initiation of coveragecapmetals.com.au/.../uploads/2018/03/180228-canaccord-coverage.pdf ·...

TRANSCRIPT

Capricorn Metals Limited

Precious Metals - Developer/Explorer

Canaccord Genuity is the global capital markets group of Canaccord Genuity Group Inc. (CF : TSX)The recommendations and opinions expressed in this research report accurately reflect the research analyst's personal, independent and objective views about any and allthe companies and securities that are the subject of this report discussed herein.

28 February 2018

SPECULATIVE BUYPRICE TARGET A$0.18Price (28-Feb)Ticker

A$0.07CMM-ASX

52-Week Range (A$): 0.05 - 0.14Avg Daily Vol (M) : 1.0Market Cap (A$M): 56.1Shares Out. (M) : 747.9Net Debt (Cash) (A$M): (11)Enterprise Value (A$M): 45.5Cash (A$M): 10.6Long-Term Debt (A$M): 0.0NAV /Shr (A$): 0.18NAV /Shr (5%) (A$): 0.23Major Shareholders: Hawkes Point 19%

FYE Jun 2017A 2018E 2019E 2020ESales (A$M) 0.0 0.0 0.0 133.6EBITDA (A$M) (3.5) (6.0) (8.4) 58.6Net Income (A$M) (3.3) (5.9) (9.4) 48.1

EV/EBITDA (x) (14.3) (8.6) (10.9) 1.0Gold Production(000oz) 0 0 0 75

All in SustainingCost (Gold) (US$ /oz)

- - - 790

0.14

0.13

0.12

0.11

0.1

0.09

0.08

0.07

0.06

0.05

0.04

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

CMM

Source:�FactSet

Priced as of close of business 28 February 2018

CMM's key asset is the Karlawinda gold project. located inthe Pilbara region of Western Australia. A Feasibility Studycompleted in 2017 demonstrated solid development meritand with further Resource and Reserve upgrades expectedin 2018, we should see the fundamentals of the projectimprove, culminating in an update Feasibility study expectedby mid-2018.Canaccord Genuity (Australia) Limited has received a fee asthe Lead Manager and Bookrunner to the Capricorn MetalsLtd capital raising announced on 30 November 2017.

Tim McCormack | Analyst | Canaccord Genuity (Australia) Ltd. | [email protected] | +61.8.6216.2088

Initiation of Coverage

Development decision rapidly approachingCMM is one of a select few gold developers, with an Australian project sufficientlyadvanced to be at a financing decision in 2018. The company's Karlawinda project isset to release an updated Reserve and Feasibility study in 1H 2018, which in our viewwill underpin a robust 100kozpa production profile, over an 8 year mine life. While atfirst glance the Resource and Reserve of its flagship Bibra deposit looks low grade at~1.1g/t, the asset has a number of other redeeming features that drive a compellingdevelopment case. We also see considerable exploration upside across the Karlawindalandholding and CMM plans to maintain an aggressive drilling effort though 2018 tobuild on the current Resource and Reserve inventory.

Key assumptions in our modellingWhile CMM has completed a Feasibility Study outlining a ~100kozpa productionscenario at an AISC of A$1025/oz for 6.5 years, we expect the pending Reserve update(CG est. JunQ'18) to underpin a longer life project, and as such assume an ~8 yearmine life in our modelling. In funding the project development and working capitalrequirements while maintaining exploration activities, we have assumed a 50:50 debt/equity split raising a total of A$140m in the 2H of 2018. CMM currently has A$10min cash (no debt), comfortably positioning the company through to finalisation of theproject financing. At steady state (from FY20/CY19), we expect CMM to generate EBITDAof A$75-85m pa and FCF of A$50-60m pa, placing the company on undemandingmultiples. With the likes of Dacian Gold (DCN-ASX: $2.63 | SPEC BUY, A$3.75 TP | TimMcCormack), Gold Road (GOR-ASX: $0.80 | SPEC BUY, A$0.95 TP| Patrick Chang) andGascoyne Resources (GCY-ASX | Not Rated) now funded and in construction, attention isturning to who’s next in the gold development pipeline, and we see CMM as a standoutamong the greenfield peer group.

Plenty of exploration upsideCMM has an active exploration program underway, testing a mix of infill, extensional andgreenfield targets. With gold only discovered on the landholding ~10 years ago, the areais significantly under-explored, and with the geological understanding improving withevery drill hole we see considerable upside to the existing Resource and Reserve. Recentdrilling results from Portrush, Southern Corridor and Tramore prospects all point towardsfurther growth in close proximity to the existing Bibra Resource/Reserve, and moreregionally, the company plans to test K3 and Francopan which have historic intersectionsunder sand cover.

Valuation and recommendationOur A$0.18/sh price target is based on an NPV10% for the Karlawinda gold project, netof corporate and other adjustments. We have also assumed A$70m in equity raised tocomplete the funding for the project (50:50 debt/equity) and our valuation is diluted toaccount for these assumptions. With very few Australian gold projects with >100kozpascale in the development pipeline, we expect CMM to demand increasing attention fromthe market as it moves towards a development decision in the 2H 2018.

For important information, please see the Important Disclosures beginning on page 20 of this document.

2

FINANCIAL SUMMARY Capricorn Metals ASX:CMM

Analyst: Tim McCormack Rating:

Date: 28/02/2018 Target Price: $0.18

Year End: June

Market Information Company Description

Share Price A$ 0.08

Market Capitalisation A$m 56.8

12 Month Hi A$ 0.14

12 Month Lo A$ 0.05

Average daily turnover (3 month) m 1.133

Issued Capital m 747.94 Profit & Loss (A$m) 2017a 2018e 2019e 2020e

Options m 56.70 Revenue 0.2 0.0 0.0 133.6

Fully Diluted for ITM options m 747.94 Operating Costs 0.0 0.0 0.0 -61.4

Royalties 0.0 0.0 0.0 -3.3

Valuation diluted for funding A$m A$/share Corporate & O'heads -3.1 -4.0 -7.8 -7.2

Karlawinda NPV @ 10% 212.7 0.13 Exploration (Expensed) -0.6 -2.0 -0.6 -3.0

Exploration & Projects 30.0 0.02 EBITDA -3.5 -6.0 -8.4 58.6

Corporate (26.6) (0.02) Dep'n 0.0 0.0 0.0 -7.5

Forwards (inc spot deferred) - - EBIT -3.5 -6.0 -8.4 51.1

Cash & Bullion 10.6 0.01 Net Interest 0.2 0.1 -1.0 -3.0

Future Equity Raised 70.0 0.04 Tax 0.0 0.0 0.0 0.0

Debt - - NPAT -3.3 -5.9 -9.4 48.1

Unpaid Capital - - Abnormals 0.0 0.0 0.0 0.0

TOTAL NAV 296.7 0.18 NPAT (reported) -3.3 -5.9 -9.4 48.1

Price:NAV 0.42x

NAV at Spot US$1,318/oz, AUDUSD $0.78 0.14 Cash Flow (A$m) 2017a 2018e 2019e 2020e

Target Price 0.18 Cash Receipts 0.0 0.0 0.0 133.6

Cash paid to suppliers & employees -1.9 -4.0 -7.8 -72.0

Assumptions 2017a 2018e 2019e 2020e Tax Paid 0.0 0.0 0.0 0.0

Gold Price (US$/oz) 1,257 1,309 1,349 1,384 Net Interest 0.1 0.1 -1.0 -3.0

AUD:USD 0.752 0.796 0.793 0.787 Operating Cash Flow -1.8 -3.9 -8.8 58.6

Gold Price (A$/oz) 1,672 1,644 1,703 1,759 Exploration and Evaluation -12.4 -6.0 -6.0 -6.0

