infrastructures, a priority for india, an opportunity for ...legemcity.com/pdf/3.pdf ·...

TRANSCRIPT

s

Infrastructures, a priority for India, an opportunity for foreign investors

www.indiaitaly.com

GAPS BETWEENIndia’s Economic & Infrastructure Development

• Despite becoming the second fastest growing and the fourth largest economy of the world(in terms of Purchasing Power Parity or PPP), India continues to face large gaps in thedemand and supply of essential social and economic infrastructure and services.

• The infrastructure shortages are proving to be the leading binding constraint in sustaining,deepening, and expanding India’s economic growth and competitiveness.

• Lack of good quality infrastructure is costing India 1–2% growth in GDP every year and ispreventing the sectoral, regional, and socioeconomic broadening of the economy and itsbenefits, as well as affecting inclusive growth in India.

• India’s global competitiveness remains constrained and is adversely affected by lack ofinfrastructure, which is critical for improved productivity across all sectors of the economy.

• Poor infrastructure has been a major barrier to foreign direct investment (FDI).

• The benefits of accelerated growth of the last decade have not been shared by large sectionsof the population.

• Infrastructure is now seen as vital necessity for economic growth and poverty alleviation.

• Studies by the ADB (Asian Development Bank) and others have confirmed a strong linkagebetween infrastructure investments, economic growth, and reduction of poverty.

• GOI has thus recognized that with better infrastructure India’s growth can be higher, with thebenefits reaching a much larger section of the population.

HISTORICALLYInvestments in infrastructure have been low in India

• Development of infrastructure was completely in the hands of the public sector and wasplagued by corruption, bureaucratic inefficiencies, urban-bias and an inability to scaleinvestment.

• The country initiated the process of partnering with the private sector in 1991, beginning withthe power sector, and since then achieved some successes through PPPs in the telecom,roads, ports and airports sectors.

• By the end of the 1990s, actual investment (public and private) in infrastructure remained atunder 4% of GDP per annum as per the World Bank 2005 report. Due emphasis was givento scale up the investment to about 8% of GDP by 2005-06.

• To realize sustained growth of 7-8% for the year 2007-2012, the government acknowledgedthat investment in infrastructure would have to be at the same rate as the economic growththat is being targeted.

• It was thus imperative that India would have to increase infrastructure spending from 4.6% inthe Tenth year Plan (2002-2006) to about 7%-8% in the Eleventh year Plan (2007-2012).

• However, at the end of the year 2010, the Gross capital formation (GCF) in Infrastructure iscurrently 5% of GDP i.e. approx €985 Billion (USD 1.3 trillion)

• The Infrastructure sector currently accounts for 26.7% of India’s industrial output and if thehas to match the more advanced Asian economies, then GCF has to be increased to a moresustainable level of 9 to 10%.

• Finally, in some areas, roads, rail lines, ports and airports are already operating at capacity, soexpansion is a necessary prerequisite to further economic growth.

INDIA’S INFRASTRUCTUREIndian government estimated investment requirements

Physical Infrastructure deficit & the XI Plan (2007-2012 ) targets

Power and Transportation (i.e. roads, ports, and airports) is expected to lead growthwith more than 50% of the planned investment allocated for these two sectors.

