information to insight ® confidentialapril 3, 2014 us patient access and eligibility screening –...

TRANSCRIPT

Information to Insight®

Confidential April 3, 2014

US Patient Access and Eligibility Screening – Technology Solutions Prepared for Novation

2

Information to Insight®ConfidentialOctober 14, 2013

Contents

• Summary

• Introduction

• Market Overview

• Market Sizing

• Market Conditions

• Competitive Structure

• Growth

• Trends

3

Information to Insight®ConfidentialAugust, 2013

3

Summary: US Patient Access and Eligibility Screening – Technology Solutions

SUMMARY OF FINDINGSSize: The 2013 Patient Access Technology market size, US Hospital subsector, is estimated to be in the range of $450 – 680 million with confidence in the higher end and expectation of significant 2014 growth. Overall 2013 RCM market size (software & services) is estimated to be $2.13B .

Landscape: Patient Access is top of mind for providers who are looking toward the next generation of front-end Revenue Cycle Management functions, which provide real-time data exchange and analysis, clinical-financial integration, and automation. Looking to pre-service interactions to stay solvent and compliant in a turbulent landscape of declining reimbursements and changes brought on by Affordable Care Act and Accountable Care Organization rollout: influx of newly insured, uninsured and Medicaid patients; increasing self-pay; new eligibility verification requirements, etc.

Market Composition/Fragmentation: Patient Access (PA) is a highly competitive and evolving marketplace – next generation offerings have been rolled out by a handful of pioneering Revenue Cycle Management (RCM) market leaders, as well as a slew of smaller, newer vendors with offerings on the spectrum from bolt-on patient access features to integrated RCM platforms. Larger players have fleshed out offerings through M&A activity, partnerships, and R&D. Competition will increase as more RCM vendors expand their suites, niche vendors mature their offerings, and new, non-traditional players enter through M&A, as did Experian and TransUnion. The predominant delivery is through SaaS subscription models.

Leaders: Emdeon, Experian (through 2013 Passport Health acquisition), and RelayHealth (McKesson) are clear market leaders, both in breadth and quality of next-gen PA offerings, an in market share and competitive positioning. A number of smaller patient access/RCM vendors rival with competitive offerings and increasing mindshare, such as Revenue360 and Recondo Technologies. RCM leaders with growing PA suites are well poised to challenge share, such as OptumInsight and SCI Solutions + MedAssets partnership. TransUnion is a strong challenger with unique strengths.

Differentiation: CFOs and CIOs are polarized on preference between favoring a single-source solution (83% CIOs) and best-in-breed solutions, regardless of vendor count (88% CFOs) according to a 2013 Black Book survey. Comprehensive offerings, along with established market and mind share are a competitive advantage. This potential advantage is mitigated by the fact that patchwork solutions are likely to continue to prevail as budgets are tight and solutions are needed in the near term. Smaller, agile patient access innovators will continue to mature their offerings. Capabilities and assets such as credit rating and scoring, and other data analytics are another area of competitive differentiation.

Outlook: Double-digit 2014 growth is expected in light of Affordable Care Act reforms and the entry of Health Insurance Exchanges. While single-source RCM solutions are largely held to be ideal, providers are behind their own expectations in implementing any coherent strategy and they are reassessing their current capabilities. Patchwork solutions of multi-vendor, in-house, and manual systems are likely to prevail near-term. Legacy RCMs are 8-11 years old and ready to be refreshed. Expected continued M&A consolidation, fleshing out of PA suites, and new entrants/partnerships.

Click here for a full list of company profilesVendor Profiles

4

Information to Insight®ConfidentialAugust, 2013

4

Contents

• Summary

• Introduction

• Market Overview

• Market Sizing

• Market Conditions

• Competitive Structure

• Growth

• Trends

5

Information to Insight®ConfidentialOctober 11, 2013

5“Patient Access” encompasses a set of functions at the “front-end” of the revenue management cycle, many of which correspond with pre-service activities and patient interactions. Thus, Patient Access (PA) solutions are a subset of Revenue Cycle Management (RCM) solutions and, like other RCM tasks, can be delivered as individual point solutions, as an integrated PA suite, or as an integrated end-to-end RCM suite. Software as a Service Solutions available on a monthly/annual subscription model are common with this generation.

“Best Practices” Patient Access Suite should include: Including, but not limited to: preauthorization, eligibility verification, ID/address verification, critical data validation, estimated patient responsibility, electronic orders management, eligibility authorization, financial screening and assistance, propensity to pay, point-of-service collections and payment plans, and collections optimization.

