innovation in the new reality - deloitte in the new reality ... walt disney & nbc & news...

TRANSCRIPT

Innovation in the New Reality

Dutch Oil & Gas Conference

Bart Cornelissen, Rotterdam, June 27th 2016

© 2016 Monitor Deloitte The Netherlands

• Innovation in Oil & Gas - A new reality?

• The challenge – Cost reduction & beyond

• Collaboration – The way forward

• Building effective ecosystems

Topics for discussion

2

© 2016 Monitor Deloitte The Netherlands

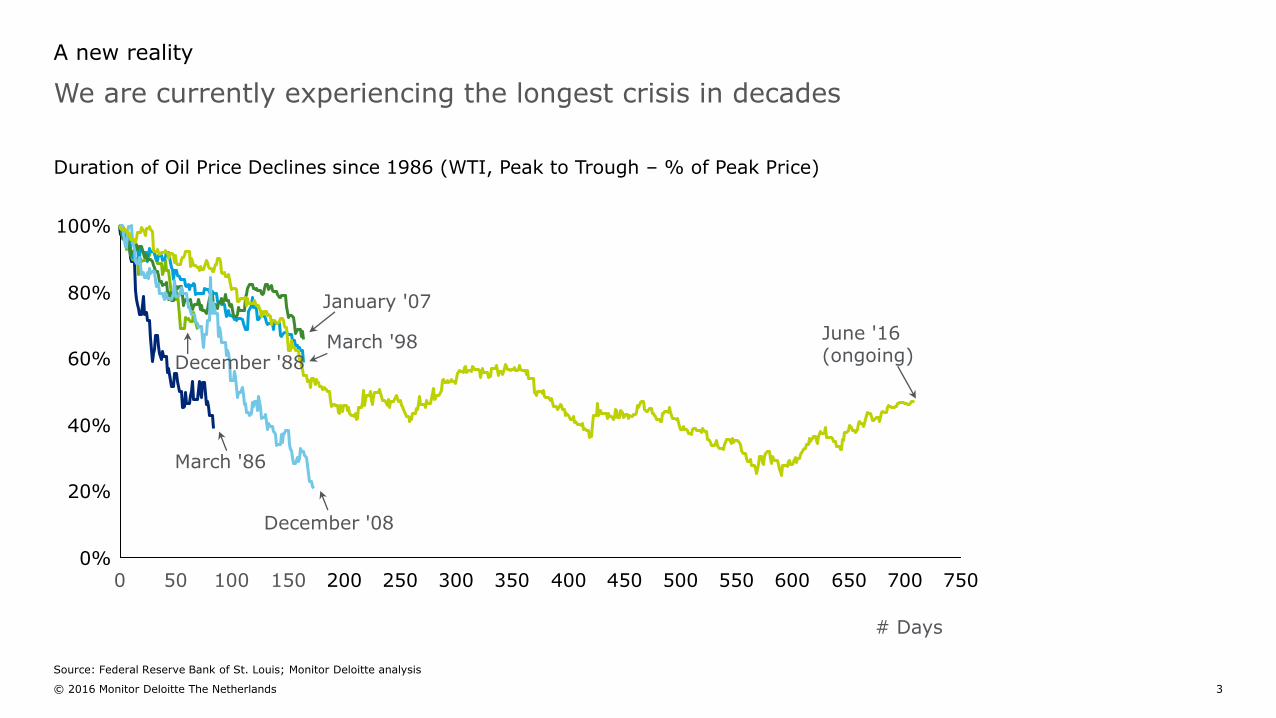

Duration of Oil Price Declines since 1986 (WTI, Peak to Trough – % of Peak Price)

We are currently experiencing the longest crisis in decades

A new reality

3

40%

100%

80%

60%

0%750

20%

700650250 400 4503502001000 500 600300 55050 150

# Days

Source: Federal Reserve Bank of St. Louis; Monitor Deloitte analysis

March '86

December '88

December '08

January '07

March '98 June '16 (ongoing)

