innovative enterprise and sustainable prosperity* · innovative enterprise and sustainable...

TRANSCRIPT

InnovativeEnterpriseandSustainableProsperity*

WilliamLazonickUniversityofMassachusettsLowell

October10,2017

*ThisessayformsthebasisforapresentationthatIwillmakeattheannualconferenceoftheInstituteforNewEconomicThinkinginEdinburgh,Scotland,October23,2017.ItalsoprovidesthesubstanceofmyFreemanLectureatthe15thGlobelicsConferenceattheNationalTechnicalUniversityofAthensinAthens,Greece,onOctober11,2017aswellasmycontributiontotheConferenceontheManyFuturesofWork,runbytheInstituteforWorkandtheEconomyinChicago,Illinois,October5,2017.

TheresearchthatunderpinsthisessayhasbeenfundedbytheInstituteforNewEconomicThinking(seehttps://www.ineteconomics.org/research/experts/wlazonick); Ford Foundation (project on FinancialInstitutions for Innovation and Development: www.fiid.org); European Commission Horizon 2020Research and Innovation Programme under grant agreement No. 649186 (ISIGrowth: Innovation-Fuelled Sustainable and Inclusive Growth: http://www.isigrowth.eu/); and the Gatsby Foundation(project on Governing Financialisation, Innovation and Productivity in UK manufacturing:https://www.soas.ac.uk/news/newsitem121890.html). I thank Ken Jacobson and Jang-Sup Shin forcommentsonthematerialinthisessay.

Lazonick:InnovativeEnterpriseandSustainableProsperity

1

Abstract

Wewantaneconomythatgeneratesstableandequitablegrowth—orwhatIcall“sustainableprosperity.”Wewantproductivitygrowth thatmakes itpossibleforthepopulationtohavehigher livingstandardsovertime.Wewantanequitablesharingofthegainsfromproductivitygrowthamongthosewhoseworkeffortsandfinancialresourcescontributetothatgrowth.Andwewantsufficientjobstabilitytoenableworkerstoremaininproductiveemploymentforsomefourdecadesatworkwhileprovidingthemwithenoughsavingstoprovidethemwithadequateincomesoversometwodecadesofretirement.Weneedinnovativeenterprisetoachievesustainableprosperity.Innovation,definedasahigher-qualityproductatalowerunitcostthanhadpreviouslybeenavailable,generatestheproductivitythatunderpinsstable and equitable growth. The innovative enterprise is the linchpin of investment in productivecapabilities through the interaction of households, governments, and businesses—orwhat I call “theinvestment triad.” In this essay, I outline The Theory of Innovative Enterprise (TIE) as a conceptualframeworkforanalyzinghowaneconomycanachievesustainableprosperity.TIEtransformsourunderstandingofhowtheeconomyfunctionsandperforms.TIEexposestheabsurdityoftheneoclassicaleconomicsconceptof“perfectcompetition,”taughttomillionsofstudentseveryyear,whichpositsthattheunproductivefirmisthefoundationofthemostefficienteconomy.IputforwardTIEasarelevantandrigorousreplacementforneoclassicaltheory.TIEcanexplainhowtheU.S.economy(asa foremost example among the rich nations of the world) displayed a tendency toward stable andequitablegrowthintheimmediatepost-WorldWarIIdecadesbutthen,fromthelasthalfofthe1970s,enteredintoaneraofunstableemployment,inequitableincome,andsaggingproductivity.Driving this epochal change was the transformation of the dominant regime of corporate resourceallocationfrom“retain-and-reinvest”to“downsize-and-distribute.”Underaretain-and-reinvestregime,companiesretaincorporaterevenuesandreinvestinproductivecapabilities,includingthoseofthelaborforce,thatcangenerateinnovativeproducts.Underadownsize-and-distributeregime,seniorcorporateexecutives—incentivizedbystock-basedpayandpressuredbyfinancialpredators—focusondownsizingthe labor force (laying off workers, cutting their pay, neglecting training) and distributing corporaterevenuestoshareholdersintheformsofcashdividendsandstockrepurchases.Thecorporateproclivitytodownsize-and-distributehasbecomesoextremeintheUnitedStatesthatitcannowbetermedthe(largelylegal)lootingofthebusinesscorporation.Itbearsprimeresponsibilityforextremeconcentrationofincomeamongtheveryrichesthouseholdsandtheongoingerosionofmiddle-classemploymentopportunities.Legitimizingthislootingofthebusinesscorporationistheneoclassicaltheoryofthemarketeconomyandits particular “agency theory” application, with its mantra that, for the sake of economic efficiency,businessenterprisesshouldberunto“maximizeshareholdervalue”(MSV).Inthisessay,Iexplainwhy,farfrombeingatheoryofvaluecreation,MSVisanideologyofpredatoryvalueextraction.IconcludebyarguingthattheeradicationofMSVideologyisanecessaryconditionforenablinganeconomy’sbusinessenterprises to contribute to, rather than undermine, the achievement of sustainable prosperity. Toprovideuswitharationalintellectualfoundationforspecificpolicyproposalstostopthelootingofthebusiness corporation—including a ban on stock buybacks, radical changes in incentives for seniorcorporateexecutives,representationofworkersandtaxpayersoncorporateboards,andreformofthetaxsystemtosupporttheinvestmenttriad—Icallforinnovationtheorytoreplaceagencytheoryinourconceptualization—andteaching—ofhowasuccessfuleconomyoperatesandperforms.

