industrials overview pm: kj chua coverage team:brandon liu jacobo ochoa joe matten michael straka...

TRANSCRIPT

INDUSTRIALS OVERVIEWPM: KJ Chua

Coverage team: Brandon Liu

Jacobo Ochoa

Joe Matten

Michael Straka

Sreyas Misra

AIRLINESJacobo Ochoa

Highlights• Expanding rapidly (83.82% in the past year)• Market Cap of $197.56 billion• Revenues highly dependent on oil prices

• Worldwide airline industry used $210 billion of oil in 2013• Fuel accounts for 30% of operating expenses (the largest cost)

• Also affected by pathogen epidemics and terrorism• U.S. market dominated by four airlines: American Airlines, Delta Airlines,

United Airlines, and Southwest Airlines• Stocks are currently rising rapidly due to low oil prices

Airline equities have routinely outperformed the S&P 500 in the past year

Reasons for Growth• Improving economy and more travel, both business and leisure• Dropping oil prices• American Airlines and U.S. Airways merger• Higher fares

Return on Equity Comparisons

Airlines Construction & Engineering Road & Rail Automobiles0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

29.22%

11.32%

20.13%

12.42%

Return on Equity

Return on Equity

Airline Margins• Aggregate Gross Margin TTM: 54.35%• Aggregate Operating Margin TTM: 9.65%

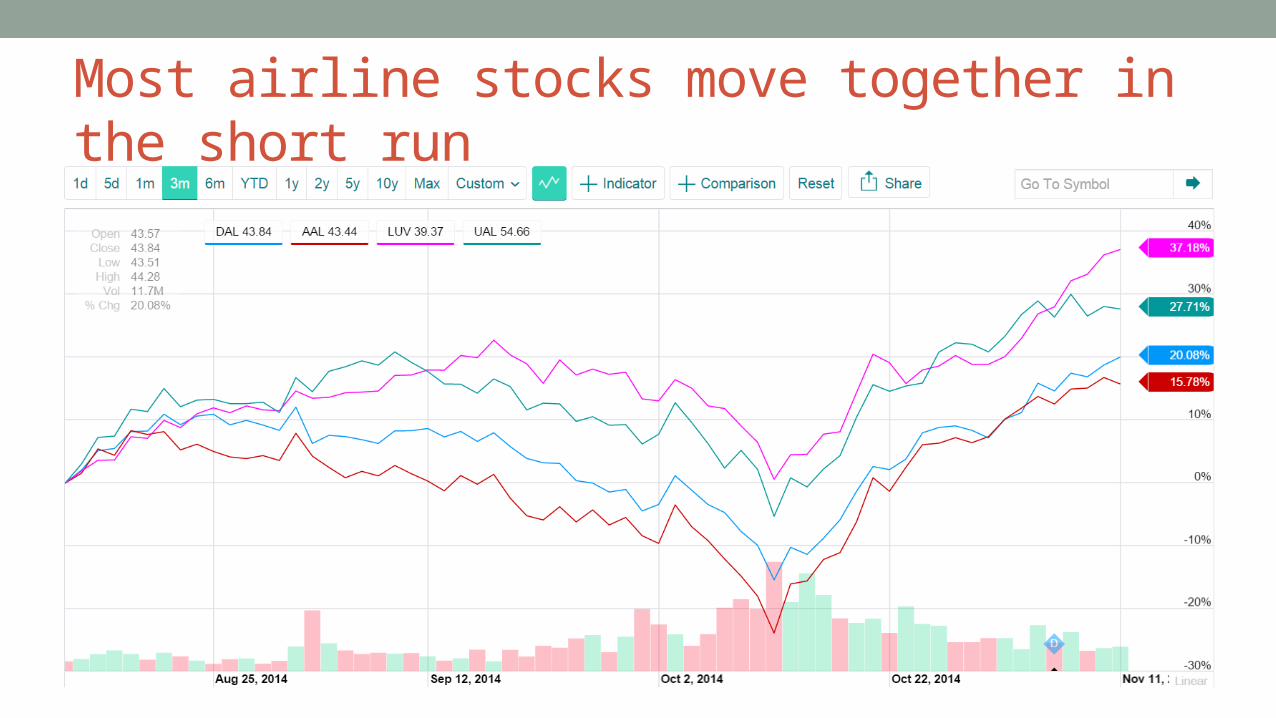

Most airline stocks move together in the short run

AIR FREIGHTJoe Matten

Market Overview• a system of transporting cargo by aircraft, aka air cargo• Largest 5 Companies (by air freight cargo volume):

