industry update health care services industry - …mpival.com/docs/industry...

TRANSCRIPT

New York Chicago Boston Hartford Orlando Princeton www.mpival.com

Industry Update

Health Care Services Industry 2015

Page 2 www.mpival.com | 2

Health Care Services Industry Report – 2015

Table of Contents*

Industry Overview .............................................................................................................................................................. 3

In The News… ....................................................................................................................................................................... 5

M&A Overview ..................................................................................................................................................................... 6

Public Market Data ............................................................................................................................................................. 7

Segments of the Health Care Services Industry Defined ................................................................................... 13

About MPI ............................................................................................................................................................................ 16 * This publication is also available in soft copy on the MPI website: http://www.mpival.com/resources.html.

Page 3 www.mpival.com | 3

Health Care Services Industry Report – 2015

Industry Overview This publication focuses on major events, developments, and trends within the following segments of the Health Care Services Industry1:

• Acute Care Hospitals • Assisted Living • Care Management/Cost Containment • Clinical Laboratories • Diagnostic Imaging • Health Care Information Technology • Health Care Staffing • Home Care/Hospice • Long-Term Care • Managed Care • Pharmacy Benefit Management • Surgicenters/Rehabilitation

Along with a substantial increase in the number of mergers and acquisitions and the aggregate volume of those deals, which will be discussed in detail in subsequent sections of this report, several other trends within the Health Care Services Industry were noted in 2015. One of the biggest concerns of 2015 was increasing drug prices. Not only have prices for branded drugs outpaced inflation in every year since 2006, there were a number of instances of predatory practices on the part of firms like Turing Pharmaceuticals and Valeant Pharmaceuticals that spurred investigation into their drug pricing strategies by federal regulators. Another development in 2015 is that providers are responding to patient preferences by beginning to offer services apart from the traditional methods of face-to-face visits in spaces such as doctor’s offices, clinics, and hospitals. A growing number of providers are embracing “telemedicine,” which involves using methods such as video calls in conjunction with connected devices and applications to provide consultation and diagnostic services to patients in their own homes or workplaces, for example. However, greater flexibility in services provided and settings is reliant upon networked technologies that must be adequately secured in order to protect patient privacy and confidentiality. An instance of an insulin pump being remotely accessed and hacked to alter dosages was an extreme example of the potential pitfalls of inadequate security regarding telemedicine. Additionally, as shown by the increased merger and acquisition activity in 2015, the Health Care Services Industry is consolidating and is predicted to consolidate further in the future. Many of the mega deals that were announced in 2015 will involve sell-offs of various portions of the businesses in order to satisfy federal regulators. The portions that are eventually sold off are predicted to be acquired by smaller insurers, pharmaceutical companies, and others.2

1 Brief descriptions of each segment of the Health Care Services Industry can be found on pages 13 through 15 of this report. 2 Source: Fortune.com

Page 4 www.mpival.com | 4

Health Care Services Industry Report – 2015

Industry Overview (cont.)

• As shown on the upper chart, the performance of the various segments of the Health Care Services

Industry have all improved over the last five years, with diagnostic imaging increasing 25.4% at the lower end, and health care staffing increasing 269.83% at the upper end.

• However, as shown on the lower chart, performance throughout 2015 is mixed. The S&P Health Care Services Index increased by a modest 3.5% in 2015. With an increase of 33.1% in 2015, the home care / hospice segment has exhibited the strongest performance. The worst performing segment was assisted living (down 45.8%).

-100.00%

0.00%

100.00%

200.00%

300.00%

400.00%

Acute Care Hospitals (ACH) Assisted Living (AL) Care Management/Cost Containment (CM/CC)Clinical Laboratories (CL) Diagnostic Imaging (DI) Healthcare Information Technology (HIT)Healthcare Staffing (HS) Home Care / Hospice (HCH) Long Term Care (LTC)Managed Care (MC) S&P 500 Index (SP500) Pharmacy Management (PM)Surgicenters/Rehabilitation (S/R) S&P Health Care Services Select Industry Index (SPSIHP)

Quarterly Benchmark Performance: January 1, 2011 through December 31, 2015 (Equally Weighted Basis)

ACH: +58.77%CM/CC: +47.96%AL: +37.43%CL: +28.78%LTC: +27.01%DI: +25.40%

Perf

orm

ance

(%)

HS: +269.83%

S/R: +175.50%

HCH: +100.64%

PM: +127.66%MC: +169.45%

SPSIHP: +118.71%

SP500: +60.70%HIT: +63.65%

33.1%

20.2%

7.0%

5.5%

5.4%

3.5%

1.9%

0.6%

0.3%

-0.7%

-12.5%

-16.7%

-40.2%

-45.8%

-50.00% -40.00% -30.00% -20.00% -10.00% 0.00% 10.00% 20.00% 30.00%

Home Care / Hospice

Managed Care

Pharmacy Management

Healthcare Staffing

Surgicenters/Rehabilitation

S&P Health Care Services Select Industry Index

Clinical Laboratories

Healthcare Information Technology

Long Term Care

Median % Change of Each Subsector (YTD Basis) - 12/31/2015

S&P 500

Acute Care Hospitals

Care Management/Cost Containment

Diagnostic Imaging

Assisted Living

Page 5 www.mpival.com | 5

Health Care Services Industry Report – 2015

In The News… • 2016 Global Health Care Outlook – Cost Pressures Become the Dominant Issue in Advanced

Economies: Policymakers are not likely to acquiesce to the large forecast growth in health spending. There are limits to the amount of health care consumption any public or private insurance system can realistically finance. This is especially true when the demand for health care services grows faster than the capacity of the sector itself, which causes prices to rise faster than the economy-wide rate of inflation. Rapidly escalating health care costs have become the dominant issue facing the health care sector in advanced economies. With societal aging expected to add over 1 percentage point to the health care share of GDP, the pressure to reduce costs and demonstrate value is intensifying. This means that while the twin forces of aging and income growth in the aggregate, incumbent providers and businesses may not be the beneficiaries of the increase. (The Carlyle Group, 9/30).