Lazonick:InnovativeEnterpriseandSustainableProsperity

2

1. Investmentinproductivecapabilities1Wewantaneconomythatgeneratesstableandequitablegrowth—orwhatIcall“sustainableprosperity.”Wewant productivity growth thatmakes it possible for the population to havehigher standards of living.Wewant stableemployment opportunities that enable people toremainproductiveforsomefourdecadesoftheirworkingliveswhileprovidingthemwithenoughsavingsforadequateincomesoversometwodecadesofretirement.Andwewantanequitablesharingof incomeamong thosewhoseworkeffortsand financial resourcescontribute to thenation’sproductivity.Sincethe1980s,theU.S.economyhasexperiencedunstableemployment,inequitableincome,andsaggingproductivity—theoppositeofsustainableprosperity.ThepurposeofthisessayistoarguethatacriticalfirststepinattainingsustainableprosperityintheUnitedStates,oranyothernationaleconomy,istochangetheintellectualunderstandingofacademics,policy-makers,andtheinformedpublicabouthowamoderneconomyoperatesandperforms.Iarguethatwecannotpursueacoherentsetofpublicpoliciestogeneratestableandequitableeconomicgrowthunlesswerejecttheneoclassicaltheoryofthemarketeconomyandreplaceitwithaneconomictheorythatfocusesonhoworganizations,includinghouseholds,governments,andbusinesses,investinproductivecapabilities,withatheoryofinnovativeenterpriseatitscore.Sustainableprosperity requires innovativeenterprise. Theessenceof innovativeenterprise isinvestmentinproductivecapabilitiesthatcangenerategoodsandservicesthatarehigherqualityand/orlowercostthanthosethathadpreviouslybeenavailable.Theinnovativeenterprisetendsto be abusiness enterprise—a unit of strategic control that over timemustmake profits tosurvive.But,inamodernsociety,businessenterprisesarenotaloneinmakinginvestmentsinthe productive capabilities required to generate innovative goods and services. Householdfamiliesandgovernmentagenciesalsomakeinvestmentsinproductivecapabilitiesuponwhichbusiness enterprises rely. Working in a harmonious fashion, I call these three types oforganizations—household families, government agencies, and business enterprises—“theinvestmenttriad.”Householdfamiliesinvestintheeducationoftheyoungwithaviewtoprovidingthemwiththeknowledgethattheywillneedtofunctionasproductiveadults,whowillthenusetheincomefromproductiveemploymenttohavefamiliesoftheirown.Criticaldeterminantsofhouseholdinvestments in productive capabilities are the relation between spouses as providers ofhouseholdcareandincome,thequalityofeducationthattheyoungareabletoreceive,andthenumber of years over which they receive their education. A productive society requires thepresenceofthesupportivefamily.Governmentagenciessupporttheinvestmentsinproductivecapabilitiesbyhouseholdfamiliesbyprovidingschoolingthathouseholds,eachactingonitsown,couldnotafford.Awell-financedprimary,secondary,andtertiaryeducationsystemisanecessaryconditionforamodernsocietytoembarkonapathofsustaineddevelopmentthroughwhichmostofthepopulationcanattain1GiventheoverarchingperspectiveoninnovativeenterpriseandsustainableprosperitythatIprovideinthisessay,mostofthebibliographicreferencesaretomyownpublications,inwhichthereadercanfindthesourcesformyarguments.

