innovating banking for greater financial inclusion david ferrand, fsd kenya

TRANSCRIPT

Innovating banking for greater financial inclusion

David Ferrand, FSD Kenya

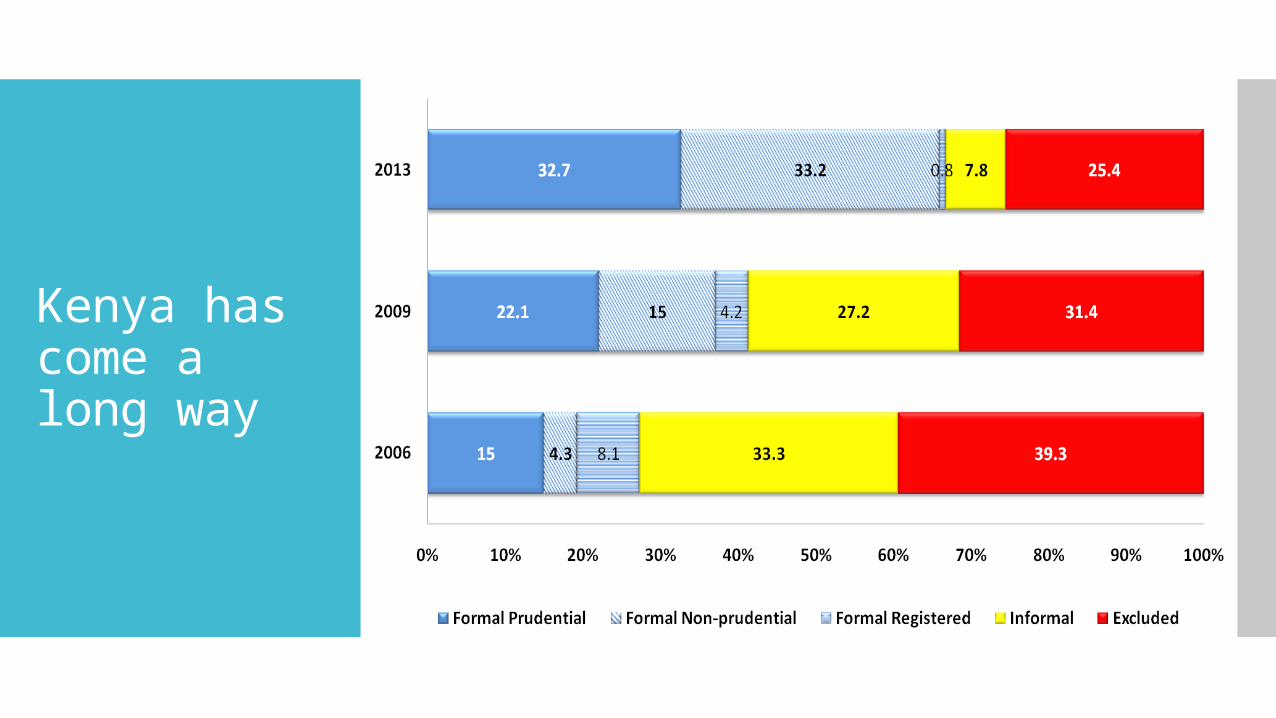

Kenya has come a long way

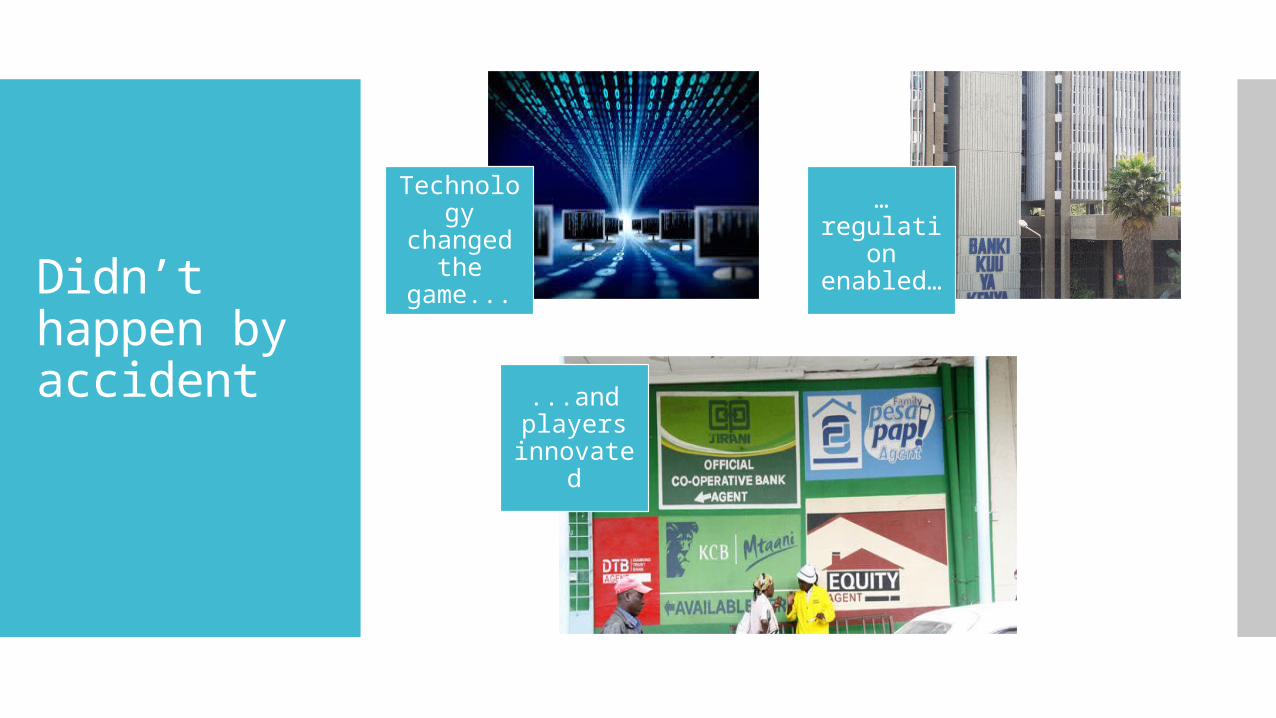

Didn’t happen by accident

Technology changed

the game...