Capex 0.0 0.0 -95.0 -43.0

Valuation Sensitivity Other -1.5 0.0 0.0 0.0

Investing Cash Flow -13.9 -6.0 -101.0 -49.0

Debt Drawdown (repayment) 0.0 0.0 70.0 -15.0

Share capital 10.2 9.0 70.0 0.0

Dividends 0.0 0.0 0.0 0.0

Financing Expenses -0.5 0.0 0.0 0.0

Others -0.1 0.0 0.0 0.0

Financing Cash Flow 9.5 9.0 140.0 -15.0

Opening Cash 11.8 5.5 4.7 34.9

Increase / (Decrease) in cash -6.2 -0.9 30.2 -5.4

FX Impact 0.0 0.0 0.0 0.0

Production Metrics 2017a 2018e 2019e 2020e Closing Cash 5.5 4.7 34.9 29.5

Gold production (koz) 0 0 0 75 Balance Sheet (A$m) 2017a 2018e 2019e 2020e

AISC (A$/oz) 0 0 0 1,003 Cash + S/Term Deposits 5.5 4.7 34.9 29.5

Other current assets 5.3 0.0 0.4 44.2

Resources & Reserves Mt Grade Moz Current Assets 10.9 4.7 35.3 73.7

Resources Property, Plant & Equip. 0.4 0.4 95.4 130.8

Measured 8.3 1.3 0.33 Exploration & Develop. 20.7 20.7 26.1 29.1

Indicated 22.6 1.1 0.77 Other Non-current Assets 0.0 0.0 0.0 0.0

Inferred 7.3 1.0 0.23 Payables 1.3 0.1 0.1 10.7

Total 38.2 1.1 1.33 Short Term debt 0.0 0.0 15.0 20.0

Long Term Debt 0.0 0.0 55.0 35.0

Reserves Other Liabilities 0.5 -7.5 -7.2 26.0

Proved 0.0 0.00 0.0 Net Assets 30.1 33.2 93.9 141.9

Probable 21.0 1.06 0.71 Shareholders Funds 42.1 51.1 121.1 121.1

Reserves 21.0 1.06 0.72 Reserves 2.3 2.3 2.3 2.3

Retained Earnings -14.3 -20.2 -29.6 18.5

Directors & Management Total Equity 30.1 33.2 93.9 141.9

Name Position

Heath Hellewell Executive Chairman Ratios & Multiples 2017a 2018e 2019e 2020e

Stuart Pether Non-Executive Director EBITDA Margin nm nm nm 44%

Peter Langworthy Non-Executive Director EV/EBITDA nm nm nm 2.5x

Debra Bakker Non-Executive Director Op. Cashflow/Share nm nm nm $0.04

Peter Thompson Chief Operating Officer P/CF nm nm nm 2.1x

Jonathon Shellabear Chief Financial Officer EPS nm nm nm $0.03

EPS Growth nm nm nm nm

Substantial Shareholders % PER nm nm nm 2.6x

Hawke's Point 19.0% Dividend Per Share $0.00 $0.00 $0.00 $0.00

Centrepeak Resources Group 6.0% Dividend Yield 0% 0% 0% 0%

ROE -11% -18% -10% 34%

ROIC -8% -12% -5% 33%

Debt/Equity 0% 0% 59% 25%

Net Interest Cover nm nm -3.9x 15.3x

Book Value/share $0.05 $0.04 $0.06 $0.09

Price/Book Value 1.4x 1.7x 1.3x 0.9x

Source: C MM & C anaccord Genuity estimates EV/FCF nm nm nm 5.9x

CMM's key asset is the Karliwinda gold project, located in the Pilbara region of Western Australia.

A Feasibilty Study completed in 2017 demonstrated solid development merit and with expected

Resource and Reserve upgrades this year, we should see the projects fundermentals improve

in the 1H 2018. We see the project supporting a ~100kozpa production profile for 8 years, and

expect to see a developmet decsion in the 2H 2018.

SPEC BUY

$0.00

$0.10

$0.20

$0.30

-15% -10% -5% 0% 5% 10% 15%

Gold Price US$ Exchange Rate

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 2

3

Valuation

We have based our A$0.18/sh valuation for CMM on a DCF analysis (forward

curve NPV10%) of the Karlawinda gold project. Our modelling has incorporated a

larger Reserve than outlined in the 2017 Feasibility Study, which reflects the

recent Resource upgrade and subsequent drilling programs. We expect to see the

update Reserve in the JunQ’18, which in our view will provide an adequate

platform to finance the project. Our valuation assumes first gold production by

late 2019, with the project forecast to produce ~100kozpa at an AISC of

A$1,050/oz for 8 years.

Figure 1 highlights the sum of parts comprising our A$0.18/sh valuation. On a per

share basis, we have diluted for assumed future equity raisings of A$70m

(A$0.08/sh) in the 1H FY19. This implies that 1.6bn shares (currently 748m) will

be on issued on a diluted basis.

Figure 1: Sum-of-parts valuation for CMM

Source: Canaccord Genuity estimates

In deriving our valuation we utilise forward curve pricing assumptions for gold and

FX. The key inputs are shown in Figure 2.

Figure 2: Gold price and FX assumptions

Source: Canaccord Genuity estimates

Figure 3 demonstrates our forecast production and AISC profile for the Karlawinda

gold project. We have assumed ore being processed at a stand-alone processing

facility at a rate of 3Mtpa (slightly higher in first two years), with ore sourced from

the Bibra open pit. In deriving our 8-year production profile, we have assumed a

Resource to Reserve conversion of 65% for the Bibra pit, which implies the

current Reserve increasing from 713koz to ~850koz at the next update. We

assume a production rate of ~100kozpa at an AISC ~A$1,050/oz in our

modelling, with the highest margin year’s front ended with the addition of higher

grade (~1.4g/) laterite ore in the mine plan.

Valuation diluted for funding A$m A$/share

Karlawinda NPV @ 10% 212.7 0.13

Exploration & Projects 30.0 0.02

Corporate (26.6) (0.02)

Forwards (inc spot deferred) - -

Cash & Bullion 10.6 0.01

Future Equity Raised 70.0 0.04

Debt - -

Unpaid Capital - -

TOTAL NAV 296.7 0.18

Price:NAV 0.42x

NAV at Spot US$1,318/oz, AUDUSD $0.78 0.14

Target Price 0.18

Assumptions 2017a 2018e 2019e 2020e 2021e 2022e 2023e LT (2024)

Gold Price (US$/oz) 1,254 1,307 1,349 1,384 1,419 1,451 1,487 1,498

AUD:USD 0.75 0.80 0.79 0.79 0.78 0.78 0.78 0.78

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 3

4

Figure 3: Assumed LOM production profile and AISC profile for Karlawinda

Source: Canaccord Genuity estimates

Key sensitivities to our valuation relate to gold price and currency fluctuations

which can be seen in Figure 4. At spot prices (US$1339/oz A$:US$ 0.79) our

valuation drops to A$0.14/sh, which still offers a healthy 45% potential upside.

We also note the sensitivity to discount rate also, which at 5% (standard once in

production) would increase the valuation to A$0.23/sh.

Figure 4: Sensitivity analysis to gold price and currency movements

Source: Canaccord Genuity estimates

Development Strategy

We have assumed CMM develops the Karlawinda gold project on a stand-alone

basis, completing construction of a 3Mtpa Carbon-in-Leach (CIL) processing plant

in the 2H 2019. LOM baseload ore supply is expected to come from the Bibra

open pit, and we have assumed the grade averaging 1.05g/t, slightly higher in the

initial years, with the inclusion of ~67koz of laterite ore at 1.4g/t. Our assumed

mine life of 8 years should be validated when the company updates the existing

713koz Reserve in the JunQ’18.

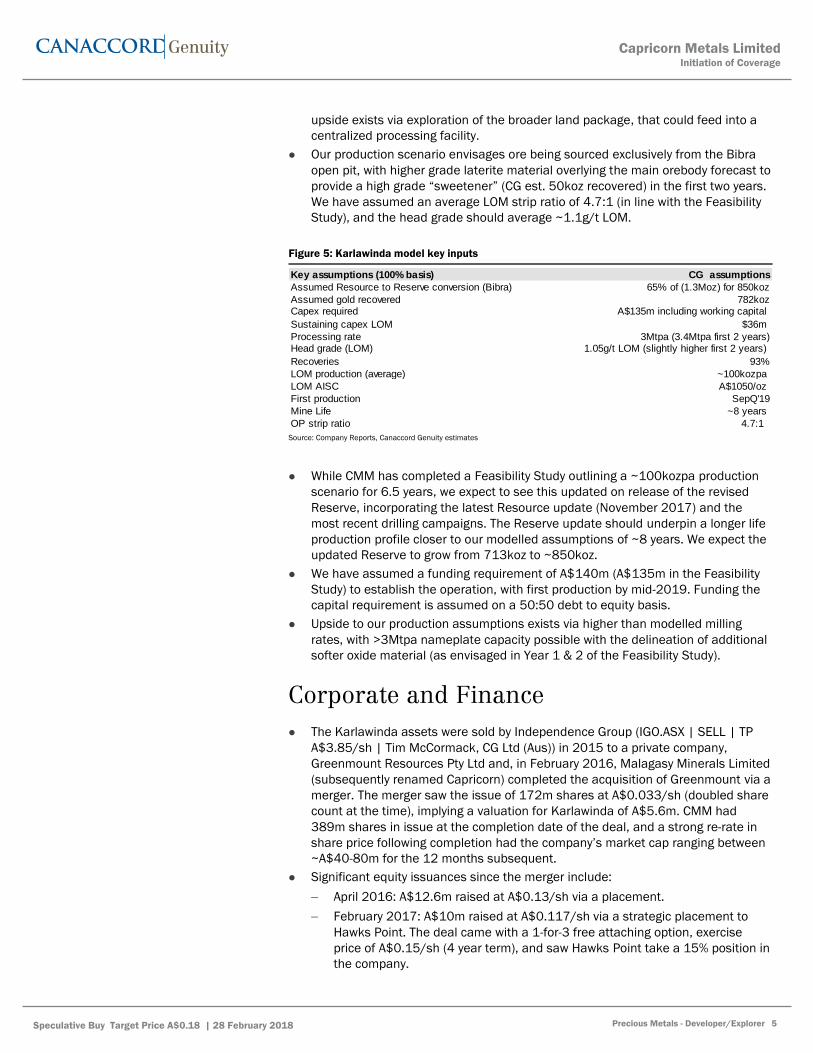

Key inputs are outlined in Figure 5, which support a ~100kozpa operation at an

average AISC of A$1,050/oz. We note that the company plans to re-optimize the

2017 Feasibility Study on the back of the upcoming Bibra Reserve update, and we

will refine our assumptions as new information becomes available. As a starting

point however, we view our current inputs as robust and believe that further

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 4

5

upside exists via exploration of the broader land package, that could feed into a

centralized processing facility.

Our production scenario envisages ore being sourced exclusively from the Bibra

open pit, with higher grade laterite material overlying the main orebody forecast to

provide a high grade “sweetener” (CG est. 50koz recovered) in the first two years.

We have assumed an average LOM strip ratio of 4.7:1 (in line with the Feasibility

Study), and the head grade should average ~1.1g/t LOM.

Figure 5: Karlawinda model key inputs

Source: Company Reports, Canaccord Genuity estimates

While CMM has completed a Feasibility Study outlining a ~100kozpa production

scenario for 6.5 years, we expect to see this updated on release of the revised

Reserve, incorporating the latest Resource update (November 2017) and the

most recent drilling campaigns. The Reserve update should underpin a longer life

production profile closer to our modelled assumptions of ~8 years. We expect the

updated Reserve to grow from 713koz to ~850koz.