• Are Obamacare Plans Affordable?: Since the Affordable Care Act began expanding health insurance through various programs, 17.6 million uninsured people have signed up for coverage, according to government data. Some signed up through online marketplaces, or exchanges, that give tax subsidies to help middle- and low-income people pay for coverage; and others signed up through Medicaid, the joint federal-state program for low-income Americans. A majority of Americans, 150 million, still get insurance through their jobs. The results of a telephone survey, “Are Marketplace Plans Affordable?,” released by the Commonwealth Fund research group, finds that 76% of people who get insurance through an employer perceive their coverage as being affordable, while only 53% of Americans who get coverage through marketplaces feel that way. (US News, 9/25).

• Health Care Staffing Report: According to Staffing Industry Analysts’ recently revised U.S. Staffing Industry Forecast, U.S. temporary health care staffing revenue is projected to grow by an upwardly revised 17% in 2015, driven by double-digit growth in each health care staffing sub-segment: travel nursing, per diem nursing, locum tenens and allied health. Travel nursing is projected to be the fastest growing segment, with revenue growth of 23% in 2015. As shown in the following table, the U.S. Congressional Budget Office projects an additional six million non-elderly Americans will gain access to insurance in 2016 as a result of the Affordable Care Act, which should help make next year another strong year for health care staffing. Projected change in insured (U.S. residents younger than 65) (Staffing Industry Analysts, 9/1):

Through 2015 2016 Exchanges 11 million 10 million

Medicaid/CHIP 10 million 2 million Employment-based (1 million) (5 million)

Nongroup/other (3 million) (1 million) Total 17 million 6 million

• HealthCare.gov Users hit 8.2 Million: A late surge of insurance applications and automatic renewals pushed the number of people using HealthCare.gov to 8.2 million through December 19th. Some 71% of the site’s enrollees – around 5.8 million – had coverage renewed, and 29% - or about 2.4 million – had been first-time buyers. (WSJ, 12/22).