…regulation enabled…

...and players

innovated

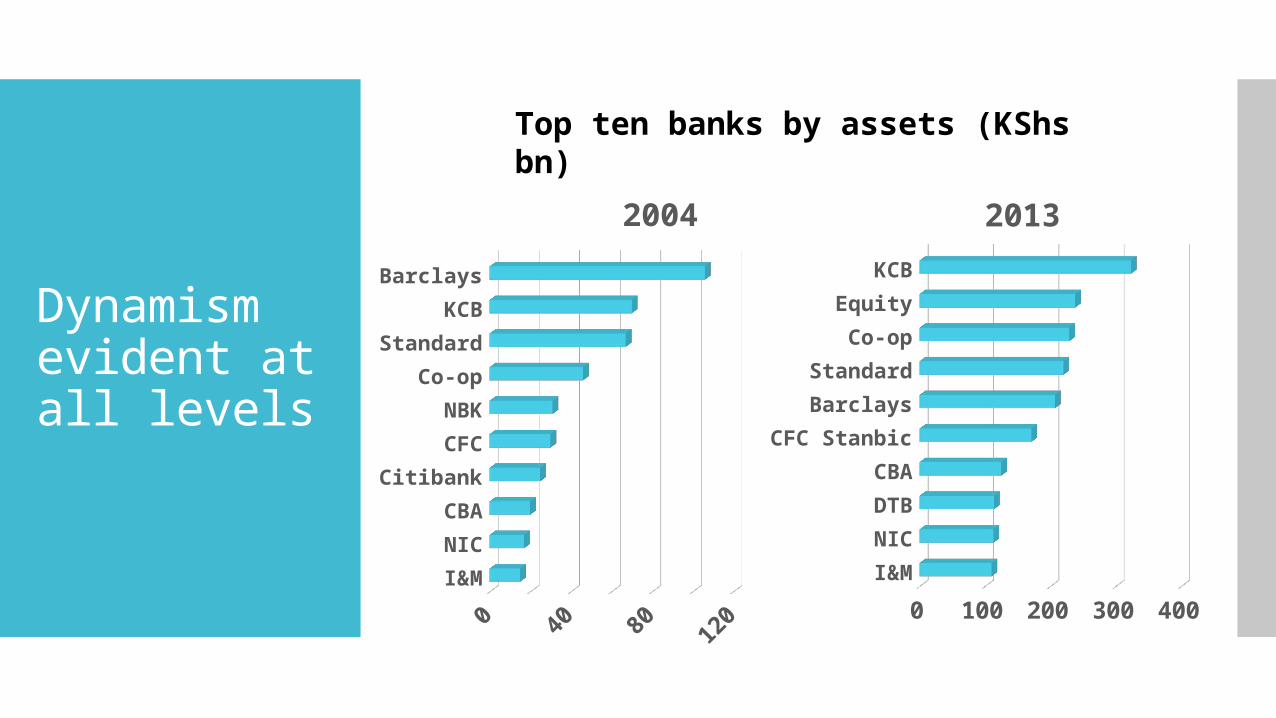

Dynamism evident at all levels

I&M

NIC

CBA

Citibank

CFC

NBK

Co-op

Standard

KCB

Barclays

2004

I&M

NIC

DTB

CBA

CFC Stanbic

Barclays

Standard

Co-op

Equity

KCB

0 100 200 300 400

2013

Top ten banks by assets (KShs bn)

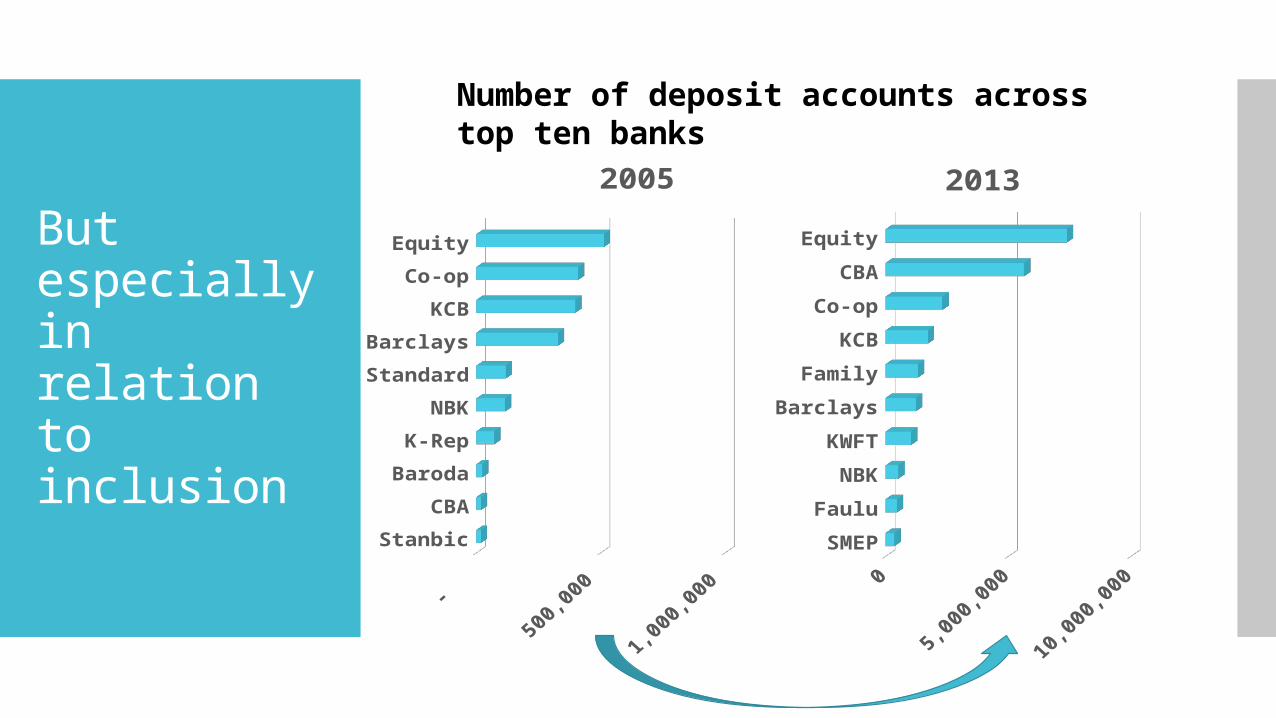

But especially in relation to inclusion

Stanbic

CBA

Baroda

K-Rep

NBK

Standard

Barclays

KCB

Co-op

Equity

- 500,000 1,000,000

2005

SMEP

Faulu

NBK

KWFT

Barclays

Family

KCB

Co-op

CBA

Equity

2013

Number of deposit accounts across top ten banks

Immediate future looks positive

Global Findex shows formal exclusion already down to 25% (2014)

800,000 accounts to be opened for the poorest

FinAccess 2015 could show only 20% exclusion in Kenya?

