inflation and economic growth projection of narodowy bank

TRANSCRIPT

Economic Analysis Department

Warsaw / 8th March 2021

Inflation and economic growth projection

of Narodowy Bank Polski

based on the NECMOD model

Outline:

Inflation and economic growth projection of the NBP

Pandemic: economic

fallout

Projection 2021 – 2023

▪ Economic conditions

abroad

▪ Polish economy

Uncertainty

2

1 Pandemic: economic fallout

2 Projection 2021 - 2023

3 Uncertainty

Outline

Outline:

Inflation and economic growth projection of the NBP

Pandemic: economic

fallout

Projection 2021 – 2023

▪ Economic conditions

abroad

▪ Polish economy

Uncertainty

3

Pandemic: economic fallout

Inflation and economic growth projection of the NBP 4

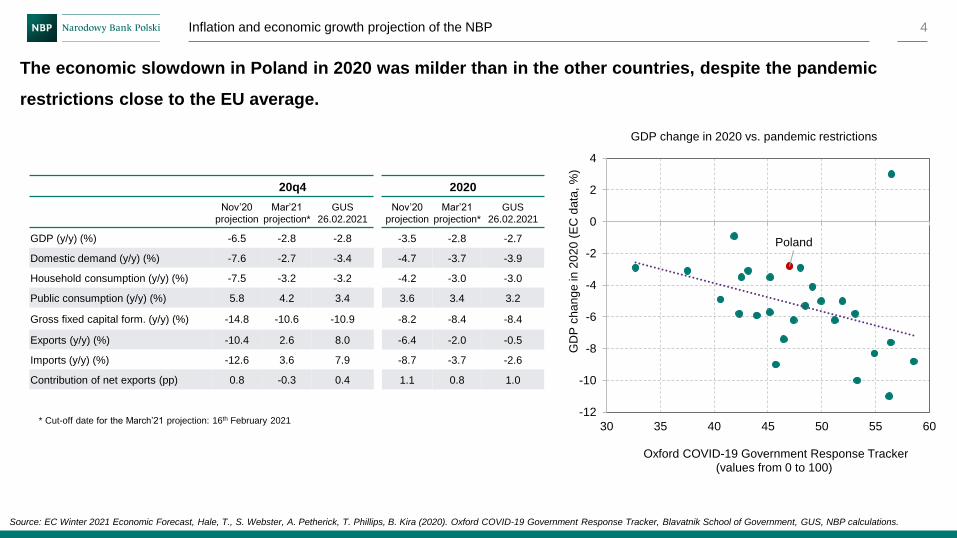

The economic slowdown in Poland in 2020 was milder than in the other countries, despite the pandemic

restrictions close to the EU average.

* Cut-off date for the March’21 projection: 16th February 2021

Source: EC Winter 2021 Economic Forecast, Hale, T., S. Webster, A. Petherick, T. Phillips, B. Kira (2020). Oxford COVID-19 Government Response Tracker, Blavatnik School of Government, GUS, NBP calculations.

Poland

-12

-10

-8

-6

-4

-2

0

2

4

30 35 40 45 50 55 60

GD

P c

ha

ng

ein

20

20

(E

C d

ata

, %

)

Oxford COVID-19 Government Response Tracker(values from 0 to 100)

GDP change in 2020 vs. pandemic restrictions

20q4

Nov’20

projection

Mar’21

projection*

GUS

26.02.2021

GDP (y/y) (%) -6.5 -2.8 -2.8

Domestic demand (y/y) (%) -7.6 -2.7 -3.4

Household consumption (y/y) (%) -7.5 -3.2 -3.2

Public consumption (y/y) (%) 5.8 4.2 3.4

Gross fixed capital form. (y/y) (%) -14.8 -10.6 -10.9

Exports (y/y) (%) -10.4 2.6 8.0

Imports (y/y) (%) -12.6 3.6 7.9

Contribution of net exports (pp) 0.8 -0.3 0.4

2020

Nov’20

projection

Mar’21

projection*

GUS

26.02.2021

-3.5 -2.8 -2.7

-4.7 -3.7 -3.9

-4.2 -3.0 -3.0

3.6 3.4 3.2

-8.2 -8.4 -8.4

-6.4 -2.0 -0.5

-8.7 -3.7 -2.6

1.1 0.8 1.0

Inflation and economic growth projection of the NBP

A favourable cyclical position and no significant imbalances at the onset of the pandemic.

5

Source: GUS, Eurostat.

0

5

10

15

20

25

0

2

4

6

8

10

GDP (y/y, %, LHS) LFS unemployment rate (%, RHS)

GDP and LFS unemployment rate

Selected macroeconomic data for 2019

GDP growth rate (y/y) 4.5%

LFS unemployment rate 3.3%

General government balance -0.7% PKB

General government debt (ESA2010) 45.7 % PKB

Current and capital account balance 2.5% PKB

Inflation and economic growth projection of the NBP

Favourable sectoral structure of the economy.

6

Source: EC Winter 2021 Economic Forecast, Eurostat, NBP calculations.

GDP change in 2020 vs. share of the sectors most affected by pandemic in GVA

Poland

-12

-10

-8

-6

-4

-2

0

2

4

0 5 10 15 20 25

GD

P c

hange

in 2

020 (

EC

data

, %

)

Section share: accommodation and food service activities (I), administrative and support service activities (N), arts,

entertainment and recreation (R) and other service activities (S) in gross value added (2019 data)

Inflation and economic growth projection of the NBP

Relatively fast adaptation of economic agents to functioning during a pandemic.

