inequality in the twenty-first century economic theory ... · 1 inequality in the twenty-first...

TRANSCRIPT

1

Inequality in the Twenty-First Century – Economic Theory Revisited

Hanna Szymborska

University of Leeds1

Abstract

This paper argues that analyses of inequality based on existing theories of

distribution do not adequately account for growing wealth disparities. This is

because the division into capitalists and workers traditionally envisaged in the

Post Keynesian wage share models has been altered by financialisation, making

these categories more heterogeneous. Financial deregulation and securitisation

have contributed to the falling wage share of national income. The rich

accumulate high-yielding assets while the middle/low-income groups suffer

from high leverage due to unsustainable debt accumulation. Rising indebtedness,

linked to stagnating wage growth and validated by the growing demand for

asset-backed securities among financial investors, has led to massive wealth

disparities. Recent contributions to the stock flow consistent modelling literature

incorporate some wealth considerations into the Post Keynesian stock flow

consistent models by distinguishing between rentiers, non-managerial and

managerial workers as well as by allowing for indebtedness of non-supervisory

workers and consumption emulation. This paper aims to complement these

contributions by focusing on how financialisation has altered the structures of

households’ balance sheets, and affected their stability. In particular, the

implications of these changes for income distribution are examined in a stock

flow consistent model of a US economy with three classes of households and a

complex financial sector. The simulation results reveal that balance sheet

heterogeneity among households has an important impact on inequality levels.

WORK IN PROGRESS – DO NOT QUOTE

Note

The author wishes to thank Yannis Dafermos, Gary Dymski, Antoine Godin, Maria

Nikolaidi, Ozlem Onaran and Cem Oyvat for comments on an earlier draft of the paper.

1 Contact e-mail: [email protected]

1

Table of Contents

I. Introduction ......................................................................................................................... 2

II. Theories of inequality and the conceptualisation of the middle class ....... 10

III. Wealth and inequality in stock-flow consistent models .................................. 16

IV. Model specification ........................................................................................................ 17

The household sector .............................................................................................................................. 20 Firms .............................................................................................................................................................. 29 Commercial banks .................................................................................................................................... 30 SPVs/underwriters .................................................................................................................................. 32 Institutional investors ............................................................................................................................ 32 Simulations ................................................................................................................................................. 33

V. Results ................................................................................................................................. 35

VI. Conclusion and future work ....................................................................................... 42

References ....................................................................................................................................... 46

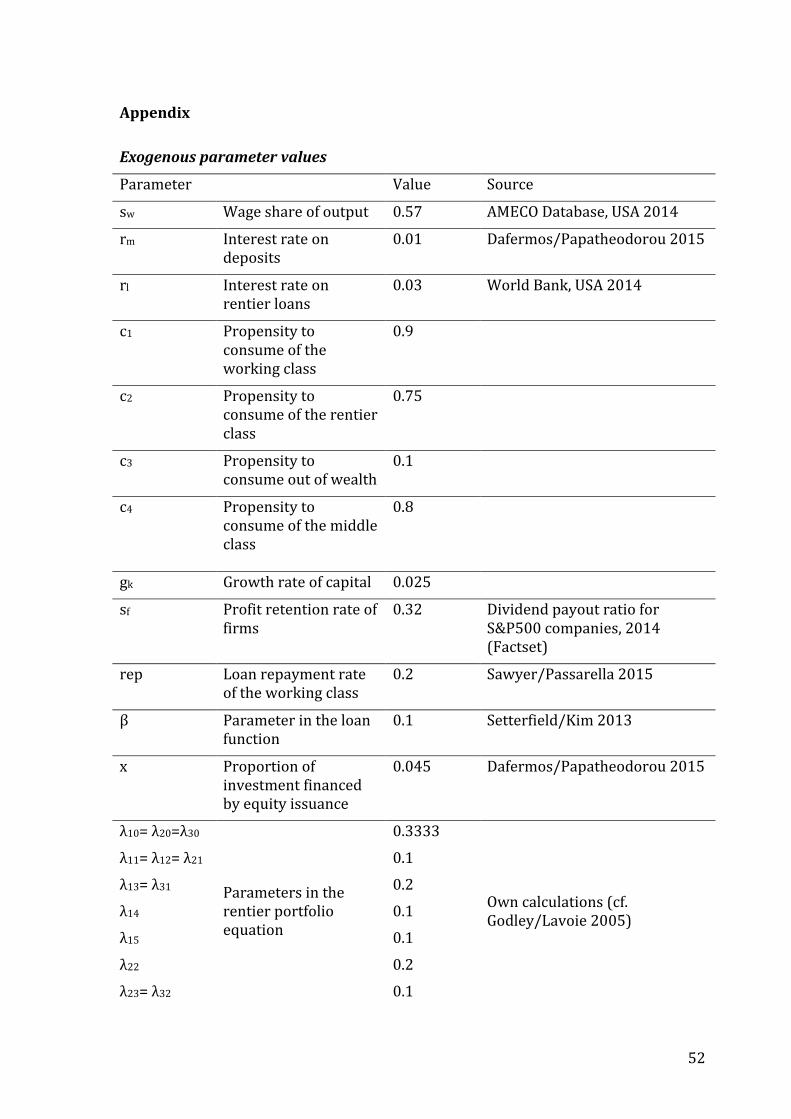

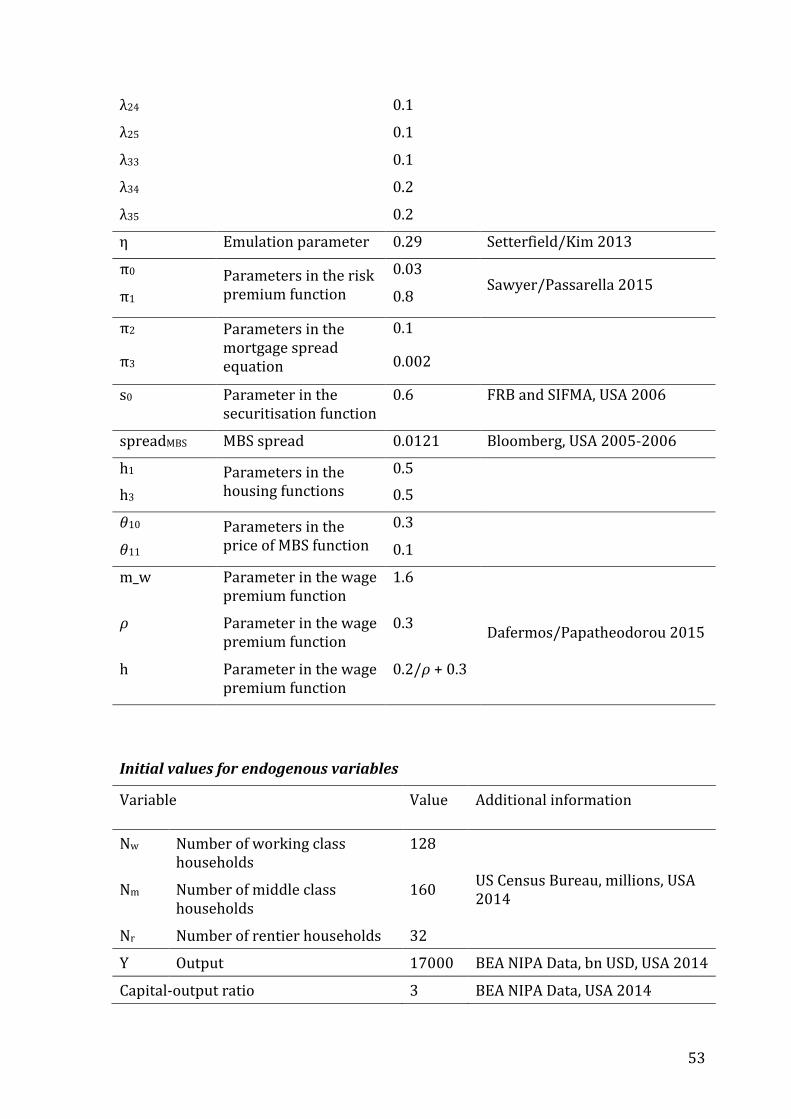

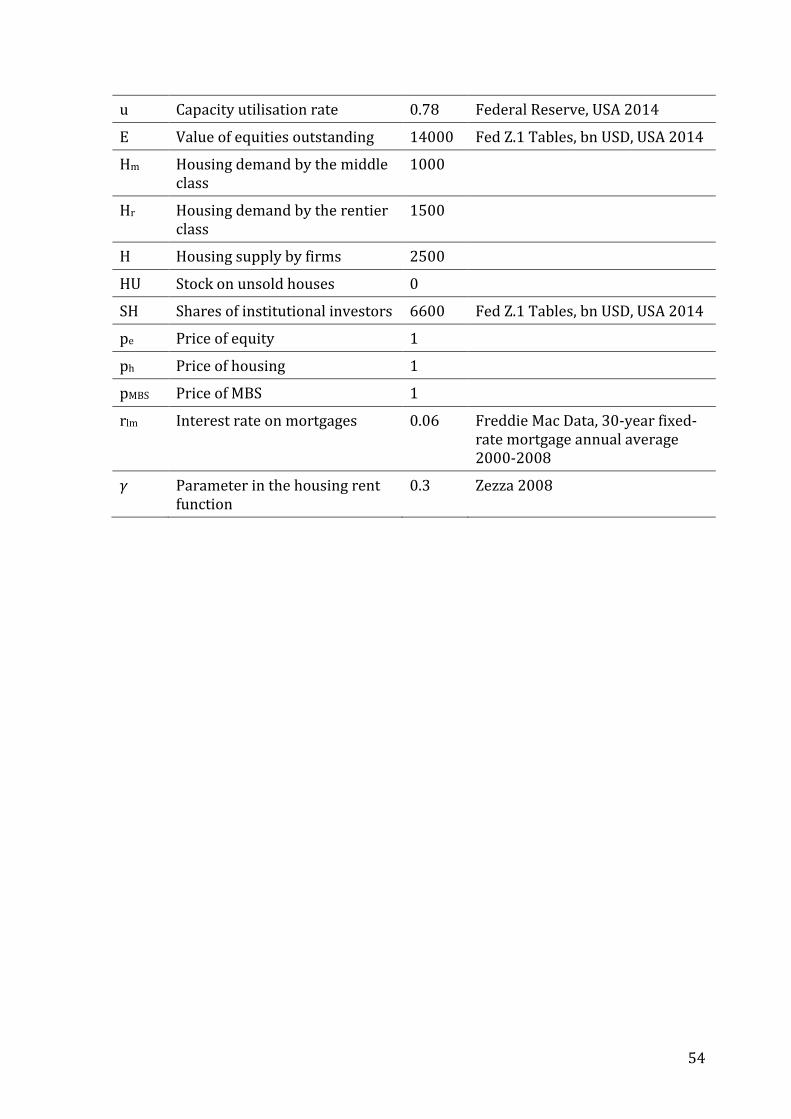

Appendix .......................................................................................................................................... 52

List of Figures

Figure 1. Change in homeownership rate by percentile, USA 1989-2012................. 4

Figure 2. The top 1% income share, USA 1980-2013 ........................................................ 5

Figure 3. Mean and median net worth, the mean-median ratio, USA 1983-2013 .. 6

Figure 4. Financial fragility measures by percentile, USA 2010 .................................... 7

Figure 5. Median net worth annual growth rate by decile, USA 1989-2013 ............ 8

Figure 6. Household portfolio composition, USA 2014 ..................................................... 9

Figure 7. Simulation results – full model ............................................................................. 35

Figure 8. Simulation results – “pure capitalists” specification .................................... 39

Figure 9. Simulation results – “pure capitalist” specification, no rentier debt ..... 40

Figure 10. Simulation results – reduced specification without securitisation ..... 41

List of Tables

Table 1. Annual growth rate of average hourly wages, USA 1979-2012 ................. 12

Table 2. Balance sheet matrix .................................................................................................. 18

Table 3. Transaction flow matrix ............................................................................................ 19

2

I. Introduction

The main goal of this paper is to examine the dynamics of income and wealth

inequality in high-income countries and the implications for the stability of

household financial positions across the distribution in the light of financial

sector transformation since 1980s. A theoretical stock flow consistent model is

proposed, aiming to explain the concentration of income and wealth at the top of

the distribution and the diffusion of financial fragility to the rest of the society.

The innovation of the model lies in its interpretation of inequality as balance

sheet structure disparities, based on a reinterpretation of the working and

rentier class and a new conceptualisation of the middle class in Post Keynesian

analysis. Three-class specification of the household sector is developed,

accounting for indebtedness, financial fragility and wage inequality – processes

strongly associated with the impact of financial sector transformation on

inequality.

Financial sector transformation, often described by the umbrella term

“financialisation”, is an extremely complex process occurring at a variety of

dimensions. Although most pronounced in USA, it has also taken place in various

aspects and at different points since 1980s in Europe (cf. Pasarella Veronese

2013).

Financialisation finds its roots in the persistently high inflation and high

interest rates in the late 1960s, which induced non-financial companies to turn

to financial markets rather than banks for investment financing. This realigned

firms’ objectives away from long-term investment towards short-term

profitability, making them more involved in financial activities (such as issuing

shares), which raised the importance of financial over real profits and

contributed to the growing share of the financial, insurance and real estate

sector (FIRE) in the economy at the expense of manufacturing (Palley 2007:18).

The processes of financialisation gained steam in the 1980s under policies

promoting market liberalisation and retrenchment of the state from public

service provision associated with the leadership of Reagan in USA and Thatcher

in UK (Sawyer 2013:13). Firstly, labour market liberalisation and the associated

3

rolling back of minimum wage, unemployment protection and union-oriented

policies resulted in gradually declining wage income growth. Simultaneously,

provision of pensions, housing and public goods such as education and

healthcare was increasingly delegated from the state to the private sector. With

stagnant wages and diminishing state provision, households found themselves in

need of additional financing through borrowing.

Rising credit demand was paralleled by the massive proliferation of

financial instruments and the development of structured finance. The

aforementioned turn of non-financial companies towards financial markets

resulting from high borrowing costs in 1960s and 70s led financial

intermediaries to seek revenue in the household sector and through innovation

of new financial products (Dymski 2009:157). An increasing volume of financial

obligations — primarily consumer debt and mortgages — was transformed into

securities in a process labelled securitisation, forming collateralised debt

obligations (CDOs), which combined financial instruments of varying risk and

return characteristics (Pollin/Heintz 2013:113). The establishment of credit

default swaps (CDS) and derivatives on existing products allowed investors to

bet against the default of any financial instrument, leading to the transformation

of traditional lending relations based on intermediation towards an “originate

and redistribute" model, where default risk became “originated" by creditors and

then spread across the financial system through securitisation. The actors of this

new lending model were not only registered banks, transformed into highly

consolidated “megabanks” as a result of intense merger activity, but also non-

bank intermediaries, which played a role similar to that of formal banks but were

outside central bank’s jurisdiction in obtaining liquidity (ibid.:115). This whole

process was validated by increasing financial deregulation measures such as the

Gramm-Leach-Bliley Act in 1999 in USA, which allowed commercial banks to

engage in financial investment activities.

