industry aspects of takeovers and divestitures: evidence ... · industry aspects of takeovers and...

TRANSCRIPT

Industry aspects of takeovers and divestitures: Evidence from the UK

Ronan G. Powell *, Alfred Yawson

School of Banking and Finance, the UNSW, Sydney, NSW 2052, Australia

Abstract

This paper examines takeover and divestiture activity at the industry level for the

population of UK firms over the period 1986 to 2000. Consistent with US research, takeovers

and divestitures in the UK cluster both across industries and over time. The paper further

investigates whether broad economic shocks, industry-specific shocks (e.g., deregulation, foreign

competition, technology) and misvaluation explain takeover and divestiture clustering at the

industry level. The results provide strong evidence for broad shocks increasing (decreasing) the

likelihood of takeovers (divestitures). Industry-specific factors are less important, although for

takeovers, growth, free cash flow and the threat of foreign competition some significance.

Deregulation, on the other hand, is only significant for the late 1990s period. Further

investigation reveals that for some UK industries deregulated in the late 1980s (e.g., Electricity

and Water), takeover activity was prevented for up to 5 years after deregulation through the use

of the ‘golden share’ by the UK government.

JEL classification: G14; G34

Keywords: Corporate restructuring; Takeovers; Divestitures; Industry shocks; Deregulation

* Corresponding author: Tel.: +61-2-9385-4925; fax: +61-2-9385-6347. E-mail address: [email protected]

2

1. Introduction

Takeovers and divestitures have played a key role in the restructuring of firms and

industries over the last century. Notable periods include the 1960s, characterized by large

conglomerate mergers, followed in the 1980s by hostile ‘bust-up’ takeovers. The last two

decades, in particular, have witnessed unprecedented takeover activity in both the US and the

UK, with many transactions setting new records in terms of value (see Andrade, Mitchell and

Stafford, 2001). While economists have advanced and tested many firm level theories (e.g.,

synergistic, managerial and diversification) in an attempt to explain takeover activity, no single

theory seems to fully explain why takeovers cluster over particular time periods (i.e., merger

waves) or across industries.

Recent papers have advocated a ‘market driven’ or misvaluation acquisitions theory to

explain the high levels of firm level takeover activity over certain decades (e.g., Shleifer and

Vishny, 2002; Ang and Cheng, 2002). The theory predicts that during periods of high stock

market values, firms are more likely to be misvalued, giving rise to opportunistic takeovers by

overvalued firms. Many of the stock financed transactions of the 1990s merger wave fit nicely

with the theory, with opportunistic managers timing deals to take advantage of highly inflated

stock. The theory also has some support from earlier periods, with contributions by Weston

(1953) and Nelson (1959) documenting a high correlation between security returns and merger

activity. While the theory explains many firm-level transactions during periods of high stock

market values, it has not, however, been applied to industry-level activity. Furthermore, some

observers note that the clustering of activity across industries is evidence of other factors playing

a role in explaining takeover activity (McGowan, 1971). Clearly, if takeover activity was

determined solely by misvaluation arising from periods of high stock prices, we should observe

3

higher activity across all industries. Evidence of significant industry clustering (e.g., Mitchell

and Mulherin, 1996) suggests that factors other than the rapid change in prices may be at play in

explaining clustering at the industry level.

Pioneering research by Coase (1937) on the nature of the firm provides some clues as to

the type of factors that should cause firms to change in size. For example, Coase (1937) argues

that technological advances allow firms to become more efficient in organizing activities in

diverse locations, thereby encouraging an increase in size. Gort (1969) argues that both rapid

changes in prices and technological changes are likely to cause valuation discrepancies between

bidding and target firms helping to induce merger activity. More recent research by Andrade,

Mitchell and Stafford (2001), Mulherin and Boone (2000) and Mitchell and Mulherin (1996)

point to additional factors or ‘shocks’ in explaining takeover activity, such as deregulation,

technological, energy price volatility and foreign competition. Since takeovers and divestitures

are mechanisms that facilitate a change in firm and industry size, industries sensitive to shocks

are likely to have higher frequencies of either or both transactions. Mitchell and Mulherin

(1996) argue that takeovers are probably the least-cost mechanism to alter firm and industry

structure.

This paper examines takeover and divestiture activity at the industry level in the UK over

the last two decades. The main focus of the paper is to test whether proxies for real market

factors (i.e., ‘shocks’) and misvaluation explain the level of takeover and divestiture activity over

time and across industries. Our paper differs from prior research in three important ways. The

first and second distinction relates to modeling. First, by modeling the real factor and

misvaluation theories simultaneously, we attempt to address the question of which theory (if any)

better explains activity. This approach also permits an examination of whether a correlation

4

exists between ‘shocks’ on the one hand, and misvaluation and subsequent activity on the other.

Clearly, factors other than an increase in prices may drive misvaluation, including some of the

factors or ‘shocks’ examined in this paper (e.g., deregulation, technological). Second, we

examine divestiture activity believing that a potential link exists between ‘shocks’, misvaluation

and divestiture activity. Prior empirical research (e.g., Mulherin and Boone, 2001) demonstrates

that divestitures, like takeovers, tend to cluster across industries. We therefore test whether

factors that cause firms to expand or consolidate through takeover, also influence the decision to

streamline operations through divestitures.

The third distinction relates to sample design. We model takeover and divestiture activity

using an industry panel dataset created by aggregating the ‘true’ population of UK firms into

their respective sectors each year, over the sample period 1986 to 2000. This approach allows us

to observe actual takeover and divestiture activity each year as a proportion of the true

population of firms each year. Prior studies (e.g., Mitchell and Mulherin, 1996) have favored the

more static approach, by keeping the population constant at the beginning of the sample period

and following the activity of only those firms observed at the beginning of the period. This

approach is likely to be biased, since it ignores newly listed firms, which arguably, may be more

vulnerable to activity.

Another distinction, although less significant, is that this paper uses a UK dataset. Prior

research is predominantly US based, with only one contribution by Schoenberg and Reeves

(1999) using UK data. The UK market, however, is similar to the US over the period examined.

For example, both countries experienced significant stock market booms in the 1980s and 1990s

and, furthermore, were impacted by similar shocks in the form of deregulation (financial and

utility industries), technological and broader shocks in oil prices, interest and exchange rates.

5

Using UK data allows for useful comparisons to be made with prior US research, e.g., Is

takeover and divestiture activity determined by similar factors?

The rest of the paper is organized as follows. Section 2 sets out the theoretical

underpinning of the paper. Section 3 explains the procedures followed in constructing the

sample. Section 4 presents some preliminary results for the level of corporate restructuring

across each industry over the sample period. Section 5 describes the model development and

discusses the choice of variables to proxy both broad and industry-specific shocks and

misvaluation. Section 6 presents some descriptive statistics and the results of the estimated

regressions. Section 7 concludes with a discussion and summary of the main results.

2. Theoretical background

The starting point for the study is Coase’s (1937) seminal analysis, ‘the nature of the

firm’. Coase provided a framework for defining the firm in terms of setting out the conditions or

forces that cause a firm to change in size. Coase (1937, p.393) asks, ‘Why does the entrepreneur

not organise one less or one more transaction?’ Coase argues that a firm will only expand

internally to the point when the marginal cost of the extra product is equal to the cost of

procuring the same product in the open market, which includes a competitor firm. Expansion

beyond this point would result in diminishing returns to scale since additional costs to facilitate

extra production would increase the marginal cost. However, assuming firms do not produce to

maximum capacity, gains, arising from lower marginal costs, will occur through the merger of

similar operations. Coase argues, however, that expansion beyond core activities will lead to

inefficiencies in terms of organising business activities in different locations. Inventions and

technological advancements that improve the efficiency of managing firms in diverse locations

6

are, therefore, likely to increase the size of the firm. Coase uses examples such as the telephone

and telegraph as inventions or technological advancements that allowed firms in different

locations to operate more efficiently. In today’s environment, clearly the fax, the personal

computer and internet (e.g., video conferencing, email) have allowed firms to operate in different

locations.

The idea that real environmental factors can have an impact on the size of the firm has

been discussed in later research by Gort (1969) and McGowan (1971). Gort (1969) advanced an

‘industry disturbance theory’ of mergers, in which real economic factors, such as rapid

technology changes, cause variations in the valuation of firms. Changes in valuation arise

because technological changes cause past earnings information to contribute less to future

predictions about earnings. That is, new products or processes cause a break from the past,

causing bidding firms to make errors in valuing potential targets. Clearly, this analysis could be

extended to any broad economic or industry-specific shock that causes a variation in the

valuation of firms, and hence, a higher likelihood of errors or discrepancies in valuing potential

targets.

Gort (1969) argues that rapid changes in share prices will also cause a break from the past

and cause increased merger activity. However, while both positive and negative movements in

prices will cause an increase in the dispersion of valuations, they will impact on merger rates in

opposite ways – high prices will lead to more activity, whereas low prices will lead to less

activity. Hence, valuation discrepancies that induce takeovers are more likely to occur in bull

markets.

The correlation between security returns and merger rates has been documented through

time (see, e.g., Nelson, 1959; Weston, 1953; and more recently, Shleifer and Vishny, 2003).

7

McGowan (1971) argues that high prices lead to disequilibria in equity markets; hence market

values fail to reflect true long-term profit opportunities, giving rise to under/over valued firms

and increased merger activity. More recent evidence at the firm level by Rhodes-Kropf and

Viswanathan (2003) and Shleifer and Vishny (2003) suggests that merger activity, particularly in

stock for stock mergers, is linked to misvaluations by bidder and targets firms. Basically,

overvalued acquiring firms use their overvalued stock to purchase assets cheaply. Shleifer and

Vishny (2003) posit that target managers accept overvalued bidder stock because they are self-

interested and ‘cash out’ their shares to generate private gains.

The strong association between merger activity and bull markets fails to explain the

clustering of takeover activity across industries. McGowan (1971) argues that this view only

emphasizes the role of generalized financial market considerations to external expansion rather

than conditions prevailing in the real markets in which firms operate. That is, in bull markets, all

firms could take advantage of merger opportunities, regardless of their industry, but yet, they fail

to do so as evident by significant industry clustering (Gort, 1969, Mitchell and Mulherin, 1996

and Mulherin and Boone, 2000). Clearly, other industry-specific factors are at work in

motivating takeovers, such as technological changes, oil price shocks, government regulation

changes. McGowan (1971) refers to these factors as real market conditions which firms through

merger are better able to adapt to. For example, through merger, firms can acquire new

technologies and highly specialized personnel. Merger also allows an increase in firm size

without adding to total industry capacity. Jensen (1993) further emphasizes the role of changes

in technology, input prices and deregulation in motivating restructuring activity during the

1980s. Andrade, Mitchell and Stafford (2001) show deregulation to be the single biggest factor

8

in explaining takeover activity in the 1990s. Jovanovic and Rousseau (2001, 2002) point to

technological changes inducing merger waves during the 1920s, the 1980s and 1990s.

The discussion so far has concentrated on merger activity. Following Coase’s (1937)

discussion, industry factors could also cause firms to decrease in size through divestitures.

Mulherin and Boone (2000) find that both takeovers and divestitures exhibit significant industry

clustering, indicating that industry-specific changes or shocks have a similar impact in that they

cause an increase in both activities. However, they do not examine the correlation between

specific industry shocks and the rate of divestitures, so it is unclear whether differences arise in

the rates of takeovers and divestitures to particular shocks. They do, however, find an

insignificant negative correlation between the rates of takeovers and divestitures, indicating that

both activities are induced by both common and dissimilar shocks.

3. Sample construction

To construct our industry panel dataset, we begin by identifying the population of UK

firms listed on the London Stock Exchange (hereafter, LSE) during the period 1986 to 2000.1 To

be classified as ‘live’ in a particular year, and be included in the population, all firms must have

financial data available from Datastream.2 Firms are classified according to Datastream’s level 6

classification scheme, which is similar to the US SIC 4 classification scheme. A total of 21,190

firm-years (average of 1,413 per year) are identified as ‘live’, representing a total of 90

industries. Note that the number of industries in any one year may change with the introduction

of new industries. For example, former utilities, such as water, electricity, plus newly

established industries such as internet, only emerged in the 1990s in the UK. We place two

further restrictions on the sample: (1) industries with less than 5 firms per year are excluded; and

9

(2) industries classified as property, investment institutions (e.g., asset managers, insurance

brokers) are removed. The final sample comprises of 71 industries or 880 industry-years.

Note that the sample construction differs from the static approach used by Mitchell and

Mulherin (1996) and Mitchell and Boone (2000). Both papers hold the number of firms in each

industry constant throughout the sample period so that takeover activity for an industry is

calculated the number of transactions over the sample period as a proportion of firms that existed

in the industry at the beginning of their sample period. This approach is likely to suffer from a

new listing bias, since newly listed firms are ignored. Takeover proportions are also likely to be

biased with a static approach if newly listed firms are more likely to be targets for takeover.