Lazonick:InnovativeEnterpriseandSustainableProsperity

3

higher standards of living.2 Government agencies can also be charged with investing in thecreation,throughbasicandappliedresearch,ofnewscientificandengineeringknowledgethatwouldotherwisenotcomeintoexistence.Asacriticalcomponentofinvestmentinproductivecapabilities, government agencies are involved in providing services for public and personalhealth.Inaddition,werelyongovernmentagenciestoinvestinphysicalinfrastructuresuchastransportationsystems,communicationsystems,energysystems,andwaterandwastesystems.Taken together, the investments in productive capabilities, both human and physical, bygovernmentagenciesmanifestthepresenceofthedevelopmentalstate.Business enterprisesmake use of the knowledge and infrastructure provided by governmentagenciesandthehumancapabilitiesprovidedbyhouseholdfamiliesasfoundationsformakingfurther in-house investments inhumanandphysicalcapabilities thatcangenerategoodsandservices that these businesses can sell on product markets. In high-tech fields, businessenterprisesmayhavetomakespecializedinvestmentsinin-housecapabilitiestoabsorbthehigh-tech knowledge that investments by government agencies have created. In many cases,government agencies make strategic investments in knowledge-creation through businessenterprises in the forms of research contracts and subsidies. Of particular importance, it istypicallythroughon-the-jobexperienceinbusinessenterprisesaswellasgovernmentagenciesthat masses of individuals, building on their formal educations, accumulate the productivecapabilities that enable them to contribute to the innovation process. The development andutilizationoftheseproductivecapabilitiesaretheessenceoftheinnovativeenterprise.Theinvestmenttriadenablesinnovativeenterprisetofunctionasafoundationforsustainableprosperity.Stableandequitablegrowthoccurswhentheinvestmentstrategiesofhouseholds,governments, and businesses interact as supportive families, developmental states, andinnovativeenterprises.Householdsandgovernmentsinteractthroughinvestmentsineducation.Governments and businesses interact in the development of the high-tech knowledge base.Businesses and households interact through the employment relation. The quality of theseinteractionsinthedevelopmentandutilizationofproductivecapabilitiesisofcriticalimportancetotheproductivityofresourcesthatareinvestedintheinnovativeenterprise.Businessenterprisesprovideadultsinhouseholdfamilieswithemploymentthat,withsufficientproductivity, should enable them to support their families. Through formal and on-the-jobtraining,businessenterprisesalsoinvestintheknowledgeofsomeorallofthepeoplewhomtheyemploy.Theseenterprises thenhavean incentive to retain thepeoplewhomtheyhavetrained.Theygenerallydosothroughpayincreasesandpromotionstojobsthatrequiresuperiorfunctional capability andgreaterhierarchical responsibility. Indeed, it is primarily through in-housepay increasesandpromotions forvaluedemployees in stableemployment relations ininnovative enterprises that households’ living standards increase over time. It is through theemploymentrelationsofproductiveenterprises,notlabor-marketsupplyanddemand,thatwegetthethrivingmiddleclassthatisthesocialsubstanceofstableandequitablegrowth.

2WilliamLazonick,SustainableProsperityintheNewEconomy?BusinessOrganizationandHigh-techEmploymentintheUnitedStates,UpjohnInstituteforEmploymentResearch,2009,ch.5.

