innovating family takaful products and linking to … · innovating family takaful products and...

TRANSCRIPT

www.actuarialpartners.com

building value together

Innovating Family Takaful Products and Linking to Better Consumer Needs5th Annual World Takaful Conference, Family Takaful Summit Malaysia 2014

11 June 2014

Farzana Ismail, [email protected]

1Actuarial Partners

Agenda

Family Takaful in Malaysia

What do customers want?

Where are the gaps in the market?

Opportunities and challenges

Conclusion

2Actuarial Partners

Family Takaful Market in Malaysia

3Actuarial Partners

Total US$5.31 billion excluding Saudi Arabia and Iran, from 2013 EY World Takaful Report. Total Africa is

527 million, split for Sudan is estimated

The Current Takaful Market

2012 Takaful Sales (US$ million):

1. Malaysia 1,931

5. Qatar 305

2. UAE 1,142

4. Sudan 491

3. Indonesia 666

4Actuarial Partners

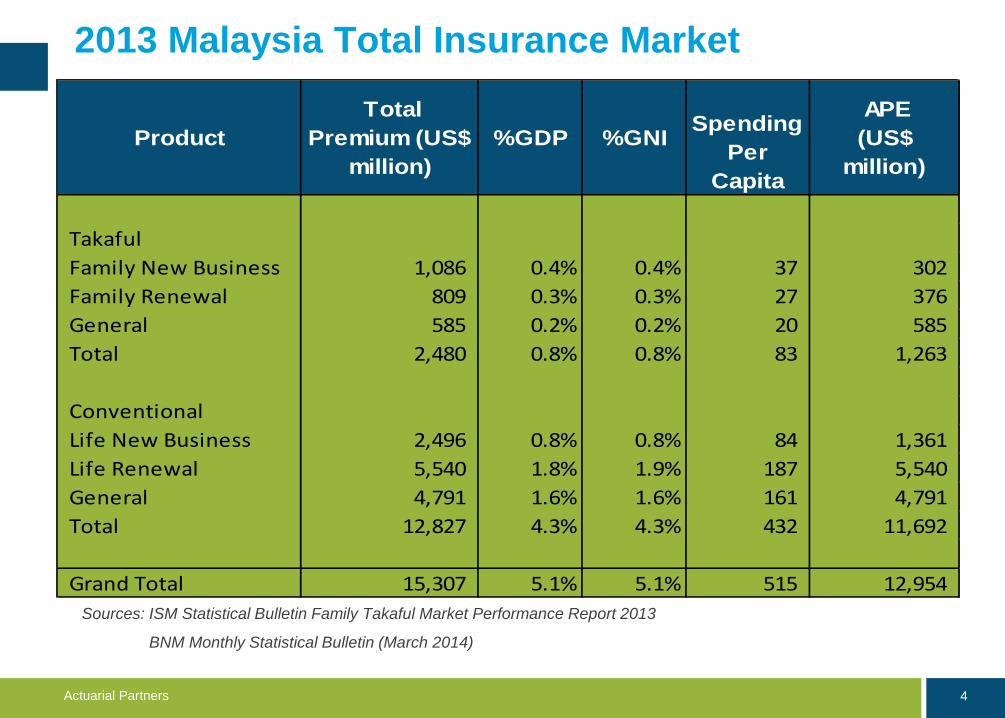

2013 Malaysia Total Insurance Market

Product Total

Premium (US$ million)

%GDP %GNI

Spending

Per Capita

APE (US$

million)

TakafulFamily New Business 1,086 0.4% 0.4% 37 302 Family Renewal 809 0.3% 0.3% 27 376 General 585 0.2% 0.2% 20 585 Total 2,480 0.8% 0.8% 83 1,263

ConventionalLife New Business 2,496 0.8% 0.8% 84 1,361 Life Renewal 5,540 1.8% 1.9% 187 5,540 General 4,791 1.6% 1.6% 161 4,791 Total 12,827 4.3% 4.3% 432 11,692

Grand Total 15,307 5.1% 5.1% 515 12,954 Sources: ISM Statistical Bulletin Family Takaful Market Performance Report 2013

BNM Monthly Statistical Bulletin (March 2014)

