industry q&a focus engagement issues · platform gets $15m california-based chinese...

TRANSCRIPT

Asia’s Private Equity News Source avcj.com March 01 2016 Volume 29 Number 08

FOCUS ANALYSIS

Engagement issuesStrategic investors, private equity target China’s media value chain Page 9

Returns on researchPharma presents choices for corporate VC Page 12

Automation agendaGPs eye cross-border industrial strategies Page 15

Data f ile Page 23

AVCJ RESEARCH

PRE-CONFERENCE ISSUE AVCJ PRIVATE EQUITY AND VENTURE CAPITAL FORUM CHINA 2016

Jonathan Li and XinWang of BHR Partners

Page 19

INDUSTRY Q&A

Investors suffer due toonline fundraising scams

Page 20

FOCUS

China-US acquisitions face regulatory scrutiny

Page 3

Asia Climate Partners, BanyanTree, Brookfield, CIC, CPPIB, GIC, IvyCap, Monk’s Hill, Shunwei, TCL, Tsinghua Unigroup, Warburg Pincus

Page 5

EDITOR’S VIEWPOINT

NEWS

Unlocking liquidity for private equity investors

www.collercapital.com London, New York, Hong Kong

Anything is possible if you work with the right partner

Number 08 | Volume 29 | March 01 2016 | avcj.com 3

EDITOR’S [email protected]

NO OFFICIAL REASON WAS GIVEN FOR the regulatory decision that led to Procon Mining & Tunnelling – which is controlled by China National Machinery Industry Corporation – unwinding its acquisition of Canada-based Lincoln Mining in 2013. The unofficial explanation was that one of Lincoln’s facilities was too close to Fallon Naval Air Station in Nevada, home to the US Navy’s TOPGUN flight school.

This investment would receive the prize for most bizarre (alleged) grounds for rejection by the Committee on Foreign Investment in the United States (CFIUS), but TOPGUN is said to have thwarted two other Chinese M&A transactions.

While it seems odd that Procon didn’t approach the regulators prior to the deal closing and seek a compromise solution, the company might not have realized it needed to do so. Lincoln is Canadian by incorporation – so on the surface it could appear beyond CFIUS’ purview – but its principal mining operations are in the US and any change in ultimate ownership must be signed off by the authorities.

Procon’s misfortune underlines the importance of good advice when dealing with a regulator that reviews the national security implications of foreign investments in companies with US operations, has the power of veto, yet is under no obligation to explain its decisions publicly. With Chinese outbound M&A at record levels – and Sino-US political relations bedeviled by issues ranging from territorial sovereignty to state-sponsored electronic espionage – perhaps it has never been more important.

According to its annual report to Congress on activities from the 2014 calendar year, CFIUS reviewed 147 filings, up 50% year-on-year and not far off the all time high of 155 from 2008. China accounted for 24 of the filings, more than any other country, retaining a position it first occupied in 2012.

CFIUS has already made an impact on several China transactions in 2016. In January, Go Scale Capital – a private equity firm sponsored by GSR Ventures and Oak Investment Partners – terminated its deal to buy a majority stake in Philips’ LED components and automotive lighting unit due to “unforeseen concerns” from the regulator. Both companies made their case

“under the principles of openness and fairness,” with Go Scale stressing its commercial and market-oriented interests, but to no avail.

The wasted process has cost Philips time and a bit of money; and the company will no doubt be more wary when it puts the asset up for auction once again. Such considerations were likely uppermost in the minds of board members at Fairchild Semiconductor International when they rejected a take-private bid from China Resources Microelectronics and Hua Capital in February. The board said the risk of rejection by CFIUS was too great, regardless of the buyer consortium’s offer to pay a $108 million break fee if approval was not forthcoming.

The following week, China’s Tsinghua Unigroup scrapped its plan to invest in US-based disk drive manufacturer Western Digital after CFIUS decided to launch a review of the transaction.

When CFIUS said in its annual report that there may be a coordinated strategy among foreign governments or companies to acquire US firms involved in the development of critical technologies, it might have been referring to semiconductors. Unigroup has made no secret of its desire to become a major player in the sector and has launched several aggressive bids for assets around the world. It is unclear whether the company really expects to be successful in some of these situations or is just testing the water as part of a longer-term strategy.

What this probably has done is heighten the sensitivity around all Chinese outbound deals targeting the US. The majority of these transactions will get through, but prospective investors would be advised to ensure they have covered all the bases – to the point of identifying areas in which they might have to appease the regulator and mitigate security concerns. The last thing companies want is to see the crown jewel of an outbound strategy torn from their grasp by a retrospective ruling.

Tim BurroughsManaging EditorAsian Venture Capital Journal

Regulatory risks Managing Editor

Tim Burroughs (852) 2158 9661

Associate Editor

Winnie Liu (852) 2158 9663

Staff Writer

Holden Mann (852) 2158 9646

Justin Niessner (852) 2158 9678

Design

Edith Leung, Mansfield Hor

Events

George Sengulovski,

Jessie Chan, Jonathon Cohen,

Sarah Doyle,

Amelie Poon, Fiona Keung,

Jovial Chung,

Marketing

Agrina Sandri, Priscilla Chu,

Yasna Mostofi

Research

Helen Lee, Herbert Yum,

Jason Chong,

Kaho Mak, Tim Wong,

Sales

Anil Nathani,

Darryl Mag, Debbie Koo,

Samuel Lau,

Pauline Chen

Subscriptions

Jade Chan, Prudence Lau,

Sally Yip

Publishing Director

Allen Lee

The Publisher reserves all rights herein. Reproduction in whole or

in part is permitted only with the written consent of AVCJ Group Limited.

ISSN 1817-1648 Copyright © 2016

A Mergermarket Group company

Hong Kong Headquarter Suite 1602-6

Grand Millennium Plaza181 Queen’s RoadCentral Hong KongT. (852) 2158 9700F. (852) 2158 9701

E. [email protected]. avcj.com

Beijing Representative OfficeNo.1-2-(2)-B-A554, 1st Building,

No.66 Nanshatan,Chaoyang District, Beijing,People’s Republic of China

T. (86) 10 5869 6203F. (86) 10 5869 6205 E. [email protected]

Unlocking liquidity for private equity investors

www.collercapital.com London, New York, Hong Kong

Anything is possible if you work with the right partner

PAUL, WEISS, RIFKIND, WHARTON & GARRISON LLPwww.paulweiss.com

E X T R A O R D I N A R Y

Opportunities.

E X T R A O R D I N A R Y

Challenges.

For more than a quarter century, our firm

has advised world-class private equity firms

in their most high-profile and significant

investments in China. With global resources

and local expertise, Paul, Weiss helps

private equity firms capitalize on opportunities

by creating long-term strategic

partnerships with Chinese enterprises that

add value beyond just capital.

Our lawyers’ extensive knowledge of the

foreign investment environment and M&A

experience in both local and global markets

helps Chinese investment managers

expand their global footprint and take

advantage of opportunities for growth.

NEW YORK

BEIJING

HONG KONG

LONDON

TOKYO

TORONTO

WASHINGTON, DC

WILMINGTON

Number 08 | Volume 29 | March 01 2016 | avcj.com 5

ASIA PACIFIC

Asian pension funds to boost alternatives exposure Pension funds in Asia Pacific expect to increase their allocations to alternative assets over the next three years in an effort to boost returns and cover liabilities. More than half of the Asia-based pension funds surveyed by State Street said they plan to increase private equity exposure.

Markus Ableitinger joins placement agent PyramidMarkus Ableitinger, formerly Asia-based managing director with Capital Dynamics, has joined Pyramid Private Equity Partners as an associate partner. He will continue to focus on Asia. At Capital Dynamics, Ableitinger handled investments into over 30 Asian GPs, overseeing commitments of more than $1.3 billion.

AUSTRALASIA

Brookfield, Qube consider joint Asciano bidA Brookfield Asset Management-led consortium and a group led by Qube Holdings that includes Canada Pension Plan Investment Board and China Investment Corporation may make a joint A$9 billion ($6.5 billion) bid for Australian rail freight and cargo port operator Asciano. It comes days after Asciano accepted an A$8.8 billion bid from Qube, rejecting an earlier Brookfield offer.

GREATER CHINA

TCL, Tsinghua Unigroup launch $1.5b M&A fundTCL Group has partnered with Tsinghua Unigroup, an investment arm of Tsinghua University, to launch an M&A fund with a target of RMB10 billion ($1.53 billion). The fund, known as Xiang Dongwei Xinghua Investment, will focus on technology and advanced manufacturing.