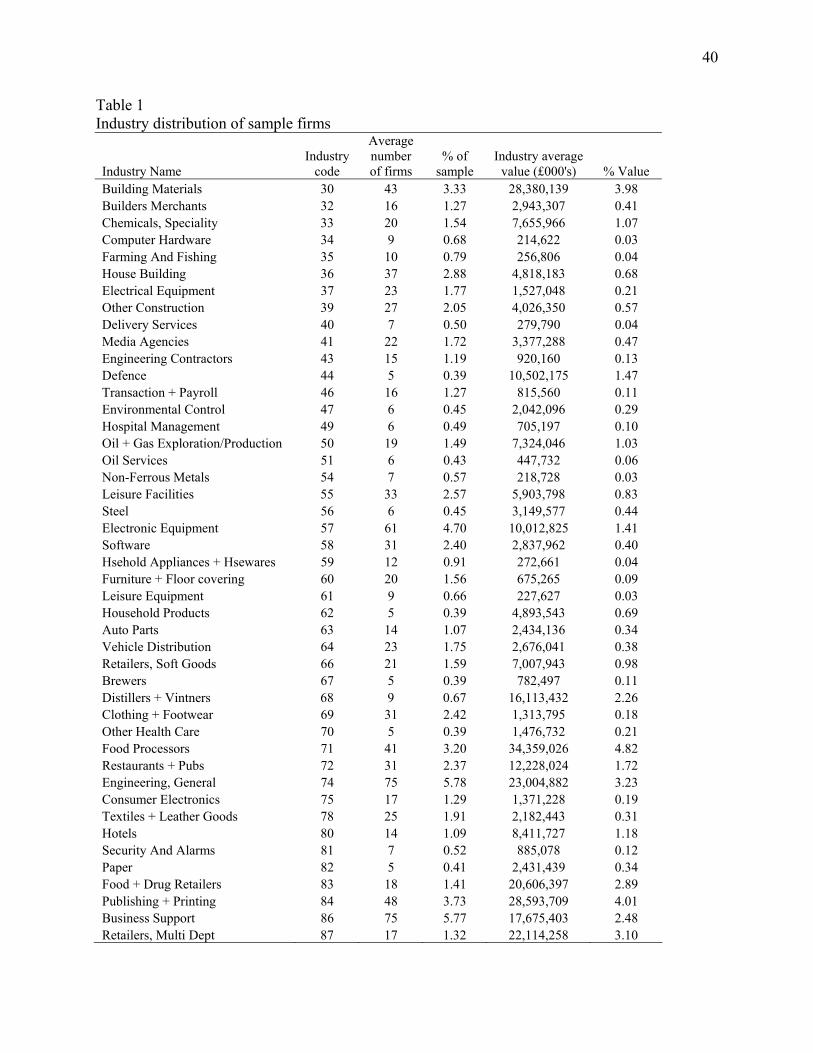

Table 1 shows the distribution of the sample by industry and average total market value

(TMV). The average number of firms each year over the sample period is about 1,294, which

have a TMV of approximately £712 billion, on average, each year. The industries in the sample

have an average TMV of approximately £10 billion over the sample period. The mean (median)

number of firms in each industry is 18 (14) with a standard deviation of 15. Since we use a panel

dataset, comparisons with prior research are difficult. For a static sample constructed in 1981

using US data, Mitchell and Mulherin (1996) report a total sample TMV for 1,064 firms,

representing 51 industries of $1,014 billion, which gives an average industry TMV of

approximately $20 billion. Mulherin and Boone (2000) construct a US sample using data from

59 industries in 1990 and report a total sample market value for 1,305 firms of $2,514 billion,

which gives an average industry market value of about 43 billion. Clearly, even accounting for

currency differences, average industry size in the US is significantly larger than in the UK.3 In

terms of the average number of firms in each industry, General Engineering and Business

Support have the highest representation across all years with an average of 75 firms each (5.78%

10

of the sample). By TMV, Banks is the largest industry across the sample period with an average

of approximately £100 billion (14.16% of the sample). Gold mining has the lowest average

TMV of £72 million (0.01% of the sample). The descriptive statistics reported at the bottom of

Table 1 indicate skewness in the distribution and value of industries across time.

The firms in each industry are followed for the period 1986 to 2000 to identify the major

restructuring choices affecting them. The information on the restructuring choices made by

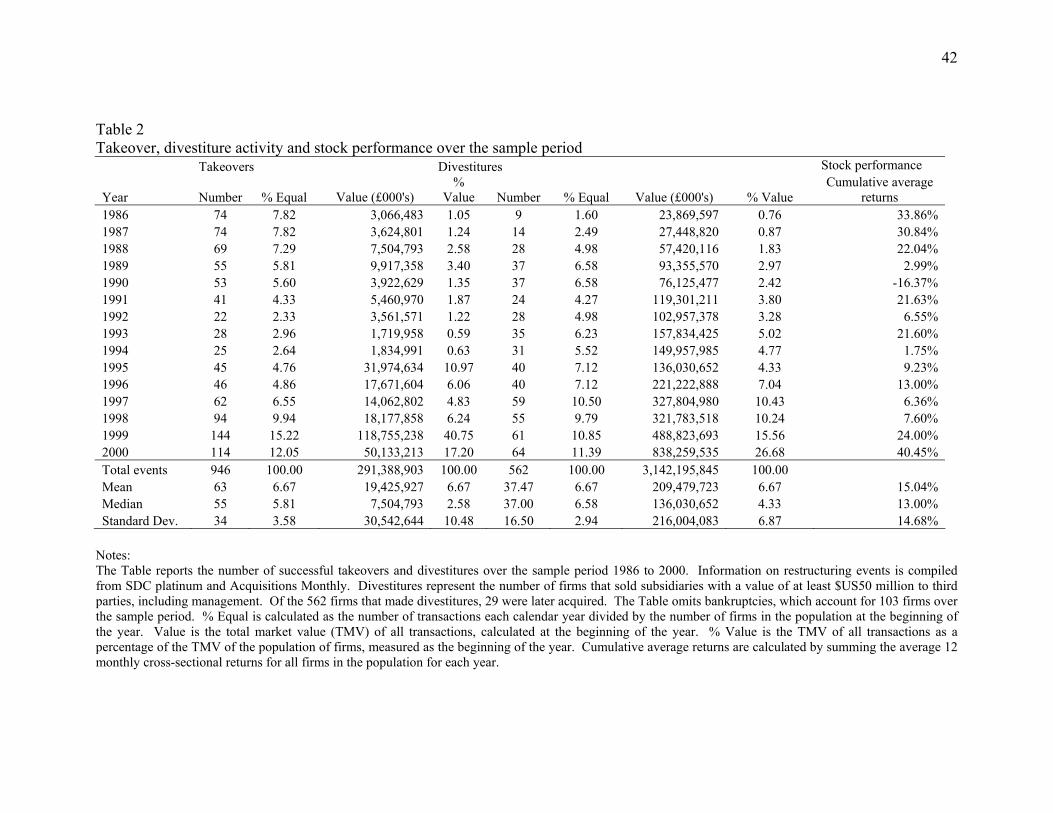

firms is compiled from the SDC Platinum database, compiled by Thomson Financial. Table 2

reports the frequency of restructuring activities pursued by sample firms.4

Insert Table 2 here

Table 2 shows that 562 firms (average of 6.67% of the sample) engaged in divestitures

over the sample period. We define a divestiture as the sale of a subsidiary by the parent to a

third party, which could include an investor group comprising of the management of the divested

subsidiary. To make the results more comparable to Mulherin and Boone (2000) we constrain

our analysis to only the largest transactions by excluding divestitures valued at less than US$50

million.5 We also identify 946 (average of 6.67 of the sample) successful takeovers. As

expected, firms restructuring through divestitures are, on average, larger than firms targeted for

takeover.

The last column in Table 2 reports the stock market performance, measured as the

cumulative monthly average returns of all firms in the population for each year. Consistent with

early research (e.g., Weston, 1953 and Nelson, 1959), the results suggest a positive association

between takeover activity and periods of high stock market values. The correlation coefficient is

11

significant and positive between the number (ρ=0.47) and value (ρ=0.28) of takeovers and stock

market performance. For divestitures, the correlation is positive for the value (ρ=0.36) of

transactions and stock market performance, but negative for the number (ρ=-0.10) of transactions