Three “Top of Mind” features: Estimated patient responsibility, Eligibility verification, and Preauthorization were reported by providers as top patient access priorities according to the 2013 KLAS Enterprise Patient Access report.

Patient Identity Management: Validate & correct demographic information.

Eligibility and Insurance Verification: Identify insurance coverage and patient’s specific plan.

Preauthorization: Determines whether a service requires prior authorization. Automates request. Retrieve payer’s authorization determination. Integrate results into HIS.

Financial Assistance Screening & Support: Predict/screen patients who meet financial assistance qualifications (Medicaid, charity, ACA enrollment). Automated enrollment for financial assistance and/or assistance in supporting financial counseling staff processes.

Point-of Service Connections: Evaluate patient’s healthcare payment risk, view outstanding balances, estimate of patient responsibility, process credit card payments.• According to FTI Consulting the impact of POS Connections is a 1.5-2% net revenue increase and registration accuracy of >95%.

Propensity-to-Pay: By leveraging hospital's patient claims data, predictive analytic models can accurately estimate a patient's propensity-to-pay with accuracies of 90 percent or higher. These probability scores can assist hospitals in allocating resources and identifying an optimal strategy for patient interaction, financial counseling, payment plans, and collections.

Collections Optimization: Assists healthcare facilities in collection analysis and routing for collections, where it may be best to keep collections in house and not pay contingency fees to an outsourced firm. This includes scoring and segmenting patient accounts, analysis of effectiveness of in house and agency collections, Managing and routing accounts to in-house or agency partners, monitoring of agency performance, monitoring patient financial improvement triggers.

Introduction: Patient Access Technology Solutions

6

Information to Insight®ConfidentialOctober 11, 2013

6

Contents

• Summary

• Introduction

• Market Overview

• Market Sizing

• Market Conditions

• Competitive Structure

• Growth

• Trends

7

Information to Insight®ConfidentialOctober 11, 2013

7

Market Dynamics Overview: US Patient Access Technology Solutions

Market Size

Leaders

Growth

# Vendors

HC Specialists

• The 2013 US Hospital Patient Access Technology market is estimated to be $450-680 million with confidence in the higher end of the range

• Frost & Sullivan predicted a 61% 5-year CAGR (2012-2017) with emphasis on front-end investment. This is mitigated by shifting hospital leadership commitment to near-term investment.

• Currently, 10-15 pioneers developing strong offerings, 10-20 more RCM prospective challengers, and a long tail of 100+ smaller RCM/PA vendors likely to offer 1+ next-generation features in the future.

• Largely comprised of HC-specific vendors, or those with HC specialty through full subsidiaries, divisions, or M&A.

• Leaders: Emdeon, Experian, RelayHealth; RCM Challengers: OptumInsight, SCI Solutions + MedAssets, ZirMed, SSI Group.

MANY: ~100%

SCORECARD REASONING

Market Dynamics Overview

A dynamic and competitive space with strong growth expected in the near term beginning in 2014 due to increasing pressures on profitability and ACA/ACO rollout. Next generation offerings are in high demand, yet few pioneers offer comprehensive solutions. Single source vendors compete with point solution providers comprised of a mix of established RCM vendors, newer niche entrants, and non-traditional players arriving through M&A and partnerships. A flurry of recent years’ consolidation is expected to continue as vendors flesh out offerings and providers decide between replacing legacy RCM systems and upgrading with multi-vendor bolt-on solutions.