Italy currently shows 13% and the US 6%

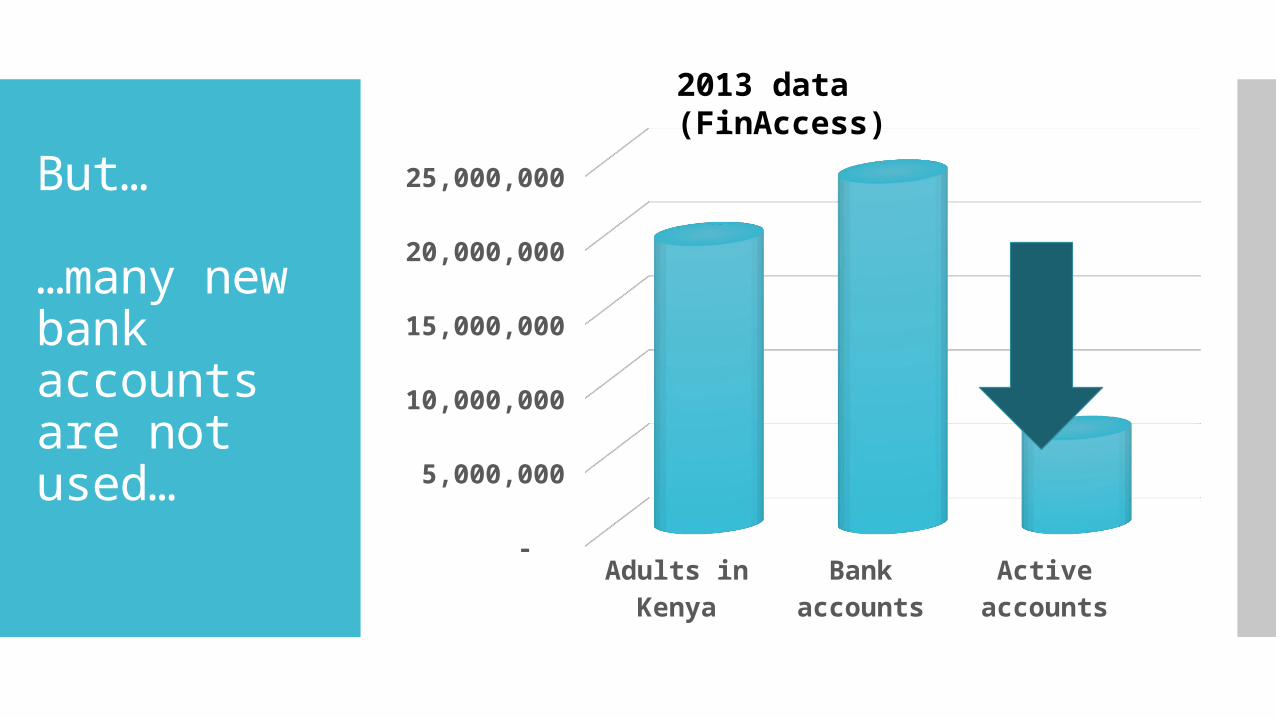

But…

…many new bank accounts are not used…

Adults in

Ken

ya

Bank

acco

unts

Activ

e ac

coun

ts -

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

2013 data (FinAccess)

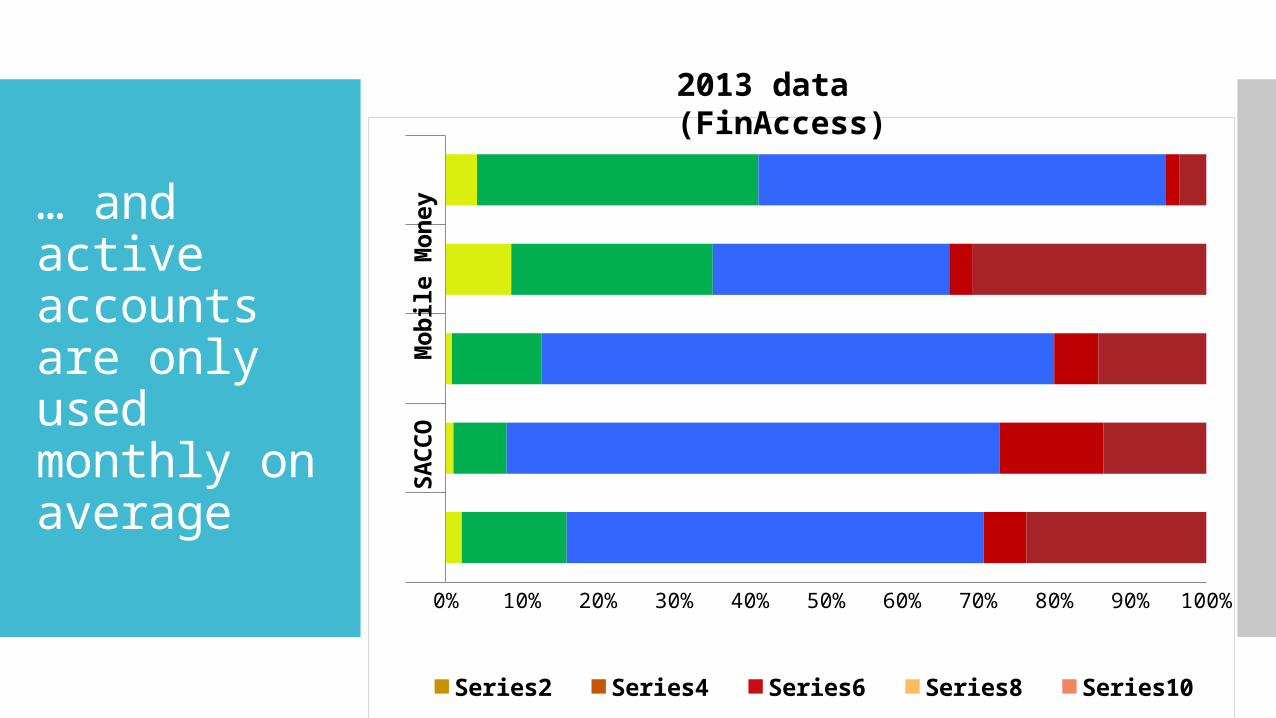

… and active accounts are only used monthly on average

SA

CC

O

Mob

ile M

on

ey

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Series2 Series4 Series6 Series8 Series10

2013 data (FinAccess)

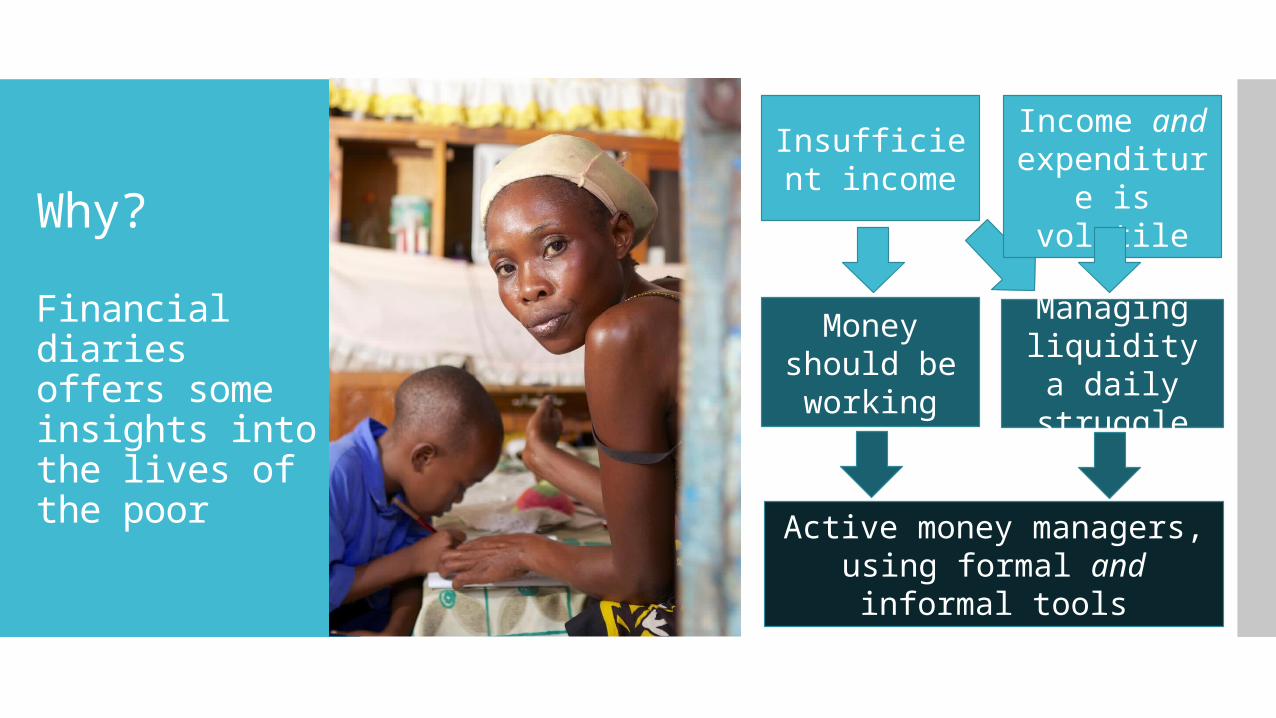

Why?