Lazonick:InnovativeEnterpriseandSustainableProsperity

4

In short, the investment triadputs inplace theproductivecapabilities thatareessential toaprosperouseconomy. Investments in theknowledgebasebyhousehold families,governmentagencies,andbusinessenterprisesmustbefinanced.Investmentsineducatingthelaborforceare generally fundedby some combinationof after-taxhousehold incomes supplementedbyhouseholddebtandgovernmenttaxrevenuessupplementedbydebtissuesatlocal,state,andfederal levels. To some extent business enterprises finance the education of the labor forcethrough corporate taxes, philanthropic contributions based on business fortunes, and directpayments to employees for the education of themselves or their children as part of theemploymentrelation.Ultimately, however, the ability of household families and government agencies to affordinvestments inproductivecapabilitiesrequirestheutilizationoftheknowledgeandskillsthathave been developed through these investments. And in a modern society, to ensure theutilizationoftheknowledgebasethathasbeendeveloped,werelyprimarilyonitsemploymentbybusinessenterprisesthat,tosurvive,mustproduceandsellcompetitive—thatis,highquality,lowcost—products.Theinnovativeenterpriseiscentraltothetriadicsocialsystemthatenablestheattainmentofsustainableprosperity.Inthenextsectionofthisessay, Icontrasttheinvestment-triadperspective,withitsfocusonorganizations—supportive families, developmental states, and innovative enterprises—as themicrofoundationsofsustainableprosperity,withtheneoclassicaleconomicstheorythatviewstheoperationofmarketsasthemicrofoundationsofthemostefficienteconomy.Ishowthattheneoclassicalperspective,whichistaughtbytensofthousandsofeconomicsPhDstomillionsofstudentsaroundtheworldeveryyear,restsontheabsurdpropositionthatthemostunproductivefirmisthefoundationofthemostefficienteconomy—anidealofeconomicorganizationknownas “perfect competition.” Indeed, the neoclassical theory of markets as omnipotent in theallocation of economy’s resources depends on a theory of the firm that portrays the idealbusinessenterpriseasimpotent.Asweshallsee,theneoclassicaltheoryofperfectcompetitionhasasitsrootsafirmthathasthecharacteristicsofanovercrowdedsweatshopinwhichworkersareunableandunwillingtobeproductive.Economicsisinneedofatheoryofinnovativeenterprisetoreplacetheneoclassicaltheoryofthefirm,andtherebyrecognizethecentralityoforganizationstotheeconomy’soperationandperformance,whileexploding“themythofthemarketeconomy.”3Thethirdsectionofthisessayoutlines the Theory of Innovative Enterprise (TIE) as a conceptual framework for analyzingwhether, how, and underwhat conditions the investment triad supports or undermines theattainmentofstableandequitablegrowth.DrawingontheexperienceoftheU.S.economyoverthepast70years,ImakeuseofTIEtoanalyzehowduringthefirstthreedecadesofthisperiod,the United States moved toward stable and equitable growth under a “retain-and-reinvest”corporate resource-allocation regime whereas from the late 1970s, under a “downsize-and-

3WilliamLazonick,BusinessOrganizationandtheMythoftheMarketEconomy,CambridgeUniversityPress,1991;WilliamLazonick,“TheTheoryoftheMarketEconomyandtheSocialFoundationsofInnovativeEnterprise,”EconomicandIndustrialDemocracy,24,1,2003:9-44;WilliamLazonick,“InnovativeEnterpriseorSweatshopEconomics?InSearchofFoundationsofEconomicAnalysis,”Challenge,59,2,2016:65-114.

Lazonick:InnovativeEnterpriseandSustainableProsperity

5

distribute” regime, unstable employment, inequitable income, and sagging productivity havecharacterizedtheU.S.economy.4In the fourth section of this essay, I place intellectual blame for the U.S. failure to achievesustainableprosperitysincethe1970sonaparticularbrandofneoclassicaleconomicsknownasagency theory, with its ideology that the business corporation should be run to “maximizeshareholder value” (MSV). Far from being a theory of value creation, MSV has legitimizedpredatory value extraction from U.S. business corporations. Effected through massivedistributionsofcorporatecashtoshareholdersandincentivizedbythestock-basedpayofseniorcorporate executives, MSV has resulted in the (largely legal) looting of the U.S. businesscorporation.IarguethatMSVhasunderminedinnovativeenterpriseandtheoperationoftheinvestment triad, andwith it thepossibility of achieving sustainable prosperity in theUnitedStates.Inthefinalsectionofthisessay,Iarguethat,asaconceptualguidetoformulatingpoliciestogettheU.S.economyonasustainable-prosperitytrajectory,innovationtheorymustreplaceagencytheory.IcontendthattheeradicationofMSVideologyisanecessaryconditionforenablinganeconomy’s business enterprises to contribute to, rather than thwart, the achievement ofsustainableprosperity.Toprovide the intellectual rationale for specificproposals (elaboratedelsewhere5)tostopthelootingofthebusinesscorporation—includingbanningstockbuybacks,compensatingseniorexecutivesfortheircontributionstothevalue-creatingenterprise,placingrepresentativesofhouseholdsasworkersandtaxpayersoncorporateboards,andreformingthetaxsystemsothatitrecognizesandsupportstheinvestmenttriad—Icallforinnovationtheorytoreplaceagencytheoryinourconceptualizationofhowtheeconomyoperatesandperforms.2. ThetheoryofthefirmandeconomicperformanceTheinvestment-triadperspectiveviewsorganizations,notmarkets,asthemicrofoundationsofsustainableprosperity.Comparative-historicalstudyrevealsthatdevelopedmarketsinproducts,finance, labor, and land are outcomes, not causes, of economic development.6 Productcompetitionassumestheexistenceofbusinessenterprisesthathavedevelopedthecapabilitiestoproducegoodsandservicesofaqualitythatbuyerswantandneedthatcanbesoldatpricesthatbuyersarewillingorabletopay.Developedmarkets instocksandbondsdependontheexistenceofbusinessenterpriseswiththecapabilitytoissueandpayyieldsonthesesecurities.Employment opportunities that can be accessed via labor markets assume the existence ofbusiness enterprises andgovernment agencies thathavedeveloped the capability to employ

