indra marked growth slowdown threatens to derail the ... · marked growth slowdown threatens to...

TRANSCRIPT

>> Employed by a non-US affiliate of MLPF&S and is not registered/qualified as a research analyst under the FINRA rules. Refer to "Other Important Disclosures" for information on certain BofA Merrill Lynch entities that take responsibility for this report in particular jurisdictions. BofA Merrill Lynch does and seeks to do business with issuers covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Refer to important disclosures on page 14 to 16. Analyst Certification on page 12. Price Objective Basis/Risk on page 12. 11608435

Indra

Marked growth slowdown threatens to derail the turnaround

Reiterate Rating: UNDERPERFORM | PO: 7.00 EUR | Price: 8.44 EUR Equity | 01 March 2016

As margins and FCF improve, growth veers off-track Indra's performance and outlook for 2016 are diverting from the turnaround plan set last year, as growth suffers from macro and political uncertainty. For Q4, there were some positives - margins came in slightly above cons. and a surprise working capital windfall delivered a FCF beat (see Table 1). However, organic growth declined sharply (0% 9M15 to -6% in Q4). The growth slowdown will also impact 2016, likely leaving revenue some way below where it was expected to be when management set out the turnaround plan (c.20% by 2018, we estimate). We think Indra is not yet past the worst: incremental restructuring charges, weak macro and election uncertainty in Spain will act as a drag on FY16 earnings and longer term FCF visibility remains low. We cut growth our forecasts by 7/11% (FY16/17 - see Table 3) and reduce our PO by 10% (based on 7% FY17E FCF yield, in-line with peers – see Table 2) to €7.00 (17% downside potential). Reiterate Underperform

Sharp deceleration in Spain and Latam As margins showed signs of recovery (6% Q4), Indra’s organic growth saw a sharp decline: growth fell from 0% 9M15 to -6% in Q4 (-8% excl. elections biz). Weak macro and operational issues caused LatAm growth to decline to -19% (vs. +3% 9M15), while political uncertainty and soft private sector demand caused a sudden halt to Spain’s recovery with Q4 sales declining -2% (vs. +11% 9M15). Furthermore, the FY16 outlook doesn’t look much brighter: Q4 order intake declined 29% and as a macro/political headwinds persists, management guided for organic growth decline in FY16 (BofAMLe FY16 growth: -4.7%, -8.2% incl. FX).

Few valuation supports, reiterate Underperform With the 2018 targets now looking increasingly tough to achieve (they were based on a +2.5 to 4.5% FY14-18 sales CAGR - we estimate Indra will be a cumulative 20%/€600m below this), the stock still looks expensive. If we add back the likely €50-60m for restructuring cash cost in 2016, underlying enterprise FCF is ~€130m this year (BofAMLe), implying a 7% yield. This is only modestly higher than Capgemini (6.2%) and far lower than several global peers with growth challenges, such as CSC/HP Enterprise. Estimates (Dec) (EUR) 2014A 2015A 2016E 2017E 2018E EPS (Adjusted Diluted) 0.76 (0.07) 0.52 0.68 0.84 EPS Change (YoY) -7.8% -109.6% 807.1% 30.5% 24.2% Dividend / Share 0 0 0 0 0

Valuation (Dec) 2014A 2015A 2016E 2017E 2018E P/E 11.1x NM 16.3x 12.5x 10.1x Dividend Yield 0% 0% 0% 0% 0% EV / EBITDA* 7.62x 15.6x 9.21x 7.97x 7.09x Free Cash Flow Yield* 5.43% -0.82% 4.78% 7.25% 9.25% * For full definitions of iQmethod SM measures, see page 13.

Key Changes

(EUR) Previous Current Price Obj. 7.80 7.00 2018E EPS 0.87 0.84 John P King, CFA >> Research Analyst MLI (UK) +44 20 7996 7265 [email protected] Tim Kindt >> Research Analyst MLI (UK) +44 20 7996 7201 [email protected] Sean Johnstone, CFA Specialist Sales MLI (UK) +44 20 7996 0157 [email protected] Stock Data

Price 8.44 EUR Price Objective 7.00 EUR Date Established 01-Mar-2016 Investment Opinion C-3-8 52-Week Range 7.61 EUR-11.53 EUR Mrkt Val / Shares Out (mn) 1,384 EUR / 163.9 Average Daily Value (mn) 13.36 USD Free Float 65.0% BofAML Ticker / Exchange ISMAF / SQC Bloomberg / Reuters IDR SM / IDR.MC ROE (2016E) 30.3% Net Dbt to Eqty (Dec2015A) 227.4%

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r m

lore

nte

o@

ind

ra.e

s.

2 Indra | 01 March 2016

iQprofile SM

Indra

Company Sector

Support Services Company Description

Indra is an IT services and industry solutions

company with revenues of c. €3bn. It has expertise

in air traffic control and defence technology.

2014E revenues will be c. 35% Spain (15% Spanish

public sector), 32% Latin America, 21%

Europe/USA and 13% Asia and the Middle East.

Investment Rationale

Indra could benefit significantly from a macro

recovery in Spain, as margins are a long way below

historical levels. However, cash generation

continues to lag P&L earnings, as working capital

has been weak. With long-run trailing FCF

generation of less than EUR60m, on average, the

stock looks overvalued and prices in a recovery,

while a lot more needs to be done. Stock Data

Price to Book Value 4.2x

Key Income Statement Data (Dec) 2014A 2015A 2016E 2017E 2018E (EUR Millions) Sales 2,938 2,850 2,616 2,582 2,640 EBITDA Adjusted 268 131 222 256 288 Depreciation & Amortization (64.2) (85.5) (65.4) (65.6) (70.5) EBIT Adjusted 204 45.1 157 191 218 Net Interest & Other Income (54.3) (56.2) (32.5) (27.4) (13.7) Tax Expense / Benefit 6.62 64.1 (15.6) (34.7) (44.1) Net Income (Adjusted) 138 (13.3) 93.9 123 152 Average Fully Diluted Shares Outstanding 181 181 181 182 182 Key Cash Flow Statement Data Net Income (Reported) (91.9) (641) 52.8 117 148 Depreciation & Amortization 64.2 85.5 65.4 65.6 70.5 Change in Working Capital 16.7 182 (9.90) (21.6) (24.6) Deferred Taxation Charge 0 0 0 0 0 Other CFO 151 398 11.0 (4.30) (5.65) Cash Flow from Operations 140 24.2 119 157 189 Capital Expenditure (56.7) (36.7) (46.2) (45.6) (46.7) (Acquisition) / Disposal of Investments (12.9) (5.15) 7.23 7.18 7.36 Other CFI 4.90 0 0 0 0 Cash Flow from Investing (64.7) (41.9) (38.9) (38.5) (39.4) Share Issue / (Repurchase) (6.90) (2.00) 0 0 0 Cost of Dividends Paid (55.8) (0.52) 0 0 0 Increase (decrease) debt (28.9) 84.7 0 0 0 Other CFF (54.1) (119) (32.5) (27.4) (13.7) Cash Flow from Financing (146) (37.0) (32.5) (27.4) (13.7) Total Cash Flow (CFO + CFI + CFF) (70.6) (54.7) 47.9 90.8 136 FX and other changes to cash 1.39 102 0 0 0 Change in Cash (69.2) 47.7 47.9 90.8 136 Change in Net Debt 40.3 37.0 (47.9) (90.8) (136) Net Debt 663 700 652 561 426 Key Balance Sheet Data Property, Plant & Equipment 127 137 130 122 113 Goodwill 583 470 470 470 470 Other Intangibles 290 289 277 265 250 Other Non-Current Assets 206 250 243 236 228 Trade Receivables 1,847 1,462 1,333 1,344 1,396 Cash & Equivalents 294 342 389 480 616 Other Current Assets 135 113 113 113 113 Total Assets 3,481 3,063 2,956 3,030 3,186 Long-Term Debt 826 962 962 962 962 Other Non-Current Liabilities 86.2 145 145 145 145 Short-Term Debt 131 79.4 79.4 79.4 79.4 Other Current Liabilities 1,485 1,569 1,430 1,420 1,447 Total Liabilities 2,528 2,755 2,617 2,606 2,633 Total Equity 954 308 339 424 553 Total Equity & Liabilities 3,481 3,063 2,956 3,030 3,186 Business Performance* Return On Capital Employed 11.6% 3.33% 11.6% 13.4% 13.9% Return On Equity 13.3% -2.15% 30.3% 33.2% 32.0% Operating Margin -1.45% -22.5% 3.69% 6.77% 7.64% Free Cash Flow (MM) 83.1 (12.6) 73.2 111 142 Quality of Earnings* Cash Realization Ratio 1.02x NM 1.27x 1.28x 1.24x Asset Replacement Ratio 0.88x 0.43x 0.71x 0.70x 0.66x Tax Rate 6.82% 9.08% 22.9% 22.9% 23.0% Net Debt/Equity 69.5% 227% 192% 132% 76.9% Interest Cover 3.75x 0.80x 4.82x 6.96x 15.9x * For full definitions of iQmethod SM measures, see page 13.