7

Source: GUS, S. Webster, A. Petherick, T. Phillips, B. Kira (2020). Oxford COVID-19 Government Response Tracker, Blavatnik School of Government, NBP calculations.

*Oxford COVID-19 Government Response Tracker – monthly averages

Industrial production and retail sales vs. pandemic restrictions in Poland*

-30

-25

-20

-15

-10

-5

0

5

10

15

0

10

20

30

40

50

60

70

80

90

20m1 20m2 20m3 20m4 20m5 20m6 20m7 20m8 20m9 20m10 20m11 20m12 21m1

Oxford COVID-19 Government Response Tracker (values from 0 to 100, monthly averages, LHS)

Industrial production (%, y/y, RHS)

Retail sales (y/y, %, RHS)

Inflation and economic growth projection of the NBP

Favourable geographic and product structure of Polish exports.

8

Source: GUS, Eurostat, World Input Output Database, NBP calculations.

▪ Consumption-oriented exports.

Share of consumption and investment final demand

in exported value added in 2014 (%)Share of geographic markets in export (%, 2014)

▪ Strong trade ties with the German economy, which coped with the

crisis better than a large part of the EU economies.

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

consumption

investment

0

5

10

15

20

25

0

5

10

15

20

25

Gross export Final demand

Inflation and economic growth projection of the NBP

Effective policy mix .

9

Source: NBP estimates based on regulatory impact assessment and ZUS, MRPiPS, MRPiT, PFR data, NBP.

▪ Prompt and considerable fiscal response to the crisis, supported by interest rate cuts and unconventional monetary policy measures.

Anti-crisis measures

- non-repayable support financed from the national sources (PLN billion) NBP interest rates and the POLONIA rate (%)

0 10 20 30 40 50

Other (incl. Polish Tourist Voucher)

Loans from Polish Development Fund for largeenterprises (non-repayable component)

Child care allowance

Work suspension benefits

Advances to micro-enterprises (5000 PLN)

Exemption from social security contributions

Wage subsidies

Loans from Polish Development Fund forMSMEs (non-repayable component)

2020 2021 - estimates under the assumption of the support being extended until February

0,0

0,5

1,0

1,5

2,0

2,5

3,0

0,0

0,5

1,0

1,5

2,0

2,5

3,0

17m1 17m7 18m1 18m7 19m1 19m7 20m1 20m7 21m1

Deposit rate Reference rate Lombard rate POLONIA

Inflation and economic growth projection of the NBP

Acceleration of economic activity due to the loosening of some epidemic restrictions in February this year.

10

Source: PSE, IMiGW, meteomodel.pl, GDKiA, Google LLC, Google LLC, "Google COVID-19 Community Mobility Reports., Shopper Trak Index Polska, NBP calculations.

Annual change in electricity consumption (Mon-Fri 8 am-4 pm,%)

Values corrected for weather

and calendar factors

Changes in population traffic in shopping centers

(monthly data, Feb 2021: weekly, y/y,%)

-12

-10

-8

-6

-4

-2

0

2

4

20m2 20m4 20m6 20m8 20m10 20m12 21m2

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

10

Weekly data for

Feb 2021

Change in vehicle traffic on national roads and motorways

(%, average for a given week, March 2-8, 2020 = 100)

50

60

70

80

90

100

110

120

50

60

70

80

90

100

110

120

20m3 20m5 20m7 20m9 20m11 21m1

Cars Tracks

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

20m3 20m4 20m5 20m6 20m7 20m8 20m9 20m10 20m11 20m12 21m1 21m2

Retail & recreation Grocery & pharmacyTransit stations WorkplacesResidential

Change in population traffic in selected locations compared to

pre-lockdown value (March 4-10, 2020 = 100)

Outline:

Inflation and economic growth projection of the NBP

Pandemic: economic

fallout

Projection 2021 – 2023

▪ Economic conditions

abroad

▪ Polish economy

Uncertainty

11

Projection 2021-2023

Economic conditions abroad

Inflation and economic growth projection of the NBP 12

Regionally diversified economic recovery in 2021 after the pandemic.

Source: Bloomberg, CBP Netherlands, OECD, NBP calculations.

GDP forecast in the selected economies

Factors determining the forecast of economic growth:

Companies and households adapting to functioning in the

pandemic.

Launching the vaccination process - limiting the spread of the

pandemic and bringing closer the prospects of lifting the restrictions.

Large fiscal packages in the major world economies.

Poor growth prospects for emerging economies.

Brexit.

World commodity trade (100 and t=0 respectively Aug 2008 and Dec 2019)

GDP y/y, % 2020 2021 2022 2023

Euro area -6.8 (-7.5) 3.9 (3.2) 3.9 (4.0) 2.0

Germany -5.3 (-5.9) 3.1 (3.4) 4.3 (3.7) 1.5

United Kingdom -9.9 (-10.4) 3.6 (4.2) 5.5 (4.5) 2.0

USA -3.5 (-3.8) 4.6 (3.3) 3.2 (2.3) 1.9

China 2.3 (1.7) 8.0 (7.7) 5.5 (5.5) 5.4

75

80

85

90

95

100

105

75

80

85

90

95

100

105

0 2 4 6 8 10 12 14 16 18 20 22 24

months

COVID-19 pandemic World financial crisis

Inflation and economic growth projection of the NBP 13

Source: Eurostat, IHS Markit, NBP calculations.