Financial diaries offers some insights into the lives of the poor

Insufficient income

Income and expenditure is volatile

Managing liquidity a

daily struggle

Money should be working

Active money managers, using formal and informal

tools

How do we tackle this?

1. Financial tools need to be low cost to use

2. Solutions must be relevant to needs

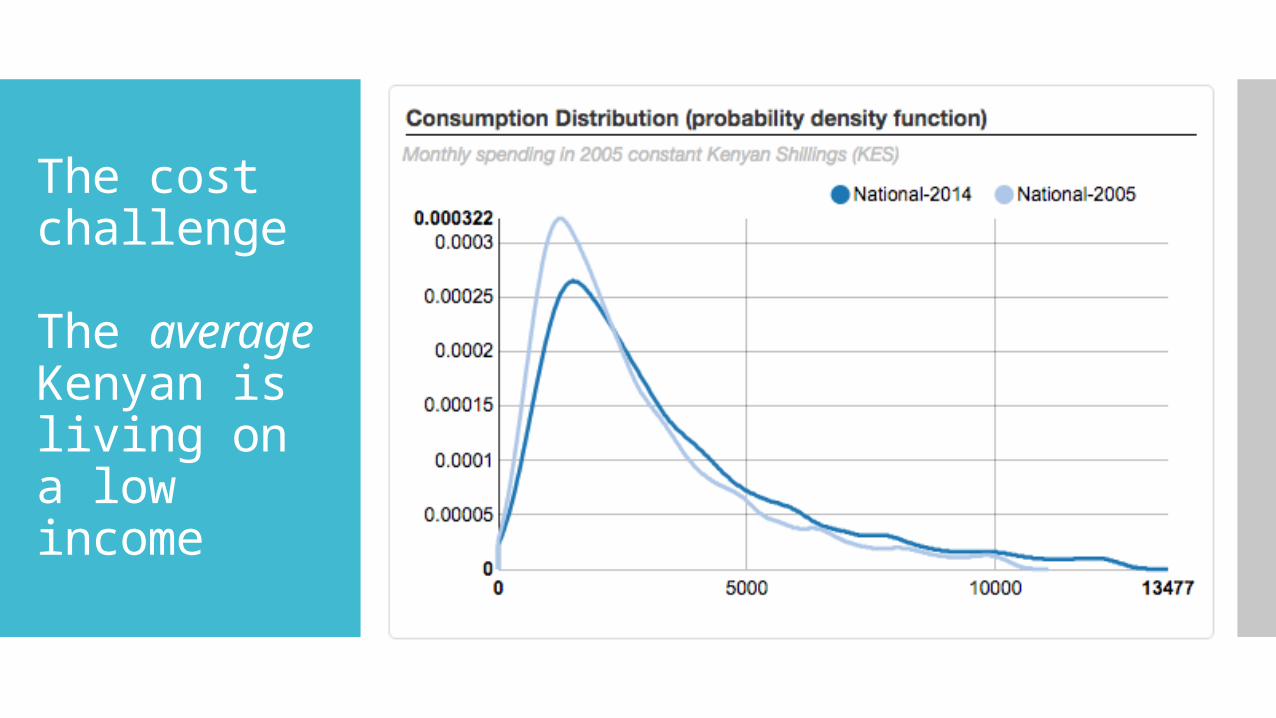

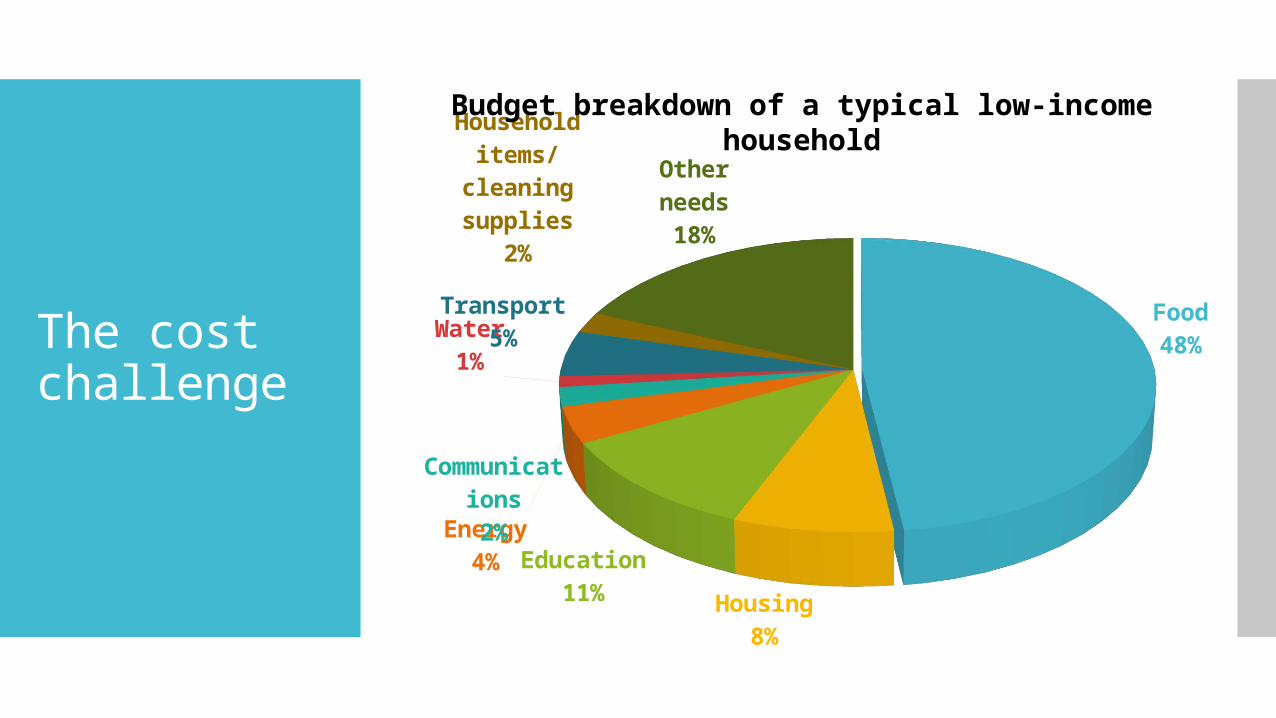

The cost challenge

The average Kenyan is living on a low income