5Actuarial Partners

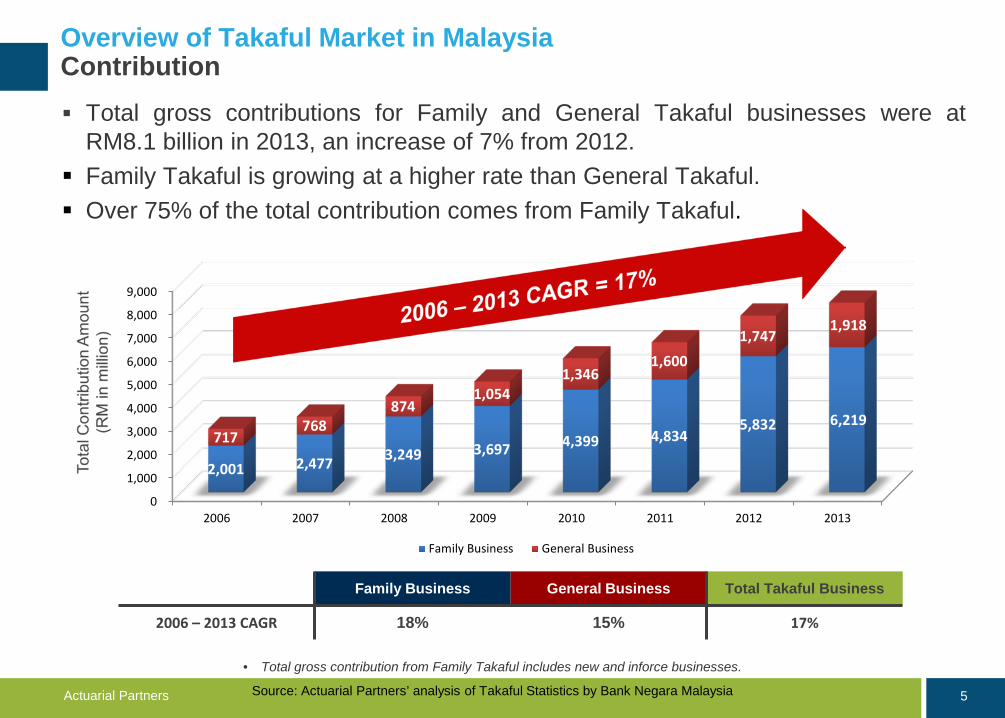

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2006 2007 2008 2009 2010 2011 2012 2013

2,001 2,477 3,249 3,697 4,399 4,834 5,832 6,219

717768

8741,054

1,3461,600

1,7471,918

Family Business General Business

Overview of Takaful Market in MalaysiaContribution Total gross contributions for Family and General Takaful businesses were at

RM8.1 billion in 2013, an increase of 7% from 2012. Family Takaful is growing at a higher rate than General Takaful. Over 75% of the total contribution comes from Family Takaful.

Family Business General Business Total Takaful Business

2006 – 2013 CAGR 18% 15% 17%

• Total gross contribution from Family Takaful includes new and inforce businesses.

Source: Actuarial Partners’ analysis of Takaful Statistics by Bank Negara Malaysia

6Actuarial Partners

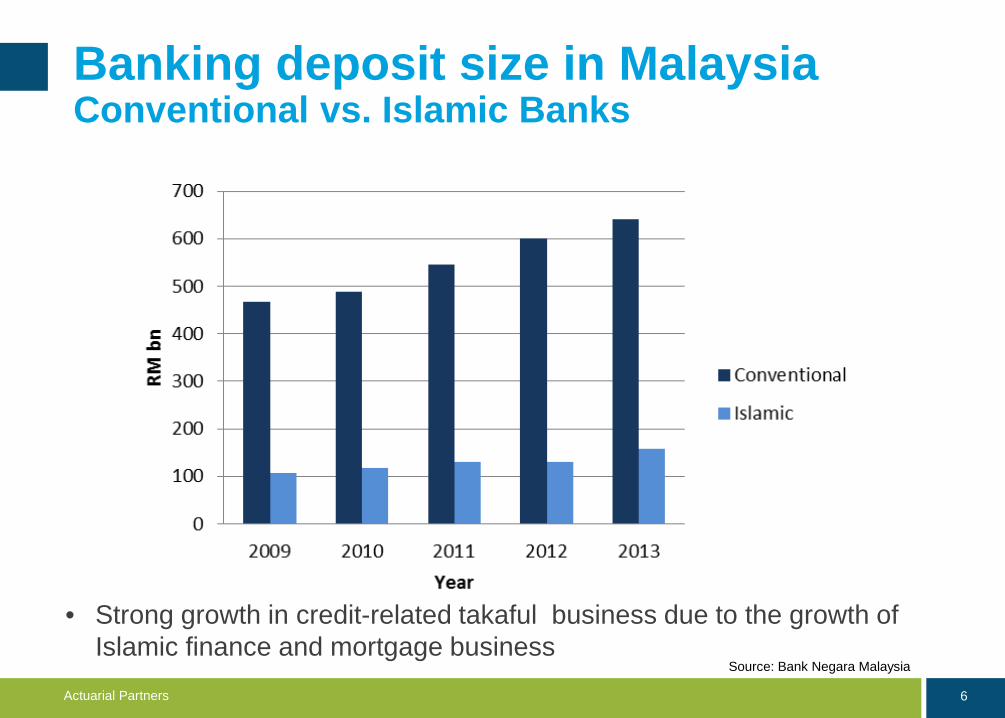

Banking deposit size in MalaysiaConventional vs. Islamic Banks

Source: Bank Negara Malaysia

• Strong growth in credit-related takaful business due to the growth of Islamic finance and mortgage business

