indonesia universal healthcare coverage - opportunities and challenges

TRANSCRIPT

Universal Healthcare Coverage - Indonesia | 1

The New Frontier of Growth

October 2012

Universal

Healthcare Coverage – Opportunities & Challenges

ahead in Indonesia

Spotlight Indonesia

Universal Healthcare Coverage - Indonesia | 2

An introduction

With the fourth largest population in the world and a growing economy accompanied with rising incomes, Indonesia

presents many opportunities to healthcare providers and suppliers looking for markets to expand in. Recent public

reforms aimed at bringing universal healthcare coverage (UHC) to all Indonesians by 2019 is likely to bring significant

changes to healthcare landscape as we currently know it.

Clearstate’s “New Frontier of Growth” market brief presents an introductory overview of the ongoing developments

within the Indonesia healthcare landscape as the UHC is being implemented, and highlights the challenges and

opportunities for market participants – specifically in the healthcare service provision, pharmaceutical, and medical

device industries.

Health access remains limited and lacking despite strong economic growth

A growing population, healthy economy, and rising incomes have been a good mixture for the Indonesian healthcare

industry in the past decade. Absolute healthcare expenditure has grown annually at a compounded rate (CAGR) of 18%

between 2001 and 2011, greatly boosting demand for healthcare services, pharmaceuticals, and medical devices. Due

to such increases in demand, Indonesia’s healthcare industry has made much progress in recent years.

Yet, there still remains a severe shortage of healthcare infrastructure and healthcare human resources. In 2011,

Indonesia spent only 2.7% of its GDP on healthcare - this translates into a meager per capita spending of USD 84 on

healthcare in 2010, well below the OECD average of USD 4,598 and the East Asia & Pacific average of USD 336 in the

same year (See Figure 1).

Figure 1: Healthcare expenditure per capita versus GDP per capita, 2010

The unequal distribution of healthcare infrastructure and resources have further exacerbated this shortage – the

majority of such resources are concentrated in Jakarta and Java Island, leaving the rest of Indonesia’s populations in the

sprawling archipelago with little accessibility to healthcare services. Additionally, an estimated 50% of total healthcare

expenditure is out-of-pocket (2011), making Indonesia’s private expenditure as a percentage of healthcare expenditure

one of the highest in the world. This has led to severe inequality in terms of healthcare provision – where there are

urban-rural and rich-poor divides, due to low affordability and accessibility of healthcare services to the general

population.

Denmark, 6,253 Indonesia, 84

South Korea, 1,452

Malaysia, 368

Singapore, 2,005

Thailand, 179

UK, 3,495

U.S., 8,233 Vietnam, 83

OECD, 4,593 East Asia & Pacific Average,

336

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0 10,000 20,000 30,000 40,000 50,000 60,000

2010

Hea

lth

expe

ndit

ure

per

capi

tal

(cur

rent

US$

)

2010 GDP per capita (current US$)

Source: Worldbank Development

Indicators

Universal Healthcare Coverage - Indonesia | 3

As such, the Indonesian government has made steps in recent years to move towards universal healthcare coverage.

Reforms first started in 2004 when a law was passed to bring about change to the Indonesian healthcare system. Weak

political resolve was a strong inhibitor for change in the initial years of reform, but these efforts have gradually been

ramped up in recent years. Most importantly, the recent healthcare bill ensuring the implementation of the Bandan

Penyelenggara Jaminan Sosial (BPJS) has ended an era of uncertainty around the government’s commitment towards

universal health coverage.

Healthcare reform in Indonesia – Moving towards Universal Healthcare Coverage

Current estimates put the total proportion of Indonesians covered by some form of insurance at 72% of the entire

population in 2013. However, the system remains fragmented in nature, leaving many poor Indonesians without proper

access to healthcare. The most recent healthcare reform law passed in 2011 aims to address this by integrating the

major insurance schemes1 that are currently active in Indonesia. A new national social security agency, the BPJS, begins

its role of integration and creating a national insurance scheme for all Indonesians in 2014, aiming to attain full

coverage by 2019. This marks an important step in Indonesia’s healthcare progress by introducing a single-payer system.