Wanda Media to raise $1.5b ahead of listingChinese conglomerate Dalian Wanda Group is seeking RMB10 billion ($1.5 billion) from domestic investors for its film and TV production division, Wanda Media, ahead of a planned onshore IPO. The films Wanda Media produced

generated $6.8 billion in box office revenue last year, accounting for 24.8% of the industry total.

Warburg Pincus joins Series B for D&J ChinaD&J Industrial Property, a business park builder co-founded by Warburg Pincus, has raised $220 million in a Series B round from the GP and Dongping Sun, D&J’s founder. They have invested $420 million in the company in all.

Tian Tian Express raises $92mChinese courier service Tian Tian Express has raised a RMB600 million ($92 million) Series A round led by domestic PE vehicle CICC Qianhai Development Fund. The new capital will be

used to build additional distribution centers and upgrade the company’s information system.

Salvage car auction platform raises $45mBeijing Fairlubo Vehicle Auction, a Chinese online salvage car auction platform, has raised a $45 million round led by PE-backed used car trading platform Uxin. Fairlubo collects damaged cars from insurance companies and helps sell them to dealers, rebuilders and exporters.

Cross-border shopping platform gets $15mCalifornia-based Chinese cross-border shopping platform 55Haitao has raised a $15 million Series A round from JJ Capital, a VC arm of Chinese game developer JJ. 55Haitao generates 5,000-10,000 orders every day; sales exceeded $150 million in 2015.

Impact Therapeutics gets $10m Series B roundExisting backer Lilly Asia Ventures has been joined by new investors, including China Summit Capital, in a $10 million Series B round for China-based cancer drug developer Impact Therapeutics. Impact has several anti-tumor drug projects in pre-clinical and clinical testing. The capital will be used to grow the product pipeline.

PE-backed SF Express targets A-share IPOChina’s largest express delivery services provider SF Express, which is backed by several PE investors including CITIC Capital, is targeting an A-share IPO. As of July 2015, the company had 340,000 employees, 160,000 logistics vehicles and 19 freight planes.

Unigroup scraps Western Digital investment planChina’s Tsinghua Unigroup has scrapped its plan to pay $3.78 billion for a 15% stake in US-based disk drive manufacturer Western Digital after US regulators decided to investigate the deal. Unisplendour will still set up a joint venture with Western, with registered capital of $158 million.

Shunwei leads round for legal services platformShunwei Capital Partners has led a Series B round for Kuaifawu.com, a Chinese legal services platform that targets small and medium-sized

Ex-Khosla partner raises $200m for tech fundAndrew Chung, formerly a partner at US-based Khosla Ventures, has launched his own VC firm - 1955 Capital - and reached a first close of $200 million on a cross-border technology fund.

The first close on the new fund is said to be above the initial target. The vehicle will invest in companies in the US and Europe that can address

challenges faced by developing countries relating to energy, healthcare, food, agriculture, education and sustainable manufacturing. Potential investees will have some degree of product traction and be

1-2 years away from product commercialization.Chung believes companies with these

characteristics are available at attractive valuations in the US and unlikely to be well-covered by local VC firms. He will help them negotiate local strategic partnerships, initially in China. “I have experience taking US companies into China – flying here a few times a year and driving for hours in the middle of nowhere outside Shanghai – and helping them negotiate head-to-head with the Chinese entrepreneurs. That is the biggest advantage I can bring to the table,” Chung said.

1955 Capital is named for the year when influential technology figures like Bill Gates, Steve Jobs, Eric Schmidt and Vinod Khosla were born.

NEWS

PAUL, WEISS, RIFKIND, WHARTON & GARRISON LLPwww.paulweiss.com

E X T R A O R D I N A R Y

Opportunities.

E X T R A O R D I N A R Y

Challenges.

For more than a quarter century, our firm

has advised world-class private equity firms

in their most high-profile and significant

investments in China. With global resources

and local expertise, Paul, Weiss helps

private equity firms capitalize on opportunities

by creating long-term strategic

partnerships with Chinese enterprises that

add value beyond just capital.

Our lawyers’ extensive knowledge of the

foreign investment environment and M&A

experience in both local and global markets

helps Chinese investment managers

expand their global footprint and take

advantage of opportunities for growth.

NEW YORK

BEIJING

HONG KONG

LONDON

TOKYO

TORONTO

WASHINGTON, DC

WILMINGTON

avcj.com | March 01 2016 | Volume 29 | Number 086

enterprises. The size of the round reportedly amounts to tens of millions of dollars.

NORTH ASIA

Mitsui Fudosan launches VC fund with Global Brain31 Ventures, a VC firm sponsored by Japanese developer Mitsui Fudosan, has launched a JPY5 billion ($44 million) fund with Global Brain Corporation. The 31 Ventures Global Innovation Fund I will commit early stage capital to start-ups in the US, Europe, Israel and Asia.

Eight Roads leads $8m round for Japan’s PortEight Roads Ventures Japan has led a JPY900 million ($7.9 million) round for Tokyo-based online content developer Port. Port mainly offers hiring and social media consulting services to Japanese businesses. It also operates several vertical media sites.

SOUTH ASIA

IDG targets $200m for third India fundIDG Ventures has launched its third India fund, targeting $200 million. IDG invests in technology-focused Indian companies at early and growth stage, committing $1-10 million per deal.

IFC commits $25m to VC-backed LenskartThe International Finance Corporation (IFC) has committed $25 million to Indian online eyewear retailer Lenskart. The company’s backers include TPG Capital, IDG Ventures, TR Capital, and Unilazer Ventures.

Accel leads $5.8m round for JuspayAccel Partners has led a INR400 million ($5.8 million) Series A round for Indian mobile payments start-up Juspay. Juspay will use the proceeds from the round to expand its team and build its technology platform.

Matrix leads $5m Series A for OfBusinessIndian B2B e-commerce platform OfBusiness has raised a $5 million Series A round led by Matrix

Partners India. The company will use the new capital to grow its team and improve its platform aimed at connecting small and medium-size enterprises with customers and suppliers.

IDFC buys toll road from Blackstone-backed NCCIDFC Alternatives will buy a controlling stake in a Bangalore toll road from NCC Infrastructure Holdings – backed by The Blackstone Group – and Soma Enterprise at an enterprise value of INR7.5 billion ($109 million). NCC and Soma each hold a 38% stake, which they will exit entirely.

Asia Climate Partners backs ColdEX LogisticsAsia Climate Partners, a fund set up by the Asian Development Bank, Orix Corp, and Robeco Institutional Asset Management, has invested in Indian cold chain provider ColdEX Logistics. The company will invest INR2.5 billion ($36.4 million) over three years to build warehousing capacity.

BanyanTree invests $9m in Safex ChemicalsBanyanTree Finance has invested INR600 million ($9 million) in farming, pesticide and agrochemical maker Safex Chemicals. The capital from the $175 million BTGC-II growth capital fund will support Safex’s growth efforts, marketing and long-term working capital requirements.

IvyCap leads $4.5m round for TaskbobIvyCap Ventures has led a INR280 million ($4.5 million) Series A round for Indian home services start-up Taskbob. The capital will be used to expand Taskbob’s presence in multiple markets, support product growth and innovation, and identify acquisition opportunities.

SOUTHEAST ASIA

GIC to invest $387m in Indonesian retailerSingapore’s GIC Private will invest IDR5.2 trillion ($387.4 million) in Trans Retail, a hypermarket operator run by Indonesian conglomerate CT Corp. With GIC’s support, Trans Retail will add locations and expand into new formats.

Telstra backs latest Monk’s Hill fundTelstra Ventures has made an LP commitment to Monk’s Hill Ventures’ debut Southeast Asia fund, which targets S$100 million ($80 million). Telstra will leverage Monk’s Hill’s network to grow businesses outside its traditional service areas.

VCs commit $15m to Indonesia’s OramiMoxyBilna, an Indonesia-based mother and baby-focused e-commerce group, has received a $15 million funding round led by Sinar Mas Digital Ventures and rebranded as Orami. Gobi Partners, Velos Partners and Facebook co-founder Eduardo Saverin also participated, as did Ardent Capital.

SAIF seeks $800m for China fundSAIF Partners is targeting $800 million for its fifth Greater China fund, which will make growth investments in the technology, healthcare and cleantech sectors. The fund – the first raised by SAIF since its India team spun-out in 2011 – has a hard cap of $1 billion, according to sources in the LP community. The firm’s fourth vehicle, which covered Greater China and India, closed at $1.3 billion in September 2010.

Investors in SAIF Partners IV include California Public Employees’ Retirement System (CalPERS), New York State Common Retirement Fund,

Massachusetts Pension Reserves Investment Management Board, and State of Wisconsin Investment Board. Performance data disclosed by CalPERS indicate that the fund delivered a net IRR of 9.6% and a multiple of 1.3x as of June 2015.