We have assumed a funding requirement of A$140m (A$135m in the Feasibility

Study) to establish the operation, with first production by mid-2019. Funding the

capital requirement is assumed on a 50:50 debt to equity basis.

Upside to our production assumptions exists via higher than modelled milling

rates, with >3Mtpa nameplate capacity possible with the delineation of additional

softer oxide material (as envisaged in Year 1 & 2 of the Feasibility Study).

Corporate and Finance

The Karlawinda assets were sold by Independence Group (IGO.ASX | SELL | TP

A$3.85/sh | Tim McCormack, CG Ltd (Aus)) in 2015 to a private company,

Greenmount Resources Pty Ltd and, in February 2016, Malagasy Minerals Limited

(subsequently renamed Capricorn) completed the acquisition of Greenmount via a

merger. The merger saw the issue of 172m shares at A$0.033/sh (doubled share

count at the time), implying a valuation for Karlawinda of A$5.6m. CMM had

389m shares in issue at the completion date of the deal, and a strong re-rate in

share price following completion had the company’s market cap ranging between

~A$40-80m for the 12 months subsequent.

Significant equity issuances since the merger include:

April 2016: A$12.6m raised at A$0.13/sh via a placement.

February 2017: A$10m raised at A$0.117/sh via a strategic placement to

Hawks Point. The deal came with a 1-for-3 free attaching option, exercise

price of A$0.15/sh (4 year term), and saw Hawks Point take a 15% position in

the company.

Key assumptions (100% basis) CG assumptions

Assumed Resource to Reserve conversion (Bibra) 65% of (1.3Moz) for 850koz

Assumed gold recovered 782kozCapex required A$135m including working capital

Sustaining capex LOM $36m

Processing rate 3Mtpa (3.4Mtpa first 2 years)Head grade (LOM) 1.05g/t LOM (slightly higher first 2 years)

Recoveries 93%

LOM production (average) ~100kozpa

LOM AISC A$1050/oz

First production SepQ'19

Mine Life ~8 years

OP strip ratio 4.7:1

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 5

6

November 2017: A$9m raised at A$0.052/sh via a placement (A$7m) and

Share Purchase Plan (A$2m)

CMM currently has 747.9m shares on issue and a cash position of ~A$10m. A

summary of the current capital structure can be seen below.

Figure 6: Capital structure of CMM

Source: Company Reports

The shareholder register is institutionally light at this stage, with the exception of

Hawkes Point (19%), which originally came onto the register in early 2017 via a

placement. Hawkes Point has maintained its position through subsequent

placements and the latest change of substantial holding filings indicates ongoing

buying in the market to its current position. Directors and Management account

for ~11%, with the lion share held by Centrepeak, an investment vehicle of which

Executive Chairman Heath Hellewell is a Director and Shareholder. As the

company moves towards production, we expect the register to transition away

from the predominantly retail holders (~50%) to a more institutional shareholder

base.

Figure 7: Major shareholders in CMM

Source: Company Reports

The company has progressed its Karlawinda project aggressively since

acquisition, spending ~A$20 on drilling and development studies. This has been

reflected in the doubling of the Resource base and delineation of a maiden

Reserve on Bibra, with the project set to be at a financing decision within 2.5

years from purchase.

We estimate CMM to have a cash position of ~A$10m currently, having raised

A$9m at A$0.052/sh in November 2017. In our view, the company is adequately

financed through to completion of an Optimised Feasibly Study (CG est. JunQ’18)

while maintaining an aggressive exploration program.

In funding the project development and working capital requirements while

maintaining exploration activities, we have assumed a 50:50 debt/equity split

raising a total of A$140m. While we don’t have clear line of sight on the borrowing

capacity of CMM, the project’s relatively long Reserve tail (which we expect to

grow to 8 years), coupled with higher FCF in the first two years of production

should make access to debt markets achievable on favorable terms. Our valuation

is sensitive to an increased debt position, which could present some upside to our

valuation. By way of example, a 70:30 debt equity split would increase our

valuation to A$0.22/sh, or if the project was entirely debt funded the valuation

would be A$0.29/sh.

Issued capital Ticker Number Expiry/Strike

Ordinary Shares CMM 748

Options CMMAA 11 Expiry 31/05/2020 @ A$0.20

Options CMMAB 7 Expiry 31/05/2020 @ A$0.20

Options CMMAC 29 Expiry 05/05/2021 @ A$0.15

Options Unlisted 9 Expiry 05/05/2021 @ A$0.15

Options Unlisted 1 Expiry 23/11/2021 @ A$0.088

Fully diluted 805

Major shareholders

Hawkes Point 19%

Directors and Management 11%

Retail 53%

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 6

7

In Figure 8, we demonstrate the EBITDA, FCF and net cash build over the

assumed mine life. At steady state (from FY20/CY19), we estimate CMM should

generate an average EBITDA of A$75-85m pa and FCF of A$50-60m pa.

Figure 8: Forecast EBITA, FCF and net cash over the assumed mine life

Source: Company Reports, Canaccord Genuity estimates

Board and management

The CMM Board and management team possess a good cross-section of skill sets,

and are capable of delivering the project, in our view. Key board and management

members are outlined below:

Heath Hellewell – Executive Chairman

Mr Hellewell is an exploration geologist with over 22 years of experience in gold,

base metals and diamond exploration predominantly in Australia and West Africa.

Mr Hellewell has previously held senior exploration positions with a number of

successful mining and exploration groups including DeBeers Australia Pty Ltd,

Resolute Mining Limited and Independence Group NL.

Most recently he was the co-founding Executive Director of Doray Minerals

Limited, where he was responsible for the Company’s exploration and new

business activities. Following the discovery of the Andy Well gold deposits in

2010, Doray Minerals was named “Gold Explorer of the Year” in 2011 by The Gold

Mining Journal and in 2014 Heath was the co-winner of the prestigious

“Prospector of the Year” award, presented by the Association of Mining and

Exploration Companies.

Mr Hellewell is currently an independent Non-Executive Director of Core

Exploration Ltd (CXO.ASX) and Duketon Mining Limited (DKM.ASX).

Peter Langworthy – Non-Executive Director

Peter Langworthy is a geologist with a career spanning 31 years in mineral

exploration and project development in Australia, Indonesia and Africa. His

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 7

8

industry experience includes 12 years in senior management roles with WMC

Resources, four years with PacMIn Mining as Exploration Manager, five years with

Jubilee Mines where he built the team responsible for numerous discoveries at

the Cosmos Nickel Mine and the Sinclair nickel project, and three years with

Talisman Mining as Technical Director.

Peter was a Director of Malagasy Minerals Ltd from 2013 which was the precursor

to CMM. Mr Langworthy is a Non-Executive chairman of Syndicated Metals Limited

(March 2012 to present) and Non-Executive Director of Silver Mines Ltd (June

2016 to present).

Stuart Pether – Non-Executive Director

Stuart Pether has over 25 years resources industry experience in project

development, technical studies, mine operations and corporate management. He

is equally skilled in open pit and underground mining in a range of commodities

including gold, nickel and lead and zinc. A qualified mining engineer, he holds a

Bachelor in Engineer (Mining Engineering) from the Western Australia School of

Mines.

Stuart was previously the Chief Executive Officer for Kula Gold and held the

position of Chief Operating Officer at Catalpa Resources where he was responsible

for the construction, commissioning and operation of the A$92m Edna May Gold

project. Following the merger of Catalpa Resources with Conquest Mining in

November 2011, to form Evolution Mining, he took up the position of Vice

President, Project Development where he was responsible for technical studies

and major capital projects, including the construction of the $140m Mt Carlton

Gold Project in Queensland.

Prior, he worked in various mining management roles for CBH Resources, PacMin

Mining Limited, Dominion Mining and Western Mining Corporation.

Debra Bakker – Non-Executive Director

Ms Bakker is an experienced financier with over 25 years’ experience in the

resource industry internationally, including as a senior banker, financier and

advisor to listed mining companies. She previously held senior positions with the

Commonwealth Bank of Australia, Standard Bank London Group and Barclays

Capital. In her role with the Commonwealth Bank, Ms Bakker established and led

the Natural Resources Division based in Western Australia for over 10 years.

Debra is currently a non-executive director of mid-tier base metals miner

Independence Group NL, a non-executive director at not-for-profit organisation

Access Housing Australia, and the Western Australian representative at Auramet

Trading LLC, a New York-based metals trading firm specialising in precious metals

and metals hedging.

Jonathon Shellabear – Chief Financial Officer

Jonathan Shellabear has over 25 years’ experience in the Australian and

international resources industry as a senior corporate executive and investment

banker specialising in the mining sector. Mr Shellabear holds a Bachelor of

Science with Honours in Geology and a Master in Business Administration from

the University of Western Australia.

He has extensive capital markets and advisory experience in the resources sector

and has held senior investment banking positions with NM Rothschild & Sons,

Deutsche Bank and Resource Finance Corporation.

Jonathan was previously the Managing Director and Chief Executive Officer of

Dominion Mining Ltd which was acquired by Kingsgate Consolidated Ltd in 2011.

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 8

9

He has also held senior corporate roles with Portman Limited (now Cliffs Natural

Resources) as General Manager, Business Development and Heron Resources Ltd

as Managing Director and Chief Executive Officer.

Peter Thompson – Chief Operating Officer

Mr Thompson trained as a geologist in Trinity College Dublin and Leicester

University, he came to Australia in 1988 and has had a continuous career in

exploration and mining for gold, nickel and copper.