MANY: 100+

SOME: ~3-7

MID: ~12%

SMALL: $450-680M

8

Information to Insight®ConfidentialOctober 11, 2013

8

Contents

• Summary

• Introduction

• Market Overview

• Market Sizing

• Market Conditions

• Competitive Structure

• Growth

• Trends

9

Information to Insight®ConfidentialOctober 11, 2013

9

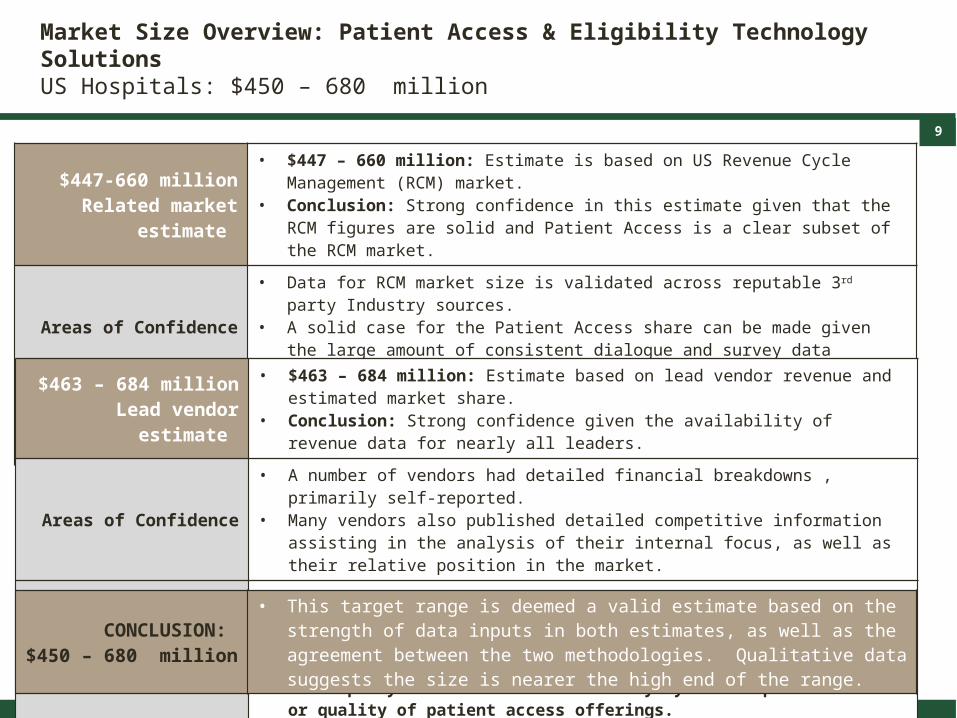

Market Size Overview: Patient Access & Eligibility Technology Solutions US Hospitals: $450 – 680 million

$447-660 millionRelated market estimate

• $447 – 660 million: Estimate is based on US Revenue Cycle Management (RCM) market.• Conclusion: Strong confidence in this estimate given that the RCM figures are solid and

Patient Access is a clear subset of the RCM market.

Areas of Confidence• Data for RCM market size is validated across reputable 3rd party Industry sources.• A solid case for the Patient Access share can be made given the large amount of consistent

dialogue and survey data available regarding Patient Access interest and adoption.

Areas of Uncertainty• Data used to evaluate “software” vs. “services” share is based solely on the revenue

breakdown of lead vendor, Emdeon. Strategies and focus differ across the vendor group.

$463 – 684 millionLead vendor estimate

• $463 – 684 million: Estimate based on lead vendor revenue and estimated market share. • Conclusion: Strong confidence given the availability of revenue data for nearly all leaders.

Areas of Confidence• A number of vendors had detailed financial breakdowns , primarily self-reported.• Many vendors also published detailed competitive information assisting in the analysis of

their internal focus, as well as their relative position in the market.

Areas of Uncertainty• The nascent and shifting landscape makes it challenging to determine leadership and

position based on either history or current reports. 2014 should provide clarity.• RCM market share differs from Patient Access share and the discrepancy cannot be

resolved merely by the comprehensiveness or quality of patient access offerings.

CONCLUSION: $450 – 680 million

• This target range is deemed a valid estimate based on the strength of data inputs in both estimates, as well as the agreement between the two methodologies. Qualitative data suggests the size is nearer the high end of the range.

10

Information to Insight®ConfidentialOctober 11, 2013

10

Patient Access & Eligibility Technology Solutions 2013 Market Size, US hospitals

Estimate #1 – Related Market Comparison: US Revenue Cycle Management (RCM)

METHOD 1 – RCM Market ComparisonA The US RCM technology and services industry - Hospitals, 2012 $1.90B Becker’s Hospital ReviewB Projected 5-year CAGR - Hospitals, 2012-2017 61.6% Frost & SullivanC Alternate 8-year CAGR - Hospitals + Physician Groups, 2010-2018 125% ST Advisors, LLCD Average annual growth rate extrapolated - Hospitals, 2012-2017 12.3% B/5E Estimated US RCM Hospital Market Size, 2013 $2.13B A*[1+D]F Estimated “Patient Access” share of 2013 RCM market* 42-62% Support on next slide

G Estimated “Software” share of RCM market 50%Emdeon’s reported RCM revenue: 50:50 software to services

HPatient Access Technology2013 Market Size, US hospitals $447-660M E*[Fmin:Fmax]*G

*Supporting information and assumptions on next slide

11

Information to Insight®ConfidentialOctober 11, 2013

11Supports & Assumptions – Patient Access as an RCM subsector

Patient Access functions are noted to be an increasingly important area of focus for the Revenue Cycle in light of the demands in forming Accountable Care Organizations (ACOs). CapSite Sr. VP and GM, Gino Johnson, 2011

45% of providers intend to pursue technology solutions for “financial assistance determinations and applications” in light of PPACA and its potential impact on financial assistance, collection practices, and Medicaid expansion.