Through collaboration with health practitioners, universities, and other related ministries, the MOH has already taken

steps to develop a road map – INA Medicare 2012-2019, and further reforms to the country’s healthcare system are

expected to follow this plan. The national insurance scheme is expected to be a comprehensive package which would

cover the cost of hospital stays in third class wards for persons whose insurance has been paid for by the government;

persons able to pay for the premium under the new scheme are entitled to first and second class wards depending on

the scheme they have chosen. On the other hand, the provider-payment structure is likely to take the form of a mix of

capitation and diagnostic-related group (DRG) methods.

Such reforms, if implemented successfully, are expected to increase the accessibility of healthcare services to

Indonesians, especially the poor and those residing in rural areas. The MOH estimates that it would be able to cover a

total of 121.6m Indonesians in 2014 by integrating the major insurance schemes. For the rest of the population,

coverage has been planned to gradually extend to the full 2019 population of 257.5m Indonesians, leading to a

significant rise in demand for healthcare services. Yet, cost concerns and the consolidation of health insurance schemes

into a single-payer system are likely to bring about pricing pressures as well, lowering the value of products or services

offered in the healthcare industry

1 Current major insurance schemes providing coverage to Indonesians include Askes (for civil servants and pensioners), Jamkesmas (poor and near poor), Jamsostek (formal sector workers), Jamkesda (district-level schemes), and private health insurance. The inefficiencies of such a fragmented system are clearly seen in Jamkesmas coverage, where there exists a huge issue of mis-targeting and leakage to the non-poor, resulting in the poor continuing to experience poor access to healthcare. Jamkesda, managed by local government units may have been able to mitigate this slightly, however access to healthcare remains a large issue to the poor.

Figure 2: Timeline for Universal Healthcare Coverage Implementation in Indonesia

Universal Healthcare Coverage - Indonesia | 4

0.941.79

1

2.712.1

2.17

4

0.001.002.003.004.005.00

01,0002,0003,0004,0005,000

Ho

spit

al b

ed

s p

er

10

0,0

00

po

p.

He

alt

hca

re e

xp

en

dit

ure

pe

r ca

pit

a (

curr

en

t U

S$

)

Hospital beds per 100,000 pop.

2011 Health expenditure per capita (current US$)

+ Data as latest available in Worldbank or Ministry of Health databases* Healthcare expenditure for OECD and World averages are 2012 estimates