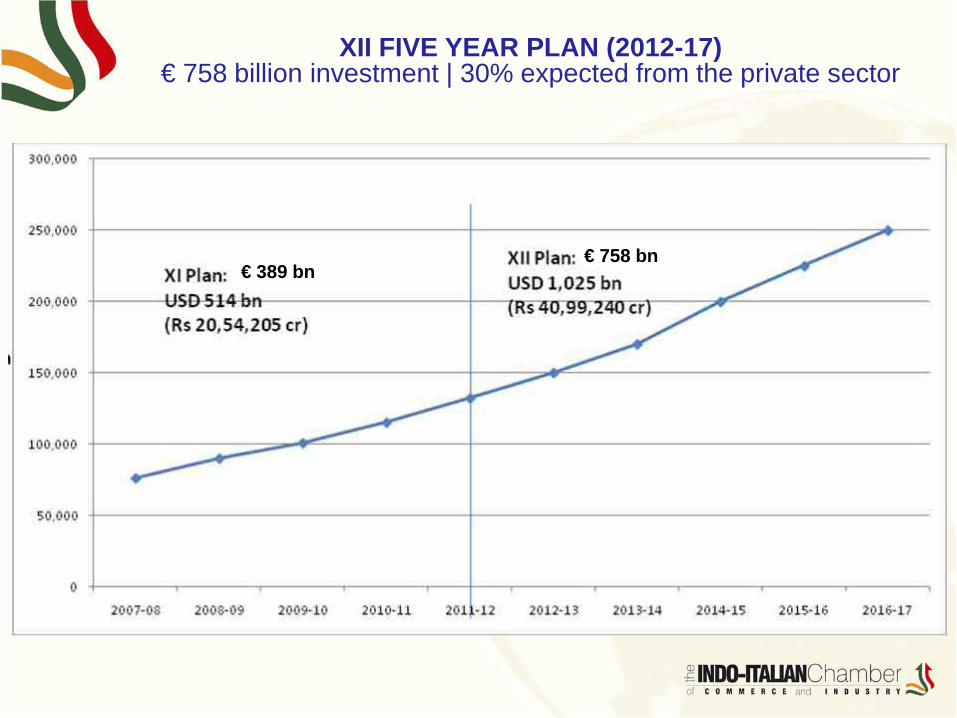

XI YEAR PLAN389 billion Euro over a period of 5 year (2007-12)

India’s infrastructure a reality checkThe government’s target and progress till date

• XI five year plan (2007-2010) targeted investment of €389 billion in infrastructure.

• XII five year plant (2012-2017) targeted investment of €758 billion in infrastructure.

• Increasing dependency upon private sector participation via Public- Private PartnershipsPPPs).

• Private sector will account for nearly 30% of infrastructure investment in XII five yearplan as against 18% in the current five year plan.

• Thus, private sector will invest €116.70 billion (US$150bn) over the five year period orabout €22.7bn (US$30bn) annually.

• Assuming that equity will fund 25-30%, this means a €5.68- €7.5billion (US$7.5-10bn)equity infusion each year by the private sector.

• Global funding in various forms such as Private Equity, dedicated InfrastructureFunds, Foreign Direct Investment (FDI) and Foreign Institutional Investment (FII)

XII FIVE YEAR PLAN (2012-17)€ 758 billion investment | 30% expected from the private sector

€ 758 bn€ 389 bn

Opportunities in Infrastructure sector

Introduction:

• Good physical connectivity in the urban and rural areas is essential for economic growth

• India’s growing economy has witnessed a rise in demand for transport infrastructure andservices by around 10 percent a year.

India’s Transport Sector:

• Railways (the largest one in Asia) and roads are the dominant means of transport carryingmore than 95% of total traffic generated in the country.

• Roads carry almost 90 percent of the country’s passenger traffic and 65 percent of its freight.

• However, most highways in India are narrow and congested with poor surface quality, and 40percent of India’s villages do not have access to all-weather roads.

• India has 12 major and 185 minor and intermediate ports along its vast coastline and 60airports, including 11 international airports.

TRANSPORT SECTOR A brief overview

ROADS & HIGHWAYS

Projected spending from (FY07-12) approx. Euro 69 billion

• 3.34 million kilometres of road network is the second largest in the world

• Road network carries nearly 65% of freight and 85% of passenger traffic.

• The National Highway Development Program (NHDP), is planning more than 200 projectsin NHDP Phase III and V to be bid out, representing around 13,000km of roads.

• The average project size is expected to €113~151million (US$150-US$200million).

• Larger projects are likely to reach the €530~€606 million ($700 million-US$800 million)range.

• 53 projects (aggregate length of 3000km) and estimated cost of around €6bn (US$8billion) are already at the pre-qualification stage.

