infrastructure markets [email protected] +61 2

TRANSCRIPT

No content below the line

Infrastructure MarketsHow Attractive Are They?

How S&P Looks At Credit Risks

Copyright © 2016 by S&P Global.

All rights reserved.

Thomas [email protected]

+61 2 9255 9872

Bertrand [email protected]

+65 6239 6303

Abhishek [email protected]

+65 6216 1121

No content below the line

Definition Of The Infrastructure Asset Class

Private & Confidential 2

25.0

18.0

5.0 4.0 3.0

20.0

13.0

5.0 4.0 3.0

Essential service to society Asset-backedInflation-Linked MonopolisticNo/Limited GDP risk High barriers to entryYield generation No/Limited commodity riskRegulation Others

• Investors associate clear

characteristics to infrastructure

assets

• In particular, they favour natural

monopolies…

• … and the long-term orientation of

such investments.

• The number of boxes they can tick

has a clear bearing on their appetite

The Way Investors See It

Source: Deloitte Infrastructure Investors Survey 2016, Deloitte Analysis

Characteristics Of Infrastructure Assets

Which factors do you see as most critical in defining what constitutes an

infrastructure asset now? (% of respondents)

No content below the line

Market Snapshot

An Overview Of The Big Numbers

3Private & Confidential

No content below the line

Setting The Scene

Private & Confidential 4

Key Statistics For 2015

US$858m

Average size of unlisted infrastructure fund closed in 2015

US$349b

Estimated aggregate value of 661 infrastructure deals completed globally in 2015

US$108bEstimated amount of “dry powder” held by infrastructure firms

US$5.3b

Aggregate capital raised in Asia, nearly double the amount of 2014

Source: 2016 Preqin Global Infrastructure Report

No content below the line

Funding Markets Remain Supportive…

Private & Confidential 5

-

3.0

6.0

9.0

12.0

15.0

18.0

21.0

24.0

27.0

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15 2H15 1H16

Bank Loans Development Finance Institution Loans Bonds Equity Equity/Debt ratio (%)

Debt And Equity Are Waiting To Be Put To Work

Source: IJ Global

Global Project Finance Value By Funding

(US$ billion)

No content below the line

… But Not All Goes To Greenfield…

Private & Confidential 6

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15 2H15 1H16

Primary Financing Refinancing Asset acquisition

As Acquisitions & Refinancing Take Their Share

Source: IJ Global

Global Project Finance Value By Purpose

(US$ billion)

No content below the line

… Constraining Net Growth In Infrastructures

Private & Confidential 7

• It seems to be a consensus among market participants that there is an

“infrastructure gap”

• “There is absolutely zero correlation between the scale of need for infrastructure

and addressable opportunities for the private sector” (Jim Barry, head of

Infrastructure at BlackRock)

• So why does demand fail to meet needs?

- Infrastructure users have to change their mindset

- Capital may be available, but not necessarily the right form of money

- Many investors restrict themselves

- Government do not monetise assets

- The infrastructure-finance market lacks transparent information

Why An Investment Shortfall?

No content below the line

An Investor’s Perspective

Overview Of Investors’ Focus and Infrastructure Needs

8Private & Confidential

No content below the line

Global - A Safe Asset Class… Really?

Private & Confidential 9

38.0

35.0

5.0

15.0

7.0

Political risk Regulatory risk Refinancing risk

Operational risk Tax risk

• The key risks that concern

infrastructure investors are external

risks…

• … including macroeconomic

circumstances, and…

• … the political and regulatory

environment

• Technological risk does not currently

seem a high concern for

infrastructure investors

The Way Investors See It

Source: Deloitte Infrastructure Investors Survey 2016, Deloitte Analysis

Risks Of Infrastructure Assets

When considering whether to invest, which risks most concern you? (% of

respondents)