GDP in the euro area (% i pp., y/y)GDP in the euro area and individual countries

(%, 2020Q4 vs. 2019Q4, * - 2020Q3 data)

Disposable income per capita (%, q/q, 4-day average), saving rate (%)

in the euro area

Euro area: return to growth path from 2021 Q2 supported by fiscal stimulus.

PMI for the euro area – manufacturing and services

-8

-6

-4

-2

0

2

4

6

-8

-6

-4

-2

0

2

4

6

2020 F 2021 F 2022 F 2023 F

Private consumption

Public consumption

Investment

Net exports

Change in inventories

GDP-14

-12

-10

-8

-6

-4

-2

0

2

4

6

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

EL

*

MT

*

ES

AT IT PT

FR

BE

CY

DE

SI*

EE

*

NL

SK FI

LV

LT

LU

*

IE*

Euro area average

10

20

30

40

50

60

70

10

20

30

40

50

60

70

18m2 18m5 18m8 18m11 19m2 19m5 19m8 19m11 20m2 20m5 20m8 20m11 21m2

Manufacturing Services4

8

12

16

20

24

28

-9

-6

-3

0

3

6

9

4q 19 1q 20 2q 20 3q 20

Wages Operating surplus and mixed income

Net Social contributions and benefits Property income and other current transfers

Current taxes on income, wealth, etc. Disposable income per capita

Savings rate (RHS)

Inflation and economic growth projection of the NBP 14

The United States: economic recovery constrained by protracted pandemic, but supported by fiscal policy.

Source: BAE, BLS, NBP calculations.

Real GDP in the USA (%, pp., y/y)

Deviation of selected components of GDP from the 2019 Q4 level (%)

Real GDP in the USA

(%, y/y, recessions according to the NBER are marked in gray)

Unemployed for at least 27 weeks as % of the labor force

(pp. change in respect to the peak of economic activity)

-4

-2

0

2

4

6

-4

-2

0

2

4

6

2020 P 2021 P 2022 P 2023 P

Private consumption Private investment Change in inventories

Net exports Public consumption GDP

-16

-12

-8

-4

0

4

8

12

16

-16

-12

-8

-4

0

4

8

12

16

2019Q4 2020Q1 2020Q2 2020Q3 2020Q4

Consumption of goods Consumption of services

Business investment Housing investment

-1

0

1

2

3

4

-1

0

1

2

3

4

t t+3 t+6 t+9 t+12 t+15 t+18 t+21 t+24 t+27 t+30

Months after the peak of economic actiivity

t = Mar 2001 t = Feb 2020 t = Dec 2007

-15

-10

-5

0

5

10

15

20

25

1930 1940 1950 1960 1970 1980 1990 2000 2010 2020

Outline:

Inflation and economic growth projection of the NBP

Pandemic: economic

fallout

Projection 2021 – 2023

▪ Economic conditions

abroad

▪ Polish economy

Uncertainty

15

Projection 2021-2023

Polish economy

Inflation and economic growth projection of the NBP 16

Source: GUS, ZUS, MRPiT, NBP calculations.

Partial recovery of labour demand in the second half of 2020. Limited growth of the unemployment

rate, owing to the anti-crisis measures.

Number of employed persons and average employment in enterprise

sector and hours worked in the economy according to LFS (y/y, %)Number of job offers declared during a month (in thous., sa)

20q3: 3.2%

21m1: 6.1%

0

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14

2011 2013 2015 2017 2019 2021 2023

LFS unemployment rate (from 20q4 forecast)

Registered unemployment rate

Registered and LFS unemployment rates (sa, %) Number of employees benefiting from the Anti-crisis Shield

by type of measure (average stock, ths.)

0

500

1 000

1 500

2 000

2 500

3 000

20m4 20m5 20m6 20m7 20m8 20m9 20m10 20m11 20m12 21m1

employees' wage subsidies - European Social Fund

stoppage benefits

employees' wage subsidies - Guaranteed EmployeeBenefits Fund

-8,9

-0.3

-2.0

-1.8

-10

-8

-6

-4

-2

0

2

4

6

-10

-8

-6

-4

-2

0

2

4

6

16m1 16m7 17m1 17m7 18m1 18m7 19m1 19m7 20m1 20m7 21m1

Hours worked in the economy according to LFS (y/y)

Av. employment in enterprise sector

No. of employed persons in enterprise sector 0

20

40

60

80

100

120

140

160

18m1 18m7 19m1 19m7 20m1 20m7 21m1

Job offers excl. subsidised offers Subsidised job offers

Note: Data from labor offices for the last month, due to the date of data availability, refer to offers in general.

Inflation and economic growth projection of the NBP 17

Source: GUS, MRPiT, ZUS, NBP calculations.

Incomplete recovery of labour supply.

Causes of inactivity (thousands) Changes in the number of foreigners insured in ZUS and the number of issued

documents entitling to legal work in Poland (annual changes, in thous.)

Effective numer of foreign workers in Poland (thous.)