The firm will partner with local entrepreneurs who have built companies with exposure to fast-growing and emerging industries and cross-border investment opportunities. Companies should be established and cash-flow positive. SAIF invests between $10 million and $100 million across one or multiple rounds of funding, typically takes a stake of 15-40%, and has board representation. The firm manages more than $4 billion in capital and has invested in over 200 companies since its inception.

NEWS

Lexington Partners is a leader in the global secondary market. Since

1990, we have completed over 380 secondary transactions, acquiring

more than 2,600 interests managed by over 600 sponsors with a total

value in excess of $34 billion. For over 25 years, we have excelled at

providing customized alternative investment solutions to banks,

�nancial institutions, pension funds, sovereign wealth funds,

endowments, family of�ces, and other �duciaries seeking to

reposition their private investment portfolios. Our unparalleled global

sponsor relationships, capital resources, and reputation as a reliable

counterparty are widely recognized, and we have skilled professionals

to work with you in six locations. To make an inquiry, please call us or

send an email to [email protected].

First Order of Business: Secondaries

Innovative Directions in Alternative Investing

www.lexingtonpartners.com

New York • Boston • Menlo Park • London • Hong Kong • Santiago

avcjindonesia.com

Enquiry

Registration & Sponsorship: Anil Nathani T: +852 2158 9636 E: [email protected]

Indonesia 2016 5th Annual Private Equity & Venture Forum

14 April • Grand Hyatt, Jakarta

GLOBAL PERSPECTIVE, LOCAL OPPORTUNITY

Early confirmed speakers to attend the event include:

Scan this QR code with your

mobile phone to review the event

latest updates

Join your peers#avcjindonesia

Forum key statistics:

200+Delegates

10Countries

30+Speakers

6Interactive Sessions

5NetworkingBreaks

Gary NgManaging Director, Private EquityCLSA CAPITAL PARTNERS

Jean-Christophe MartiSenior PartnerNAVIS CAPITAL PARTNERS

Kimihiro FukuyamaDirector, Growth & CrossBorder Investment DepartmentDEVELOPMENT BANK OF JAPAN

Jeffrey ChiVice Chairman - Asia VICKERS VENTURE PARTNERS

Fazil Erwin AlfitriPresident Director PT MEDCO POWER INDONESIA

Veronika LinardiCo-Founder & CEOQERJA

And many more...

H.E. Dr. Sofyan A. DjalilMinister of National Development Planning & Chairperson of National Development Planning Agency REPUBLIC OF INDONESIA

KEYNOTE SPEAKER

Finding routes to create alpha

Co-Sponsor

For the latest programme and speaker line-up, visit avcjindonesia.com

AND SAVEUS$200 (until 4 MAR only)

SIGN UP NOW!

EARLY BIRD ENDS FRIDAY

Number 08 | Volume 29 | March 01 2016 | avcj.com 9

COVER [email protected]

CMC CAPITAL PARTNERS HAS CLOSED two funds – one renminbi-denominated and the other in US dollars – and deployed around $650 million over the past five years, leveraging its status as the first private equity firm to focus exclusively on China’s media and entertainment industry. A second US dollar fund is understood to be in the market, targeting around $1 billion.

But to capture the whole gamut of opportunities presented by a fast-evolving industry, CMC wanted a level of flexibility not offered by traditional private equity fund structures. This led to the establishment last November of CMC Holdings, a vehicle designed to remain invested in assets – typically greenfield project that require deep operational involvement – beyond a 10-year horizon.

The holding company received RMB10 billion ($1.6 billion) in seed capital from Alibaba Group, Tencent Holdings and fund-of-funds Oriza Holdings. While CMC Holdings will continue to make shorter-term investments, CMC Holdings is the vehicle of choice for the likes of smart TV manufacturer Whaley Technology and DreamCenter, a Shanghai-based entertainment complex developed by CMC in conjunction with Hong Kong’s Lan Kwai Fong Group and DreamWorks Animation.

“Today investing in media and entertainment sector, it’s no longer mainly about traditional movie and TV businesses. We have to look at the entire media value chain from content creation to distribution platforms, and there are so many new models coming out from each segment, especially driven by the disruption from internet and mobile,” Ruigang Li, the media mogul who founded CMC, told AVCJ in an interview last November.

CMC’s approach is unique within Chinese private equity but it closely resembles the investment strategies of the country’s internet giants, Baidu, Alibaba and Tencent (BAT), as well as strategic players such as Dalian Wanda Group and Huayi Brothers. These companies are trying to monetize changes in media consumption – driven by rising disposable incomes and rapid adoption of handheld devices – by creating their own industry value chains that run all the way from origination to distribution. For PE and VC investors that pick the right points in this

ecosystem, the rewards could be substantial.“The Chinese media industry is generally

maturing, so we will see more high-profile outbound and inbound deals – actually you could argue this trend is long overdue,” says Marcel Fenez, president at Hong Kong-based advisory firm Fenez Media. “But it is important to consider what these deals are about; obviously many of them are around films and sports.”

History lessons The idea of controlling a media value chain is not new. Right up until they were taken apart at the end of the 1940s by antitrust legislation, the US movie studios took this approach: they held actors under strict contracts; they employed the film makers; they were directly responsible for distribution. Regulators separated them from the movie theaters, but to this day the industry remains highly consolidated. A handful of companies generate the bulk of the revenue, distributing content through multiple channels.

Nevertheless, in recent years the internet has shaken up traditional business models. For example, Netflix started out in 1998 as a DVD mailing service but has since developed an online TV and movie streaming platform that doesn’t rely on cable networks for distribution. It had more than 74 million subscribers, most of them in the US, at the end of last year and is expanding globally. Netflix has also moved upstream, developing content itself or in partnership with different production studios.

“Amazon and Netflix do not yet control the

media business, but they are rapidly gaining in influence because they control highly valuable distribution channels and are able to spend more on production than the traditional studios,” says Rob Caine, a partner in film co-production company Pacific Bridge Pictures. “More and more of the top talent and writers are working for these internet companies. TV and movie production will eventually be dominated by the internet players.”

In contrast, China is much more fragmented than the US, and this is almost entirely the result of strict regulation. The major television broadcasters, like most of the media distribution apparatus, are all state-owned, which means they have never been fully commercialized.

Foreign investment therefore squeezed into the spaces beyond these red lines, and on occasion edging over them. In this sense, the internet has also been a change agent in China. Venture capitalists got direct exposure to the nascent online advertising industry through

investments in web portals and then supported internet-enabled business models as they evolved, moving into e-commerce, online video, social networking and online-to-offline services.

According to PwC, China’s entertainment and media market – a broad classification that ranges from book publishing to out-of-home advertising to online gaming – was worth $164.8 billion in 2015, with internet access and internet advertising accounting for 45% of the total. This share is projected to exceed 50% as the overall market reaches $242.2 billion by 2019, but

Kings of contentFrom Alibaba Group to Wanda Group, Chinese companies are looking to tighten their hold on the media value chain, moving upstream and downstream. Private equity can profit from this evolving ecosystem

China’s entertainment and media market

Soures: PwC

2010 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E

US$

mill

ion

250,000

200,000

150,000

100,000

50,000

0

avcjindonesia.com

Enquiry

Registration & Sponsorship: Anil Nathani T: +852 2158 9636 E: [email protected]

Indonesia 2016 5th Annual Private Equity & Venture Forum

14 April • Grand Hyatt, Jakarta

GLOBAL PERSPECTIVE, LOCAL OPPORTUNITY

Early confirmed speakers to attend the event include:

Scan this QR code with your

mobile phone to review the event

latest updates

Join your peers#avcjindonesia

Forum key statistics:

200+Delegates

10Countries

30+Speakers

6Interactive Sessions

5NetworkingBreaks

Gary NgManaging Director, Private EquityCLSA CAPITAL PARTNERS

Jean-Christophe MartiSenior PartnerNAVIS CAPITAL PARTNERS

Kimihiro FukuyamaDirector, Growth & CrossBorder Investment DepartmentDEVELOPMENT BANK OF JAPAN

Jeffrey ChiVice Chairman - Asia VICKERS VENTURE PARTNERS

Fazil Erwin AlfitriPresident Director PT MEDCO POWER INDONESIA

Veronika LinardiCo-Founder & CEOQERJA

And many more...

H.E. Dr. Sofyan A. DjalilMinister of National Development Planning & Chairperson of National Development Planning Agency REPUBLIC OF INDONESIA

KEYNOTE SPEAKER

Finding routes to create alpha

Co-Sponsor

For the latest programme and speaker line-up, visit avcjindonesia.com

AND SAVEUS$200 (until 4 MAR only)

SIGN UP NOW!