7Actuarial Partners

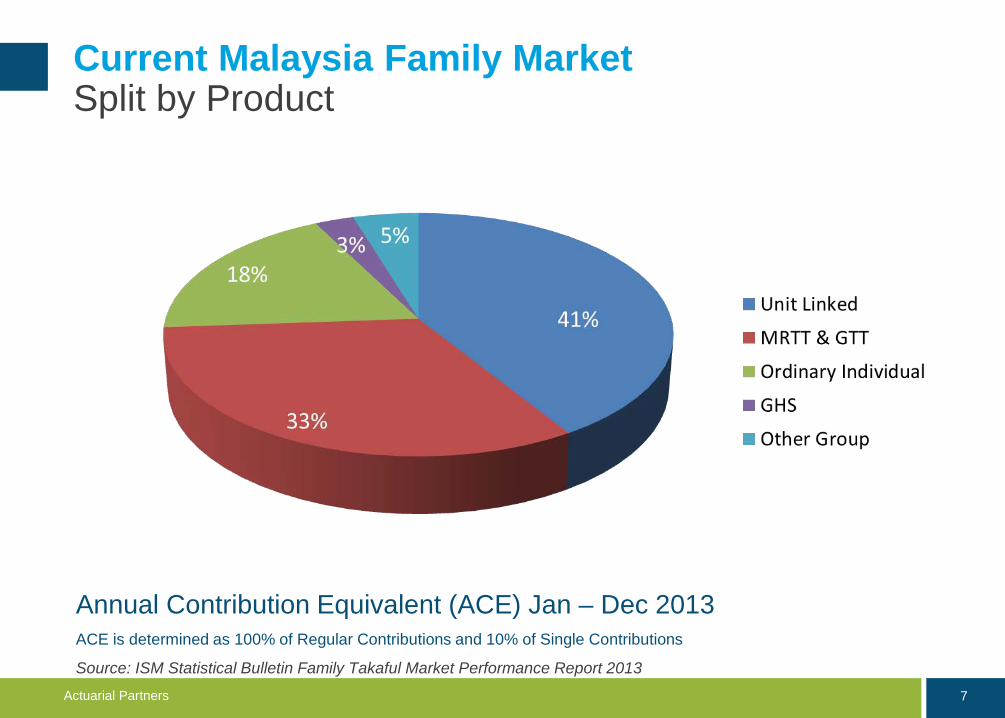

Current Malaysia Family MarketSplit by Product

Annual Contribution Equivalent (ACE) Jan – Dec 2013ACE is determined as 100% of Regular Contributions and 10% of Single Contributions