55

56

57

-3,0

-2,5

-2,0

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

14q1 15q1 16q1 17q1 18q1 19q1 20q1 21q1 22q1 23q1 23q4

Employment (y/y, %)

Participation rate (%, RHS)

Employment and participation rate forecast

-600

-400

-200

0

200

400

-600

-400

-200

0

200

400

18q1 18q3 19q1 19q3 20q1 20q3 21q1 21q3 22q1 22q3 23q1 23q3

Discouraged Education Family Retirement

Health Other Inactive

0

500

1 000

1 500

0

500

1 000

1 500

2006 2008 2010 2012 2014 2016 2018 2020 2022

Th

ousands

Effective no. of foreign workers excl. UA and BY

Effective no. of Belarussian workers in Poland

Effective no. of Ukrainian workers in Poland

Effective no. of foreign workers in Poland

-150

-100

-50

0

50

100

20m1 20m6 20m12 20m1 20m6 20m12

foreigners of citizenshipother than Ukrainian

declarations onentrusting work to a foreigner

Ukrainians seasonal work permits

foreigners insured in ZUS issued documents entitling to legal work

in Poland

Inflation and economic growth projection of the NBP 18

Annual wage growth (in%, y/y, latest data from the GN for 2020Q4, from the

enterprise sector for January 2021)

A gradual recovery in labour demand amid a low unemployment rate will lead to wage growth.

Minimum wage in Poland (PLN) and its ratio to mean wage in the economy (%)

Source: GUS, Szybki Monitoring NBP, NBP calculations.

Share of enterprises declaring wage pressure (%)

-8

-4

0

4

8

12

-8

-4

0

4

8

12

14q1 15q1 16q1 17q1 18q1 19q1 20q1 21q1 22q1 23q1 23q4

Nominal wages (y/y, %)

Real wages (y/y, %)

Labour productivity (y/y, %)

ULC (y/y, %)

Wages and ULC forecast (y/y, %)

0

10

20

30

40

50

60

0

500

1 000

1 500

2 000

2 500

3 000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Minimum wage

Minimum wage to mean wage in the economy (RHS)

20q4: 5.0%

21m1: 4.8%

0

2

4

6

8

10

0

2

4

6

8

10

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Nominal wages in national economy (from21q1 forecast)

Nominal wages in enterprise sector

0

10

20

30

40

50

60

70

80

0

10

20

30

40

50

60

70

80

15q4 16q4 17q4 18q4 19q4 20q4

Existence of wage pressure Intensification of wage pressure

Inflation and economic growth projection of the NBP 19

Consumer sentiment driven by the development of the pandemic and the scale of the related restrictions.

Source: GUS, Hale, T., S. Webster, A. Petherick, T. Phillips, B. Kira (2020). Oxford COVID-19

Government Response Tracker, Blavatnik School of Government, NBP calculations.

Financial situation of households and fear of being unemployed

Consumer confidence indicators vs. pandemic restrictions

(Oxford COVID-19 Government Responce Tracker – monthly averages)

-6

-4

-2

0

2

4

6

8

10

-6

-4

-2

0

2

4

6

8

10

20q1 21q1 22q1 23q1 23q4

Net transfers and taxes excl. 500 plus500 plusWage fundProperty incomeOperating surplusDisposable income (y/y, %)

Decomposition of disposible income (constant prices) (y/y, %)

-40

-20

0

20

40

60

80

100

-40

-20

0

20

40

60

80

100

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Current financial situation of households

Financial situation of households in the next 12 months

Fear of being unemployed

-20

-10

0

10

20

30

40

50

60

70

80

90-90

-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

2015 2016 2017 2018 2019 2020 2021

Oxford COVID-19 Government Response Tracker(monthly averages, RHS)

Consumer confidence indicator - current (BWUK, sa)

Consumer confidence indicator - leading (WWUK, sa)

Inflation and economic growth projection of the NBP 20

Expected increase in consumption demand along with the improvement of the epidemic situation

and lifting the restrictions.

Source: GUS, NBP calculations.

Retail sales (%)

-5

0

5

10

15

20

25

-5

0

5

10

15

20

25

14q1 15q1 16q1 17q1 18q1 19q1 20q1 21q1 22q1 23q1 23q4

Households saving rate forecast (%, sa)

-25

-20

-15

-10

-5

0

5

10

15

20

-25

-20

-15

-10

-5

0

5

10

15

20

19m1 19m7 20m1 20m7 21m1

m/m sa y/y

Inflation and economic growth projection of the NBP 21

Private consumption:

Worsening of the epidemic situation in the autumn and winter period:

▪ imposed restrictions

▪ changes in the behaviour of the population for fear of

contracting the coronavirus

▪ a precautionary motive resulting from high uncertainty.

Gradual lifting of epidemic restrictions.

High level of savings accumulated during the pandemic (due to low

propensity to consume and anti-crisis fiscal support).

Public consumption:

Increase in health care expenditure related to the pandemic

(2020: costs of treatment and purchase of protective measures, 2021:

purchase of vaccines)

The decrease in expenditure on public services in 2020, due to the

pandemic restrictions in force, followed by the increase in 2021.

Travel vouchers (strongest impact in 2021).

Freeze of salaries in the public administration in 2021.

Return to neutral fiscal policy towards the end of the projection

horizon.