Indra | 01 March 2016 3

Results summary

Table 1: Results vs. our estimates & consensus Q4'15 ∆ (%)

Actual BofAML Cons Actual vs. BofAML Actual vs. Cons

Transport & Traffic 189 201 -6% Telecom & Media 68 127 -46% P.A. & Healthcare 119 76 55% Financial Services 114 117 -2% Energy & Industry 300 147 104% Security & Defence 187 159 18%

Total Revenue 781 826 812 -5.5% -3.9% % growth - reported -8.3% -3.0% -4.6% -531 bps -368 bps Adjusted Operating Profit € 47 € 62 € 45 -24.6% 3.3% % margins 6.0% 7.5% 5.6% -152 bps 41 bps Reported Operating Profit -€ 83 -€ 31 € 8 167.2% -1177.9% % margins -10.6% -3.8% 0.9% -687 bps -1157 bps Reported Net Income -€ 80 € 71 € 3 -212.1% -2452.9% Source: BofA Merrill Lynch Global Research estimates, Company compiled consensus

4 Indra | 01 March 2016

Chart 1: Organic revenue growth

Source: BofA Merrill Lynch Global Research

Chart 2: Book - to - bill ratio

Source: BofA Merrill Lynch Global Research

-8%-6%-4%-2%0%2%4%6%8%

10%12%14%

Q1'12

Q2'12

Q3'12

Q4'12

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

Q1'15

Q2'15

Q3'15

Q4'15

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Q1'10

Q2'10

Q3'10

Q4'10

Q1'11

Q2'11

Q3'11

Q4'11

Q1'12

Q2'12

Q3'12

Q4'12

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

Q1'15

Q2'15

Q3'15

Q4'15

Indra | 01 March 2016 5

Chart 3: Headcount growth (q/q, annualized)

Source: BofA Merrill Lynch Global Research

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%Q1

'10Q2

'10Q3

'10Q4

'10Q1

'11Q2

'11Q3

'11Q4

'11Q1

'12Q2

'12Q3

'12Q4

'12Q1

'13Q2

'13Q3

'13Q4

'13Q1

'14Q2

'14Q3

'14Q4

'14Q1

'15Q2

'15Q3

'15Q4

'15

6 Indra | 01 March 2016

Valuation

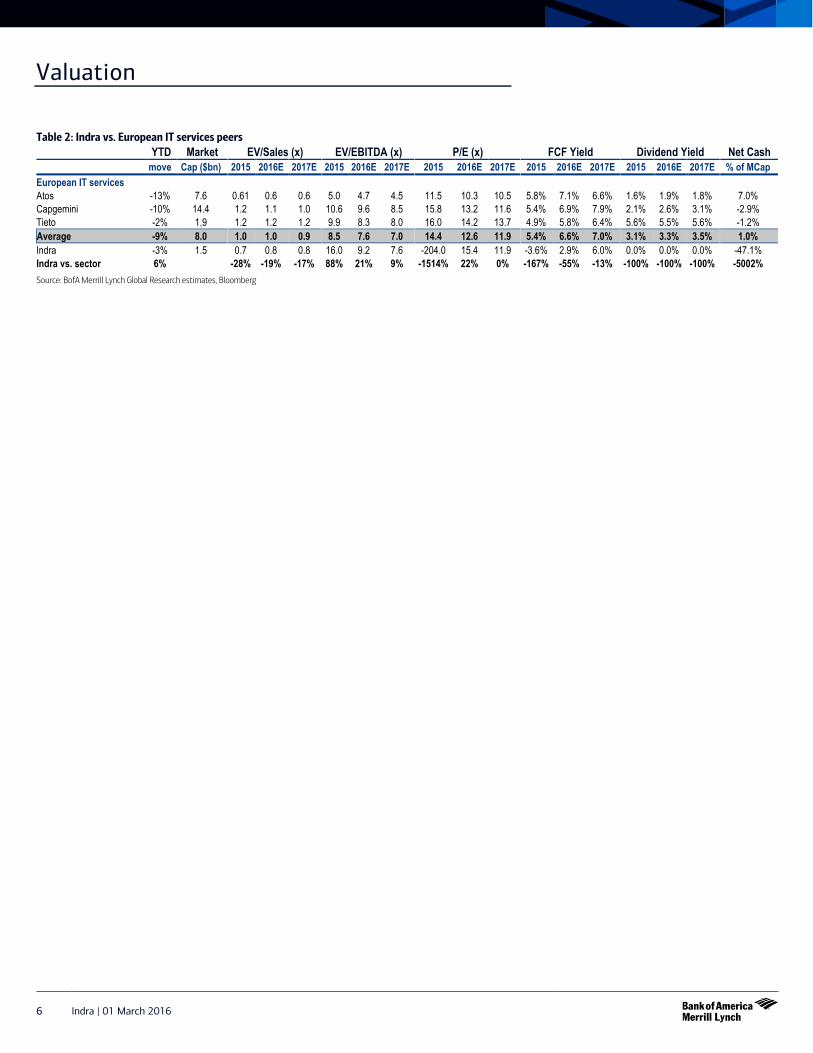

Table 2: Indra vs. European IT services peers

YTD Market EV/Sales (x) EV/EBITDA (x) P/E (x) FCF Yield Dividend Yield Net Cash move Cap ($bn) 2015 2016E 2017E 2015 2016E 2017E 2015 2016E 2017E 2015 2016E 2017E 2015 2016E 2017E % of MCap European IT services Atos -13% 7.6 0.61 0.6 0.6 5.0 4.7 4.5 11.5 10.3 10.5 5.8% 7.1% 6.6% 1.6% 1.9% 1.8% 7.0% Capgemini -10% 14.4 1.2 1.1 1.0 10.6 9.6 8.5 15.8 13.2 11.6 5.4% 6.9% 7.9% 2.1% 2.6% 3.1% -2.9% Tieto -2% 1.9 1.2 1.2 1.2 9.9 8.3 8.0 16.0 14.2 13.7 4.9% 5.8% 6.4% 5.6% 5.5% 5.6% -1.2% Average -9% 8.0 1.0 1.0 0.9 8.5 7.6 7.0 14.4 12.6 11.9 5.4% 6.6% 7.0% 3.1% 3.3% 3.5% 1.0% Indra -3% 1.5 0.7 0.8 0.8 16.0 9.2 7.6 -204.0 15.4 11.9 -3.6% 2.9% 6.0% 0.0% 0.0% 0.0% -47.1% Indra vs. sector 6% -28% -19% -17% 88% 21% 9% -1514% 22% 0% -167% -55% -13% -100% -100% -100% -5002% Source: BofA Merrill Lynch Global Research estimates, Bloomberg