• FedEx Express - largest volume & largest dedicated fleet• UPS Airlines - recently announced large investment in fleet• DHL Aviation - 12% of world market; leader in Europe; privately owned• Cathay Pacific Cargo – Hong Kong; growth opportunity as China grows• Korean Air Cargo – Part of largest airline in S. Korea; recently announced large investment

in fleet

Market Trends• Air Freight is a growing industry

• Q3 earnings are up due to lower oil prices and increased consumer demand • Demand expected to rise in Q4

(Cargo) (Capacity) (%age of Capacity)

Recent Market News• 8/13/14 – Cathay’s net profit for the six months ended June 30 was 347 million

Hong Kong dollars (US$44.8 million) compared with a first-half net profit of HK$24 million a year earlier

• 11/10/14 – Korean Air Lines Co.’s Q3 operating profit up 50% from a year earlier due to drop in oil prices.• Earnings expected to improve further in the Q4 on lower fuel costs, a weaker yen and

increased cargo traffic toward the end of the year.

Earnings growth

Lawsuit

Strong Earnings

Weak profit Lower Earnings Forecast

Domestic Charts

Regional Trends (Cargo & Capacity Growing)• Asia Pacific – iPhone 6; +5.7% FTK/+5.6%

AFTK• Europe – weak Eurozone, sanctions on

Russia, Air France strike -1.6% FTK/+1.2% AFTK

• North America – Strong business activity +5.4%FTK/ -0.02% AFTK

• Middle East – Demand grew by 10.1%. +17.0% FTK/+14.5% AFTK

• Latin American - +0.3% FTK/+1.7% AFTK• African – Volatile regional trade volumes

+11.5% FTK/-1.3% AFTK

However, revenue growth is slowing

Market Trends Continued• Largely affected by macro outlook, consumer spending, & oil prices• Slowing global macro environment hit on consumer spending• Yields for cargo are fairly low due to overcapacity in the market • Companies making large capital investments in fleet Margins are getting

squeezed

Thesis• Air Freight looks good (oil and Q4 shopping), but only for a shorter time

horizon than Blyth’s 3-5 year horizon.

• Freight yields have declined at an average rate of 2.3% • per year over the past 20 years.• Cargo revenue represents approximately 14% of total air traffic revenue on

average (up to 35% for some airlines). • Continuing industrywide declines in yield for cargo reflect productivity gains,

technical improvements, and intense competition (which is increasing)• Decreasing yields along with slowing global macro environment Don’t

invest

LOGISTICS & SHIPPINGBrandon Liu

Notable trends in shipping• Trucking capacity issues: freight rates remained pretty flat in 2013 and 2014

while volume rose• Rising costs for drivers, equipment and maintenance pushed smaller companies into

bankruptcy• “Freight rate hikes by as much as 5% to 8% before 2014 is over” – Fleetowner.com• New regulations are hampering productivity

• Far East importing raw materials and exporting manufactured goods at an accelerating clip• growth in demand for air and ocean shippers looks good

• Investors typically stay away from shipping because of its cyclical nature (follows the business cycle)• might be interesting due to increased demand for US natural gas…• …but also depends on the development of export capabilities