+

UHC and its impact to healthcare service providers

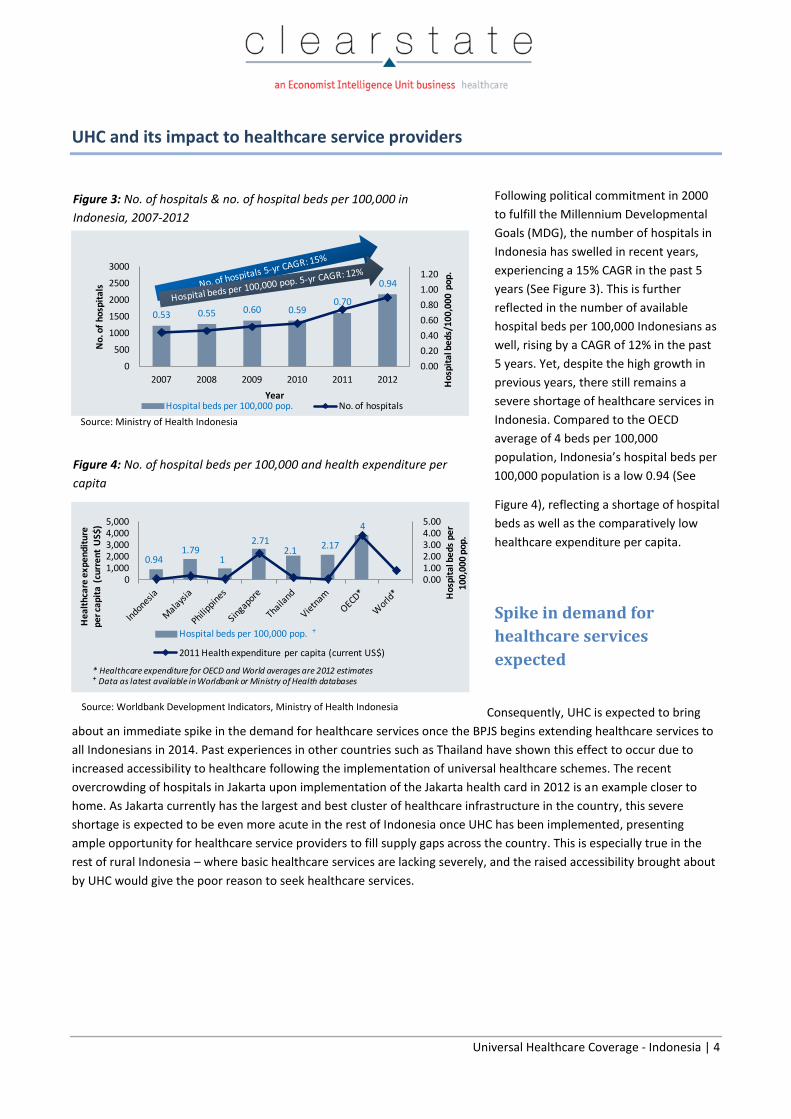

Following political commitment in 2000

to fulfill the Millennium Developmental

Goals (MDG), the number of hospitals in

Indonesia has swelled in recent years,

experiencing a 15% CAGR in the past 5

years (See Figure 3). This is further

reflected in the number of available

hospital beds per 100,000 Indonesians as

well, rising by a CAGR of 12% in the past

5 years. Yet, despite the high growth in

previous years, there still remains a

severe shortage of healthcare services in

Indonesia. Compared to the OECD

average of 4 beds per 100,000

population, Indonesia’s hospital beds per

100,000 population is a low 0.94 (See

Figure 4), reflecting a shortage of hospital

beds as well as the comparatively low

healthcare expenditure per capita.

Spike in demand for

healthcare services

expected

Consequently, UHC is expected to bring

about an immediate spike in the demand for healthcare services once the BPJS begins extending healthcare services to

all Indonesians in 2014. Past experiences in other countries such as Thailand have shown this effect to occur due to

increased accessibility to healthcare following the implementation of universal healthcare schemes. The recent

overcrowding of hospitals in Jakarta upon implementation of the Jakarta health card in 2012 is an example closer to

home. As Jakarta currently has the largest and best cluster of healthcare infrastructure in the country, this severe

shortage is expected to be even more acute in the rest of Indonesia once UHC has been implemented, presenting

ample opportunity for healthcare service providers to fill supply gaps across the country. This is especially true in the

rest of rural Indonesia – where basic healthcare services are lacking severely, and the raised accessibility brought about

by UHC would give the poor reason to seek healthcare services.

Source: Ministry of Health Indonesia

Source: Worldbank Development Indicators, Ministry of Health Indonesia

Figure 3: No. of hospitals & no. of hospital beds per 100,000 in

Indonesia, 2007-2012

Figure 4: No. of hospital beds per 100,000 and health expenditure per

capita

0.53 0.55 0.60 0.590.70

0.94

0.00

0.20

0.40

0.60

0.80

1.00

1.20

0

500

1000

1500

2000

2500

3000

2007 2008 2009 2010 2011 2012 Ho

spit

al b

ed

s/1

00

,00

0 p

op

.

No

. of

ho

spit

als

YearHospital beds per 100,000 pop. No. of hospitals

Universal Healthcare Coverage - Indonesia | 5

Expected overcrowding of public facilities to benefit private providers

At the start of 2013, public hospitals accounted for only 40% of all hospitals in Indonesia; yet, the high concentration of

hospital beds (83%) situated in public hospitals indicates that the majority of Indonesians are serviced by large publicly

run hospitals. This is expected to change gradually over time as the more affluent population seeks better quality

healthcare in and shorter waits in public hospitals. Many rich Indonesians currently go to Singapore and Malaysia to

seek specialist treatment as there is insufficient infrastructure to provide good quality care despite there being over

1,800 hospitals within the country. Thus private providers of healthcare services can expect to see more opportunity in

the near-term as the more affluent population demands for premium healthcare services.

