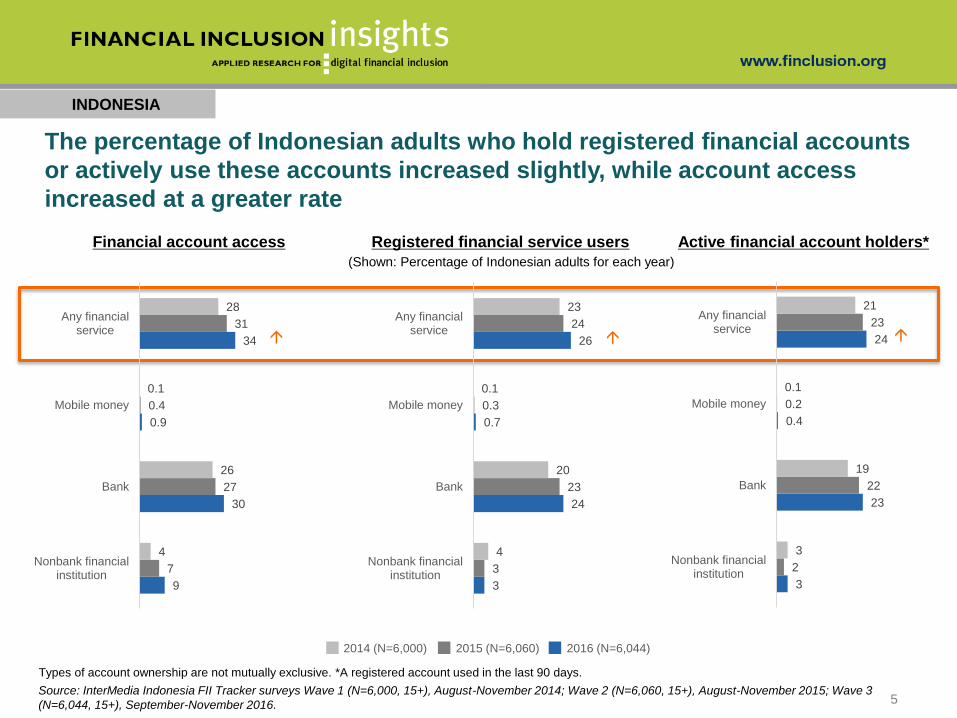

The percentage of Indonesian adults who hold registered financial accounts

or actively use these accounts increased slightly, while account access

increased at a greater rate

Financial account access Registered financial service users

(Shown: Percentage of Indonesian adults for each year)

Active financial account holders*

Types of account ownership are not mutually exclusive. *A registered account used in the last 90 days.

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.

2014 (N=6,000) 2015 (N=6,060) 2016 (N=6,044)

9

30

0.9

34

7

27

0.4

31

4

26

0.1

28

Nonbank financialinstitution

Bank

Mobile money

Any financialservice

3

24

0.7

26

3

23

0.3

24

4

20

0.1

23

Nonbank financialinstitution

Bank

Mobile money

Any financialservice

3

23

0.4

24

2

22

0.2

23

3

19

0.1

21

Nonbank financialinstitution

Bank

Mobile money

Any financialservice

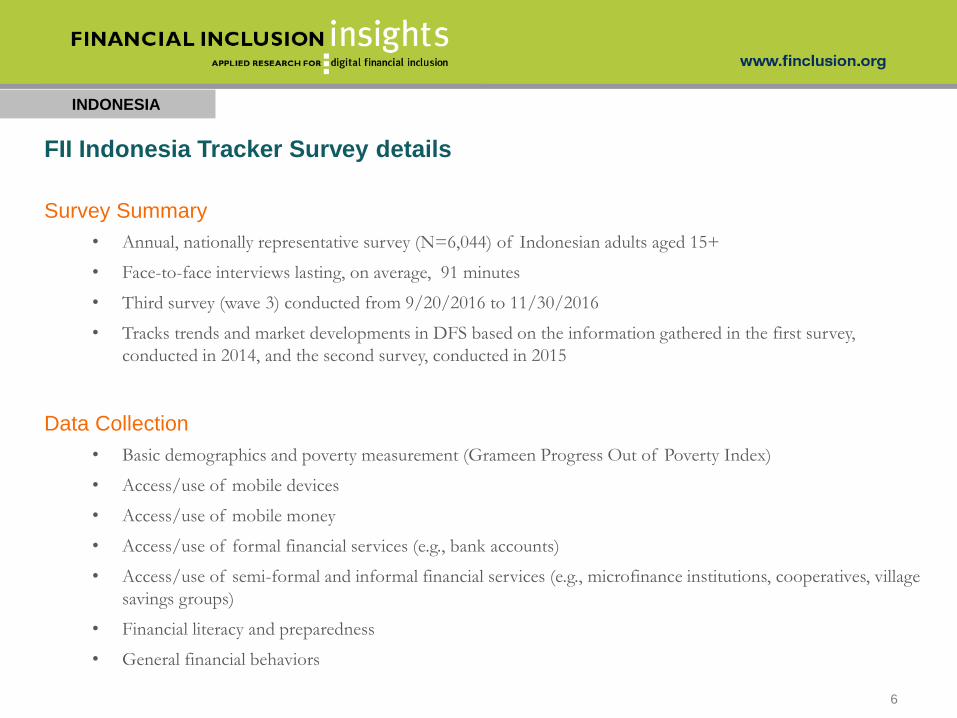

5

Survey Summary

• Annual, nationally representative survey (N=6,044) of Indonesian adults aged 15+

• Face-to-face interviews lasting, on average, 91 minutes

• Third survey (wave 3) conducted from 9/20/2016 to 11/30/2016

• Tracks trends and market developments in DFS based on the information gathered in the first survey,

conducted in 2014, and the second survey, conducted in 2015

Data Collection

• Basic demographics and poverty measurement (Grameen Progress Out of Poverty Index)

• Access/use of mobile devices

• Access/use of mobile money

• Access/use of formal financial services (e.g., bank accounts)

• Access/use of semi-formal and informal financial services (e.g., microfinance institutions, cooperatives, village

savings groups)