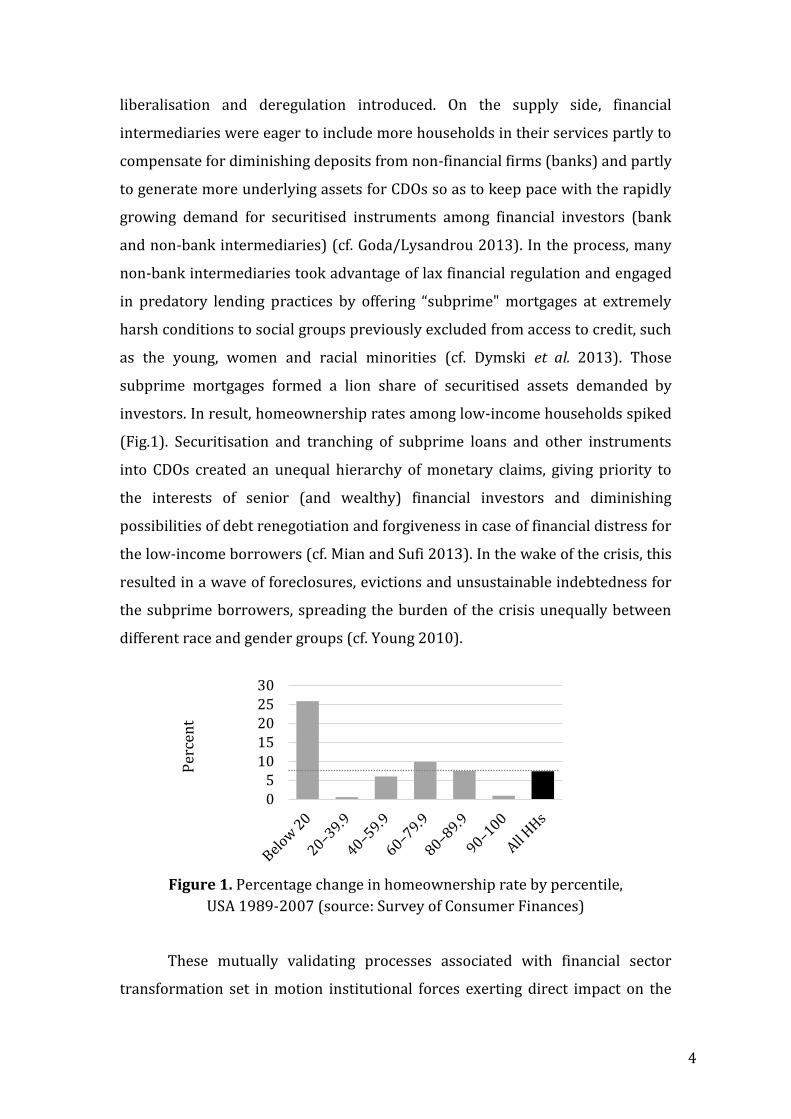

The combination of demand factors (stagnant earnings, privatisation of

public services) and supply factors (securitisation, deregulation) led households

in high-income economies to become more involved in financial markets,

although to a varying extent in different countries depending on the degree of

4

liberalisation and deregulation introduced. On the supply side, financial

intermediaries were eager to include more households in their services partly to

compensate for diminishing deposits from non-financial firms (banks) and partly

to generate more underlying assets for CDOs so as to keep pace with the rapidly

growing demand for securitised instruments among financial investors (bank

and non-bank intermediaries) (cf. Goda/Lysandrou 2013). In the process, many

non-bank intermediaries took advantage of lax financial regulation and engaged

in predatory lending practices by offering “subprime" mortgages at extremely

harsh conditions to social groups previously excluded from access to credit, such

as the young, women and racial minorities (cf. Dymski et al. 2013). Those

subprime mortgages formed a lion share of securitised assets demanded by

investors. In result, homeownership rates among low-income households spiked

(Fig.1). Securitisation and tranching of subprime loans and other instruments

into CDOs created an unequal hierarchy of monetary claims, giving priority to

the interests of senior (and wealthy) financial investors and diminishing

possibilities of debt renegotiation and forgiveness in case of financial distress for

the low-income borrowers (cf. Mian and Sufi 2013). In the wake of the crisis, this

resulted in a wave of foreclosures, evictions and unsustainable indebtedness for

the subprime borrowers, spreading the burden of the crisis unequally between

different race and gender groups (cf. Young 2010).

Figure 1. Percentage change in homeownership rate by percentile,

USA 1989-2007 (source: Survey of Consumer Finances)

These mutually validating processes associated with financial sector

transformation set in motion institutional forces exerting direct impact on the

05

1015202530

Per

cen

t

5

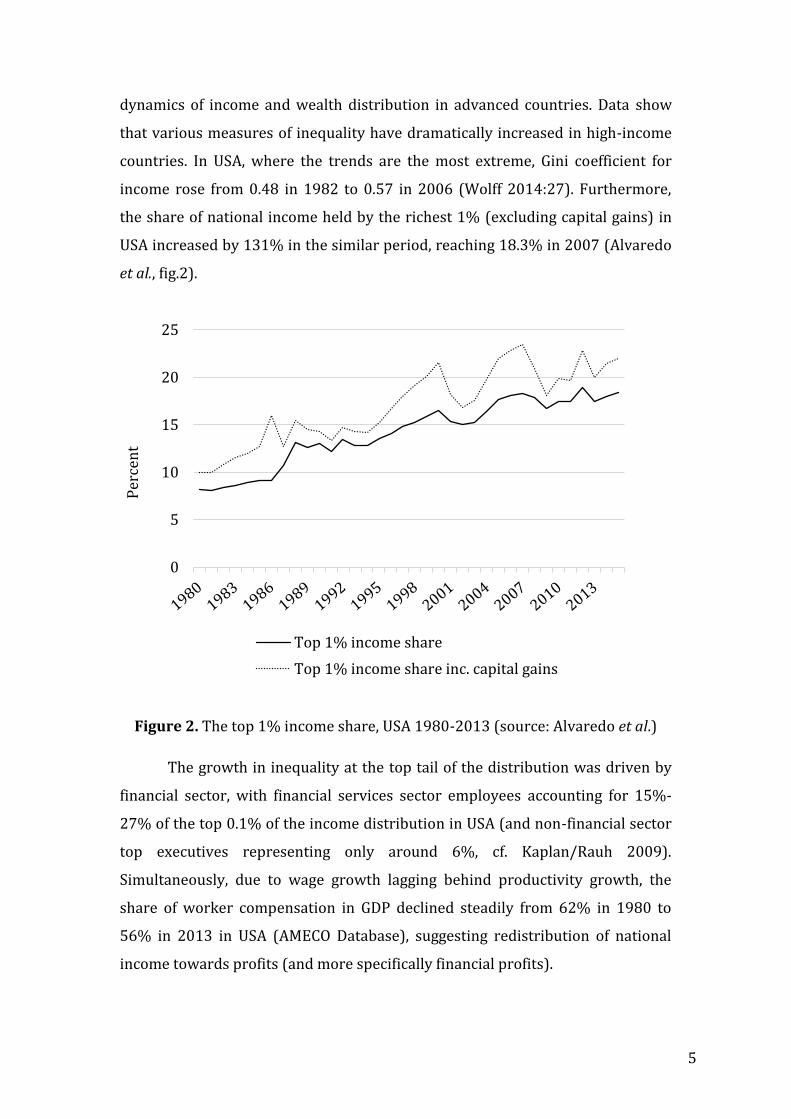

dynamics of income and wealth distribution in advanced countries. Data show

that various measures of inequality have dramatically increased in high-income

countries. In USA, where the trends are the most extreme, Gini coefficient for

income rose from 0.48 in 1982 to 0.57 in 2006 (Wolff 2014:27). Furthermore,

the share of national income held by the richest 1% (excluding capital gains) in

USA increased by 131% in the similar period, reaching 18.3% in 2007 (Alvaredo

et al., fig.2).

Figure 2. The top 1% income share, USA 1980-2013 (source: Alvaredo et al.)

The growth in inequality at the top tail of the distribution was driven by

financial sector, with financial services sector employees accounting for 15%-

27% of the top 0.1% of the income distribution in USA (and non-financial sector

top executives representing only around 6%, cf. Kaplan/Rauh 2009).

Simultaneously, due to wage growth lagging behind productivity growth, the

share of worker compensation in GDP declined steadily from 62% in 1980 to

56% in 2013 in USA (AMECO Database), suggesting redistribution of national

income towards profits (and more specifically financial profits).

Per

cen

t

0

5

10

15

20

25

Top 1% income share

Top 1% income share inc. capital gains

6

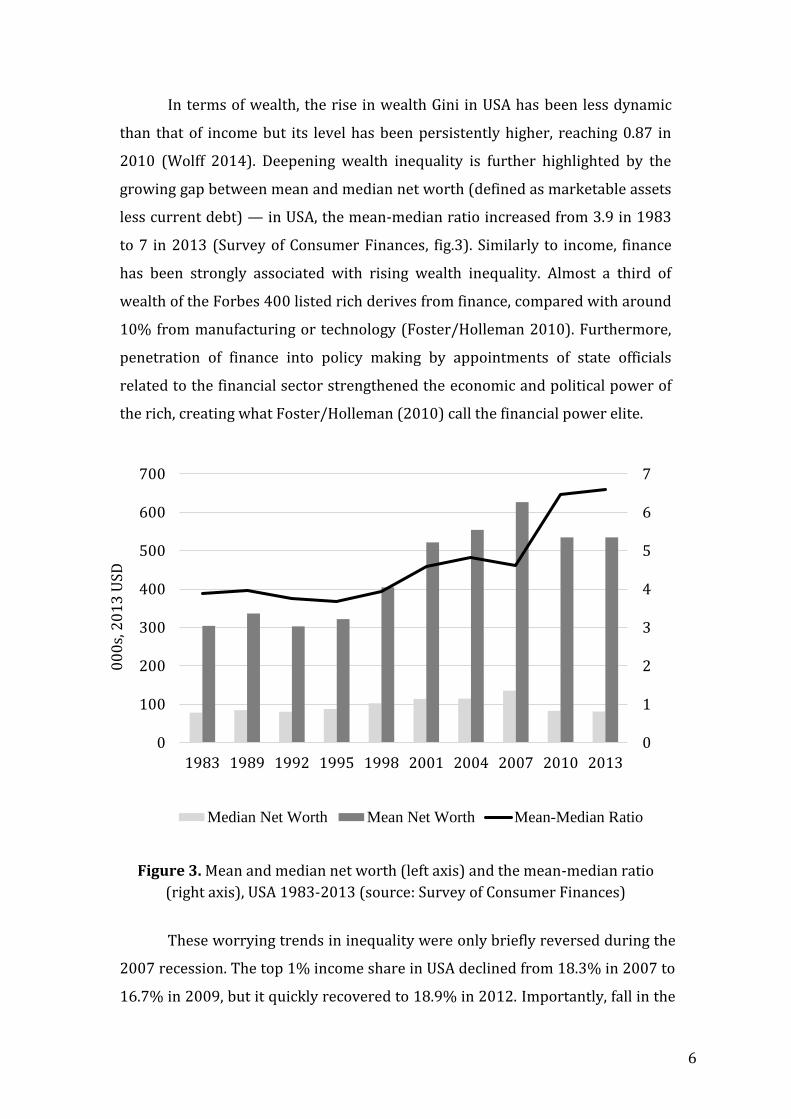

In terms of wealth, the rise in wealth Gini in USA has been less dynamic

than that of income but its level has been persistently higher, reaching 0.87 in

2010 (Wolff 2014). Deepening wealth inequality is further highlighted by the

growing gap between mean and median net worth (defined as marketable assets

less current debt) — in USA, the mean-median ratio increased from 3.9 in 1983

to 7 in 2013 (Survey of Consumer Finances, fig.3). Similarly to income, finance

has been strongly associated with rising wealth inequality. Almost a third of

wealth of the Forbes 400 listed rich derives from finance, compared with around

10% from manufacturing or technology (Foster/Holleman 2010). Furthermore,

penetration of finance into policy making by appointments of state officials

related to the financial sector strengthened the economic and political power of

the rich, creating what Foster/Holleman (2010) call the financial power elite.

Figure 3. Mean and median net worth (left axis) and the mean-median ratio

(right axis), USA 1983-2013 (source: Survey of Consumer Finances)

These worrying trends in inequality were only briefly reversed during the

2007 recession. The top 1% income share in USA declined from 18.3% in 2007 to

16.7% in 2009, but it quickly recovered to 18.9% in 2012. Importantly, fall in the

0

1

2

3

4

5

6

7

0

100

200

300

400

500

600

700

1983 1989 1992 1995 1998 2001 2004 2007 2010 2013

Median Net Worth Mean Net Worth Mean-Median Ratio

00

0s,

20

13

US

D

7

3.5

60.6

18.921

127

41.2

71.5

134.5

51.3

0

20

40

60

80

100

120

140

Debt / equity ratio Debt / income ratio Principal residencedebt / house value

Top 1%

All HHs

Middle 3

quintiles

top 1% share of national income was redistributed within the top quintile, as the

share of the top 10% decreased by far less than the top 1% share between

2007-2011 (Dufour/Orhangazi 2016:165). Real wages were temporarily on the

rise and despite growing unemployment, low and middle income households

suffered smaller income losses than the top 1%. The latter saw they capital

income diminished in result of falling asset and property prices

(Dufour/Orhangazi 2016:165). The overall Gini coefficient for income fell from

0.57 to 0.55 (Wolff 2014:27). Nevertheless, there are reasons to believe that the

relative income gains for the working class are likely to be short lived as positive

growth of real wages in recent years has been driven primarily by low inflation

(caused mainly by falling commodity prices, which are known to be highly

volatile) rather than rising nominal wages (Gould 2016).