Indra | 01 March 2016 7

Changes to estimates

Table 3: Changes to our estimates 2016E 2017E 2018E New estimates

Revenue € 2,616 € 2,582 € 2,640 % yoy growth -8.2% -1.3% 2.2%

EBITDA 222 256 288 Adjusted operating profit 157 191 218

% margin 6.0% 7.4% 8.2%

Reported operating profit 97 175 202 % margin 3.7% 6.8% 7.6%

Adjusted EPS € 0.55 € 0.71 € 0.87

% yoy growth -1427.3% 28.7% 23.1%

FCF to equity € 41 € 84 € 128

∆ (%)

Revenue -7.2% -11.0% -11.5% % yoy growth -56 bps -41 bps -6 bps

EBITDA -4.1% -4.5% -5.8% Adjusted operating profit -2.8% -2.1% -3.8%

% margin 28 bps 67 bps 66 bps

Reported operating profit -13.0% -2.2% -4.1% % margin -25 bps 60 bps 59 bps

Adjusted EPS 0.1% -0.3% -3.1%

% yoy growth -18861 bps -5 bps -36 bps

FCF to equity -18.1% -2.2% -3.2% Source: BofA Merrill Lynch Global Research estimates

8 Indra | 01 March 2016

Our estimates vs. consensus

Table 4: Our estimates vs. consensus 2016E ∆ (%) 2017E ∆ (%) BofAML Cons. BofAML vs Cons BofAML Cons. BofAML vs Cons

Revenue € 2,616 € 2,885 -9.3% € 2,582 € 2,964 -12.9% % yoy growth -8.2% 0.0% -819 bps -1.3% 2.8% -406 bps Adjusted Operating Profit € 157 € 180 -12.9% € 191 € 241 -20.8% Margin 6.0% 6.2% -25 bps 7.4% 8.1% -74 bps Adjusted diluted EPS € 0.55 € 0.61 -9.3% € 0.71 € 0.83 -15.1% FCF to equity € 41 € 87 -53.2% € 84 € 170 -50.9% Net debt € 652 € 876 -25.6% € 561 € 760 -26.2% Source: BofA Merrill Lynch Global Research estimates, Bloomberg consensus

Indra | 01 March 2016 9

Table 5: P&L forecast (€m) Q1'15 Q2'15 Q3'15 Q4'15 Q1'16E Q2'16E Q3'16E Q4'16E 2013 2014 2015 2016E 2017E 2018E Revenue 702 707 660 781 695 704 675 542 2,914 2,938 2,850 2,616 2,582 2,640

% yoy growth -4% -5% 8% -8% -1.1% -0.4% 2.2% -30.6% -1% 1% -3% -8% -1% 2% Organic growth -5% -5% 12% -5% 4.6% 4.5% 4.9% -29.3% 2% 5% -2% -5% -1% 2%

Other Income 33 15 17 22 33 15 17 22 75 93 86 86 86 86 Materials consumed and other operating expenses 332 342 318 376 322 331 315 233 1,333 1,354 1,369 1,202 1,150 1,148

% of revenue 47% 48% 48% 48% 46% 47% 47% 43% 46% 46% 48% 46% 45% 43% Personnel expenses 369 393 315 359 365 392 322 200 1,454 1,406 1,436 1,279 1,262 1,290

% of revenue 53% 56% 48% 46% 53% 56% 48% 37% 50% 48% 50% 49% 49% 49% Results on non-current assets 0 1 0 0 0 0 0 0 -76 4 1 0 0 0 Gross Operating Profit (EBITDA) 34 -14 43 67 41 -4 54 131 278 268 131 222 256 288

% yoy growth -52% -119% -23% 6% 20% -70% 25% 94% -7% -4% -51% 70% 16% 12% EBITDA margin 10% 9% 5% 8% 10% 11% YoY -1% 0% -5% 4% 1% 1%

Depreciation 31 14 20 21 32 14 20 -1 52 64 86 65 66 70 Adjusted Operating Profit 3 -28 23 46 10 -19 34 132 226 204 45 157 191 218

% margin 0% -4% 4% 6% 1% -3% 5% 24% 8% 7% 2% 6% 7% 8%

Financial results -13 -15 -16 -4 -10 -24 -22 24 -64 -54 -56 -33 -27 -14 Share of profits (losses) of associates and other investees -2 -2 -2 -3 1 1 1 1 12 0 -8 4 4 4 Adjusted Profit before taxation -11 -44 6 40 0 -42 13 157 175 149 -19 128 167 208 Taxation -5 1 -1 11 0 1 -3 -33 -36 -10 5 -35 -45 -56

% tax rate 47% -3% -23% 26% 26% -3% -23% -21% -20% -7% -28% -27% -27% -27% Net Profit for the period -17 -43 5 51 0 -40 10 124 139 139 -14 93 122 152 Minority interest 0 1 -1 1 0 1 -1 1 -1 -2 1 0 0 0 Consolidated Income -17 -42 4 52 0 -40 9 124 138 138 -13 94 123 152 Adjusted EPS (Basic) -0.10 -0.26 0.02 0.32 0.00 -0.24 0.05 0.75 0.84 0.84 -0.08 0.57 0.75 0.93 Adjusted EPS (Diluted) -0.09 -0.23 0.02 0.34 0.06 -0.18 0.08 0.61 0.82 0.76 -0.04 0.55 0.71 0.87 WASO (Basic) 164 164 164 164 164 164 164 165 164 164 164 164 164 164 WASO (Diluted) 181 181 181 181 181 181 181 182 168 181 181 181 182 182 Dividend Dividends 0 0 0 0 0 0 0 0 56 0 0 0 0 0 DPS 0.34 0.00 0.00 0.00 0.00 0.00

% payout ratio 49% 0% 0% 0% 0% 0% Source: BofA Merrill Lynch Global Research estimates