EARLY BIRD ENDS FRIDAY

avcj.com | March 01 2016 | Volume 29 | Number 0810

segments such as filmed entertainment and TV subscriptions and license fees are also likely to see rapid growth.

BAT attackThe BAT have in recent years sought to diversify their businesses, entering new verticals in order to create more points of contact with users and gain a better understanding of consumption patterns. Leveraging rising demand for entertainment is part of this: it enables companies to engage a younger demographic that is increasingly resistant to traditional forms of advertising and content consumption.

Alibaba has launched Tmall Box Office, a subscription service along the lines of Netflix,

and recently took full ownership of Youku-Tudou, an online video platform that has deals in place to stream Hollywood movies, at a valuation of $4.8 billion. It has also created movie studio Ali Pictures which has production and distribution agreements with a string of local TV stations and invested directly in the latest Mission: Impossible movie.

Meanwhile, search giant Baidu has China’s largest internet video streaming business in iQiyi, which has about 10 million paid subscribers who watch more than 1.28 billion hours of content every month, and Tencent can use the powerful QQ and WeChat social networking platforms as tools for content marketing and distribution.

“Previously many distribution platforms faced challenges when it came to monetization, because they relied on advertising-driven models. No one believed that the Chinese population would pay for content, but now we are starting to see the subscription model being putting in place,” says Deborah Mei, managing partner at The Raine Group, a financial advisory group that has worked on numerous media-related transactions.

More tie-ups between digital platforms and high-quality content providers at home and overseas are inevitable as monetization efforts gather pace. While it is difficult for venture capital investors to tap directly into areas like film production, they see user-generated content platforms, ranging from text format to short-term video apps, as a sweet spot. Virtual reality (VR) technology also has potential.

“Don’t forget that the quality of content is also complemented by computer graphics and animation technology,” explains Jixun Foo, managing partner at GGV Capital. “All the movies you’re seeing right now will become more appealing, thanks to a combination of acting, story-telling and technology.”

Light Chaser Animation Studios, which sees itself as “China’s answer to Pixar” is an example of this. Set up by Gary Wang and Zhou Yu – who left their roles as founder and senior executive at Tudou following the merger with Youku – it wants to combine advanced computer processing technology from the US with China’s cheaper operating costs. Yu says the risks are lower for animation than movie production because

monetization channels are more diversified – from box office revenue, to VR platforms, to merchandising. GGV led a $20 million Series B round for Light Chaser two years ago.

Lacking the domain expertise to mitigate this risk factor in traditional movie production, some private equity investors have targeted foreign players that need local partners to assist with distribution and monetization of their products in China.

The likes of Hony Capital, CMC, FountainVest Partners and Fosun International have all participated in Sino-US media investments where the value they bring is knowledge and networks in China. For example, Hony introduced STX Entertainment – a greenfield Hollywood venture it is backing alongside other investors – to Huayi, resulting in a three-year partnership that will see Huayi co-fund, co-produce and co-distribute almost all of STX’s movies through 2017.

Versions of this co-investment or slate financing model are being pursued by numerous other Chinese companies. Two weeks ago, China’s Perfect World Pictures agreed to invest $250 million in 50 films produced by Universal Pictures over the next five years. It will receive 25% of the revenues from each release. Hunan TV, China’s second-largest broadcaster, signed a $1.5 billion slate deal with US-based Lionsgate that will see it underwrite 25% of the production costs of at least 50 movies over the next three years in return for a share of the box office.

“The advantage of a slate is it de-risks the investment: they aren’t investing in a single

project but in multiple projects. And where the film slate is global in nature, there are common models on the fund flows. Chinese counterparts and investors can then easily lever production financing with debt. And then there is a brand association financing a foreign studio, as the Chinese partners are forging the strategic relationship with the whole Hollywood majors,” says Raine’s Mei.

The Wanda modelWanda, on the other hand, took a more direct route. Earlier this year, the conglomerate controlled by billionaire Wang Jianlin paid $3.5 billion for Legendary Entertainment, the studio responsible for the Batman and Jurassic World franchises. It is the first Chinese acquisition of US studio, and also facilitated an exit for several private market investors.

The rationale for the deal is rooted in Wanda’s origins as a commercial property developer. The company wants to complement its core business by entering three other sectors, culture, financial services and e-commerce. The Legendary purchase makes Wanda’s movie production business, which was previously domestic only, truly global; the same can be said of overseas acquisitions in the cinema chain space. By essentially adding a front-end services component to its existing real estate offering, the company is approaching the media value chain from a different angle to the BAT.

“Traditional investors like Wanda are building their content production capabilities, while the BAT are enhancing their online operations. It is natural for companies to focus on areas in which they are already strong, and a successful business model doesn’t need to be simply content-driven or channel-driven,” says Laurence IP, executive director at LKF Capital, a PE arm affiliated to Lan Kwai Fong Group. “The bottom line is monetizing resources in order to build a sustainable business model.”

With this in mind, Wanda’s interest in the media value chain extends beyond visual content. In the past six months, it has bought two sport-related assets from overseas PE investors: World Triathlon Corporation (WTC), the leading global operator of Ironman events, was acquired from Providence Equity Partners for $650 million; and marketing specialist Infront Sports & Media was picked up from BridgePoint Private Equity for $1.19 billion.

CMC has also been active in the segment, paying a record $1.3 billion for broadcast rights to matches in China’s domestic football league and then teaming with CITIC Capital among others to buy a 13% stake in City Football Group, owner of Manchester City Football Club and other global assets.

COVER [email protected]

No one believed that the Chinese population would pay for content, but now we are starting to see the subscription model being putting in place – Deborah Mei

COVER [email protected]

There is a policy angle to these investments. Culture and entertainment is one of the pillar industries in China’s latest five-year plan, which outlines the government’s economic priorities. Support for the domestic sports was also the subject of a State Council guideline that envisaged creating an industry worth RMB5 trillion by 2025. Wanda and CMC are not the only private sector players to unveil headline-grabbing deals in this space.

And as with television and movie production, there is an element of soft power to China’s efforts to bolster sports. Through its investments, CMC wants to improve the standard of domestic football, bringing more foreign professionals into a league that is still weak by global standards, while Wanda is said to be eying a potential Chinese bid for the football world cup.

“When it comes to football, there is a lot of national pride – success in the world cup would be far better than winning table tennis medals at the Olympic Games. China wants to become a leading global power, not only economically but also in knowledge terms. Its ‘soft power’ has historically lagged behind developed countries such as the US and it is now trying to catch up through support for films and sport,” says Mark Dreyer, a Shanghai-based sports commentator who runs Chinasportsinsider.com.

However, for strategic investors looking to redefine markets through landmark deals, and for private equity investors targeting investment opportunities in these markets, it is a consumption-driven game. China’s disposable income per capita reached RMB21,966 in 2015, with year-on-year growth consistently in the high single digits. This increasing capacity for discretionary consumption translates into stronger demand for services and a greater willingness to pay a premium for quality.

A consumer storyMedia and entertainment is a logical beneficiary of this trend. China box office revenues hit a record $6.8 billion last year, up 49% from 2014, according to the State Administration of Press, Publication, Radio, Film and Television. The country will soon overtake the US and become the leading global market by movie ticket sales. Wanda expects sport to follow a similar growth trajectory. On closing the WTC deal, Wang noted that the US has a population of 300 million and a sports industry worth $500 billion per year. In China, annual revenues currently stand at just $10 billion.

“As the economy matures, the pursuit of ‘spiritual consumption’ will become more significant. It is similar to the US 50 years ago,”

says GGV’s Foo. “This will drive more media-related deals over the next 5-10 years. China needs local content to fit into the taste of local consumers and domestic content creation will be benefit from learning overseas experiences and production techniques.”

Establishing a grip on the media value chain – and maximizing the revenue generated by consumers subscribing to content and advertisers that pay to reach those consumers in new, engaging ways – has therefore never been more important. Private equity strategies vary and certain groups will no doubt find success by targeting specific niches in the ecosystem. For CMC, though, mobile and internet technology area the primary focus, but flexibility is the key. Much like the strategic players, the firm wants to leverage consumer activity at multiple points, from sofa to cinema to amusement park.

“The traditional model won’t go away – people will still dine out and go to the cinema, instead of staying home and watching videos on their iPads. But technology is bringing new business models to every sector, everywhere, and changing consumer behavior,” says LKF Capital’s Ip. “As a result, the media industry will see enormous change. Thirty years from now, reading the news on an iPad might be considered old-fashioned. Who knows?”

The Asian Private Equity Online Directory is the most comprehensive online directory on private equity and venture capital in Asia. It is easy to navigate, enabling access to a listing of around 4,200 Asian private equity firms and over 11,000 professionals.

For a free trial, please visit asianfn.com/VCDemo.