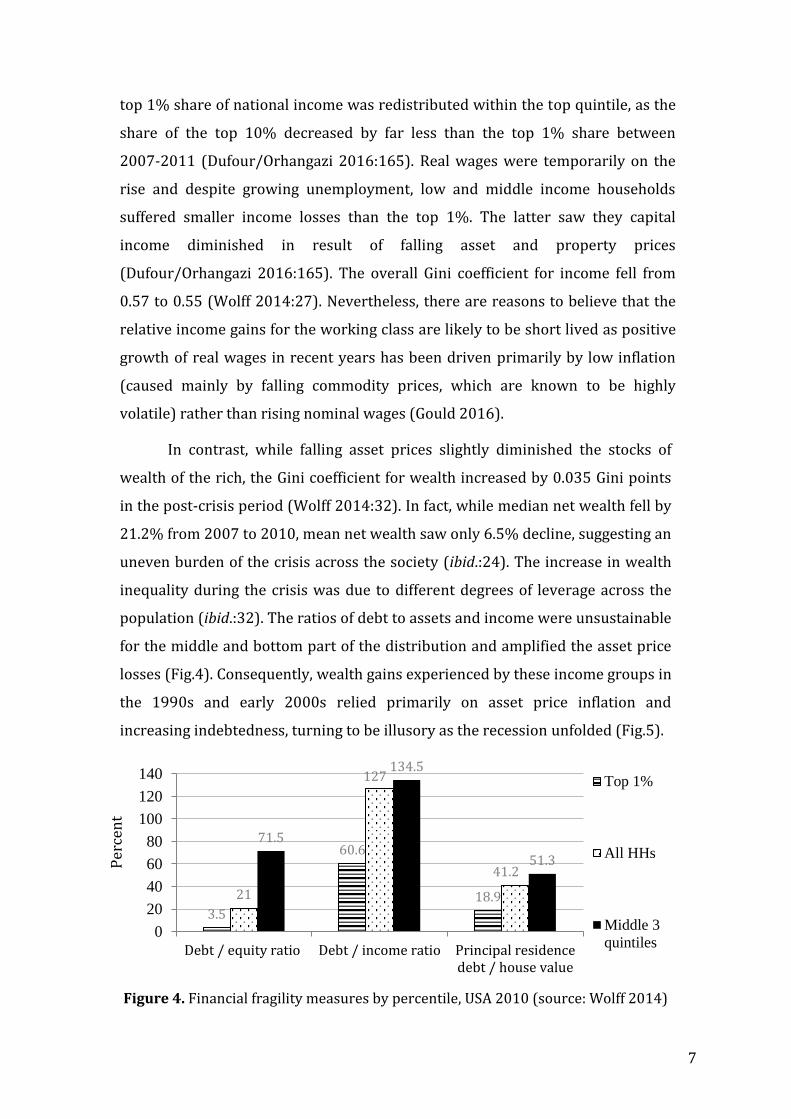

In contrast, while falling asset prices slightly diminished the stocks of

wealth of the rich, the Gini coefficient for wealth increased by 0.035 Gini points

in the post-crisis period (Wolff 2014:32). In fact, while median net wealth fell by

21.2% from 2007 to 2010, mean net wealth saw only 6.5% decline, suggesting an

uneven burden of the crisis across the society (ibid.:24). The increase in wealth

inequality during the crisis was due to different degrees of leverage across the

population (ibid.:32). The ratios of debt to assets and income were unsustainable

for the middle and bottom part of the distribution and amplified the asset price

losses (Fig.4). Consequently, wealth gains experienced by these income groups in

the 1990s and early 2000s relied primarily on asset price inflation and

increasing indebtedness, turning to be illusory as the recession unfolded (Fig.5).

Figure 4. Financial fragility measures by percentile, USA 2010 (source: Wolff 2014)

Per

cen

t

8

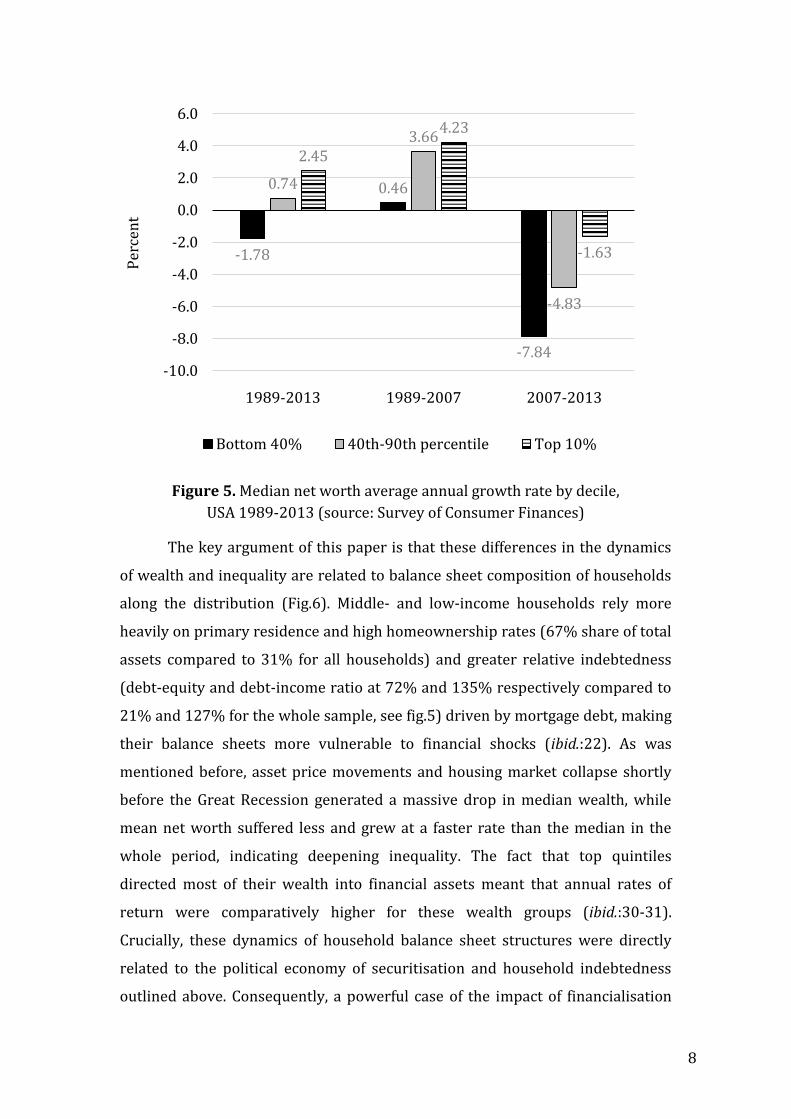

Figure 5. Median net worth average annual growth rate by decile,

USA 1989-2013 (source: Survey of Consumer Finances)

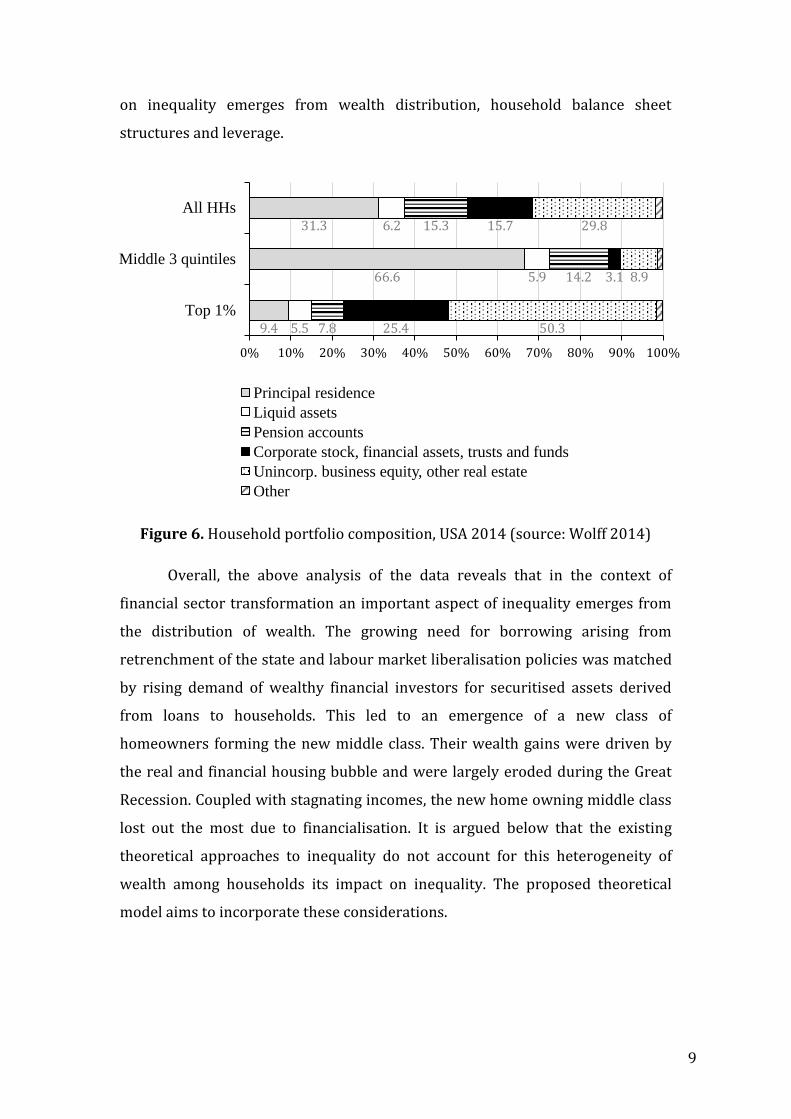

The key argument of this paper is that these differences in the dynamics

of wealth and inequality are related to balance sheet composition of households

along the distribution (Fig.6). Middle- and low-income households rely more

heavily on primary residence and high homeownership rates (67% share of total

assets compared to 31% for all households) and greater relative indebtedness

(debt-equity and debt-income ratio at 72% and 135% respectively compared to

21% and 127% for the whole sample, see fig.5) driven by mortgage debt, making

their balance sheets more vulnerable to financial shocks (ibid.:22). As was

mentioned before, asset price movements and housing market collapse shortly

before the Great Recession generated a massive drop in median wealth, while

mean net worth suffered less and grew at a faster rate than the median in the

whole period, indicating deepening inequality. The fact that top quintiles

directed most of their wealth into financial assets meant that annual rates of

return were comparatively higher for these wealth groups (ibid.:30-31).

Crucially, these dynamics of household balance sheet structures were directly

related to the political economy of securitisation and household indebtedness

outlined above. Consequently, a powerful case of the impact of financialisation

Per

cen

t

-1.78

0.46

-7.84

0.74

3.66

-4.83

2.45

4.23

-1.63

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

1989-2013 1989-2007 2007-2013

Bottom 40% 40th-90th percentile Top 10%

9

on inequality emerges from wealth distribution, household balance sheet

structures and leverage.

Figure 6. Household portfolio composition, USA 2014 (source: Wolff 2014)

Overall, the above analysis of the data reveals that in the context of

financial sector transformation an important aspect of inequality emerges from

the distribution of wealth. The growing need for borrowing arising from

retrenchment of the state and labour market liberalisation policies was matched

by rising demand of wealthy financial investors for securitised assets derived

from loans to households. This led to an emergence of a new class of

homeowners forming the new middle class. Their wealth gains were driven by

the real and financial housing bubble and were largely eroded during the Great

Recession. Coupled with stagnating incomes, the new home owning middle class

lost out the most due to financialisation. It is argued below that the existing

theoretical approaches to inequality do not account for this heterogeneity of

wealth among households its impact on inequality. The proposed theoretical

model aims to incorporate these considerations.

9.4

66.6

31.3

5.5

5.9

6.2

7.8

14.2

15.3

25.4

3.1

15.7

50.3

8.9

29.8

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Top 1%

Middle 3 quintiles

All HHs

Principal residence

Liquid assets

Pension accounts

Corporate stock, financial assets, trusts and funds

Unincorp. business equity, other real estate

Other

10

II. Theories of inequality and the conceptualisation of the middle

class

Despite its importance in inequality dynamics described above, middle class as

an analytical category has been neglected in the existing theories of inequality.

Although aspects of wealth have been increasingly incorporated into

distributional theories, heterogeneity of households financial positions has not

been taken into consideration explicitly.

Theory putting the largest emphasis on the importance of wealth for

inequality is found in the seminal work of Piketty (2014). The main premise of

his “Capital in the Twenty-First Century” is that inequality is driven by

accumulation of persistently higher returns to wealth (r) relative to the growth

of income (g) (historically averaging at 5% and 1% respectively). Compounding

of the returns to wealth overtime generates higher income flows for the wealth

holders and their inheritors (identified with the top 0.1-1%) than for the rest of

the society. Higher capital income in turn allows for greater saving, facilitating

further wealth generation and perpetuating inequality. In other work

(Piketty/Zucman 2014) it is emphasised that due to its high concentration and

the aforementioned accumulation dynamics, inequality of wealth is more

important for the overall structure of inequality in the 21st century than in the

post-war era. Importantly, saving and consumption propensities are not enough

to predict wealth-income levels in advanced countries (higher wealth-income

ratios suggesting large economic power of asset holders and deepening

inequality). This is because capital gains (often driven by housing wealth) are

found to account for around 40% of increase in national wealth to income ratios

between 1970 and 2010 (Piketty/Zucman 2014:1288).

Piketty’s insight regarding the interplay between income and wealth

dynamics and its impact on inequality is particularly relevant in the age of

financialisation. As highlighted in the introduction, financial innovation and

securitisation influenced inequality by generating differential rates of return and

degrees of volatility across the distribution. Large wealth holdings of the rich

allowed them to invest in high-yielding financial instruments (often requiring

large initial payments, which can only be afforded at high levels of net worth),

11

generating sizeable capital income. Moreover, they were able to use their

economic power to secure higher wages, particularly when employed in financial

sector.

Despite the importance of its general conclusions, Piketty’s “Capital in the

Twenty-First century” suffers from several drawbacks. The most relevant

criticisms for our analysis concern the weakness of Piketty’s theoretical

explanation and insufficient emphasis on household debt in contributing to

inequality.

While his empirical work is to be applauded, theoretical explanation for

inequality based on “r greater than g” relies on the expectation that these trends

observed in the past would continue into the future (Pressman 2016:159).

Hence, Piketty does not provide any explicit theoretical explanation why returns

to wealth should always exceed the growth of income. Consequently, despite the

relevance of his conclusions, there is no formal link between inequality and

financial sector transformation in Piketty’s framework.

The alternative body of theoretical literature identified with the Post

Keynesian functional distribution explicitly takes into account the link between

financialisation and distribution. It focuses on the macroeconomic impact of

increasingly unequal functional distribution of national income between two

factors of production – capital and labour – which are associated with higher

propensity to save and consume respectively (cf. Kalecki 1971). The distributive

forces of financialisation are seen as the maximisation of shareholder value,

proxied by a higher rentier (i.e. capitalist) income share, although the precise

view on which of the aspects of financialisation is the most important for

redistribution varies among researchers (cf. Hein 2009, 2015; Hein/Van Treeck

2010; Palley 2012, 2013; Van Treeck 2009). These models often draw from

Bhaduri/Marglin (1990) argument that the macroeconomic effects of income

transfers between wage and profit earners hinge on whether the economy is

wage- or profit-led. Onaran et al. (2011) establish that the majority of advanced

economies are wage-led, which in the Bhaduri/Marglin framework signifies that

lower wage share resulting from financial sector transformation has a negative

impact on aggregate demand and growth by undercutting effective investment

12

demand because resources are taken away from those who are more likely to

spend them to those who are more likely to hoard them.