4WilliamLazonickandMaryO’Sullivan,“MaximizingShareholderValue:ANewIdeologyforCorporateGovernance,”EconomyandSociety,29,1,2000:13-35.

5WilliamLazonick,“TheValue-ExtractingCEO:HowExecutiveStock-BasedPayUnderminesInvestmentinProductiveCapabilities,”InstituteforNewEconomicThinkingWorkingPaperNo.54,December4,2016,athttps://www.ineteconomics.org/research/research-papers/the-value-extracting-ceo-how-executive-stock-based-pay-undermines-investment-in-productive-capabilities

6Lazonick,BusinessOrganizationandtheMythoftheMarketEconomy;Lazonick,“TheTheoryoftheMarketEconomyandtheSocialFoundationsofInnovativeEnterprise”;WilliamLazonick,“VarietiesofCapitalismandInnovativeEnterprise,”ComparativeSocialResearch,24,2007:21-69.

Lazonick:InnovativeEnterpriseandSustainableProsperity

6

laborproductively.Amarketforlandexistsbecausehouseholds,governments,andbusinesseshaveinvestedintheinfrastructureofaparticularlocality.For the sake of continued innovation, the organizations onwhich the economy depends forinvestments inproductivecapabilitiesneedgovernmentstoregulatethesedevelopedmarketsoncetheyhaveemerged.7AsdemonstratedrepeatedlyinthehistoryofAmericancapitalism,intheabsenceofregulation,developedmarketstendtodisruptandunderminetheorganizationalprocessesthatenableinvestmentinproductivecapabilities.HerearejustafewexamplesfromthehistoryoftheUnitedStates:• Inthe1920s,industriessuchastextiles,coalmining,andagriculture,characterizedbylarge

numbersof competitors,were“sick”becauseof cut-throat competition,even though thefirmsintheseindustrieshadaccesstothemostadvancedtechnologiesintheworld.Amajorroleof1930sNewDealgovernmentinterventionwastoimplementregulationsandprogramsthathelpedtomaketheseindustrieshealthy.

• Today, with the prices of medicines largely unregulated in the United States despitegovernment-funded research, government-granted monopoly patents, and government-subsidizeddemand,pharmaceutical companieshavebecomeprimesources forpredatoryvalueextraction,underminingtheircapabilitiestoengageindruginnovation.

• The 1982 deregulation of the practice of stock repurchases by the U.S. Securities andExchange Commission through Rule 10b-18 has resulted in more than three decades oflooting of corporate treasuries by well-positioned stock-market traders, including seniorexecutives,resultingintheconcentrationofincomeatthetopandthedestructionofmiddle-classemploymentopportunities.

• Inadequate minimum wages that result from overcrowded labor markets have lefthardworkingfamiliesinpoverty,evenwhentheheadsofhouseholdsareholdingdowntwofull-timejobs.

• The “free-market” approach to college tuitions and student loans have made highereducationunaffordabletomostworking-classhouseholds,inanationthathadoncebeenintheforefrontoffreeorlow-costpublichighereducation.

• Weneedonlylookbacktothefinancialcrisisof2008-2009forthevastdevastationvisitedonhouseholdfamiliesbygovernmentfailuretoregulatehousingmarkets.

• Devastatingdestructionoccursthrough“natural”disasterscausedbythefailuretoregulateindustrieswhoseprocessesandproductcontributetoclimatechange.