• Financial literacy and preparedness

• General financial behaviors

INDONESIA

FII Indonesia Tracker Survey details

6

INDONESIA

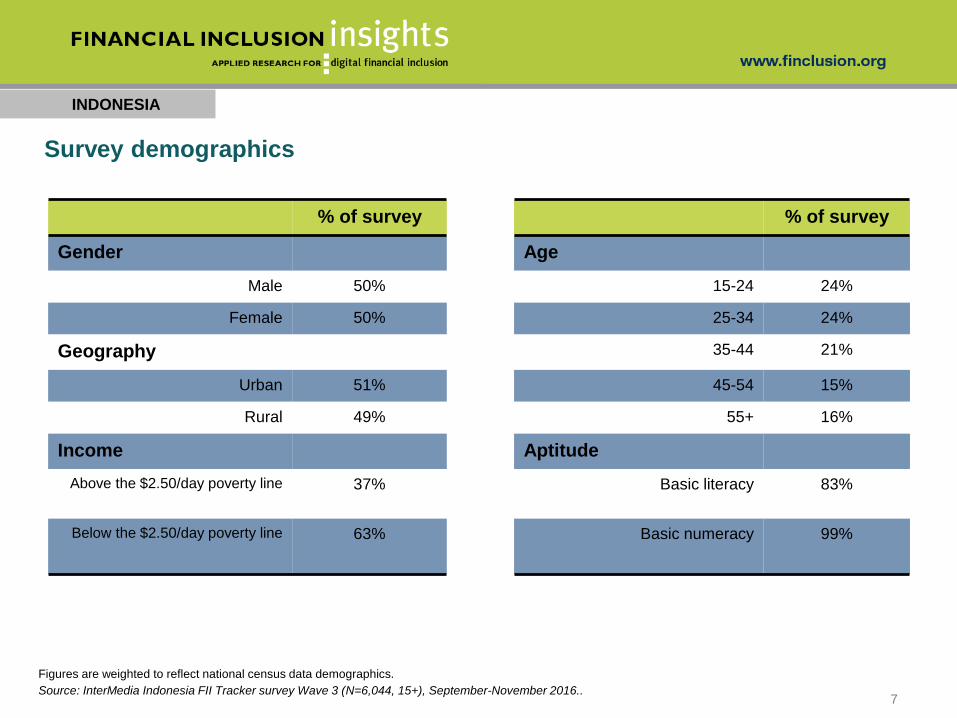

Survey demographics

Figures are weighted to reflect national census data demographics.

Source: InterMedia Indonesia FII Tracker survey Wave 3 (N=6,044, 15+), September-November 2016..

% of survey % of survey

Gender Age

Male 50% 15-24 24%

Female 50% 25-34 24%

Geography 35-44 21%

Urban 51% 45-54 15%

Rural 49% 55+ 16%

Income Aptitude

Above the $2.50/day poverty line 37% Basic literacy 83%

Below the $2.50/day poverty line 63% Basic numeracy 99%

7

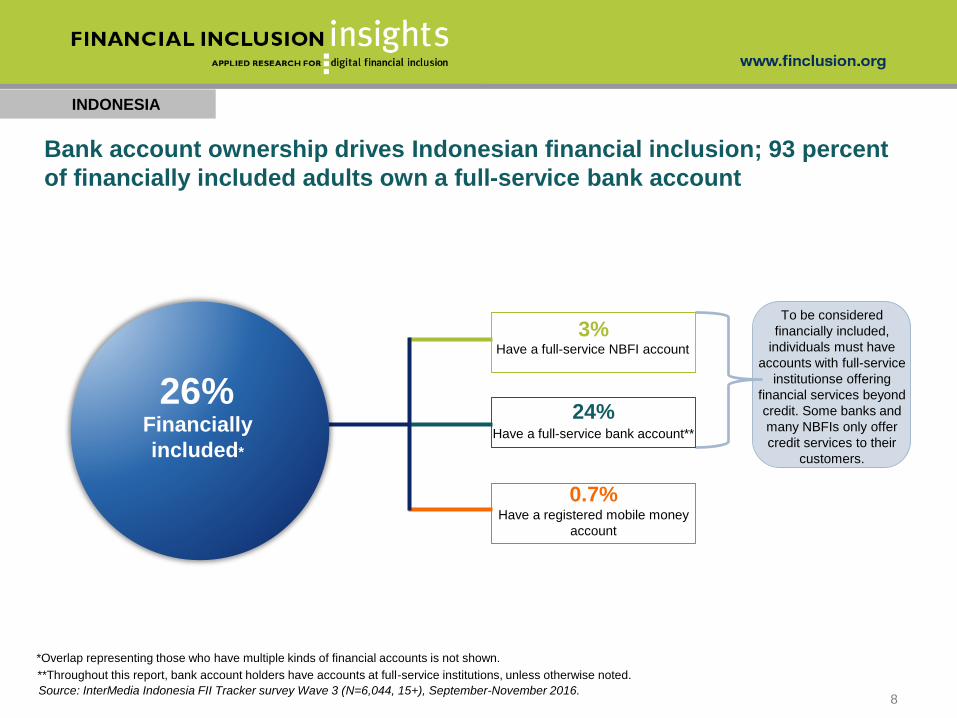

To be considered

financially included,

individuals must have

accounts with full-service

institutionse offering

financial services beyond

credit. Some banks and

many NBFIs only offer

credit services to their

customers.

INDONESIA

Have a full-service NBFI account

Have a full-service bank account**

Have a registered mobile money

account

24%

3%

0.7%

*Overlap representing those who have multiple kinds of financial accounts is not shown.

**Throughout this report, bank account holders have accounts at full-service institutions, unless otherwise noted.

Source: InterMedia Indonesia FII Tracker survey Wave 3 (N=6,044, 15+), September-November 2016.

26%Financially

included*

Bank account ownership drives Indonesian financial inclusion; 93 percent

of financially included adults own a full-service bank account

8

INDONESIA

Access to financial services(Shown: Percentage of Indonesian adults for each year)

Types of accounts are not mutually exclusive.

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.