and stock market performance. The evidence suggest that the both takeovers and

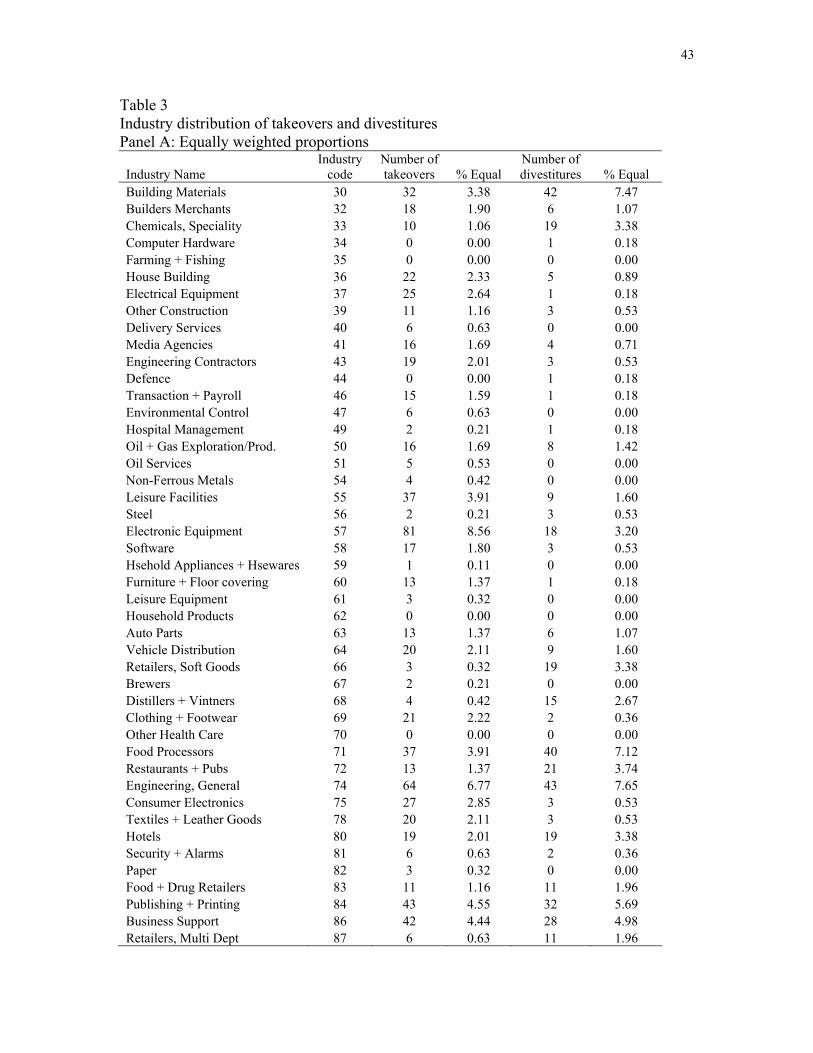

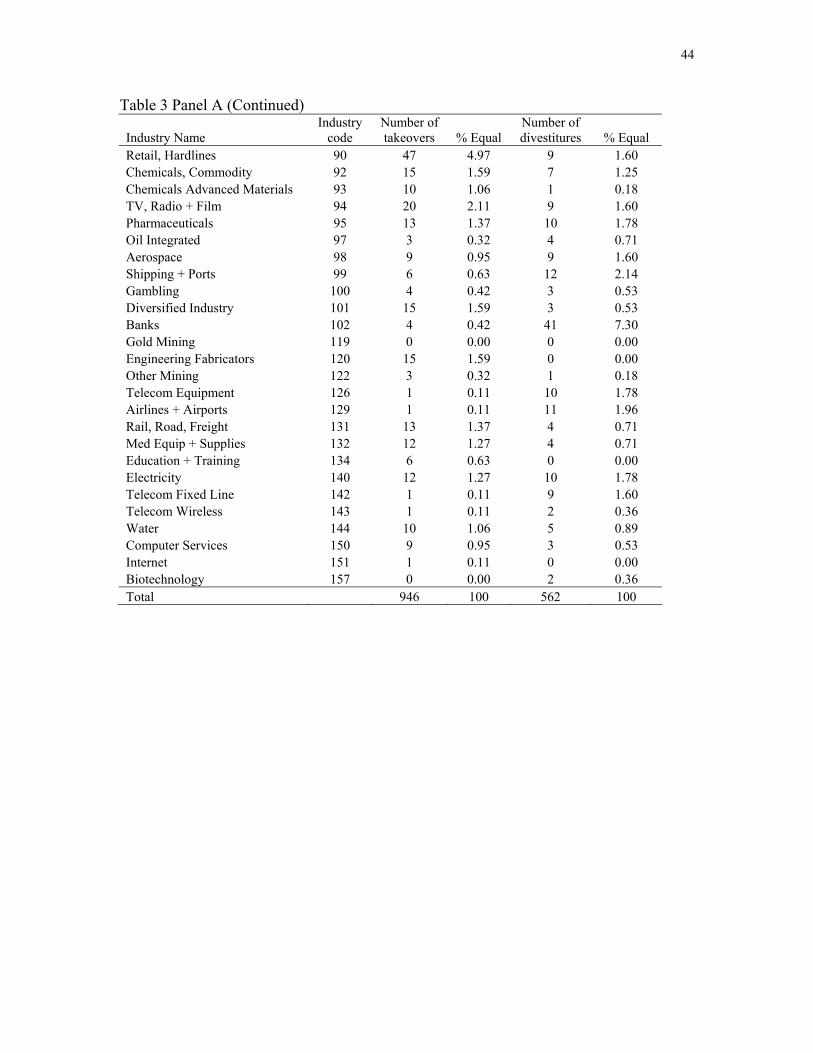

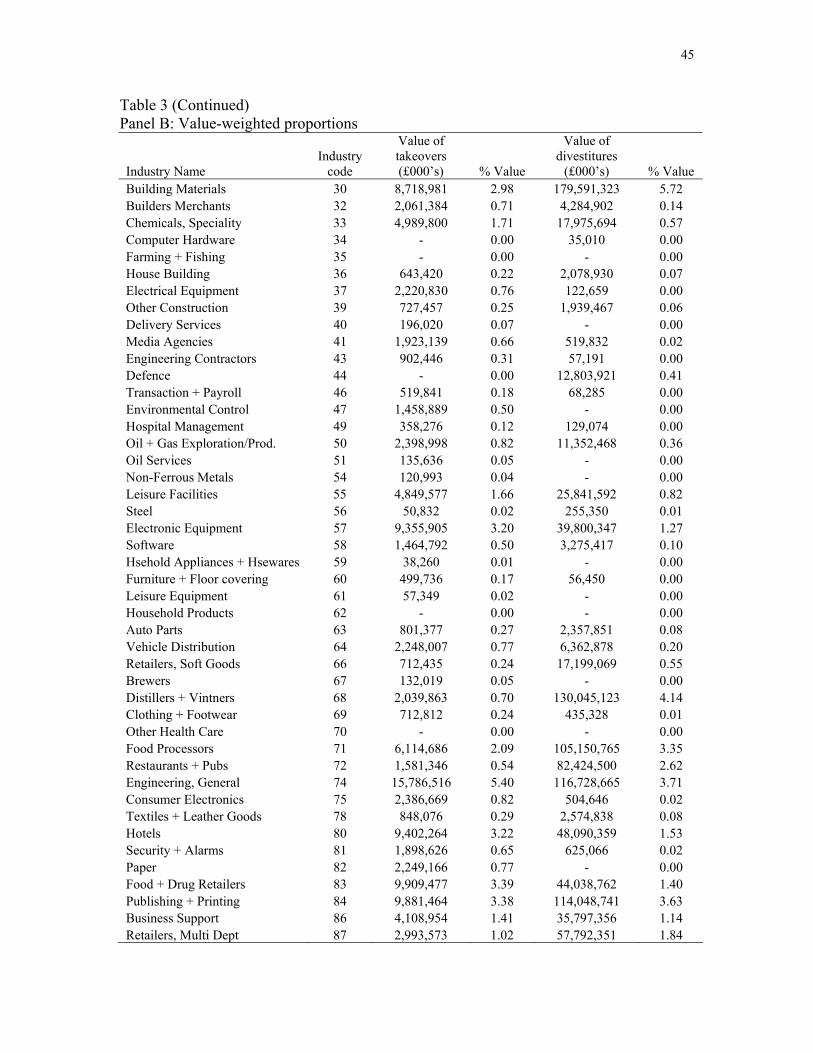

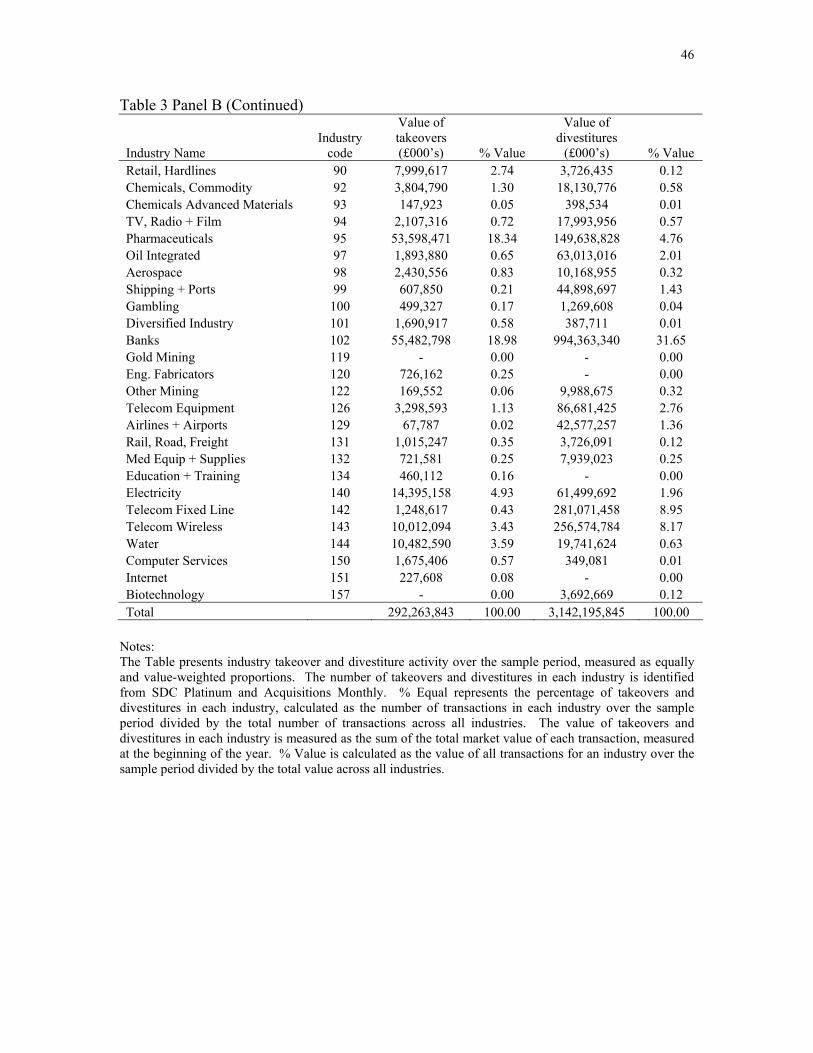

4. Industry patterns in takeovers and divestitures

Following from Mitchell and Mulherin (1996) and Mulherin and Boone (2000), we

analyze whether there are any differences in the rate of takeovers and divestitures across

industries over the sample period. Table 3 reports average equally weighted (Panel A) and

average value weighted (Panel B) proportions for takeovers and divestitures over the sample

period.

Insert Table 3 here

While the likelihood of takeovers and divestitures is generally low, some industries show

higher rates of activity indicating clustering. For example, Electronic Equipment and

Engineering General report average takeover rates of 9% and 7% respectively, compared to Steel

(0.21%) and Airlines and Airports (0.11%). Divestitures also appear to cluster around certain

industries with Engineering General and Building Materials reporting rates of 8% and 7%,

respectively. The results using value weighted averages (Panel B) show that the largest

transactions seem to occur in Banks, Pharmaceuticals and Engineering General, reporting

takeover rates of 19%, 18% and 5.4%, respectively. For divestitures, Banks,

Telecommunications (Fixed and Wireless) and Building Materials industries report the highest

rates of 31.65%, 8.95% and 5.72%, respectively. There is some similarity between industries

12

with high takeover and divestiture rates reported here and those reported in the US. For

example, Mulherin and Boone (2000) for the 1990s period, also report high takeover activity

rates for Banking and the Electronics industry. For Divestitures, they also report high activity

for Telecommunications, but not for Banks and Building Materials.

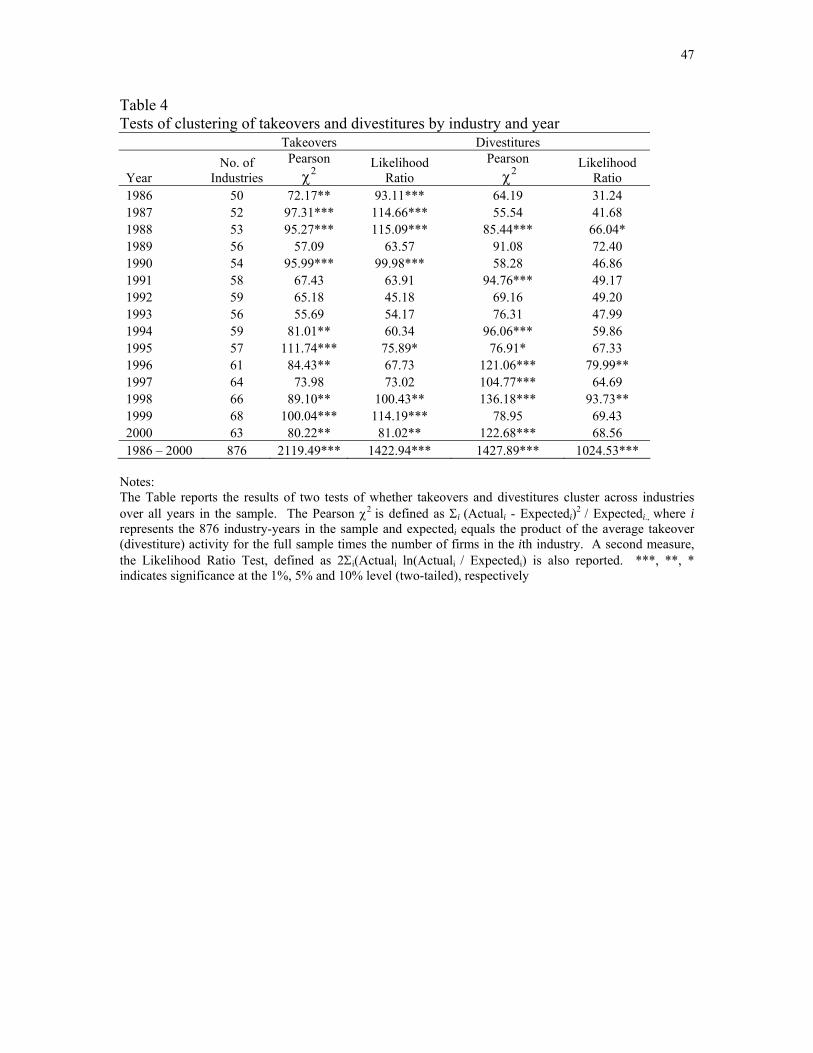

To test whether the variation in the rates of restructuring activity is statistically

significant across all years, we estimate the Pearson χ2, which tests the null hypothesis that the

actual takeover or divestiture rate in each industry equals its expected rate (see Table 4).6 The

value of the statistic for takeovers is 2,119 (df = 875), which is significant at the 1% level,

indicating a rejection of the null hypothesis. The value of the statistic for divestitures is 1,428 (df

= 875), indicating significant clustering of divestitures over the sample period. To test whether

industry clustering is specific to certain years, Table 4 also reports the Pearson χ2 for each year.

The results suggest significant clustering of takeovers and divestitures across significant stock

market growth periods in the late 1980s and mid to late 1990s.7 To check the robustness of this

result, Table 4 reports a variant of the Pearson χ2, the Likelihood Ratio Test, defined as

2Σi(Actuali ln(Actuali / Expectedi). While the results are broadly similar for takeovers, for

divestitures they suggest that clustering was only specific to 1988, 1996 and 1998.

4.1. Do takeovers and divestitures cluster over time?

As a natural extension of the previous section, we examine which industries drive the

clustering of takeovers and divestitures across the sample period.