10 Indra | 01 March 2016

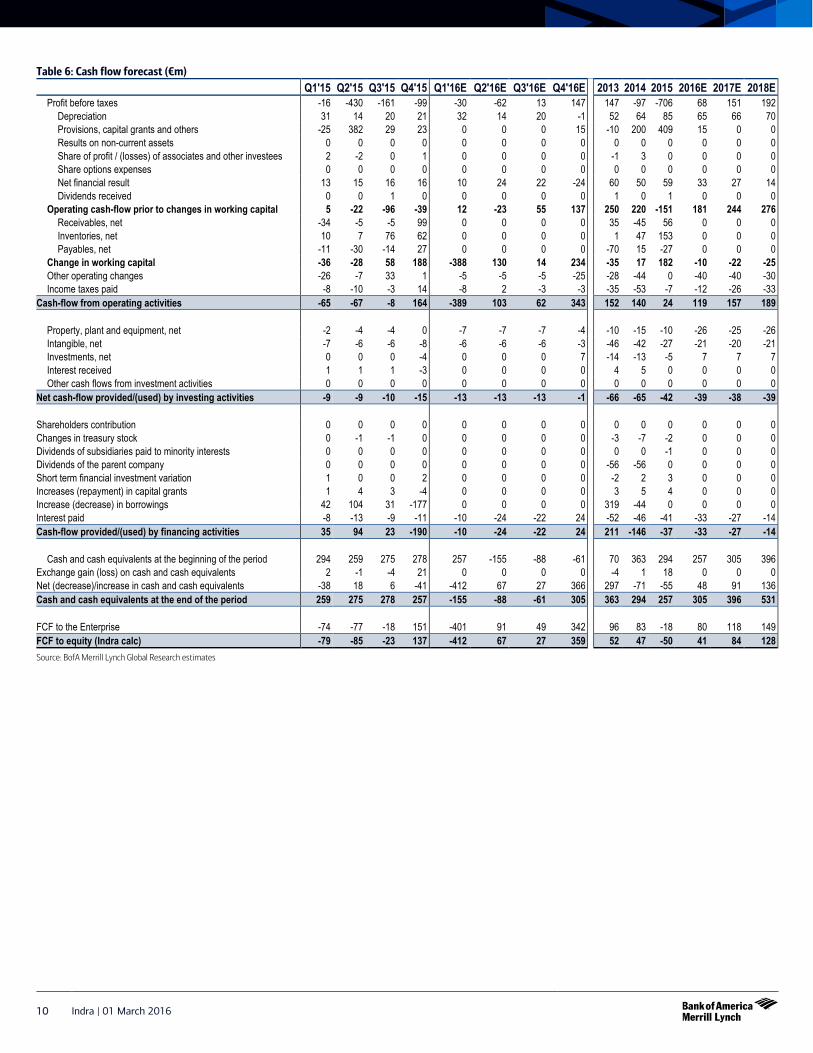

Table 6: Cash flow forecast (€m) Q1'15 Q2'15 Q3'15 Q4'15 Q1'16E Q2'16E Q3'16E Q4'16E 2013 2014 2015 2016E 2017E 2018E

Profit before taxes -16 -430 -161 -99 -30 -62 13 147 147 -97 -706 68 151 192 Depreciation 31 14 20 21 32 14 20 -1 52 64 85 65 66 70 Provisions, capital grants and others -25 382 29 23 0 0 0 15 -10 200 409 15 0 0 Results on non-current assets 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Share of profit / (losses) of associates and other investees 2 -2 0 1 0 0 0 0 -1 3 0 0 0 0 Share options expenses 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Net financial result 13 15 16 16 10 24 22 -24 60 50 59 33 27 14 Dividends received 0 0 1 0 0 0 0 0 1 0 1 0 0 0

Operating cash-flow prior to changes in working capital 5 -22 -96 -39 12 -23 55 137 250 220 -151 181 244 276 Receivables, net -34 -5 -5 99 0 0 0 0 35 -45 56 0 0 0 Inventories, net 10 7 76 62 0 0 0 0 1 47 153 0 0 0 Payables, net -11 -30 -14 27 0 0 0 0 -70 15 -27 0 0 0

Change in working capital -36 -28 58 188 -388 130 14 234 -35 17 182 -10 -22 -25 Other operating changes -26 -7 33 1 -5 -5 -5 -25 -28 -44 0 -40 -40 -30 Income taxes paid -8 -10 -3 14 -8 2 -3 -3 -35 -53 -7 -12 -26 -33

Cash-flow from operating activities -65 -67 -8 164 -389 103 62 343 152 140 24 119 157 189

Property, plant and equipment, net -2 -4 -4 0 -7 -7 -7 -4 -10 -15 -10 -26 -25 -26 Intangible, net -7 -6 -6 -8 -6 -6 -6 -3 -46 -42 -27 -21 -20 -21 Investments, net 0 0 0 -4 0 0 0 7 -14 -13 -5 7 7 7 Interest received 1 1 1 -3 0 0 0 0 4 5 0 0 0 0 Other cash flows from investment activities 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Net cash-flow provided/(used) by investing activities -9 -9 -10 -15 -13 -13 -13 -1 -66 -65 -42 -39 -38 -39 Shareholders contribution 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Changes in treasury stock 0 -1 -1 0 0 0 0 0 -3 -7 -2 0 0 0 Dividends of subsidiaries paid to minority interests 0 0 0 0 0 0 0 0 0 0 -1 0 0 0 Dividends of the parent company 0 0 0 0 0 0 0 0 -56 -56 0 0 0 0 Short term financial investment variation 1 0 0 2 0 0 0 0 -2 2 3 0 0 0 Increases (repayment) in capital grants 1 4 3 -4 0 0 0 0 3 5 4 0 0 0 Increase (decrease) in borrowings 42 104 31 -177 0 0 0 0 319 -44 0 0 0 0 Interest paid -8 -13 -9 -11 -10 -24 -22 24 -52 -46 -41 -33 -27 -14 Cash-flow provided/(used) by financing activities 35 94 23 -190 -10 -24 -22 24 211 -146 -37 -33 -27 -14

Cash and cash equivalents at the beginning of the period 294 259 275 278 257 -155 -88 -61 70 363 294 257 305 396 Exchange gain (loss) on cash and cash equivalents 2 -1 -4 21 0 0 0 0 -4 1 18 0 0 0 Net (decrease)/increase in cash and cash equivalents -38 18 6 -41 -412 67 27 366 297 -71 -55 48 91 136 Cash and cash equivalents at the end of the period 259 275 278 257 -155 -88 -61 305 363 294 257 305 396 531 FCF to the Enterprise -74 -77 -18 151 -401 91 49 342 96 83 -18 80 118 149 FCF to equity (Indra calc) -79 -85 -23 137 -412 67 27 359 52 47 -50 41 84 128 Source: BofA Merrill Lynch Global Research estimates