2014 (N=6,000) 2015 (N=6,060) 2016 (N=6,044)

An additional 3 percent of the Indonesian adult population gained access to

financial services between 2015 and 2016

9

30

0.9

34

7

27

0.4

31

4

26

0.1

28

Nonbank financialinstitution

Bank

Mobile money

Any financialservice

9

INDONESIA

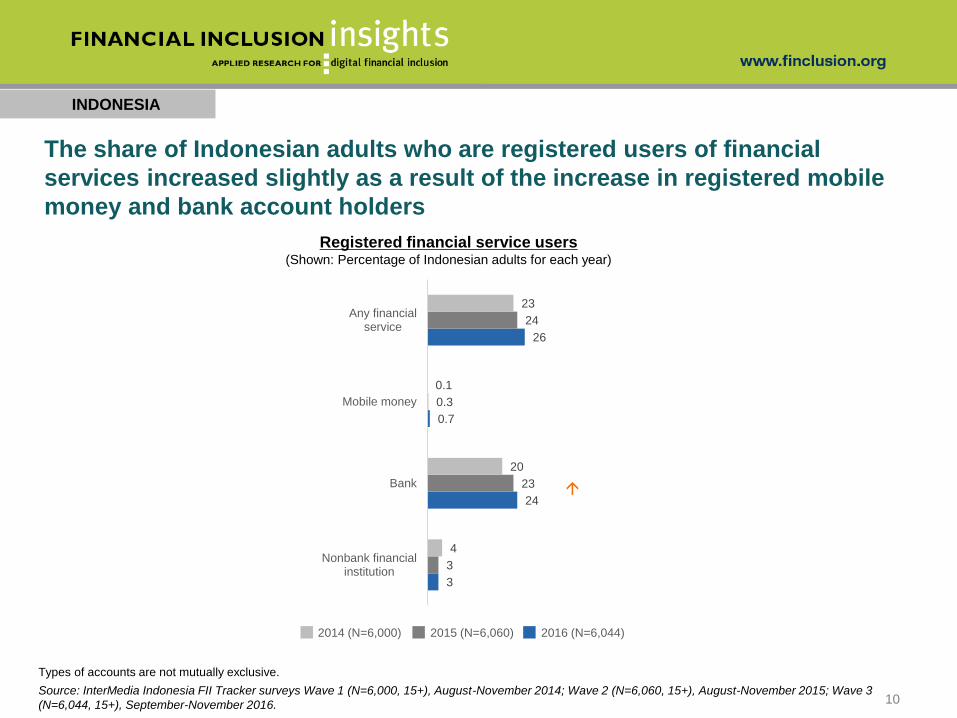

Types of accounts are not mutually exclusive.

Registered financial service users(Shown: Percentage of Indonesian adults for each year)

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.

The share of Indonesian adults who are registered users of financial

services increased slightly as a result of the increase in registered mobile

money and bank account holders

2014 (N=6,000) 2015 (N=6,060) 2016 (N=6,044)

3

24

0.7

26

3

23

0.3

24

4

20

0.1

23

Nonbank financialinstitution

Bank

Mobile money

Any financialservice

10

INDONESIA

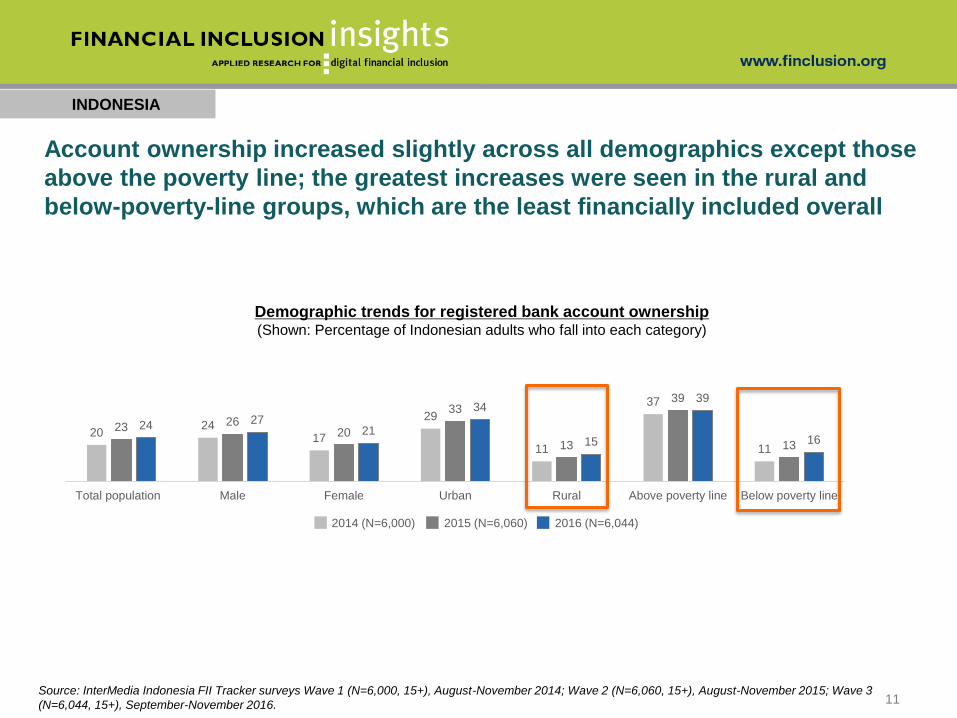

2024

17

29

11

37

11

23 2620

33

13

39

13

24 2721

34

15

39

16

Total population Male Female Urban Rural Above poverty line Below poverty line

Demographic trends for registered bank account ownership (Shown: Percentage of Indonesian adults who fall into each category)

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.

2014 (N=6,000) 2015 (N=6,060) 2016 (N=6,044)