To subscribe, call Sally Yip at +(852) 2158 9658 or email [email protected]

The most widely used online directory for private equity investors in Asia

avcj.comFor a free trial, please visit asianfn.com/VCDemo.

avcj.com | March 01 2016 | Volume 29 | Number 0812

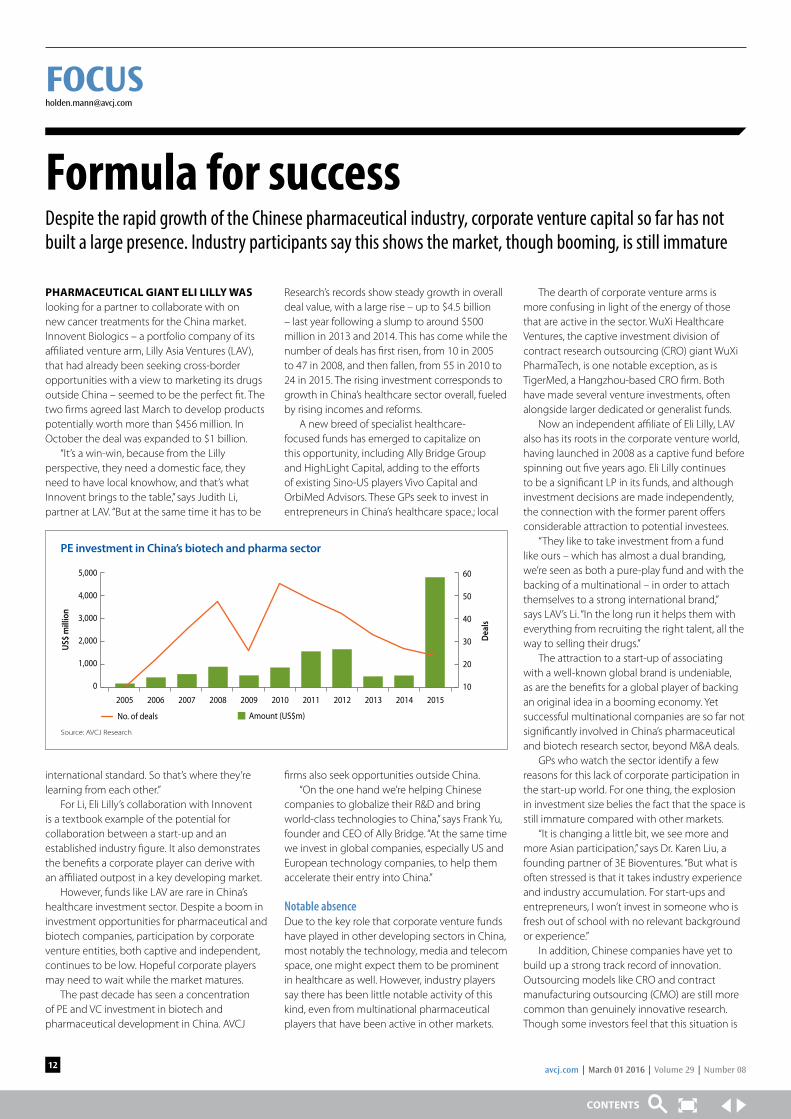

PHARMACEUTICAL GIANT ELI LILLY WAS looking for a partner to collaborate with on new cancer treatments for the China market. Innovent Biologics – a portfolio company of its affiliated venture arm, Lilly Asia Ventures (LAV), that had already been seeking cross-border opportunities with a view to marketing its drugs outside China – seemed to be the perfect fit. The two firms agreed last March to develop products potentially worth more than $456 million. In October the deal was expanded to $1 billion.

“It’s a win-win, because from the Lilly perspective, they need a domestic face, they need to have local knowhow, and that’s what Innovent brings to the table,” says Judith Li, partner at LAV. “But at the same time it has to be

international standard. So that’s where they’re learning from each other.”

For Li, Eli Lilly’s collaboration with Innovent is a textbook example of the potential for collaboration between a start-up and an established industry figure. It also demonstrates the benefits a corporate player can derive with an affiliated outpost in a key developing market.

However, funds like LAV are rare in China’s healthcare investment sector. Despite a boom in investment opportunities for pharmaceutical and biotech companies, participation by corporate venture entities, both captive and independent, continues to be low. Hopeful corporate players may need to wait while the market matures.

The past decade has seen a concentration of PE and VC investment in biotech and pharmaceutical development in China. AVCJ

Research’s records show steady growth in overall deal value, with a large rise – up to $4.5 billion – last year following a slump to around $500 million in 2013 and 2014. This has come while the number of deals has first risen, from 10 in 2005 to 47 in 2008, and then fallen, from 55 in 2010 to 24 in 2015. The rising investment corresponds to growth in China’s healthcare sector overall, fueled by rising incomes and reforms.

A new breed of specialist healthcare-focused funds has emerged to capitalize on this opportunity, including Ally Bridge Group and HighLight Capital, adding to the efforts of existing Sino-US players Vivo Capital and OrbiMed Advisors. These GPs seek to invest in entrepreneurs in China’s healthcare space.; local

firms also seek opportunities outside China.“On the one hand we’re helping Chinese

companies to globalize their R&D and bring world-class technologies to China,” says Frank Yu, founder and CEO of Ally Bridge. “At the same time we invest in global companies, especially US and European technology companies, to help them accelerate their entry into China.”

Notable absenceDue to the key role that corporate venture funds have played in other developing sectors in China, most notably the technology, media and telecom space, one might expect them to be prominent in healthcare as well. However, industry players say there has been little notable activity of this kind, even from multinational pharmaceutical players that have been active in other markets.

The dearth of corporate venture arms is more confusing in light of the energy of those that are active in the sector. WuXi Healthcare Ventures, the captive investment division of contract research outsourcing (CRO) giant WuXi PharmaTech, is one notable exception, as is TigerMed, a Hangzhou-based CRO firm. Both have made several venture investments, often alongside larger dedicated or generalist funds.

Now an independent affiliate of Eli Lilly, LAV also has its roots in the corporate venture world, having launched in 2008 as a captive fund before spinning out five years ago. Eli Lilly continues to be a significant LP in its funds, and although investment decisions are made independently, the connection with the former parent offers considerable attraction to potential investees.

“They like to take investment from a fund like ours – which has almost a dual branding, we’re seen as both a pure-play fund and with the backing of a multinational – in order to attach themselves to a strong international brand,” says LAV’s Li. “In the long run it helps them with everything from recruiting the right talent, all the way to selling their drugs.”

The attraction to a start-up of associating with a well-known global brand is undeniable, as are the benefits for a global player of backing an original idea in a booming economy. Yet successful multinational companies are so far not significantly involved in China’s pharmaceutical and biotech research sector, beyond M&A deals.

GPs who watch the sector identify a few reasons for this lack of corporate participation in the start-up world. For one thing, the explosion in investment size belies the fact that the space is still immature compared with other markets.

“It is changing a little bit, we see more and more Asian participation,” says Dr. Karen Liu, a founding partner of 3E Bioventures. “But what is often stressed is that it takes industry experience and industry accumulation. For start-ups and entrepreneurs, I won’t invest in someone who is fresh out of school with no relevant background or experience.”

In addition, Chinese companies have yet to build up a strong track record of innovation. Outsourcing models like CRO and contract manufacturing outsourcing (CMO) are still more common than genuinely innovative research. Though some investors feel that this situation is

Formula for successDespite the rapid growth of the Chinese pharmaceutical industry, corporate venture capital so far has not built a large presence. Industry participants say this shows the market, though booming, is still immature

No. of deals

PE investment in China’s biotech and pharma sector

Source: AVCJ Research

5,000

4,000

3,000

2,000

1,000

0

60

50

40

30

20

10

US$

mill

ion

Dea

ls

Amount (US$m)

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

What is often stressed is that it takes industry experience and industry accumulation. For start-ups and entrepreneurs, I won’t invest in someone who is fresh out of school with no relevant background or experience – Karen Liu

changing, currently too few companies are doing research that a larger firm would want to invest in, rather than acquiring the company outright.

The immaturity of the market also means that there has been little chance for homegrown corporate venture investing to take off. Most Chinese entrepreneurs so far lack the experience

and capital to be able to invest on their own.“In other countries, you may have people who

have been successful in building one business and taking it to IPO, and then come back to do another start-up. But in China you don’t have that cycle yet,” says Jenny Yao, the head of healthcare at KPMG. “And even the first round of people are still kind of testing the roads to see whether they can be successful.”

In light of these limitations, China-focused

GPs express little surprise that corporate VC does not make up a larger part of the ecosystem. However, the activity that does occur is viewed positively. TigerMed and WuXi are seen as offering local expertise while following an international standard; several GPs have invested alongside them.