Indra | 01 March 2016 11

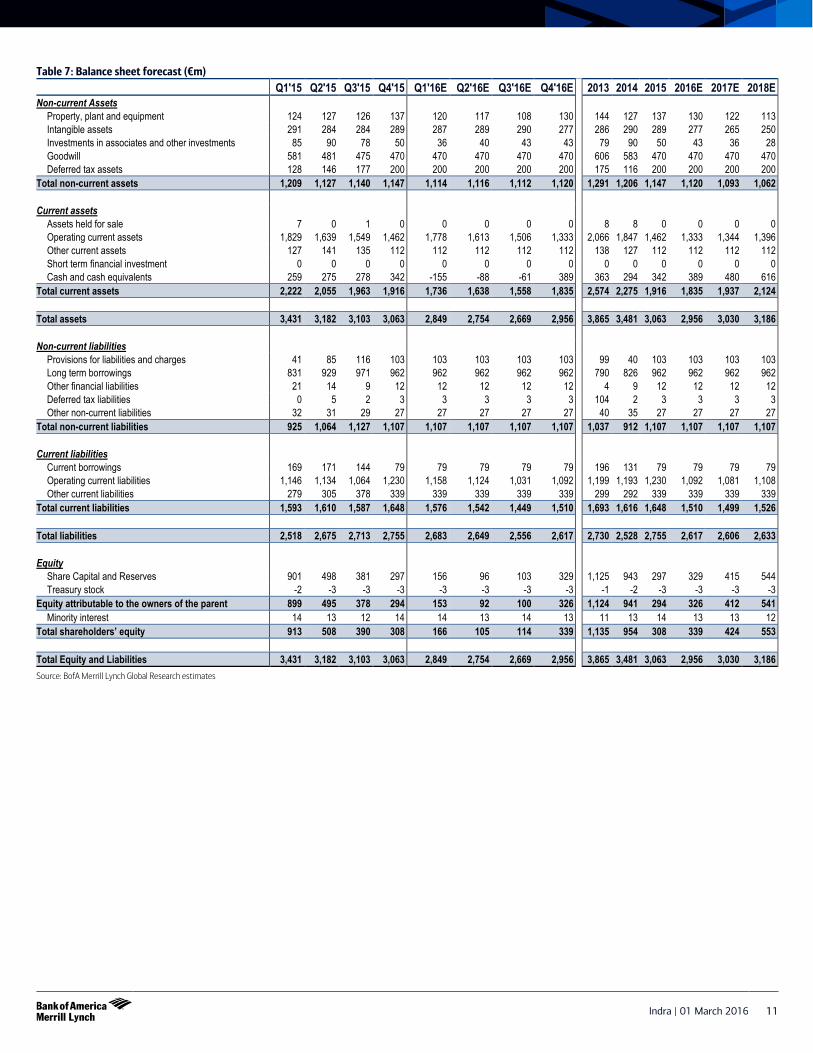

Table 7: Balance sheet forecast (€m) Q1'15 Q2'15 Q3'15 Q4'15 Q1'16E Q2'16E Q3'16E Q4'16E 2013 2014 2015 2016E 2017E 2018E Non-current Assets

Property, plant and equipment 124 127 126 137 120 117 108 130 144 127 137 130 122 113 Intangible assets 291 284 284 289 287 289 290 277 286 290 289 277 265 250 Investments in associates and other investments 85 90 78 50 36 40 43 43 79 90 50 43 36 28 Goodwill 581 481 475 470 470 470 470 470 606 583 470 470 470 470 Deferred tax assets 128 146 177 200 200 200 200 200 175 116 200 200 200 200

Total non-current assets 1,209 1,127 1,140 1,147 1,114 1,116 1,112 1,120 1,291 1,206 1,147 1,120 1,093 1,062 Current assets

Assets held for sale 7 0 1 0 0 0 0 0 8 8 0 0 0 0 Operating current assets 1,829 1,639 1,549 1,462 1,778 1,613 1,506 1,333 2,066 1,847 1,462 1,333 1,344 1,396 Other current assets 127 141 135 112 112 112 112 112 138 127 112 112 112 112 Short term financial investment 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Cash and cash equivalents 259 275 278 342 -155 -88 -61 389 363 294 342 389 480 616

Total current assets 2,222 2,055 1,963 1,916 1,736 1,638 1,558 1,835 2,574 2,275 1,916 1,835 1,937 2,124 Total assets 3,431 3,182 3,103 3,063 2,849 2,754 2,669 2,956 3,865 3,481 3,063 2,956 3,030 3,186 Non-current liabilities

Provisions for liabilities and charges 41 85 116 103 103 103 103 103 99 40 103 103 103 103 Long term borrowings 831 929 971 962 962 962 962 962 790 826 962 962 962 962 Other financial liabilities 21 14 9 12 12 12 12 12 4 9 12 12 12 12 Deferred tax liabilities 0 5 2 3 3 3 3 3 104 2 3 3 3 3 Other non-current liabilities 32 31 29 27 27 27 27 27 40 35 27 27 27 27

Total non-current liabilities 925 1,064 1,127 1,107 1,107 1,107 1,107 1,107 1,037 912 1,107 1,107 1,107 1,107 Current liabilities

Current borrowings 169 171 144 79 79 79 79 79 196 131 79 79 79 79 Operating current liabilities 1,146 1,134 1,064 1,230 1,158 1,124 1,031 1,092 1,199 1,193 1,230 1,092 1,081 1,108 Other current liabilities 279 305 378 339 339 339 339 339 299 292 339 339 339 339

Total current liabilities 1,593 1,610 1,587 1,648 1,576 1,542 1,449 1,510 1,693 1,616 1,648 1,510 1,499 1,526 Total liabilities 2,518 2,675 2,713 2,755 2,683 2,649 2,556 2,617 2,730 2,528 2,755 2,617 2,606 2,633 Equity

Share Capital and Reserves 901 498 381 297 156 96 103 329 1,125 943 297 329 415 544 Treasury stock -2 -3 -3 -3 -3 -3 -3 -3 -1 -2 -3 -3 -3 -3

Equity attributable to the owners of the parent 899 495 378 294 153 92 100 326 1,124 941 294 326 412 541 Minority interest 14 13 12 14 14 13 14 13 11 13 14 13 13 12

Total shareholders’ equity 913 508 390 308 166 105 114 339 1,135 954 308 339 424 553 Total Equity and Liabilities 3,431 3,182 3,103 3,063 2,849 2,754 2,669 2,956 3,865 3,481 3,063 2,956 3,030 3,186 Source: BofA Merrill Lynch Global Research estimates

12 Indra | 01 March 2016

Price objective basis & risk Indra (ISMAF) Our price objective for Indra is €7.0, based on a 2017 FCF yield of 7%, inline with peers growing at similar rates. Downside risks to our price objective are: (1) that the nascent recovery in the Spanish economy stalls, (2) that Indra is not successful in growing its solutions business in international markets, and (3) that demand in its defensive divisions slows. Upside risks are if: (1) Indra is faster at expanding overseas, and (2) produces better cash conversion than our estimates. Analyst Certification I, John P King, CFA, hereby certify that the views expressed in this research report accurately reflect my personal views about the subject securities and issuers. I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendations or view expressed in this research report. EMEA - Technology Coverage Cluster

Investment rating Company BofA Merrill Lynch ticker Bloomberg symbol Analyst

BUY ARM Holdings PLC ARMHF ARM LN Kai Korschelt ARM Holdings PLC ARMH ARMH US Kai Korschelt ASML Holding N.V. ASMLF ASML NA Kai Korschelt ASML Holding N.V. ASML ASML US Kai Korschelt Dassault Systemes DASTF DSY FP John P King, CFA Dassault Systemes DASTY DASTY US John P King, CFA Dialog Semiconductor plc DLGNF DLG GR Adithya Metuku, CFA Ericsson ERIXF ERICB SS Kai Korschelt Ericsson ERIC ERIC US Kai Korschelt Infineon Technologies AG IFNNF IFX GR Adithya Metuku, CFA Infineon Technologies AG IFNNY IFNNY US Adithya Metuku, CFA Just Eat plc JSTLF JE/ LN John P King, CFA Sage SGGEF SGE LN Tim Kindt SAP AG SAPGF SAP GR John P King, CFA SAP AG SAP SAP US John P King, CFA Travelport TVPT TVPT US John P King, CFA Windeln.de XWKTF WDL GR John P King, CFA Wirecard AG WRCDF WDI GY Adithya Metuku, CFA Worldpay Group plc WDDYF WPG LN Adithya Metuku, CFA NEUTRAL Amadeus AMADF AMS SM John P King, CFA Capgemini CAPMF CAP FP John P King, CFA Gemalto N.V. GTOFF GTO NA Adithya Metuku, CFA Nokia NOKBF NOKIA FH Kai Korschelt Nokia NOK NOK US Kai Korschelt Rocket Internet XIFKF RKET GR John P King, CFA STMicroelectronics NV STMEF STM FP Adithya Metuku, CFA STMicroelectronics NV STM STM US Adithya Metuku, CFA Worldline XLDSF WLN FP John P King, CFA UNDERPERFORM Atos AEXAF ATO FP John P King, CFA Indra ISMAF IDR SM John P King, CFA Ingenico S.A. INGIF ING FP Adithya Metuku, CFA Micro Focus MCFUF MCRO LN Tim Kindt