However, what this theoretical approach has not yet done is to examine

how the transformation in the nature of financial intermediation has

complexified the division of society into two distinct categories. Both groups of

“workers” and “capitalists” have become heterogeneous, which complicates their

analytical usefulness. In the course of financialisation workers became the

recipients of capital income through homeownership and private pension

schemes, while capitalists became the recipients of the highest wages in the

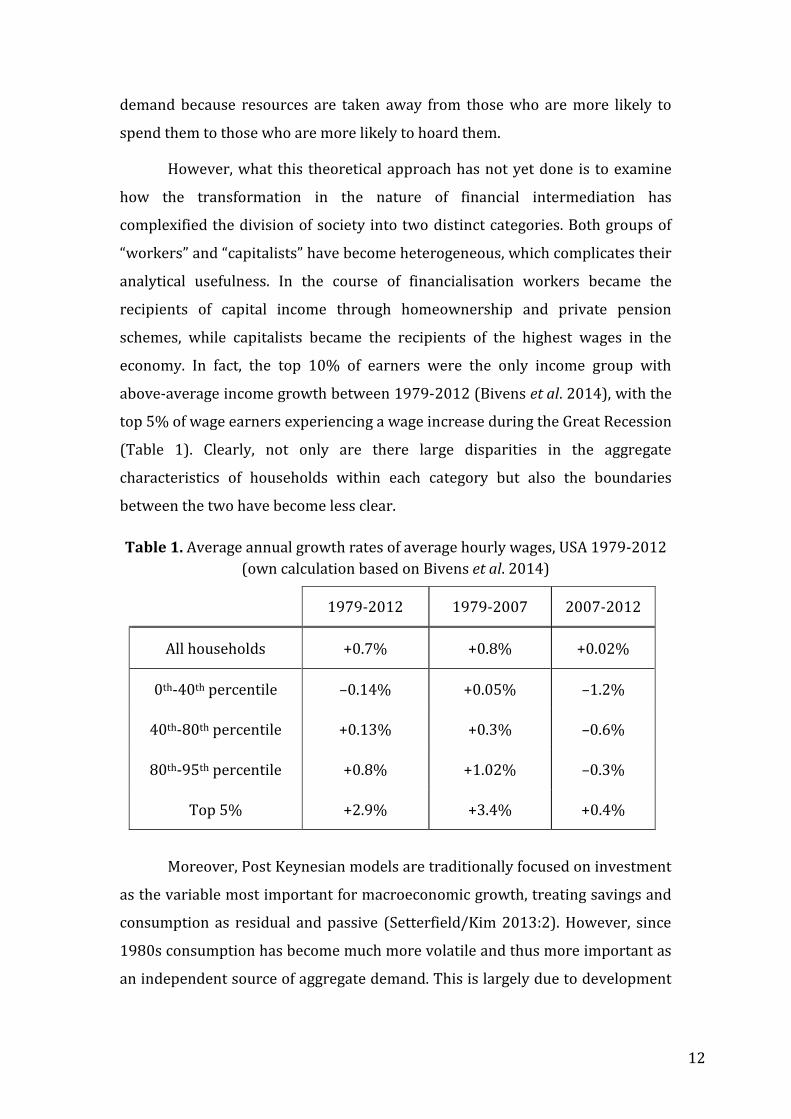

economy. In fact, the top 10% of earners were the only income group with

above-average income growth between 1979-2012 (Bivens et al. 2014), with the

top 5% of wage earners experiencing a wage increase during the Great Recession

(Table 1). Clearly, not only are there large disparities in the aggregate

characteristics of households within each category but also the boundaries

between the two have become less clear.

Table 1. Average annual growth rates of average hourly wages, USA 1979-2012

(own calculation based on Bivens et al. 2014)

Moreover, Post Keynesian models are traditionally focused on investment

as the variable most important for macroeconomic growth, treating savings and

consumption as residual and passive (Setterfield/Kim 2013:2). However, since

1980s consumption has become much more volatile and thus more important as

an independent source of aggregate demand. This is largely due to development

1979-2012 1979-2007 2007-2012

All households +0.7% +0.8% +0.02%

0th-40th percentile –0.14% +0.05% –1.2%

40th-80th percentile +0.13% +0.3% –0.6%

80th-95th percentile +0.8% +1.02% –0.3%

Top 5% +2.9% +3.4% +0.4%

13

of financial sectors and massive expansion of credit to households, leading

household spending to become increasingly disconnected from income.

Similar drawback can be identified in Piketty. This is because his

argument relies on comparing average growth rates of wealth and income.

However, there is a substantial variability in income and wealth trends across

the distribution, which is particularly important when it comes to understanding

the impact of financialisation on inequality. As suggested in the introduction, the

top 10% experienced the most rapid and above average wage income and net

wealth growth over the past decades. In contrast, income and wealth gains to the

middle and lower class were illusory as they were underpinned by a housing

price bubble and large household debt holdings relative to income and assets.

Consequently, differential degrees of leverage across the population turned to be

an important driver of inequality, particularly during the 2007 recession. It is not

only the access to financial resources but also the stability of that access across

the population that has implications for inequality. For instance, financial

investors owning a diversified portfolio of securitised assets with return

guaranteed by the seniorage of their claims (due to tranching) are better able to

bear financial losses associated with risky financial instruments than households

whose portfolios are based on housing equity withdrawal (HEW). In the latter

case, price deflation of collateralised assets prevents further withdrawal of

equity to cover outstanding loan repayments, generating higher volatility of

household’s balance sheet position relative to the former case. Since interest

rates differ for the bottom/middle and high-income households, there is a

disproportionate impact of borrowing on financial stability of households’

balance sheets (Pressman/Scott 2009). When interest payments are considered,

smaller portion of income is available of consumption and hence inequality is

deepened.

Examination of household balance sheets structures remains relevant

after the Great Recession. Scott/Pressman (2015) show that households have

not deleveraged their massive debt levels after the 2008 crisis. Using data from

US Survey of Consumer Finances (SCF) they show that the decrease in total

median monthly debt payments and debt payments to income ratio have been

14

illusory and reflected low interest rates rather than real reduction in debt. In

fact, mortgage debt levels have not fallen much since the recession. Moreover,

the share of households filing for bankruptcy has been rising since 2010. Because

households have not deleveraged properly after the Great Recession, there have

been no increases in consumption and saving allowing for more equitable

growth of the economy.

Consequently, there is a gap in the existing literature on inequality. On the

one hand, Piketty’s insight on the interplay between wealth and income is not

fully developed on a theoretical level. On the other hand, the Post Keynesian

theoretical literature does not take into sufficiently explore the role of wealth

distribution for overall inequality dynamics. This provides an opportunity to

complement the existing literature with a theoretical model incorporating

wealth into the analysis of inequality. We propose a three-class theoretical

model aiming to explain the observed trends in inequality, accounting for

disparate wage growth, unequal returns to wealth and leverage across the

population and the role played by the middle class.

Definition of the middle class is a complex task as it can be considered

along a variety of dimensions. In monetary terms it is defined, according to the

relative size of income, as the middle 60% of the population, with incomes

ranging from 75% to 125% of median income as the standard, although some

studies have extended the upper limit to as much as 300% of median income

(this is because with 125% as the cut-off a disproportionately large portion of

the population in certain countries falls into the upper class category, cf.

Pressman 2007). Atkinson/Brandolini (2011) develop a wealth criterion to

qualify the income definition of the middle class. Based on various studies, the

rich can be classified as having net wealth at least 30 times larger than mean

income. As for the lower cut-off point, members of the middle class should have

enough real and financial assets to be clear from the risk of falling into poverty

for a certain period of time, e.g. 6 months, if income suddenly falls.

Atkinson/Brandolini argue that asset-poor individuals may need to be excluded

from the middle class even if their income exceeds the poverty threshold.

Furthermore, classification of the middle class depends on social criteria such as

15

class consciousness, social status, lifestyle and type of employment, which

influences individual’s economic security and prospects.

In the Post Keynesian literature, Palley (2015) constitutes one of the first

attempts at formalising the middle class. He models a Goodwinian three-class

economy, with household sector divided into upper, middle and working class

according to the type of employment. Class membership is defined through

capital ownership terms. Upper class is identified with the richest 1% of the

population, corresponding to the top managers. The middle class consisting of

middle managers is defined as the next 19% and hence is much smaller than

traditionally envisaged in the literature and does not contain the median

household. The working class is the bottom 80% and consists of non-supervisory

production workers. Palley’s model introduces a complex class struggle, where

the middle managerial class has conflicts with both the upper and the working

class. Managerial pay is seen as a deduction from surplus in line with Kalecki

(1971), as top managers receive a share of firms’ profit. In contrast, middle

managers’ pay is treated, as is the non-managerial wage, as part of the wage bill

and hence the cost of production based on which the mark-up prices are

determined. Moreover, while non-managerial workers are paid hourly, middle

managers receive a salary. The workers’ share of the wage bill is dependent on

exogenously determined labour bargaining power as well as employment rate

and working hours. Middle and top managers save part of their income, while

workers are traditionally assumed to consume all their wages. Hence, since

middle managers own part of the capital stock, transfer of income towards non-

managerial workers increases consumption. Similarly, because middle managers

have larger propensity to consume than top managers, increase in middle

managerial income boosts consumption. In this setting, class conflict is

complexified as the middle class benefits from higher profit share (which aligns

their interests with those of top managers) as well as from a higher wage share

(creating a common interest with the working class). Simultaneously, it is in

conflict with both the top managerial and working class over the share of profits

and the wage bill respectively. The political alliance of the middle class will

ultimately depend on which source of income – wages or capital – is preferred

(Palley 2015:240).

16

While Palley’s model constitutes an important contribution to the

literature, its conclusions concern the functional distribution of income. The

middle class is argued to have contradicting interests and conflicts with the

upper and lower income groups. However, as argued before, the process of

financialisation harmed the middle class’ wealth and incomes, making their fate

more similar to the working class in terms of class and power struggle. Since the

task of our analysis is to incorporate wealth aspects into the analysis of

inequality in the age of financial sector transformation and since distribution is

interpreted through household balance sheets rather than wage/profit shares, a

new conceptualisation of the middle class is proposed below.

III. Wealth and inequality in stock-flow consistent models

To maintain dialogue with the existing literature on financialisation and

distribution described above, we adopt the method frequently used among the

Post Keynesians, namely the stock flow consistent modelling (thereby SFCM).

Originating in Copeland (1949) and the works of Tobin and Godley in 1980s, the

framework has recently been formalised by Godley/Lavoie (2007). It is a

macroeconomic tool integrating stocks and flows across real and financial

sectors in the economy in a consistent fashion, relying on the quadruple-entry

system, which necessitates that every inflow has a corresponding outflow in the

system (Caverzasi/Godin 2013).

A number of recent contributions in the SFCM literature take into account

some aspects of household wealth into the analyses of growth and

macroeconomic stability (Zezza 2008; Caversazi/Godin 2013; Setterfield/Kim

2013; Nikolaidi 2015; Sawyer/Passarella Veronese 2015;

Dafermos/Papatheodorou 2015). Most commonly, it is by allowing for

borrowing by workers, whose debt becomes financial assets of the rentiers via

banks. Wealth of rentiers is usually divided into equities and deposits and

allocation between these two components depends on the relative rates of

return. We argue, however, that current analyses do not adequately capture the

impact of financialisation on balance sheet structures of different households

and hence inequality. The models do not consider the importance of the middle

17

class in this context as the standard two-class division of households into

workers and capitalists prevails.

With the exception of Dafermos/Papatheodorou (2015), most of the

SFCMs reviewed above do not explain income distribution endogenously. This is

because they are ultimately concerned with macroeconomic growth and

stability. Consequently, analysis of household balance sheets based on the

division of society in two classes of workers and capitalists encounters the same

difficulties as described in the previous section, namely that they do not

sufficiently account for the heterogeneity of wealth among different households.

Apart from Sawyer/Passarella Veronese (2015) borrowing is restricted to

workers, while in most high-income countries it is the rich who are indebted the

most both in terms of value and participation (Survey of Consumer Finances).

Furthermore, few of the studies reviewed above take into account changes

within the financial sector brought about by financialisation – Nikolaidi (2015)

and Sawyer/Passarella Veronese (2015) constitute one of the few analyses

incorporating a sophisticated financial sector. Consequently, the proposed model

attempts to fill the emergent gap in the literature, providing an analysis of

endogenous inequality determination in an economy with a complex financial

sector. Emphasis is put on balance sheet structures within the household sector

and, in particular, different levels of leverage across the population.