© 2016 Monitor Deloitte The Netherlands

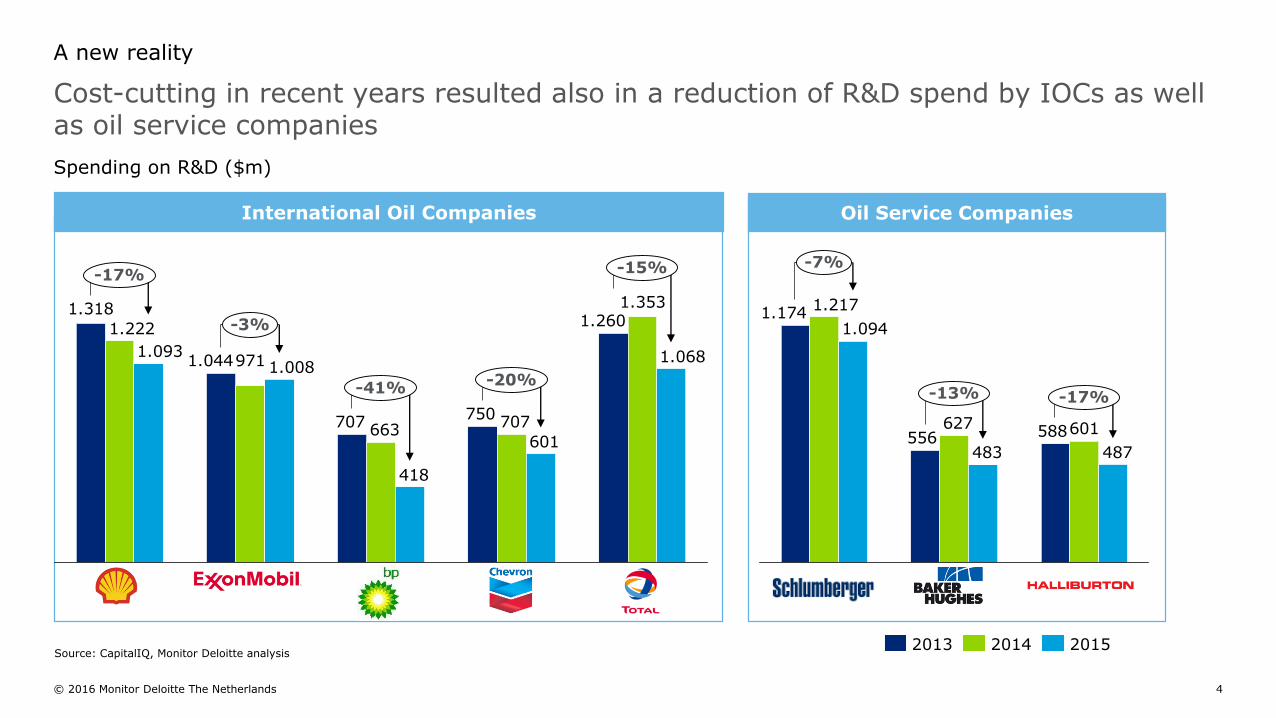

Spending on R&D ($m)

Cost-cutting in recent years resulted also in a reduction of R&D spend by IOCs as well as oil service companies

A new reality

4

Oil Service CompaniesInternational Oil Companies

Source: CapitalIQ, Monitor Deloitte analysis

1.260

750707

1.044

1.318 1.353

707663

971

1.222

1.068

601

418

1.0081.093

-20%

-15%

-41%

-17%

-3%

20142013 2015

588556

1.174

601627

1.217

487483

1.094

-13% -17%

-7%

© 2016 Monitor Deloitte The Netherlands

0

40

60

20

50

10

70

30

Oil Price ($/bbl)

19941992 200019901986 1996 19981988 2002

0

200

300

100

800

700

500

600

400

900

Index price ($)

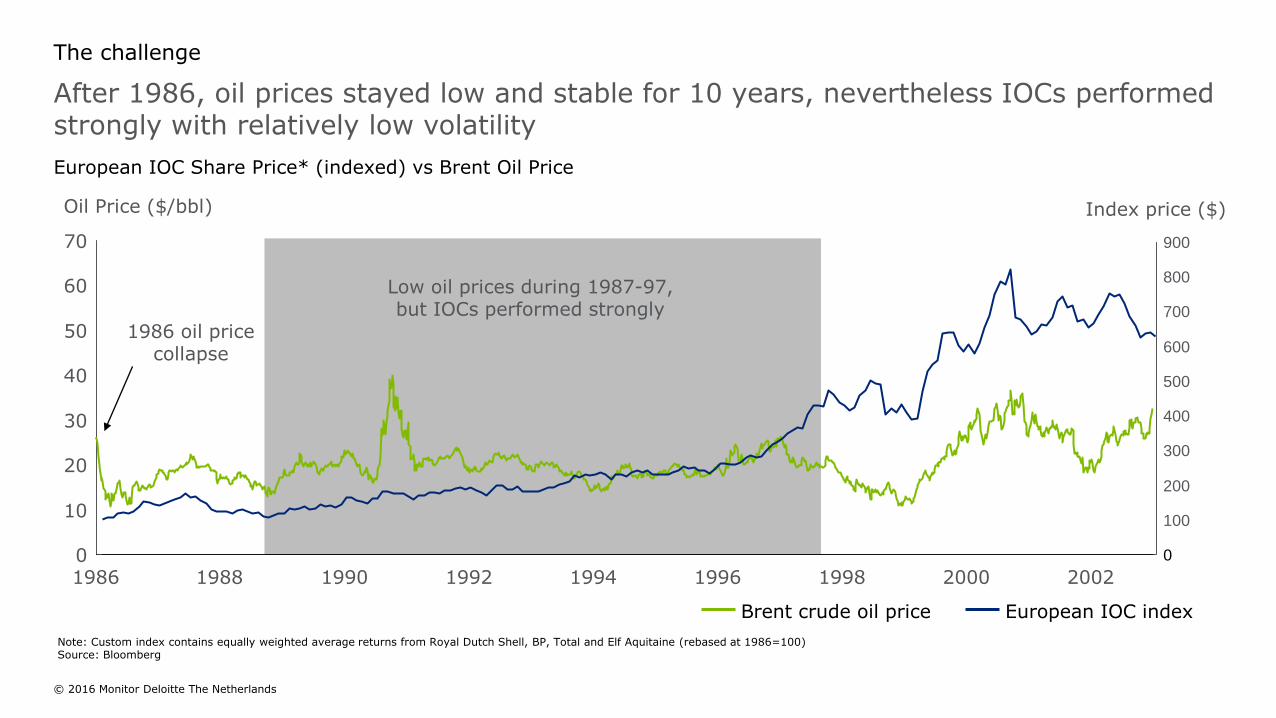

European IOC Share Price* (indexed) vs Brent Oil Price

After 1986, oil prices stayed low and stable for 10 years, nevertheless IOCs performed strongly with relatively low volatility

The challenge

Note: Custom index contains equally weighted average returns from Royal Dutch Shell, BP, Total and Elf Aquitaine (rebased at 1986=100)Source: Bloomberg