Insert Table 4 here

13

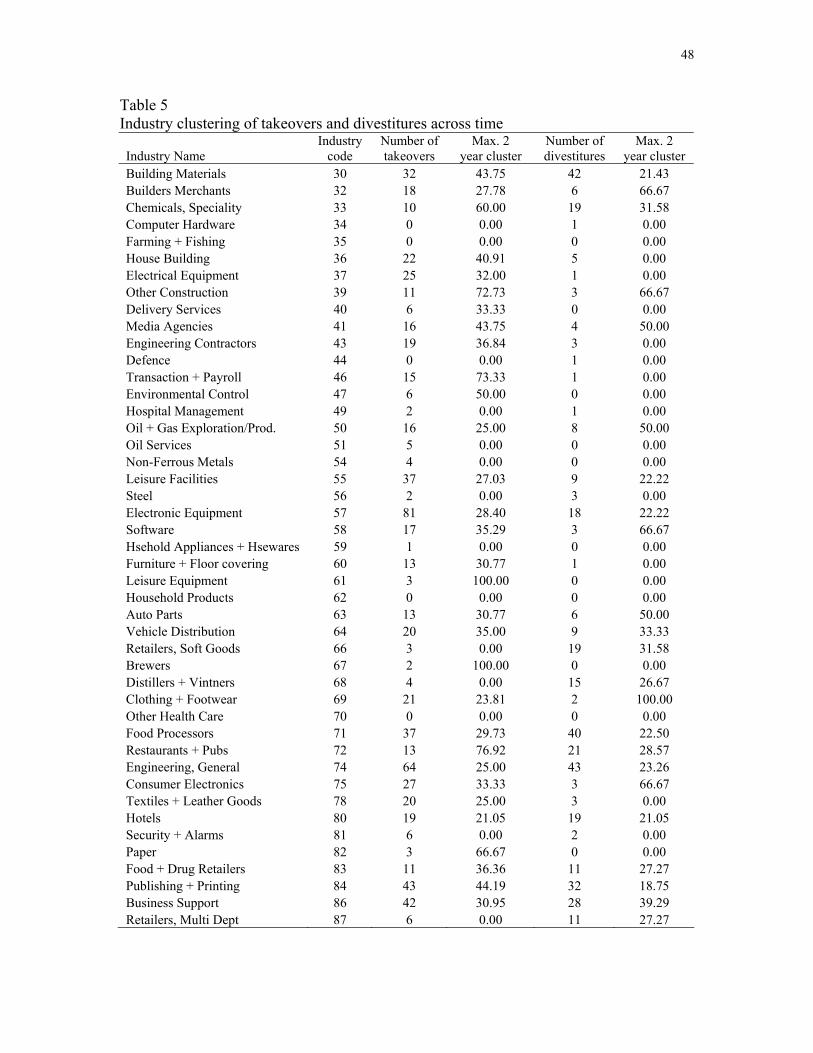

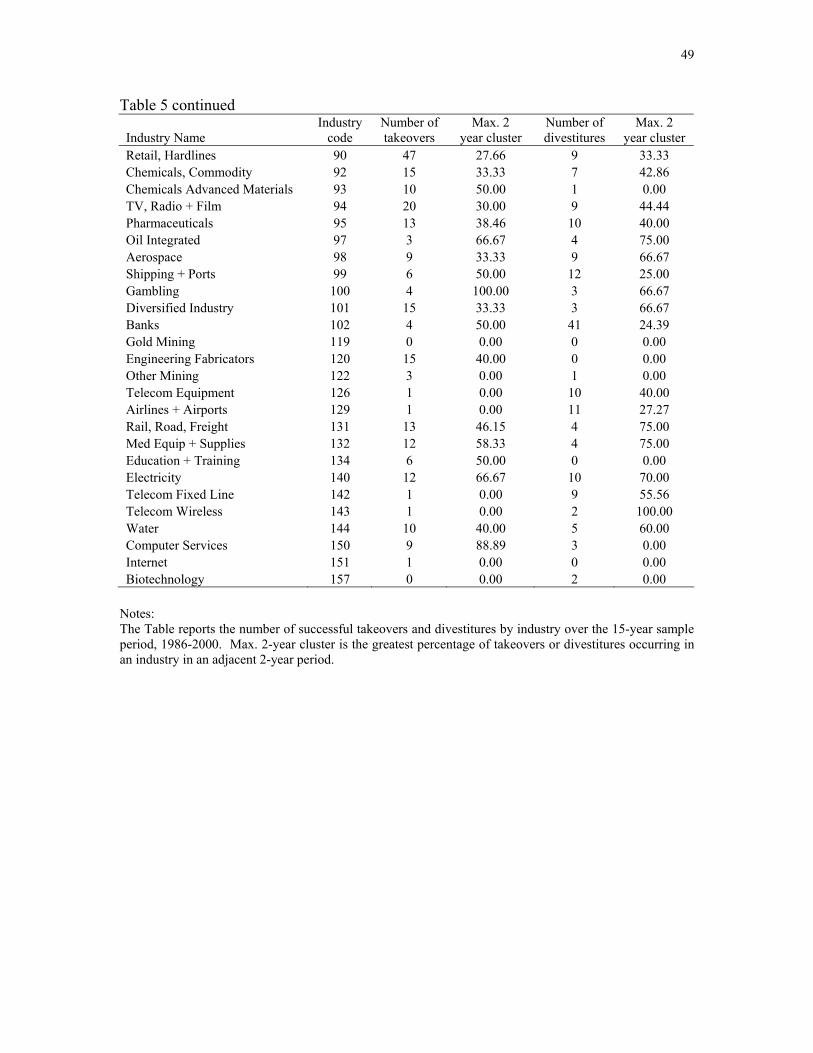

Table 5 reports the number of takeovers by industry across the sample period. We have

sorted the data in terms of the maximum clustering percentage reported in an adjacent 2-year

period within the 15-year sample period. The evidence suggests that takeovers are clustered in

specific industries across time. For example, over half of all takeovers in the Chemicals

Specialty industry occur within a 2 year period. Similar findings exist for Other Construction,

Electricity and Computer Services. Table 5 also presents the results for divestitures. Again, the

results indicate some clustering across time for certain industries, including Builders Merchants

(67%), Electricity (70%) and Clothing and Footwear (100%).

Insert Table 5 here

5. Modelling shocks and misvaluation

The results from Section 4 provide some evidence that takeovers and divestitures appear

to cluster both across industries and time. This section attempts to identify the causes of this

clustering. We use the discussion of the main theoretical issues discussed in Section 2 as a guide

to building a model of takeover and divestiture activity at the industry level. However, there is a

caveat in that the theories posited in Section 2 relate primarily to takeovers; hence we have no

strong priors that proxies for those theories will be useful in explaining the variation in

divestiture activity across industries and, to a lesser extent, over time.

We suspect, given past research, that ‘real’ factors in the form of broad (i.e., interest and

exchange rate shocks) and industry-specific shocks (i.e., deregulation, foreign competition and

technology) play some role in explaining this clustering. Also, given recent research on

valuation discrepancies as a driving force in explaining takeover activity, we use proxies for

14

misvaluation in our estimated models. This section describes the process followed in developing

a model to explain the clustering of takeovers and divestitures. We describe the variables used to

proxy broad economic shocks, industry-specific shocks and misvaluation.

5.1. Broad economic shocks

Generally, previous studies assume that whatever the source of the broad shock (e.g.,

exchange and interest rate changes) the outcome is a change in industry structure,

operationalized through takeovers and other forms of corporate restructuring. To create a proxy

for broad economic shocks, Mitchell and Mulherin (1996) compute the absolute value of

abnormal industry sales and employment growth for the period of five years prior to their sample

period. They define the absolute value as the difference between an industry’s sales

(employment) growth and the average sales (employment) growth across all industries. Taking

the absolute value recognises that a shock could have either a positive or negative effect on

restructuring. In this paper, we also define broad economic shocks using sales and employment

data. However, we also employ a third measure - operating cash flows. Our motivation for

using operating cash flows is that they are more sensitive to cost side shocks, as well as income

side shocks, unlike sales, which is purely income based. Following Mitchell and Mulherin

(1996), we measure the absolute value of the abnormal industry sales, employment and cash flow

growth over a five year period, starting in 1986. Each of these proxies is used in a pooled

regression to explain the variation in takeover and divestiture activity across all industries over

the sample period. Formally, the model takes the following specification,

tititi SHKR ,,1, εβα ++= (1)

15

where Ri,t represents the restructuring proportions in industry i, during period t. SHKi,t is a proxy

for broad economic shocks for industry i, during period t (i.e., absolute industry-specific growth).

If broad economic shocks are significant determinants of corporate restructuring, we should

expect β1 to be significant and positive. Clearly, given that the dataset is panel in design,

estimation of the model raises some econometric issues. In particular, any inferences placed on

the estimated coefficients could be open to criticism due to understated standard errors arising

from correlated residuals across panel years. Following Fama and McBeth (1973), and more

recently, Fama and French (2002), we use the average coefficients estimated from yearly

regressions and infer statistical significance using time-series standard errors estimated from the

cross-sectional yearly regressions. For the pooled regression model, we report White’s (1980)

standard errors corrected for heteroscedasticity.

4.2. Industry-specific shocks

Since industry-specific shocks are also likely to have some impact on industry

restructuring, we expand the above basic model to include variables that proxy industry-specific

factors. Broadly, the literature has divided industry-specific factors into internal and external

factors. The internal factors include growth opportunities, profitability, availability of cash and

industry concentration (Jensen, 1989, 1993). The external factors include changes in technology,

industry deregulation and foreign competition (Mitchell and Mulherin, 1996; Mulherin and

Boone, 2000). These factors are discussed in more detail below.

16

Internal factors

Two hypotheses related to growth have received attention in the literature. The first

predicts that industries characterized as high growth are more susceptible to restructuring,

especially takeovers. The hypothesis is derived from the ‘empire building’ theory of takeovers,

which suggests that a high growth industry will be more attractive to managers who derive a

higher utility from controlling larger firms. For example, Mulherin and Boone (2000) provide

evidence of greater takeover and divestiture activities in high growth sectors, such as electronics,

telecommunications and electrical equipment. Takeovers in high growth industries by low

growth acquirers with high resources are also more likely to be value enhancing (Myers and

Majluf, 1984).

The second hypothesis argues that industries characterized as low growth, with high free

cash flow, will be subject to hostile takeovers and leverage buyouts. The theory received some

support for the 1980s, a period of high hostile takeovers directed at industries with low growth

options (e.g., oil exploration), but high level of free cash flow (Jensen, 1986 and 1989). The

1990s period, however, has experienced very few hostile transactions, with most transactions

being characterized as ‘consolidated’ deals by firms within the same industry (Holmstrom and

Kaplan, 2001). To capture these effects, we include industry growth (defined using sales,

employment and cash flows) and a proxy for free cash flow (industry-specific operating cash

flow less capital expenditures scaled by total assets) in the estimated models.

The degree of concentration within an industry is likely to be an important determinant of

the level of corporate restructuring. The concentration of firms in an industry has been related to

industry growth, with concentration ratios increasing as firms reach maturity. For example,

Mitchell and Mulherin (1996) document that the excess capacity in Metals and Mining and Food

17

processing industries in the US led to greater restructuring activities, which in turn led to

industry consolidation. The theory suggests that low concentration industries will have a higher

rate of takeovers as firms compete to gain a greater share of the market. Moreover, the desire to

have fewer firms within an industry to enhance market power may lead to takeovers and other

restructuring activities.

In terms of corporate restructuring, industry concentration has only been related to

takeovers. As far as we are aware, there is no evidence of a relationship between industry

concentration on the one hand, and divestitures on the other. This is an empirical issue that will

be addressed in this paper. To the extent that firms selling assets via divestitures are larger in

size, it may be reasonable to expect a higher incidence of these activities in high concentration

industries.

Several measures are used to determine the extent of concentration in an industry. These

measures attempt to capture the prevailing structure and the extent of competitive forces in an

industry (see, e.g., Liebeskind, Opler and Hatfield, 1996 and Ratnayake, 1999). Two of these

measures are commonly used in calculating industry concentration. First, the four firm

concentration ratio, defined as the proportion of total sales accounted for by the four largest firms

in an industry. Second, the Herfindahl index, defined as the sum of the squared market shares of

all incumbent firms. The market share for each firm is defined as the ratio of its sales to the total

value of sales in the industry (Liebeskind, et al., 1996). Hence, larger firms are allocated higher

weights to reflect their relative importance in the industry. We employ the Herfindahl index

since a few of the industries in our sample are relatively small. Using the four firm approach in

such cases is likely to result in an upward bias in the concentration ratios.

18

External Factors

External factors include changes in government policies, such as deregulation,

privatization and the impact of foreign competition. To identify the specific industry shocks

affecting UK industries, we search through the industry background and news contained in Key

Note Market Research Reports and Sequencer for each industry. We identify deregulation,

foreign competition and technological innovations as the key shocks affecting specific UK

industries over the sample period.