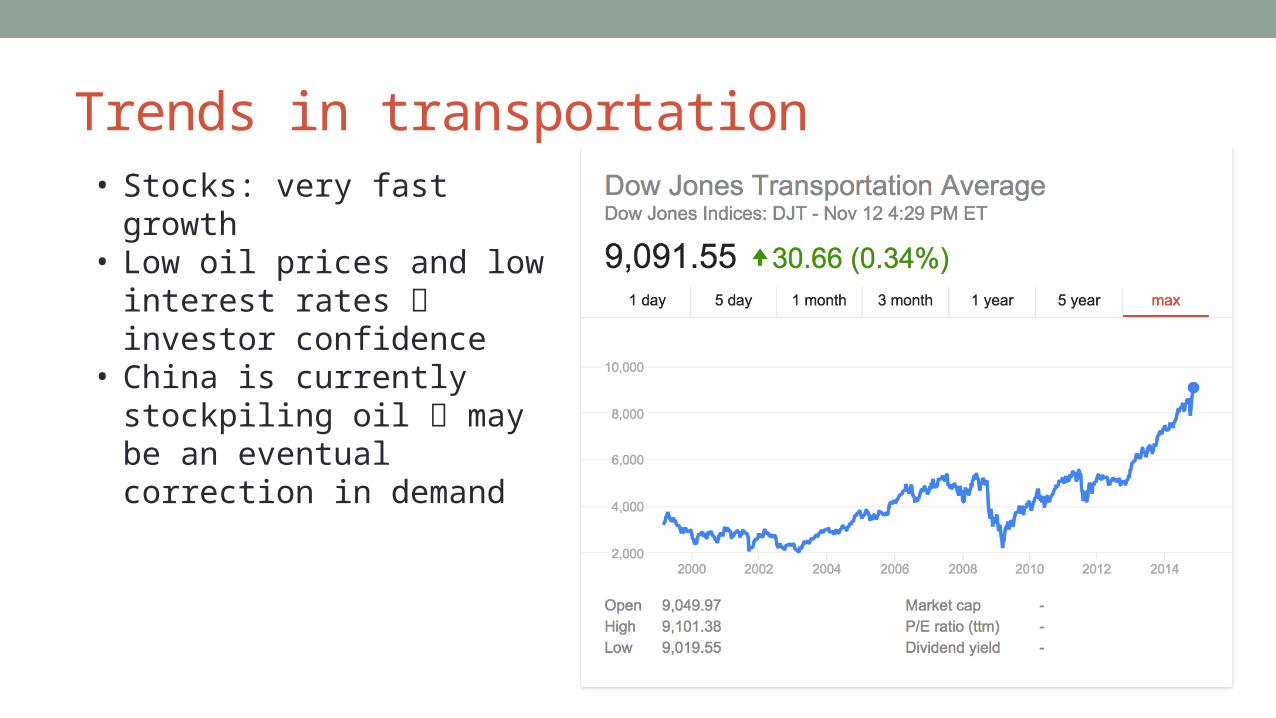

Trends in transportation• Stocks: very fast growth• Low oil prices and low interest

rates investor confidence• China is currently stockpiling

oil may be an eventual correction in demand

Trends in transportation• Uncertainty with trucking capacity

interest in maritime and air freight• However, there have also been

shifts from air to ocean freight• Air cargo industry lost 5.4 million metric

tons of cargo to container lines between 2000 and 2013• as shippers opted for slower but cheaper

transit via the ocean

General trends in international trade• Steady growth in

international trade paired with tech advancements + expanding market demands

Consequently, on the logistics side, there has been steady growth in 3rd party logistics providers (3PL)• “Non-asset-based” shippers

• serve as shipping coordinators & use their own technology and systems…• …but use other shippers’ assets to handle the physical delivery• Business model: steadier earnings growth and less volatile share prices

• Some interesting companies: "non-asset-based" shippers:• Landstar System1

• C. H. Robinson Worldwide• posting consistent gains + impressive histories of growth

1http://www.thestreet.com/story/12867810/1/why-landstar-system-lstr-stock-is-higher-today.html

3rd party logistics• Looks very promising• Trends in big data, analytics:

• The expansion of global trade requires more interconnected management systems• Big data will improve global supply chain performance and help quantify risk• Centralization of information systems allows for more swift response to market events

• Looking at companies that have traditionally done well may not be as good of an indicator of future performance• Researching tech and systems expansion of these 3PLs may be a better indicator of their

future performance