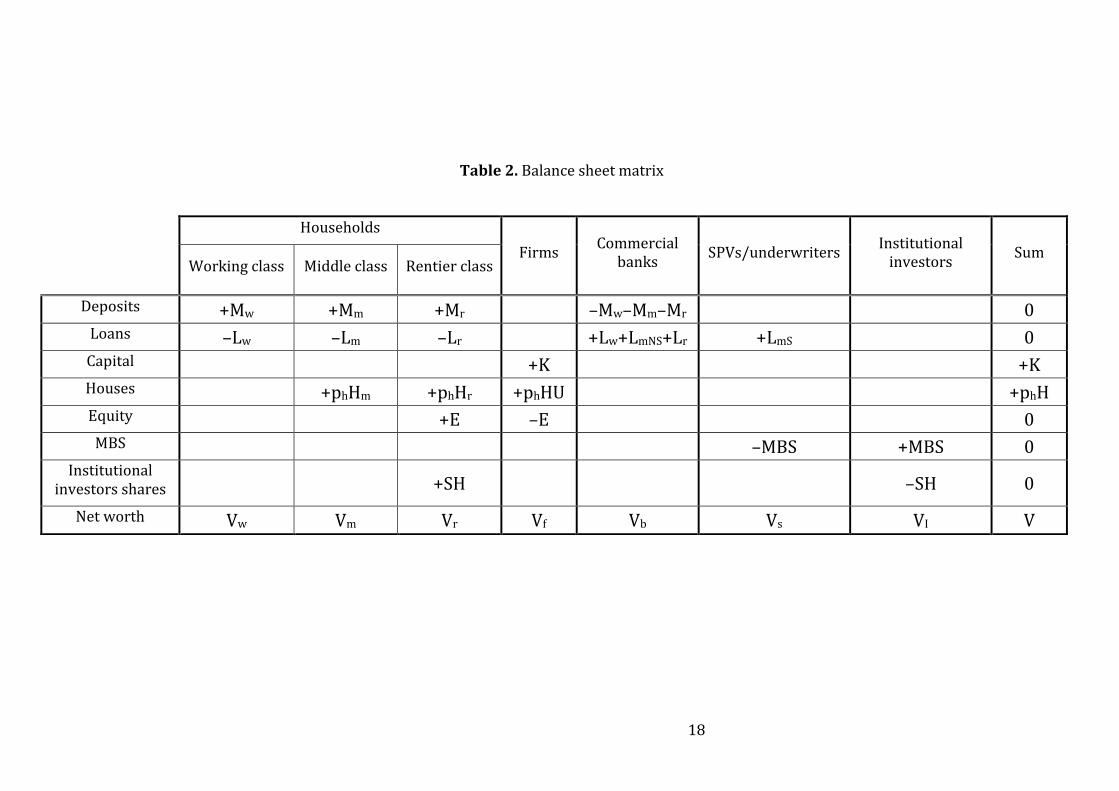

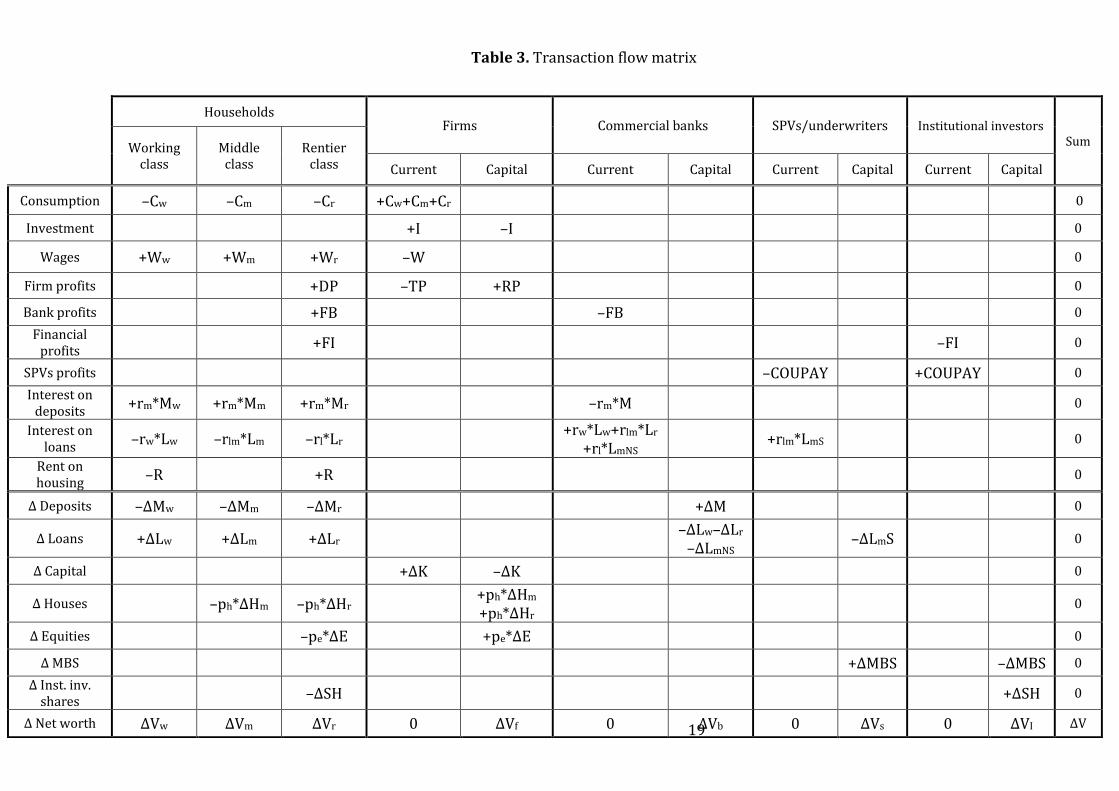

IV. Model specification

The aim of the model presented in this paper is to account for household wealth

dynamics in explaining inequality in a financialised economy, using the

benchmark framework developed by Dafermos/Papatheodorou (2015). The US

economy is taken as an example. The methodology of SFCM yields itself to

consideration of the reinforcing dynamics between stocks of wealth and flows of

income a la Piketty. Tables 2 and 3 present the balance sheet and transaction

flow matrices respectively. The model considers a closed economy with no

government consisting of 5 sectors: a three-tier household sector, firms,

commercial banks, special purpose vehicles (SPVs) and underwriters, as well as

institutional investors. m

18

Table 2. Balance sheet matrix

Households

Firms Commercial

banks SPVs/underwriters

Institutional investors

Sum Working class Middle class Rentier class

Deposits +Mw +Mm +Mr –Mw–Mm–Mr 0 Loans –Lw –Lm –Lr +Lw+LmNS+Lr +LmS 0 Capital +K +K Houses +phHm +phHr +phHU +phH Equity +E –E 0 MBS –MBS +MBS 0

Institutional investors shares +SH –SH 0

Net worth Vw Vm Vr Vf Vb Vs VI V

19

Table 3. Transaction flow matrix

Households Firms Commercial banks SPVs/underwriters Institutional investors

Sum Working class

Middle class

Rentier class Current Capital Current Capital Current Capital Current Capital

Consumption –Cw –Cm –Cr +Cw+Cm+Cr 0

Investment +I –I 0

Wages +Ww +Wm +Wr –W 0

Firm profits +DP –TP +RP 0

Bank profits +FB –FB 0

Financial profits

+FI –FI 0

SPVs profits –COUPAY +COUPAY 0

Interest on deposits

+rm*Mw +rm*Mm +rm*Mr –rm*M 0

Interest on loans

–rw*Lw –rlm*Lm –rl*Lr +rw*Lw+rlm*Lr

+rl*LmNS +rlm*LmS 0

Rent on housing

–R +R 0

Δ Deposits –ΔMw –ΔMm –ΔMr +ΔM 0

Δ Loans +ΔLw +ΔLm +ΔLr –ΔLw–ΔLr

–ΔLmNS –ΔLmS 0

Δ Capital +ΔK –ΔK 0

Δ Houses –ph*ΔHm –ph*ΔHr +ph*ΔHm +ph*ΔHr

0

Δ Equities –pe*ΔE +pe*ΔE 0

Δ MBS +ΔMBS –ΔMBS 0

Δ Inst. inv. shares

–ΔSH +ΔSH 0

Δ Net worth ΔVw ΔVm ΔVr 0 ΔVf 0 ΔVb 0 ΔVs 0 ΔVI ΔV

20

The household sector

In contrast to the existing Post Keynesian approaches to distribution, social

groups in our analysis are defined not by the type of employment or ownership

of the means of production but by their balance sheet characteristics. As argued

previously, this is a more suitable method to understanding inequality in the age

of financial sector transformation and massive indebtedness of the society.

Moreover, it links with the theory developed by Piketty, which highlights the

importance of wealth in contributing to overall inequality.

The working class

Classification of the working class in the present model is conceptually the

closest to the “workers” category encountered in the literature. The working

class includes non-supervisory production/“blue collar” workers. In line with the

Kaleckian approach, this group has the highest propensity to consume. Critically,

they are the most leveraged group. It is identified with the bottom 40% of US

population, which experience net wealth losses over the past three decades (see

fig.5 above).

One of the phenomena associated with financial sector transformation

has been the massive extension of credit to those previously excluded from

access to it based on their low incomes and low or non-existent wealth. As was

argued before, this credit expansion wasn’t accidental as household loans,

primarily mortgages and consumer credit, constituted the basis for asset-backed

securities. Consequently, there were strong incentives in the financial sector to

generate as many household loans as possible to satisfy the growing demands of

financial investors for securitised instruments. For these reasons, analysis of the

household sector in the model accounting for financial sector transformation

calls for consideration of credit among the lowest income groups. In the present

model, the working class households are seen as subprime borrowers. We

assume that they do not carry enough wealth and income that would allow them

to take out mortgages and hence that all working class households rent houses.

Consequently, it is assumed that credit to the working class households consists

of unsecured short-term consumer credit and payday loans. This has been

particularly relevant in recent years as unsecured debt and payday borrowing

21

have been on the rise after the crisis (cf. The Pew Charitable Trust 2012; PWC

2015).

Working class households rely primarily on wage income (Bivens et al.

2014:6). In our model, real disposable income of the working class consists of

wages and interest earned on deposits, less interest paid on loans and house

rental payments to rentiers (eq.1). Households consume part c1 of their

disposable income as well as proportion c3 of their wealth, and store the

remaining savings as bank deposits (eq.3–4). We assume that the propensity to

consume of this income group is the highest among all households. Furthermore,

we assume constant propensity to consume out of wealth c3 across all household

groups.

Assuming simple adaptive expectations, borrowing by the working class

is determined by their past consumption level, adjusted by parameter β (eq.5). β

captures household borrowing norms as well as lending norms in the financial

sector (Setterfield/Kim 2013:10). In this way, we are able to indirectly account

for borrowing constraints for workers, reflecting commercial banks’ attitude

towards creditworthiness of borrowers. We can think of β as high during the

housing bubble, when lending norms were lax due to the perceived minimisation

of credit risk by securitisation. In times of recessions, β can be thought of as low

as lenders are more concerned about creditworthiness and lending norms are

strict. Because workers are constrained in their access to credit, their demand

for loans also includes the debt burden ratio, capturing the repayment capacity

of past loans.

𝑌𝐷𝑤 =𝑁𝑤

𝑁𝑤+𝑁𝑚+𝑁𝑟𝑊 + 𝑟𝑚𝑀𝑤,−1 − 𝑟𝑤,−1𝐿𝑤,−1 − 𝑅 (1)

𝑌𝐺𝑤 =𝑁𝑤

𝑁𝑤+𝑁𝑚+𝑁𝑟𝑊 + 𝑟𝑚𝑀𝑤,−1 + 𝑟𝑤,−1𝐿𝑤,−1 (2)

𝐶𝑤 = 𝑐1𝑌𝐷𝑤,−1 + 𝑐3𝑉𝑤,−1 (3)

𝑀�̇� = 𝑌𝐷𝑤 − 𝐶𝑤 (4)

𝐿�̇� = 𝛽𝐶𝑤,−1 − 𝐷𝑆𝑌𝑤𝐿𝑤,−1, , 𝛽 > 0 (5)

𝑉𝑤 = 𝑀𝑤 − 𝐿𝑤 (6)

22

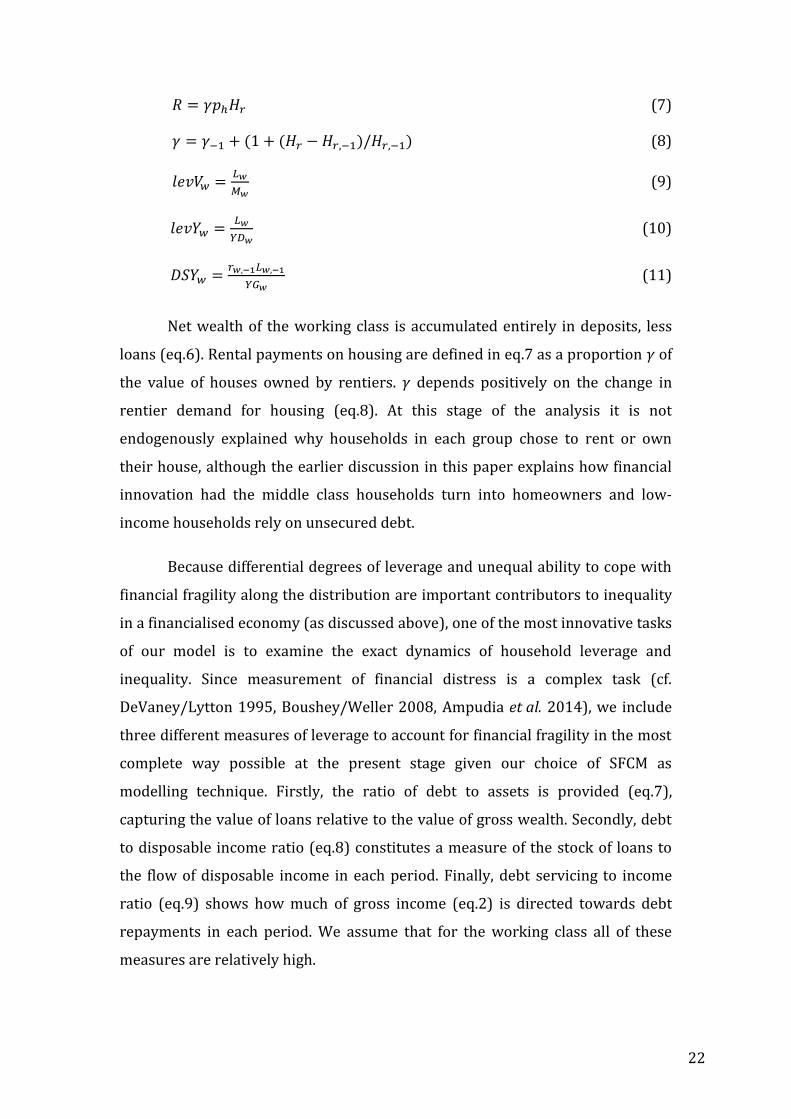

𝑅 = 𝛾𝑝ℎ𝐻𝑟 (7)

𝛾 = 𝛾−1 + (1 + (𝐻𝑟 − 𝐻𝑟,−1)/𝐻𝑟,−1) (8)

𝑙𝑒𝑣𝑉𝑤 =𝐿𝑤

𝑀𝑤 (9)

𝑙𝑒𝑣𝑌𝑤 =𝐿𝑤

𝑌𝐷𝑤 (10)

𝐷𝑆𝑌𝑤 =𝑟𝑤,−1𝐿𝑤,−1

𝑌𝐺𝑤 (11)

Net wealth of the working class is accumulated entirely in deposits, less

loans (eq.6). Rental payments on housing are defined in eq.7 as a proportion 𝛾 of

the value of houses owned by rentiers. 𝛾 depends positively on the change in

rentier demand for housing (eq.8). At this stage of the analysis it is not

endogenously explained why households in each group chose to rent or own

their house, although the earlier discussion in this paper explains how financial

innovation had the middle class households turn into homeowners and low-

income households rely on unsecured debt.

Because differential degrees of leverage and unequal ability to cope with

financial fragility along the distribution are important contributors to inequality

in a financialised economy (as discussed above), one of the most innovative tasks

of our model is to examine the exact dynamics of household leverage and

inequality. Since measurement of financial distress is a complex task (cf.