Table 6 provides a summary of the sources of specific industry shocks and the industries

affected over the sample period. Although several external factors affect corporate restructuring

in an industry, deregulation seems to be one of the most significant external factors (Andrade,

Mitchell and Stafford, 2001). Deregulation removes the artificial constraints imposed on an

industry and this induces free entry and exit of firms (Rose, 1985). The exposure of these

industries to the pressures of the market and competition requires adaptation, which is facilitated

by takeovers and other restructuring activities. In the UK, for example, the privatization of the

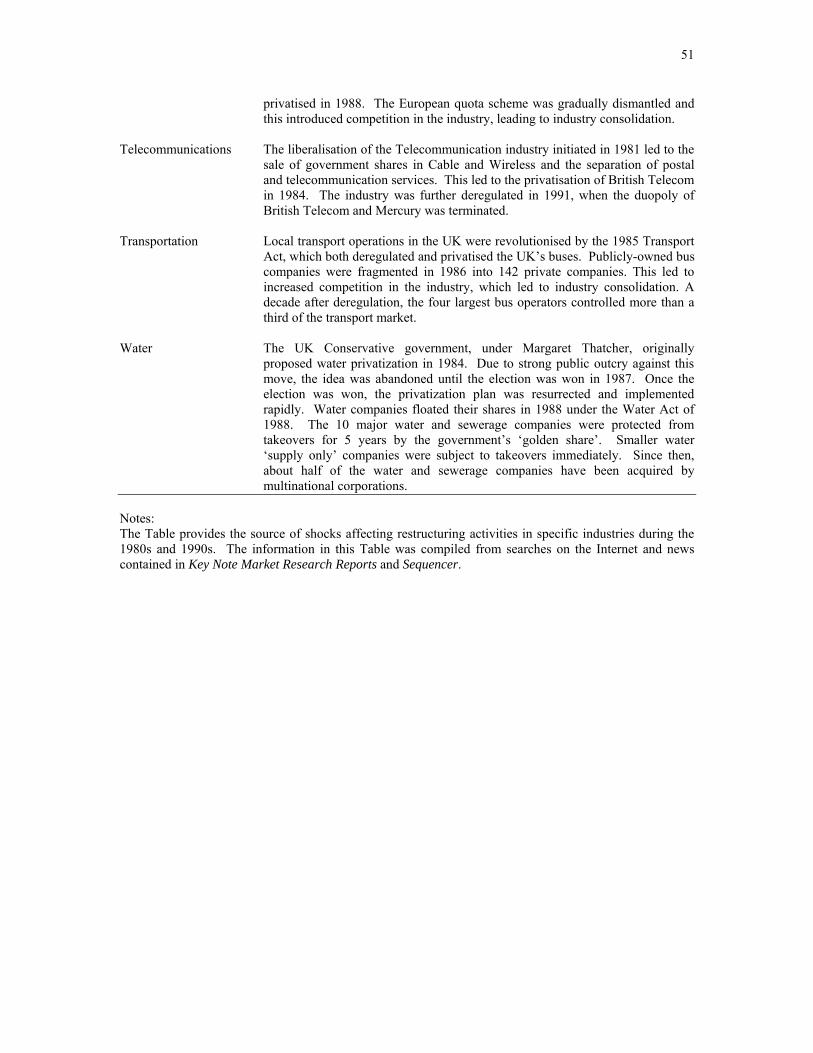

Telecommunications industry initiated in 1981 led to the sale of government shares in Cable and

Wireless and the separation of postal and telecommunication services. This led to the

privatization of British Telecom in 1984. The industry was further deregulated in 1991 when the

duopoly of British Telecom and Mercury was terminated. These changes have dramatically

altered the Telecommunications industry, allowing numerous new entrants into the market.

Similar developments have taken place in the Electricity, Water and Transport industries. We

create a dummy variable equal to one for the deregulated industries (i.e., Electricity, Oil and Gas,

Steel, Telecommunications, Transport and Water) for all post-deregulation years.8

Insert Table 6 about here

19

Foreign competition affects the demand and profitability of the affected industries, which

may lead to various forms of corporate restructuring. For example, new competition from

overseas can impact significantly on an industry’s sales growth. Acquiring other firms within

the industry is one mechanism to quickly increase market power providing a defense against

overseas competition. In the UK, foreign competition has been a major problem affecting some

industries, particularly Automobiles, Aerospace and Defense, Construction and Electronics. In

the 1990s, the UK Motor industry suffered greatly from foreign competition, which led to low

profitability in the industry. Furthermore, the high value of the pound resulted in the industry

losing ground to overseas imports. There is some similarity (albeit small) in industries impacted

by foreign competition in the US (e.g., Electronics and Motor Vehicle Parts) to those reported

here (see, Mitchell and Mulherin, 1996). To create a proxy for foreign competition, we use a

dummy variable equal to one for those industries sensitive to foreign competition (i.e.,

Aerospace and Defense, Automobile, Auto Parts, Construction, Electronics and Food

Processing) and zero otherwise.

The need for continuous improvement in products and processes is widely publicized.

The mechanisms needed to achieve these improvements are often less clearly defined. Changes

in technology and innovations are largely brought about by research and development activities

(R&D). For example, the Pharmaceutical industry in the UK has and is currently undergoing

rapid technological advances with the aim of improving the quality of their products.

Computers, Telecommunications, Electronics and Media are other sectors that are experiencing

fast technological changes. Technological changes are common to almost all sectors of UK

economy, although it is more dramatic in certain industries. It is argued that the rate of

restructuring, in particular takeovers, should be higher in low technology industries. Such

20

industries are likely to spend less on R&D expenditures, and as such, will have relatively low

growth options. While Mitchell and Mulherin (1996) find significant evidence of takeover

activity being concentrated in low R&D industries for the 1980s, Mulherin and Boone (2000) fail

to find any relationship for the 1990s. In other words, takeovers in the 1990s were not restricted

to industries characterized as having low growth options or low technology levels. We use the

ratio of R&D to sales as a proxy for the level of technological and innovation within an industry.

4.3. Misvaluation

The theoretical discussion in Section 2 posits that takeovers are more likely when

valuation discrepancies occur, that is, when a firm’s market value (MV) is different from its true

or fundamental value (FV). Generally, the theory predicts that takeovers are more likely to occur

when firms are overvalued, i.e., MV>FV, consistent with the observation that merger waves

occur during times of high stock prices. Clearly, the determination of misvaluation is dependent

on correctly measuring a firm’s FV. Unfortunately, no perfect measure of FV exists, hence prior

papers typically adopt proxies for FV, common amongst these being the book value of assets or

FV determined by a valuation model (e.g., residual income). While imperfect in that the proxy

for misvaluation may simply be capturing some other phenomenon, e.g., growth opportunities,

past use suggests a strong correlation with between different proxies proxies.9 For example, Ang

and Cheng (2002) report a correlation coefficient of 72% between MTB and residual income

misvaluation proxies.

Following from prior literature (i.e., Ang and Cheng, 2002), we construct two

misvaluation proxies using the MTB ratio. The first is simply the mean MTB ratio of all firms in

the industry (log MTB). The second proxy is the industry-adjusted MTB, where the mean

21

industry MTB is adjusted for the mean MTB across all industries. Subtracting the mean across

all industries is an attempt to remove economy-wide factors, so that the industry MTB reflects

industry-specific misvaluation effects only.

We also include the standard deviation of TMV in the models to capture the dispersion in

industry size. A higher dispersion between the size of firms within an industry is likely to result

in higher takeover activity with smaller firms targeted by larger, both of which increase activity

within the industry.10 Including the above industry-specific variables to our basic model, we

arrive at the full model,

titititititi

tititititi

STDMISVALTECHFCOMDERGCONFCFGROSHKR

,,9,8,7,6,5

,4,3,2,1,

εβββββββββα

++++++

++++= (2)

simplifying to,

tititiR ,,'

, εβα +Χ+= (3)

where SHK is our proxy for broad economic shocks, GRO is industry growth (measured using

sales, employment and cash flows), FCF is a proxy for free cash flow (industry-adjusted), CON

is a proxy for industry concentration (Herfindahl index), DERG is a dummy variable for

deregulation, FCOM is a dummy variable for foreign competition, TECH is a proxy for

technological innovation (R&D/sales), MISVAL is our proxy for industry misvaluation (Industry

and industry-adjusted MTB) and STD is the standard deviation of industry TMV.

22

6. Results

This section first reports some descriptive statistics and correlation coefficients between

the variable proxies and the rates of takeovers and divestitures. The results of the regressions are

then reported in section 6.2.

6.1. Descriptive statistics

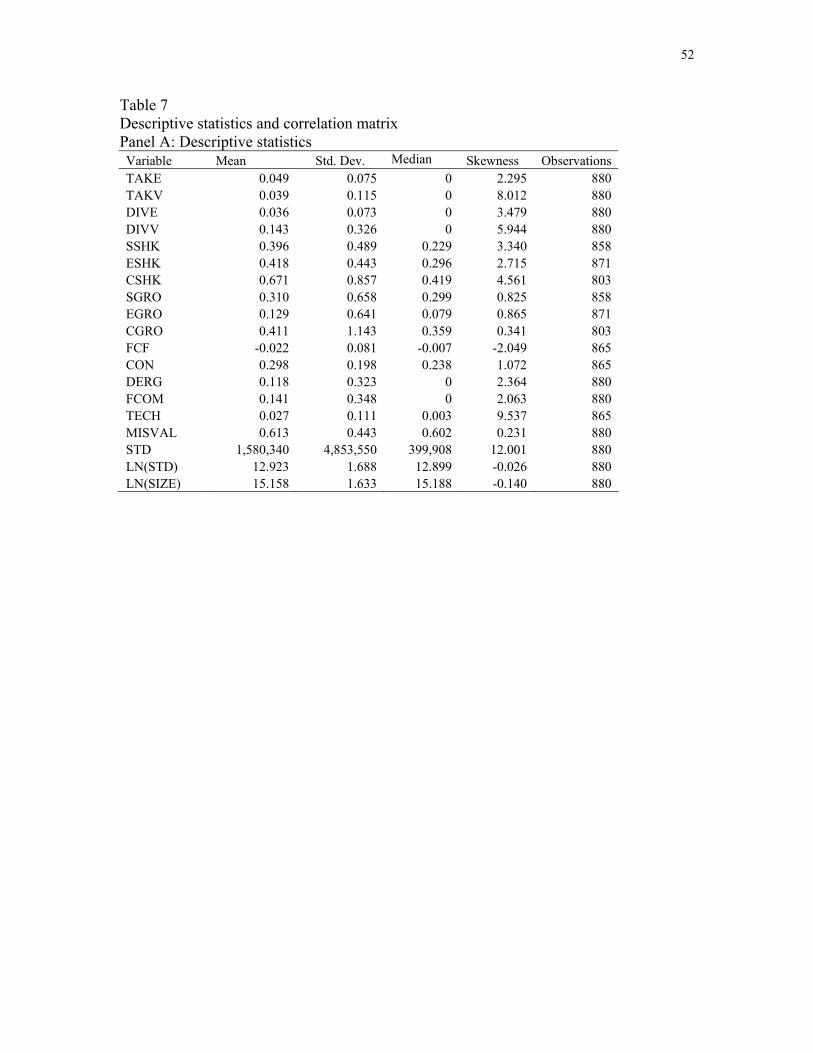

Table 7 presents descriptive statistics (Panel A) and correlation coefficients (Panel B) for

the variables employed in the models. The likelihood of takeover (divestiture) across the sample

period is approximately 5% (3.6%) using equally-weighted proportions. While the likelihood

using value-weighed measures is similar for takeovers, the rate for divestitures increases to about

14%, indicating that divestitures are significantly larger transactions. The mean absolute

deviation of an industry’s growth from the average across all industries (SHK) is approximately

40% when measured using sales (SSHK) and employment (ESHK) data, and 67% for cash flow

data (CSHK). Mean industry growth is positive for all measures (SGRO, EGRO, CGRO),

indicating that industries, on average, experienced increases in sales, the number of employees

and cash flows over the sample period. On average, about 12% and 14% of industries,

respectively, were impacted by deregulation (DERG) and foreign competition (FCOM) over the

sample period. The descriptive statistics indicate that many of the variables are positively

skewed (with the exception of free cash flow, FCF).11

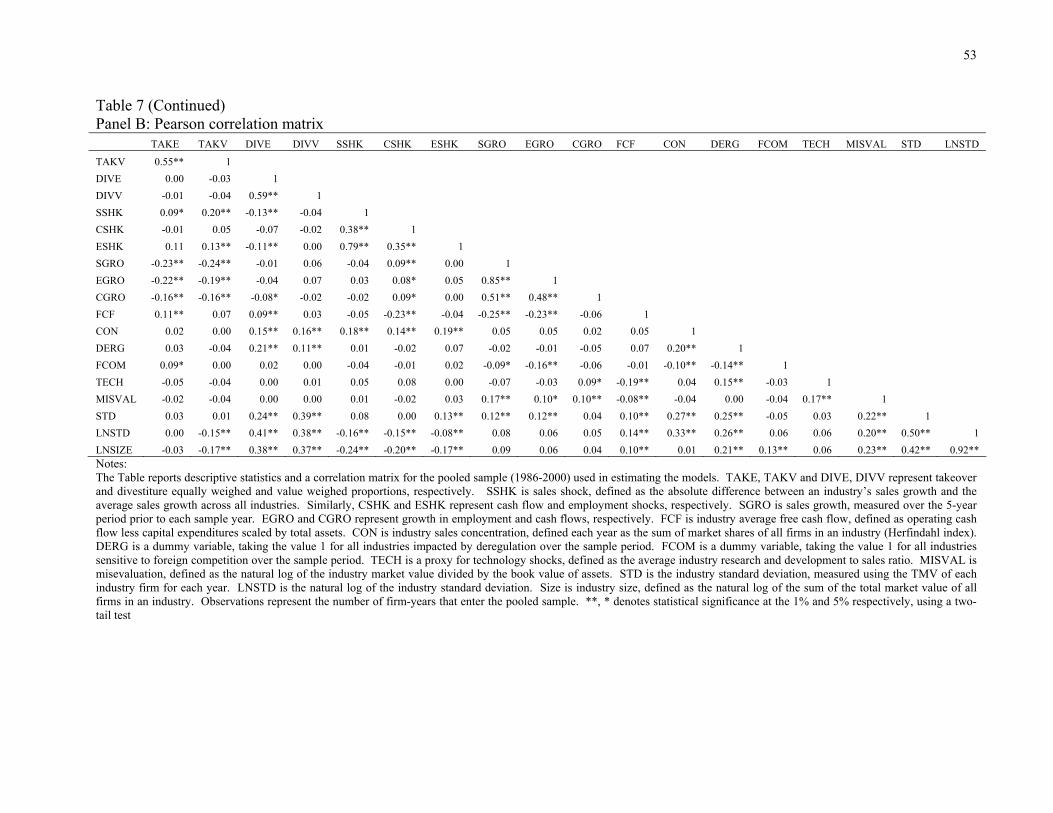

The correlation coefficients presented in Panel B of Table 7 provide more interesting

results. We find a positive and significant correlation between our proxies for broad economic

shocks and takeover activity, with value-weighted proportions providing stronger results. On the

other hand, we find a significant negative relationship between the rate of divestitures and

23

shocks, although the result is sensitive to whether equally or value-weighted proportions are

used. The results suggest that industries sensitive to broad economic shocks are more likely to

experience takeovers, but less likely to experience divestitures. The high correlation between the

different proxies for broad economic shocks indicates that they capture similar economic effects.