Account ownership increased slightly across all demographics except those

above the poverty line; the greatest increases were seen in the rural and

below-poverty-line groups, which are the least financially included overall

11

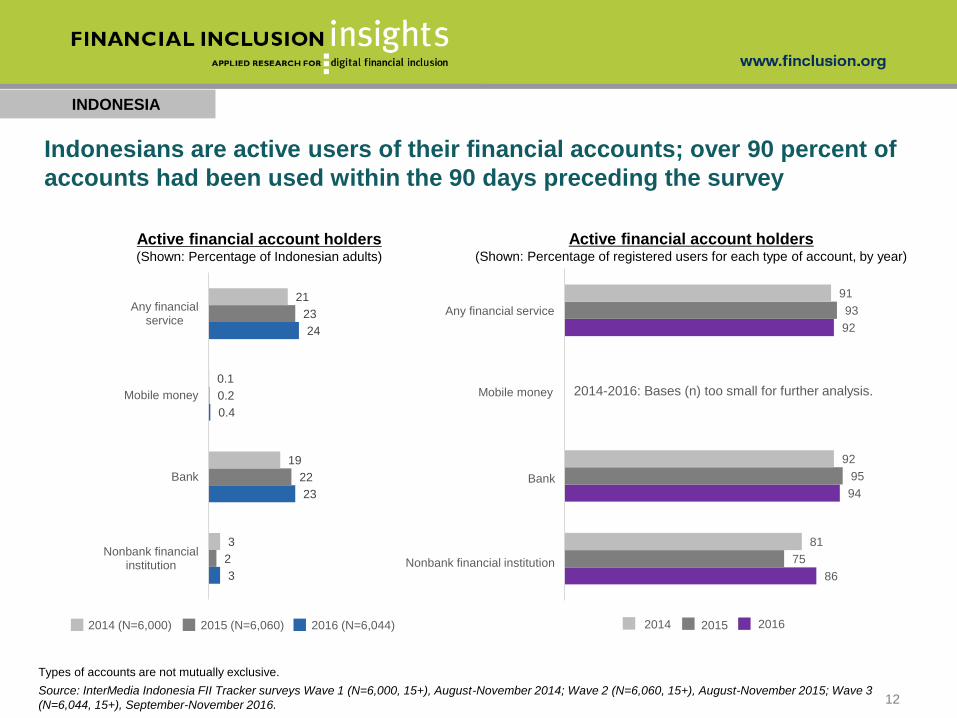

86

94

92

75

95

93

81

92

91

Nonbank financial institution

Bank

Mobile money

Any financial service

INDONESIA

Active financial account holders(Shown: Percentage of Indonesian adults)

Active financial account holders(Shown: Percentage of registered users for each type of account, by year)

2014 2016

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.

2014-2016: Bases (n) too small for further analysis.

Any financial service

Bank

Mobile money

Nonbank financial institution

2014 (N=6,000) 2015 (N=6,060) 2016 (N=6,044) 2015

Indonesians are active users of their financial accounts; over 90 percent of

accounts had been used within the 90 days preceding the survey

Types of accounts are not mutually exclusive.

3

23

0.4

24

2

22

0.2

23

3

19

0.1

21

Nonbank financialinstitution

Bank

Mobile money

Any financialservice

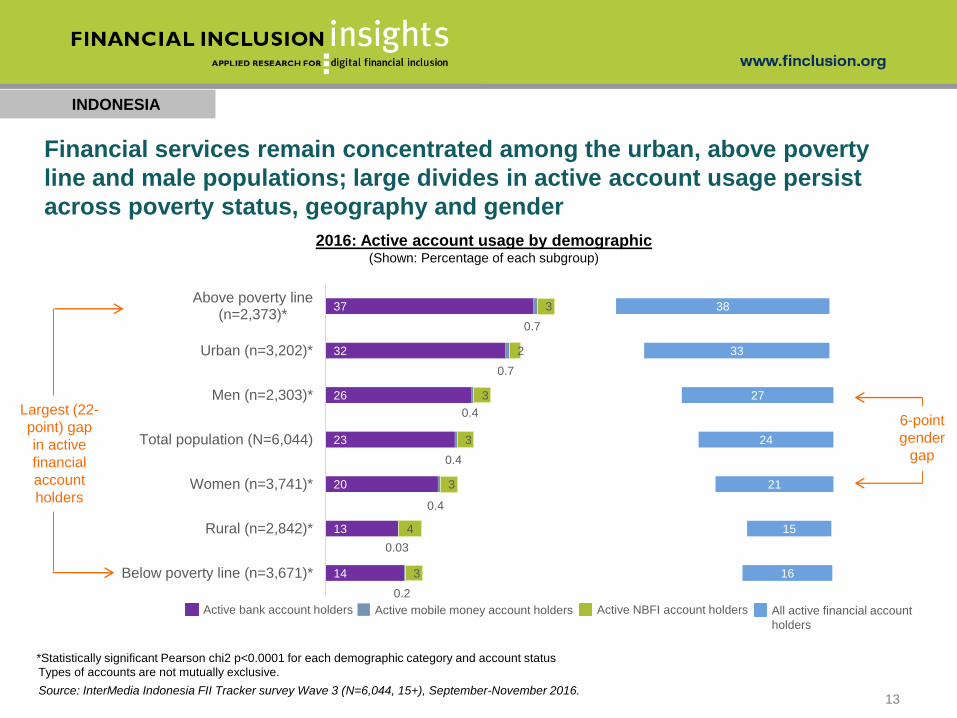

12

14

13

20

23

26

32

37

0.2

0.03

0.4

0.4

0.4

0.7

0.7

3

4

3

3

3

2

3

16

15

21

24

27

33

38

Below poverty line (n=3,671)*

Rural (n=2,842)*

Women (n=3,741)*

Total population (N=6,044)

Men (n=2,303)*

Urban (n=3,202)*

Above poverty line(n=2,373)*

INDONESIA

2016: Active account usage by demographic(Shown: Percentage of each subgroup)

Types of accounts are not mutually exclusive.

Active mobile money account holders Active NBFI account holdersActive bank account holders All active financial account

holders

Source: InterMedia Indonesia FII Tracker survey Wave 3 (N=6,044, 15+), September-November 2016.

Financial services remain concentrated among the urban, above poverty

line and male populations; large divides in active account usage persist

across poverty status, geography and gender

*Statistically significant Pearson chi2 p<0.0001 for each demographic category and account status

6-point

gender

gap

Largest (22-

point) gap

in active

financial

account

holders

13

INDONESIA

Bank uses, by type(Shown: Percentage of active bank account holders)

.

Due to the changes in the questionnaire some data points may not be directly comparable across years.

28

14

29

6

8

6

65

77

65

2014 (n=1,100)

2015 (n=1,291)

2016 (n=1,302)

Basic activities and P2P onlyAt least one advanced activity

(i.e., bill pay, loan activities)

Basic activities only

(CICO and account management)