Page 6 www.mpival.com | 6

Health Care Services Industry Report – 2015

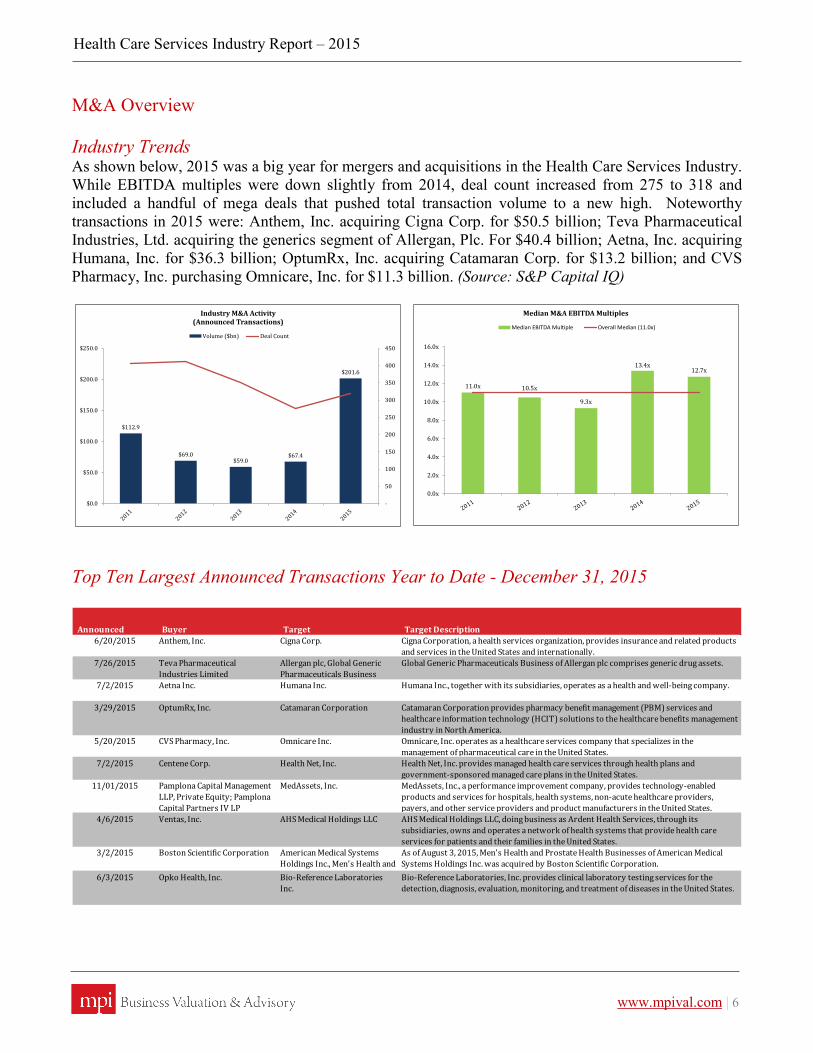

M&A Overview

Industry Trends As shown below, 2015 was a big year for mergers and acquisitions in the Health Care Services Industry. While EBITDA multiples were down slightly from 2014, deal count increased from 275 to 318 and included a handful of mega deals that pushed total transaction volume to a new high. Noteworthy transactions in 2015 were: Anthem, Inc. acquiring Cigna Corp. for $50.5 billion; Teva Pharmaceutical Industries, Ltd. acquiring the generics segment of Allergan, Plc. For $40.4 billion; Aetna, Inc. acquiring Humana, Inc. for $36.3 billion; OptumRx, Inc. acquiring Catamaran Corp. for $13.2 billion; and CVS Pharmacy, Inc. purchasing Omnicare, Inc. for $11.3 billion. (Source: S&P Capital IQ)

Top Ten Largest Announced Transactions Year to Date - December 31, 2015

$112.9

$69.0$59.0

$67.4

$201.6

-

50

100

150

200

250

300

350

400

450

$0.0

$50.0

$100.0

$150.0

$200.0

$250.0

Industry M&A Activity(Announced Transactions)

Volume ($bn) Deal Count

11.0x 10.5x

9.3x

13.4x12.7x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

Median M&A EBITDA Multiples

Median EBITDA Multiple Overall Median (11.0x)

6/20/2015 Anthem, Inc. Cigna Corp. Cigna Corporation, a health services organization, provides insurance and related products and services in the United States and internationally.

7/26/2015 Teva Pharmaceutical Industries Limited

Allergan plc, Global Generic Pharmaceuticals Business

Global Generic Pharmaceuticals Business of Allergan plc comprises generic drug assets.

7/2/2015 Aetna Inc. Humana Inc. Humana Inc., together with its subsidiaries, operates as a health and well-being company.

3/29/2015 OptumRx, Inc. Catamaran Corporation Catamaran Corporation provides pharmacy benefit management (PBM) services and healthcare information technology (HCIT) solutions to the healthcare benefits management industry in North America.

5/20/2015 CVS Pharmacy, Inc. Omnicare Inc. Omnicare, Inc. operates as a healthcare services company that specializes in the management of pharmaceutical care in the United States.

7/2/2015 Centene Corp. Health Net, Inc. Health Net, Inc. provides managed health care services through health plans and government-sponsored managed care plans in the United States.

11/01/2015 Pamplona Capital Management LLP, Private Equity; Pamplona Capital Partners IV LP

MedAssets, Inc. MedAssets, Inc., a performance improvement company, provides technology-enabled products and services for hospitals, health systems, non-acute healthcare providers, payers, and other service providers and product manufacturers in the United States.

4/6/2015 Ventas, Inc. AHS Medical Holdings LLC AHS Medical Holdings LLC, doing business as Ardent Health Services, through its subsidiaries, owns and operates a network of health systems that provide health care services for patients and their families in the United States.

3/2/2015 Boston Scientific Corporation American Medical Systems Holdings Inc., Men's Health and

As of August 3, 2015, Men's Health and Prostate Health Businesses of American Medical Systems Holdings Inc. was acquired by Boston Scientific Corporation.

6/3/2015 Opko Health, Inc. Bio-Reference Laboratories Inc.

Bio-Reference Laboratories, Inc. provides clinical laboratory testing services for the detection, diagnosis, evaluation, monitoring, and treatment of diseases in the United States.

Buyer Target Target DescriptionAnnounced

Page 7 www.mpival.com | 7

Health Care Services Industry Report – 2015

Public Market Data

12/31/2015 EnterpriseClose (2) High Low Value (EV)(3) LTM NFY LTM NFY LTM NFY

Acute Care Hospitals

Community Health Systems, Inc. 26.53 65.00 24.49 20,543 7.3x 7.0x 14.3% 14.9% 9.2x 8.5x

HCA Holdings, Inc. 5.00 13.00 4.69 37 48.3x 15.0x 2.0% NA -30.5x NA

Kindred Healthcare Inc. 11.91 24.66 11.12 4,132 8.2x 6.9x 7.7% 8.4% NM -8.4x

LifePoint Health, Inc. 73.40 88.18 58.61 5,232 8.1x 7.4x 12.7% 13.4% 21.1x 17.8x

Tenet Healthcare Corp. 30.30 60.93 26.60 19,222 8.5x 8.5x 12.6% 11.4% NM -508.8x

Universal Health Services Inc. 119.49 148.57 101.20 15,136 9.2x 9.2x 18.9% 17.0% 17.3x 17.3x

Median 8.3x 7.9x 12.6% 13.4% 13.3x 8.5x

Assisted Living

Brookdale Senior Living Inc. 18.46 39.89 16.58 9,826 12.1x 12.2x 19.1% 16.2% NM NM

Capital Senior Living Corp. 20.86 27.75 19.20 1,333 18.7x 16.1x 17.7% 20.1% NM NM

Five Star Quality Care Inc. 3.18 5.07 2.74 201 10.3x 5.7x 1.7% 2.6% -1.4x -12.4x

Median 12.1x 12.2x 17.7% 16.2% -1.4x -12.4x

Company52-Week EV/EBITDA EBITDA Margin Market Cap/Earnings

6.2x6.5x 8.0x

8.7x8.3x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Acute Care Hospitals

Average of Medians (7.6x)

11.0x

15.1x 14.1x

21.3x

12.1x

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Assisted Living

Average of Medians (14.7x)

Page 8 www.mpival.com | 8

Health Care Services Industry Report – 2015

Public Market Data (cont.)