The cost challenge

Food48%

Housing8%

Education11%

Energy4%

Commu-nications

2%

Water1%

Transport5%

Household items/

cleaning supplies

2%

Other needs18%

Budget breakdown of a typical low-income household

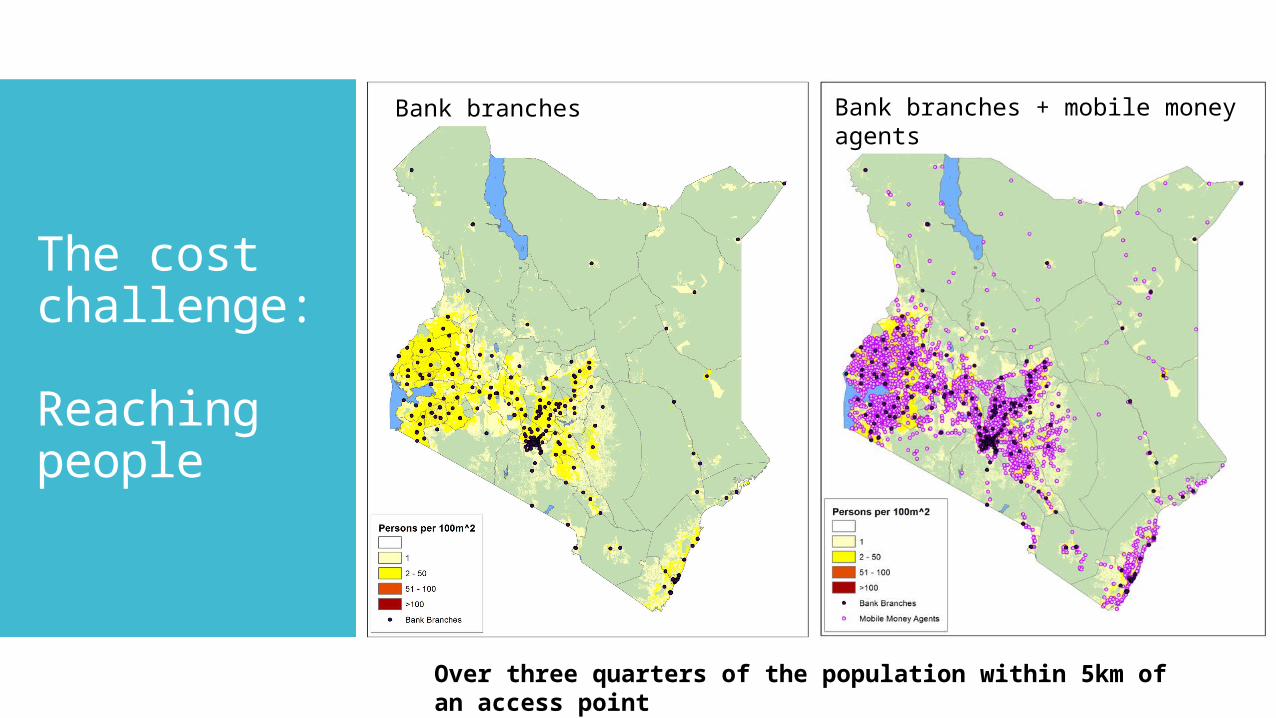

The cost challenge:

Reaching people

Bank branches + mobile money agents

Bank branches

Over three quarters of the population within 5km of an access point

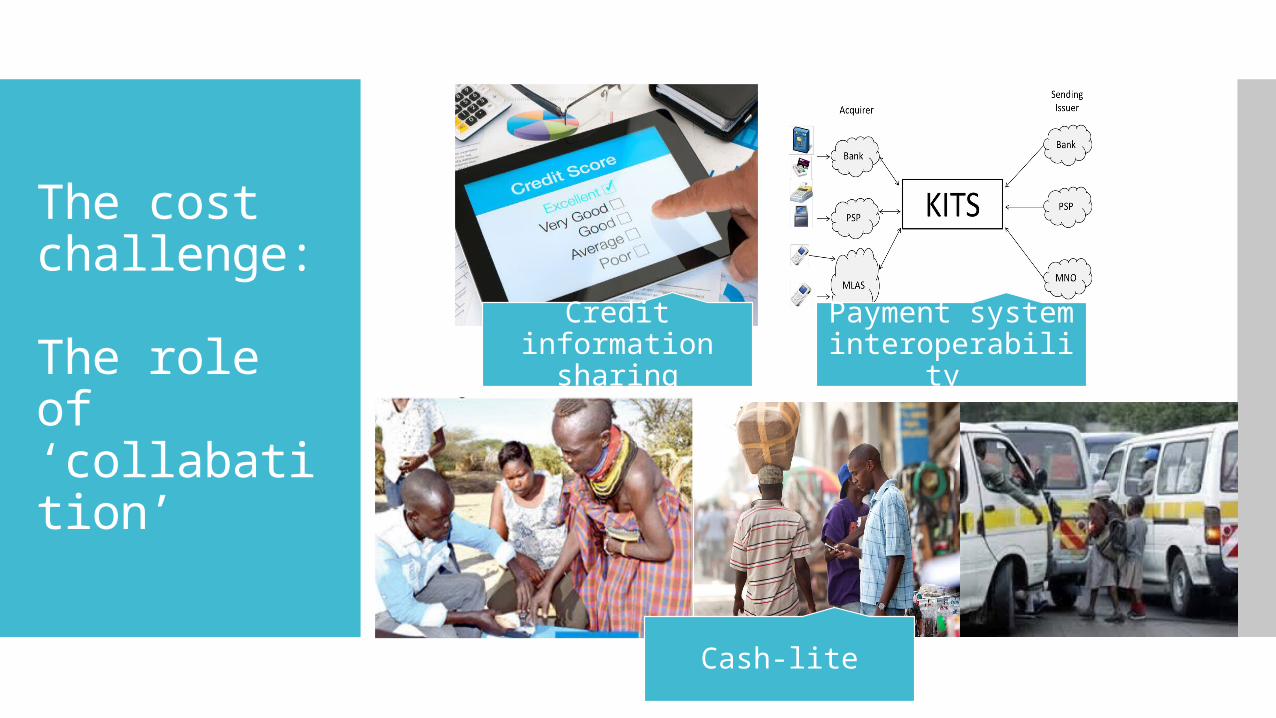

The cost challenge:

The role of ‘collabatition’