Brent crude oil price

1986 oil pricecollapse

European IOC index

Low oil prices during 1987-97, but IOCs performed strongly

© 2016 Monitor Deloitte The Netherlands

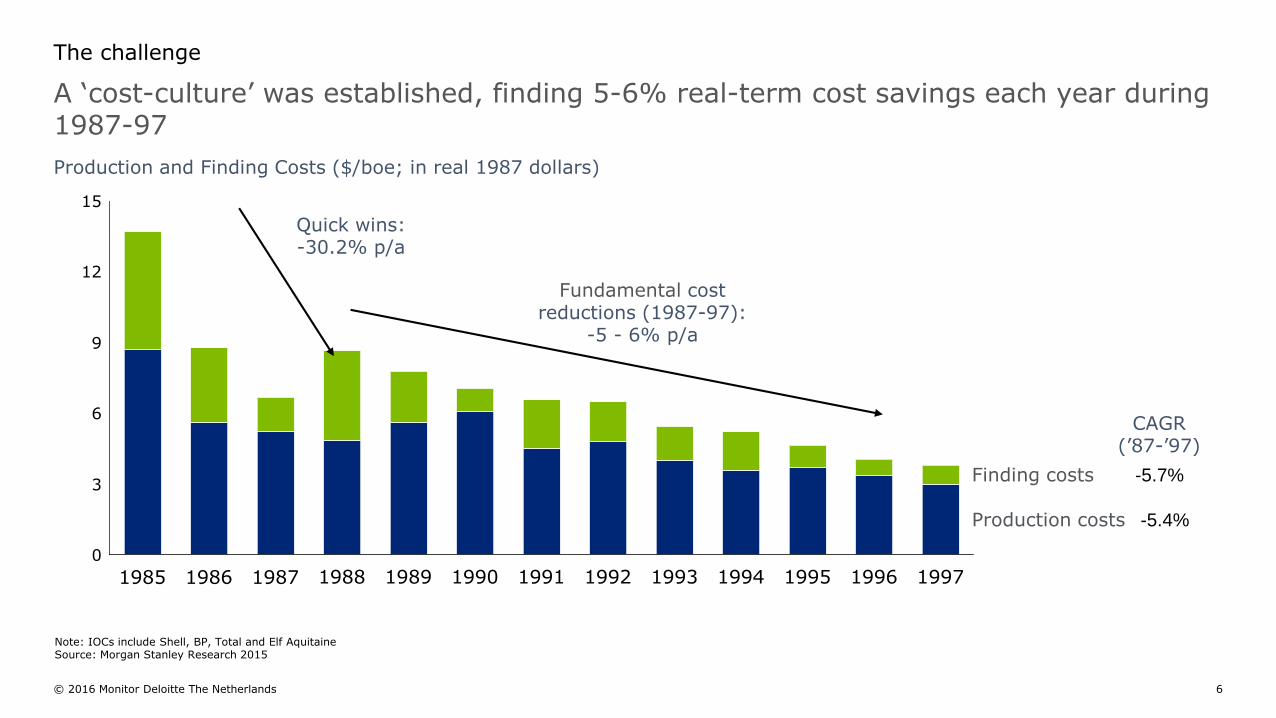

Production and Finding Costs ($/boe; in real 1987 dollars)

A ‘cost-culture’ was established, finding 5-6% real-term cost savings each year during 1987-97

The challenge

6

3

15

12

9

6

0

1994199319911989

Finding costs -5.7%

19971995 199619921990198819871985 1986

Production costs -5.4%

CAGR (’87-’97)

Fundamental costreductions (1987-97):

-5 - 6% p/a

Quick wins:-30.2% p/a

Note: IOCs include Shell, BP, Total and Elf AquitaineSource: Morgan Stanley Research 2015

© 2016 Monitor Deloitte The Netherlands

240

200

160

80

120

0

40

20102008 20112006 2014201320122002 2007200420032001 20152000 2005 2009

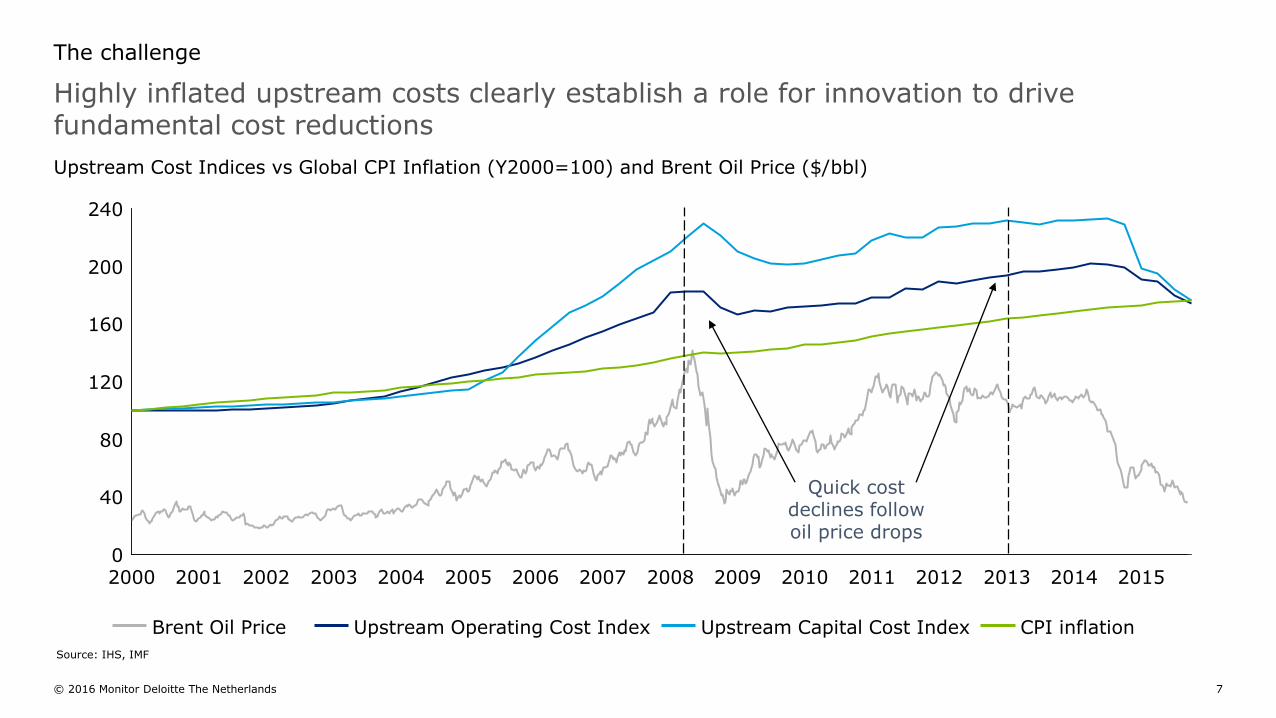

Upstream Cost Indices vs Global CPI Inflation (Y2000=100) and Brent Oil Price ($/bbl)