12/31/2015 EnterpriseClose (2) High Low Value (EV)(3) LTM NFY LTM NFY LTM NFY

Care Management/Cost Containment

Accretive Health, Inc. 3.20 6.90 1.77 193 -1.3x 9.1x (152.0%) NA -3.1x -4.1x

CorVel Corporation 43.92 46.20 29.27 840 13.3x NA 12.8% NA 31.4x NA

ExamWorks Group, Inc. 26.60 44.33 21.98 1,528 13.7x 11.0x 13.7% 17.1% NM NM

HMS Holdings Corp. 12.34 21.99 8.11 1,114 13.1x 10.1x 18.5% 23.6% 79.2x 44.8x

MAXIMUS, Inc. 56.25 70.00 47.95 3,815 12.3x 11.2x 14.8% 14.0% 23.3x 21.9x

Median 13.1x 10.6x 13.7% 17.1% 27.3x 21.9x

Clinical Laboratories

Laboratory Corp. of America Holdings 123.64 131.19 105.77 18,496 11.8x 10.7x 20.2% 20.4% 28.3x 25.7x

Psychemedics Corp. 10.14 17.83 9.50 60 17.2x NA 12.6% NA 27.5x NA

Quest Diagnostics Inc. 71.14 89.00 60.07 13,907 9.3x 9.2x 19.8% 20.2% 14.3x 15.1x

Sonic Healthcare Limited 17.87 23.73 16.84 9,415 14.1x 10.8x 15.9% 17.5% 21.2x 16.1x

Median 12.9x 10.7x 17.9% 20.2% 24.4x 16.1x

Company52-Week EV/EBITDA EBITDA Margin Market Cap/Earnings

9.3x

12.1x13.3x 12.5x 13.1x

0.0x2.0x4.0x6.0x8.0x

10.0x12.0x14.0x16.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Care Management / Cost Containment

Average of Medians (12.1x)

8.3x

8.5x 8.7x 9.9x

12.9x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Clinical Laboratories

Average of Medians (9.7x)

Page 9 www.mpival.com | 9

Health Care Services Industry Report – 2015

Public Market Data (cont.)

12/31/2015 EnterpriseClose (2) High Low Value (EV)(3) LTM NFY LTM NFY LTM NFY

Diagnostic Imaging

Alliance Healthcare Services, Inc. 33.53 35.40 7.50 695 6.0x NA 25.2% NM 10.9x NA

RadNet, Inc. 2.84 3.35 1.50 692 8.8x 7.1x 14.8% 14.6% 55.1x 26.9x

Median 7.4x 7.1x 20.0% 14.6% 33.0x 26.9x

Healthcare Information Technology

Allscripts Healthcare Solutions, Inc. 18.03 19.68 12.36 3,728 35.5x 14.2x 7.1% 17.6% NM NM

athenahealth, Inc. 160.24 206.70 82.01 6,149 94.2x 35.9x 7.8% 19.4% NM NM

Cerner Corporation 56.25 63.07 45.27 18,633 18.3x 14.6x 27.6% 32.1% 48.6x 35.4x

Computer Programs & Systems Inc. 64.60 71.89 47.23 699 14.9x 15.9x 19.1% 17.9% 22.0x 19.5x

MedAssets, Inc. 24.71 26.58 16.31 2,298 12.1x 11.1x 28.5% 31.0% 55.7x 37.6x

Merge Healthcare Incorporated 2.44 4.71 1.99 448 NA NA 17.3% NA NM NM

Quality Systems Inc. 16.88 24.15 16.28 922 15.2x 10.7x 11.5% 16.2% NM 44.5x

Streamline Health Solutions, Inc. 5.03 8.50 5.00 103 -6.9x 11.5x (17.8%) 10.4% -5.0x -7.0x

Median 15.2x 14.2x 14.4% 17.9% 35.3x 35.4x

Company52-Week EV/EBITDA EBITDA Margin Market Cap/Earnings

5.5x5.4x

6.1x7.3x 7.4x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Diagnostic Imaging

Average of Medians (6.3x)

16.2x17.1x 17.3x 19.0x

15.2x

0.0x

5.0x

10.0x

15.0x

20.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Healthcare Information Technology

Average of Medians (16.9x)

Page 10 www.mpival.com | 10

Health Care Services Industry Report – 2015

Public Market Data (cont.)