Source: ISM Statistical Bulletin Family Takaful Market Performance Report 2013

8Actuarial Partners

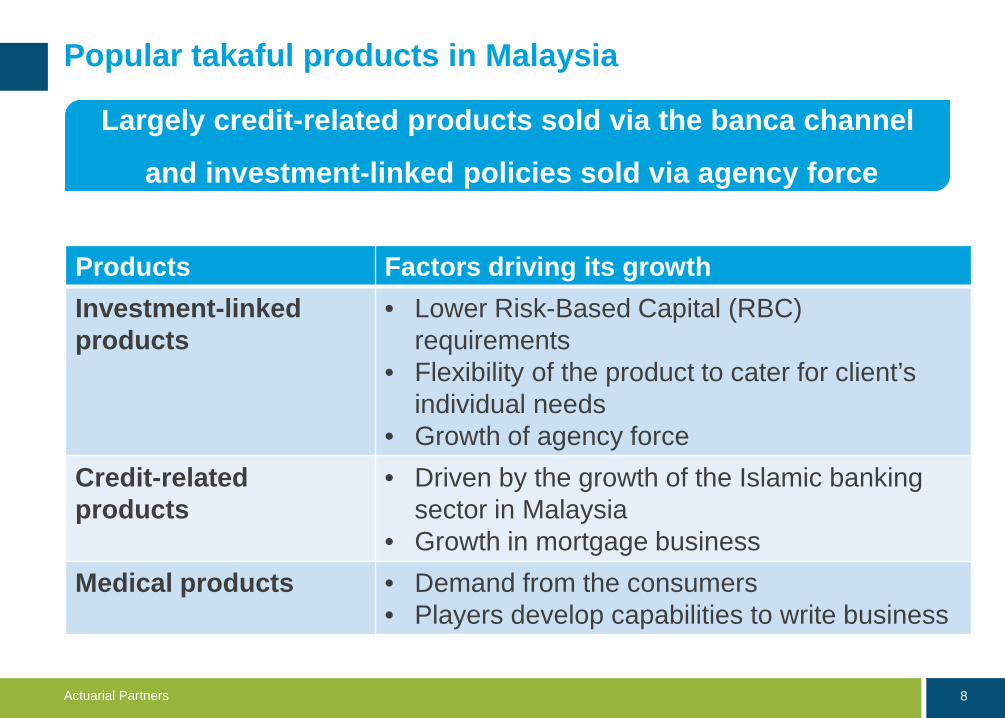

Popular takaful products in Malaysia

Products Factors driving its growthInvestment-linkedproducts

• Lower Risk-Based Capital (RBC) requirements

• Flexibility of the product to cater for client’s individual needs

• Growth of agency forceCredit-relatedproducts

• Driven by the growth of the Islamic banking sector in Malaysia

• Growth in mortgage businessMedical products • Demand from the consumers

• Players develop capabilities to write business

Largely credit-related products sold via the banca channel

and investment-linked policies sold via agency force

9Actuarial Partners

What do customers want?

10Actuarial Partners

What do customers want?

Credits to the movie “Jobs” (2013)Source: http://www.youtube.com/watch?v=NMQDTQnNsZ0

11Actuarial Partners

Do customers know what they want?

“How does somebody know what they want if

they haven’t even seen it?”

Steve Jobs

12Actuarial Partners

What customers do not want?

To be pestered and bothered To be confused To be pressurised

e.g. product pushing

To feel time is wasted To feel ripped off

13Actuarial Partners

What customers might want?

To get a good deal To feel important Sales process that is efficient

To have control To deal in trust and confidence Purchase satisfaction

14Actuarial Partners

How can Takaful products be better shaped to meet market needs?

What are the gaps in the market?

15Actuarial Partners

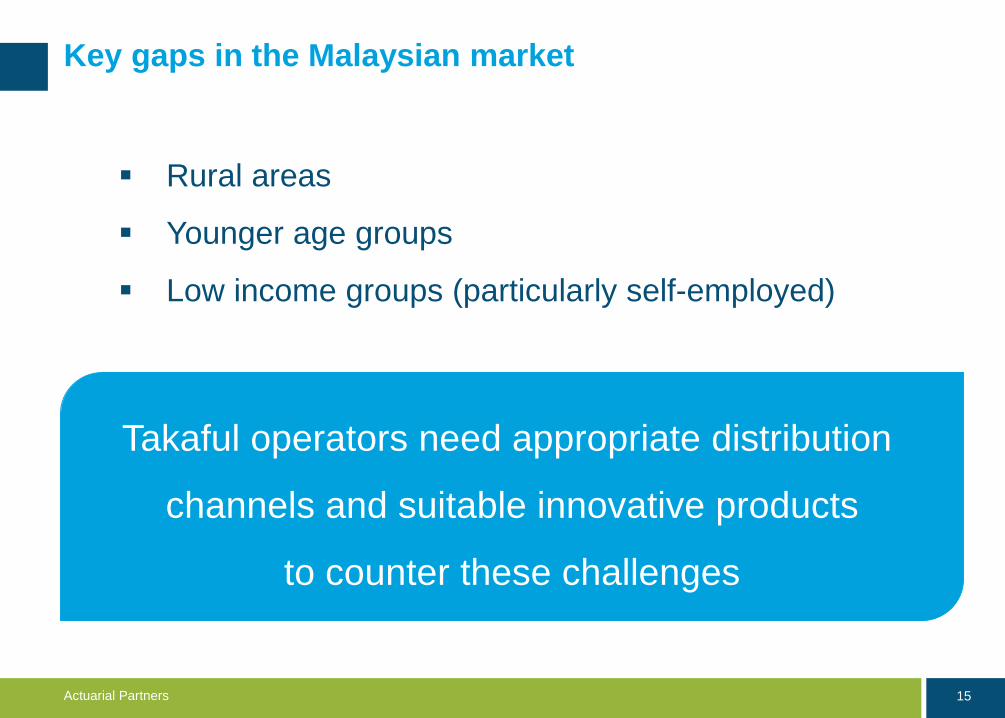

Key gaps in the Malaysian market

Rural areas

Younger age groups

Low income groups (particularly self-employed)