DeVaney/Lytton 1995, Boushey/Weller 2008, Ampudia et al. 2014), we include

three different measures of leverage to account for financial fragility in the most

complete way possible at the present stage given our choice of SFCM as

modelling technique. Firstly, the ratio of debt to assets is provided (eq.7),

capturing the value of loans relative to the value of gross wealth. Secondly, debt

to disposable income ratio (eq.8) constitutes a measure of the stock of loans to

the flow of disposable income in each period. Finally, debt servicing to income

ratio (eq.9) shows how much of gross income (eq.2) is directed towards debt

repayments in each period. We assume that for the working class all of these

measures are relatively high.

23

The middle class

As suggested previously, definition of the middle class in our model differs

sharply from Palley’s analysis as it is centred on the stylised facts on balance

sheet composition and income trends found in the income and wealth data for

USA.

Importantly, the middle class is defined as a group whose balance sheets

depend on housing. Their wealth was rising in the 1990s and 2000s due to

increasing house prices, allowing them to refinance their mortgages by taking on

more credit and engage in home equity withdrawal, a strategy which was only

feasible in house price bubble. When the price trends reversed during 2006 and

2007, these households saw their wealth gains largely wipe out. Separation of

this group from the working class is important as the evidence shows that in USA

inequality growth has been the most striking between the middle and upper

parts of the population rather than between the top and the bottom (cf. Wolff

2014). This is because of the differential rates of return on wealth of the upper

and middle income groups as well as stagnant income for the latter. For these

reasons, the middle class is assumed to have high leverage ratios.

Our definition of the middle class encompasses the portion of the

population between the 40th and the 90th percentile and thus includes the

median household. The lower cut-off has been chosen as households below the

40th percentile saw negative wage and net worth growth between 1989-2013

(see table 1 and fig.5). In contrast, the upper cut-off has been chosen as only

households above the 90th percentile experienced above average income growth

(Bivens et al. 2014).

Because the middle class is assumed to account for 50% of population in

our analysis, issues associated with heterogeneity of this group need to be

acknowledged. Currently, the middle class in our model includes both subprime

mortgage borrowers, whose incomes resemble more the income of the working

class, and the middle-managers in the 80th-90th percentile, whose incomes and

wealth are closer to the rentier households.

24

We argue that heterogeneity issues cannot be avoided in analysing the

household sector. Three class division adopted here is superior to the two-class

conceptualisation of households in the literature because it allows for a more

intricate examination of household balance sheets, leverage and incomes in the

age of financialisation, which altered the traditionally envisaged economic

relationships. There is a possibility of extending the division of households even

further, which has been done by Dafermos/Papatheodorou (2015). Such detailed

division is not necessary in the present model for two reasons. Firstly, it would

introduce a considerable degree of complexity to an already elaborate model of

heterogeneous households and financial institutions. Secondly, in an aggregate

model that SFCM is, it would be difficult to meaningfully break down the social

classes into upper/lower groups and introduce a drastically different picture of

balance sheets than already provided in the three class model. This is because at

the aggregate level the most important distinctions between the different types

of debt and wealth accumulation possibilities are already made.

Real disposable income of the middle class consists of wage income and

interest earned on deposits less interest payments on loans (eq.10). A fraction of

disposable income and wealth is consumed (eq.13). Residual income is saved as

deposits, including realised capital gains on housing (eq.14).

Borrowing of the middle class depends on their target consumption and

their debt burden (eq.15). Target consumption incorporates past consumption

(due to simple adaptive expectations) and relative consumption concerns, which

depend on rentier consumption adjusted by an emulation parameter η (eq.16). η

is exogenously defined as the Ravina emulation parameter (Ravina 2007).

Consumption emulation has recently emerged as a potentially important driver

of borrowing (cf. Cynamon/Fazzari 2008, Pressman/Scott 2009), leading to

lower levels of consumption than income inequality (cf. Krueger/Perri 2006).

However, while in existing SFCM studies emulation is applied to low-income

workers (see above and Kapeller/Schuetz 2015; Detzer 2016), we restrict

relative consumption to the middle class. This approach is more reflective of

reality as emulation motives are more likely to be relevant among the more

affluent households belonging to the middle class, who can afford necessities

25

such as owning their house. In contrast, working class households are more

concerned with maintaining their living standards in the light of rising living

costs (rent payments). Their demand for loans is thus more likely to be driven by

necessitous borrowing concerns (cf. Pollin 1988) rather than their desire to

follow the celebrity lifestyle of the rich. It would be possible to introduce

emulation of the middle class consumption by the working class, in line with the

expenditure cascades theory where each group emulates consumption of the one

just above it in the distribution (Frank et al. 2014). However, we believe that in

the age of financial sector transformation, due to falling median incomes and

increases in the prices of housing, rising demand of low-income households for

unsecured credit such as payday loans is motivated primarily by sustaining a

constant standard of living rather than achievement of social status.

𝑌𝐷𝑚 =𝑁𝑚

𝑁𝑤+𝑁𝑚+𝑁𝑟𝑊 + 𝑟𝑚𝑀𝑚,−1 − 𝑟𝑙𝑚,−1𝐿𝑚,−1 (11)

𝑌𝐺𝑚 =𝑁𝑚

𝑁𝑤+𝑁𝑚+𝑁𝑟𝑊 + 𝑟𝑚𝑀𝑚,−1 + 𝑟𝑙𝑚,−1𝐿𝑚,−1 (12)

𝐶𝑚 = 𝑐4𝑌𝐷𝑚,−1 + 𝑐3𝑉𝑚,−1 (13)

𝑀�̇� = 𝑌𝐷𝑚 − 𝐶𝑚 + 𝐶𝐺𝐻𝑚 (14)

𝐿�̇� = 𝛽𝐶𝑚𝑇 − 𝐷𝑆𝑌𝑚𝐿𝑚,−1, 𝛽 > 0 (15)

𝐶𝑚𝑇 = 𝐶𝑚,−1 + 𝜂𝐶𝑟,−1 (16)

𝑉𝑚 = 𝐷𝑚 + 𝐻𝑚 − 𝐿𝑚 (17)

𝐻�̇� = (𝑌𝐷𝑚 − 𝐶𝑚 + (𝐿𝑚 − 𝐿𝑚,−1) − 𝑙𝑒𝑣𝑌𝑚)/𝑝ℎ (18)

𝐶𝐺𝐻𝑚 = 𝐻𝑚,−1∆𝑝ℎ (19)

𝑙𝑒𝑣𝑉𝑚 =𝐿𝑚

𝑉𝑚+𝐿𝑚 (20)

𝑙𝑒𝑣𝑌𝑚 =𝐿𝑚

𝑌𝐷𝑚 (21)

𝐷𝑆𝑌𝑚 =𝑟𝑙𝑚𝐿𝑚,−1

𝑌𝐺𝑚 (22)

Net wealth of the middle class is composed of deposits and housing, less

loans (eq.17). We therefore assume that middle class households are owner-

occupiers of their houses (and hence that they don’t rent out their property) and

26

that loans to the middle class consist exclusively mortgages. Demand for houses

by the middle class depends positively on their income and change in the

provision of mortgages and negatively on their consumption and debt-to-income

ratio, adjusted by the price of housing (eq.18). As in the case of the working class,

different measures of financial fragility for the middle class are presented,

including the debt-to-asset ratio (eq.20), debt-to-income ratio (eq.21) and the

debt-service-to-income ratio (eq.22).

Rentier class

Households in this group are defined as the top 10% of the population. In

contrast to the other household groups, they saw income growth equal or above

the average since 1980s (Bivens et al. 2014). Moreover, their balance sheets are

relying primarily on financial wealth rather than housing or wages, which

differentiates this group from the middle and the working class respectively (see

fig.6).

Existing studies accounting for distributional heterogeneity often adopt

social classification from the times of Marx and treat the rich as pure rentiers,

deriving their income purely from capital ownership. This is also envisaged by

Piketty – as wealth becomes inherited and compounding returns to wealth

exceed income growth overtime, the rich abandon work as they are able to live

off the returns to their wealth. While this was true in the pre-Fordist era and

seems like a plausible scenario for the future in light of the deepening wealth

concentration, it doesn’t describe the realities seen since the post-war period.

Data for USA show that inheritance accounts for a small portion of existing

wealth for the rich (Keister/Lee 2014:20). In turn, much of the income of the top

10% derives not only from large returns to capital but also from extremely high

salaries, particularly for financial sector executives (cf. Kaplan/Rauh 2010). To

account for growing wage inequality we can describe the rentier class in our

model as “working rentiers”. This complements the traditional Post Keynesian

view of the capitalist class as owners of capital earning no wage income.

Importantly, the rentier class engages in work not because of necessity (as is in

the case of the working and the middle class) but because institutional

conditions made employment an alternative “investment strategy” for the rich

27

along the ownership of capital, as they are able to use their financial power to

influence their earnings.

Furthermore, in contrast to the majority of SFCM studies including debt,

we allow for indebtedness of the rich. This is because the analysis of household

survey data reveals that the top decile undertakes sizeable debt and constitutes

the most indebted income group in terms of both participation and the amount

of debt. Consequently, in our model it is assumed that rentiers borrow from

banks to consume and invest in excess of their wage and capital income. Rentier

borrowing depends positively on their wealth, which serves as a collateral. What

is different about indebtedness of the rich is their leverage. In contrast to other

income groups, debt of the top decile constitutes a small portion of their assets.

Rentiers’ disposable income consists of wages, interest on deposits,

profits of firms, commercial banks and institutional investors, return on equity,

institutional investors’ shares as well as housing rent payments by the working

class households, less interest paid on loans (eq.23). As other household groups,

rentiers consume a fraction of their income and wealth (eq.25). In line with

Kalecki, rentiers are assumed to have the lowest propensity to consume among

all household groups. Deposits of rentiers consist of residual saving as well as

realised capital gains on housing and equity (eq.26).

Borrowing of rentiers (eq.27) depends on their past consumption and

debt burden ratio and does not include relative consumption concerns. It should

be mentioned, however, that since growth in the national income share of the top

10% is driven by the top 1%, and the growth of the top 1% share is driven by the

top 0.1% (cf. Piketty 2014), relative consumption motives are bound to be

especially strong among the richest 10%, who engage in luxury goods

consumption and aim to attain the highest status and the associated “celebrity

lifestyle”. However, high aggregation of SFCM and the elaborate character of the

current model prevent us from modelling the precise consumption behaviour of

different income groups within the top 10%.

It is assumed that the allocation of rentiers’ wealth between houses,

equities, institutional investors’ shares and deposits (treated as a buffer stock)

(eq.29–31) follows a Tobinesque portfolio principle and depends on the relative

28

rates of return offered on these assets (Caverzasi/Godin 2015:16). Business

equity accounts for an important part of wealth for the richest 10% and thus

rentiers in our model are assumed to own all firm equity. Return on housing

considered by the rentiers is given by the ratio of rent payments by the working

class and capital gains on housing to the value of housing in the previous period

(eq.32).

Equations 35 to 37 provide measures of leverage for the rentier

households, expected to be the lowest among all the household groups.

𝑌𝐷𝑟 =𝑁𝑟

𝑁𝑤+𝑁𝑚+𝑁𝑟𝑊 + 𝑊𝑝𝑟 + 𝑟𝑚𝑀𝑟,−1 + 𝐷𝑃 + 𝐹𝐵 + 𝐹𝐼 + 𝑅 − 𝑟𝑙𝐿𝑟,−1 (23)

𝑌𝐺𝑟 =𝑁𝑟

𝑁𝑤+𝑁𝑚+𝑁𝑟𝑊 + 𝑊𝑝𝑟 + 𝑟𝑚𝑀𝑟,−1 + 𝐷𝑃 + 𝐹𝐵 + 𝐹𝐼 + 𝑅 + 𝑟𝑙𝐿𝑟,−1 (24)

𝐶𝑟 = 𝑐2𝑌𝐷𝑟,−1 + 𝑐3𝑉𝑟,−1 (25)

𝑀𝑟̇ = 𝑌𝐷𝑟 − 𝐶𝑟 + 𝐶𝐺𝐻𝑟 + 𝐶𝐺𝐸 (26)

𝐿�̇� = 𝛽𝐶𝑟,−1 − 𝐷𝑆𝑌𝑟𝐿𝑟,−1 (27)

𝑉𝑟 = 𝐷𝑟 + 𝐻𝑟 + 𝐸 + 𝑆𝐻 − 𝐿𝑟 (28)

𝑝𝑒 = (𝜆1,0 + 𝜆1,1𝑟𝑒,−1 + 𝜆1,2𝑟𝑚 + 𝜆1,3𝑌𝐷𝑟,−1

𝑉𝑟,−1+ 𝜆1,4𝑟𝐻𝑟,−1 + 𝜆1,5𝑟𝑠,−1)𝑉𝑟,−1/𝐸−1 (29)

𝐻𝑟 = (𝜆2,0 + 𝜆2,1𝑟𝑒,−1 + 𝜆2,2𝑟𝑚 + 𝜆2,3𝑌𝐷𝑟,−1 − 𝜆2,4𝑟𝐻𝑟,−1 + 𝜆2,5𝑟𝑠,−1)/𝑝ℎ,−1 (30)

𝑆𝐻 = 𝜆3,0 + 𝜆3,1𝑟𝑒,−1 + 𝜆3,2𝑟𝑚 + 𝜆3,3𝑌𝐷𝑟,−1 − 𝜆3,4𝑟𝐻𝑟,−1 + 𝜆3,5𝑟𝑠,−1 (31)

𝑟𝐻𝑟 = (𝑅 + 𝐶𝐺𝐻𝑟)/𝐻𝑟,−1 (32)

𝐶𝐺𝐻𝑟 = 𝐻𝑟,−1∆𝑝ℎ (33)

𝐶𝐺𝐸 = 𝑒−1∆𝑝𝑒 (34)

𝑙𝑒𝑣𝑉𝑟 =𝐿𝑟

𝑉𝑟+𝐿𝑟 (35)

𝑙𝑒𝑣𝑌𝑟 =𝐿𝑟

𝑌𝐷𝑟 (36)

𝐷𝑆𝑌𝑟 =𝑟𝑙𝐿𝑟,−1

𝑌𝐺𝑟 (37)

29

Firms

Firms follow the standard Kaleckian behaviour. Profits are residual (eq.41) and

the profit share is determined as a mark-up over unit labour costs. It is assumed

that firms invest in housing and produce a single capital good on demand so that

capital inventories are not taken into account. Furthermore, we assume that

firms retain part of their profits (eq.42) and distribute the rest to rentiers

(eq.43).