12/31/2015 EnterpriseClose (2) High Low Value (EV)(3) LTM NFY LTM NFY LTM NFY

Healthcare Staffing

AMN Healthcare Services Inc. 31.05 37.47 17.92 1,684 12.5x 10.5x 10.1% 11.1% 20.7x 18.3x

Cross Country Healthcare, Inc. 16.39 18.76 9.36 582 19.0x 15.5x 4.0% 4.9% -55.0x 31.4x

On Assignment Inc. 44.95 51.00 30.60 3,129 14.6x 13.0x 10.4% 11.7% 24.0x 27.2x

Team Health Holdings, Inc. 43.89 70.21 43.15 3,926 11.6x 10.2x 9.9% 10.8% 29.4x 26.6x

Median 13.5x 11.7x 10.0% 10.9% 22.4x 26.9x

Home Care / Hospice

Addus HomeCare Corporation 23.28 38.08 18.75 245 10.2x 9.8x 7.2% 7.4% 21.0x 22.0x

Almost Family Inc. 38.23 50.48 28.10 464 12.7x 11.4x 7.2% 7.6% 17.1x 16.4x

Amedisys Inc. 39.32 48.34 24.81 1,369 15.4x 12.4x 7.2% 8.8% -194.9x -372.1x

Chemed Corp. 149.80 160.12 100.49 2,628 12.1x 11.4x 14.3% 15.0% 23.0x 22.8x

LHC Group, Inc. 45.29 51.83 27.51 860 11.1x 11.5x 10.0% 9.3% 27.0x 24.9x

Median 12.1x 11.4x 7.2% 8.8% 21.0x 22.0x

Company52-Week EV/EBITDA EBITDA Margin Market Cap/Earnings

10.5x

12.5x14.7x 14.5x 13.5x

0.0x2.0x4.0x6.0x8.0x

10.0x12.0x14.0x16.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Healthcare Staffing

Average of Medians (13.1x)

4.5x5.5x

11.1x10.5x

12.1x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Home Care / Hospice

Average of Medians (8.8x)

Page 11 www.mpival.com | 11

Health Care Services Industry Report – 2015

Public Market Data (cont.)

12/31/2015 EnterpriseClose (2) High Low Value (EV)(3) LTM NFY LTM NFY LTM NFY

Long Term Care

AdCare Health Systems, Inc. 2.49 4.50 1.90 217 9.6x NA 11.1% NM -2.5x NA

Diversicare Healthcare Services Inc. 8.15 17.15 6.45 104 4.6x NA 5.9% NM 43.0x NA

National HealthCare Corporation 61.70 69.40 58.98 952 9.0x NA 11.8% NM 17.4x NA

The Ensign Group, Inc. 22.63 27.04 19.22 1,185 11.3x 8.8x 8.4% 10.1% 21.8x 19.3x

Median 9.3x 8.8x 9.7% 10.1% 19.6x 19.3x

Managed Care

Aetna Inc. 108.12 134.40 87.25 43,807 8.4x 7.8x 8.7% 9.3% 16.4x 15.2x

Centene Corp. 65.81 83.00 50.93 7,619 8.9x 9.2x 4.3% 3.7% 22.4x 22.6x

Cigna Corp. 146.33 170.68 100.67 40,599 10.2x 9.8x 10.7% 10.9% 17.7x 17.6x

Health Net, Inc. 68.46 76.67 50.79 4,928 11.5x 8.1x 2.7% 3.7% 34.5x 22.1x

Humana Inc. 178.51 219.79 137.45 28,991 10.8x 9.9x 5.1% 5.4% 20.0x 19.8x

Magellan Health, Inc. 61.66 73.00 45.40 1,590 7.6x 6.5x 4.8% 5.4% 59.1x 75.5x

Molina Healthcare, Inc. 60.13 82.37 49.37 2,135 4.4x 4.2x 3.8% 3.6% 22.9x 22.4x

Triple-S Management Corporation 23.91 27.07 17.34 470 5.9x 7.9x 3.0% 2.1% 9.3x 12.8x

UnitedHealth Group Incorporated 117.64 126.21 95.00 137,503 11.0x 10.9x 8.5% 8.0% 18.4x 19.3x

Universal American Corp 7.00 11.16 6.38 434 23.8x 32.6x 0.9% 0.8% -37.8x -105.3x

WellCare Health Plans, Inc. 78.21 98.79 71.40 3,239 7.2x 6.2x 3.2% 3.8% 30.4x 23.8x

Anthem, Inc. 139.44 173.59 122.86 52,634 8.3x 10.1x 8.1% 6.7% 12.6x 13.7x

Median 8.7x 8.7x 4.6% 4.6% 19.2x 19.6x

Company52-Week EV/EBITDA EBITDA Margin Market Cap/Earnings

6.2x

8.0x

11.7x

9.2x 9.3x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Long Term Care

Average of Medians (8.9x)

5.4x 5.8x

7.5x

9.0x 8.7x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Managed Care

Average of Medians (7.3x)

Page 12 www.mpival.com | 12

Health Care Services Industry Report – 2015

Public Market Data (cont.)

12/31/2015 EnterpriseClose (2) High Low Value (EV)(3) LTM NFY LTM NFY LTM NFY

Pharmacy Management

BioScrip, Inc. 1.75 7.01 1.30 601 -19.9x 31.4x (2.9%) 1.9% -0.3x -0.4x

Express Scripts Holding Company 87.41 94.61 68.06 74,370 10.7x 10.5x 6.8% 6.9% 25.9x 23.5x

PharMerica Corporation 35.00 36.96 20.25 1,363 10.2x 9.9x 6.6% 6.8% 58.9x 42.3x

Median 10.2x 10.5x 6.6% 6.8% 25.9x 23.5x

Surgicenters/Rehabilitation

AmSurg Corp. 76.00 87.42 52.42 7,008 10.8x 14.3x 26.5% 19.3% 33.1x 28.3x

Hanger, Inc. 16.45 26.79 13.27 1,100 6.9x 6.7x 15.0% 15.2% 9.6x 9.8x

HEALTHSOUTH Corp. 34.81 48.37 32.55 5,480 8.4x 8.0x 22.8% 21.8% 17.9x 16.1x

Select Medical Holdings Corporation 11.91 17.20 10.07 4,220 11.6x 10.5x 10.6% 10.8% 12.3x 12.9x