Providers need to expect future challenges ahead in terms of quality standards

and pricing

As demand stabilizes, healthcare service providers can expect challenges ahead as well. Under a single-payer system,

the BPJS would be able to wield considerably more influence and power on issues concerning standards in the

healthcare services industry – including quality standards and pricing. The MOH’s experimentation with DRG-based

methods to calculate provider payments instead of the usual capitation or fee-for-service methods is a sign of the

situation possibly changing towards this trend. More adoption of DRG-based methods of provider payments may

ultimately lead to standardized quality of care and the gradual lowering of prices for healthcare services. During the

implementation of universal health coverage in Thailand, pricing pressures from the government led to the demise of

many small hospitals facing cost pressures which made it uneconomical to run small operations. In the long-term,

healthcare service providers in Indonesia may also face similar pricing pressures due to the consolidation to the single-

payer system.

Private healthcare service providers better poised to take advantage of UHC

The implementation of UHC in Indonesia presents more opportunities for healthcare service providers in the near

future, especially due to the current chronic undersupply of healthcare infrastructure within the country. We have

already witnessed a slew of private investments into the country’s healthcare service industry looking to take

advantage of the situation – such as Ramsay Healthcare’s collaboration with Sime Darby in the region, and the rapid

expansion of Siloam hospitals. With more breadth and depth in the pockets, we expect that large private providers are

expected to be better poised than the public sector to navigate within the new UHC system in Indonesia.

Universal Healthcare Coverage - Indonesia | 6

UHC and its impact to the Med-Tech and Pharmaceutical industries

The Med-Tech and Pharmaceutical industries in Indonesia have enjoyed healthy growth in the past decade – led by

expansions in not only the quantity of healthcare service providers, but also the quality of healthcare service providers

within the country. This is likely to continue as the healthcare services industry in Indonesia continues to grow more

aggressively following the implementation of UHC.

Figure 5: Overview of Med-Tech and Pharmaceutical industries in Indonesia

Rural areas presents opportunities for large Med-Tech players with localized and

innovative business models

As rural areas currently face chronic shortages of hospital services, the supply of medical equipment and technology in

areas ramping up on healthcare infrastructure is expected to be one of the highest contributors to growth in the short

to mid-term. Although strong in Indonesia due to their technological advantages, the traditionally dominant MNCs are

likely to be slower in this volume race to supply rural healthcare service providers. This is largely because rural

healthcare service providers are more cost-conscious or have lower awareness of the technology at hand. We have

previously observed such a preference for low-cost products from China and South Korea in rural areas during the the

government’s last spending spree on healthcare.

Despite this, MNCs may still be able to take advantage of the tremendous opportunity in the untapped rural areas by

committing developing localized and adopt innovate business models suited for this segment. Possible methods include

education programs for healthcare service providers in rural areas to raise awareness, more collaboration with local

distributors to attain better reach in far-flung rural areas, or even customizing a product to fit rural areas’ needs.

MNC Med-Tech players expected to do well in larger cities, however pricing

pressures may be a damper on value in the future

Conversely, MNC players would be able to keep their hold on larger cities – where the increasingly affluent middle

income population is likely to demand higher quality healthcare services accompanied with higher quality medical

technology, especially in the private sector. Changes likely to bring advantages to MNC players include possible

Universal Healthcare Coverage - Indonesia | 7

standardization of care under the DRG-system and increased regulations to bring about improvements in quality of care

– eventually leading to more demand in areas where the traditionally dominant MNC players are stronger in.

Yet, even in larger cities, MNC players may soon need to contend with promoting cost-efficiency as healthcare service

providers begin to grapple with pricing pressures. This is in contrast to the current trend where Indonesian hospitals

with large budgets are clamoring to purchase high-end medical technology, such as 3.0 Tesla MRIs, in order to compete

and attract affluent patients. The development of a “value product segment” that provides not only cost efficiency but

value-added features may likely be the long-term direction for MNCs in the med-tech sector to develop in order to fully

take advantage of Indonesia’s growth.

Local Pharmaceutical companies in prime position for UHC implementation

Local pharmaceutical companies currently have a strong hold on the Indonesian market, where low healthcare

expenditure has generally favored the use of generics – which makes up close to 70% of the Indonesian pharmaceutical

market. Furthermore, regulators require all pharmaceuticals sold in the country to be produced locally, putting big

Pharma at a disadvantage. Consequently, local players with their strong distributor networks are expected to gain

tremendously from an expected surge in demand for low-cost generics under the UHC, especially in rural areas where

the provision of basic healthcare would greatly increase population access to medicines.