Employed by WMC, Anaconda Nickel, Jubilee Mines, St Barbara Ltd, Beaconsfield

Gold and Central Asia Resources in a range of roles, he has overseen several

discoveries, project developments, feasibility studies, acquisitions, divestments

and company start-ups.

Recent responsibilities as CEO of Beaconsfield Resources and Central Asia

Resources have been for operating deep underground gold and heap leach start-

up operations. Currently a non-executive director of Central Asia Resources Ltd

and Marmota Energy Ltd.

Michael Martin – Chief Geologist

Mr Martin has 18 years’ experience in all aspects of resource projects through

Western Australia and Queensland. Prior to joining Capricorn Metals, Mr Martin

has held senior positions at Pacmin, Sons of Gwalia, Sipa Resources, Jubilee

Mines, Xstrata, Talisman Mining and Syndicated Metals. With these companies he

has undertaken a variety of senior and leadership roles in mineral exploration,

resource development, resource estimation and mining in multiple commodities

such as gold, nickel, copper, lead and zinc. Mr Martin graduated from the

University of Ballarat with an Honours Degree in Geology and is a member of the

Australian Institute of Geoscientists (AIG).

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 9

10

Peer Comparisons

A key observation of the gold companies under coverage is the lack of valuation

upside among the larger cap (+A$1bn) steady state producers, with EVN, NST,

OGC, SAR, SBM and RRL currently trading on an average P/NAV of 1.0x.

Conversely, at the smaller end of the sector, the pipeline of new gold projects,

those not funded and in construction, is largely void of options with the exception

of Echo Resources (EAR.ASX | SPEC BUY | PT: A$0.50/sh |Tim McCormack). In

our view this positions CMM well, as it moves towards a funding decision in the

2H 2018.

The company screens well on a number of metrics as demonstrated in the charts

below.

Figure 9: Strip ratio and grade vs similar development assets Figure 10: Capital intensity vs peer projects

Source: Company Reports, Canaccord Genuity estimates Source: Company Reports, Canaccord Genuity estimates

Figure 11: Production vs AISC of peers in development Figure 12: EV/Resource & Reserve of peer projects

Source: Company Reports, Canaccord Genuity estimates Source: Company Reports, Canaccord Genuity estimates

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 10

11

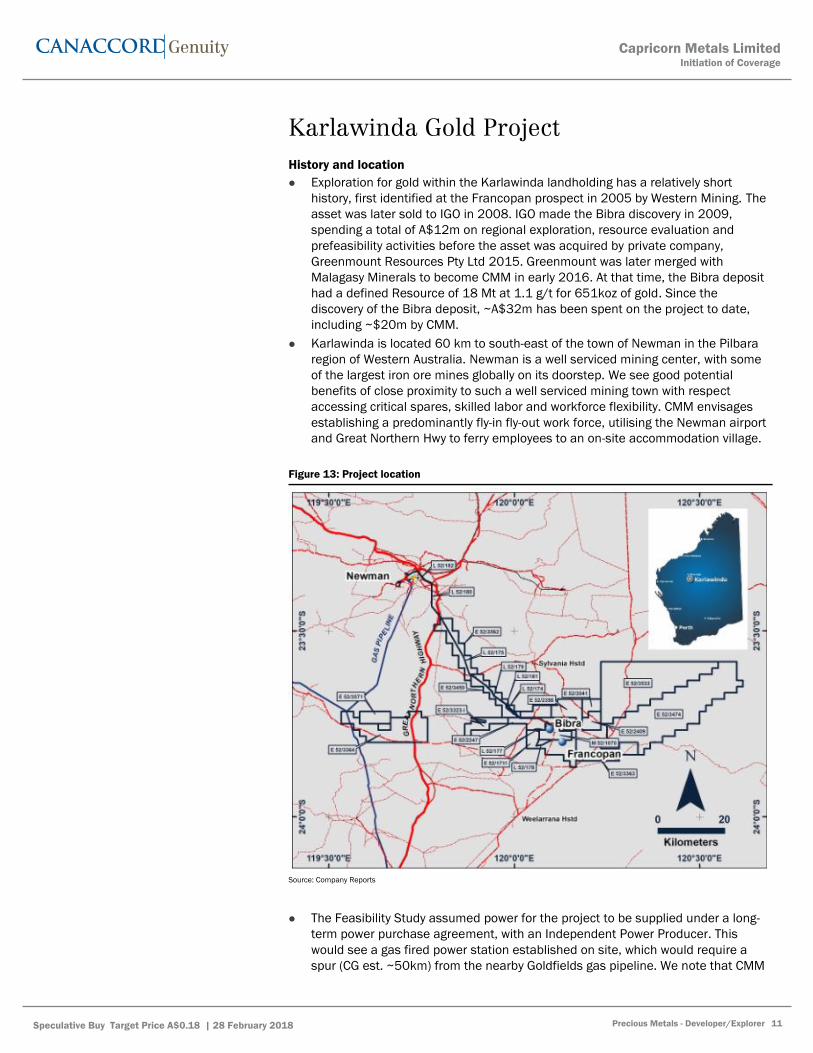

Karlawinda Gold Project

History and location

Exploration for gold within the Karlawinda landholding has a relatively short

history, first identified at the Francopan prospect in 2005 by Western Mining. The

asset was later sold to IGO in 2008. IGO made the Bibra discovery in 2009,

spending a total of A$12m on regional exploration, resource evaluation and

prefeasibility activities before the asset was acquired by private company,

Greenmount Resources Pty Ltd 2015. Greenmount was later merged with

Malagasy Minerals to become CMM in early 2016. At that time, the Bibra deposit

had a defined Resource of 18 Mt at 1.1 g/t for 651koz of gold. Since the

discovery of the Bibra deposit, ~A$32m has been spent on the project to date,

including ~$20m by CMM.

Karlawinda is located 60 km to south-east of the town of Newman in the Pilbara

region of Western Australia. Newman is a well serviced mining center, with some

of the largest iron ore mines globally on its doorstep. We see good potential

benefits of close proximity to such a well serviced mining town with respect

accessing critical spares, skilled labor and workforce flexibility. CMM envisages

establishing a predominantly fly-in fly-out work force, utilising the Newman airport

and Great Northern Hwy to ferry employees to an on-site accommodation village.

Figure 13: Project location

Source: Company Reports

The Feasibility Study assumed power for the project to be supplied under a long-

term power purchase agreement, with an Independent Power Producer. This

would see a gas fired power station established on site, which would require a

spur (CG est. ~50km) from the nearby Goldfields gas pipeline. We note that CMM

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 11

12

has other optionality here given the proximity to Newman, and is investigating the

potential for accessing reticulated power from Alinta’s 210MW gas-fired power

station at Newman.

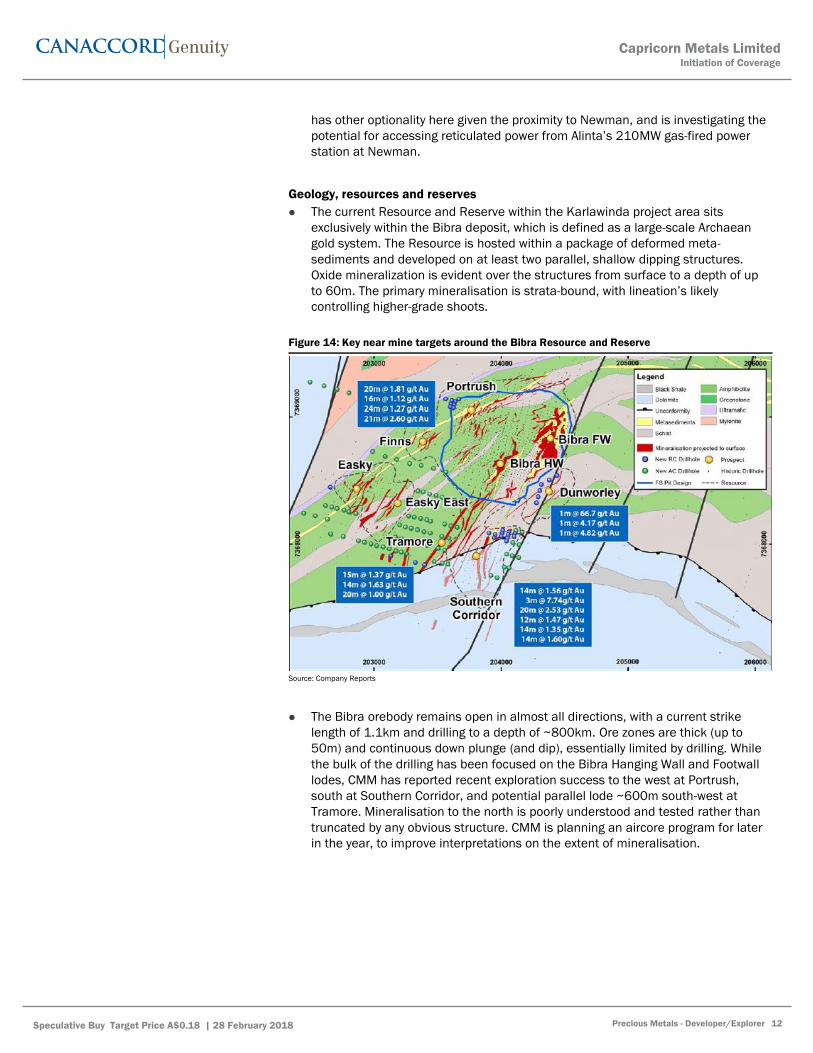

Geology, resources and reserves

The current Resource and Reserve within the Karlawinda project area sits

exclusively within the Bibra deposit, which is defined as a large-scale Archaean

gold system. The Resource is hosted within a package of deformed meta-

sediments and developed on at least two parallel, shallow dipping structures.