Private consumption growth accelerates over the longer projection horizon.

y/y, % 2020 2021 2022 2023

Household

consumption-3.0 4.9 6.3 5.8

Public consumption 3.4 4.4 3.7 4.9

Source: GUS, NBP calculations.

Consumption forecast

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

14

14q1 15q1 16q1 17q1 18q1 19q1 20q1 21q1 22q1 23q1 23q4

Household consumption (y/y, %)

Public consumption (y/y, %)

Inflation and economic growth projection of the NBP

38.3 5.6 6.4 16.4 18.1 11.3 3.80

5

10

15

20

25

30

35

40

45

now up to 3 months 4-6 months 6-12 months 12-24 months in more than24 months

never

% o

f com

panie

s w

ith s

pecifie

d

pla

ns

full sample (weighted with employment)

22

Improving sentiments, especially among large and public enterprises. However, persistent high uncertainty.

Still low investment activity in 2021.

Share of enterprises assessing uncertainty as high and indicating

uncertainty as a barrier to development (%, sa)

Contribution to investment growth of the 100 largest investors

(y/y, pp, quarterly data)

Source: GUS, SM NBP (January 2021).

0

2

4

6

8

10

5

8

11

14

17

20

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

high uncertainty rating (LHS) uncertainty barrier

-20

-10

0

10

20

30

40

2008 2010 2012 2014 2016 2018 2020

100 largest investors others

Quarterly index of new investments and index of continuation of

commenced investments (% of companies)

70

75

80

85

90

95

100

15

20

25

30

35

40

45

2001 2004 2007 2010 2013 2016 2019

Quarterly index of new investments

Index of continuation of commencedinvestments

The prospect of investment returning to pre-pandemic levels (% of companies)

29.2

5.9

3.317.0

9.35.1

3.5

Not specified;

26.7

Inflation and economic growth projection of the NBP 23

Contributions to public investment growth

(current prices, y/y, %)

Grants under the Next Generation EU instrument will significantly change the dynamics of EU funds

absorption in the coming years.

Source: GUS, Eurostat, MF, MFiPR, NBP calculations. All values are presented in nominal terms.

EU funds absorption (PLN billion) The use of EU funds for public investments (PLN billion)

* - NBP estimates

F – NBP forecast

▪ As a part of the new instrument, grants of approx. EUR 30 billion are provided to Poland, of which EUR 23.9 billion are payments under the

Recovery and Resilience Facility that will be distributed and settled based on the National Recovery and Resilience Plan (which is to be submitted to

the European Commission by the end of April this year). The remaining part of the grants will be included in the traditional cohesion policy funds.

▪ The projection is based on a cautious assumption that the loan component of NGEU (the allocation for Poland amounts to approx. EUR 34 billion)

will not increase total investment outlays – these repayable funds will only be used to finance those expenditures which would have been incurred

anyway (substituting for other forms of financing of the government borrowing requirement).

-30

-20

-10

0

10

20

30

40

-30

-20

-10

0

10

20

30

40

2013

2014

2015

2016

2017

2018

2019

2020*

2021P

2022P

2023P

Contribution of other entitites

Contribution of Local Government

Public investment (current prices)

0

10

20

30

40

50

60

70

80

90

IXIII* IX III IX III III

2018 2019 2020 2021 F 2022 F 2023 F

Funds allocated to agriculture

Recovery and Resilience Facility (within the NGEU)

Cohesion policy funds

0

5

10

15

20

25

30

35

IX III* IX III IX III III

2018 2019 2020 2021 F 2022 F 2023 F

Anti-crisis funds

Recovery and Resilience Facility (within the NGEU)

Inflation and economic growth projection of the NBP 24

Private investment:

Pandemic restrictions curbing the activities of certain industries,

persistent high uncertainty and the related reluctance to incur long-

term financial obligations.

Gradual lifting of epidemic restrictions.

Low degree of automation and robotization of the Polish industry and

rising labour costs.

Relatively high housing demand, supported by the expected

improvement in the labour market situation, the elevated level of some

households’ savings and a record low level of interest rates.

Absorption of the EU funds from the Next Generation UE instrument.

General government investment:

Decline in funds from the 2014-2020 EU perspective, which, according

to the n + 3 rule, ends in 2023.

Absorption of the funds under the Next Generation EU instrument.

Beginning of the new EU perspective – it is assumed that the

absorption of the funds from 2021-2027 perspective will start in 2023.

Gradual return of gross fixed capital formation to pre-crisis values.

Source: GUS, NBP calculations.

y/y, % 2020 2021 2022 2023

Gross fixed capital formation -8.4 1.5 7.7 9.9

Investment dynamics and its decomposition (y/y %)

-15

-10

-5

0

5

10

15

-15

-10

-5

0

5

10

15

20q1 21q1 22q1 23q1 23q4

Private sector

General government sector

Gross fixed capital formation

Inflation and economic growth projection of the NBP 25

Recovery of exports in the second half of 2020, after a strong slump in foreign trade - possible, inter alia, due

to the favourable structure of Polish exports.

Exports of goods and services in Q2 and Q3 2020 (volume, %, y / y)Dynamics of Polish exports of goods (current prices,% and percentage points, y / y)

Dynamics of Polish exports of goods (current prices,% and percentage points, y / y)

Source: Eurostat, WIOD, NBP calculations.