Ally Bridge, which participated in the privatization deal for WuXi Pharmatech, later invested with WuXi Healthcare Ventures in San Diego molecular diagnostic company AltheaDX. Yu believes that Chinese corporate partners will be more attractive as China’s market grows.

“WuXi has a lot of China knowhow, and, at the same time, they play by global rules and operate on world-class standards, so they are trusted by Chinese and international partners alike,” says Yu.

“This is a phenomenon that’s becoming more prevalent, which is that global companies seek help from someone like WuXi to get into China.”

Corporate investors can also be useful for conventional GPs, which may see portfolio companies as candidates for future investment. However, industry participants point out that the the corporate parent, which might be thinking in strategic rather than financial terms, could influence a captive fund’s investment decisions.

Changing timesThough China’s healthcare sector may not be developed enough yet to attract corporate venture investors, some GPs feel this is likely to change. The first specialist healthcare funds are less than a decade old, and need time to build up a healthy market with expertise beyond outsourcing. In this light it is understandable that overseas corporate funds are still reluctant to dip their toes in the water.

“I think they’re still trying to learn about collaboration, and what is the best model for them to expand their reach into China, and then whether or not it takes too long for this particular collaboration to grow into something that’s significant,” says Nisa Leung, a managing partner at Qiming Venture Partners, which has invested both in and alongside TigerMed.

Wider reach to everyone in your organisation

avcj.com site licence allows everyone in your organisation to have instant access to in-depth analysis, real-time news and information on private equity in Asia and beyond. Sign up for an avcj.com site licence now and empower your team with critical information and data to soar above your competitors in Asian private equity.

How does it work?

We will arrange online access for your employees to avcj.com, either with individual passwords or by general access through IP address recognition.

How much does it cost

That depends on how much access you want, but we can customise cost-effective packages to all firms, regardless of size. For more information, contact Sally Yip at +(852) 2158 9658 or email [email protected]..

avcj.com

Building funds in China for 25 Years

25年来竭诚协助中国基金管理人创设基金

© 2016 Cooley LLP, IFC - Tower 2, Level 35, Unit 3510, 8 Century Avenue, Pudong New Area, Shanghai, 200120, China +86 21 6030 0600

Number 08 | Volume 29 | March 01 2016 | avcj.com 15

WHEN CITIC CAPITAL INVESTED IN Stackpole International and Henniges Automotive Holdings, it was not expecting exits to Chinese strategic players. The PE firm’s typical approach for international deals has been to identify an asset with an underexploited China angle and then team up with a US-based GP to make the acquisition. If everything went according to plan, the asset would be sold to a multinational keen to boost its China exposure.

Then last August, Canadian auto parts supplier Stackpole – acquired two years earlier in conjunction with Crestview Partners – was acquired by Hong Kong-listed Johnson Electric. The following month majority shareholder Littlejohn & Co. and CITIC sold Henniges to a joint venture between Aviation Industry Corporation of China (AVIC) and BHR Partners, a Chinese PE firm that targets cross-border transactions.

“We did these deals in 2011 and 2012 and we didn’t really start seeing Chinese strategics going overseas until 2014 and 2015, so that kind of exit was not something we underwrote on going in,” says Boon Chew, a senior managing director at CITIC Capital Partners. “But if you look at the cross-border deals we’ve done, we self-select ourselves into businesses that have the technology, knowhow and footprint to be relevant to the Chinese market. Chinese strategic investors are looking for the same things.”

Given the surge in Chinese M&A globally, the changing identity of the likely buyers for CITIC-backed businesses comes as little surprise. At the same time, these transactions say much about how private equity can tap into this trend as a partner for companies going overseas – two of the bidders for Henniges were Chinese strategics with PE co-investors – and as a seller to them.

A rising tideOutbound M&A by Chinese companies reached $99.2 billion last year, with 313 deals announced, close to twice the volume seen in 2013 on both counts, according to Mergermarket. Already this year, 49 transactions have been agreed worth a combined $69.6 billion, higher than the full-year figure for 2014 with 10 months still to go.

The industrial sector is playing an increasingly significant role in this deal flow. A total of 71 transactions were announced in 2015, up from 51 the previous year, and the capital committed

more than doubled year-on-year to $14.9 billion. In the first two months of 2016 alone, investment stands at $49.1 billion, although one of the 15 deals announced accounts for more than 90% of the total: the proposed acquisition of Switzerland’s Syngenta by China National Chemical Corporation (ChemChina), corporate China’s largest-ever outbound deal.

“Clearly the government is encouraging the transformation of Chinese manufacturing from labor intensive to more high-value-added through the acquisition of overseas advanced technology companies. And because of this support, companies have access to financing, with a lot of outbound transactions supported by Chinese banks,” says John Gu, a partner at KPMG. “A third factor is currency. The consensus view is that the renminbi may devalue over time and so it might make sense to buy a company while the currency is still strong.”

The Syngenta deal says everything about these cross-border ambitions. A global leader

in agribusiness with $15.1 billion in revenues in 2014, half of which came from emerging markets, it is the stuff of dreams to Chinese corporates: rich in technology and knowhow that can be used to offset the impact of slowing domestic economic growth by carving out a defensible and sustainable market position. However, the transaction also underlines the gulf in ability between best in class and rest of the class in outbound M&A.

Shortly before the Syngenta deal, ChemChina teamed up with Guoxin International Investment Corp. and AGIC Capital to acquire KraussMaffei Group, a Germany-based machinery manufacturer, for EUR925 million ($1.01 billion). It was at the time the largest direct Chinese investment in Europe, topping the EUR738 million Weichai Group paid for a stake in forklift truck maker Kion in 2012.

For those seeking technology, the Mittelstand – small and mid-size German, Swiss and Austrian companies – is a rich hunting ground. But ChemChina and Weichai are exceptions to the rule in corporate China: strategic investors with the talent to close cross-border deals. Others are not as far along the curve.

In Germany particularly, Chinese appetite for Mittelstand exposure is not as enthusiastically reciprocated by the companies themselves. Alberto Forchielli, managing partner at Mandarin Capital Partners, which has participated in numerous Europe-based deals with a China angle, observes that the German M&A market is expensive and highly competitive. This is largely because family owners are not willing sellers.

It is a view echoed by several industry participants, with the addendum that when assets do become available prospective Chinese buyers rarely prevail in competitive situations. Longstanding obstacles such as a reluctance to participate in auction processes – due to fears

that deals will become too expensive – and an inability to make quick decisions if they do participate have yet to be overcome. Many Chinese companies also fail to communicate effectively with their targets.

“There is a gap between what they are looking for and what the owners of the European companies are looking for,” says one transaction advisor with experience in China and Germany. “A Chinese group might be more interested in capital arrangements where they can arbitrage the difference in P/E (price-to-earnings) ratios between the target and the Chinese stock market. It is difficult to make these approaches work because there is a misalignment of interest.”

Value-add opportunitySuccessful investments in mid-market family-owned Mittelstand businesses tend to emphasize

Strategic rationaleChinese outbound investment in advanced technology assets is soaring, but the patchy nature of deal flow underlines the gulf in class between those that aspire to do deals and those that get them done

If you buy a company and half the engineers, floor managers and manufacturing leaders leave, that’s a problem – you just have blueprints and you have to figure out how it is done – Waikay Eik

Building funds in China for 25 Years

25年来竭诚协助中国基金管理人创设基金

© 2016 Cooley LLP, IFC - Tower 2, Level 35, Unit 3510, 8 Century Avenue, Pudong New Area, Shanghai, 200120, China +86 21 6030 0600

As one of China’s most premier full-service law firms, Han Kun has placed itself at the forefront of the legal profession in China by specializing in cross-border and domestic transactions, and is particularly well-known in areas such as investment funds/asset management, private equity/venture capital, mergers and acquisitions, technology, media and telecommunications (TMT), healthcare, competition law, and capital markets, among others. Han Kun has been consistently ranked as a Tier 1 PRC law firm in the areas of private equity, mergers and acquisitions, Investment Funds, TMT and Healthcare by authoritative international legal rankings, such as Chambers and Partners, Legal 500, ALB, Euromoney and the Asian-Mena Counsel. Han Kun employs more than 150 lawyers at our four offices, strategically located in each of China’s major commercial centers, Beijing, Shang-hai, Shenzhen and Hong Kong. Our lawyers come from a variety of educational and professional backgrounds. Most of our lawyers have worked with other first tier PRC and international law firms or multinational corporations.