Highly inflated upstream costs clearly establish a role for innovation to drive fundamental cost reductions

The challenge

7

Source: IHS, IMF

CPI inflationUpstream Capital Cost IndexUpstream Operating Cost IndexBrent Oil Price

Quick costdeclines follow oil price drops

© 2016 Monitor Deloitte The Netherlands

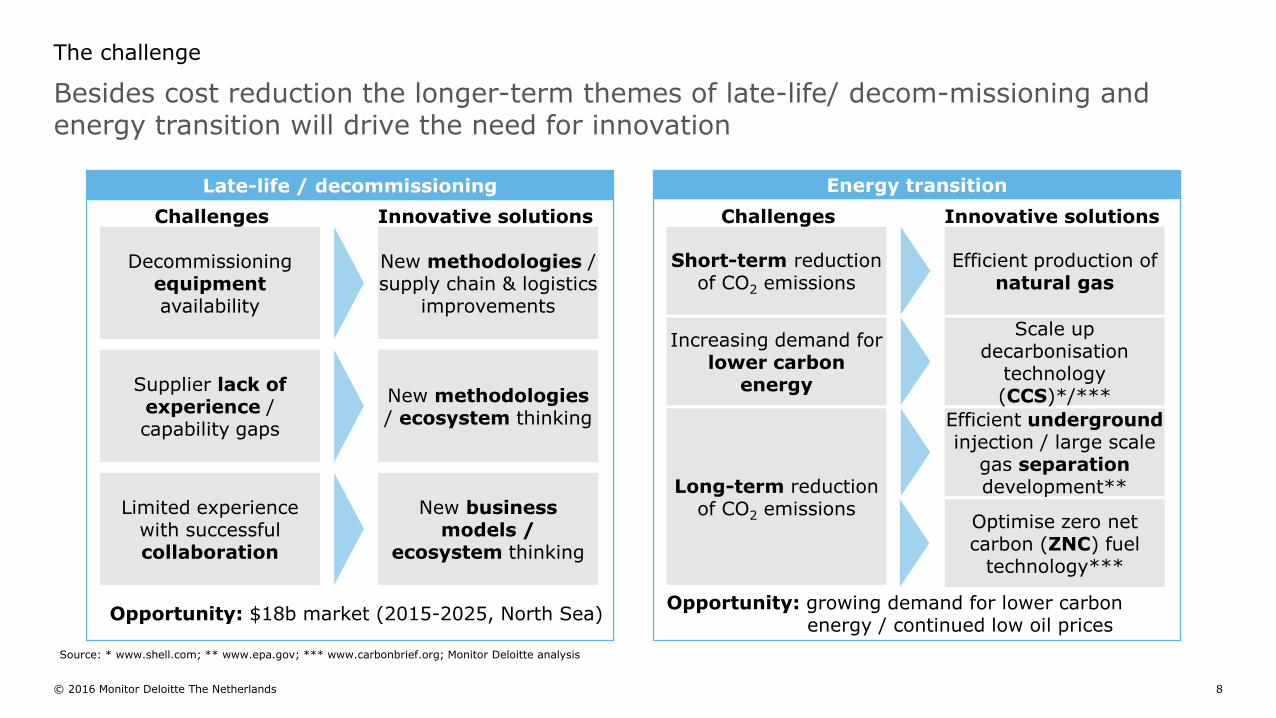

Besides cost reduction the longer-term themes of late-life/ decom-missioning and energy transition will drive the need for innovation

The challenge

8

Late-life / decommissioning

Challenges Innovative solutions

Decommissioning equipmentavailability

New methodologies /supply chain & logistics

improvements

Supplier lack of experience / capability gaps

New methodologies/ ecosystem thinking

Limited experience with successful collaboration

New business models /

ecosystem thinking

Opportunity: $18b market (2015-2025, North Sea)

Energy transition

Challenges Innovative solutions

Short-term reduction of CO2 emissions

Efficient production of natural gas

Increasing demand for lower carbon

energy

Scale up decarbonisation

technology (CCS)*/***

Long-term reduction of CO2 emissions

Efficient undergroundinjection / large scale

gas separationdevelopment**

Optimise zero net carbon (ZNC) fuel

technology***

Opportunity: growing demand for lower carbon energy / continued low oil prices

Source: * www.shell.com; ** www.epa.gov; *** www.carbonbrief.org; Monitor Deloitte analysis