-30

-25

-20

-15

-10

-5

0

5

-30

-25

-20

-15

-10

-5

0

5

Q2 Q3 Q2 Q3 Q2 Q3 Q2 Q3 Q2 Q3

Poland Czech Rep. Hungary Slovakia Germany

Goods Services Total

-30

-20

-10

0

10

20

-30

-20

-10

0

10

20

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12

2019 2020

Germany CEE-3 Others from the EU

Outside the EU Total export of goods

-30

-20

-10

0

10

20

-30

-20

-10

0

10

20

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12

2019 2020

Food and consumption goods Means of transport

Supply goods for industry Investment goods

Fuels and other goods Total export of goods

0,00

0,04

0,08

0,12

0,16

0,20

HR

LV IT LT

NL

PL

BG

EE

FR

AT

PT

ES

SE

BE FI

DK

DE

LU

HU SI

RO

CZ

GR

MT

SK IE CY

* A lower value means a greater diversification of the product structure of exports.

Export Product Concentration Index *, 2019

Inflation and economic growth projection of the NBP 26

Source: GUS, WIOD, NBP calculations.

Due to anti-cyclical nature of net exports, its contribution to GDP growth will decrease and become

negative in the projection horizon.

y/y, pp 2020 2021 2022 2023

Net exports

contribution to growth0.8 -0.2 -1.6 -0.9

Net exports contribution to GDP growth Current and capital account (% GDP)

-6

-4

-2

0

2

4

6

8

10

-6

-4

-2

0

2

4

6

8

10

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Compensation of employees & remittances

Primary income (excl. compensation of employees)

Capital account & secondary income (excl. remittances)

Goods and services

Current and capital account (% GDP)

-4

-3

-2

-1

0

1

2

3

4

5

6

-20

-15

-10

-5

0

5

10

15

20

25

30

14q1 15q1 16q1 17q1 18q1 19q1 20q1 21q1 22q1 23q123q4

Net exports contribution (pp., RHS)

Exports (y/y, %, LHS)

Imports (y/y, %, LHS)

Inflation and economic growth projection of the NBP 27

The economy will gradually return to its pre-pandemic long-term growth path over the projection horizon.

From 2021 Q2, a sustained economic recovery,

conditional on the normalization of the epidemic situation,

recovery of activity abroad and an improvement in the

outlook for private demand.

Private consumption growth will accelerate over the

longer horizon of the projection, due to gradual lifting of

epidemic restrictions and a relatively high level of savings

accumulated by households during the pandemic.

In 2021, the recovery of investments will continue to be

hampered by restrictions, increased uncertainty and

reluctance to incur long-term financial obligations. In the

following years, the corporate investment rate will increase.

The contribution of net exports to GDP growth will

decline below zero in line with its countercyclical nature

over the projection horizon.

y/y, % 2020 2021 2022 2023

GDP -2.8 4.1 5.4 5.4

Źródło: dane GUS, obliczenia NBP

GDP dynamics and decomposition (y/y, %, pp)

-12

-9

-6

-3

0

3

6

9

12

-12

-9

-6

-3

0

3

6

9

12

20q1 21q1 22q1 23q1 23q4

Private consumption Public consumption

Gross capital formation Net exports

GDP

Inflation and economic growth projection of the NBP 28

March projection of GDP compared to the November projection

Source: GUS, NBP calculations

Weaker than expected negative impact of the pandemic on the

economy and the labour market at the turn of 2020-2021.

Faster than expected economic recovery abroad.

Launching new anti-crisis programs in Poland to support the

labour market and entrepreneurs in 2021.

Absorption of EU funds under the new EU Next Generation

instrument included in the projection.

GDP y/y, % 2020 2021 2022

November 2020 -3.5 3.1 5.7

March 2021 -2.8 4.1 5.4

pp

-1,0

-0,5

0,0

0,5

1,0

1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2020 2021 2022

Private consumption Public consumption

Gross capital formation Net exports

GDP

85

90

95

100

105

110

115

85

90

95

100

105

110

115

19q4 20q2 20q4 21q2 21q4 22q2 22q4

90% 60% 30%

Nov 20 Mar 21

GDP level (2019Q4 =100, sa)

Decomposition of changes in GDP dynamics (y/y, pp)

Inflation and economic growth projection of the NBP 29

In 2020 Q4, the decline in inflation resulted from a lower growth in the prices of food and non-alcoholic

beverages, due to the favorable supply situation.

Source: NBP, GUS, NBP calculations.

CPI decomposition (y/y, pp, monthly data)

Values from the November projection are given in brackets (seasonally adjusted).

Indicators with values higher than in the November projection are marked green,

whereas indicators with lower values are marked red.

CPI and core inflation (y/y, % monthly data)

2.7

3.8

-4

-2

0

2

4

6

-4

-2

0

2

4

6

2015 2016 2017 2018 2019 2020 2021

CPI

Inflation target

Inflation excl. administered prices

Inflaion excl. food and energy prices-3

-2

-1

0

1

2

3

4

5

-3

-2

-1

0

1

2

3

4

5

2015 2016 2017 2018 2019 2020 2021

Energy Fuels

Services Non-food goods

Food and non-alcoholic beverages CPI

y/y, % 20q3 20q4

CPI inflation 3.0 2.8 (2.9)

Core inflation 4.2 4.1 (4.2)

Food prices 3.2 1.7 (2.0)

Energy prices -1.6 -0.1 (-0.4)

Note: Data for January 2021: CPI, preliminary GUS data, CPI inflation excluding food

and energy prices - NBP estimate based on preliminary GUS data.