Oxide mineralization is evident over the structures from surface to a depth of up

to 60m. The primary mineralisation is strata-bound, with lineation’s likely

controlling higher-grade shoots.

Figure 14: Key near mine targets around the Bibra Resource and Reserve

Source: Company Reports

The Bibra orebody remains open in almost all directions, with a current strike

length of 1.1km and drilling to a depth of ~800km. Ore zones are thick (up to

50m) and continuous down plunge (and dip), essentially limited by drilling. While

the bulk of the drilling has been focused on the Bibra Hanging Wall and Footwall

lodes, CMM has reported recent exploration success to the west at Portrush,

south at Southern Corridor, and potential parallel lode ~600m south-west at

Tramore. Mineralisation to the north is poorly understood and tested rather than

truncated by any obvious structure. CMM is planning an aircore program for later

in the year, to improve interpretations on the extent of mineralisation.

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 12

13

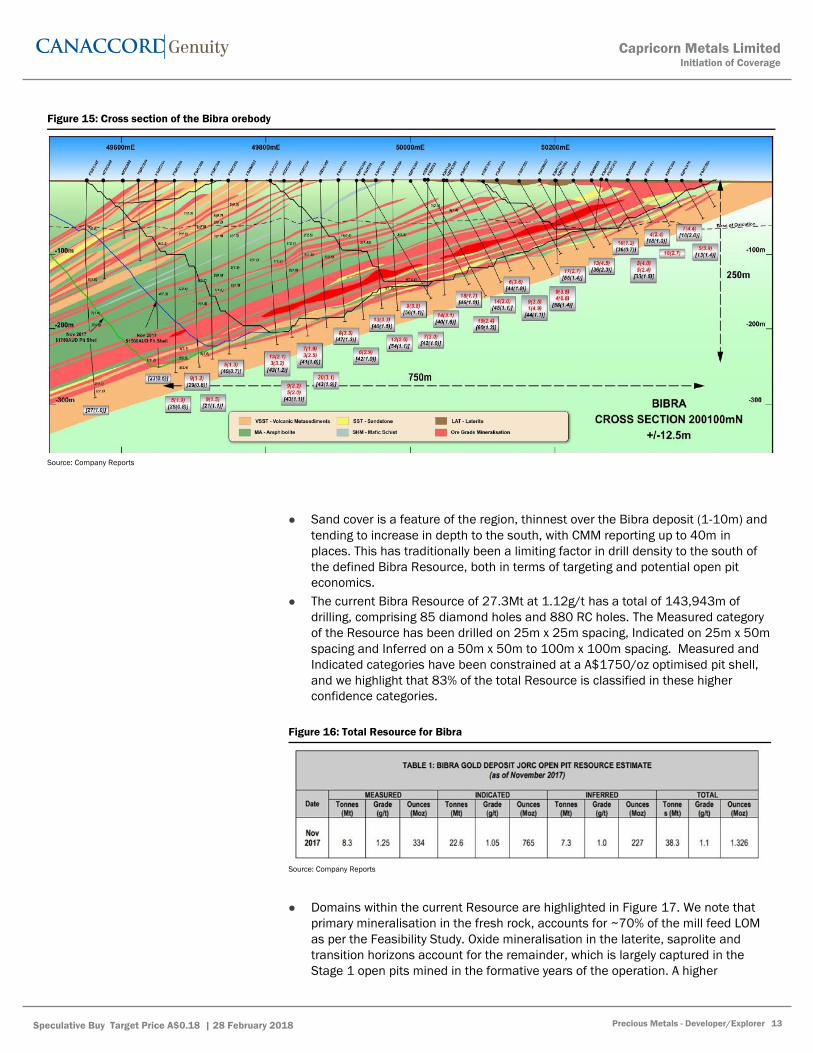

Figure 15: Cross section of the Bibra orebody

Source: Company Reports

Sand cover is a feature of the region, thinnest over the Bibra deposit (1-10m) and

tending to increase in depth to the south, with CMM reporting up to 40m in

places. This has traditionally been a limiting factor in drill density to the south of

the defined Bibra Resource, both in terms of targeting and potential open pit

economics.

The current Bibra Resource of 27.3Mt at 1.12g/t has a total of 143,943m of

drilling, comprising 85 diamond holes and 880 RC holes. The Measured category

of the Resource has been drilled on 25m x 25m spacing, Indicated on 25m x 50m

spacing and Inferred on a 50m x 50m to 100m x 100m spacing. Measured and

Indicated categories have been constrained at a A$1750/oz optimised pit shell,

and we highlight that 83% of the total Resource is classified in these higher

confidence categories.

Figure 16: Total Resource for Bibra

Source: Company Reports

Domains within the current Resource are highlighted in Figure 17. We note that

primary mineralisation in the fresh rock, accounts for ~70% of the mill feed LOM

as per the Feasibility Study. Oxide mineralisation in the laterite, saprolite and

transition horizons account for the remainder, which is largely captured in the

Stage 1 open pits mined in the formative years of the operation. A higher

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 13

14

proportion of laterite and saprolite has a two-fold impact benefit on the economics

of the project, due to higher grade and the softer nature of the ore allowing ~15%

higher through-put when processed.

Figure 17: Total gold Resource by domain

Source: Company Reports

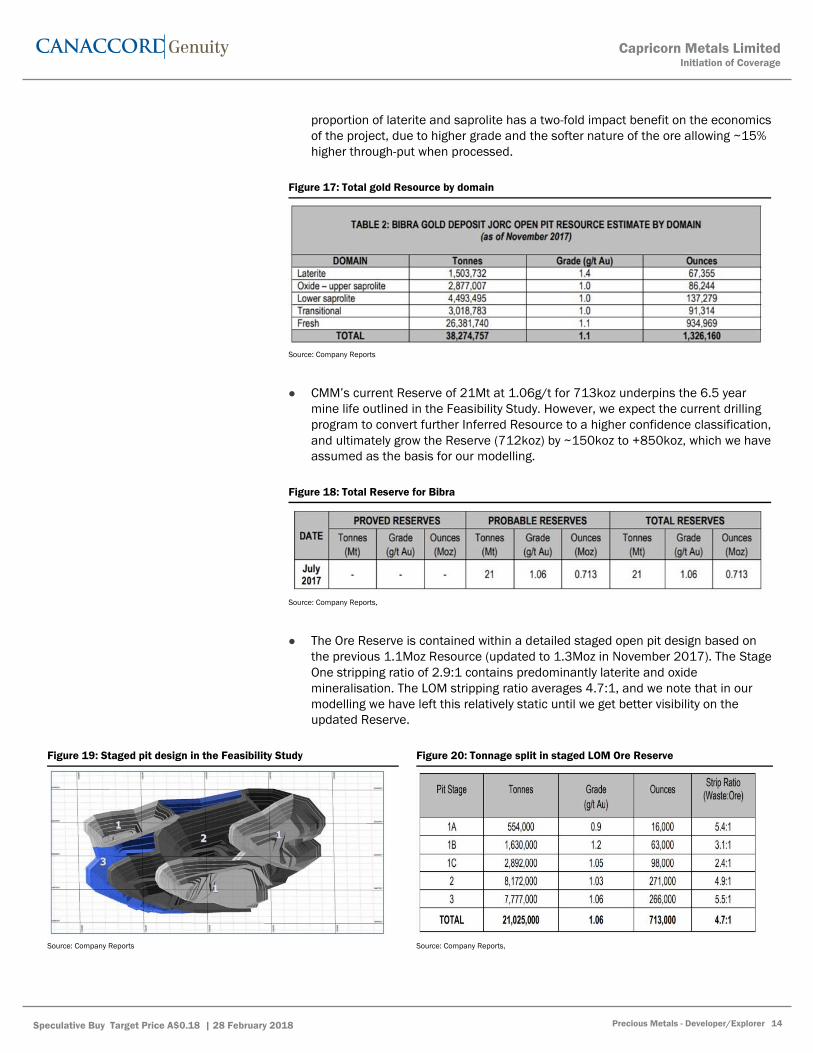

CMM’s current Reserve of 21Mt at 1.06g/t for 713koz underpins the 6.5 year

mine life outlined in the Feasibility Study. However, we expect the current drilling

program to convert further Inferred Resource to a higher confidence classification,

and ultimately grow the Reserve (712koz) by ~150koz to +850koz, which we have

assumed as the basis for our modelling.

Figure 18: Total Reserve for Bibra

Source: Company Reports,

The Ore Reserve is contained within a detailed staged open pit design based on

the previous 1.1Moz Resource (updated to 1.3Moz in November 2017). The Stage

One stripping ratio of 2.9:1 contains predominantly laterite and oxide

mineralisation. The LOM stripping ratio averages 4.7:1, and we note that in our

modelling we have left this relatively static until we get better visibility on the

updated Reserve.

Figure 19: Staged pit design in the Feasibility Study Figure 20: Tonnage split in staged LOM Ore Reserve

Source: Company Reports Source: Company Reports,

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 14

15

A significant amount of drilling along strike, down dip and down plunge of the

Bibra Resource has been completed and ongoing since the Feasibility Study, and

we see good potential for positive Resource and Reserve growth. Recent results

are a mix of infill and extensional drilling, but outcomes on both fronts are

supportive of further growth across the landholding.