Credit information

sharing

Payment system interoperability

Cash-lite

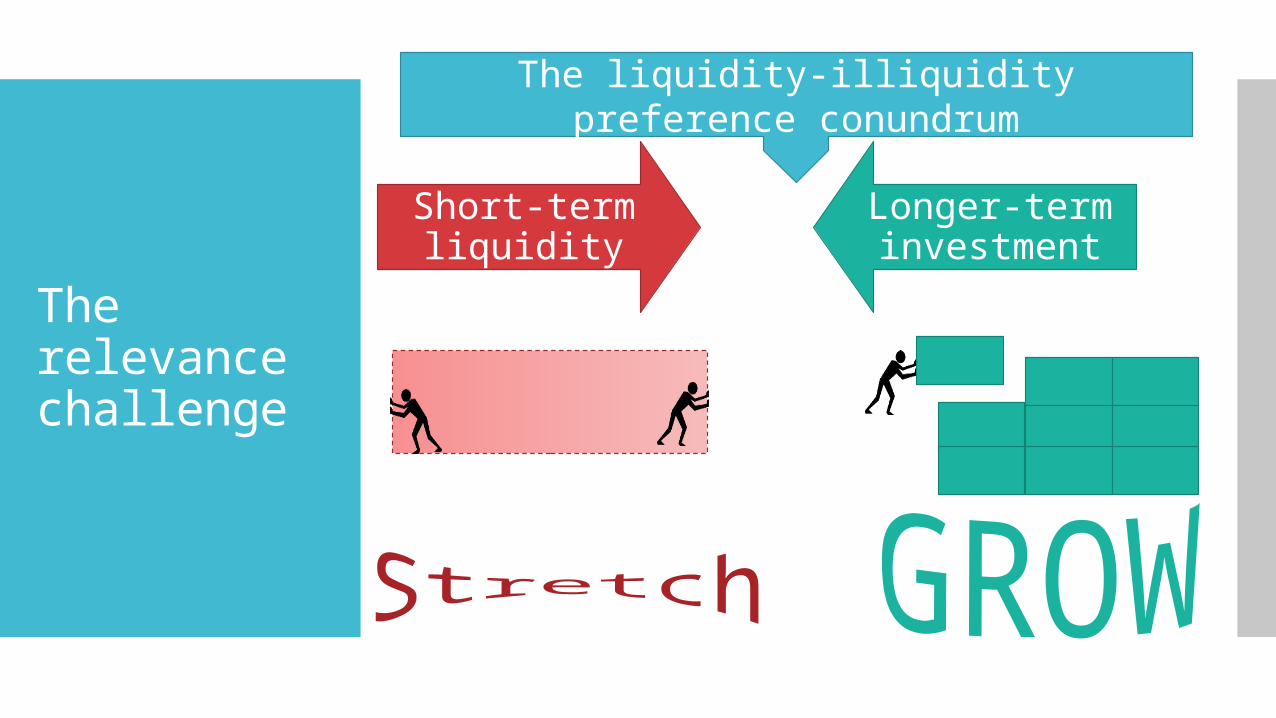

The relevance challenge

Short-term liquidity

Longer-

term investment

.The liquidity-illiquidity preference

conundrum

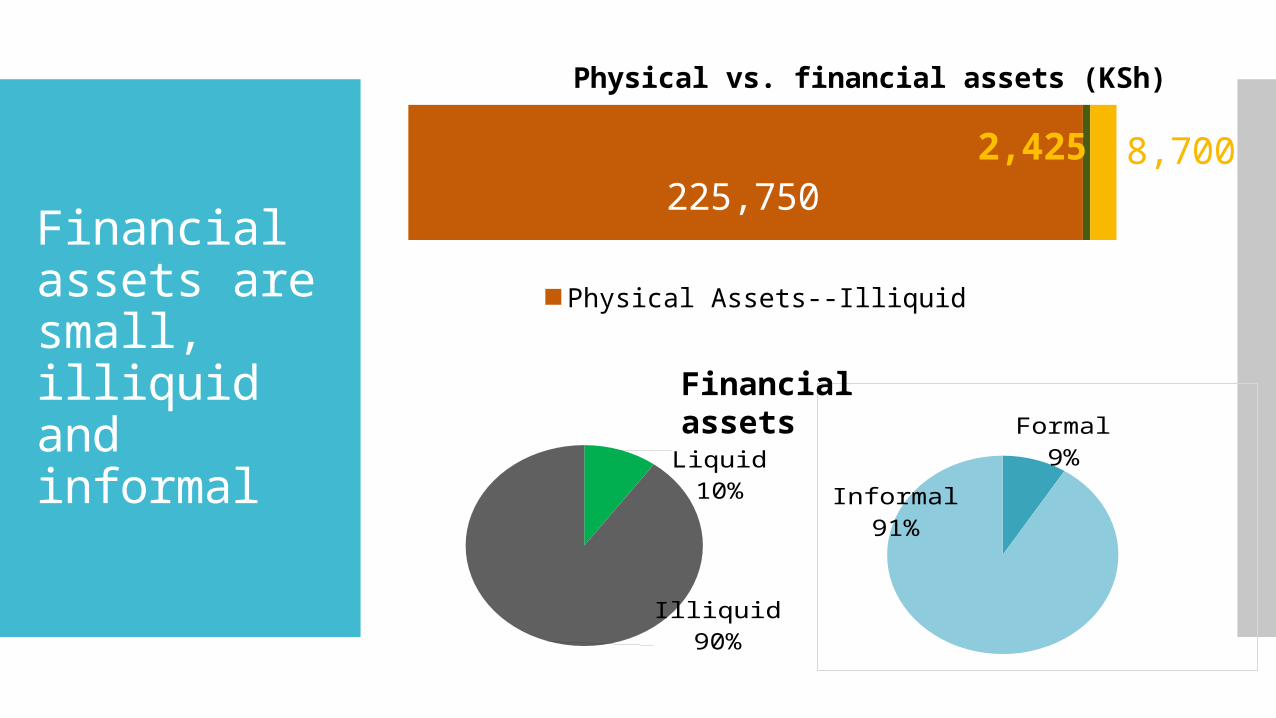

Financial assets are small, illiquid and informal

225,750

2,425 8,700

Physical vs. financial assets (KSh)

Physical Assets--Illiquid Physical Assets--LiquidFinancial Assets

Formal9%

Informal91%

Financial assets

Liquid10%

Illiquid90%

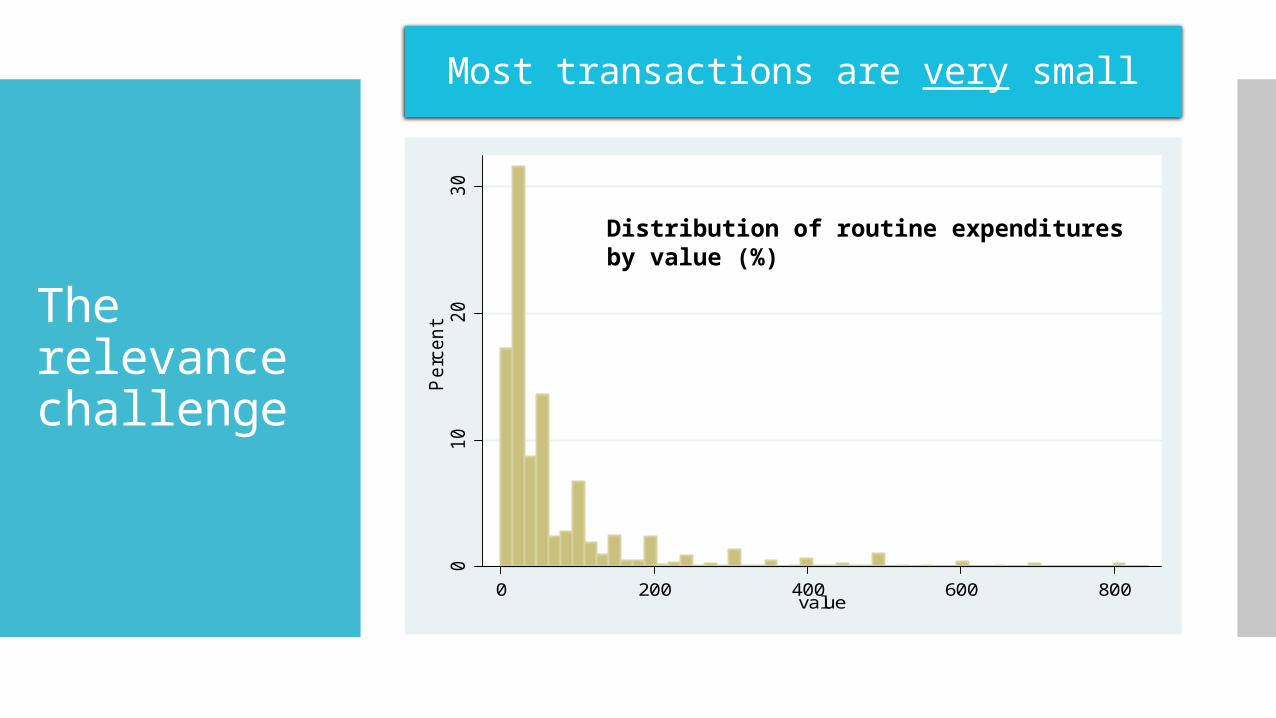

The relevance challenge

010

20

30

Percent

0 200 400 600 800value

Distribution of routine expenditures by value (%)