Output of the modelled economy is given by consumption spending of

households as well as investment in productive capital and housing (eq.38).

Wage bill follows from a bargaining process and is defined according to an

exogenously given wage share of output (eq.39). Wage rates of the working and

the middle class depend on the share of each group (Nw and Nm respectively) in

total population. Importantly, wages paid to rentiers are linked to a variable

remuneration dependent on firms’ profits. The rentier wage premium (eq.40) is

given by a premium mw > 1 over the workers’ wage rate, the profit sharing

element 𝜌ℎ and exogenous parameter 𝜌 ∈ (0,1) reflecting the relative

importance of profit remuneration in the wage rate determination

(Dafermos/Papatheodorou 2015:13).

Investment is defined simply as the growth rate of capital stock (eq.44-45).

A fraction x of investment spending is financed by equity issue (eq.46). Return

on equity is given in eq.47, while the value of equities outstanding is defined in

eq.48. Capacity utilisation rate (eq.49) is given as the ratio of actual to potential

output, which is defined in eq.50.

𝑌 = 𝐶𝑤 + 𝐶𝑚 + 𝐶𝑟 + 𝐼 + ∆𝐻 (38)

𝑊 = 𝑠𝑤𝑌 (39)

𝑊𝑝𝑟 = (1 − 𝜌)𝑚𝑤𝑁𝑤+𝑁𝑚

𝑁𝑤+𝑁𝑚+𝑁𝑟+

+ 𝜌ℎ ((𝑌 −𝑁𝑤+𝑁𝑚

𝑁𝑤+𝑁𝑚+𝑁𝑟𝑊 − (1 − 𝜌)𝑚𝑤

𝑁𝑤+𝑁𝑚

𝑁𝑤+𝑁𝑚+𝑁𝑟𝑁𝑟) 𝑁𝑟⁄ ) (40)

𝑇𝑃 = 𝑌 − 𝑊 (41)

𝑅𝑃 = 𝑠𝑓𝑇𝑃 (42)

𝐷𝑃 = 𝑇𝑃 − 𝑅𝑃 (43)

30

𝐼 = 𝑔𝑘𝐾−1 (44)

Δ𝐾 = 𝐼 (45)

𝑒 = 𝑒−1+𝑥𝐼−1/𝑝𝑒 (46)

𝑟𝑒 =𝐷𝑃+𝐶𝐺𝐸

𝑝𝑒,−1𝑒−1 (47)

𝐸 = 𝑝𝑒𝑒−1 + 𝑥𝐼−1 (48)

𝑢 =𝑌

𝑌∗ (49)

𝑌∗ = 𝑣𝐾 (50)

Δ𝐻 = ℎ1 ((𝐻𝑚,−1 + 𝐻𝑟,−1) − 𝐻−1) (51)

Δ𝐻𝑈 = (𝐻 − 𝐻−1) − (𝐻𝑚 − 𝐻𝑚,−1) (52)

𝑝ℎ = 𝑝ℎ,−1 + ℎ2 ((𝐻𝑚+𝐻𝑟)−(𝐻𝑚,−1+𝐻𝑟,−1)

(𝐻𝑚,−1+𝐻𝑟,−1)−

𝐻−𝐻−1

𝐻−1) (53)

Apart from productive capital, firms invest in housing, which depends on

the difference between housing demanded by rentiers and the middle class and

the available housing supply in the previous period (eq.51). In every period, a

stock of houses remains unsold (eq.52), depending on the change in the supply

and demand for housing among the middle class (note that the Tobinesque

portfolio equation implies that all houses demanded by rentiers are sold).

Change in the price of housing is given by the difference between the change in

the demand for housing by rentiers and the middle class and the change in

supply of housing by firms (eq.53).

Commercial banks

Since the aim of our model is to account for inequality determination in the age

of financialisation, commercial banks are envisaged as active profit-seeking

entities rather than passive intermediaries between debtors and creditors.

Profits of commercial banks are generated by charging higher interest rates on

loans than offered on deposits. They are derived as a sum of interest payments

on non-securitised mortgages of the middle class (eq.61), consumer loans of the

working class and loans to rentiers, less interest payments on deposits to

31

households (eq.54). A constant interest rate on deposits is assumed for all

households. All commercial bank profits are transferred to rentier households,

who are the owners of all financial institutions.

Commercial banks accept deposits from the household sector. However,

each household group faces a different rate of interest depending on the

perception of their creditworthiness by banks. Interest on loans to the working

class is higher than the rate charged to the middle class and rentiers (eq.55). This

risk premium depends on exogenous parameters 𝜋0 and 𝜋1, capturing

institutional conditions in financial markets, the debt to income ratio of the

working class, and their debt service ratio (eq.56).

Importantly, part of mortgages taken out by the middle class are

securitised and sold to underwriters and their SPVs (eq.60). The share of

securitised loans (eq.62) depends on an exogenous parameter s0 (capturing

institutional conditions such as the degree of financial regulation) and the target

yield on mortgage-based securities (MBS) (given by the past yield under the

assumption of simple adaptive expectations), adjusted by parameter s1.

Middle class loans are subject to a mortgage rate (eq.57), defined as a

spread over the commercial bank lending rate (eq.58). The mortgage spread

depends positively on parameter 𝜋0, the debt service ratio and the debt to

income ratio of the middle class adjusted by parameter 𝜋2, and negatively on the

rate of return on MBS adjusted by parameter 𝜋3. The redundant equation of the

model is given in eq.59.

𝐹𝐵 = 𝑟𝑤,−1𝐿𝑤,−1 + 𝑟𝑙𝑚𝐿𝑚𝑁𝑆,−1 + 𝑟𝑙𝐿𝑟,−1 − 𝑟𝑚𝑀𝑤,−1 − 𝑟𝑚𝑀𝑚,−1 − 𝑟𝑚𝑀𝑟,−1 (54)

𝑟𝑤 = 𝑟𝑙 + 𝜋 (55)

𝜋 = 𝜋0 + 𝜋1𝑙𝑒𝑣𝑌𝑤,−1𝐷𝑆𝑌𝑤,−1 (56)

𝑟𝑙𝑚 = 𝑟𝑙 + 𝑠𝑝𝑟𝑒𝑎𝑑𝑚 (57)

𝑠𝑝𝑟𝑒𝑎𝑑𝑚 = 𝜋0 + 𝜋2𝑙𝑒𝑣𝑌𝑚,−1𝐷𝑆𝑌𝑚 − 𝜋3𝑟𝑀𝐵𝑆,−1 (58)

𝑀𝑟𝑒𝑑 = 𝐿𝑤 + 𝐿𝑚 + 𝐿𝑟 (59)

𝐿𝑚𝑆 = 𝑠𝐿𝑚 (60)

32

𝐿𝑚𝑁𝑆 = (1 − 𝑠)𝐿𝑚 (61)

𝑠 = 𝑠0 + 𝑠1𝑦𝑖𝑒𝑙𝑑𝑀𝐵𝑆,−1 (62)

SPVs/underwriters

The main role of the sector of SPVs and underwriters is to transform securitised

mortgages bought from commercial banks into mortgage-backed securities

(MBS, eq.63). It is assumed that SPVs/underwriters pay no administrative fees to

banks for this transaction.

It is assumed that all MBS are sold to institutional investors without any

fee in the form of coupon payments (eq.64) at a coupon rate determined by an

exogenous spread over the mortgage rate (eq.65). Consequently, the

SPVs/underwriters sector accumulates no profits. Importantly, MBS issued are

assumed to be of the single “pass-through” type rather than consisting of various

pooled MBS (cf. Nikolaidi 2015:4).

𝑀𝐵𝑆 = 𝑀𝐵𝑆−1 + ∆𝐿𝑚𝑆 (63)

𝐶𝑂𝑈𝑃𝐴𝑌 = 𝑐𝑜𝑢𝑝𝑀𝐵𝑆−1 (64)

𝑐𝑜𝑢𝑝 = 𝑟𝑙𝑚 + 𝑠𝑝𝑟𝑒𝑎𝑑𝑀𝐵𝑆 (65)

Institutional investors

The institutional investors sector includes entities such as pension funds, mutual

funds, hedge funds, insurance companies, and investment banks (cf. Davis 2003).

They earn revenue from holding MBS and finance their operations by issuing

shares, which are purchased by rentiers. For simplicity, a constant price of

shares equal to $1 is assumed. Demand for MBS follows the portfolio principle

(eq.68), where the return on MBS (eq.69) depends on the yield (eq.70) and

capital gains on MBS (eq.71).

Institutional investors accumulate profits equal to the coupon payments

from SPVs/underwriters, which are entirely distributed to rentiers (eq.66).

Return on institutional investors’ shares is given as the ratio of their profits to

shares demanded by rentiers in the previous period (eq.67).

𝐹𝐼 = 𝐶𝑂𝑈𝑃𝐴𝑌 (66)

33

𝑟𝑠 =𝐹𝐼

𝑆𝐻−1 (67)

𝑝𝑀𝐵𝑆 =(𝜃10+𝜃11𝑟𝑀𝐵𝑆,−1)𝑆𝐻−1

𝑀𝐵𝑆 (68)

𝑟𝑀𝐵𝑆 = 𝑦𝑖𝑒𝑙𝑑𝑀𝐵𝑆 +𝐶𝐺𝑀𝐵𝑆

𝑝𝑀𝐵𝑆,−1𝑀𝐵𝑆−1 (69)

𝑦𝑖𝑒𝑙𝑑𝑀𝐵𝑆 =𝐶𝑂𝑈𝑃𝐴𝑌

𝑝𝑀𝐵𝑆,−1𝑀𝐵𝑆−1 (70)

𝐶𝐺𝑀𝐵𝑆 = 𝑀𝐵𝑆−1(𝑝𝑀𝐵𝑆 − 𝑝𝑀𝐵𝑆,−1) (71)

Simulations

The model is calibrated to the US economy (see Appendix). The main objective of

the simulation exercise is to examine the impact of the proposed model on

inequality patters. Specifically, we analyse how changes in household balance

sheet composition and leverage affect quantitative measures of income

inequality such as the Gini index (eq.72), the Atkinson index (with inequality

aversion parameter 𝜀=2 in eq.73) and the squared coefficient of variation

(eq.74). While the Gini and Atkinson indices range between 0 and 1, squared

coefficient of variation ranges from 0 to infinity. In all indices, higher value

indicates higher inequality level. This follows the benchmark exercise outlined in

Dafermos/Papatheodorou (2015) where the choice of these three inequality

measures is motivated by their different sensitivity to inequality in different

moments of the distribution (the middle, the bottom and the top of the

distribution respectively).

In addition, we calculate the Theil T index to capture wealth inequality

(eq.78). This is because the other measures of income inequality incorporated in

our model cannot be readily adapted to the distribution of wealth due to possible

negative net worth values (cf. Cowell 2009:72). Theil T index is a generalised

entropy measure of inequality, ranging between 0 and infinity, higher value

corresponding to a higher inequality level (World Bank 2005). To compare the

distributions of income and wealth in our model, we also compute the Theil T

index for income (eq.77).

𝐺𝐼𝑁𝐼 =1

2𝑁2𝜇∑ |𝑌𝐻𝑖 − 𝑌𝐻𝑗|𝑁𝑖𝑁𝑗𝑖,𝑗 where i,j = w, m, r (72)

34

𝐴𝜀=2 = 1 − [1

𝑁∑ 𝑁𝑖 (

𝑌𝐻𝑖

𝜇)

−1

𝑖 ]−1

where i,j = w, m, r (73)

𝐶2 =1

𝑁𝜇2∑ 𝑁𝑖(𝑌𝐻𝑖 − 𝜇)2

𝑖 where i,j = w, m, r (74)

𝜇 =∑ 𝑌𝐷𝑖𝑖

∑ 𝑁𝑖𝑖 where i,j = w, m, r (75)

𝑌𝐻𝑖 =𝑌𝐷𝑖

𝑁𝑖 where i,j = w, m, r (76)

𝑇ℎ𝑒𝑖𝑙𝑇𝑌 =∑

𝑌𝐻𝑖𝜇

ln(𝑌𝐻𝑖

𝜇)𝑖

𝑁𝑤+𝑁𝑚+𝑁𝑟 where i,j = w, m, r (77)

𝑇ℎ𝑒𝑖𝑙 𝑇 =∑

𝑉𝐻𝑖�̅�

ln(𝑉𝐻𝑖

�̅�)𝑖

𝑁𝑤+𝑁𝑚+𝑁𝑟 where i,j = w, m, r (78)

𝑉𝐻𝑖 =𝑉𝑖

𝑁𝑖 where i,j = w, m, r (79)

�̅� =∑ 𝑉𝑖𝑖

∑ 𝑁𝑖𝑖 where i,j = w, m, r (80)

It is expected that the balance sheet heterogeneity should produce more

acute long-run polarisation of income. This is because the inclusion of wealth in

the model creates forces which pull the upper class even further away from the

rest of the distribution, drowning the middle and working class in debt.

Consideration of the different types of debt, which is reflected in our distinction

between the working and the middle class, could also explain the middle class

meltdown in countries like USA and should reproduce the illusion of short-run

prosperity for the middle class in the run up to the crisis.

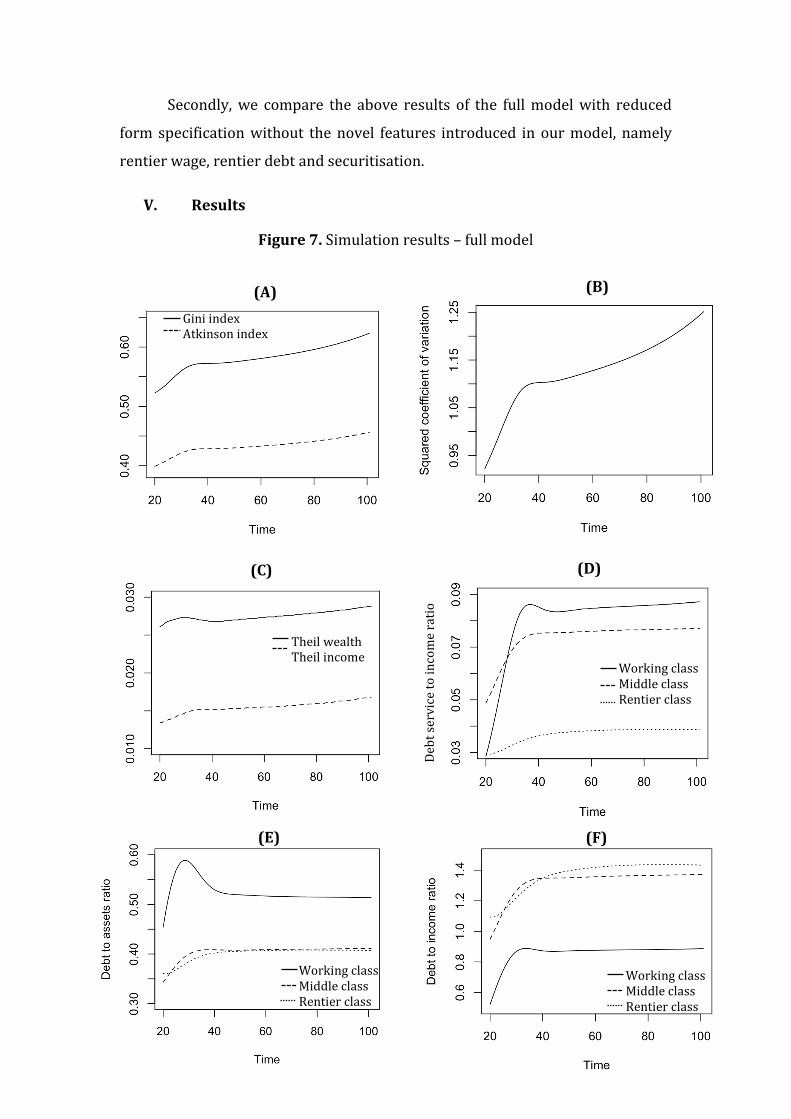

Firstly, a full model, which is outlined above, is simulated for 100 periods.