• More than 10 states are also actively planning the development of their highways(average project size €75~ €94 million range).

• 100% FDI under the automatic route is permitted for all roaddevelopment projects.

• 100% income tax exemption is available for a period of 10 consecutive assessment years outof the 20 years beginning from the year in which the undertaking begins to operate thebusiness.

• Subscription to equity shares or debentures issued by public company (infra projects) eligiblefor deduction equal to 20 per cent of the amount subscribed

• Import duty completely exempted on certain identified high quality construction plants andEquipments, while import of bitumen is now permitted under Open General License.

• NHAI agreeable to provide grants/viability gap funding for marginal projects

• Model Concession Agreement formulated and Long Concession period of upto 30 years.

• IIFCL to provide funding upto 20% of project cost

• Dispute resolution will be in line with Arbitration and Conciliation Act 1996, based onUnited Nations Commission on International Trade Law (UNCITRAL) provisions

ROADS | Policy Initiatives

• The Indian Government has projected investments in the XI Plan (2007-2012) totalling €49bnof which 40% is expected to be contributed by the private sector.

• Indian Railways (IR) has one of the largest and busiest rail networks in the world, transportingover 18 million passengers and more than 2 million tonnes of freight everyday.

• With 1.4 million people, it is the world's largest commercial or utility employer.

• The railways traverse the length and breadth of the country, covering 6,909 stations over atotal route length of over 63,327 kilometers (39,350 miles).

• Indian Railways own over 200,000 wagons, 50,000 coaches and 8,000 locomotives of rollingStock

• One major PPP programme is already in its initial phases (Dedicated Freight Corridor project)at an estimated cost of US$6-7 billion.

RAILWAYS

projected spending from (FY07-12) approx. Euro 49 billion

• Investment in infrastructure as well as modernization of wagonstechnology.

• Advanced signalling & telecommunication.

• Induction of high horsepower locomotives.

• Grade separation.

• Use of information technology specifically tailored to improve transit times and lower unitcost operation

• Building world - class passenger and freight terminals bench - marked to the best globalstandards.

• Other proposed initiatives include the development of manufacturing plants for rolling stock,setting up of logistics parks and for projects focused on increasing connectivity with ports.

• City metro systems are also in the pipeline with the first corridor of the Mumbai MetroProject been awarded to Reliance Infrastructure.

RAILWAYS | Sector Initiatives

• An estimated investment of around €16bn is targeted for port projects.

• The National Maritime Development Program includes 276 projects, with a requiredinvestment of about €11.37bn over the next ten years, with private investment targeted ataround €6 billion.

• Port traffic is estimated to reach 877 million tonnes by 2011-12, and containerised cargo isexpected to grow at 15.5% (CAGR) over the next 7 years.

• Major opportunities for projects related to port development (construction of jetties, berths,container terminals, deepening of channels to improve draft..etc)

• 100% FDI, and an independent tariff regulatory authority has been set up to facilitate projectsat major ports.

PORTS

Projected spending from (FY07-12) approx. Euro 16 billion

• 100% FDI under the automatic route is permitted for port development projects.

• 100% income tax exemption is available for a period of 10 years in a block of 15 years.

• Tariff Authority for Major Ports (TAMP) regulates the ceiling for tariffs charged by Majorports/port operators (not applicable to minor ports).

• Major port trusts permitted to form Joint Ventures with foreign port operators, minor portsand other companies to attract new technology and creation of optimal infrastructure.

• A comprehensive National Maritime Policy is being formulated to lay down the vision andstrategy for development of the sector till 2025.

PORTS | Policy Initiatives

Power Generation• India has the fifth largest generation capacity in the world with

an installed capacity of 152 GW as on 30 September 2009 (Source: in a recent report by Netscribes,“Power Sector – India”, March 2009), which is about 4 percent of global power generation.

• The average per capita consumption of electricity in India is estimated to be 704 kWh during2008-09, which is relatively low in comparison to world average stands at 2,300 kWh2.