Takaful operators need appropriate distribution

channels and suitable innovative products

to counter these challenges

16Actuarial Partners

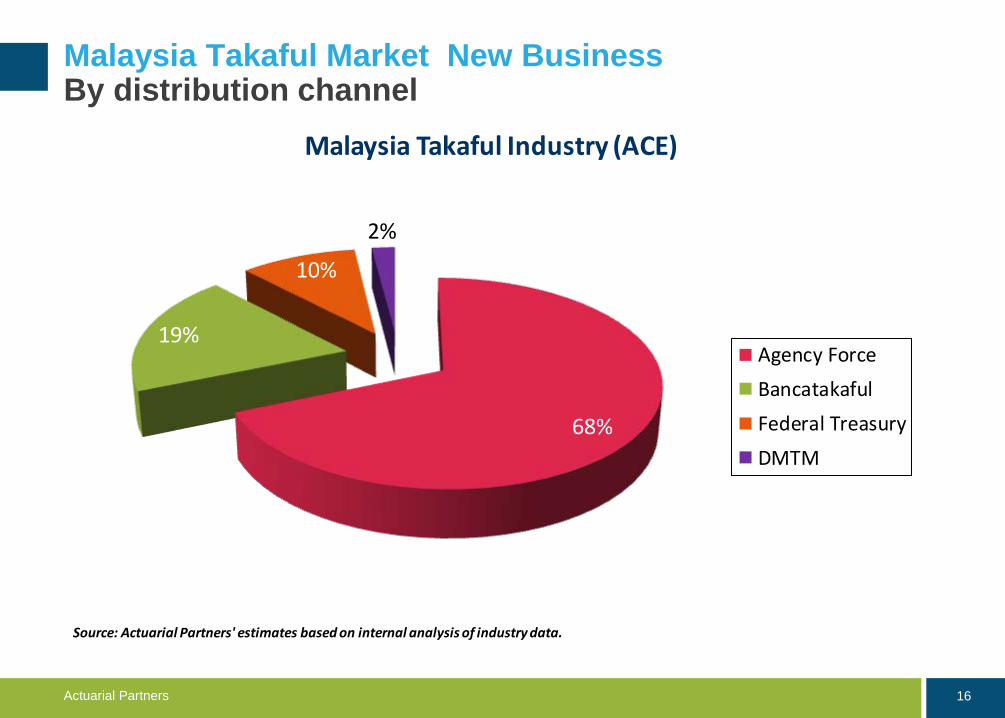

68%

19%

10%

2%

Malaysia Takaful Industry (ACE)

Agency ForceBancatakafulFederal TreasuryDMTM

Source: Actuarial Partners' estimates based on internal analysis of industry data.

Malaysia Takaful Market New Business By distribution channel

17Actuarial Partners

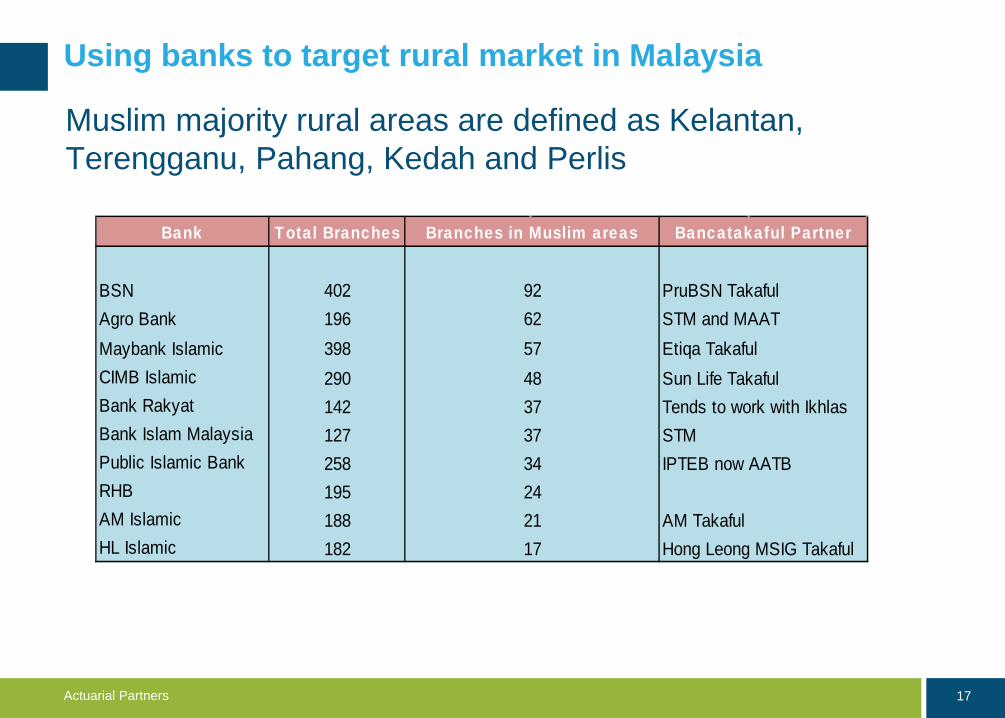

Using banks to target rural market in Malaysia

Muslim majority rural areas are defined as Kelantan, Terengganu, Pahang, Kedah and Perlis