For clarity, simulation results are presented from period 20 onwards to allow for

adjustment of the system to a steady state. The steady state is defined as a

situation where all variables in the economy grow at the same rate, given by the

exogenous growth rate of capital gk. Results for the income Gini coefficient, the

Atkinson index and the squared coefficient of variation as well as for the Theil T

index for income and wealth are presented. Additionally, we report the three

measures of leverage for each household group.

35

Secondly, we compare the above results of the full model with reduced

form specification without the novel features introduced in our model, namely

rentier wage, rentier debt and securitisation.

V. Results

Figure 7. Simulation results – full model

Gini index Atkinson index

Working class Middle class Rentier class

Working class Middle class Rentier class

Working class Middle class Rentier class

Deb

t se

rvic

e to

inco

me

rati

o

(A) (B)

(C) (D)

(E) (F)

Theil wealth Theil income

36

Simulations of the model produce a consistent result of increasing

inequality according to all measures. The Gini index in the model tends towards

0.6, which is close to the actual 2006 value recorded in USA (see introduction).

The Atkinson index tends towards 0.45 and the squared coefficient variation

towards 1.25 (Fig.7, panels A and B). Furthermore, model results show that

wealth inequality is higher than income inequality, which reproduces the stylised

fact outlined in the introduction (panel C in fig.7). This is measured using Theil T

indices for both income and wealth to maintain comparability.

Interesting results follow from simulating various financial fragility

measures. Looking at the debt-to-asset ratio, the working class is the most

leveraged, with the ratio stabilising at 0.5 (panel E in fig.7). The ratio for the

middle and the rentier class reaches 0.4, with rentiers being slightly less

leveraged than the middle class. This is because of the presence of housing on the

asset side of the middle class balance sheet. However, although the ratio for

rentiers reaches similar values as the middle class, rentiers do not face the

negative consequences of large debt holdings as the middle and the working

class due to high returns to their assets and diverse income sources. This is best

highlighted by examination of the debt service to income ratio (panel D, fig.7).

This measure shows clearly that debt is the most burdensome for the working

class, as debt repayments in each period correspond to 8.7% of their income.

Similarly, despite lower debt-to-asset ratio of the middle class, their debt

repayment ratio of 0.077 puts them closer to the working class in terms of their

balance sheet fragility. Conversely, due to multiple income sources and large

high-yielding asset holdings rentiers debt service corresponds to only 3.8% of

their income in each period.

In contrast, an opposite picture emerges from the debt-to-income ratio

analysis (panel F, fig.7). By this measure, the working class is leveraged the least,

with the ratio reaching 0.87. The ratio for the middle class stabilises at 1.3 and

for rentiers at 1.4. This order is surprising and does not corresponds to the debt-

to-income ratios found in the household survey data. Hence, while our model

reproduces the empirical fact that debt of rentiers is large, it either understates

the demand for loans by the working and the middle class or it overstates their

37

income. This may be either because the part of the wage share accruing to the

working and the middle class is overstated in our model compared to the real

world or because the impact of securitisation on household indebtedness does

not generate enough supply and demand for debt among the lower and middle

income groups. Both of these explanations are related to the aggregate nature of

the SFCM method and the inability to decompose the imposed aggregated

structures. Consequently, in the context of our model it is important to examine

household financial fragility holistically, as each of the commonly used measures

provides different information on households’ capacity to handle financial

distress.

Secondly, we present the simulation results of a reduced form model to

highlight the importance of the novel features presented in our model for

analysing inequality. Fig.8 reports the simulation results of the model with a

“pure capitalist” class, i.e. it is assumed in line with the existing literature that

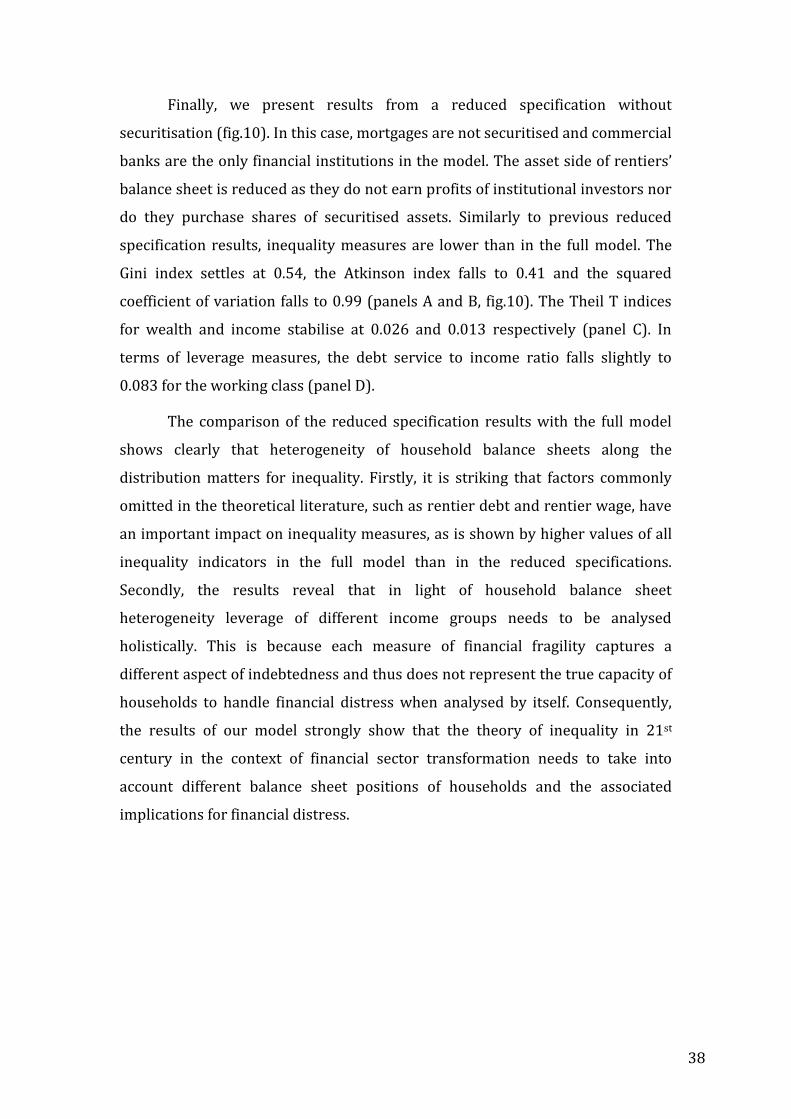

rentiers earn only capital income and no wages. In this case, the overall trends in

the indicators reported in the full model are replicated. However, all measures of

inequality are understated. The Gini index for income is lower at 0.5, the

Atkinson index decreases to 0.37 and the squared coefficient of variation falls to

0.8 (panels A and B, fig.8). Similarly, the reported Theil T indices are lower, with

values of 0.024 and 0.013 for wealth and income respectively (panel C). The

leverage indicators remain largely unchanged, although the debt-to-asset ratio of

the rentier class increases slightly to 0.4 (panel E).

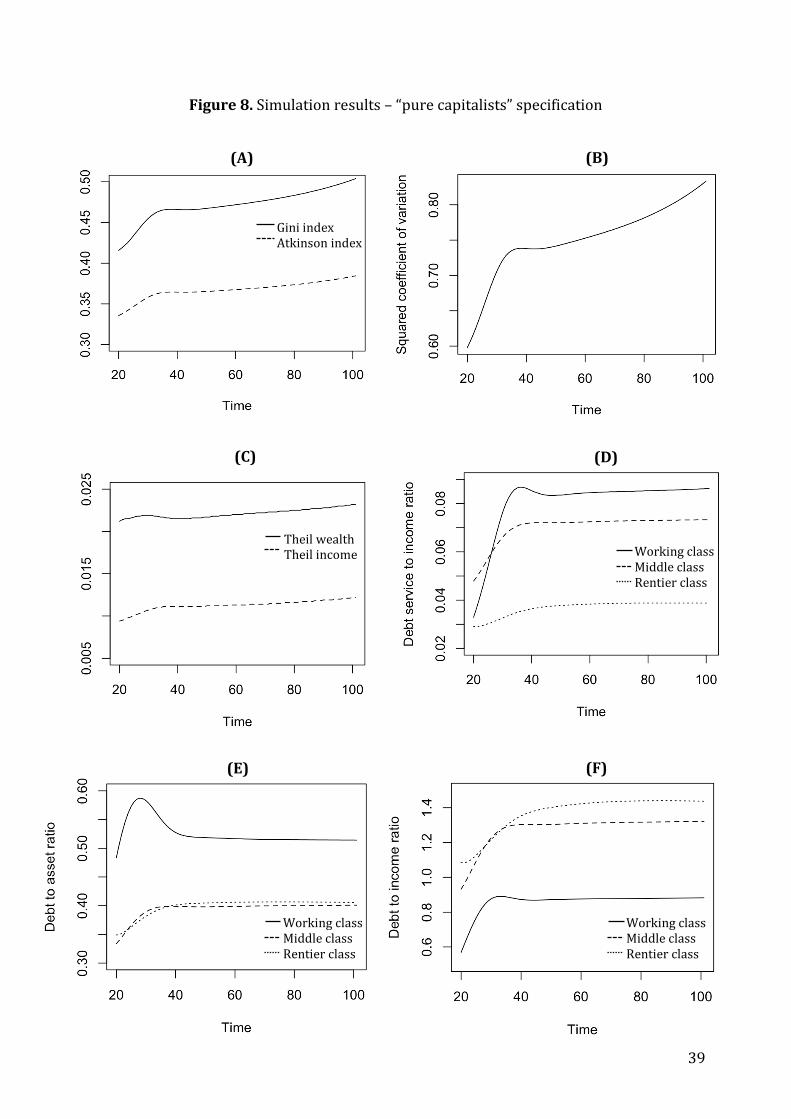

Similar results follow from a reduced form specification without neither

wage nor debt holdings for rentiers (fig.9). The Gini index and the Atkinson index

decrease to 0.5 and 0.38 respectively (panel A), while the squared coefficient of

variation falls to 0.85 (panel B). The values for the Theil indices for wealth and

income decrease to 0.028 and 0.016 respectively (panel C). Since no rentier debt

is considered, leverage ratios are only reported for the working and the middle

class. The values for both groups remain similar to the full specification, although

the debt service to income ratio for the middle class decreases slightly to 0.074

(panel D).

38

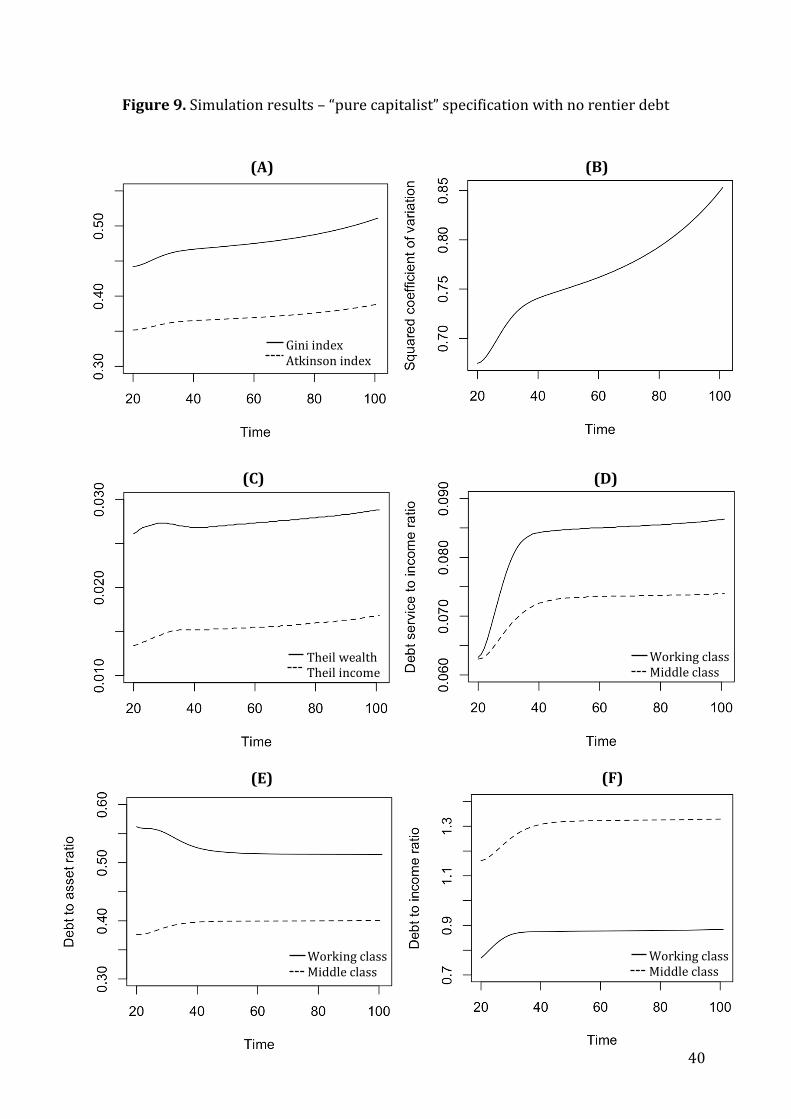

Finally, we present results from a reduced specification without

securitisation (fig.10). In this case, mortgages are not securitised and commercial

banks are the only financial institutions in the model. The asset side of rentiers’