Healthcare Business Insights; Volume 14, Issue 1: data from Revenue Cycle Academy surveys.

"Most of the efficiencies have been squeezed out of the back-end, and now pushed to the front-end," Paul Pitcher, research director at KLAS, Healthcare Finance News, 2013

John Casillas, Sr. VP, Business-Centered Systems at HIMSS asserts that the patient portal will be a future trend of successful RCM processes. Healthcare Finance News, 2013

A key find of 2013 Voice of the Customer HIMSS study was respondents’ intent on replacing or purchasing net new solutions for front-end patient access functions such as: Address Validation, Pre-Authorization, and Bill Estimation, among others.

2013 HIMSS Analytics Inpatient RCM Study

Assumption: Investment in “front-end” Patient Access technology will drive growth in the RCM market over the next five years, versus investment in other aspects of RCM.

The License model provided by many RCM vendors requires clients to reinvest in their products every year or every few years.

Brad Boyd, a vice president at Culbert Healthcare Solutions, KLAS report 2012

Assumption: 2013 RCM revenue can not entirely squeeze out back-end spending in light of regular renewal fees/upgrades for existing technology. Traditionally, back-end functions have prevailed and thus, currently are likely to represent over 50% of the overall RCM technology in service.

Overall RCM 5-year CAGR of 61.6% (~12%/year) projected for US hospital market: 2012-2017 Frost & Sullivan

Assumption: A minimum of 12% of the 2013 RCM market will be attributable to new patient access investment, which is driving growth.

Assumption: Patient Access functions are roughly 50% of RCM functions and there is high penetration of some areas, i.e. 90% of respondents to a Capsite 2011 study had invested in a patient eligibility solution. Therefore, existing patient access share may not be far below 50 percent.Assumption: Hospitals are shifting their priorities from back-end RCM toward front-end, thus they will find ways to reduce back-end expenditures and limit new outputs in order to reallocate to front-end, such as, move processes in house to reduce outsourcing expense. Hospitals will thereby increase the patient access share of their investment, in addition to the increase reflected in new growth.

CONCLUSION: Patient Access Solutions are estimated to have garnered 42-62% of RCM revenue in 2013.

Addendum to Market Sizing Method 1: Related Market Comparison

Estimated “Patient Access” share of 2013 RCM marketSupports and Assumptions

12

Information to Insight®ConfidentialOctober 11, 2013

12METHOD 2 – Vendor Revenue Estimates*(RCM Software, US Providers)

A Emdeon $121M 2013 annual report

B Experian Healthcare $115M Company press release, annual report (2013, 2012)

C SCI Solutions + MedAssets $100M MedAssets annual report, HC Informatics (2013, 2012)

D RelayHealth (Parent Co: McKesson) $68M 2013 annual report

E OptumInsight (Parent Co: UHG) $64M 2013 annual report, HC Informatics

F ZirMed $50M 2013 HC Informatics

J The Advisory Board $40M 2013 annual report, HC Informatics

G Craneware, Inc. $36M 2013 annual report, HC Informatics

I TransUnion $35M 2012 annual report

H SSI Group, Inc. $32M 2013 HC Informatics

K MedeAnalytics $29M 2013 HC Informatics

L Recondo Technology $27M 2013 press releases, HC Informatics

M Est. “Patient Access” share in 2013 42-62% Support on previous slide

N Estimated market share of leaders 65% Junicon estimatePatient Access Technology2013 Market Size, US hospitals $463-684M (SUM [A:L] * Mmin)/N - (SUM [A:L] * Mmax)/N

Patient Access & Eligibility Technology Solutions 2013 Market Size, US hospitals

Estimate #2 – Bottom Up: Vendor Revenue Estimates

*Sources cited above provided actual revenue figures. See next slide for methodology of deriving the “US RCM provider software” contribution to company revenue. RCM data is used in respect to the integrity of the data in respect to the patient access-specific data.

13

Information to Insight®ConfidentialOctober 11, 2013

1313

Addendum to Market Sizing Method 2: Vendor Revenue Estimate

Estimated “RCM Software” share of 2013 vendor revenueSources and Methodology

Sources and Methodology

Actual revenue data for companies was gleaned from a variety of industry and company sources, such as annual reports, press releases, and industry rankings. Wherever possible, segmented data applicable to the target market was identified.