US Physical Therapy Inc. 53.68 56.37 38.17 732 13.6x 14.7x 16.8% 15.1% 31.4x 30.1x

Nobilis Health Corp. 61.70 69.40 58.98 952 11.4x NA 11.8% NM 17.4x NA

Median 11.1x 8.3x 15.2% 14.1% 14.4x 15.8x

Company52-Week EV/EBITDA EBITDA Margin Market Cap/Earnings

9.7x11.4x 11.0x 11.4x

10.2x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Pharmacy Management

Average of Medians (10.7x)

7.2x 7.0x

8.8x9.5x

11.1x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

2011 2012 2013 2014 2015

Median EBITDA Multiples -Surgicenters/Rehabilitation

Average of Medians (8.7x)

Page 13 www.mpival.com | 13

Health Care Services Industry Report – 2015

Segments of the Health Care Services Industry Defined

• Acute Care Hospitals: This industry segment includes hospitals and other health care providers that

focus on short-term treatment for severe injuries or illnesses. Health care reform, reimbursement trends, electronic records, and nursing shortages are the top concerns faced by operators in the Acute Care Hospital industry. Health care reform will likely increase the number of insured patients, which will boost revenue. Other factors, such as aging population, will contribute to revenue growth over the next five years. Profitability will remain pressured as labor costs rise; however, the industry’s profit margin will get a boost from the increasing number of people who have health insurance.

• Assisted Living: The Assisted Living industry segment is made up of a variety of senior care services, including assisted living facilities, continuing care retirement communities, nursing homes, and elderly and disabled services. The number of elderly Americans is anticipated to continue to expand in the coming years, which will stimulate demand within the industry. However, Medicare and Medicaid reimbursement cuts are expected to severely limit the growth of the industry. Furthermore, a recovery from the housing market downturn over the past five years will boost revenues as more of the aging American population is able to afford the transition into assisted living accommodations.

• Care Management/Cost Containment: Companies in this industry segment reduce the overall cost of medical treatment by establishing controls across many providers of health care services for the use of expensive procedures, in-patient admission criteria, the lengths of stay, and other factors affecting the cost of care. Importantly, a company in this industry may represent a number of physician practices, laboratories and/or other service providers. This gives them much more leverage than a single physician practice would have in negotiating reimbursement prices with insurance companies or government medical programs. The cost of providing health care services has risen as a result of new technologies, malpractice insurance rates, and labor costs. However, insurance companies and the government continue to lower their reimbursement rates. The demand for companies in this industry is expected to increase as health care service providers utilize industry companies to operate more efficiently and to avoid severe margin pressure from reduced reimbursement fees from large insurance entities.

• Clinical Laboratories: This industry segment consists of companies that conduct analytic services to provide health care practitioners with information concerning the onset, severity and cause of patients’ physical ailments. While the industry has long been an essential component of health care, the aging population and ongoing progress toward preventive care has further boosted revenue over the past five years. During the next five years, the Clinical Laboratories industry is expected to benefit from health care reform and the aging U.S. population. As many laboratories consolidate, operators will increasingly compete on the basis of price with hospitals that provide industry services in-house. In particular, large laboratories are acquiring smaller labs that provide either routine or specialized services, such as biomarkers. Also, as more patients seek an individually tailored health care plan, demand for high-margin molecular testing, such as with regard to genetics, will cause industry profit to increase.