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.14

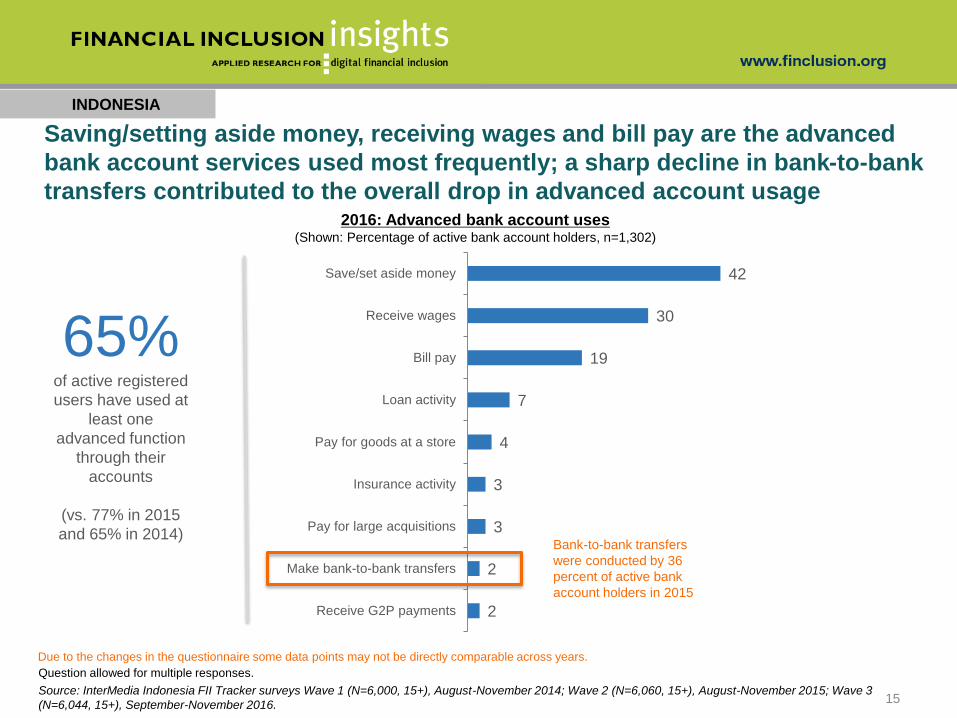

Fewer active bank account holders are undertaking advanced banking

activities compared to 2015; however, the majority still use their accounts

for advanced activities

2

2

3

3

4

7

19

30

42

Receive G2P payments

Make bank-to-bank transfers

Pay for large acquisitions

Insurance activity

Pay for goods at a store

Loan activity

Bill pay

Receive wages

Save/set aside money

INDONESIA

2016: Advanced bank account uses(Shown: Percentage of active bank account holders, n=1,302)

65%of active registered

users have used at

least one

advanced function

through their

accounts

(vs. 77% in 2015

and 65% in 2014)

Due to the changes in the questionnaire some data points may not be directly comparable across years.

Question allowed for multiple responses.

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.15

Saving/setting aside money, receiving wages and bill pay are the advanced

bank account services used most frequently; a sharp decline in bank-to-bank

transfers contributed to the overall drop in advanced account usage

Bank-to-bank transfers

were conducted by 36

percent of active bank

account holders in 2015

INDONESIA

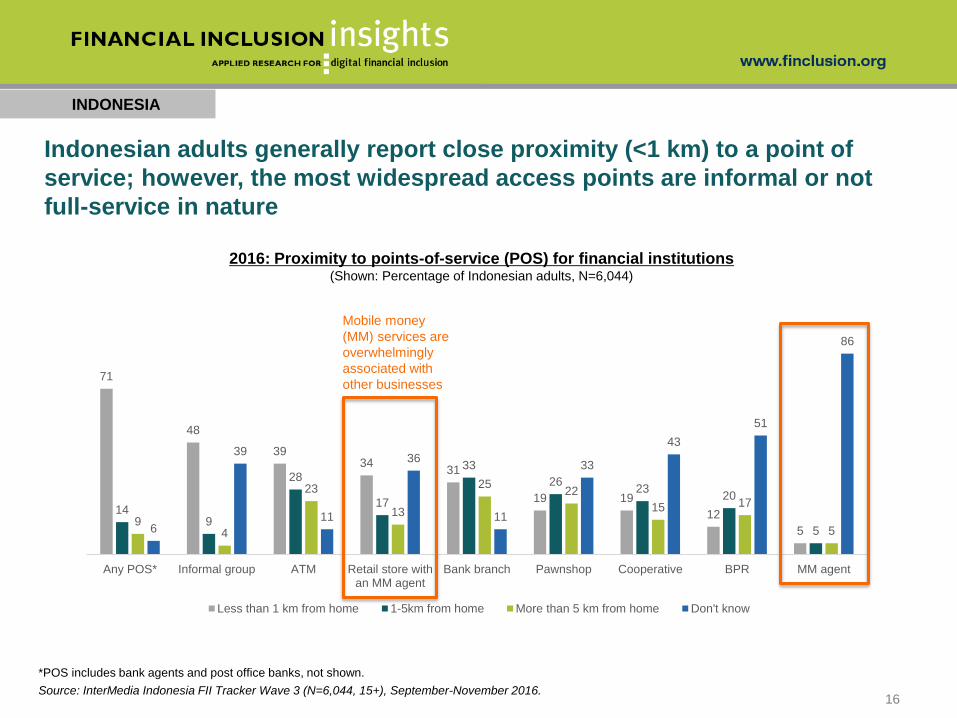

2016: Proximity to points-of-service (POS) for financial institutions(Shown: Percentage of Indonesian adults, N=6,044)

*POS includes bank agents and post office banks, not shown.

Indonesian adults generally report close proximity (<1 km) to a point of

service; however, the most widespread access points are informal or not

full-service in nature

71

48

3934

31

19 19

12

5

149

28

17

33

2623

20

59

4

23

13

2522

15 17

56

39

11

36

11

33

43

51

86

Any POS* Informal group ATM Retail store withan MM agent

Bank branch Pawnshop Cooperative BPR MM agent

Less than 1 km from home 1-5km from home More than 5 km from home Don't know

Mobile money

(MM) services are

overwhelmingly

associated with

other businesses

Source: InterMedia Indonesia FII Tracker Wave 3 (N=6,044, 15+), September-November 2016.16