A range of additional quantitative data and subjective information was used to further parse apart the target market share for each company.Items considered include: Market share, mind share, company focus on RCM and/or Patient Access, Provider to Payer focus, offering maturity, company reputation, direction, and growth. Sources include: press releases, annual reports, company websites, industry analysis such as: studies by KLAS, HIMSS, Black Book, and Capsite, and Healthcare provider discussion.

14

Information to Insight®ConfidentialOctober 11, 2013

14

Contents

• Summary

• Introduction

• Market Overview

• Market Sizing

• Market Conditions

• Competitive Structure

• Growth

• Trends

15

Information to Insight®ConfidentialOctober 11, 2013

15Market Conditions – Patient Access Technology

Degree of Fragmentation (How many participants are there in the market – fragmented markets have few leaders – dominated markets have few incentivized partners)

• Moderately fragmented. Point solutions and multi-vendor systems rule.• Predominant model is to offer features as single solutions that can be

integrated within an integrated RCM suite or with third party systems.• 3-7 RCM leaders; 10-20 RCM vendors are competitive in 1+ features. • With SaaS barriers to entry low, 10+ smaller Patient Access vendors, or

RCM vendors with strong front-end offerings, are competitive.

Market Maturity (Nascent markets can provide opportunities but lack established processes and players – mature markets can be stagnant)

• The market has history, yet is currently redefining “patient access”. • Next generation Patient Access technology is still emerging, yet some

point solutions have had multiple releases and opportunity to evolve.• Comprehensive offerings are few and expected to continue to emerge.

Degree of Penetration (No penetration means a case needs to be made for the service but full penetration requires switching to drive growth)

• Penetration varies. For example: 90% eligibility, 46% propensity to pay.• Top 3 planned for investment: Eligibility verification, POS collections and

medical necessity checking (2012 Capsite VoC study).

Degree of Stability (Volatile markets can be difficult to predict whereas flat markets may have a lower upside)

• A spate of M&A occurred in the past 3+ years, with more expected.• A handful of established RCM vendors innovated early and have a

lead.• Smaller PA pioneers challenge the rule of legacy RCM vendors.• Non-traditional companies may enter the market through M&A or

R&D, leveraging their data analytics, credit scoring, or clearinghouse laurels.

Market Conditions: US Patient Access Technology Solutions

Fragmented Dominated

Nascent Mature

0% 100%

Fragmented Dominated

16

Information to Insight®ConfidentialOctober 11, 2013

16

Contents

• Summary

• Introduction

• Market Overview

• Market Sizing

• Market Conditions

• Competitive Structure

• Growth

• Trends

17

Information to Insight®ConfidentialOctober 11, 2013

17Competitive Structure: The Patient Access software market has a handful of dominant players who are established RCM vendors. Early innovators who focused on next generation front-end features with back-end integration. These vendors offer potential single-source solutions for providers. They are challenged by an active and maturing segment of “patient access pioneers”, who offer well-rounded patient access suites, sometimes with full RCM integration or other next-gen features, such as credit clearinghouse or analytics capabilities. These companies are not as well established in the RCM world, but are making headway and have gone beyond “bolt-on” offerings. A selection of established RCM vendors have begun to flesh out their PA offerings and are well-positioned to become increasingly competitive in this realm. Not depicted are a long tail of 100+ smaller niche vendors, some who have 1+ next-generation patient access offerings.

Competitive Structure: US Patient Access Technology Solutions

ESTABLISHED RCM - PA CHALLENGERS

Annual Revenue: $41M – 2.8B# Companies: ~5

PATIENT ACCESS PIONEERS Annual Revenue: $2M – 98M

# Companies: ~10-20

ESTABLISHED RCM - PA LEADERS

Annual Revenue: $700M-122B# Companies: 4

Emdeon, Experian, and RelayHealth are clear market share leaders: comprehensive PA and end-to-end RCM. Each are established RCM vendors (Experian partners its credit core with Passport’s RCM expertise.) SCI Solutions & new PA partner, MedAssets, rivals in breadth, market reach, & mind share. Well positioned to expand share.

A motley crew of early patient access innovators. Vary in company size, age, historical focus, and patient access offerings & strategies. Includes point solution SaaS, new paradigm RCM, novel partnerships and entrants from credit clearinghouse and analytics realms. Significant aggregate market share. Competitive position.

Full RCM suites with significant market & mind share. Some next generation patient access functionality. PA breadth and maturity of some are close to the leaders. Others challenge based on current RCM leadership. Medium to long term competitive prospects.