© 2016 Monitor Deloitte The Netherlands

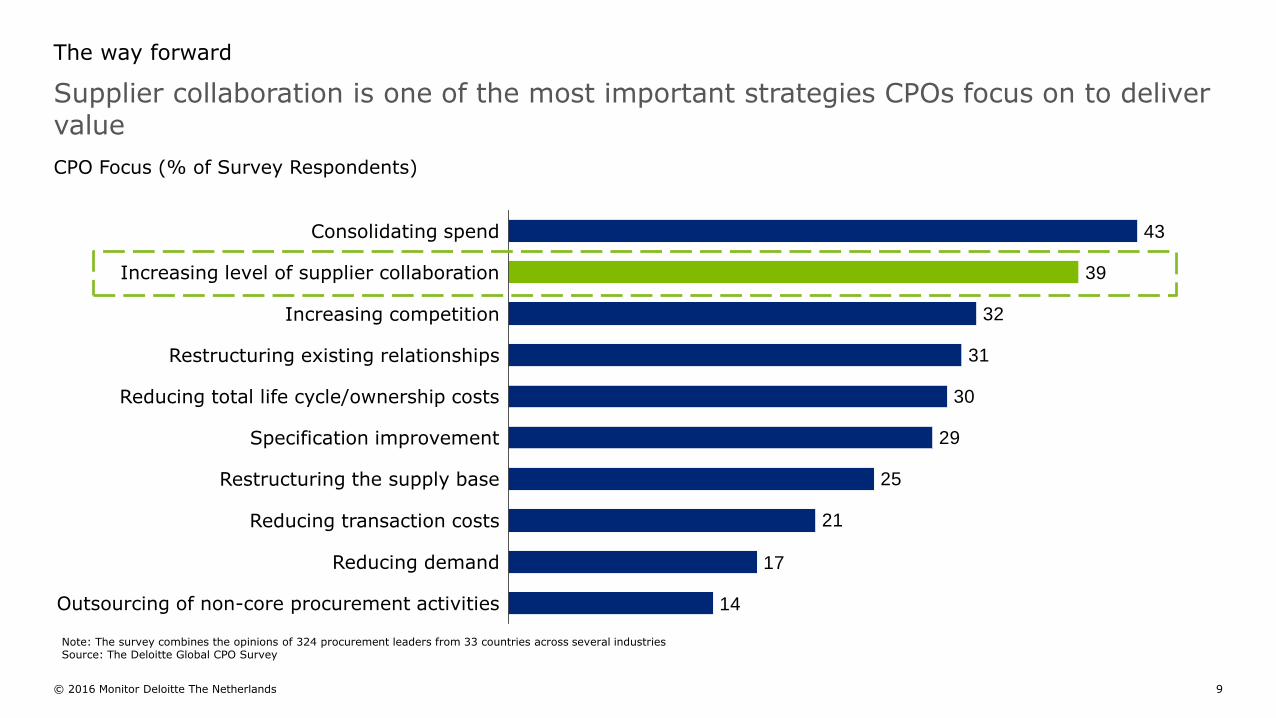

CPO Focus (% of Survey Respondents)

Supplier collaboration is one of the most important strategies CPOs focus on to deliver value

The way forward

9

14

17

21

25

29

30

31

32

39

43

Restructuring existing relationships

Reducing total life cycle/ownership costs

Restructuring the supply base

Specification improvement

Consolidating spend

Reducing transaction costs

Increasing level of supplier collaboration

Increasing competition

Reducing demand

Outsourcing of non-core procurement activities

Note: The survey combines the opinions of 324 procurement leaders from 33 countries across several industriesSource: The Deloitte Global CPO Survey

© 2016 Monitor Deloitte The Netherlands

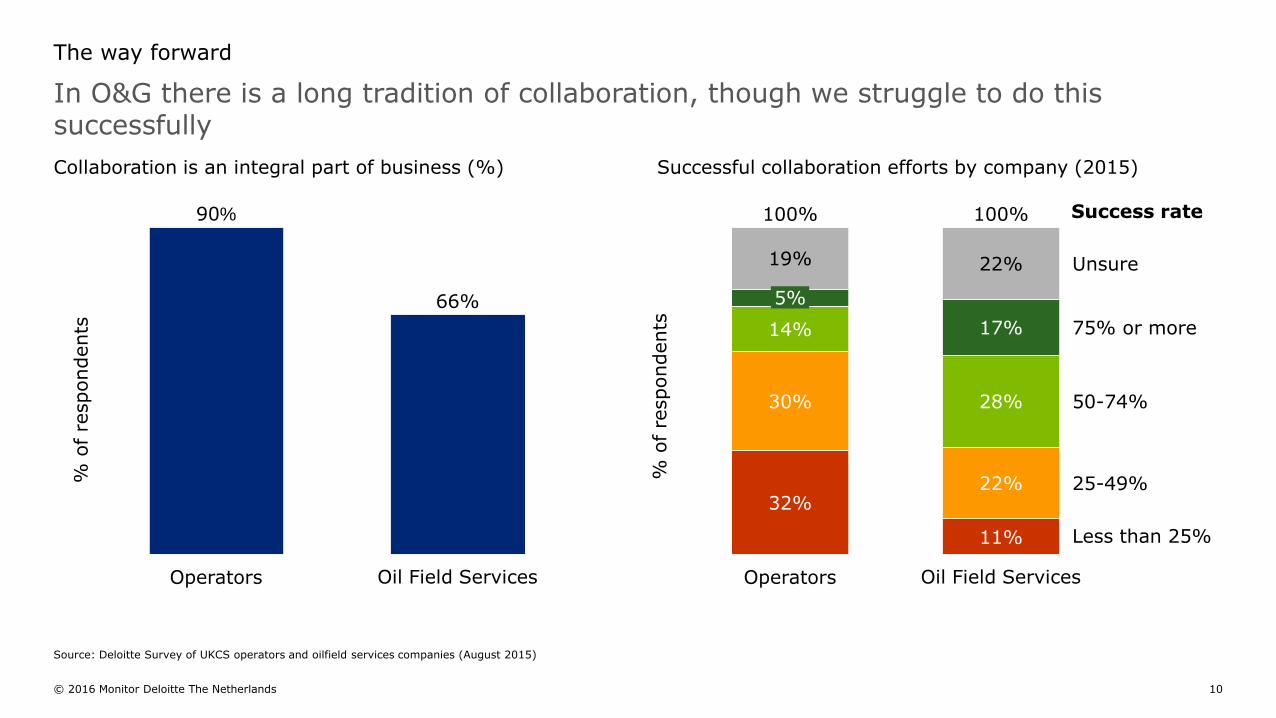

Collaboration is an integral part of business (%) Successful collaboration efforts by company (2015)