No content below the line

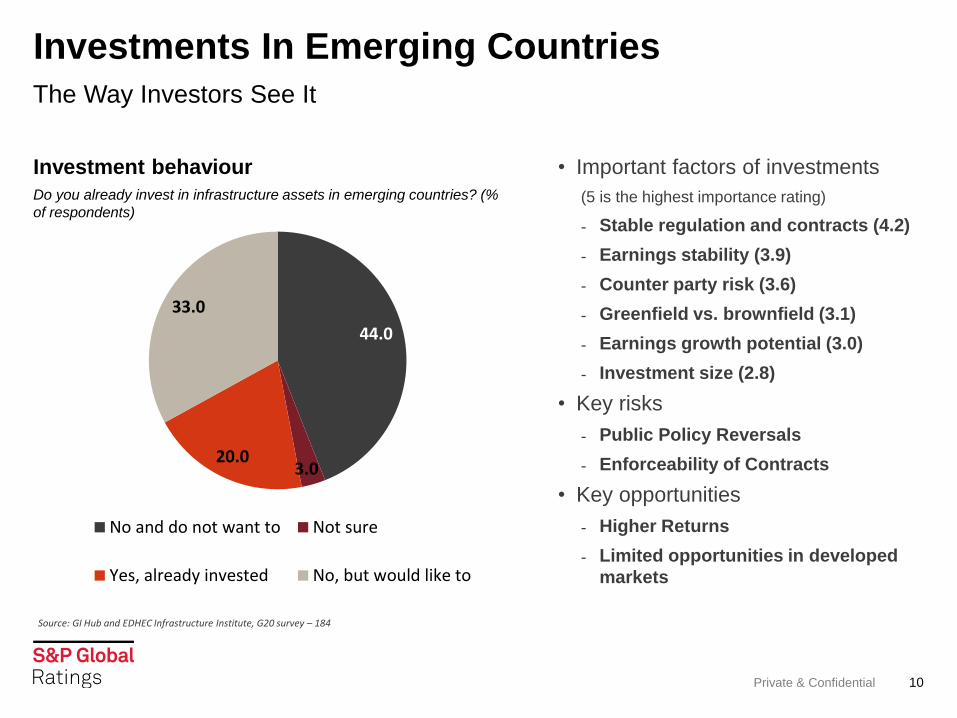

Investments In Emerging Countries

Private & Confidential 10

The Way Investors See It

Source: GI Hub and EDHEC Infrastructure Institute, G20 survey – 184

• Important factors of investments

(5 is the highest importance rating)

- Stable regulation and contracts (4.2)

- Earnings stability (3.9)

- Counter party risk (3.6)

- Greenfield vs. brownfield (3.1)

- Earnings growth potential (3.0)

- Investment size (2.8)

• Key risks

- Public Policy Reversals

- Enforceability of Contracts

• Key opportunities

- Higher Returns

- Limited opportunities in developed

markets

44.0

3.0 20.0

33.0

No and do not want to Not sure

Yes, already invested No, but would like to

Investment behaviour

Do you already invest in infrastructure assets in emerging countries? (%

of respondents)

No content below the line

Investment Needs In Emerging Asia

Private & Confidential 11

Source: ADB

Actual Infrastructure Investments Lower-Deficit Likely To Increase Further

No content below the line

Infrastructure Investment – Why It Matters

Private & Confidential 12

-

20.0

40.0

60.0

80.0

100.0

120.0

Quality of overallinfrastructure

Transport infrastructure Electricity and telephonyinfrastructure

Global Competitiveness Index

China India Indonesia Malaysia Philippines Singapore Thailand

Developing Asia - Infrastructure a relative Weakness

Source: WEF (World Economic Forum) 2016-2017 Global Competitiveness Index. The lower the score, the higher the quality of infrastructure

Infrastructure Quality Comparisons Across 7 Asian Nations

No content below the line

Philippines - Past Investments In Infra

Private & Confidential 13

-

3.0

6.0

9.0

12.0

15.0

18.0

21.0

-

5.0

10.0

15.0

20.0

25.0

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

PPP Investments (US$ billion) [Left axis] Other Investments (US$ billion) [Left axis]

# Other Projects [Right axis] # PPP Projects [Right axis]

A Fluctuating Record

Source: World Bank, PPI Visualisation Dashboard

No content below the line

Philippines: Infrastructure

Private & Confidential 14

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

2010-2011 2011-2012 2012-2013 2013-2014 2014-2015 2015-2016 2016-2017

Transportation Electricity & Telecommunications Global Competitiveness Index

Infrastructure Quality Has Been Deteriorating

Infrastructure Weakness Hurts Competitiveness

Source: WEF (World Economic Forum) 2016-2017 Global Competitiveness Index. The lower the score, the higher the quality of infrastructure

No content below the line

Putting The Infrastructure Puzzle Pieces Together

Private & Confidential 15

• Demand:

• Need to bridge the gap between existing assets and needs for new assets

• Support growth in population and economy

• Funding:

• Governments will support increase in infrastructure spending but have fiscal constraints

• Private sector is keen to participate, but will evaluate projects based on commercial returns

• PPP:

• Public-Private-Partnership success is key to meeting funding needs

• Stable regulations/ policy, economically feasible projects are pre-requisites

PPPs Must Be Successful To Meet The Needs For Infrastructure

No content below the line

Copyright © 2016 by Standard & Poor’s Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse

engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor’s Financial Services LLC or

its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders,

employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or

omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is

provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF

MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL

BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any

direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits

and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P’s opinions,

analyses and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the

suitability of any security. S&P assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill,

judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary or an

investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due

diligence or independent verification of any information it receives.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to

assign, withdraw or suspend such acknowledgement at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of

an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of

S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non-public information received

in connection with each analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and

analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com

(subscription), and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at

www.standardandpoors.com/usratingsfees.

Australia

Standard & Poor's (Australia) Pty. Ltd. holds Australian financial services license number 337565 under the Corporations Act 2001. Standard & Poor’s credit ratings and related research are not

intended for and must not be distributed to any person in Australia other than a wholesale client (as defined in Chapter 7 of the Corporations Act).

STANDARD & POOR’S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor’s Financial Services LLC.

16Private & Confidential