TheTIEapproachtounderstandingtheoperationandperformanceoftheeconomy,includingthe interactions of households, governments, and businesses as investors in productivecapabilities,standsinstarkcontrasttotheneoclassicalfocusonmarketcoordinationofeconomicactivity.Theneoclassicaltheoryofthemarketeconomyposesaprofoundintellectualbarriertoanalyzing and understanding the organizational foundations of economic development.Neoclassical economists assume that an advanced economy is a market economy in whichmillions of household decisions concerning the allocation of the economy’s resources are7See,forexample,WilliamLazonick,CompetitiveAdvantageontheShopFloor,HarvardUniversityPress,1990;WilliamLazonick,“TheFunctionsoftheStockMarketandtheFallaciesofShareholderValue,”InstituteforNewEconomicThinkingWorkingPaperNo.58,July20,2017,athttps://www.ineteconomics.org/research/research-papers/the-functions-of-the-stock-market-and-the-fallacies-of-shareholder-value.

Lazonick:InnovativeEnterpriseandSustainableProsperity

7

aggregatedintopricesforinputstoandoutputsfromproductionprocesses.Anyimpedimentstothis process of market aggregation are deemed to be “market imperfections,” and anyundesirablesocialoutcomesfromtheprocessaredeemedtobe“marketfailures.”Developedmarketsareofutmostimportancetooureconomyandsociety;theycanallowusasindividualstochoosetheworkwedo,forwhomwework,wherewelive,andwhatweconsume.Insofar aswehavemarket choices, however, it is because the economy iswealthy, and it iswealthybecauseofthehousehold,government,andbusinessorganizationsthatconstitutetheinvestmenttriad.Ifmarketprocessescannotexplaininvestmentinproductivecapabilities,thenthetheoryofthemarketeconomycannotexplainthewealthofnations.Ifeconomistswanttodevise public policies to shape the processes and influence the outcomes of investment inproductivecapabilities,weneedtoconstructaneconomictheoryof“organizationalsuccess.”Atitscenterisatheoryofinnovativeenterprise.Yetitisthetheoryofthemarketeconomythatdominatestheteachingofeconomicsandthe“well-trained”economist’smindsetonhowtheeconomyoperatesandperforms.Thetheoryofperfectcompetition,whichistheneoclassicaleconomist’sidealofeconomicefficiency,viewsthefirm as impotent and themarket omnipotent in allocating the economy’s resources. By theneoclassical theory’s keyassumptions, the firm inperfect competition is, as Iwill explain,anunproductive firm. Yet neoclassical theory posits the firm in perfect competition as themicrofoundation of an economy in which the allocation of resources results in the ideal ofeconomicefficiency,evenifthatidealisdifficultorimpossibletoattain.If,thusput,neoclassicallogicconcerningtherelationbetweenfirmproductivityandeconomicperformancesoundsabsurd, that isbecause it is.Seventy-fiveyearsago, JosephSchumpeter,with his focus on innovation as the fundamental phenomenon of economic development,confrontedthemythofthemarketeconomywhenhearguedthat“perfectcompetitionisnotonlyimpossiblebutinferior,andhasnotitletobeingsetupasamodelofidealefficiency.”Thereason: Large-scale enterprise is “the most powerful engine of [economic] progress and inparticularofthelong-runexpansionoftotaloutput.”8Theneoclassical theoryof the firm inperfectcompetitioncannotexplainwhy forwelloveracentury very large firms have dominated the U.S. economy.9 In 2012 (the most up-to-datestatistics that include revenues), 964 companies that had 10,000 ormore employees in theUnited States, with an average workforce of 33,542, were only 0.017 percent of all U.S.businesses. But these 964 companies had 9 percent of all establishments, 28 percent ofemployees,31percentofpayrolls,and36percentofreceipts.For1,909companieswith5,000ormoreemployees,theseshareswere11percentofestablishments,34percentofemployees,38percentofpayrolls, and44percentof receipts.10How these largecompaniesallocate the8JosephA.Schumpeter,Capitalism,Socialism,andDemocracy,Harper,1950,thirdedition,p.106;originallypublishedin1942.

9WilliamLazonick,“AlfredChandler’sManagerialRevolution:DevelopingandUtilizingProductiveResources,”inMorgenWitzel,andMalcolmWarner,eds.,OxfordHandbookofManagementTheorists,OxfordUniversityPress,2012:361-384.

10UnitedStatesCensusBureau,“StatisticsofU.S.Businesses,”Dataon“U.S.,NAICSsectors,largeremploymentsizes”athttps://www.census.gov/data/tables/time-series/econ/susb/susb-.Unlikethedatafor2012,thelatestdataonfirmsizefor2014donotincludereceipts(collectedonlyeveryfiveyears).