Southern Corridor (largely infill)

14m @ 1.56g/t Au from 42m (KBRC1082)

3m @ 7.74g/t Au from 54m (KBRC1084)

20m @ 2.53g/t Au from 38m (KBRC1092)

12m @ 1.47g/t Au from 41m (KBRC1097)

14m @ 1.35g/t Au from 60m (KBRC1098)

14m @ 1.60g/t Au from 83m (KBRC1099)

Portrush-Bibra Hanging wall (testing down-dip extensions to Resource)

20m @ 1.81g/t Au from 86m (KBRC1053)

16m @ 1.12g/t Au from 98m (KBRC1054)

24m @ 1.27g/t Au from 88m (KBRC1055)

21m @ 2.60g/t Au from102m (KBRC1056)

Dunworely prospect (early stage footwall target)

1m @ 66.7g/t Au from 112m end of hole (KBRC1074)

1m @ 4.17g/t Au from 66m (KBRC1075)

1m @ 4.82g/t Au from 94m end of hole (KBRC1076)

CMM has also recently reported (25 January 2018) encouraging exploration

results at the Tramore prospect, 600m south of Bibra. Shallow gold mineralisation

over a strike length of >600m has been traced in the RC drilling program and is

coincident with a modeled magnetic anomaly. Mineralisation is interpreted to be

the southern extension of the Main Footwall Lode, which we highlight as

comprising ~60% of the total Bibra Resource. Better RC results from the program

include:

15m @ 1.37g/t Au from 88m (KBRC1060)

14m @ 1.63g/t Au from 184m (KBRC1061)

20m @ 1.00g/t Au from 49m (KBRC1069)

7m @ 1.79g/t Au from 143m (KBRC022)

20m @ 1.20g/t Au from 155m (KBRC148)

11m @ 1.65g/t Au from 220m (KBRC145)

12m@ 1.48g/t Au from 316m (KBRC021)

Exploration efforts since the Bibra discovery (both under IGO and CMM ownership)

have been focused on within close proximity (<2km) to the deposit), and very little

regional drilling has been done. CMM is planning to test the K3 and Francopan

prospects (~5km south east of Bibra), with a view to better understanding the

regional mineralisation controls and relationship to gold at Bibra. Limited broad

spaced drilling beneath the cover sequence has intersected broad zones of

mineralization containing narrower higher-grade intervals.

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 15

16

We also note that a drilling grant through the WA State Government EIS program

was won in late-2017. The funding provides CMM with A$200k towards direct

drilling costs and was awarded on the basis of drilling up to a 1km stratigraphic

diamond hole to test the stratigraphic succession and a series of possible major

structural controls that host the Bibra mineralised system. This hole has recently

started and will be the deepest drilled into the project, with results expected in 4-6

weeks.

Mining, processing and support infrastructure

As Karlawinda is a proposed greenfield development, no infrastructure or services

exist at the project site. The Feasibility Study outlined a total capital cost of

A$146.3m (including A$13.1m contingency) to construct a 3Mtpa processing

plant, project infrastructure and owner’s costs. We note that the CMM has also

proposed an owner-operator mining fleet, which is assumed to be financed under

a standard equipment lease agreement. Capital cost estimates in the Feasibility

Study are to an accuracy level of +/-15% with a 90% level of confidence.

Figure 21: Capital cost estimates

Source: Company Reports

The Karlawinda process plant has been designed to treat 3Mtpa of primary ore,

producing an average of ~100kozpa of gold. We note that during the initial two

years of the operation, while laterite and oxide material are more pronounced in

the blend, it is envisaged the plant will sustain a run rate of ~3.75Mtpa (CG model

3.4Mt). Redundancy has been built into the ultimate plant design to deal with the

higher tonnages.

As part of the Feasibility Study, a number of “best fit” flowsheets were modelled to

incorporate the laterite, oxide, primary ore characteristics in the LOM plan. This

process resulted in the selection of a single stage SAG (6.5MW) milling circuit for

processing predominantly oxide ore blends in first two years and the addition of a

ball mill (2.5Mw) to create a SAB circuit from year 3 to facilitate processing of

predominantly primary ore blends. The additional cost of the ball mill is

incorporated in the sustaining capital LOM estimate, but we estimate it to be

a~A$10m requirement at the end of FY21. The back end of the flow sheets

remains the same for both ore types being a conventional CIP circuit.

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 16

17

Metallurgical test work has been conducted on 32 composites samples prepared

from 779m of drill core, totaling 90 ore intervals. Testing encompassed 27

variability composites samples, from the five different weathering horizons, two

master composites samples of primary mineralisation, and three master

composites samples of oxide mineralisation. The test work conducted by CMM

builds on similar work completed by IGO in 2012 and 2013, and we view the level

of confidence in the metallurgy of the deposit as high. The ore at Bibra is

classified as free milling, with a high gravity recoverable gold component (40-45%

in fresh, 20-30% in weathered oxide). Overall, gravity plus leach gold recoveries

range from 93- 96%, noting that we use 93% LOM in our modelling.

We note that the ultimate flowsheet could potentially change when the Feasibility

Study is re-optimised on the back of the Reserve update in JunQ’18. CMM has

flagged that “trade-off “ studies are underway, and we are of the view that

integrating similar size SAG and Ball mills from the beginning may increase the

production flexibility at the operation. The ultimate flow sheet as it stands as per

the Feasibility is shown below.

Figure 22: Karlawinda process flow sheet for fresh ore

Source: Company Reports

Construction of a tailings facility is a significant capital works item, which will be

expanded in line with production. The Feasibility Study outlined a plan for a 21Mt

facility to account for the proposed 6.5 year life, which naturally will need to be

expanded on our mine life assumptions. The Feasibility envisages an integrated

tailings storage and waste landform with basal area of approximately 100ha and

maximum embankment height of 18.5m. Upfront capital will only require CMM to

establish a “starter” embankment (~1 year’s storage) with a maximum height of

6.5m, and the ultimate design will be met via a minimum of two stages of 5m

vertical lifts against the waste stockpile as the mine life advances.

The requirement for surface water management was also identified as part of the

hydrological assessment, given the project is situated near the top of a small

upstream rainfall catchment basin (7.1km2), and the potential for seasonal

cyclonic related rainfall. Recommended measures to mitigate the impact of a

flooding event include a 3.4km long single, continuous flood protection berm

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 17

18

around the pit and a 2.8km long roadside diversion channel constructed along the

upstream (Northern) side of the mine access road.

In terms of accessing process water for the plant, CMM has completed significant

ground and surface water studies. Drilling has identified extensive groundwater in

the weathered dolomite aquifer in Bangemall Group rocks to the west of Bibra, as

well as an adjacent fracture zone aquifer, which is thought to have a significant

regional extent. Subsequent hydrogeological investigations have concluded that

the local groundwater system should be able to supply the expected water

demand for the mining and processing operation at Karlawinda. The company

envisages that a network of 15 bores will be required to sustain the LOM water

demands of between 10.7-13.1ML per day (higher in the initial two years)

Major site infrastructure items to be constructed include site and internal access

roads (proposing a new 31km unsealed road from the Hwy), mine equipment

service facilities, a 200-man accommodation village and site infrastructure

buildings.

The Feasibility Study allowed a duration of 64 weeks from the formal award of the

process plant contract to the commencement of ore commissioning (practical

completion) which is in line with our modelling.

Permitting

The Company has obtained a granted Mining Lease for the project along with a

signed Native Title access agreement. Base line and detailed environmental

studies have been completed and the process of obtaining other key permits and

approvals has commenced. We see no obvious impediments to fully permitting

the project.

CMM also has seven Miscellaneous Licenses under application, to facilitate the

construction of a site access road, powerlines as required and the erection of a

microwave tower. The Miscellaneous Licenses are expected to be granted in the

1H 2018.

Figure 23: CMM’s latest published development timeline (December 2017)

Source: Company Reports

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 18

19

Investment Risks

The risks below are inherent in the metals and mining industry and one or all could

impact our valuation and therefore our SPECULATIVE BUY rating.

Funding risk

As a pre-production company with no material income, CMM is reliant on equity

and debt markets to fund Feasibility Studies and development of its Karlawinda

gold project. We can make no assurances that accessing these markets will be

done without further dilution to shareholders.

Exploration risk

Exploration is subject to a number of risks and can require a high rate of capital

expenditure. Risks can also be associated with conversion of Inferred resources

and lack of accuracy in the interpretation of geochemical, geophysical, drilling and

other data. No assurances can be given that exploration will delineate further

minable reserves.

Operating risks

Once in production, the company will be subject to risks such as plant/equipment

breakdowns, metallurgical, seismic activity and other technical issues. An

increase in operating costs could reduce the profitability and free cash generation

from the operating assets considerably and negatively impact valuation. Further,

the actual characteristics of an ore deposit may differ significantly from initial

interpretations which can also materially impact forecast gold production from

original expectations.

Commodity price and currency fluctuations

As with any mining Company, CMM is directly exposed to commodity price and

currency fluctuations. Commodity price fluctuations are driven by many

macroeconomic forces including inflationary pressures, interest rates and supply

and demand of commodities. These factors could reduce the profitability, costing

and prospective outlook for the business.

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 19

Appendix: Important DisclosuresAnalyst CertificationEach authoring analyst of Canaccord Genuity whose name appears on the front page of this research hereby certifies that (i) therecommendations and opinions expressed in this research accurately reflect the authoring analyst’s personal, independent andobjective views about any and all of the designated investments or relevant issuers discussed herein that are within such authoringanalyst’s coverage universe and (ii) no part of the authoring analyst’s compensation was, is, or will be, directly or indirectly, related to thespecific recommendations or views expressed by the authoring analyst in the research.Analysts employed outside the US are not registered as research analysts with FINRA. These analysts may not be associated persons ofCanaccord Genuity Inc. and therefore may not be subject to the FINRA Rule 2241 and NYSE Rule 472 restrictions on communicationswith a subject company, public appearances and trading securities held by a research analyst account.Sector CoverageIndividuals identified as “Sector Coverage” cover a subject company’s industry in the identified jurisdiction, but are not authoringanalysts of the report.