INDONESIA

2015

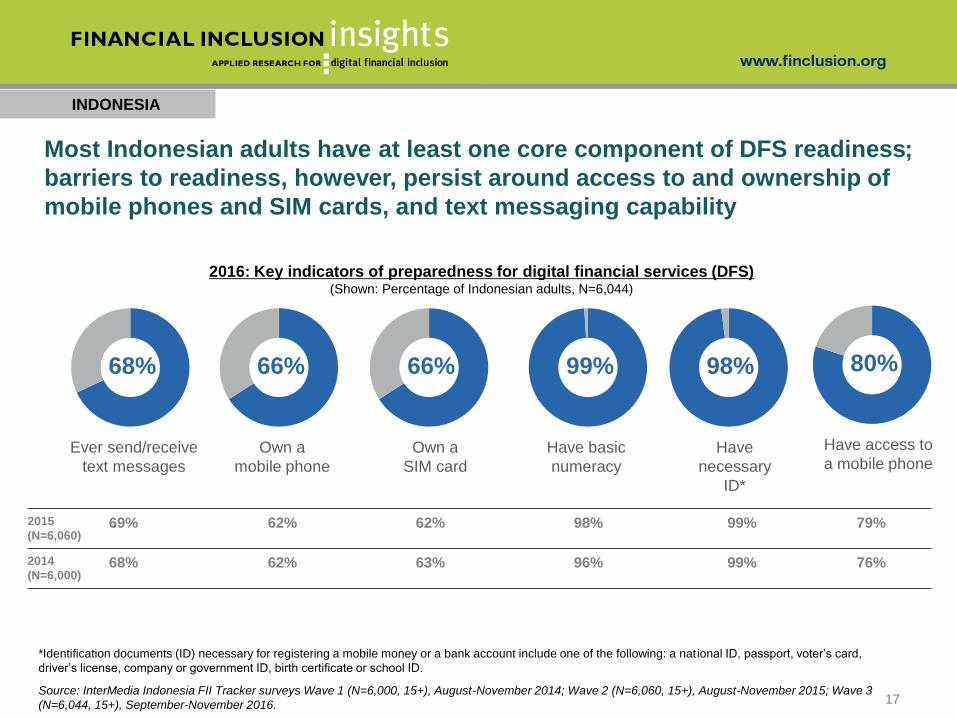

(N=6,060)69% 62% 62% 98% 99% 79%

2014

(N=6,000)68% 62% 63% 96% 99% 76%

80%

Have access to

a mobile phone

68%

Ever send/receive

text messages

99%

Have basic

numeracy

98%

Have

necessary

ID*

66%

Own a

SIM card

66%

Own a

mobile phone

*Identification documents (ID) necessary for registering a mobile money or a bank account include one of the following: a national ID, passport, voter’s card,

driver’s license, company or government ID, birth certificate or school ID.

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.

Most Indonesian adults have at least one core component of DFS readiness;

barriers to readiness, however, persist around access to and ownership of

mobile phones and SIM cards, and text messaging capability

2016: Key indicators of preparedness for digital financial services (DFS)(Shown: Percentage of Indonesian adults, N=6,044)

17

MM OTC use, 0.1%

MM registered

users, 0.3%

INDONESIA

2014 (N=6,000) 2015 (N=6,060)

MM registered

users, 0.1%

0.02

conversion

rate

6%

aware

0.1% use

mobile

money

0.05

conversion

rate

8%

aware

0.4% use

mobile

money

MM OTC use, 0.3%

MM registered

users, 0.7%

2016 (N=6,044)

0.06

conversion

rate

15%

aware

0.9% use

mobile

money**

Despite substantial growth in both mobile money awareness and the rate of

conversion from awareness to use, a negligible share of the Indonesian

population currently uses mobile money

Conversion from awareness of mobile money (MM) providers* to mobile money use(Shown: Percentage of Indonesian adults for each year)

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.

**Sum of components may not match total due to rounding.

*Aware of at least one provider

18

INDONESIA

6 6 68

3

10

3

8 9 8

13

3

14

4

15 16 15

22

8

21

12

Total population Male Female Urban Rural Above poverty line Below poverty line

2014 2015 2016

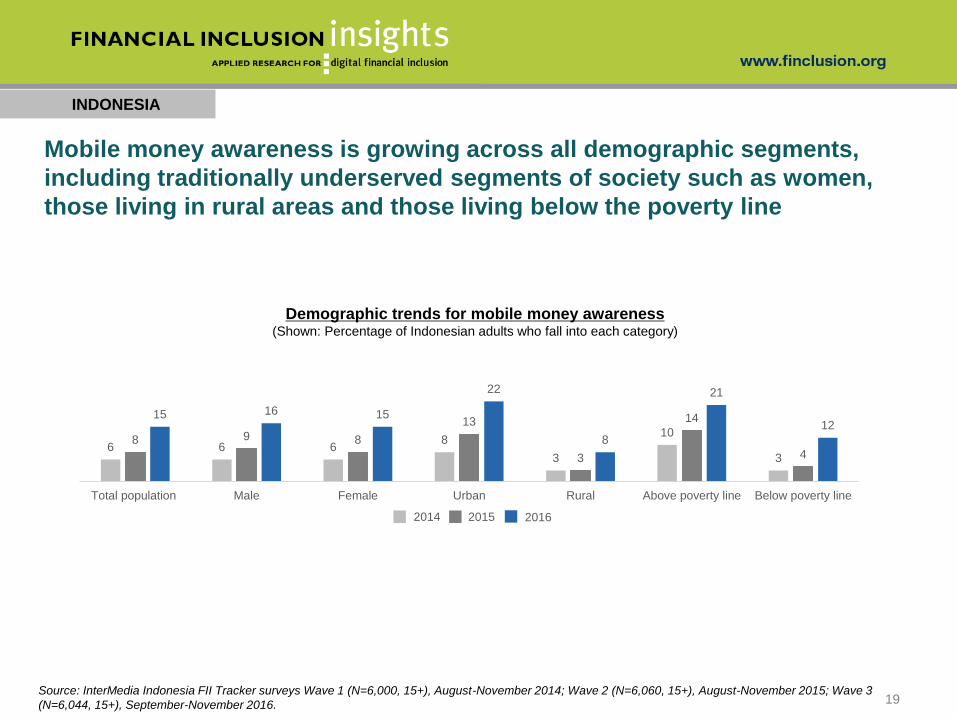

Mobile money awareness is growing across all demographic segments,

including traditionally underserved segments of society such as women,

those living in rural areas and those living below the poverty line

Demographic trends for mobile money awareness(Shown: Percentage of Indonesian adults who fall into each category)