Big Pharma should also be excited about UHC implementation in Indonesia

Despite dominance of local players, various international players such as Sanofi and Pfizer have invested in significant

resource in the Indonesian market by setting up production facilities. This is likely the case as these companies still see

tremendous opportunity in bringing innovative medicines to an increasingly affluent population and a country with

rapidly improving healthcare infrastructure. UHC implementation is likely to further expand this base of patients willing

to pay for innovative medicines as general access to medicines increase.

Price suppression expected for both generics and branded pharmaceuticals in the

long term

Although the volume of pharmaceutical products is expected to surge following the implementation of UHC, many

within the industry also expect to see the price-volume effect in action. Further exacerbating the price-volume effect is

the transformation of the system into a single-payer system, giving the government more power in reducing the prices

of drugs. Rising costs of medicines and healthcare services over the past few years has already run several local

healthcare schemes dry. As pharmaceutical products form the largest proportion of healthcare expenses, the

government is expected to fight to keep the costs of pharmaceuticals low.

Already, pharmaceutical companies are beginning to feel the effect of other reforms accompanying UHC

implementation. The launch of the e-catalog in 2013 opened the bidding process to the public, and has led to

reductions in prices of up to 40% or more. Furthermore, many within the industry expect stricter regulations in the

coming years to accompany a rise in the quality of healthcare services provided, raising costs for the pharmaceutical

industry. Hence, value growth from increased access to healthcare services under the UHC is expected to be less

optimistic in light of lower margins.

Universal Healthcare Coverage - Indonesia | 8

Opportunities are abound despite challenges faced in UHC implementation

Amidst the excitement of the implementation of UHC in one of the most populous countries in the world, the road to

providing full health coverage to all Indonesians is still filled with many challenges. Successful unification of provider

payment mechanisms under the BPJS would take significant cooperation from the various agencies, whilst the specifics

of what UHC would cover and premium rates have yet to be set. The collection of premiums would also be a significant

issue in a country consisting of 70% of informal workers spread across 10,000 plus islands dispersed over a wide area.

Furthermore, a chronic undersupply of medical infrastructure and healthcare manpower would limit the accessibility to

healthcare services despite the implementation of UHC. It is imperative that the Indonesian government looks upon

experiences locally (including Bali, Aceh, and Jakarta) as well as in other countries (such as South Korea, Taiwan, and

Thailand) in order to avoid pitfalls along the way.

Yet regardless of these challenges, UHC’s accompanying reforms and widespread effects are still expected to bring

about significant changes to the healthcare landscape in Indonesia. The bill implementing BPJS in the beginning of next

year is a positive sign of the country’s growing demand for healthcare amidst growing affluence within the general

population. Additionally, the country’s young population puts it in a position to enjoy demographic dividends in the

near future, allowing smoother implementation of any reform requiring large public investments. Consequently,

despite the industry’s expectations of a gradual lowering of margins, opportunities are still abound as general

accessibility and affordability to healthcare services rise rapidly. With this in mind, healthcare companies looking to

successfully navigate in Indonesia would need to be increasingly invested within this diverse country in order to take

full advantage of the potential that UHC will bring to the market.

Universal Healthcare Coverage - Indonesia | 9

About Clearstate

Clearstate (www.clearstate.com), a business of the Economist Intelligence Unit, is a highly specialized healthcare

research consulting firm that offers in-market insights and business intelligence complimented by strategic advisory to

help clients to implement pragmatic and innovative growth strategies to tap into opportunities in the emerging

economies.

Clearstate’s expertise extends across key healthcare and life sciences domain namely pharmaceuticals, medical devices,

hospital services and applied sciences.

Clearstate also offers:

Gateway Market Trackers The only quarterly updated market size and share by segmentation tracker for Healthcare markets in Asia. The Gateway

market trackers provide comprehensive coverage of imaging, in-vitro diagnostics and surgical device markets in value

and volume, by country.

Strategic Advisory Services Whether it is a market entry country scan, competitor benchmarking, channel optimization or customer insight

problem, we can tailor a solution that is driven by primary research and credibly synthesized through healthcare centric

analysis frameworks.

Contact:

Ivy Teh, Managing Director

Tel: +65 6303 5030