In O&G there is a long tradition of collaboration, though we struggle to do this successfully

The way forward

10

90%

66%

Oil Field ServicesOperators

Less than 25%

25-49%

50-74%

75% or more17%

100%

28%

32%

30%

14%

Unsure

100%

19%

Operators Oil Field Services

22%

22%

5%

11%

Success rate

% o

f re

spondents

% o

f re

spondents

Source: Deloitte Survey of UKCS operators and oilfield services companies (August 2015)

© 2016 Monitor Deloitte The Netherlands

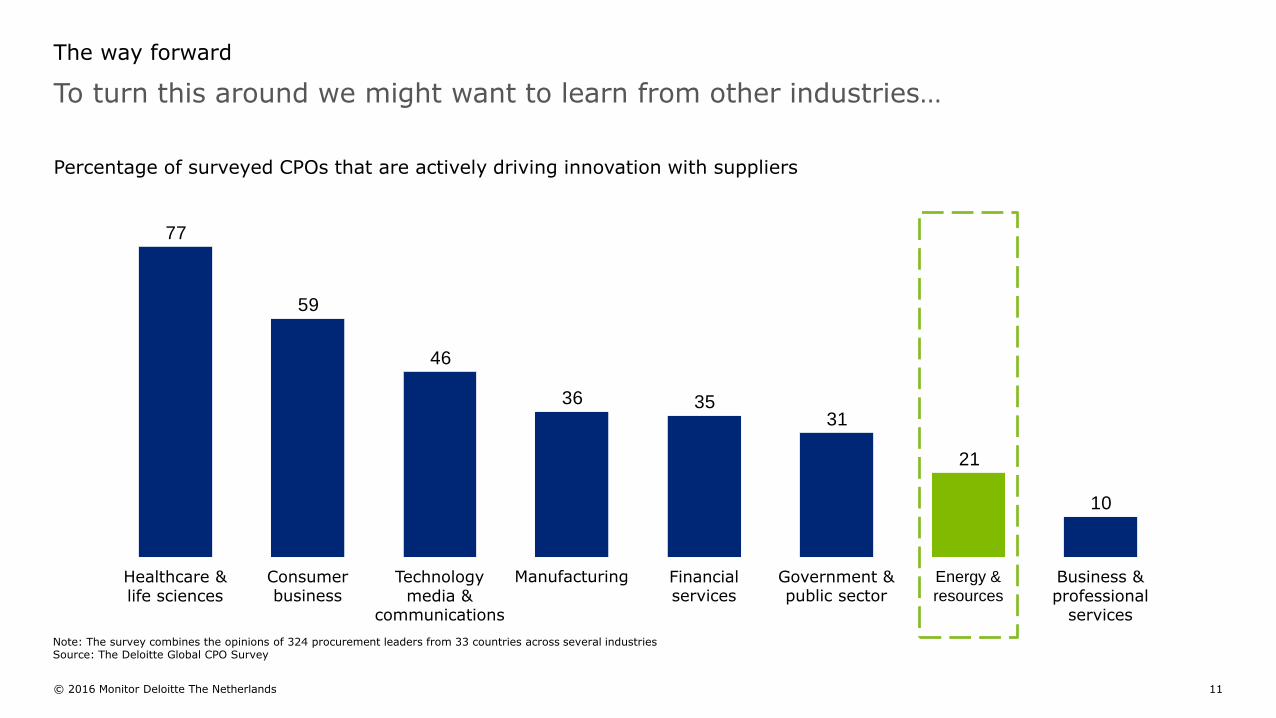

Percentage of surveyed CPOs that are actively driving innovation with suppliers

To turn this around we might want to learn from other industries…

The way forward

11

10

21

313536

46

59

77

Healthcare & life sciences

Financial services

Technology media &

communications

Manufacturing Energy &

resources

Consumer business

Business & professional

services

Government & public sector

Note: The survey combines the opinions of 324 procurement leaders from 33 countries across several industriesSource: The Deloitte Global CPO Survey