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016. 19

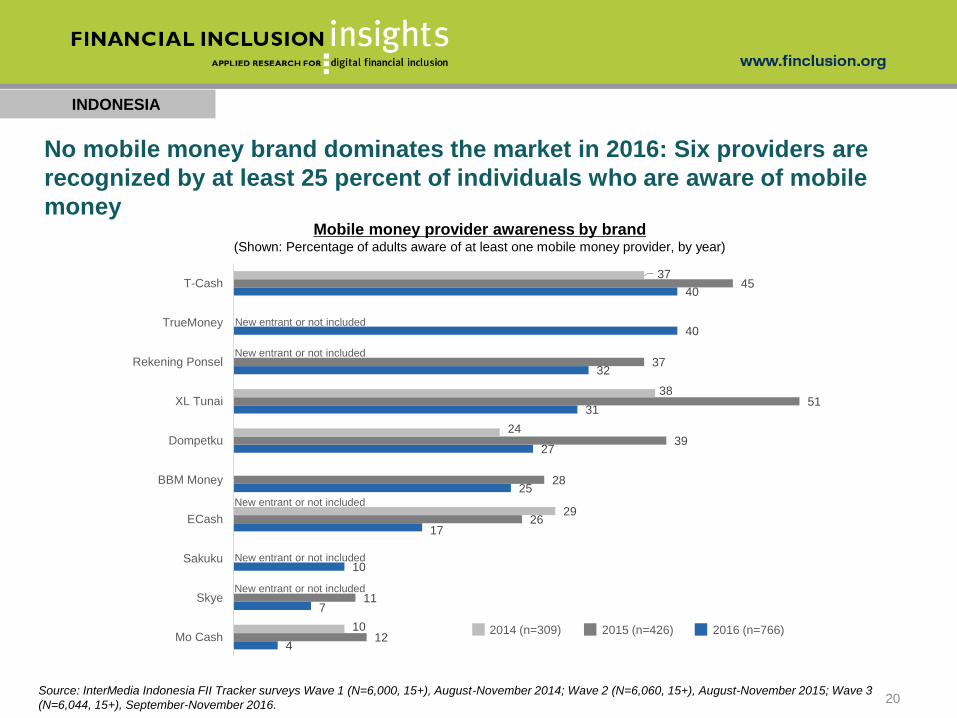

4

7

10

17

25

27

31

32

40

40

12

11

26

28

39

51

37

45

10

29

24

38

37

Mo Cash

Skye

Sakuku

ECash

BBM Money

Dompetku

XL Tunai

Rekening Ponsel

TrueMoney

T-Cash

New entrant or not included

New entrant or not included

New entrant or not included

New entrant or not included

New entrant or not included

INDONESIA

Mobile money provider awareness by brand(Shown: Percentage of adults aware of at least one mobile money provider, by year)

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.

2014 (n=309) 2015 (n=426) 2016 (n=766)

20

No mobile money brand dominates the market in 2016: Six providers are

recognized by at least 25 percent of individuals who are aware of mobile

money

INDONESIA

Question allowed for multiple responses. Not all response options shown.

Source: InterMedia Indonesia FII Tracker survey Wave 3 (N=6,044, 15+), September-November 2016.

2014 (n=305) 2015 (n=401) 2016 (n=727)

21

A lack of understanding of the purpose and use(s) of mobile money drives

nonuse among those who are aware of mobile money

4

4

14

40

2

4

14

28

2

8

12

27

I do not trust thatmy money is safe

I never have moneyto make

transactions withthe service

I don't need (anaccount), I don't

make anytransactions

I don't know what itis for

Top reasons for mobile money nonuse among MM-aware individuals(Shown: Percentage of Indonesian adults who are aware, but do not use, MM by year)

INDONESIA

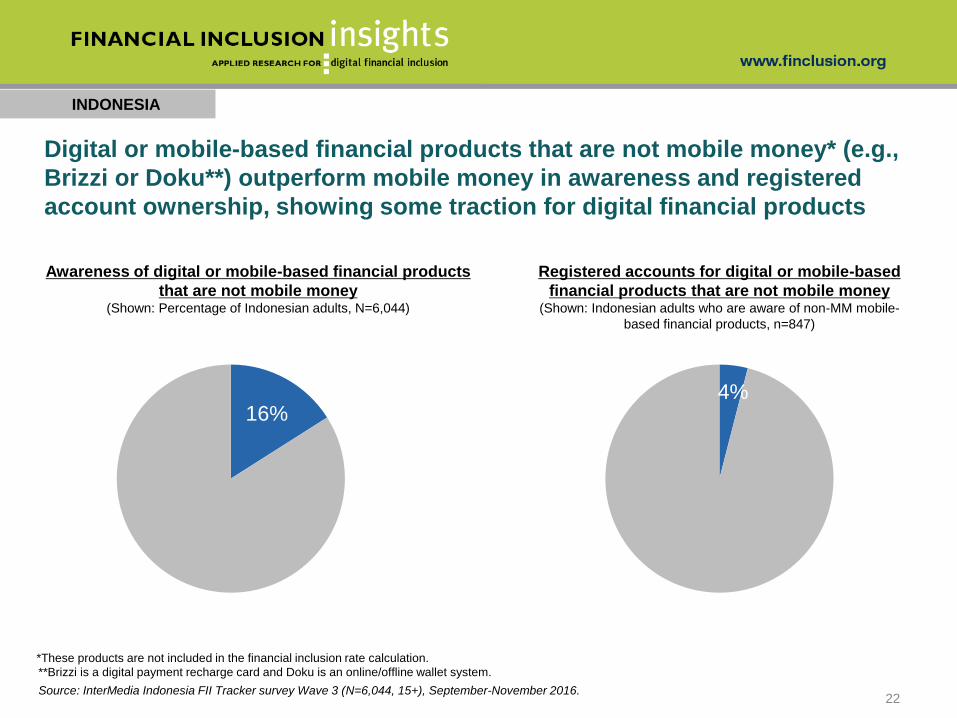

22

Digital or mobile-based financial products that are not mobile money* (e.g.,

Brizzi or Doku**) outperform mobile money in awareness and registered

account ownership, showing some traction for digital financial products

16%

Awareness of digital or mobile-based financial products

that are not mobile money(Shown: Percentage of Indonesian adults, N=6,044)

Registered accounts for digital or mobile-based

financial products that are not mobile money(Shown: Indonesian adults who are aware of non-MM mobile-

based financial products, n=847)

4%

Source: InterMedia Indonesia FII Tracker survey Wave 3 (N=6,044, 15+), September-November 2016.

**Brizzi is a digital payment recharge card and Doku is an online/offline wallet system.

*These products are not included in the financial inclusion rate calculation.