Power Transmission• The current installed transmission capacity is only 13 percent of the total installed generation

capacity (Source: Ministry of Power Website 2009)

• The Ministry of Power plans to establish an integrated National Power Grid in the country by2012 with close to 200,000 MW generation capacities and 37,700 MW of inter-regional powertransfer capacity.

Power Distribution• While some progress has been made at reducing the Transmission and Distribution (T&D)

losses, these still remain substantially higher than the global benchmarks, at approximately 33percent.

POWER

Projected spending from (FY07-12) approx. Euro126 billion

• The 11th Five Year Plan (2007-2012) envisaged an addition of 78.7 GW (gigawatt).

• The 12th five year plan projects an addition of 100 gigawatt of which tendering for about43GW has already been done, with the rest likely to be tendered over the next three tofive years.

• 100% FDI permitted in Generation, Transmission & Distribution.

• Income tax holiday for a block of 10 years in the first 15 years of operation.

• Waiver of capital goods import duties on mega power projects (above 1,000 MW generationcapacity)

• Policy framework in place and also emphasizes the need of meeting future powerrequirements through non conventional sources.

• Main objectives: access to electricity for all households, meet full power demand andincrease per capita availability of power to 1,000 units by 2012.

• Independent Regulators: Central Electricity Regulatory Commission for Central PSUsand inter- state issues. Each State has its own Electricity Regulatory Commission

POWER | Sector Initiatives

• The Indian aviation industry is one of the fastest growing aviationindustries in the world with private airlines accounting for more than75 per cent of the sector of the domestic aviation market.

• The country has 454 airports and airstrips, of which 16 are designated as internationalairports.

• As per certain projections by 2020, Indian airports are estimated to handle:

280 million passengers.Investment opportunities envisaged: € 61 billion (US$80 billion) in new aircraft and €22.87billion (US$30bn) in development of airport infrastructure.Cargo in the range of 3.4 million tones per annum.Air cargo traffic to grow at over 11.4% p.a. over the next 5 years.

• Major opportunities lie in Greenfield airport projects in resort destinations and emergingmetros such as Kannur, Goa, Pune, Navi Mumbai, Ludhiana, etc.

• City-side development opportunities for upgradation of 35 non-metro airports.

• About 25 regional greenfield/unutilised airports likely to be bid out for private development.

AIRPORTS

Projected spending from (FY07-12) approx. Euro 6 billion

• 100% FDI is permissible for airports.

• FIPB approval required for FDI beyond 74%.

• 100% FDI under automatic route is permissible for greenfield airports.

• Private developers allowed to setup captive airstrips and general airports 150 km awayfrom an existing airport.

• 100% tax exemption for airport projects for a period of 10 years.

• 49% FDI is permissible in domestic airlines under the automatic route, but not by foreignairline companies

• 100% equity ownership by Non-Resident Indians (NRIs) is permitted.

• 74% FDI permissible in cargo and non-scheduled airlines.

AIRPORTS | Sector Initiatives

• Significant increase in foreign money entering India in the year 2008 in the wake of elevatedinterest in PPP investments in the year 2006 and 2007 respectively.

• In the year 2008, the sector witnessed an India focused Infrastructure fund raisings of €1.5bn(US$2.2bn) of which was over and above the Private Equity money raised for infrastructure.

• Influx of foreign equity dried up in the year 2009 only (€758 million) of infrastructure PrivateEquity was raised.

• FDI into Indian infrastructure also rose sharply in 2007 and 2008 but then declined in thefinancial year 2009 due to the global financial crisis and lack of meaningful projects.