Indra | 01 March 2016 13

iQmethod SM Measures Definitions Business Performance Numerator Denominator Return On Capital Employed NOPAT = (EBIT + Interest Income) * (1 - Tax Rate) + Goodwill Amortization Total Assets – Current Liabilities + ST Debt + Accumulated Goodwill

Amortization Return On Equity Net Income Shareholders’ Equity Operating Margin Operating Profit Sales Earnings Growth Expected 5-Year CAGR From Latest Actual N/A Free Cash Flow Cash Flow From Operations – Total Capex N/A Quality of Earnings Cash Realization Ratio Cash Flow From Operations Net Income Asset Replacement Ratio Capex Depreciation Tax Rate Tax Charge Pre-Tax Income Net Debt-To-Equity Ratio Net Debt = Total Debt, Less Cash & Equivalents Total Equity Interest Cover EBIT Interest Expense Valuation Toolkit Price / Earnings Ratio Current Share Price Diluted Earnings Per Share (Basis As Specified) Price / Book Value Current Share Price Shareholders’ Equity / Current Basic Shares Dividend Yield Annualised Declared Cash Dividend Current Share Price Free Cash Flow Yield Cash Flow From Operations – Total Capex Market Cap. = Current Share Price * Current Basic Shares Enterprise Value / Sales EV = Current Share Price * Current Shares + Minority Equity + Net Debt +

Other LT Liabilities Sales

EV / EBITDA Enterprise Value Basic EBIT + Depreciation + Amortization

iQmethod SMis the set of BofA Merrill Lynch standard measures that serve to maintain global consistency under three broad headings: Business Performance, Quality of Earnings, and validations. The key features of iQmethod are: A consistently structured, detailed, and transparent methodology. Guidelines to maximize the effectiveness of the comparative valuation process, and to identify some common pitfalls. iQdatabase ® is our real-time global research database that is sourced directly from our equity analysts’ earnings models and includes forecasted as well as historical data for income statements, balance sheets, and cash flow statements for companies covered by BofA Merrill Lynch. iQprofile SM, iQmethod SM are service marks of Bank of America Corporation.iQdatabase ®is a registered service mark of Bank of America Corporation.

14 Indra | 01 March 2016

Disclosures Important Disclosures ISMAF Price Chart

0

3

6

9

12

15

1-Jan-14 1-Jan-15 1-Jan-16

B: Buy, N: Neutral, U: Underperform, PO: Price Objective, NA: No longer valid, NR: No RatingISMAF

1-Feb USriraman

PO:EUR9.501-Mar

PO:EUR9.00

10-Dec BKing

PO:EUR156-Jan

PO:EUR16

30-Jul PO:EUR15

9-Oct PO:EUR14

31-Oct NPO:EUR10

12-Dec PO:EUR9.20

12-Jan UPO:EUR7.10

2-Mar PO:EUR7.00

14-Jul PO:EUR9.00

31-Jul PO:EUR8.50

11-Jan PO:EUR7.80

Review Restricted No Coverage

The Investment Opinion System is contained at the end of the report under the heading "Fundamental Equity Opinion Key". Dark grey shading indicates the security is restricted with the opinion suspended. Medium grey shading indicates the security is under review with the opinion withdrawn. Light grey shading indicates the security is not covered. Chart is current as of January 31, 2016 or such later date as indicated. Equity Investment Rating Distribution: Services Group (as of 31 Dec 2015) Coverage Universe Count Percent Inv. Banking Relationships* Count Percent Buy 6 54.55% Buy 5 83.33% Hold 1 9.09% Hold 1 100.00% Sell 4 36.36% Sell 4 100.00% Equity Investment Rating Distribution: Global Group (as of 31 Dec 2015) Coverage Universe Count Percent Inv. Banking Relationships* Count Percent Buy 1673 50.16% Buy 1244 74.36% Hold 777 23.30% Hold 545 70.14% Sell 885 26.54% Sell 533 60.23% * Issuers that were investment banking clients of BofA Merrill Lynch or one of its affiliates within the past 12 months. For purposes of this Investment Rating Distribution, the coverage universe includes only stocks. A stock rated Neutral is included as a Hold, and a stock rated Underperform is included as a Sell.

FUNDAMENTAL EQUITY OPINION KEY: Opinions include a Volatility Risk Rating, an Investment Rating and an Income Rating. VOLATILITY RISK RATINGS, indicators of potential price fluctuation, are: A - Low, B - Medium and C - High. INVESTMENT RATINGS reflect the analyst’s assessment of a stock’s: (i) absolute total return potential and (ii) attractiveness for investment relative to other stocks within its Coverage Cluster (defined below). There are three investment ratings: 1 - Buy stocks are expected to have a total return of at least 10% and are the most attractive stocks in the coverage cluster; 2 - Neutral stocks are expected to remain flat or increase in value and are less attractive than Buy rated stocks and 3 - Underperform stocks are the least attractive stocks in a coverage cluster. Analysts assign investment ratings considering, among other things, the 0-12 month total return expectation for a stock and the firm’s guidelines for ratings dispersions (shown in the table below). The current price objective for a stock should be referenced to better understand the total return expectation at any given time. The price objective reflects the analyst’s view of the potential price appreciation (depreciation). Investment rating Total return expectation (within 12-month period of date of initial rating) Ratings dispersion guidelines for coverage cluster*

Buy ≥ 10% ≤ 70% Neutral ≥ 0% ≤ 30%

Underperform N/A ≥ 20% * Ratings dispersions may vary from time to time where BofA Merrill Lynch Research believes it better reflects the investment prospects of stocks in a Coverage Cluster.

INCOME RATINGS, indicators of potential cash dividends, are: 7 - same/higher (dividend considered to be secure), 8 - same/lower (dividend not considered to be secure) and 9 - pays no cash dividend. Coverage Cluster is comprised of stocks covered by a single analyst or two or more analysts sharing a common industry, sector, region or other classification(s). A stock’s coverage cluster is included in the most recent BofA Merrill Lynch report referencing the stock. Price charts for the securities referenced in this research report are available at http://pricecharts.baml.com, or call 1-800-MERRILL to have them mailed. The issuer is or was, within the last 12 months, an investment banking client of MLPF&S and/or one or more of its affiliates: Indra. MLPF&S or an affiliate has received compensation from the issuer for non-investment banking services or products within the past 12 months: Indra. The issuer is or was, within the last 12 months, a non-securities business client of MLPF&S and/or one or more of its affiliates: Indra. In the US, retail sales and/or distribution of this report may be made only in states where these securities are exempt from registration or have been qualified for sale: Indra. MLPF&S or an affiliate expects to receive or intends to seek compensation for investment banking services from this issuer or an affiliate of the issuer within the next three months: Indra. The issuer is or was, within the last 12 months, a securities business client (non-investment banking) of MLPF&S and/or one or more of its affiliates: Indra. BofA Merrill Lynch Research personnel (including the analyst(s) responsible for this report) receive compensation based upon, among other factors, the overall profitability of Bank of America Corporation, including profits derived from investment banking revenues.