Page 14 www.mpival.com | 14

Health Care Services Industry Report – 2015

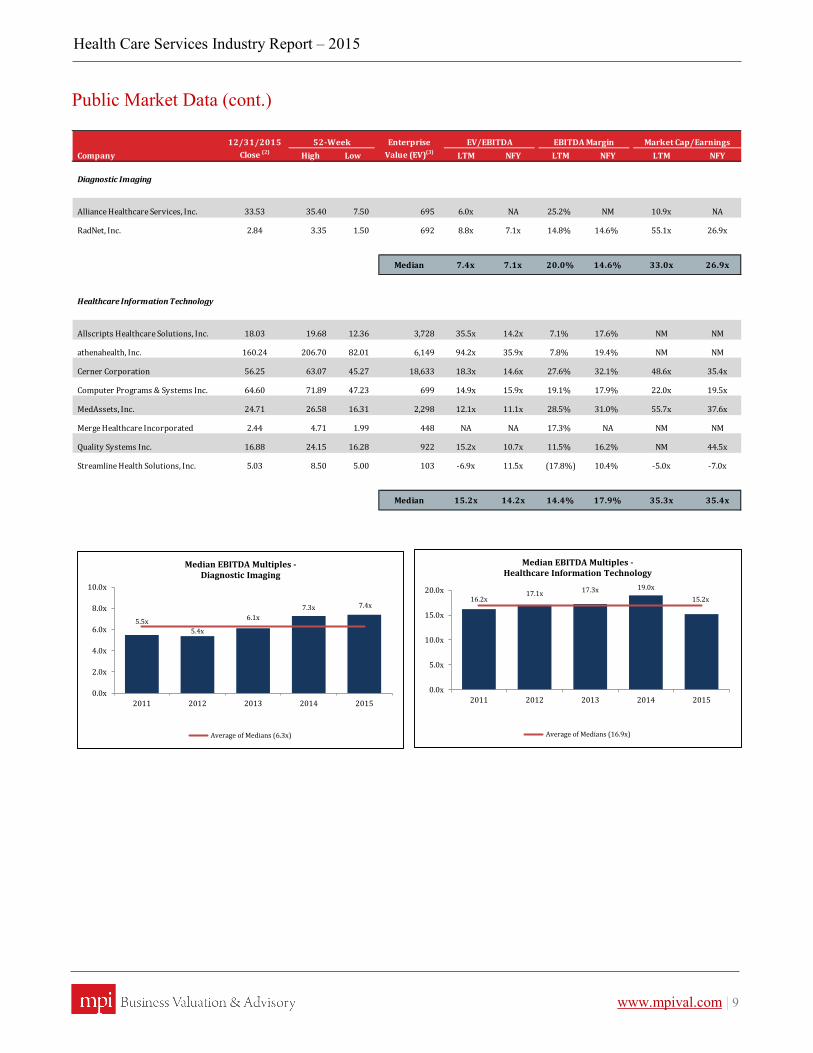

Segments of the Health Care Services Industry (cont.) • Diagnostic Imaging: Diagnostic imaging involves the use of non-invasive procedures to generate

representations of internal anatomy and function that can be recorded on film or digitized for display on a video monitor. Diagnostic imaging procedures facilitate the early diagnosis and treatment of diseases and disorders and may reduce unnecessary invasive procedures, often minimizing the cost and amount of care for patients. It is estimated that the national imaging market in the U.S. is $100 billion annually, with projected mid-single digit growth for MRI, CT and PET/CT over the next several years. This growth will be driven by the aging of the U.S. population, wider physician and payor acceptance for imaging technologies, and greater consumer and physician awareness of diagnostic screening capabilities.

• Health Care Information Technology: This industry provides technology solutions to optimize processes and help eliminate errors, variance, and waste for health care organizations. Companies in this industry provide computer software-based solutions that help hospitals and physician groups improve efficiencies and business processes across the enterprise to enhance and protect revenues. This industry is poised for further growth going forward. Ongoing contributors to growth in this industry include: incentives in the American Recovery and Reinvestment Act; a shift away from fee-for-service or volume-based reimbursement towards value-based or outcomes-based reimbursement; and a shift in the U.S. marketplace towards a preference for a single platform across inpatient and ambulatory settings.

• Health Care Staffing: The health care staffing industry is faced with the challenge of orchestrating care in an increasingly complex and converging health care labor market. Acceleration of industry growth is forecasted for 2014 as health care staffing continues to benefit from the secular growth in total health care jobs due to an aging population and the buildup of staff at health care companies in preparation for as many as 20 million newly insured individuals due to health care reform.

• Home Care/Hospice: The Home Care/Hospice industry is becoming one of the fastest-growing health care industries in the U.S.. The industry saves patients billions of dollars every year by treating them in their homes instead of in hospitals. An aging population, the prevalence of chronic disease, growing physician acceptance of home care, medical advancements, and a movement toward cost-efficient treatment options from public and private payers continue to foster industry growth. costs.