• In March 2010, FDI in infrastructure stood at €1.13bn~€1.51bn (US$1.5-2bn)

Public Private PartnershipOverview of foreign investments

Foreign Direct Investment (FDI) & the regulatoryenvironment

The tax environment for E&C companies Investing in India

Nature of tax Governing Authority Rate of Tax (in %)

Income Tax Central Government 33.99

Custom Duty Central Government Up to 31.70

Excise Duty Central Government Up to 14.42

Service Tax 1 Central Government 12.36

Sales Tax/Value Added Tax (‘VAT’) 1

Central Government 4.00 to 12.50

1India is planning to implement a unified goods and service tax (GST) in 2010 at a rate still to be determined

Overview of tax holidaysFor various infrastructure segments

PPP MODELS Stabilized in roads & evolving in other sectors

• Most PPP projects are in Transportation, especially roads sector, which accounts for morethan 60% of the total number of projects and 45% by total value.

• Concession agreements, especially in roads and ports have evolved over the last 4-5 yrs.

• Private participation has not been forthcoming in railways due to systemic hurdles andimplementation issues

• Water sector in India is least amenable for PPP due to political sensitivity of the sector.

PPP MODELInternational players in Indian market

• Foreign multinationals have equity participation only in 22 PPP projects valued at €287million.

• Malaysian companies are leading investors in public private partnership (PPP) projects inIndia, involving nearly six major infrastructure ventures.

• UK (4 projects), Mauritius (3), France (2), Germany (2), UAE (2), Philippines (2) and UnitedStates (1), Italy(1) and Switzerland (1).

• Prominent PPP projects: modernisation of Mumbai and Delhi international airports, Delhi-Noida toll bridge, Pipavav port, Bangalore international airports and JNPT container terminal.

• Mauritius-based ACSA Global (Airports Company South Africa), has Euro 26 million equitystake in modernization of Mumbai international airport project.

• Apollo Enterprises from UK has equity stakes of Euro 8 million and Euro 1.8 million inLucknow-Sitapur road project and Raipur Durg expressway respectively.

Sector-wise break-up of foreign investor participation in PPP projects

Foreign Investor Versus Sector

No. of Projects

Investment in million Euro

% of total project cost

Ports 9 315.34 24%Roads 9 194 15%Airports 4 798.21 61%Total 22 1307.55 100%

PPP MODELExamples of International players in Indian market

Atlantia S.p.A (Italy) has formed a JV with Tata Realty and Infrastructure Limited Theconsortium has been awarded a project on BOT basis in the State of Maharashtra.

Balfour Beatty, is a London based leading worldwide engineering, construction, andservices company which is planning to enter India and is one of the bidders for a $1Billion project to be awarded by NHAI.

Leighton India is a 100% subsidiary of Leighton Holdings, Australia. Recently it hasbagged $ 460 million EPC contract for a NHAI road project from ILFS TransportationNetworks Ltd. It has also been participating in PPP projects as co-developer andhas two NHAI road projects in JV with Indian Developers and has completed EPCworth ~$200 million for these projects. It also has been awarded two port terminalprojects in JV with Sterlite Industries Ltd.

Methods of finance Various methods of finance for infrastructure projects via domestic

&foreign sources

KEY GOVERNMENT INITIATIVES

1) Committee on Infrastructure (COI)

2) Cabinet Committee on Infrastructure (CCI

3) Public Private Partnership Appraisal Committee (PPPAC)

4) Viability Gap Funding (VGF) Scheme

5) India Infrastructure Finance Company Limited (IIFCL)

6) Tax Exemption

7) Advisory Services

8) Model Documents

Whilst key government personnel are aware of the concerns raised by the industryparticipants in they are also keen to stress that a number of changes and reforms have beenundertaken over the past three to five years. Moreover, listed below are some of the key initiativesundertaken:

PROJECT DESCRIPTION COSTEuro Mn

1. Rail network1.1 MRTS1.2 MUTP

A 146 km metro rail networkEnhancing the existing suburban rail network

1,4611,291

2. Road network2.1 MUIP Enhancing Mumbai’s road network 473

3. Sea Link3.1 Western freeway link 21 km sea link to decongest western

corridor696

4. MTHL A road and rail bridge between Mumbai and the mainland

719

5. Navi Mumbai International Airport

Mumbai’s second international airport over 2400 acres

678

6. Water Supply Project Augmenting water supply in the hinterland

321

7. Slum rehabilitation Rehabilitate 6 million people in 10 years

978

8. Reconstruction of dilapidated buildings

Reconstruction of 10,000 old buildings

267

9. Mumbai Sewerage disposal project

Rehabilitate and augment sewerage network

322

10. Storm Water Drain project Rehabilitate and augment drain network

305

Some Major Infrastructure Projects in Mumbai (Public Funding Needed)

Transport

Opening uphinterland

Housing & otherinfrastructure

Sr. No.