Insert Table 7 about here

The correlation between the industry-specific shocks and takeovers and divestiture

activity also provide some insights. First, deregulation (DERG) only appears to have a

significant positive impact on divestiture activity. This result clearly contradicts prior research

documenting a strong link between deregulation and subsequent takeover activity (see, e.g.,

Mitchell and Mulherin, 2000). The lack of significance reported here is due to the pooled sample

design. Examining individual years, in particular the mid to late 1990s, deregulation shows a

positive and significant correlation with takeover activity. Second, the results suggest that

takeovers, and to a lesser extent, divestitures, are more likely to occur in low growth industries.

As expected, divestitures are more likely to occur in large highly concentrated industries.

Interestingly, we also find a significant and positive correlation between misvaluation

(MISVAL), industry growth and technology shocks (TECH). While this supports our hypothesis

that some industry shocks may drive misvaluation, it is more likely that our proxies for industry

growth and technology also proxy for growth options. This result is also robust to the industry-

adjusted measure of misvaluation. Overall, the correlations between the variables entering the

models are fairly low, so multicollinearity should not pose a problem. However, correlation

between variables could still lead to spurious results. As a robustness check, Section 6.3 reports

24

the results of several robustness tests, including, testing the impact of correlated variables,

different proxies for variables, the impact of outliers and alternative regression estimation

methods.

6.2. Regression results

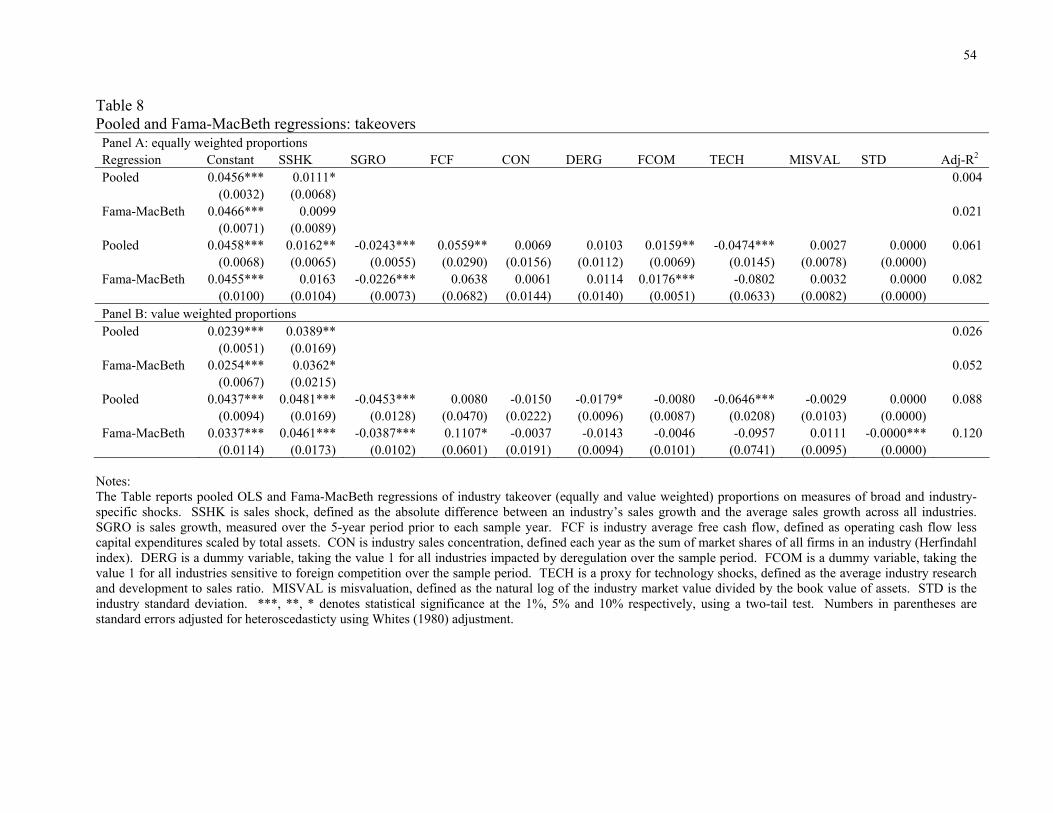

Tables 8 and 9 report the results for the estimated OLS regressions for takeovers and

divestitures, respectively. Equation (1) and (2) are estimated using equally-weighted (Panel A)

and value-weighed (Panel B) proportions for takeovers and divestitures. Both pooled OLS and

Fama and MacBeth (1973) type regressions are estimated and reported in Tables 8 and 9.

Insert Tables 8 and 9 about here

The results reported in Table 8 for equation (1) show evidence of broad economic shocks

(SSHK) increasing the likelihood of takeovers. The results are stronger for value-weighted

proportions (Panel B) and are robust to the Fama and MacBeth (1973) regression method.

Controlling for industry-specific factors (equation 2) does not alter our conclusions on the impact

of broad economic shocks on takeover activity. However, while economic shocks impact on

takeover activity, the magnitude of the impact is small. For example, using value-weighted

proportions (Panel B), the results suggest that a 10% deviation in industry sales growth from the

population average leads to only a 0.5% increase in takeover activity in an industry. This is

significantly lower than the 4.6% reported by Mitchell and Mulherin (1996).12

The results for equation 2 suggest that some industry-specific factors impact on the

likelihood of takeover, but are sensitive to whether equally or value-weighted proportions are

25

used. Industry growth (GRO) is the exception, indicating strong evidence of a significant

negative relationship between sales growth and the likelihood of takeover. This result suggests

that takeovers are more likely to occur in low growth industries, indicating maybe, the need for

firms to exit via takeover from low growth or declining industries. There is some evidence that

foreign competition (FCOM) increases the likelihood of smaller transactions, with a significant

positive relationship using equally-weighted proportions, but not for value-weighted proportions.

High industry free cash flows (FCF) also seems to be a characteristic that attracts takeover

activity, providing some support for Jensen’s (1986) free cash flow theory. Furthermore, while

there is some evidence of lower takeover activity in technological intensive (TECH) or high

R&D industries, the results are not robust to the Fama and MacBeth (1973) regression procedure.

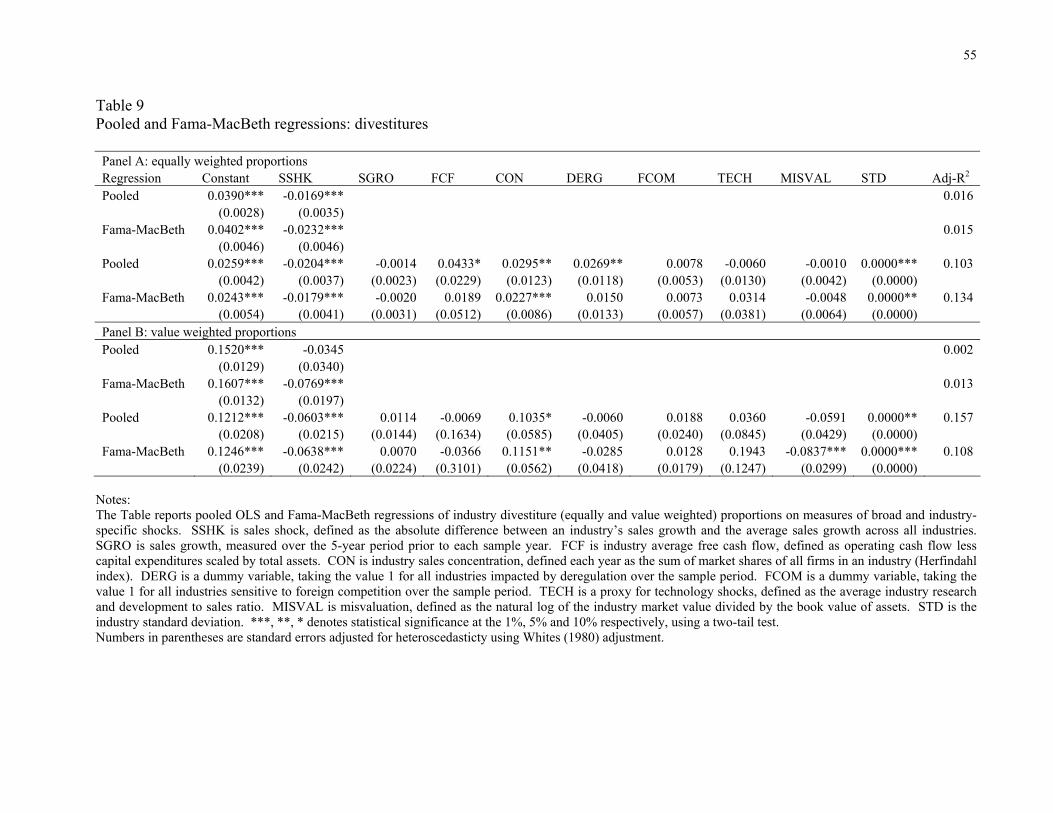

Table 9 reports the results for divestitures. The results for equation (1) indicate that

broad economic shocks decrease the likelihood of divestitures (Panel A), although there appears

to be some sensitivity when value-weighted proportions are used in a pooled model (Panel B).

Controlling for industry-specific factors (equation 2) suggests strong evidence of a negative

relationship between broad shocks and the likelihood of divestitures. Also, the results for both

pooled and Fama and MacBeth (1973) regressions suggest that a few industry-specific factors

impact significantly on the likelihood of divestitures. For example, a higher dispersion in

industry size (STD) and higher industry concentration (CON) are characteristics which seem to

increase the likelihood of divestitures. The negative and significant sign on MISVAL (Panel B)

suggests that undervalued industries are more likely to divest.

26

6.3. Robustness tests

To confirm that our inferences above are robust, and not the result of spurious

regressions, we perform the following additional tests. First, we use alternative proxies for broad

and industry-specific shocks. The regressions are re-estimated using employment and cash flow

data to estimate the variables SHK and GRO. Furthermore, FCF and MISVAL are measured as

industry-adjusted variables, as opposed to industry averages. Second, we test the sensitivity of

the results to the exclusion of several variables that are significantly correlated (see Table 7,

Panel B). Third, we test the suitability of OLS as an estimation method in light of the level of

skewness in some of the variables (see Table 7, Panel A) and, furthermore, the censored nature

of takeover and divestiture proportions. OLS may not be appropriate for data where the

dependent variable lies between 0 and 1. To address these issues we address the problem of

outliers in the sample and use censored regressions methods. Fourth, we re-estimate the takeover

models using industry proportions estimated from the acquiring firm’s perspective, as opposed to

the takeover target’s perspective. Theories of misvaluation are more likely to hold for acquiring

firm industries, which are more likely to be overvalued, as opposed to target firm industries,

which could be either over or undervalued (Shleifer and Vishny, 2003).13

Substituting employment and cash flows definitions for SHK and GRO measured using

sales results in no significant change to the results reported in Tables 8 and 9. The high positive

and significant correlations between different shock and growth proxies, as reported in Table 7

(Panel B), suggests that we should not be too surprised by the robustness of the impact of broad

economic shocks, whether measured using sales, employment or cash flow data. Substituting

industry adjusted measures for free cash flow (FCF) and misvaluation (MISVAL) also has no

significant impact on our results. Estimating the regressions using a forward and backward step-

27

wise procedure, by adding one variable at a time or removing one variable at a time from the full

model, indicates that only one variable, STD, has a minor impact on the significance of other

variables. In particular, when STD is removed from the takeover regressions, deregulation

changes from being negative and significant for value-weighed proportions to negative and

insignificant. For divestitures, the only change is an increase in the statistical significance for

concentration (CON) for both equal and value-weighted proportions.14 All other regression

results remain unchanged.