Investment RecommendationDate and time of first dissemination: February 28, 2018, 19:36 ETDate and time of production: February 28, 2018, 19:36 ETTarget Price / Valuation Methodology:Capricorn Metals Limited - CMMOur A$0.18/sh price target is based on an NPV10% for the Karlawinda gold project, net of corporate and other adjustments. We havealso assumed A$70m in equity raised to complete the funding for the project (50:50 debt/equity) and our valuation is diluted to accountfor these assumptions.Risks to achieving Target Price / Valuation:Capricorn Metals Limited - CMMThe risks below are inherent in the metals and mining industry and one or all could impact our valuation and therefore our SPECULATIVEBUY rating.Funding risk

As a pre-production company with no material income, CMM is reliant on equity and debt markets to fund Feasibility Studies anddevelopment of its karlawinda gold project. We can make no assurances that accessing these markets will be done without furtherdilution to shareholders.

Exploration riskExploration is subject to a number of risks and can require a high rate of capital expenditure. Risks can also be associated withconversion of Inferred resources and lack of accuracy in the interpretation of geochemical, geophysical, drilling and other data. Noassurances can be given that exploration will delineate further minable reserves.Operating risksOnce in production, the company will be subject to risks such as plant/equipment breakdowns, metallurgical, seismic activity andother technical issues. An increase in operating costs could reduce the profitability and free cash generation from the operating assetsconsiderably and negatively impact valuation. Further, the actual characteristics of an ore deposit may differ significantly from initialinterpretations which can also materially impact forecast gold production from original expectations.Commodity price and currency fluctuationsAs with any mining Company, CMM is directly exposed to commodity price and currency fluctuations. Commodity price fluctuations aredriven by many macroeconomic forces including inflationary pressures, interest rates and supply and demand of commodities. Thesefactors could reduce the profitability, costing and prospective outlook for the business.

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 20

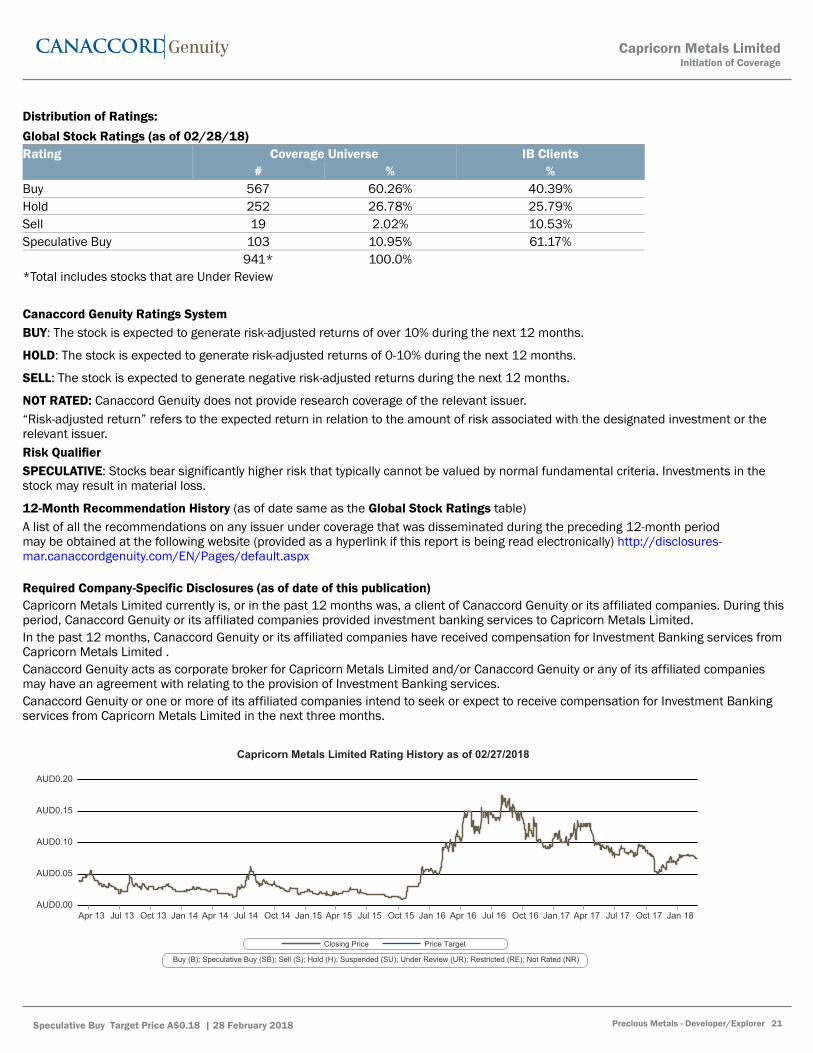

Distribution of Ratings:Global Stock Ratings (as of 02/28/18)Rating Coverage Universe IB Clients

# % %Buy 567 60.26% 40.39%Hold 252 26.78% 25.79%Sell 19 2.02% 10.53%Speculative Buy 103 10.95% 61.17%

941* 100.0%*Total includes stocks that are Under Review

Canaccord Genuity Ratings SystemBUY: The stock is expected to generate risk-adjusted returns of over 10% during the next 12 months.

HOLD: The stock is expected to generate risk-adjusted returns of 0-10% during the next 12 months.

SELL: The stock is expected to generate negative risk-adjusted returns during the next 12 months.

NOT RATED: Canaccord Genuity does not provide research coverage of the relevant issuer.“Risk-adjusted return” refers to the expected return in relation to the amount of risk associated with the designated investment or therelevant issuer.Risk QualifierSPECULATIVE: Stocks bear significantly higher risk that typically cannot be valued by normal fundamental criteria. Investments in thestock may result in material loss.

12-Month Recommendation History (as of date same as the Global Stock Ratings table)A list of all the recommendations on any issuer under coverage that was disseminated during the preceding 12-month periodmay be obtained at the following website (provided as a hyperlink if this report is being read electronically) http://disclosures-mar.canaccordgenuity.com/EN/Pages/default.aspx

Required Company-Specific Disclosures (as of date of this publication)Capricorn Metals Limited currently is, or in the past 12 months was, a client of Canaccord Genuity or its affiliated companies. During thisperiod, Canaccord Genuity or its affiliated companies provided investment banking services to Capricorn Metals Limited.In the past 12 months, Canaccord Genuity or its affiliated companies have received compensation for Investment Banking services fromCapricorn Metals Limited .Canaccord Genuity acts as corporate broker for Capricorn Metals Limited and/or Canaccord Genuity or any of its affiliated companiesmay have an agreement with relating to the provision of Investment Banking services.Canaccord Genuity or one or more of its affiliated companies intend to seek or expect to receive compensation for Investment Bankingservices from Capricorn Metals Limited in the next three months.

Capricorn Metals Limited Rating History as of 02/27/2018

AUD0.20

AUD0.15

AUD0.10

AUD0.05

AUD0.00Apr 13 Jul 13 Oct 13 Jan 14 Apr 14 Jul 14 Oct 14 Jan 15 Apr 15 Jul 15 Oct 15 Jan 16 Apr 16 Jul 16 Oct 16 Jan 17 Apr 17 Jul 17 Oct 17 Jan 18

Closing Price Price Target

Buy (B); Speculative Buy (SB); Sell (S); Hold (H); Suspended (SU); Under Review (UR); Restricted (RE); Not Rated (NR)

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 21

Past performanceIn line with Article 44(4)(b), MiFID II Delegated Regulation, we disclose price performance for the preceding five years or the whole periodfor which the financial instrument has been offered or investment service provided where less than five years. Please note price historyrefers to actual past performance, and that past performance is not a reliable indicator of future price and/or performance.