Most transactions are very small

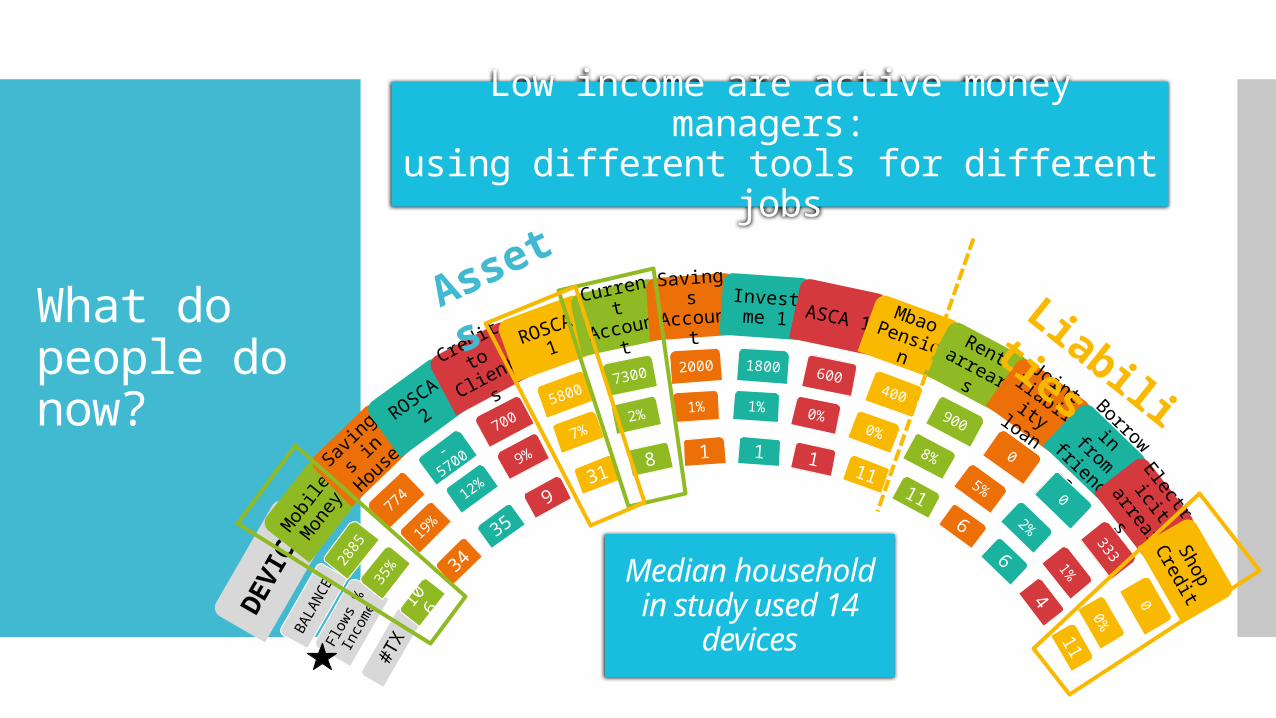

What do people do now?

DEVIC

EMob

ile

Mon

ey

Saving

s in

House

ROSCA

2

Credit

to

Clients

ROSCA

1

Current

Account

Savings

Account

Investme 1 ASCA 1

Mbao Pension Rent arrears Joint liability loan

Borrowi

n from

friends

Electric

it

arrears Shop

Credit

Low income are active money managers: using different tools for different jobs

BALA

NCE

2885

774

-

5700

7005800

7300 2000 1800 600400

900

0

0

333

0

Flow

s %

In

com

e35

%

19%

12%

9%

7%2% 1% 1% 0%

0%8%

5%

2%

1%

0%

#TX

10 6

34

359

318 1 1 1

1111

6

6

4

11

Asset

sLiabiliti

es

Median household in

study used 14 devices

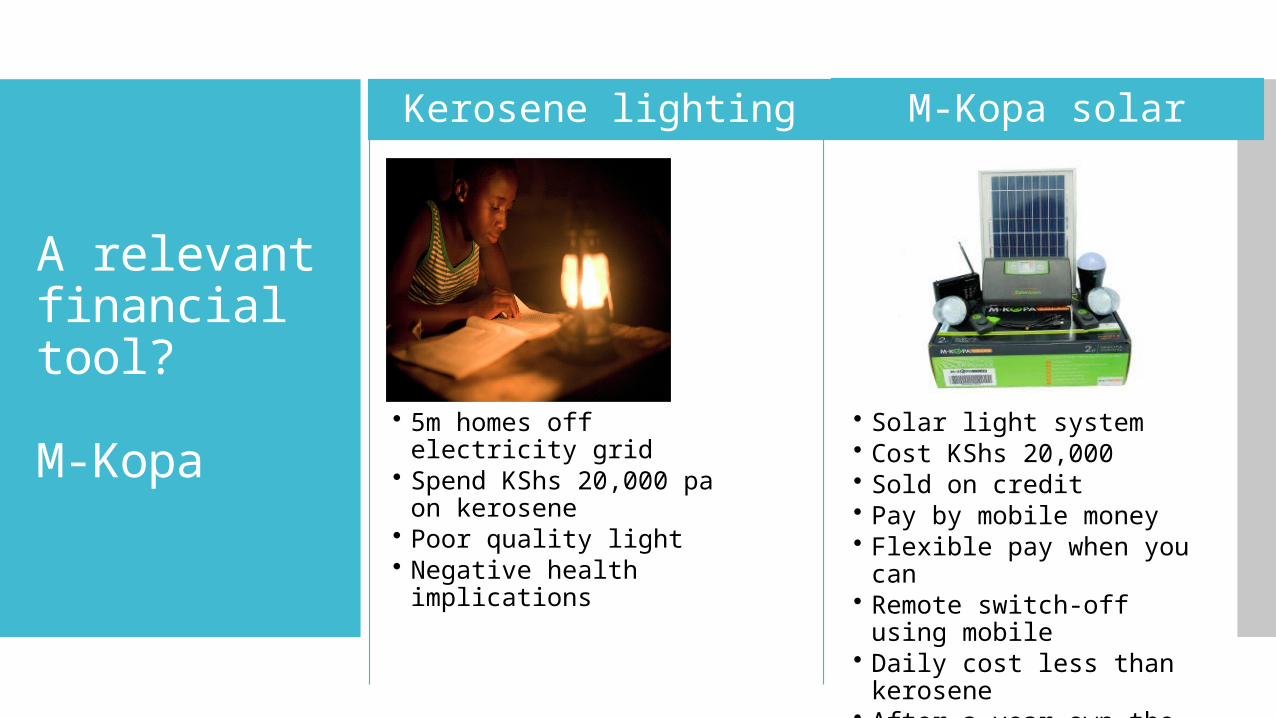

A relevant financial tool?