While re-estimating the models using a pooled sample with outliers winsorized results in

a significant decrease in the skewness of the variables, the significance of the variables remains

unchanged, suggesting that OLS is fairly robust to some skewness in variables. Re-estimating

the models using tobit regressions results in minor changes as follows: (1) for takeovers,

concentration (CON) changes from statistically insignificant to negative and significant for

equally and value-weighted proportions; (2) for divestitures, foreign competition (FCOM)

changes from positive and insignificant to positive and significant for both equally and value-

weighted proportions; (3) the constant terms for all regressions become insignificant. Overall,

the OLS results are fairly robust to different estimation methods.

Lastly, we re-examine the robustness of insignificant results for the impact of industry

misvaluation (MISVAL) on the likelihood of takeovers. The theory suggests that overvalued

acquiring firms are likely to use their inflated stock to bid for targets. Since we use takeover

proportions derived from industries targeted by takeover, our results could be biased against

finding industry overvaluation significant, since target industries may be under or overvalued

(Shelifer and Vishny, 2003). We re-estimate the takeover models substituting industry takeover

proportions based on the acquiring firm’s industry for proportions based on the target firm’s

28

industry. While the coefficient for MISVAL is positive, it remains insignificant indicating that

misvaluation at the industry level does not significantly impact on the likelihood of takeover

activity. The result suggests that overvalued acquiring firms do not cluster across certain

industries.

6.4 Discussion of the main results

To summarize, the regression results suggest that broad economic shocks significantly

increase (decrease) the likelihood of takeovers (divestitures). For takeovers, industry-specific

factors, such as growth (GRO), free cash flow (FCF) and the threat of foreign competition

(FCOM) seem to have an impact on takeover likelihood. For divestitures, only concentration

(CON), and the variation in industry size (STD) seem to play a significant role in explaining

divestitures at the industry level. For the 1980s period in the US, Mitchell and Mulherin (1996)

find broad economic shocks plus two industry-specific factors, deregulation and technological

(R&D/sales) to be significant in explaining actual takeovers at the industry level. The results

from this paper support broad economic shocks, but fail to find convincing robust statistical

evidence for deregulation and technology factors. While we do find technology significant using

a pooled OLS regression, the robustness of this result becomes suspect when we use the Fama

and MacBeth (1973) regression method.

As for deregulation, our results suggest that it is important in explaining takeovers, but

only for one or two years in the latter part of the 1990s. This result makes intuitive sense

because the full effects of deregulation for many industries in the UK only became realized when

the UK government’s ‘golden share’ in these industries expired. For example, while the

Electricity industry was deregulated in July of 1989, takeovers only become possible from March

29

1995, when the government’s ‘golden share’ expired, which restricted any single private entity

stake to 15%. As expected, immediately after March 1995, the Electricity industry experienced

several takeover bids. In fact, two thirds of all takeovers in the Electricity industry occurred

within the two year period, 1995-1996 (see Table 5).15 Other deregulated industries in Water,

Telecommunications and Oil and Gas faced similar restrictions to control changes post-

deregulation through the use of the ‘golden share’. Interestingly, deregulated industries in the

US did not face these restrictions, allowing for higher takeover activity immediately after

deregulation.16

7. Summary and conclusions

This paper provides evidence of clustering across industries and time in the rates of

takeover and divestitures. The paper then attempts to explain clustering using proxies for broad

economic shocks, misvaluation and industry-specific shocks. The results provide evidence to

support broad shocks increasing (decreasing) the likelihood of takeovers (divestitures). Industry-

specific factors appear to play less of a significant role in explaining both takeovers and

divestitures, although some factors are important, particularly growth, free cash flow and foreign

competition for takeovers. Little evidence is found for deregulation as a significant factor in

explaining takeover activity over the pooled sample period. Further investigation reveals that

deregulation is important, but only for the latter part of the 1990s when the full effects of

deregulation were felt when the UK government’s ‘golden share’ expired in some deregulated

industries.

The paper has implications for researchers interested in modeling takeovers and

divestitures. Researchers, for example, may be interested in predicting takeovers with a view to

30

developing a successful investment strategy (Palepu, 1986). The results suggest that prediction

models may benefit from the inclusion of variables that capture broad economic and industry-

specific factors, as opposed to the norm of including only firm-level variables.

31

Notes

1. We carefully reconstruct the population of firms each year because Datastream removes

‘dead’ firms from its lists, so the constituents of industries at the time of extracting the

data would not be representative of the ‘true’ constituents at the beginning of the sample

period. So, for example, the list of firms in the Datastream Metals industry for December

1984, extracted in December 2003, would include only firms that survived the period

December 1984 to December 2003. Any firms that died between these dates would be

removed from the industry list by Datastream and placed in a ‘dead’ companies list.

Naturally, this would inflict a serious survivorship bias on any sample constructed solely

from the current Datastream industry lists. In order to avoid this bias, we reconstructed

the ‘true’ population of firms each year using the official stock exchange list, the

alternative investment market list (i.e., small capitalization list) and the dead companies

list.

2. A firm is classified as ‘live’ in a given year if it reported total assets (DS#392). We use

total assets because it is reported by both financial and industrial firms.

3. Using an average conversion rate of $US/£0.61over the period 1986-2000 provides an

industry average TMV for our sample of $US of approximately $16.4 billion. More

specifically, if we examine the 1990 period for the UK, our sample provides an average

industry TMV of approximately £7.8 billion or $US12.5, using the appropriate currency

rate for the beginning of 1990 ($US/£0.62). Hence, even matching by time, the average

size of US industries is significantly larger. This is not surprising since both Mitchell and

32

Mulherin (1996) and Mulherin and Boone (2000) use firms identified from the Value

Line Investment Survey, which represents the largest and most actively traded firms in

the US. Furthermore, the US market is larger than the UK, so even if both US papers

used all firms in their sample construction, the TMV of industries is still likely to be

larger than the UK.

4. A takeover occurs when the acquiring firm accumulates a controlling interest in the target

firm, either through a friendly (with the agreement of the target management) or hostile

bid (rejected by management). A divestiture is defined as the sale of a subsidiary by the

parent company to a third party (otherwise known as a sell-off) or to management

(otherwise known as a management buyout).

5. While Mitchell and Mulherin (2000) use US$100 million as their selection criteria for

‘major’ divestitures, we use the lower value of US$50 million due to the smaller size of

UK transactions. Note, that if we adopted a US$100 million cut-off, the number of

divestitures in our sample would fall to about 342 (or 60% of the current sample).

6. The Pearson χ2 is defined as Σi (Actuali - Expectedi)2 / Expectedi., where i represents the

925 industry-years in the sample and expectedi equals the product of the average takeover

(divestiture) activity for the full sample times the number of firms in the ith industry.

7. The Pearson χ2 and Likelihood Ratio Tests computed using value-weighted averages are

similar to those reported in Table 4.

33

8. There is one important caveat: For several deregulated industries (e.g., Electricity and

Water), corporate control changes were prevented for a period of up to 5 years following

deregulation by the use of the ‘golden share’ by the UK government. The ‘golden share’

simply restricts private equity ownership to 15%, hence preventing control changes

through takeovers. For affected industries, the deregulation dummy only takes a value of

1 for the period after the UK government’s ‘golden share’ expired. For example,

although the Electricity industry was deregulated at the end of 1989, the UK

government’s golden share did not expire until 1995.

9. Note that we control for growth in the estimated models by using growth in sales of the

industry, measured over the previous 5 years.

10. Note that using a measure of dispersion within an industry ignores takeovers that occur

outside the industry (i.e., diversified takeovers). Put differently, while a large dispersion

in industry size facilitates takeovers within an industry between large and small firms, it

says little about large firms acquiring smaller firms from outside the industry. Hence, if

takeovers are more likely to be diversified, it is unclear what sign the dispersion measure

should take. As an alternative measure, we use the natural log of the industry total

market value. Since smaller firms are more likely to be acquired, this result may extend

to smaller industries, indicating a negative relationship. However, given the uncertainty

attached to both measures, we do not specify an exact relationship.

34

11. Section 6.3 discusses some robustness tests conducted, including the winsorizing of

outliers, defined as those observations that lie ± 3 standard deviations from the mean for a

given variable. While winsorizing significantly reduces the skewness of all variables, the

results of the estimated models remain unchanged. For brevity, we report only the results

for the models estimated using unwinsorized data. All unreported results, including

robustness tests reported in Section 6.3, are available from the authors upon request.

12. On examining the yearly regression, the results show that 1996 records the highest

sensitivity to sales shocks, with a 2.2% increase in takeover activity for a 10% deviation

in industry sales growth from the population.

13. Clearly, this view makes the implicit assumption that overvalued acquirers cluster across

specific industries. If overvaluation is firm-specific, we should expect no correlation

between proxies for misvaluation and bidder activity.

14. We substitute the natural log of STD (LNSTD) for the absolute value of STD. For the

value-weighed takeover regression, the coefficient is negative and significant, suggesting

that takeovers are targeted at industries with lower dispersion in size. All other results

remain unchanged. We also test the sensitivity of the results to the natural log of industry

TMV (LNSIZE). The coefficient on LNSIZE is negative and significant for the value-

weighed takeover regression, suggesting that takeovers are directed at smaller industries.

The result is not surprising given the highly significant correlation (0.92) between

LNSTD and LNSIZE (see Table 7, Panel B).

35

15. Schoenberg and Reeves (1999) report evidence of deregulation, industry growth and

concentration as significant factors in determining takeover likelihood at the industry

level in the UK. The authors compile a sample of 200 UK industries over the period

1991 to 1995 and calculate the level of takeover activity as the sum of the number of

takeovers in each industry times the average takeover value. They sort their sample into

two groups based on the value measure, but only select the top and bottom 10%, giving a

total of only 40 industries. We replicate the Schoenberg and Reeves (1999) methodology

by sorting the total value of all takeovers within the 71 industries in our sample over the

sample period, 1986-2000. We select the top 20 and bottom 20 industries and re-estimate

the OLS models. The results provide strong evidence for deregulation, concentration,

foreign competition and industry standard deviation. The explanatory power of the

takeover model is also significantly larger, 36% compared to the 8% reported in Table 8,

Panel B. Clearly, self selecting the estimation sample to include only the largest and

smallest transactions gives rise to significantly better results.

16. The usual explanation for the use of ‘golden shares’, which are used predominantly by

European governments, is to safeguard strategic interests from foreign buyers, such as

defense or energy supply. A political explanation also exists in that retaining control of

valuable utilities, governments can ally the fears of potential voters that state-owned

assets are being taken out of public hands. This explanation is often used to explain the

first use of the ‘golden share’ by the UK Thatcher government in the 1980s.

Interestingly, the European Court of Justice, the EU’s highest court, ruled in favour of the

36

European Commission in 2002 and 2003 in cases against ‘golden shares’ in the UK,

Spain, France and Portugal. Hence, the demise of the ‘golden share’ in Europe is fast

approaching.

37

References

Andrade, G., Mitchell, M., Stafford, E., 2001. New evidence and perspectives on mergers.

Journal of Economic Perspectives 15, 103-120.

Ang, J., Cheng, Y., 2002. Direct evidence on the market driven acquisitions theory. Flordia State

University Working Paper.

Baltagi, B.H., 2001. Econometric analysis of panel data, 2nd Edition. John Wiley and Sons Ltd,

England, UK.

Coase, R.H., 1937. The nature of the firm. Economica 4, 386-405.

Fama, E.F., French, K.R., 2002. Testing trade-off and pecking order predictions about dividends

and debt. Review of Financial Studies 15, 1-33.

Fama, E.F., MacBeth, J.D., 1973. Risk, return, and equilibrium: Empirical tests. Journal of

Political Economy 81, 607-636.

Gort, M., 1969. An economic disturbance theory of mergers. Quarterly Journal of Economics 83,

624-642.

Greene, W., 2000. Econometric Analysis, Fourth Edition. Prentice Hall International, New

Jersey, US.

Gujarati, D.N., 2003. Basic Econometrics, Fourth Edition. McGraw-Hill, New York, US.

Holmstrom, B. Kaplan, S., 2001. Corporate governance and merger activity in the United States:

Making sense of the 1980s and 1990s. Journal of Economic Perspectives 15, 121-145.

Jovanovic, B., Rousseau, P., 2001. Mergers and technological change: 1885-2001. New York

University Working Paper.

Jovanovic, B., Rousseau, P., 2002. The Q-theory of mergers. American Economic Review 92,

198-204.

38

Jensen, M. C., 1986. Agency costs of free cash flow, corporate finance and takeovers. American

Economic Review 76, 323-329.