Lazonick:InnovativeEnterpriseandSustainableProsperity

8

resourcesundertheircontrolhasprofoundimplicationsforemploymentopportunities,incomedistribution,andproductivitygrowthintheUnitedStates.Theneoclassical answermust be that these large firms representmarket imperfections, alsoknownasmonopoliesoroligopolies.Butthatdoesnotexplaintheproductivepoweroftheselarge firms.Nordoes itexplain, intuitivelyat least,why,as theneoclassical theoryposits, aneconomydominatedbyvery largenumbersofsmallunproductivefirmswouldyieldthemostefficienteconomy.Thisintellectualpuzzleissolvedwhenwerealizethattheneoclassicaltheoryisutterlyillogical.Thetheoryoftheunproductivefirmasthefoundationofthemostefficienteconomydominatesthethinkingofeconomistsbecauseitservestomakethemarketomnipotentand the firm impotent in theallocationof theeconomy’s resources. In effect, this ideologicaltenet,which is held dear by both liberal and conservative economists, obviates the need toconsider the role of the investment triad, including the innovative enterprise, in achievingsuperioreconomicperformance—thatis,stableandequitablegrowth.Let’sgobacktobasicstoseewhy“perfectcompetition”isillogical.Asconventionallydefined,perfectcompetitionexistswhenaverylargenumberofidenticalfirmsinanindustryeachhassuch a small share of total industry output that each firm, acting on its own, can choose toproduceitsprofit-maximizingoutputwithoutinfluencingthepriceoftheindustry’sproduct.Eachoftheseidenticalfirmsisconstrainedtobeverysmallbytheassumptionthatataverylowlevelof the firm’s output relative to industry output increasing average variable costs (AVC)overwhelmdecreasingaveragefixedcosts(AFC),sothatthefirmfacesaU-shapedcostcurveindecidinghowmuchoutputtoproduce.Itfollowsmathematicallythatthefirmmaximizesprofitsattheoutputatwhichmarginalrevenueequalsmarginalcost.Thus,wehavethetheoryoftheoptimizing firm that holds center stage (and generally the only stage) in virtually everyintroductoryeconomicstextbookusedworldwide.11Themodelforthemodern“principles”textbookwascreatedbyPaulSamuelson,Economics:AnIntroductory Analysis, first published in 1948 and reissued in 18 subsequent editions (withSamuelsonasthesoleauthorthroughthe12thedition,publishedin1985).ThelargecorporationwasnotunknowntoSamuelson.Inthefirstedition,heobservedthat“alistofthe200largestnonfinancialcorporationsreadslikeanhonorrollofAmericanbusiness,almosteverynamebeinga familiar household word...In manufacturing alone, the 100 most important companiesemployedmorethanone-fifthofallmanufacturinglaborandaccountedforone-thirdofthetotalvalue of all manufactured products.”12 After commenting that “their power did not growovernight,”Samuelsonstates:“Largesizebreedssuccess,andsuccessbreedsfurthersuccess.”Howdid these large corporations attain these dominant positions, andwhy did the top 100manufacturersachievehigh laborproductivity relative toallmanufacturers?Theexistenceofverylarge,highlyproductivefirmsshouldhaveledeconomiststosearchforatheoryofinnovativeenterpriseasafoundationofeconomicanalysis.13YetSamuelson’sscientificpapers(whichare11Iwouldbepleasedtobeinformedofanymicroeconomicstextbookthatcontradictsthisstatementonthetheoryofthefirm.12PaulA.Samuelson,Economics;AnIntroductoryAnalysis,firstedition,McGrawHill,1948,p.125.13Inthe1940s,economistscouldhavebuiltonSchumpeter’sfocusoninnovationasthefundamentalphenomenonofeconomicdevelopment,apropositionthatheputforwardinJosephA.Schumpeter,TheTheoryofEconomicDevelopment,