Other Important Disclosures Officers of MLPF&S or one or more of its affiliates (other than research analysts) may have a financial interest in securities of the issuer(s) or in related investments. From time to time research analysts conduct site visits of covered issuers. BofA Merrill Lynch policies prohibit research analysts from accepting payment or reimbursement for travel expenses

Indra | 01 March 2016 15

from the issuer for such visits. BofA Merrill Lynch Global Research policies relating to conflicts of interest are described at http://go.bofa.com/coi. "BofA Merrill Lynch" includes Merrill Lynch, Pierce, Fenner & Smith Incorporated ("MLPF&S") and its affiliates. Investors should contact their BofA Merrill Lynch representative or Merrill Lynch Global Wealth Management financial advisor if they have questions concerning this report. "BofA Merrill Lynch" and "Merrill Lynch" are each global brands for BofA Merrill Lynch Global Research. Information relating to Non-US affiliates of BofA Merrill Lynch and Distribution of Affiliate Research Reports: MLPF&S distributes, or may in the future distribute, research reports of the following non-US affiliates in the US (short name: legal name): BAMLI Paris: Bank of America Merrill Lynch International Limited, Paris Branch; BAMLI Frankfurt: Bank of America Merrill Lynch International Limited, Frankfurt Branch; Merrill Lynch (South Africa): Merrill Lynch South Africa (Pty) Ltd.; Merrill Lynch (Milan): Merrill Lynch International Bank Limited; MLI (UK): Merrill Lynch International; Merrill Lynch (Australia): Merrill Lynch Equities (Australia) Limited; Merrill Lynch (Hong Kong): Merrill Lynch (Asia Pacific) Limited; Merrill Lynch (Singapore): Merrill Lynch (Singapore) Pte Ltd.; Merrill Lynch (Canada): Merrill Lynch Canada Inc; Merrill Lynch (Mexico): Merrill Lynch Mexico, SA de CV, Casa de Bolsa; Merrill Lynch (Argentina): Merrill Lynch Argentina SA; Merrill Lynch (Japan): Merrill Lynch Japan Securities Co., Ltd.; Merrill Lynch (Seoul): Merrill Lynch International Incorporated (Seoul Branch); Merrill Lynch (Taiwan): Merrill Lynch Securities (Taiwan) Ltd.; DSP Merrill Lynch (India): DSP Merrill Lynch Limited; PT Merrill Lynch (Indonesia): PT Merrill Lynch Indonesia; Merrill Lynch (Israel): Merrill Lynch Israel Limited; Merrill Lynch (Russia): OOO Merrill Lynch Securities, Moscow; Merrill Lynch (Turkey I.B.): Merrill Lynch Yatirim Bank A.S.; Merrill Lynch (Turkey Broker): Merrill Lynch Menkul Değerler A.Ş.; Merrill Lynch (DIFC): Merrill Lynch International (DIFC Branch); MLPF&S (Zurich rep. office): MLPF&S Incorporated Zurich representative office; Merrill Lynch (Spain): Merrill Lynch Capital Markets Espana, S.A.S.V.; Merrill Lynch (Brazil): Bank of America Merrill Lynch Banco Multiplo S.A.; Merrill Lynch KSA Company, Merrill Lynch Kingdom of Saudi Arabia Company. This research report has been approved for publication and is distributed in the United Kingdom to professional clients and eligible counterparties (as each is defined in the rules of the Financial Conduct Authority and the Prudential Regulation Authority) by Merrill Lynch International and Bank of America Merrill Lynch International Limited, which are authorized by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority, and is distributed in the United Kingdom to retail clients (as defined in the rules of the Financial Conduct Authority and the Prudential Regulation Authority) by Merrill Lynch International Bank Limited, London Branch, which is authorised by the Central Bank of Ireland and subject to limited regulation by the Financial Conduct Authority and Prudential Regulation Authority - details about the extent of our regulation by the Financial Conduct Authority and Prudential Regulation Authority are available from us on request; has been considered and distributed in Japan by Merrill Lynch Japan Securities Co., Ltd., a registered securities dealer under the Financial Instruments and Exchange Act in Japan; is distributed in Hong Kong by Merrill Lynch (Asia Pacific) Limited, which is regulated by the Hong Kong SFC and the Hong Kong Monetary Authority is issued and distributed in Taiwan by Merrill Lynch Securities (Taiwan) Ltd.; is issued and distributed in India by DSP Merrill Lynch Limited; and is issued and distributed in Singapore to institutional investors and/or accredited investors (each as defined under the Financial Advisers Regulations) by Merrill Lynch International Bank Limited (Merchant Bank) and Merrill Lynch (Singapore) Pte Ltd. (Company Registration No.’s F 06872E and 198602883D respectively). Merrill Lynch International Bank Limited (Merchant Bank) and Merrill Lynch (Singapore) Pte Ltd. are regulated by the Monetary Authority of Singapore. Bank of America N.A., Australian Branch (ARBN 064 874 531), AFS License 412901 (BANA Australia) and Merrill Lynch Equities (Australia) Limited (ABN 65 006 276 795), AFS License 235132 (MLEA) distributes this report in Australia only to 'Wholesale' clients as defined by s.761G of the Corporations Act 2001. With the exception of BANA Australia, neither MLEA nor any of its affiliates involved in preparing this research report is an Authorised Deposit-Taking Institution under the Banking Act 1959 nor regulated by the Australian Prudential Regulation Authority. No approval is required for publication or distribution of this report in Brazil and its local distribution is made by Bank of America Merrill Lynch Banco Múltiplo S.A. in accordance with applicable regulations. Merrill Lynch (DIFC) is authorized and regulated by the Dubai Financial Services Authority (DFSA). Research reports prepared and issued by Merrill Lynch (DIFC) are prepared and issued in accordance with the requirements of the DFSA conduct of business rules. BAMLI Frankfurt distributes this report in Germany. BAMLI Frankfurt is regulated by BaFin. This research report has been prepared and issued by MLPF&S and/or one or more of its non-US affiliates. MLPF&S is the distributor of this research report in the US and accepts full responsibility for research reports of its non-US affiliates distributed to MLPF&S clients in the US. Any US person receiving this research report and wishing to effect any transaction in any security discussed in the report should do so through MLPF&S and not such foreign affiliates. Hong Kong recipients of this research report should contact Merrill Lynch (Asia Pacific) Limited in respect of any matters relating to dealing in securities or provision of specific advice on securities. Singapore recipients of this research report should contact Merrill Lynch International Bank Limited (Merchant Bank) and/or Merrill Lynch (Singapore) Pte Ltd in respect of any matters arising from, or in connection with, this research report. General Investment Related Disclosures: Taiwan Readers: Neither the information nor any opinion expressed herein constitutes an offer or a solicitation of an offer to transact in any securities or other financial instrument. No part of this report may be used or reproduced or quoted in any manner whatsoever in Taiwan by the press or any other person without the express written consent of BofA Merrill Lynch. This research report provides general information only. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer, to buy or sell any securities or other financial instrument or any derivative related to such securities or instruments (e.g., options, futures, warrants, and contracts for differences). This report is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation and the particular needs of any specific person. Investors should seek financial advice regarding the appropriateness of investing in financial instruments and implementing investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Any decision to purchase or subscribe for securities in any offering must be based solely on existing public information on such security or the information in the prospectus or other offering document issued in connection with such offering, and not on this report. Securities and other financial instruments discussed in this report, or recommended, offered or sold by Merrill Lynch, are not insured by the Federal Deposit Insurance Corporation and are not deposits or other obligations of any insured depository institution (including, Bank of America, N.A.). Investments in general and, derivatives, in particular, involve numerous risks, including, among others, market risk, counterparty default risk and liquidity risk. No security, financial instrument or derivative is suitable for all investors. In some cases, securities and other financial instruments may be difficult to value or sell and reliable information about the value or risks related to the security or financial instrument may be difficult to obtain. Investors should note that income from such securities and other financial instruments, if any, may fluctuate and that price or value of such securities and instruments may rise or fall and, in some cases, investors may lose their entire principal investment. Past performance is not necessarily a guide to future performance. Levels and basis for taxation may change. This report may contain a short-term trading idea or recommendation, which highlights a specific near-term catalyst or event impacting the issuer or the market that is anticipated to have a short-term price impact on the equity securities of the issuer. Short-term trading ideas and recommendations are different from and do not affect a stock's fundamental equity rating, which reflects both a longer term total return expectation and attractiveness for investment relative to other stocks within its Coverage Cluster. Short-term trading ideas and recommendations may be more or less positive than a stock's fundamental equity rating. BofA Merrill Lynch is aware that the implementation of the ideas expressed in this report may depend upon an investor's ability to "short" securities or other financial instruments and that such action may be limited by regulations prohibiting or restricting "shortselling" in many jurisdictions. Investors are urged to seek advice regarding the applicability of such regulations prior to executing any short idea contained in this report. Foreign currency rates of exchange may adversely affect the value, price or income of any security or financial instrument mentioned in this report. Investors in such securities and instruments, including ADRs, effectively assume currency risk. UK Readers: The protections provided by the U.K. regulatory regime, including the Financial Services Scheme, do not apply in general to business coordinated by BofA Merrill Lynch entities located outside of the United Kingdom. BofA Merrill Lynch Global Research policies relating to conflicts of interest are described at http://go.bofa.com/coi. Officers of MLPF&S or one or more of its affiliates (other than research analysts) may have a financial interest in securities of the issuer(s) or in related investments. MLPF&S or one of its affiliates is a regular issuer of traded financial instruments linked to securities that may have been recommended in this report. MLPF&S or one of its affiliates may, at any time, hold a trading position (long or short) in the securities and financial instruments discussed in this report. BofA Merrill Lynch, through business units other than BofA Merrill Lynch Global Research, may have issued and may in the future issue trading ideas or recommendations that are inconsistent with, and reach different conclusions from, the information presented in this report. Such ideas or recommendations reflect the different time frames, assumptions, views and analytical methods of the persons who prepared them, and BofA Merrill Lynch is under no obligation to ensure that such other trading ideas or recommendations are brought to the attention of any recipient of this report. In the event that the recipient received this report pursuant to a contract between the recipient and MLPF&S for the provision of research services for a separate fee, and in connection therewith MLPF&S may be deemed to be acting as an investment adviser, such status relates, if at all, solely to the person with whom MLPF&S has contracted directly and does not extend beyond the delivery of this report (unless otherwise agreed specifically in writing by MLPF&S). MLPF&S is and continues to act solely as a broker-dealer in connection with the execution of any transactions, including transactions in any securities mentioned in this report.