• Emdeon (leader)• Experian (Acquired Passport Health)• RelayHealth (Subsidiary of McKesson)• SCI Solutions + MedAssets

• Revenue360• Healthware Systems• TransUnion• Recondo Technologies• RevPoint

• OptumInsight (UHG)• ZirMed• The Advisory Board• SSI Group • Craneware

18

Information to Insight®ConfidentialOctober 11, 2013

18

Recondo Technology

Vendor Stratification: RCM leadership is an advantage, but not the sole determinant of Patient Access leadership. The market is in flux and the landscape is likely to shift over 2014. Exceptional PA technology, comprehensive RCM suites, consolidations, and partnerships are all expected to play out as vendors vie for market share and advantage.

Vendor Stratification: US Patient Access Technology Solutions

RelayHealth (McKesson)

Emdeon

OptumInsight (UHG)

SCI Solutions + MedAssets

BREADTH/MATURITY OF OFFERINGS

RCM

SO

FTW

ARE

REVE

NU

E

Experian (Passport)

ZirMedThe Advisory Board

SSI Group

TransUnion HealthcareCraneware

MedeAnalyticsRevenue360

Healthware Systems

DCS Global

RevPoint (nTelagent)

KEYCredit Data Vendor

Newer/Less established

RCM Leader

RCM Challenger

Leaders’Circle

Challengers’Zone

19

Information to Insight®ConfidentialOctober 11, 2013

19

Patient Access Offerings – Feature Comparison

Identity Management

Eligibility/Insurance Verification

Financial Assistance Screening

Patient Responsibility Estimate

Propensity to Pay

POS collections/payment plans

Collections Optimization

HIE Enrollment Assistance

Registration QA, medical necessity checking and ABN forms,

Emdeon ✔ ✔ ✔ ✔ ✔ ✔ ✔

Experian (Passport) ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

RelayHealth (McKesson) ✔ ✔ ✔ ✔ ✔ ✔ Indeterminate

SCI Solutions + MedAssets ✔ ✔ ✔ ✔ ✔

OptumInsight (UHG) ✔ ✔ ✔ IndeterminateRCM Leader in ACOs, IDNs, RCM leader in small hospitals, <250 beds, & Academic

160M (products

64 $1.15B "HC IT"; 40% software (HC informatics)- estimate 35% provider rev; estimate 40% RCM………….4 markets: care providers (e.g.,physician practices and hospitals),

207.00 #REF! #REF!

ZirMed ✔ ✔ ✔ ✔ Indeterminate

The Advisory Board ✔ ✔ ✔ ✔ Indeterminate

Craneware ✔ ✔ ✔

TransUnion ✔ ✔ ✔ ✔ ✔ ✔

SSI Group ✔ ✔ ✔ ✔

MedeAnalytics Indeterminate ✔ Medicaid only ✔

Revenue360 ✔ ✔ ✔ ✔ ✔ ✔

Recondo Technologies ✔ ✔ ✔ ✔ ✔

RevPoint (nTelagent) ✔ ✔ ✔ ✔ Capacity to Pay ✔ Indeterminate

Healthware Systems ✔ ✔ ✔ ✔ ✔ ✔ ✔

DCS Global ✔ ✔ ✔ ✔ ✔ ✔ Indeterminate

20

Information to Insight®ConfidentialOctober 11, 2013

20

Contents

• Summary

• Introduction

• Market Overview

• Market Sizing

• Market Conditions

• Competitive Structure

• Growth

• Trends

21

Information to Insight®ConfidentialOctober 11, 2013

21

Patient Access Technology Solutions, US hospitals

2013 Market Growth Estimate: New investment + Upgrades

METHOD – Market Adoption EstimateA Total Number of All U.S. Registered Hospitals 5,723 American Hospital AssociationB 2011: US Hospitals planning to invest in Patient Access Solutions 23% CapSite US Patient Access Study, 2011

C2012: Hospitals planning to replace core RCM solutions “in the next 24 months”; Hospitals planning to upgrade.

1) 21%2) 26%

CapSite Revenue Cycle Management Study, 2012

DQ3 2013: Rough percentage of above hospitals who had yet to initiate a sustainable RCM plan as of Q3 2013. ~66% CapSite US Patient Access Study, 2013

E2013: Hospitals considering investment in, “Technology to Streamline Financial Assistance” in response to PPACA . 45%

Healthcare Business Insights 2013 report

F2013: % CFOs confirming they are reassessing the capabilities of their current legacy, core, and bolt-on RCM applications. 36% CapSite US Patient Access Study, 2013

G Estimated # of 2013 hospital investments in Patient Access 1,775 [(A*C1*D) + (A*C2*D)]H Annual price range for a Patient Access Suite: low to high end $60k-360k Recondo Technology, SaaS vendor

Assumption: Given the tentative investment climate, a lower end of the investment range is assumed for 2013. Hospitals may increase their commitment through 2014 and beyond as ACA changes begin to make an impact.