INDONESIA

23

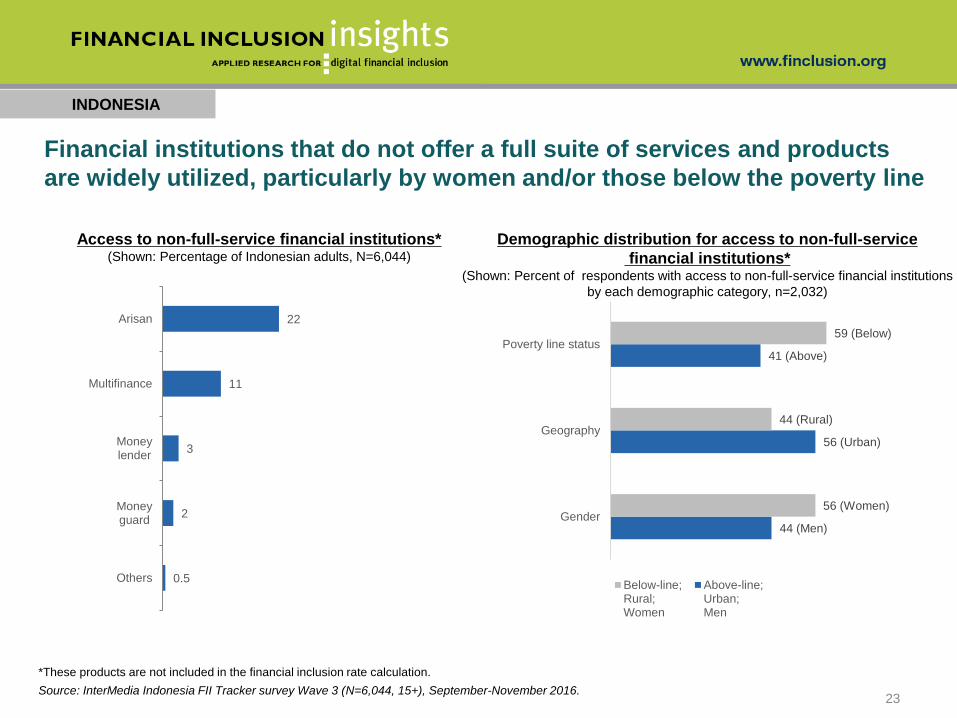

Financial institutions that do not offer a full suite of services and products

are widely utilized, particularly by women and/or those below the poverty line

Source: InterMedia Indonesia FII Tracker survey Wave 3 (N=6,044, 15+), September-November 2016.

Access to non-full-service financial institutions*(Shown: Percentage of Indonesian adults, N=6,044)

0.5

2

3

11

22

Others

Moneyguard

Moneylender

Multifinance

Arisan

Demographic distribution for access to non-full-service

financial institutions*(Shown: Percent of respondents with access to non-full-service financial institutions

by each demographic category, n=2,032)

44 (Men)

56 (Urban)

41 (Above)

56 (Women)

44 (Rural)

59 (Below)

Gender

Geography

Poverty line status

Below-line;Rural;Women

Above-line;Urban;Men

*These products are not included in the financial inclusion rate calculation.

INDONESIA

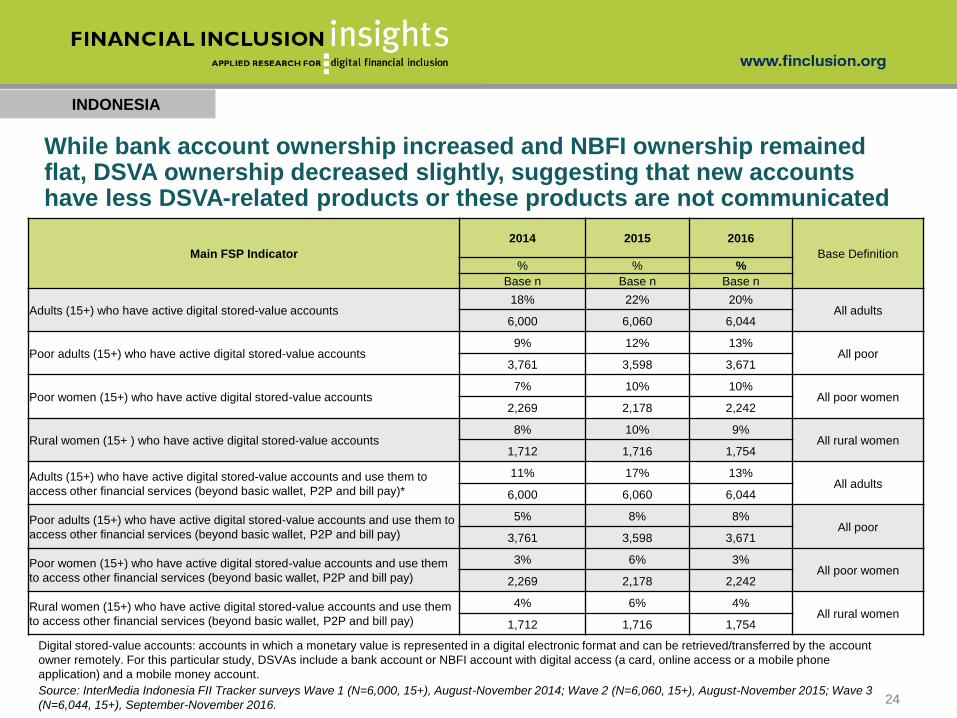

Digital stored-value accounts: accounts in which a monetary value is represented in a digital electronic format and can be retrieved/transferred by the account

owner remotely. For this particular study, DSVAs include a bank account or NBFI account with digital access (a card, online access or a mobile phone

application) and a mobile money account.

Main FSP Indicator

2014 2015 2016

Base Definition% % %

Base n Base n Base n

Adults (15+) who have active digital stored-value accounts18% 22% 20%

All adults6,000 6,060 6,044

Poor adults (15+) who have active digital stored-value accounts9% 12% 13%

All poor3,761 3,598 3,671

Poor women (15+) who have active digital stored-value accounts7% 10% 10%

All poor women2,269 2,178 2,242

Rural women (15+ ) who have active digital stored-value accounts 8% 10% 9%

All rural women1,712 1,716 1,754

Adults (15+) who have active digital stored-value accounts and use them to

access other financial services (beyond basic wallet, P2P and bill pay)*

11% 17% 13%All adults

6,000 6,060 6,044

Poor adults (15+) who have active digital stored-value accounts and use them to

access other financial services (beyond basic wallet, P2P and bill pay)

5% 8% 8%All poor

3,761 3,598 3,671

Poor women (15+) who have active digital stored-value accounts and use them

to access other financial services (beyond basic wallet, P2P and bill pay)

3% 6% 3%All poor women

2,269 2,178 2,242

Rural women (15+) who have active digital stored-value accounts and use them

to access other financial services (beyond basic wallet, P2P and bill pay)

4% 6% 4%All rural women

1,712 1,716 1,754

Source: InterMedia Indonesia FII Tracker surveys Wave 1 (N=6,000, 15+), August-November 2014; Wave 2 (N=6,060, 15+), August-November 2015; Wave 3

(N=6,044, 15+), September-November 2016.

While bank account ownership increased and NBFI ownership remained flat, DSVA ownership decreased slightly, suggesting that new accounts have less DSVA-related products or these products are not communicated

24

For more information, contact:

Alex Moler, Research Manager [email protected]

Sam Schueth, Director of Research [email protected]