16 Indra | 01 March 2016

Copyright and General Information regarding Research Reports: Copyright 2016 Merrill Lynch, Pierce, Fenner & Smith Incorporated. All rights reserved. iQmethod, iQmethod 2.0, iQprofile, iQtoolkit, iQworks are service marks of Bank of America Corporation. iQanalytics®, iQcustom®, iQdatabase® are registered service marks of Bank of America Corporation. This research report is prepared for the use of BofA Merrill Lynch clients and may not be redistributed, retransmitted or disclosed, in whole or in part, or in any form or manner, without the express written consent of BofA Merrill Lynch. BofA Merrill Lynch Global Research reports are distributed simultaneously to internal and client websites and other portals by BofA Merrill Lynch and are not publicly-available materials. Any unauthorized use or disclosure is prohibited. Receipt and review of this research report constitutes your agreement not to redistribute, retransmit, or disclose to others the contents, opinions, conclusion, or information contained in this report (including any investment recommendations, estimates or price targets) without first obtaining expressed permission from an authorized officer of BofA Merrill Lynch. Materials prepared by BofA Merrill Lynch Global Research personnel are based on public information. Facts and views presented in this material have not been reviewed by, and may not reflect information known to, professionals in other business areas of BofA Merrill Lynch, including investment banking personnel. BofA Merrill Lynch has established information barriers between BofA Merrill Lynch Global Research and certain business groups. As a result, BofA Merrill Lynch does not disclose certain client relationships with, or compensation received from, such issuers in research reports. To the extent this report discusses any legal proceeding or issues, it has not been prepared as nor is it intended to express any legal conclusion, opinion or advice. Investors should consult their own legal advisers as to issues of law relating to the subject matter of this report. BofA Merrill Lynch Global Research personnel’s knowledge of legal proceedings in which any BofA Merrill Lynch entity and/or its directors, officers and employees may be plaintiffs, defendants, co-defendants or co-plaintiffs with or involving issuers mentioned in this report is based on public information. Facts and views presented in this material that relate to any such proceedings have not been reviewed by, discussed with, and may not reflect information known to, professionals in other business areas of BofA Merrill Lynch in connection with the legal proceedings or matters relevant to such proceedings. This report has been prepared independently of any issuer of securities mentioned herein and not in connection with any proposed offering of securities or as agent of any issuer of any securities. None of MLPF&S, any of its affiliates or their research analysts has any authority whatsoever to make any representation or warranty on behalf of the issuer(s). BofA Merrill Lynch Global Research policy prohibits research personnel from disclosing a recommendation, investment rating, or investment thesis for review by an issuer prior to the publication of a research report containing such rating, recommendation or investment thesis. Any information relating to the tax status of financial instruments discussed herein is not intended to provide tax advice or to be used by anyone to provide tax advice. Investors are urged to seek tax advice based on their particular circumstances from an independent tax professional. The information herein (other than disclosure information relating to BofA Merrill Lynch and its affiliates) was obtained from various sources and we do not guarantee its accuracy. This report may contain links to third-party websites. BofA Merrill Lynch is not responsible for the content of any third-party website or any linked content contained in a third-party website. Content contained on such third-party websites is not part of this report and is not incorporated by reference into this report. The inclusion of a link in this report does not imply any endorsement by or any affiliation with BofA Merrill Lynch. Access to any third-party website is at your own risk, and you should always review the terms and privacy policies at third-party websites before submitting any personal information to them. BofA Merrill Lynch is not responsible for such terms and privacy policies and expressly disclaims any liability for them. Subject to the quiet period applicable under laws of the various jurisdictions in which we distribute research reports and other legal and BofA Merrill Lynch policy-related restrictions on the publication of research reports, fundamental equity reports are produced on a regular basis as necessary to keep the investment recommendation current. Certain outstanding reports may contain discussions and/or investment opinions relating to securities, financial instruments and/or issuers that are no longer current. Always refer to the most recent research report relating to an issuer prior to making an investment decision. In some cases, an issuer may be classified as Restricted or may be Under Review or Extended Review. In each case, investors should consider any investment opinion relating to such issuer (or its security and/or financial instruments) to be suspended or withdrawn and should not rely on the analyses and investment opinion(s) pertaining to such issuer (or its securities and/or financial instruments) nor should the analyses or opinion(s) be considered a solicitation of any kind. Sales persons and financial advisors affiliated with MLPF&S or any of its affiliates may not solicit purchases of securities or financial instruments that are Restricted or Under Review and may only solicit securities under Extended Review in accordance with firm policies. Neither BofA Merrill Lynch nor any officer or employee of BofA Merrill Lynch accepts any liability whatsoever for any direct, indirect or consequential damages or losses arising from any use of this report or its contents.