I Estimated average 2013 patient access investment range/hospital $60k-200k Junicon Assumption

JPatient Access Technology2013 Market Growth Estimate, US hospitals $106-355M [(G*Imin) – (G*Imax)]

22

Information to Insight®ConfidentialOctober 11, 2013

22

Growth Drivers: Patient Access Technology Solutions, US hospitals

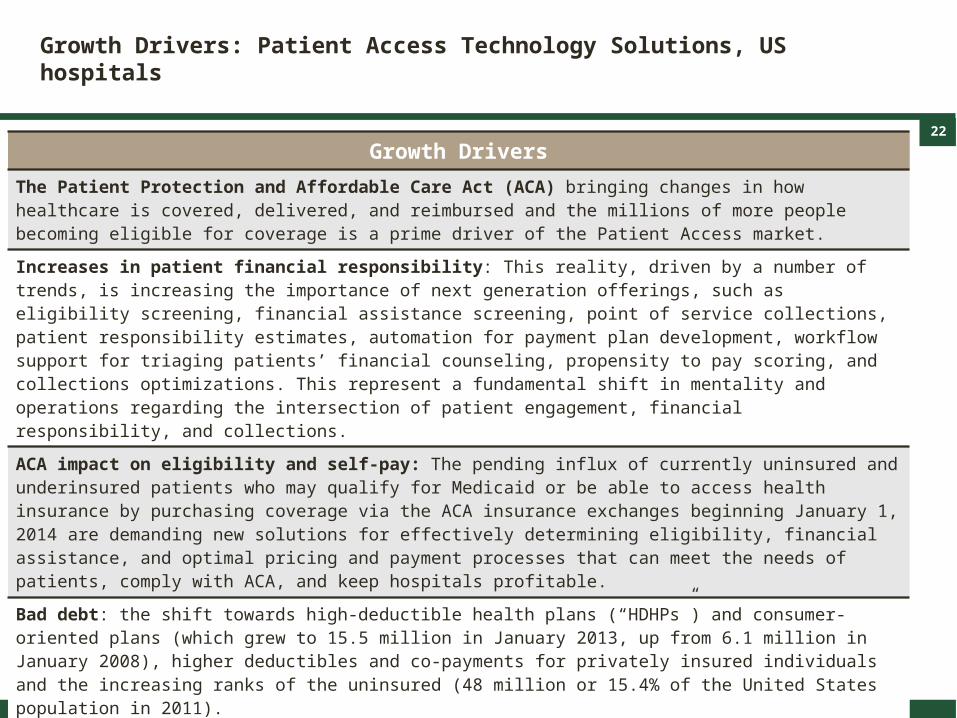

Growth DriversThe Patient Protection and Affordable Care Act (ACA) bringing changes in how healthcare is covered, delivered, and reimbursed and the millions of more people becoming eligible for coverage is a prime driver of the Patient Access market.

Increases in patient financial responsibility: This reality, driven by a number of trends, is increasing the importance of next generation offerings, such as eligibility screening, financial assistance screening, point of service collections, patient responsibility estimates, automation for payment plan development, workflow support for triaging patients’ financial counseling, propensity to pay scoring, and collections optimizations. This represent a fundamental shift in mentality and operations regarding the intersection of patient engagement, financial responsibility, and collections.

ACA impact on eligibility and self-pay: The pending influx of currently uninsured and underinsured patients who may qualify for Medicaid or be able to access health insurance by purchasing coverage via the ACA insurance exchanges beginning January 1, 2014 are demanding new solutions for effectively determining eligibility, financial assistance, and optimal pricing and payment processes that can meet the needs of patients, comply with ACA, and keep hospitals profitable.

Bad debt: the shift towards high-deductible health plans (“HDHPs”) and consumer-oriented plans (which grew to 15.5 million in January 2013, up from 6.1 million in January 2008), higher deductibles and co-payments for privately insured individuals and the increasing ranks of the uninsured (48 million or 15.4% of the United States population in 2011).

Responding to self-pay and mounting collections: 45% pf providers are considering investment in, “Technology to Streamline Financial Assistance” in response to PPACA roll-out according to a Healthcare Business Insights report; 26% are considering moving financial counseling upstream.

Outdated Legacy RCM systems: In an interview with Healthcare IT News Managing Editor Mike Miliard, HIMSS Analytics Executive Vice President John Hoyt asserted, "There's a new future for revenue cycle." It's time - past time - for replacement, he suggested. The systems are 8 to 11 years old and not able to respond to the current demands.