0,20.21.01.2

3.2

3.63.64.3

6.06.5

7.240.0

46.9

0 5 10 15 20 25 30 35 40 45 50

CommunicationsHousing, water, electricity, gas and other fuels

Transport

Miscellaneous goods and servicesEducation

Food and non-alcoholic beveragesFurnishings and household goods

Clothing and footwearHealth

Alcoholic beverages and tobaccoRecreation and culture

Restaurants and hotels

The total share of imputations in

December 2020: approx. 8%.

Share of imputations by 12 main COICOP groups (%) in December 2020

Inflation and economic growth projection of the NBP 30

CPI inflation excluding food and energy prices (y/y, %, monthly data)

Decomposition of core inflation (y/y, pp, monthly data)Decomposition of core inflation - contributions

(y/y, pp)

Dynamics of core inflation and its components

(y/y, %)

Core inflation in 2020 Q4 driven by lower prices of non-food goods amid high growth in prices of services.

Source: NBP. GUS, NBP calculations.

y/y, % 20q1 20q2 20q3 20q4

Core inflation 3.4 3.8 4.2 4.1

Excise goods 3.6 4.6 4.7 4.5

Other goods 0.5 0.3 1.1 0.8

Administered services 13.9 15.1 14.8 15.0

Market services 4.7 5.2 5.3 5.4

y/y, % 20q1 20q2 20q3 20q4

Core inflation 3.4 3.8 4.2 4.1

Excise goods 0.4 0.5 0.5 0.5

Other goods 0.2 0.1 0.5 0.3

Administered services 1.1 1.2 1.2 1.3

Market services 1.7 1.9 2.0 2.0

-2

0

2

4

6

8

10

12

14

16

-2

0

2

4

6

8

10

12

14

16

2015 2016 2017 2018 2019 2020

Core inflation

Market services

Non-food goods

Administered services

-1

0

1

2

3

4

5

-1

0

1

2

3

4

5

2015 2016 2017 2018 2019 2020

Excise goodsOther goodsClothing and footwearAdministered servicesMarket services

Inflation and economic growth projection of the NBP 31

Increase in commodity prices at the end of 2020. In the forecast horizon: a gradual increase in demand for

crude oil counterbalanced by the expected supply-side adjustments.

Source: GUS, Bloomberg, Reuters, EIA, NBP calculations.

Global oil production, consumption and change in stocks (milion b/d)

Market crude oil inventories in the US (milion b/d)

Energy commodities’ prices index (USD, 2011=1)

and crude oil prices (USD/b) in the projection

Changes in consumption of crude oil and liquid fuels worldwide

(annual changes, mln b/d)

20

40

60

80

100

120

0,2

0,4

0,6

0,8

1,0

1,2

14q1 15q1 16q1 17q1 18q1 19q1 20q1 21q1 22q1 23q1 23q4

Energy Index (LHS) Brent oil (RHS)

-6

-3

0

3

6

9

80

85

90

95

100

105

2015 2016 2017 2018 2019 2020 2021 2022

Global change in stocks (implied, annual, million b/d)

Global oil production (million b/d)

Global oil consumption (million b/d) -4

-3

-2

-1

0

1

2

2019 2020 2021 2022

China

USA

India

Middle East

Other OECD

Other non-OECD

300

350

400

450

500

550

600

300

350

400

450

500

550

600

2015 2016 2017 2018 2019 2020 2021 2022

Inflation and economic growth projection of the NBP 32

The decline in demand observed in 2020 impacts price growth with a delay. In the following years

inflation will be driven by the recovery of domestic and foreign demand.

Source: GUS, NBP calculations.

-2

-1

0

1

2

3

4

5

6

-2

-1

0

1

2

3

4

5

6

TFP CapitalNAWRU Economically active pop.Potential output (y/y, %)

-8

-4

0

4

8

12

-8

-4

0

4

8

12

14q1 15q1 16q1 17q1 18q1 19q1 20q1 21q1 22q1 23q1 23q4

Nominal wages (y/y, %) Labour productivity (y/y, %)

ULC (y/y, %)

-6

-4

-2

0

2

4

6

-6

-4

-2

0

2

4

6

14q1 15q1 16q1 17q1 18q1 19q1 20q1 21q1 22q1 23q1 23q4

Import prices excl. oil and gas prices (y/y, %)Import prices (y/y, %)

-9

-6

-3

0

3

6

9

12

-9

-6

-3

0

3

6

9

12

14q1 15q1 16q1 17q1 18q1 19q1 20q1 21q1 22q1 23q1 23q4

Output gap (% of potential output)

GDP (y/y, %)

Potential output (y/y, %)

Inflation and economic growth projection of the NBP 33

Source: GUS, NBP calculations.

Throughout the projection horizon, CPI inflation will remain within the range for deviations from the NBP

inflation target set at 2.5% +/- 1 percentage point.

Fall in demand in 2020 affecting prices with a delay; in

subsequent years inflation driven by the recovery of domestic

and foreign demand.

Slow growth of unit labour costs, and its acceleration in the

longer projection horizon.