Bank Total Branches

BSN 402 PruBSN TakafulAgro Bank 196 STM and MAATMaybank Islamic 398 Etiqa TakafulCIMB Islamic 290 Sun Life TakafulBank Rakyat 142 Tends to work with IkhlasBank Islam Malaysia 127 STM Public Islamic Bank 258 IPTEB now AATBRHB 195AM Islamic 188 AM TakafulHL Islamic 182 Hong Leong MSIG Takaful17

Branches in Muslim areas Bancatakaful Partner

9262

4857

3734

37

2124

18Actuarial Partners

Alternative channels to reach rural areas

Tie up with existing infrastructure e.g. postal services

Other existing infrastructures which can be utilized include insurancesales via mobile phones and small retailers.

Telemarketing as those in rural areas are typically more receptive totelemarketing compared to those in the urban areas

19Actuarial Partners

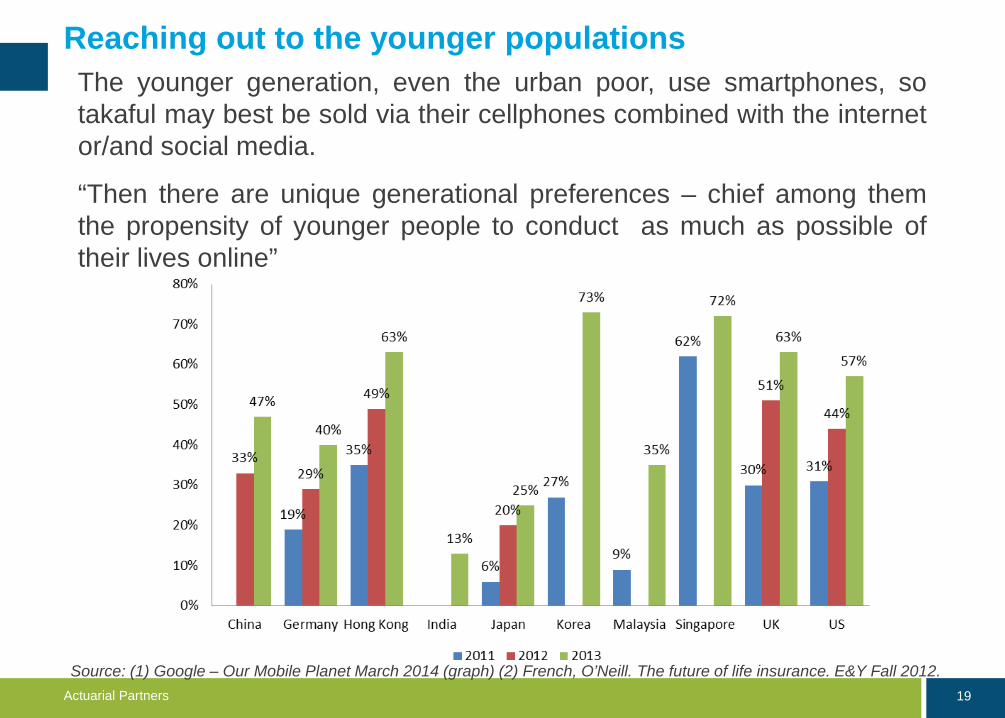

Reaching out to the younger populationsThe younger generation, even the urban poor, use smartphones, sotakaful may best be sold via their cellphones combined with the internetor/and social media.

“Then there are unique generational preferences – chief among themthe propensity of younger people to conduct as much as possible oftheir lives online”

Source: (1) Google – Our Mobile Planet March 2014 (graph) (2) French, O’Neill. The future of life insurance. E&Y Fall 2012.