PROJECTEstimated Cost (Rs in

Crores)

Approx. Estimate in USD/Euro

SCOPE

A Transport Infrastructure Projects -

1 Mumbai Trans Harbour Sea Link Project

8311 USD1843 mn orEuro 1.4billion

(8 lane road) or (6 lane road) with provision for 2 lanes of metro. Length - 22 kms. - 4

lanes of elevated road

2Mumbai Metro Rail Project -MMRP

20921USD4639 mn or

Euro3.5bn 9 corridors, 135 kms

Western Freeway

3 Worli Haji Ali Section 1950USD432 mn or

Euro 329million8 lanes, length - 3 kms.

4 Haji Ali - Nariman Point section 6000USD1331 mn or Euro 1.04billion

4 lanes, length - 9 kms - Sea bridge + Tunnel

5 Bandra - Versova section 2650USD588 mn or

Euro488 million8 lanes, length - 11 kms

6 Airport at Navi Mumbai - Phase 1 (Area 1140 Ha. Airport will have 2 parallel runways of 3.7 kms each. Designed to handle 60 m passengers per annum by 2030

4767USD1057 mn or Euro 805 million

Phase 1 will have 1 run way and 1 terminal

Projects in the Mumbai Metropolitan Region

7 Eastern Expressway 920USD 204 million or Euro 155 million

15 lanes , 19 kms

8Vasai / Virar - Alibaugh multimodal corridor -

10000USD 2218 mn or Euro 1.6billion

8 lane corridor of 140 kms length from Virar to Alibaugh with a provision of metro rail and separate lanes for buses

9 SION - PANEVL EXPRESSWAY 1838USD408 mn or Euro311million

20 lanes + 4 lanes of service roads , length 31 kms

10Development of World class station at Chhatrapati Shivaji Terminus - Central Railways

NA

CST station to be converted into a World Class station with modern facilities and commercial utilization of

space

B URBAN RENEWAL

11Dharavi Redevelopment Project - OSD, DRP

5600USD 1242 mn or Euro946 million

12Redevelopment of Nariman Point Business District and Eastern Water Front

NA

13 INNOVATION PARK in MMR OVER 5000 acres C WATER TRANSPORT

14 Western Waterways - MSRDC 1200 USD318 mn or Euro 242 million

length 45 kms15 Eastern Waterways - MMRDA 234 length 19 kms

OPPORTUNITIES FOR ITALIAN COMPANIES

Real EstateResidential (townships, skyscrapers, holiday homes, etc…) | shopping malls | educational institutes | industrial units | offices

Building equipmentsEarthmoving | Concrete equipments | Material Handling | Road construction equipments and special purpose vehicles

Construction ServicesProject management | engineering and consultancy services | quality accreditation services

Building materialsPre-cast concrete

Urban InfrastructureSolid Waste Management | Water Treatment Plants | Seawater desalination plants

InfrastructureRoad and national highways building | Road operations and maintenance (O&M), | Tunneling construction for roads and railways | ircraft maintenance, repair & overhauling (MRO) hubs, | Metro rail / Light Rail Transit (LRT) | High speed train building | Solar , minimum 1 MW farm | Wind farms | Gas based power generation modules

Indian companies are on the look out for International players with good technology and would like to explore various possibilities like joint ventures. acquisition (part or full) or commercial agreements for distributorship or license agreements. Such opportunity can be broadly classified as follow:

The Indo-Italian Chamber of Commerce and Industry