Increase in energy commodity prices in the world markets at

the end of 2020; their stabilisation in the following years.

Increase in electricity prices for households from January

2021, due to the increase in prices of CO2 emission

allowances, wholesale prices on the Polish Power Exchange

and the introduction of the capacity charge.

Introduction of the sugar levy in January 2021.

High harvest of vegetables and fruits in 2020.

Further spread of the ASF epidemic (among others in Poland

and Germany) - an increase in the supply of pork in Poland in

2021.

The waning impact of the so-called „Covid fees".

y/y, % 2020 2021 2022 2023

CPI inflation 3.4 3.1 2.8 3.2

-2

-1

0

1

2

3

4

5

-2

-1

0

1

2

3

4

5

14q1 15q1 16q1 17q1 18q1 19q1 20q1 21q1 22q1 23q1 23q4

Core inflation Food prices

Energy prices CPI inflation%, pp

Inflation and economic growth projection of the NBP 34

March CPI projection compared to the November projection

Source: GUS, NBP calculations.

CPI y/y, % 2020 2021 2022

November 2020 3.4 2.6 2.7

March 2021 3.4 3.1 2.8

pp

y/y, %

-0,4

-0,2

0,0

0,2

0,4

0,6

2020 2021 2022

-0,4

-0,2

0,0

0,2

0,4

0,6

Core inflation Food prices

Energy prices CPI inflation

-1

0

1

2

3

4

5

6

-1

0

1

2

3

4

5

6

17q1 18q1 19q1 20q1 21q1 22q1 22q4

90% 60% 30%

Nov 20 Mar 21 Inflation target

Significant increase of crude oil prices in the world

markets after the cut-off date of the previous projection.

Higher than expected prices of CO2 emission

allowances related to the tightening of the EU carbon

dioxide emission target by 2030 and, consequently, an

upward trend in wholesale prices on the the Polish

Power Exchange in recent months.

Outline:

Inflation and economic growth projection of the NBP

Pandemic: economic

fallout

Projection 2021 – 2023

▪ Economic conditions

abroad

▪ Polish economy

Uncertainty

35

Uncertainty

▪ Risk factors

▪ Fan charts

Risk area Description Impact

Scale

of

impact

More severe course

of the pandemic,

combined with a

permanent decline

in economic activity

in Poland

▪ Smaller effectiveness of the measures to contain the COVID-19 pandemic, especially in terms of new infection and

illness prevention: emergence of new coronavirus mutations with higher transmission, increased mortality or

resistance to the vaccines used; shorter than expected vaccine-induced immunity; slower vaccination pace due to

supply constraints. As a result, recurring periods of epidemic expansion and return of restrictions in Poland and

around the world.

▪ Permanent change in the economic behaviour of the population – decline in demand for certain services.

▪ Increase in the number of bankruptcies of enterprises, mainly in the service industries, in particular hotels,

recreation, culture and catering. High uncertainty and pessimistic business sentiment.

▪ Intensification of international trade disputes, resulting in: higher barriers to world trade, foreign investment

reduction and a slowdown in technology transfer to less developed economies. Limited productivity growth in the

global economy.

▪ Sustained loss of potential output in Poland (reduction in corporate investment, increase in equilibrium

unemployment rate, lower participation rate, slower growth of total factor productivity).

Inflation

GDP **

Milder course of the

pandemic

▪ Significant progress in reducing the pandemic in Poland and abroad (high vaccination effectiveness and

acceleration of vaccination pace, milder mutations of the coronavirus).

▪ Increase in optimism of economic agents, return of consumer and investor behaviour to the pre-pandemic

patterns. Unleashing of households’ pent up demand.

▪ Improvement in the global sentiment and stronger positive impact of anti-crisis packages launched due to

pandemic in Poland and abroad.

Inflation

GDP **

Prices of energy

and agricultural

commodities

▪ Volatility of the global prices of energy commodities due to changes in demand and actions taken by the major

producers.

▪ Risk of a significant deviation of meteorological conditions compared to the long-term average in countries that are

important food producers and in Poland. Spread of ASF disease in the European Union.

Inflation

GDP *

SummaryInflation

GDP

Inflation and economic growth projection of the NBP 37

GDP

y/y, %

central

path

50% probability

interval

2021 4.1 2.6 5.3

2022 5.4 4.0 6.9

2023 5.4 4.0 6.8

Source: GUS, NBP calculations.

CPI

y/y, %

below

1.5%

below

2.5%

below

3.5%

below

centr.

path

within

1.5-3.5%

range

2021 1% 20% 73% 53% 72%

2022 15% 42% 73% 52% 58%

2023 13% 33% 60% 51% 46%

CPI

y/y, %

central

path

50% probability

interval

2021 3.1 2.7 3.6

2022 2.8 2.0 3.6

2023 3.2 2.2 4.2

Inflation CPI y/y, % GDP level (Q4 2019 = 100)

-1

0

1

2

3

4

5

6

7

-1

0

1

2

3

4

5

6

7

18q1 19q1 20q1 21q1 22q1 23q1 23q4

90% 60% 30% central path inflation target

85

90

95

100

105

110

115

120

125

85

90

95

100

105

110

115

120

125

19q4 20q2 20q4 21q2 21q4 22q2 22q4 23q2 23q4

90% 60% 30% central path