汉坤律师事务所(“汉坤”)为中国最领先的综合性律师事务所之一,专注于跨境和境内交易,始终处于中国律师行业的

最前沿。汉坤尤其以投资基金/资产管理、私募股权/风险投资、并收购、电信、媒体和科技(TMT)、医疗、竞争法以及

资本市场领域的法律服务著称。汉坤连年被国际权威法律媒体钱伯斯、legal 500、ALB、Euromoney和Asian-Mena

Counsel等评为亚太区投资基金、私募股权/创业投资、并购、TMT及医疗等领域的顶级中国律所。汉坤目前拥有超过150

名律师,分布于中国几个主要商业中心城市,北京、上海、深圳和香港。汉坤的律师拥有不同的学历背景和工作经验,他

们中的大部分曾在国内和国际一流的律师事务所或跨国公司工作过。

上海

中国上海市静安区南京西路1266号

恒隆广场一期5709室

邮编:200040

电话:(86 21) 6080 0909

传真:(86 21) 6080 0999

Email:[email protected]

深圳

中国广东省深圳市福田区中心四路1-1号

嘉里建设广场第三座21层03室

邮编:518048

电话:(86 755) 3680 6500

传真:(86 755) 3680 6599

Email:[email protected]

香港

香港中环夏悫道10号和记大厦

20楼2001-02室

电话:00852 2820 5600

传真:00852 2820 5611

Email:[email protected]

北京

中国北京市东长安街1号

东方广场办公楼C1座906室

邮编:100738

电话:(86 10) 8525 5500

传真:(86 10) 8525 5511 / 5522

Email:[email protected]

www.hankunlaw.com

Number 08 | Volume 29 | March 01 2016 | avcj.com 17

the strategic angle – starting as minority interests, building trust and creating a longer alignment between investor and investee. While Chinese groups increasingly appreciate these nuances, it has yet to manifest in substantial deal flow.

For AGIC, which stands for Asia-Germany Industrial Promotion Capital, helping Chinese companies get transactions over the line justifies a dedicated fund. The GP is targeting $1 billion and reached a first close of $550 million last October with China International Capital Corporation (CIC) as an anchor investor.

“A lot of Chinese companies are interested in going to Germany but it’s not easy,” Henry Cai, chairman of AGIC, told AVCJ after the KraussMaffei deal closed. “First, there is a different culture and investment philosophy. Then you have to deal with German companies’ concerns about patent protection and whether the Chinese investor is going to shut all the plants in Germany. We know how to get access in Germany, this is unique knowhow and IP.”

The fund will focus on companies specializing in intelligent production and automation, medical equipment and healthcare technologies, and high-end systems and components. Check sizes, for minority and control positions, will be in the $20-100 million range, suggesting AGIC will spend most of its time with smaller groups than ChemChina on smaller deals than KraussMaffei.

BHR sees itself playing a similar role, as do numerous other middle-market private equity firms in China. However, their value-add is not necessarily limited to sourcing and execution. Post-deal integration is the area in which previous acquisitions have often gone awry. “It is tempting to think that moving up the value chain simply means acquiring technology, but so many things need to happen within a company’s manufacturing ecosystem for technology to be adopted effectively,” says CITIC’s Chew.

When switching in an automated process for one guided by the human hand, the margin for error is very small. Successful integration is contingent on having engineers and line workers who can operate the machinery, as well as upstream suppliers and downstream customers who operate at an equally high level so the costs saved or value created through automation is not lost elsewhere in the chain. A process that works in Germany might not be as effective in China because there is a different mindset.

In some industries, integration patterns are well established. Waikay Eik, partner and head of the deal value and M&A integration practice for Greater China at PwC, describes starting with careful analysis of where the Chinese company’s technology trails the European counterpart, with particular emphasis on different functions in terms of productivity and cost.

Higher value components continue to be manufactured in Europe, or manufacturing is transferred from China to Europe, where greater productivity offsets a heavier wage burden. Meanwhile, all the lower value manufacturing is relocated to China, taking advantage of economies of scale and relatively lower costs. Throughout this process, people are moving back and forth: Chinese managers will spend at least six months in Europe learning the processes, then European engineers will come to China to ensure the substance of the lessons is being applied. People are the key to these synergies.

“The value is often deeply embedded in the systems but behind that it is all about people.

If you buy a company and half the engineers, floor managers and manufacturing leaders leave, that’s a problem – you just have blueprints and you have to figure out how it is done,” says Eik. “Quality is all about that intangible element, how you select suppliers, decide how much refinement you want, and how much testing should be done. It is in culture and knowhow.”

Private equity firms can help instill the required discipline. As investors sitting in between strategic players they are positioned to identify paths through bureaucratic and political chaos. This may involve maintaining stability by convincing each party of the other’s merits.

The other sideEqually, they may see integration opportunities that cannot be realized within a private equity holding period. “It’s nice to think that new technology will bring a paradigm shift in how these companies operate, but it will probably not happen so quickly,” says CITIC’s Chew. “You are waiting for an ecosystem to catch up and there is nothing a private equity firm can do about that. All you can do is identify which sectors are at an inflection point and which are not.”

As such, prior to working with a Chinese corporate on an outbound deal, a private equity firm might carry out as much due diligence on its partner as on the potential target. For some, these arrangements remain a challenge despite progress made in recent years. CITIC has yet to do this and Chew says it would be considered on two conditions: the partner must be well known and trusted by the GP; and the asset should offer strong strategic value, with clear synergies.

Mandarin Capital has worked with Zoomlion Heavy Industry Science & Technology on a few deals but Forchielli says partnerships are rare. “It slows us down,” he explains. “Co-investment with Chinese groups is burdensome. They say, ‘We can

come in,’ but then the torture starts. You have to deal with people at the top and further down explaining everything 10 times. In 2008 it would take five meetings and five conference calls. Now it is down to four meetings and four conference calls; it is not one and one.”

Although pursuing deals independently and exiting to a Chinese strategic can be just as painful, several GPs have done so successfully with industrial businesses. Stackpole and Henniges are not isolated incidents – if an asset has achieved significant enough scale, it might fall within the scope of the country’s more sophisticated outbound investors. Germany is once again a reference point.

Weichai bought its stake in Kion from KKR and Goldman Sachs, while the ChemChina consortium bought KrassMaffei from Onex Corp, the investment group that prevailed over an unnamed Chinese player when purchasing the asset – from another PE owner – nearly four years earlier. And when, a few weeks later, the mantle of China’s largest direct investment in Germany changed hands again, as Beijing Enterprises Holding agreed to buy EEW Energy from Waste, the seller was EQT Partners.

China outbound M&A - industrial sector vs overall

Source: MergerMarket

100,000

80,000

60,000

40,000

20,000

0

350

300

250

200

150

100

0

US$

mill

ion

Dea

ls

Total - no. of dealsIndustrials - no. of deals

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 YTD

Total (US$m) Industrials (US$m)

As one of China’s most premier full-service law firms, Han Kun has placed itself at the forefront of the legal profession in China by specializing in cross-border and domestic transactions, and is particularly well-known in areas such as investment funds/asset management, private equity/venture capital, mergers and acquisitions, technology, media and telecommunications (TMT), healthcare, competition law, and capital markets, among others. Han Kun has been consistently ranked as a Tier 1 PRC law firm in the areas of private equity, mergers and acquisitions, Investment Funds, TMT and Healthcare by authoritative international legal rankings, such as Chambers and Partners, Legal 500, ALB, Euromoney and the Asian-Mena Counsel. Han Kun employs more than 150 lawyers at our four offices, strategically located in each of China’s major commercial centers, Beijing, Shang-hai, Shenzhen and Hong Kong. Our lawyers come from a variety of educational and professional backgrounds. Most of our lawyers have worked with other first tier PRC and international law firms or multinational corporations.

汉坤律师事务所(“汉坤”)为中国最领先的综合性律师事务所之一,专注于跨境和境内交易,始终处于中国律师行业的

最前沿。汉坤尤其以投资基金/资产管理、私募股权/风险投资、并收购、电信、媒体和科技(TMT)、医疗、竞争法以及

资本市场领域的法律服务著称。汉坤连年被国际权威法律媒体钱伯斯、legal 500、ALB、Euromoney和Asian-Mena

Counsel等评为亚太区投资基金、私募股权/创业投资、并购、TMT及医疗等领域的顶级中国律所。汉坤目前拥有超过150

名律师,分布于中国几个主要商业中心城市,北京、上海、深圳和香港。汉坤的律师拥有不同的学历背景和工作经验,他

们中的大部分曾在国内和国际一流的律师事务所或跨国公司工作过。

上海

中国上海市静安区南京西路1266号

恒隆广场一期5709室

邮编:200040

电话:(86 21) 6080 0909

传真:(86 21) 6080 0999

Email:[email protected]

深圳

中国广东省深圳市福田区中心四路1-1号

嘉里建设广场第三座21层03室

邮编:518048

电话:(86 755) 3680 6500

传真:(86 755) 3680 6599

Email:[email protected]

香港

香港中环夏悫道10号和记大厦

20楼2001-02室

电话:00852 2820 5600

传真:00852 2820 5611

Email:[email protected]

北京

中国北京市东长安街1号

东方广场办公楼C1座906室

邮编:100738

电话:(86 10) 8525 5500

传真:(86 10) 8525 5511 / 5522

Email:[email protected]

www.hankunlaw.com

STRONG IDEAS NEED STRONG GLOBAL PARTNERS TO UNLEASH THEIR POTENTIAL.GE Ventures provides small businesses, startups, and entrepreneurs with access to its global network of business units, partners and customers, and to its world-class training resources. All working to identify, scale and accelerate ideas that can advance industries and improve lives.