Online DisclosuresUp-to-date disclosures may be obtained at the following website (provided as a hyperlink if this report is being read electronically)http://disclosures.canaccordgenuity.com/EN/Pages/default.aspx; or by sending a request to Canaccord Genuity Corp. Research, Attn:Disclosures, P.O. Box 10337 Pacific Centre, 2200-609 Granville Street, Vancouver, BC, Canada V7Y 1H2; or by sending a requestby email to [email protected]. The reader may also obtain a copy of Canaccord Genuity’s policies and proceduresregarding the dissemination of research by following the steps outlined above.General DisclaimersSee “Required Company-Specific Disclosures” above for any of the following disclosures required as to companies referred to in thisreport: manager or co-manager roles; 1% or other ownership; compensation for certain services; types of client relationships; researchanalyst conflicts; managed/co-managed public offerings in prior periods; directorships; market making in equity securities and relatedderivatives. For reports identified above as compendium reports, the foregoing required company-specific disclosures can be found ina hyperlink located in the section labeled, “Compendium Reports.” “Canaccord Genuity” is the business name used by certain whollyowned subsidiaries of Canaccord Genuity Group Inc., including Canaccord Genuity Inc., Canaccord Genuity Limited, Canaccord GenuityCorp., and Canaccord Genuity (Australia) Limited, an affiliated company that is 50%-owned by Canaccord Genuity Group Inc.The authoring analysts who are responsible for the preparation of this research are employed by Canaccord Genuity Corp. a Canadianbroker-dealer with principal offices located in Vancouver, Calgary, Toronto, Montreal, or Canaccord Genuity Inc., a US broker-dealerwith principal offices located in New York, Boston, San Francisco and Houston, or Canaccord Genuity Limited., a UK broker-dealer withprincipal offices located in London (UK) and Dublin (Ireland), or Canaccord Genuity (Australia) Limited, an Australian broker-dealer withprincipal offices located in Sydney and Melbourne.The authoring analysts who are responsible for the preparation of this research have received (or will receive) compensation based upon(among other factors) the Investment Banking revenues and general profits of Canaccord Genuity. However, such authoring analystshave not received, and will not receive, compensation that is directly based upon or linked to one or more specific Investment Bankingactivities, or to recommendations contained in the research.Some regulators require that a firm must establish, implement and make available a policy for managing conflicts of interest arising asa result of publication or distribution of research. This research has been prepared in accordance with Canaccord Genuity’s policy onmanaging conflicts of interest, and information barriers or firewalls have been used where appropriate. Canaccord Genuity’s policy isavailable upon request.The information contained in this research has been compiled by Canaccord Genuity from sources believed to be reliable, but (with theexception of the information about Canaccord Genuity) no representation or warranty, express or implied, is made by Canaccord Genuity,its affiliated companies or any other person as to its fairness, accuracy, completeness or correctness. Canaccord Genuity has notindependently verified the facts, assumptions, and estimates contained herein. All estimates, opinions and other information containedin this research constitute Canaccord Genuity’s judgement as of the date of this research, are subject to change without notice and areprovided in good faith but without legal responsibility or liability.From time to time, Canaccord Genuity salespeople, traders, and other professionals provide oral or written market commentary ortrading strategies to our clients and our principal trading desk that reflect opinions that are contrary to the opinions expressed in thisresearch. Canaccord Genuity’s affiliates, principal trading desk, and investing businesses also from time to time make investmentdecisions that are inconsistent with the recommendations or views expressed in this research.This research is provided for information purposes only and does not constitute an offer or solicitation to buy or sell any designatedinvestments discussed herein in any jurisdiction where such offer or solicitation would be prohibited. As a result, the designatedinvestments discussed in this research may not be eligible for sale in some jurisdictions. This research is not, and under nocircumstances should be construed as, a solicitation to act as a securities broker or dealer in any jurisdiction by any person or companythat is not legally permitted to carry on the business of a securities broker or dealer in that jurisdiction. This material is prepared forgeneral circulation to clients and does not have regard to the investment objectives, financial situation or particular needs of anyparticular person. Investors should obtain advice based on their own individual circumstances before making an investment decision.To the fullest extent permitted by law, none of Canaccord Genuity, its affiliated companies or any other person accepts any liabilitywhatsoever for any direct or consequential loss arising from or relating to any use of the information contained in this research.Research Distribution PolicyCanaccord Genuity research is posted on the Canaccord Genuity Research Portal and will be available simultaneously for access by allof Canaccord Genuity’s customers who are entitled to receive the firm's research. In addition research may be distributed by the firm’ssales and trading personnel via email, instant message or other electronic means. Customers entitled to receive research may alsoreceive it via third party vendors. Until such time as research is made available to Canaccord Genuity’s customers as described above,Authoring Analysts will not discuss the contents of their research with Sales and Trading or Investment Banking employees without priorcompliance consent.

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 22

For further information about the proprietary model(s) associated with the covered issuer(s) in this research report, clients shouldcontact their local sales representative.Short-Term Trade IdeasResearch Analysts may, from time to time, discuss “short-term trade ideas” in research reports. A short-term trade idea offers a near-term view on how a security may trade, based on market and trading events or catalysts, and the resulting trading opportunity that maybe available. Any such trading strategies are distinct from and do not affect the analysts' fundamental equity rating for such stocks. Ashort-term trade idea may differ from the price targets and recommendations in our published research reports that reflect the researchanalyst's views of the longer-term (i.e. one-year or greater) prospects of the subject company, as a result of the differing time horizons,methodologies and/or other factors. It is possible, for example, that a subject company's common equity that is considered a long-term ‘Hold' or 'Sell' might present a short-term buying opportunity as a result of temporary selling pressure in the market or for otherreasons described in the research report; conversely, a subject company's stock rated a long-term 'Buy' or “Speculative Buy’ could beconsidered susceptible to a downward price correction, or other factors may exist that lead the research analyst to suggest a sale overthe short-term. Short-term trade ideas are not ratings, nor are they part of any ratings system, and the firm does not intend, and does notundertake any obligation, to maintain or update short-term trade ideas. Short-term trade ideas are not suitable for all investors and arenot tailored to individual investor circumstances and objectives, and investors should make their own independent decisions regardingany securities or strategies discussed herein. Please contact your salesperson for more information regarding Canaccord Genuity’sresearch.For Canadian Residents:This research has been approved by Canaccord Genuity Corp., which accepts sole responsibility for this research and its disseminationin Canada. Canaccord Genuity Corp. is registered and regulated by the Investment Industry Regulatory Organization of Canada (IIROC)and is a Member of the Canadian Investor Protection Fund. Canadian clients wishing to effect transactions in any designated investmentdiscussed should do so through a qualified salesperson of Canaccord Genuity Corp. in their particular province or territory.For United States Persons:Canaccord Genuity Inc., a US registered broker-dealer, accepts responsibility for this research and its dissemination in the United States.This research is intended for distribution in the United States only to certain US institutional investors. US clients wishing to effecttransactions in any designated investment discussed should do so through a qualified salesperson of Canaccord Genuity Inc. Analystsemployed outside the US, as specifically indicated elsewhere in this report, are not registered as research analysts with FINRA. Theseanalysts may not be associated persons of Canaccord Genuity Inc. and therefore may not be subject to the FINRA Rule 2241 and NYSERule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analystaccount.For United Kingdom and European Residents:This research is distributed in the United Kingdom and elsewhere Europe, as third party research by Canaccord Genuity Limited,which is authorized and regulated by the Financial Conduct Authority. This research is for distribution only to persons who are EligibleCounterparties or Professional Clients only and is exempt from the general restrictions in section 21 of the Financial Services andMarkets Act 2000 on the communication of invitations or inducements to engage in investment activity on the grounds that it is beingdistributed in the United Kingdom only to persons of a kind described in Article 19(5) (Investment Professionals) and 49(2) (High NetWorth companies, unincorporated associations etc) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005(as amended). It is not intended to be distributed or passed on, directly or indirectly, to any other class of persons. This material is not fordistribution in the United Kingdom or elsewhere in Europe to retail clients, as defined under the rules of the Financial Conduct Authority.For Jersey, Guernsey and Isle of Man Residents:This research is sent to you by Canaccord Genuity Wealth (International) Limited (CGWI) for information purposes and is not to beconstrued as a solicitation or an offer to purchase or sell investments or related financial instruments. This research has been producedby an affiliate of CGWI for circulation to its institutional clients and also CGWI. Its contents have been approved by CGWI and we areproviding it to you on the basis that we believe it to be of interest to you. This statement should be read in conjunction with your clientagreement, CGWI's current terms of business and the other disclosures and disclaimers contained within this research. If you are in anydoubt, you should consult your financial adviser.CGWI is licensed and regulated by the Guernsey Financial Services Commission, the Jersey Financial Services Commission and the Isleof Man Financial Supervision Commission. CGWI is registered in Guernsey and is a wholly owned subsidiary of Canaccord Genuity GroupInc.For Australian Residents:This research is distributed in Australia by Canaccord Genuity (Australia) Limited ABN 19 075 071 466 holder of AFS Licence No234666. To the extent that this research contains any advice, this is limited to general advice only. Recipients should take into accounttheir own personal circumstances before making an investment decision. Clients wishing to effect any transactions in any financialproducts discussed in the research should do so through a qualified representative of Canaccord Genuity (Australia) Limited. CanaccordGenuity Wealth Management is a division of Canaccord Genuity (Australia) Limited.For Hong Kong Residents:This research is distributed in Hong Kong by Canaccord Genuity (Hong Kong) Limited which is licensed by the Securities and FuturesCommission. This research is only intended for persons who fall within the definition of professional investor as defined in the Securities

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 23

and Futures Ordinance. It is not intended to be distributed or passed on, directly or indirectly, to any other class of persons. Recipients ofthis report can contact Canaccord Genuity (Hong Kong) Limited. (Contact Tel: +852 3919 2561) in respect of any matters arising from, orin connection with, this research.Additional information is available on request.Copyright © Canaccord Genuity Corp. 2018 – Member IIROC/Canadian Investor Protection Fund

Copyright © Canaccord Genuity Limited. 2018 – Member LSE, authorized and regulated by the Financial Conduct Authority.

Copyright © Canaccord Genuity Inc. 2018 – Member FINRA/SIPC

Copyright © Canaccord Genuity (Australia) Limited. 2018 – Participant of ASX Group, Chi-x Australia and of the NSX. Authorized andregulated by ASIC.

All rights reserved. All material presented in this document, unless specifically indicated otherwise, is under copyright to CanaccordGenuity Corp., Canaccord Genuity Limited, Canaccord Genuity Inc or Canaccord Genuity Group Inc. None of the material, nor its content,nor any copy of it, may be altered in any way, or transmitted to or distributed to any other party, without the prior express writtenpermission of the entities listed above.None of the material, nor its content, nor any copy of it, may be altered in any way, reproduced, or distributed to any other partyincluding by way of any form of social media, without the prior express written permission of the entities listed above.

Capricorn Metals LimitedInitiation of Coverage

Speculative Buy Target Price A$0.18 | 28 February 2018 Precious Metals - Developer/Explorer 24