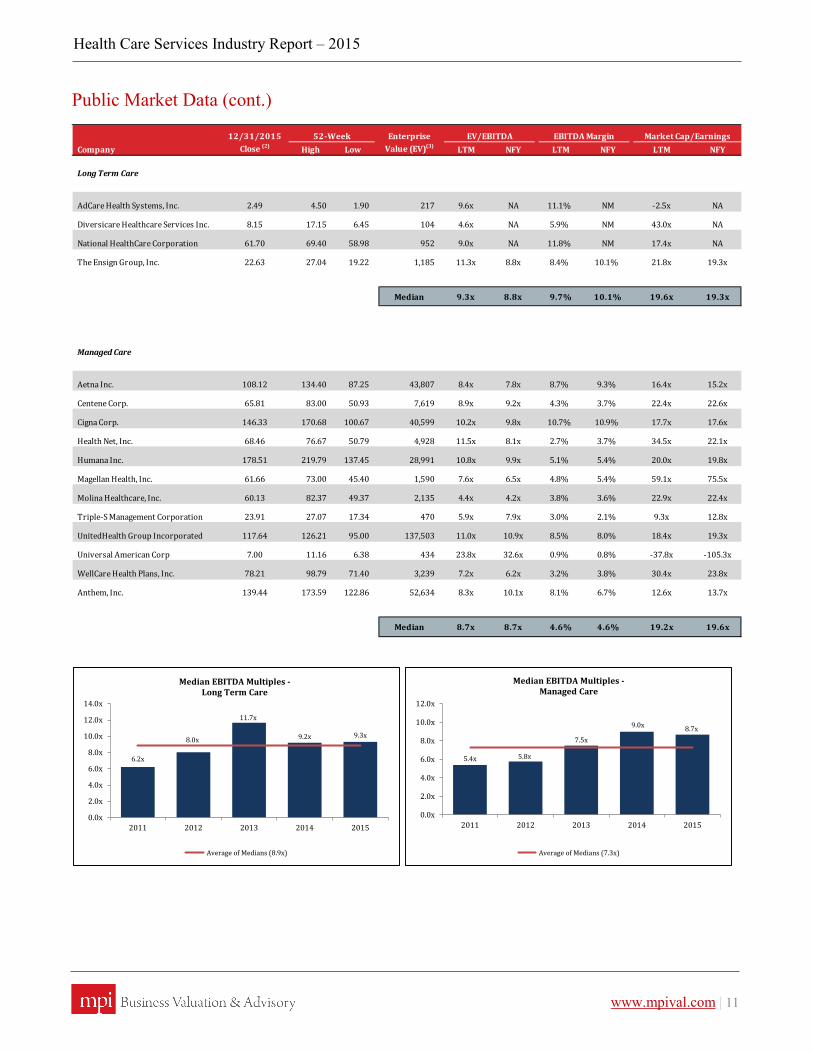

• Long-Term Care: The Long-Term Care industry provides long-term skilled nursing care and social services in residential facilities. The profitability of the long-term care facilities depends on efficient operations, as revenue per patient is largely controlled by Medicare and Medicaid. The industry is forecast to grow in the five years to 2018, largely due to an improving economic environment, an aging population, favorable health care reform legislation, and new service offerings.

Page 15 www.mpival.com | 15

Health Care Services Industry Report – 2015

Segments of the Health Care Services Industry (cont.)

• Managed Care: The term managed care is used in the U.S. to describe a variety of techniques intended to reduce the cost of providing health benefits and improve the quality of care. The Managed Care industry has been characterized by slow growth over the five years to 2013, as a result of reduced employer coverage and per capita disposable income. However, consistent increases in health care expenditure, or medical cost inflation, have continued to drive industry growth. Despite this growth, cost increases and new legislation mandating minimum medical loss ratios have pressured profit for operators. Industry revenue will remain highly correlated with total health expenditure, which is expected to continue its trend upward from 2013 to 2018. Yet, the industry’s average profit margin is forecast to decline due to increased compliance costs caused by the health care reform.

• Pharmacy Management: This industry includes firms that provide pharmacy benefit management services. Industry firms are third-party administrators of government and employer-sponsored prescription drug programs. They are primarily responsible for processing and paying prescription drug claims. Though it felt the recession's effects, the Pharmacy Benefit Management industry has recovered quickly and is poised to grow on the back of rising insurance coverage and increased physician visits, which will yield a higher number of prescriptions filled. As the median age of the U.S. population continues to rise, more Americans will rely on medications, increasing demand for the industry's services from insurers and employer-sponsored coverage plans.

• Surgicenters/Rehabilitation: The Surgicenters and Rehabilitation industry focuses on orthopedics. Surgicenters are establishments that provide surgical and emergency care services on an outpatient basis. This includes the provision of services such as orthoscopic, cataract surgery and setting broken bones. Rehabilitation centers provide follow-up physical therapy and other treatment and activities to help patients regain or improve mental or physical functionality following an injury or illness. Looking ahead, industry growth is expected to accelerate because of legislation and improving economic conditions. The introduction of the Patient Protection and Affordable Care Act will extent health care to a number of Americans, which will hasten increasing demand for the industry.

Page 16 www.mpival.com | 16

Health Care Services Industry Report – 2015

About MPI MPI is a business valuation and advisory firm that was founded in 1939. MPI provides tax-based valuations, business appraisals, financial reporting valuations, fairness opinions, sell-side and corporate advisory services, and litigation support. MPI's senior professionals have extensive experience presenting and defending work product in front of financial statement auditors, management teams, corporate boards and fiduciaries, the IRS, other government agencies, and in various courts. For additional information pertaining to MPI and our valuation and advisory services, visit http://www.mpival.com.

For More Information, Contact:

Bjørn A. Midtlyng, CFA Partner (609) 955-5745 [email protected] Daniel M. Kerrigan, CFA President (609) 955-5732 [email protected] DISCLAIMERS: The information provided in this publication is only general in nature. It has been prepared without taking into account any specific objectives, financial circumstances or needs. Accordingly, MPI disclaims any and all guarantees, undertakings and warranties, expressed or implied, and shall not be liable for any loss or damage whatsoever (including human or computer error, negligent or otherwise, or actual, incidental, consequential or any other loss or damage) arising out of or in connection with any use or reliance upon the information or advice contained within this publication. The viewer must accept sole responsibility associated with the use of the material in this publication, irrespective of the purpose for which such use or results are applied. This material should not be viewed as advice or recommendations. This information is not intended to, and should not, form a primary basis for any investment, valuation or other decisions. MPI is not acting as a fiduciary, an expert or advisor in any capacity whatsoever in providing the information set forth herein. The information set forth herein may not be relied upon and is not a substitute for competent legal and financial advice. The viewer of this material is cautioned and advised to consult with his or her own legal and financial counsel in evaluating the information provided herein. The information provided in this publication is based on public information. MPI makes every effort to use reliable and comprehensive information, but makes no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the information provided herein and MPI shall not have liability for any damages of any kind relating to any reliance on such data. Further, the information set forth herein is continuously subject to change and may fluctuate. MPI has no obligation to update the information set forth herein or to advise the viewer when opinions or information may change. Investment banking and transaction advisory services are provided by MPI Securities, Inc., member FINRA/SIPC. Persons affiliated with MPI Securities, Inc. are registered representatives of and securities are offered through MPI Securities, Inc. This publication is not a solicitation or offer to buy or sell securities. The information contained in this publication was prepared for information purposes only and was not intended or written to be used as investment or tax advice or as a recommendation to buy or sell securities.