Learn more at geventures.com.

Imagination at work.

Number 08 | Volume 29 | March 01 2016 | avcj.com 19

Q: Bohai Industrial Investment Fund (Bohai Capital) has been in existence for 10 years. How did BHR come together?

JONATHAN LI: I became the CEO in Bohai Capital in 2009 and conceived the idea for BHR two years later. It took almost three years to get it set up. I wanted diversified ownership, including both Chinese and foreign partners, to make the firm more international. On the foreign side, I spent two years talking to large financial institutions before we ended up with RST, which includes Rosemont, a boutique real estate and TMT PE firm, and Thornton Advisory, a US advisory firm specializing in Sino-US relations. On the Chinese side, along with the Bohai lineage, we lined up a subsidiary of Harvest Fund as our second partner. As one of the largest mutual fund companies here, Harvest is able to reach industrial players in China. Meanwhile, Bohai itself has connections with large Chinese financial institutions.

Q: How do you feel the firm is differentiated from other PE investors looking at cross-border opportunities?

XIN WANG: As early birds in cross-border M&A, we have first-mover advantage. In addition, BHR offers the best of the Chinese private equity world and the Western private equity world. Bohai Capital has a state-owned background, with Bank of China and China Development Bank Capital, and then we have a global network. The combination of Sino-US ownership, a diversified, market-oriented team and global resources brings multiple dimensions to our decision making.

Q: There are two main investment angles – cross-border and state-owned enterprise (SOE) reform. What led to the introduction of the latter angle?

LI: BHR was originally set up solely for cross-border investment, but then the Sinopec Marketing transaction came along. I approached them as Bohai but they advised me to use BHR; in their eyes BHR represents a mixture of private enterprise and SOE – the kind of mixed-ownership structure advocated by the government’s reform initiatives. Given that BHR was not designated for SOE reform, we set up a special vehicle for that deal. We feel the strategy makes a lot of sense and so we are looking at new transactions from the same angle.

Q: So there doesn’t have to be a cross-border element to SOE investments?

WANG: Not necessarily, but we do try to cross-fertilize our different investment units. For example, as we invest in SOEs with private capital we envisage opportunities to work with companies in overseas endeavors.

LI: Henniges [an automotive equipment manufacturer acquired last year] is our typical business model. We set up a joint venture with AVIC for the acquisition. AVIC has industry experience, operates in China, and knew Henniges well. As a financial investor, we use our international network and professionalism. AVIC has done international acquisitions, but some Chinese companies don’t have that experience and may appreciate what we offer.

WANG: A lot of it is optics as well. Just by virtue of being an SOE there is the perception that there will be some cross-cultural issues. Having us and our global resources there to serve as a

conduit can facilitate the deal.

Q: To what extent is Henniges typical of the sectors BHR is targeting?

LI: Industrial technology is one area we are interested in. We want companies with good technology and a strong international sales network and management team. Working with strategic partners, we can help them tap China’s market

Q: You set up dedicated funds for the Sinopec Marketing and Henniges investments. Is this BHR’s standard approach?

WANG: As of the end of 2015 we have achieved aggregate assets under management of $1.75 billion, much of which has been invested through dedicated funds. We also operate blind pool funds but find that, for large transactions, dedicated deal funds allow flexibility in funding, execution and exit strategies. One of the key objectives for 2016 is to diversify our LP base. We are hoping to build a US and a European fund this year.

Q: Where do investments in internet-related companies like Didi Kuaidi and Tuniu come in?

WANG: We have two key themes and of the $1.75 billion we

have invested, 60% has been in cross-border and 30% in SOE reform. The remaining 10% is in a third bucket, which operates more on an opportunistic basis for growth-stage investments in the likes of Didi Kuaidi. We look to do more of these deals this year. China’s consumption mentality is changing away from product-based to experience-based consumption. Didi Kuaidi enhances an experience that facilitates everyday life.

Q: Are valuations a concern in these investments and do you get downside protection?

LI: Downside protection is not an imperative, as we focus on the fundamentals of the target. Neither is valuation the biggest concern – we focus more on the target’s potential for growth and synergies with Chinese strategic partners. However, we do ask for downside protection, and depending on the investment we may or may not get it. If there is no downside protection and we like the company then we will still invest.

JONATHAN LI & XIN WANG | INDUSTRY Q&A [email protected]

Crest of a waveBHR Partners was set up as an extension of Bohai Industrial Investment Fund to support Chinese companies going overseas. CEO Jonathan Li and Managing Partner Xin Wang explain the strategy

STRONG IDEAS NEED STRONG GLOBAL PARTNERS TO UNLEASH THEIR POTENTIAL.GE Ventures provides small businesses, startups, and entrepreneurs with access to its global network of business units, partners and customers, and to its world-class training resources. All working to identify, scale and accelerate ideas that can advance industries and improve lives.

Learn more at geventures.com.

Imagination at work.

Jonathan Li Xin Wang

avcj.com | March 01 2016 | Volume 29 | Number 0820

IT TOOK JUST 18 MONTHS OF AGGRESSIVE advertising for Ezubao to emerge as one of China’s largest peer-to-peer (P2P) lending platforms. The company, which claimed to match investors with potential borrowers, promised annual returns of up to 14%, well beyond the rates offered by traditional banks. It facilitated RMB70 billion ($11 billion) worth of transactions between July 2014 and December 2015.

But the sums didn’t add up. Ezubao was a Ponzi scheme: instead of distributing returns from revenue from real projects, it paid existing investors with money deposited by new ones.

About 95% of borrowers were fictional, Xinhua News Agency reported after the arrest of Ezubao’s founder. Over 900,000 investors lost an estimated RMB50 billion ($7.8 billion), potentially the biggest financial fraud in China’s history.

Despite its scale, Ezubao represented only a small portion of the fraud perpetrated in the booming but unruly online finance industry. The malfeasance extends to private equity, with a large number of local managers recently exposed for engaging in illegal fundraising activity online.

Deceit is hardly a new phenomenon in this field, but the extent to which managers used the internet to run small-scale scams is unprecedented. The Asset Management Association of China (AMAC) – an industry body set up by the Chinese securities regulator – responded with predictable force: registration requirements for private fund managers have been tightened up and tougher fundraising rules are set to follow.

“The regulators studied US and European regulatory models before coming out with these new rules,” says James Wang, a partner in the investment funds group at Han Kun Law Office. “They are trying to distinguish the good guys from the bad guys, and drive the bad guys out of the industry.”

Trigger point Over the course of 2014 and 2015, online lending proliferated in China. As of the end of last year, about 2,600 P2P lending platforms were in operations, up from 1,600 in 2014, according

to industry tracker Online Lending House. Total outstanding loans came to RMB439 billion in 2015, compared to RMB104 billion in 2014 and RMB26.8 billion in 2013.

Many of these platforms serve a positive purpose, connecting lenders to small and medium-sized enterprises, many of which cannot get funding from traditional banks. But several have been the cause of sizeable scandals, as in the case of Fanya Metals Exchange.

“As China’s economy slows, investors can no longer generate good returns from traditional investment channels. They become opportunistic and so they are drawn to online finance platforms that promise much higher returns. Some domestic fund managers have entered this space by packaging private equity funds as wealth management products and raising capital from public investors. They are taking advantage of regulatory loopholes,” says Raymond Wang, managing partner at law firm Anli Partners.

The scale of illegal activity and resultant public outcry alerted regulators to the problem. Last year, the State Council set up a special committee and called upon local governments to investigate illegal fundraising activities, particularly those involving online investment products. In Beijing, the authorities responded by suspending domestic PE investment registration. Any proposals that included wording such as project investment, equity investment, investment management and financial leasing were banned. Local authorities in Shenzhen, Shanghai and Tianjin followed suit.

Then in January, the China Security Regulatory Commission (CSRC) announced that at least 27 private fund managers would be fined or placed under administrative supervision due to suspected violations. They included high-profile names such as Shanghai Gopher Asset Management and China Science & Merchants Investment Management Group (CSC Group).