23

Information to Insight®ConfidentialOctober 11, 2013

23

Contents

• Summary

• Introduction

• Market Overview

• Market Sizing

• Market Conditions

• Competitive Structure

• Growth

• Trends

24

Information to Insight®ConfidentialOctober 11, 2013

24

Outlook & Trends: Patient Access Technology Solutions, US hospitals2014 and beyond

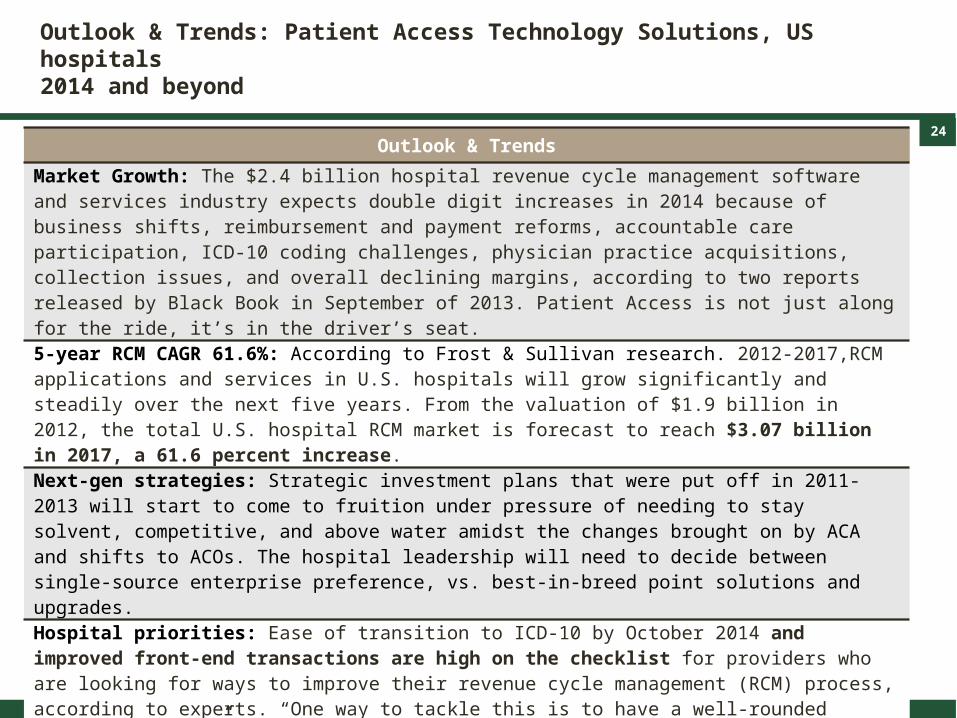

Outlook & TrendsMarket Growth: The $2.4 billion hospital revenue cycle management software and services industry expects double digit increases in 2014 because of business shifts, reimbursement and payment reforms, accountable care participation, ICD-10 coding challenges, physician practice acquisitions, collection issues, and overall declining margins, according to two reports released by Black Book in September of 2013. Patient Access is not just along for the ride, it’s in the driver’s seat. 5-year RCM CAGR 61.6%: According to Frost & Sullivan research. 2012-2017,RCM applications and services in U.S. hospitals will grow significantly and steadily over the next five years. From the valuation of $1.9 billion in 2012, the total U.S. hospital RCM market is forecast to reach $3.07 billion in 2017, a 61.6 percent increase.Next-gen strategies: Strategic investment plans that were put off in 2011-2013 will start to come to fruition under pressure of needing to stay solvent, competitive, and above water amidst the changes brought on by ACA and shifts to ACOs. The hospital leadership will need to decide between single-source enterprise preference, vs. best-in-breed point solutions and upgrades.Hospital priorities: Ease of transition to ICD-10 by October 2014 and improved front-end transactions are high on the checklist for providers who are looking for ways to improve their revenue cycle management (RCM) process, according to experts. “One way to tackle this is to have a well-rounded technology suite”, June 2013 Healthcare Finance News.“Top of mind” Patient Access Factors considered most important by providers according to the The KLAS Enterprise Patient Access report for 2013: 1) Patient responsibility; 2) Eligibility verification; 3) Preauthorization Vendor behavior: M&A activity is expected to continue as vendors vie for integrated RCM suites with best-in-breed Patient Access technologies for the next generation. Traditional RCM vendors are still rivaled by newer upstarts who are fleshing out their offerings, as well as by new entrants with big bucks and complementary offerings, such as TransUnion. Vendors are fleshing out offerings and continuing to evolve existing features.