© 2016 Monitor Deloitte The Netherlands

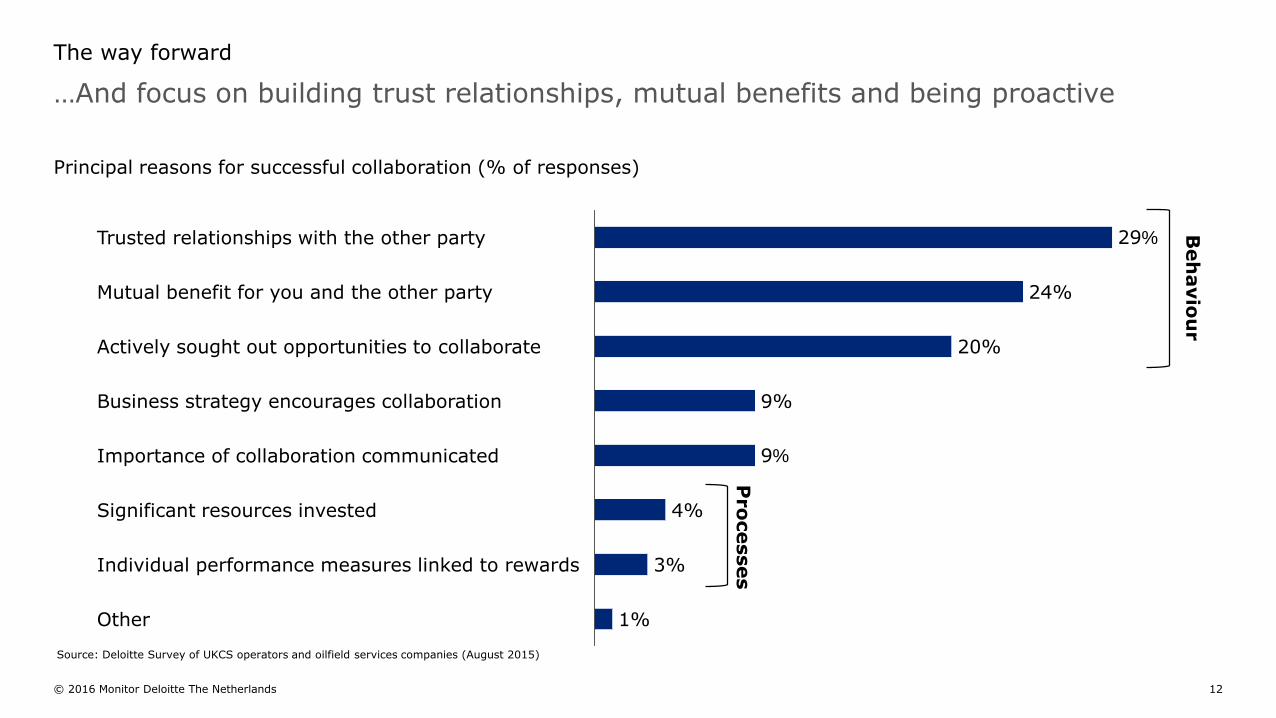

Principal reasons for successful collaboration (% of responses)

…And focus on building trust relationships, mutual benefits and being proactive

The way forward

12

Importance of collaboration communicated

9%

Actively sought out opportunities to collaborate 20%

1%

4%

29%

24%

Other

Individual performance measures linked to rewards

9%

3%

Business strategy encourages collaboration

Significant resources invested

Mutual benefit for you and the other party

Trusted relationships with the other party

Beh

avio

ur

Pro

cesses

Source: Deloitte Survey of UKCS operators and oilfield services companies (August 2015)

© 2016 Monitor Deloitte The Netherlands

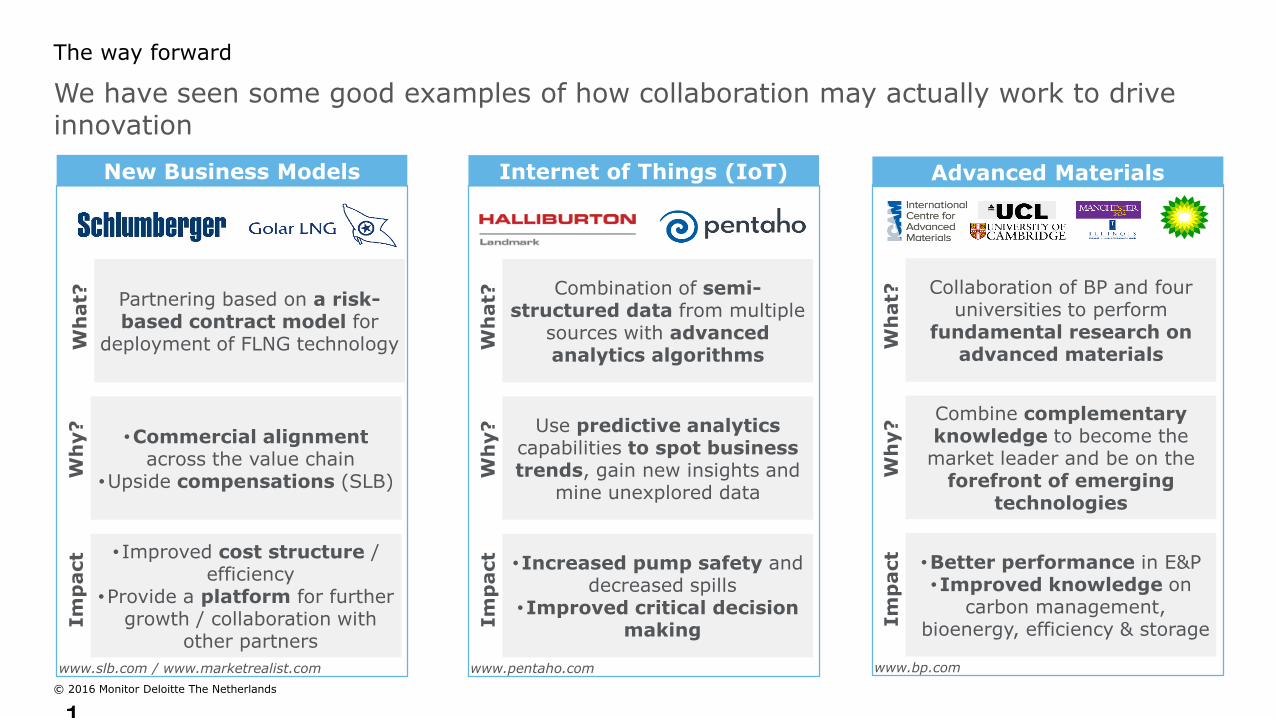

We have seen some good examples of how collaboration may actually work to drive innovation

The way forward

1

Internet of Things (IoT)

Combination of semi-structured data from multiple

sources with advanced analytics algorithms

Use predictive analytics capabilities to spot business trends, gain new insights and

mine unexplored data

•Increased pump safety and decreased spills

•Improved critical decision making

Wh

at?

Wh

y?