M-Kopa• 5m homes off electricity

grid• Spend KShs 20,000 pa on

kerosene• Poor quality light• Negative health

implications

Kerosene lighting

• Solar light system• Cost KShs 20,000• Sold on credit• Pay by mobile money• Flexible pay when you can• Remote switch-off using

mobile • Daily cost less than

kerosene• After a year own the asset

M-Kopa solar

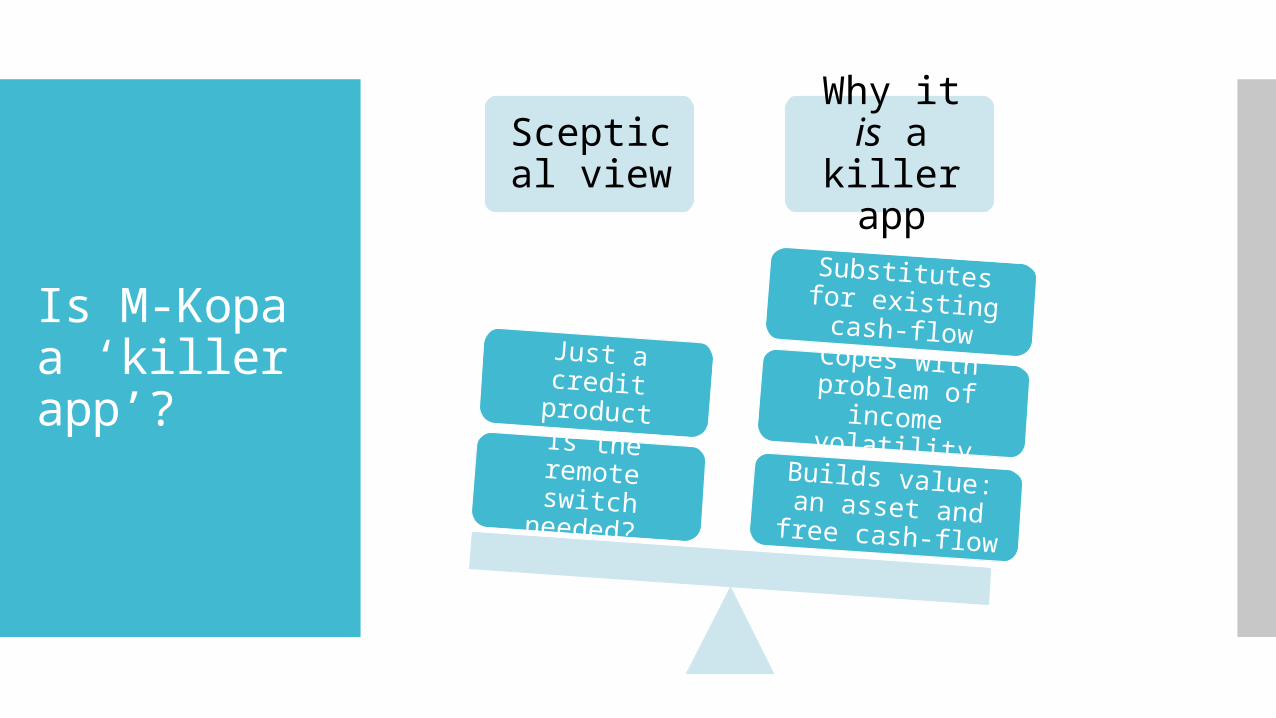

Is M-Kopa a ‘killer app’?

Sceptical view

Why it is a killer

app

Builds value: an asset and free cash-flow

Copes with problem of

income volatility

Substitutes for existing cash-flow

Is the remote switch

needed?

Just a credit product

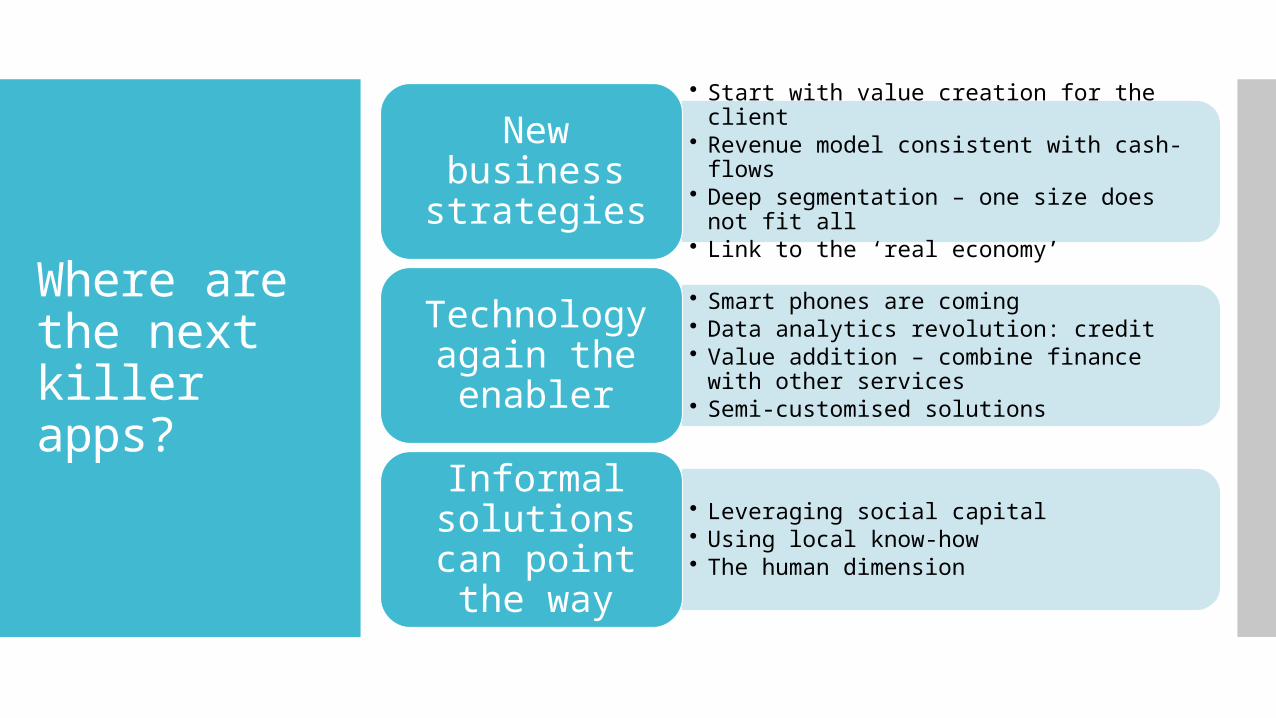

Where are the next killer apps?

• Start with value creation for the client• Revenue model consistent with cash-flows• Deep segmentation – one size does not fit

all• Link to the ‘real economy’

New business strategies

• Smart phones are coming• Data analytics revolution: credit• Value addition – combine finance with other

services• Semi-customised solutions

Technology again the enabler

• Leveraging social capital• Using local know-how• The human dimension

Informal solutions can point the way