20Actuarial Partners

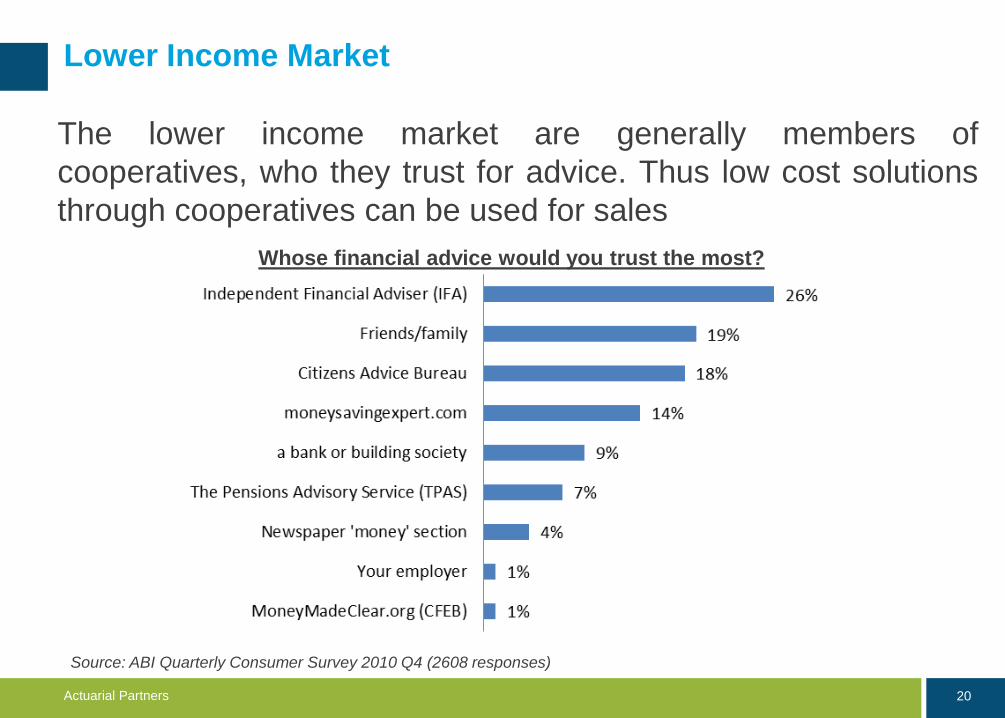

Lower Income Market

The lower income market are generally members ofcooperatives, who they trust for advice. Thus low cost solutionsthrough cooperatives can be used for sales

Source: ABI Quarterly Consumer Survey 2010 Q4 (2608 responses)

Whose financial advice would you trust the most?

21Actuarial Partners

Mosques are a natural means of sales and collections for a pure takaful pool

Sultan Omar Ali Saifuddin Mosque (Bandar Seri Begawan, Brunei) (Image Credit: Tylerdurden1)

22Actuarial Partners

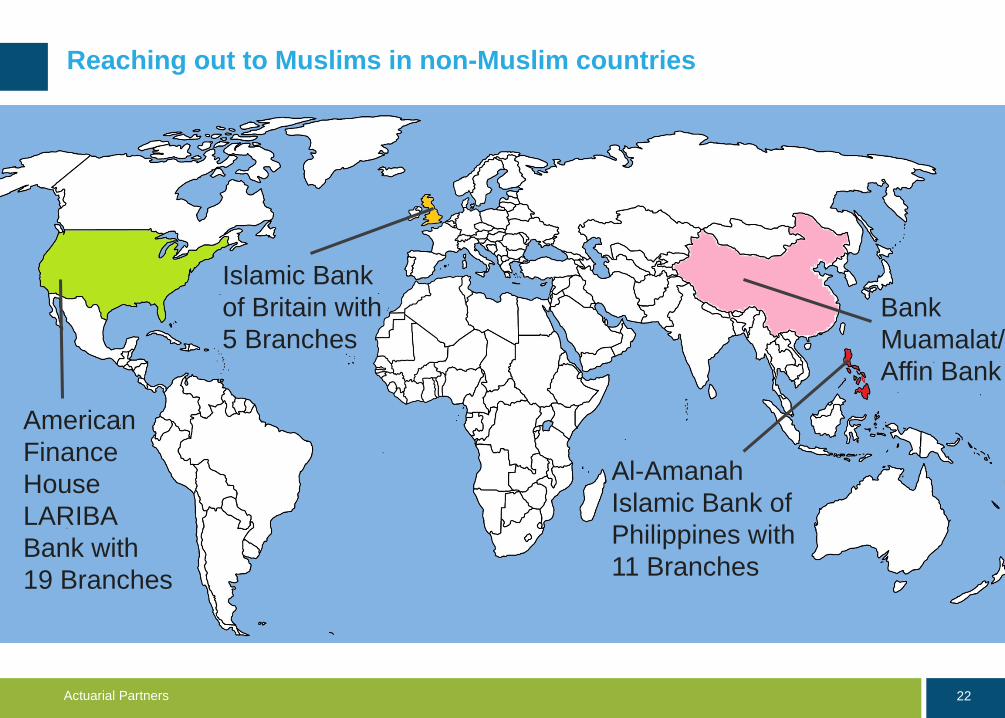

Reaching out to Muslims in non-Muslim countries

Put a map of the world and color in countries with Islamic banks and put some names of banks in. Intern….