Im

pact

www.pentaho.com

Advanced Materials

Collaboration of BP and four universities to perform

fundamental research on advanced materials

Combine complementary knowledge to become the market leader and be on the

forefront of emerging technologies

•Better performance in E&P•Improved knowledge on

carbon management, bioenergy, efficiency & storage

Wh

at?

Wh

y?

Im

pact

www.bp.com

New Business Models

Partnering based on a risk-based contract model for

deployment of FLNG technology

•Commercial alignment across the value chain

•Upside compensations (SLB)

• Improved cost structure / efficiency

•Provide a platform for further growth / collaboration with

other partners

Wh

at?

Wh

y?

Im

pact

www.slb.com / www.marketrealist.com

© 2016 Monitor Deloitte The Netherlands

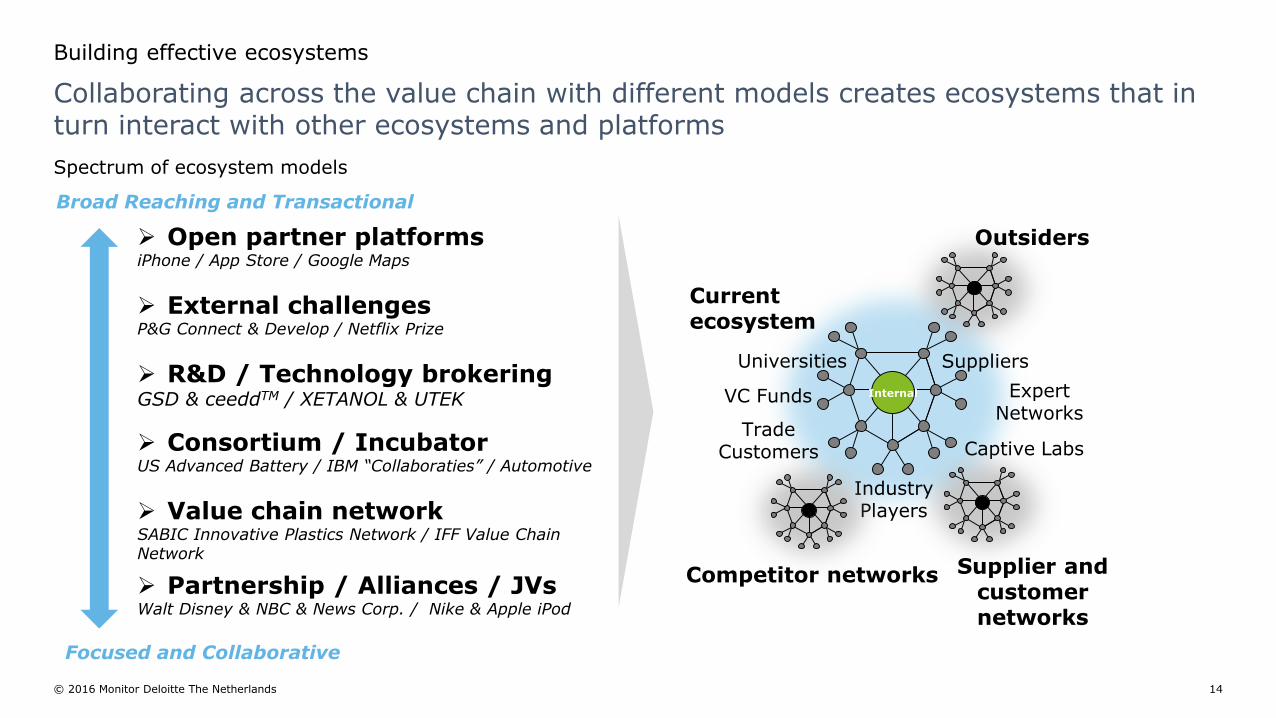

Open partner platformsiPhone / App Store / Google Maps

External challengesP&G Connect & Develop / Netflix Prize

R&D / Technology brokeringGSD & ceeddTM / XETANOL & UTEK

Consortium / IncubatorUS Advanced Battery / IBM “Collaboraties” / Automotive

Value chain networkSABIC Innovative Plastics Network / IFF Value Chain Network

Partnership / Alliances / JVsWalt Disney & NBC & News Corp. / Nike & Apple iPod

Spectrum of ecosystem models

Collaborating across the value chain with different models creates ecosystems that in turn interact with other ecosystems and platforms

Building effective ecosystems

14

Captive Labs

SuppliersUniversities

Trade Customers

Industry Players

Expert Networks

VC Funds Internal

Competitor networks Supplier and customernetworks

Outsiders

Current ecosystem

Broad Reaching and Transactional

Focused and Collaborative

© 2016 Monitor Deloitte The Netherlands

In order to be successful, eight key elements need to be properly covered in the ecosystem

Building effective ecosystems

15

PARTNERS

STRATEGIC ALLIANCE

CHALLENGES

OPPORTUNITIESEXTERNAL EXPERTISE

ANALOGIES

KNOWLEDGE SHARING

SPONSORING & INCENTIVESIdentify & manage partner & portfolio relationships

Define long-term collaborative strategy fitting for all partners

Frame market problem statements and challenges

Create high impact opportunities

Attract relevant external expertise

Spot useful analogies in external companies and adjacent industries

Define optimal levels of IP and knowledge sharing with

partners

Provide sponsorships, metrics & incentives

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firmsare legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.nl/about for a more detailed description of DTTL and its memberfirms.

Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. Deloitte serves four out of five Fortune Global 500®companies through a globally connected network of member firms in more than 150 countries bringing world-class capabilities, insights, and high-quality service to address clients’ most complex business challenges.To learn more about how Deloitte’s approximately 225,000 professionals make an impact that matters, please connect with us on Facebook, LinkedIn, or Twitter.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of thiscommunication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entityin the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2016 Monitor Deloitte The Netherlands