Jensen, M. C., 1989. Eclipse of the public corporation. Harvard Business Review (September-

October), 60-74.

Jensen, M. C., 1993. The modern industrial revolution and the challenge to the internal control

systems. Journal of Finance 48, 831-880.

Johnston, J., 1984. Econometric methods, 3rd ed. McGraw-Hill, New York, NY.

Liebeskind, J.L., Opler, T.C., Hatfield, D.E., 1996. Corporate restructuring and the

consolidation of US industry. Journal of Industrial Economics 44, 53-68.

McGowan, J., 1971. International comparisons of merger activity. The Journal of Law and

Economics 14, 233-251

Mitchell, M.L., Mulherin, J.H., 1996. The impact of industry shocks on takeover and

restructuring activity. Journal of Financial Economics 41, 193-229.

Mulherin, J.H., Boone, A.L., 2000. Comparing acquisitions and divestitures. Journal of

Corporate Finance 6, 117-139.

Myers, S.C., Majluf, N.S., 1984. Corporate financing and investment decisions when firms have

information that investors do not have. Journal of Financial Economics 35, 99-122.

Nelson, R., 1959. Merger movements in American industry, 1895-1956. Princeton University

Press, Princeton NJ.

Palepu, K.G., 1986. Predicting takeover targets: A methodological and empirical anaysis.

Journal of Accounting and Economics 8, 3-35.

Ratnayake, R., 1999. Industry concentration and competition: New Zealand experience.

International Journal of Industrial Organisation 17, 1041-1057.

39

Rhodes-Kropf, M., Viswanathan, S., 2003. Market valuation and merger waves. Columbia

University Working Paper.

Rose, N.L., 1985. The incidence of regulatory rents in the motor carrier industry. Rand Journal

of Economics 16, 299-318.

Schoenberg, R., Reeves, R., 1999. What determines acquisition activity within an industry?

European Management Journal 17, 93-98.

Shleifer, A., Vishny, R., 2003. Stock market driven acquisitions. Journal of Financial

Economics 70, 295-311.

Weston, J.F., 1953. The role of mergers in the growth of large firms. University of California

Press, Berkeley and Los Angeles.

40

Table 1 Industry distribution of sample firms

Industry Name Industry

code

Average number of firms

% of sample

Industry average value (£000's) % Value

Building Materials 30 43 3.33 28,380,139 3.98 Builders Merchants 32 16 1.27 2,943,307 0.41 Chemicals, Speciality 33 20 1.54 7,655,966 1.07 Computer Hardware 34 9 0.68 214,622 0.03 Farming And Fishing 35 10 0.79 256,806 0.04 House Building 36 37 2.88 4,818,183 0.68 Electrical Equipment 37 23 1.77 1,527,048 0.21 Other Construction 39 27 2.05 4,026,350 0.57 Delivery Services 40 7 0.50 279,790 0.04 Media Agencies 41 22 1.72 3,377,288 0.47 Engineering Contractors 43 15 1.19 920,160 0.13 Defence 44 5 0.39 10,502,175 1.47 Transaction + Payroll 46 16 1.27 815,560 0.11 Environmental Control 47 6 0.45 2,042,096 0.29 Hospital Management 49 6 0.49 705,197 0.10 Oil + Gas Exploration/Production 50 19 1.49 7,324,046 1.03 Oil Services 51 6 0.43 447,732 0.06 Non-Ferrous Metals 54 7 0.57 218,728 0.03 Leisure Facilities 55 33 2.57 5,903,798 0.83 Steel 56 6 0.45 3,149,577 0.44 Electronic Equipment 57 61 4.70 10,012,825 1.41 Software 58 31 2.40 2,837,962 0.40 Hsehold Appliances + Hsewares 59 12 0.91 272,661 0.04 Furniture + Floor covering 60 20 1.56 675,265 0.09 Leisure Equipment 61 9 0.66 227,627 0.03 Household Products 62 5 0.39 4,893,543 0.69 Auto Parts 63 14 1.07 2,434,136 0.34 Vehicle Distribution 64 23 1.75 2,676,041 0.38 Retailers, Soft Goods 66 21 1.59 7,007,943 0.98 Brewers 67 5 0.39 782,497 0.11 Distillers + Vintners 68 9 0.67 16,113,432 2.26 Clothing + Footwear 69 31 2.42 1,313,795 0.18 Other Health Care 70 5 0.39 1,476,732 0.21 Food Processors 71 41 3.20 34,359,026 4.82 Restaurants + Pubs 72 31 2.37 12,228,024 1.72 Engineering, General 74 75 5.78 23,004,882 3.23 Consumer Electronics 75 17 1.29 1,371,228 0.19 Textiles + Leather Goods 78 25 1.91 2,182,443 0.31 Hotels 80 14 1.09 8,411,727 1.18 Security And Alarms 81 7 0.52 885,078 0.12 Paper 82 5 0.41 2,431,439 0.34 Food + Drug Retailers 83 18 1.41 20,606,397 2.89 Publishing + Printing 84 48 3.73 28,593,709 4.01 Business Support 86 75 5.77 17,675,403 2.48 Retailers, Multi Dept 87 17 1.32 22,114,258 3.10

41

Table 1 (Continued)

Industry Name Industry

code

Average number of firms

% of sample

Industry average value (£000's) % Value

Retail, Hard lines 90 35 2.72 4,657,454 0.65 Chemicals, Commodity 92 10 0.75 7,970,673 1.12 Chemicals Advanced Materials 93 7 0.56 1,004,716 0.14 TV, Radio + Film 94 27 2.05 3,446,935 0.48 Pharmaceuticals 95 12 0.90 55,151,377 7.74 Oil Integrated 97 7 0.54 44,235,743 6.21 Aerospace 98 14 1.08 5,403,645 0.76 Shipping + Ports 99 12 0.91 6,447,532 0.91 Gambling 100 8 0.60 1,237,403 0.17 Diversified Industry 101 12 0.94 1,072,348 0.15 Banks 102 9 0.72 100,841,513 14.16 Gold Mining 119 5 0.39 71,798 0.01 Eng. Fabricators 120 22 1.66 640,584 0.09 Other Mining 122 9 0.68 14,723,432 2.07 Telecom Equipment 126 7 0.54 11,067,723 1.55 Airlines + Airports 129 7 0.53 12,716,335 1.79 Rail, Road, Freight 131 17 1.34 6,161,309 0.86 Med Equip + Supplies 132 21 1.64 3,583,511 0.50 Education + Training 134 13 1.04 491,650 0.07 Electricity 140 13 0.98 24,655,969 3.46 Telecom Fixed Line 142 6 0.50 44,540,962 6.25 Telecom Wireless 143 5 0.41 30,142,867 4.23 Water 144 17 1.29 15,491,432 2.17 Computer Services 150 25 1.90 3,828,309 0.54 Internet 151 9 0.71 625,987 0.09 Biotechnology 157 15 1.13 2,019,470 0.28 Total 1,294 712,327,316 Mean 18.23 10,032,779 Median 13.93 3,583,511 Standard Deviation 15.06 16,076,540

Notes: The Table reports the average number of firms in each industry as a percentage of the population of firms (% of sample) over the sample period. The industry code is Datastream’s level 6, which is similar to SIC 4. Industry average value is measured as industry average total market value (TMV). % Value is calculated as the industry average TMV as a percentage of the population of firms. TMV is calculated as the sum of the market value of equity plus the book value of debt, measured at the beginning of each year.

42

Table 2 Takeover, divestiture activity and stock performance over the sample period Takeovers Divestitures Stock performance

Year Number % Equal Value (£000's) %

Value Number % Equal Value (£000's) % Value Cumulative average

returns 1986 74 7.82 3,066,483 1.05 9 1.60 23,869,597 0.76 33.86% 1987 74 7.82 3,624,801 1.24 14 2.49 27,448,820 0.87 30.84% 1988 69 7.29 7,504,793 2.58 28 4.98 57,420,116 1.83 22.04% 1989 55 5.81 9,917,358 3.40 37 6.58 93,355,570 2.97 2.99% 1990 53 5.60 3,922,629 1.35 37 6.58 76,125,477 2.42 -16.37% 1991 41 4.33 5,460,970 1.87 24 4.27 119,301,211 3.80 21.63% 1992 22 2.33 3,561,571 1.22 28 4.98 102,957,378 3.28 6.55% 1993 28 2.96 1,719,958 0.59 35 6.23 157,834,425 5.02 21.60% 1994 25 2.64 1,834,991 0.63 31 5.52 149,957,985 4.77 1.75% 1995 45 4.76 31,974,634 10.97 40 7.12 136,030,652 4.33 9.23% 1996 46 4.86 17,671,604 6.06 40 7.12 221,222,888 7.04 13.00% 1997 62 6.55 14,062,802 4.83 59 10.50 327,804,980 10.43 6.36% 1998 94 9.94 18,177,858 6.24 55 9.79 321,783,518 10.24 7.60% 1999 144 15.22 118,755,238 40.75 61 10.85 488,823,693 15.56 24.00% 2000 114 12.05 50,133,213 17.20 64 11.39 838,259,535 26.68 40.45% Total events 946 100.00 291,388,903 100.00 562 100.00 3,142,195,845 100.00 Mean 63 6.67 19,425,927 6.67 37.47 6.67 209,479,723 6.67 15.04% Median 55 5.81 7,504,793 2.58 37.00 6.58 136,030,652 4.33 13.00% Standard Dev. 34 3.58 30,542,644 10.48 16.50 2.94 216,004,083 6.87 14.68%

Notes: The Table reports the number of successful takeovers and divestitures over the sample period 1986 to 2000. Information on restructuring events is compiled from SDC platinum and Acquisitions Monthly. Divestitures represent the number of firms that sold subsidiaries with a value of at least $US50 million to third parties, including management. Of the 562 firms that made divestitures, 29 were later acquired. The Table omits bankruptcies, which account for 103 firms over the sample period. % Equal is calculated as the number of transactions each calendar year divided by the number of firms in the population at the beginning of the year. Value is the total market value (TMV) of all transactions, calculated at the beginning of the year. % Value is the TMV of all transactions as a percentage of the TMV of the population of firms, measured as the beginning of the year. Cumulative average returns are calculated by summing the average 12 monthly cross-sectional returns for all firms in the population for each year.

43

Table 3 Industry distribution of takeovers and divestitures Panel A: Equally weighted proportions

Industry Name Industry

code Number of takeovers % Equal

Number of divestitures % Equal

Building Materials 30 32 3.38 42 7.47 Builders Merchants 32 18 1.90 6 1.07 Chemicals, Speciality 33 10 1.06 19 3.38 Computer Hardware 34 0 0.00 1 0.18 Farming + Fishing 35 0 0.00 0 0.00 House Building 36 22 2.33 5 0.89 Electrical Equipment 37 25 2.64 1 0.18 Other Construction 39 11 1.16 3 0.53 Delivery Services 40 6 0.63 0 0.00 Media Agencies 41 16 1.69 4 0.71 Engineering Contractors 43 19 2.01 3 0.53 Defence 44 0 0.00 1 0.18 Transaction + Payroll 46 15 1.59 1 0.18 Environmental Control 47 6 0.63 0 0.00 Hospital Management 49 2 0.21 1 0.18 Oil + Gas Exploration/Prod. 50 16 1.69 8 1.42 Oil Services 51 5 0.53 0 0.00 Non-Ferrous Metals 54 4 0.42 0 0.00 Leisure Facilities 55 37 3.91 9 1.60 Steel 56 2 0.21 3 0.53 Electronic Equipment 57 81 8.56 18 3.20 Software 58 17 1.80 3 0.53 Hsehold Appliances + Hsewares 59 1 0.11 0 0.00 Furniture + Floor covering 60 13 1.37 1 0.18 Leisure Equipment 61 3 0.32 0 0.00 Household Products 62 0 0.00 0 0.00 Auto Parts 63 13 1.37 6 1.07 Vehicle Distribution 64 20 2.11 9 1.60 Retailers, Soft Goods 66 3 0.32 19 3.38 Brewers 67 2 0.21 0 0.00 Distillers + Vintners 68 4 0.42 15 2.67 Clothing + Footwear 69 21 2.22 2 0.36 Other Health Care 70 0 0.00 0 0.00 Food Processors 71 37 3.91 40 7.12 Restaurants + Pubs 72 13 1.37 21 3.74 Engineering, General 74 64 6.77 43 7.65 Consumer Electronics 75 27 2.85 3 0.53 Textiles + Leather Goods 78 20 2.11 3 0.53 Hotels 80 19 2.01 19 3.38 Security + Alarms 81 6 0.63 2 0.36 Paper 82 3 0.32 0 0.00 Food + Drug Retailers 83 11 1.16 11 1.96 Publishing + Printing 84 43 4.55 32 5.69 Business Support 86 42 4.44 28 4.98 Retailers, Multi Dept 87 6 0.63 11 1.96

44

Table 3 Panel A (Continued)

Industry Name Industry

code Number of takeovers % Equal

Number of divestitures % Equal