American Finance House LARIBA Bank with 19 Branches

Islamic Bank of Britain with 5 Branches

Bank Muamalat/ Affin Bank

Al-AmanahIslamic Bank of Philippines with 11 Branches

23Actuarial Partners

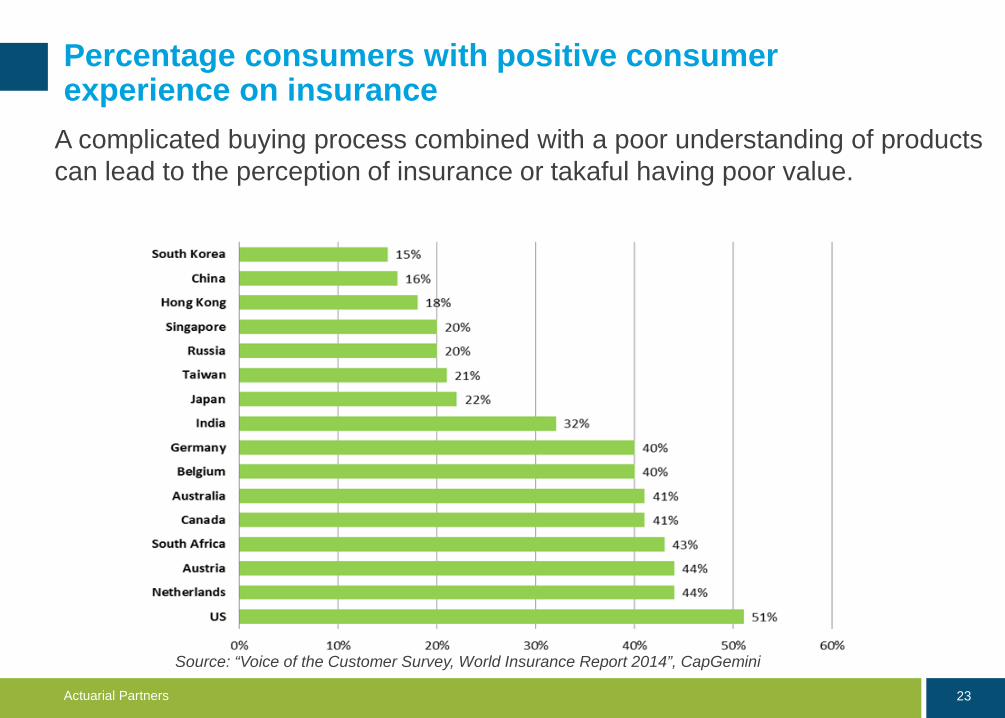

Percentage consumers with positive consumer experience on insurance

A complicated buying process combined with a poor understanding of productscan lead to the perception of insurance or takaful having poor value.

Source: “Voice of the Customer Survey, World Insurance Report 2014”, CapGemini

24Actuarial Partners

Simplifying the sales process

The need of medical underwriting only gives opportunities forbuyers to procrastinate.

Remove underwriting burdens from frontline sales using newsolutions in processes and technology.

25Actuarial Partners

Selling the appropriate products to the target market

Products sold need to be appropriate to the distribution channel.

Banca products:

Savings and investment products is consistent with thetypical mindset of banking consumers.

However it should not be in competition with bankingproducts, but complements it.

Direct sales channels (e.g. online, telemarketing) is onlyappropriate for simple products and for certain market segments(e.g. internet savvy and financial savvy individuals).

Products for the younger generation ideally should be packagedtogether with another commodity (e.g. gym membership)

Products for the low income group need to be very simple and takeinto account affordability of consumers.

26Actuarial Partners

Takaful annuities

With increasing longevity risk in most parts of the world, there is ademand for retirement products.

Defined ambition pensions:

Sharing the unknowns

Minimising guarantees

Addressing some of the financial needs at retirement

Takaful annuities can be structured similar

to defined ambition pensions, sharing the risk with

participants and minimising capital requirements

27Actuarial Partners

Conclusion

Developing affordable products and using the appropriatedistribution channel are essential factors to tap into the marketgaps of younger ages as well as the lower income groups.

The product gap at retirement continues to be a challenge.

Diversification into other distribution channels will likely gainstrength.

The sales process should be simplified.

In developed and internet-savvy countries such as the UK,France and Germany with a large proportion of Muslimminority, banca and the internet are likely to be one of themore effective approach to sell takaful.

28Actuarial Partners

Q & A

Suite 17.02, Kenanga InternationalJalan Sultan Ismail

50250 Kuala Lumpur, MalaysiaTel 603 2161 0433

www.actuartialpartners.com