Lazonick:InnovativeEnterpriseandSustainableProsperity

9

virtuallyallmathematical,devoidofempiricalcontent)andhisfamous“principlesofeconomics”textbookinitssuccessiveeditionspromulgatedthetheoryoftheunproductivefirminperfectcompetitionastheidealofeconomicefficiency.Perfect competition idealizes the very small firm, its growth constrained by rising AVC as itexpandsoutput.Itisassumedthatataverylowlevelofoutput(forthefirmtoremainverysmall),theincreaseinAVCoutweighsthedeclineinAFCsothataveragetotalcostsrise,givingthefirm’scostcurveitsUshape.ButwhydoAVCrisetosuchanextentthattheyoutweighdecliningAFC?Currenttextbooksdonotsupplyanexplanation.Forexample,N.GregoryMankiw,PrinciplesofMicroeconomicssimplystatesthatthecostcurveisU-shaped—representing“costcurvesforatypicalfirm”14—andillustratesthis“principle”withmade-upnumbersforahypotheticalcoffeeshopinwhichAVCincreasefrom$0.30foronecupofcoffeeto$12.00for10cups,withrisingAVCsurpassingdecliningAFCafter6cups.15Similarly,PaulKrugmanandRobinWells,EssentialsofEconomicsarguesthata“realisticmarginalcostcurvehasa’swoosh’shape,”16andgivestheexampleofasalsamakerwhoseAVCrisefrom$12.00foronecaseofsalsato$120.00fortencases, with rising AVC surpassing declining AFC after three cases.17 In both theMankiw andKrugman/Wells textbooks, the “explanation” for the U-shaped cost curve—and hence theunproductive firm that is the ideal of economic efficiency—is simply themade-up numericalexample!We can, however, find an explanation for the U-shaped cost curve in the early editions ofSamuelson’stextbook.18InthefirstthroughfiftheditionsofEconomics,SamuelsonexplainedtheU-shapedcostcurvebyassumingthat(asistypicallythecase)laboristhefirm’smainvariable-costinputandthatastheemploymentoflaborincreasesasthefirmexpandsoutput,theaverageproductivity of labor falls because of, in Samuelson’s words, “limitations of plant space andmanagement difficulties.” As the professor put it (with my emphasis) in the fifth edition ofEconomics,publishedin1961(withwordingonlyslightlydifferentfromthatinthefirstedition):“Aftertheoverheadhasbeenspreadthinovermanyunits,fixedcostscannolongerhavemuchinfluenceonaveragecosts.Variablecostsbecomeimportant,andasaveragevariablecostsbegintorisebecauseoflimitationsofplantspaceandmanagementdifficulties,averagecostsfinallybegintoturnup.”19Thereitis:Theexplanationofthemostimportant“principle”oftheneoclassicaltheoryofthefirm—andIwouldargue,ofneoclassicaleconomicsmoregenerally—buriedawayonpage524of

HarvardUniversityPress,1934(firstpublishedinGermanin1911).SeeWilliamLazonick,“WhatHappenedtotheTheoryofEconomicDevelopment?”inPatriceHiggonet,DavidS.Landes,andHenryRosovsky,eds.,FavoritesofFortune:Technology,Growth,andEconomicDevelopmentsincetheIndustrialRevolution,HarvardUniversityPress,1991:267-296.Bythe1960s,Samuelsoncouldhavefoundpowerfulexplanations,boththeoreticalandhistorical,forthegrowthofthefirminEdithT.Penrose,TheTheoryoftheGrowthoftheFirm,Blackwell,1959;andAlfredD.Chandler,Jr.,StrategyandStructure:ChaptersintheHistoryoftheAmericanIndustrialEnterprise,MITPress,1962.Initsvariouseditionsoverthedecades,Samuelson,Economics,hasneverreferencedthesescholarsorthebodyofresearchthattheirideashavespawned.

14N.GregoryMankiw,PrinciplesofMicroeconomics,CengageLearning,eighthedition,nodate,p.259.15Ibid.,p.254.16PaulKrugmanandRobinWells,EssentialsofEconomics,WorthPublishers,fourthedition,2017,p.189.17Ibid.,p.185.18IamgratefultoWynnTuckerforsearchingthroughthefirsteditionofSamuelson,Economics,tolocatetheexplanation.19PaulA.Samuelson,Economics:AnIntroductoryAnalysis,fifthedition,McGraw-Hill,1961,p.524.

Lazonick:InnovativeEnterpriseandSustainableProsperity

10

as an 853-page textbook.The theory of the firm in perfect competition in turn provided thefoundation for Samuelson’s “grand neoclassical synthesis” of microeconomics andmacroeconomics, which continues to dominate economics teaching and thinking. ButSamuelson’s twocryptic sentencesprovide farmoreofanexplanation for theU-shapedcostcurve than Mankiw and Krugman/Wells (as but two examples from the crowded field ofSamuelson-cloneintroductoryeconomicstextbooks)havetooffer.Sowhatdothosesentencesmean?WhenIusedthefiftheditionofSamuelson,Economicsinmyveryfirsteconomicscoursein1964,IwastoldthatwhatProfessorSamuelsonwasarguingwasthatasmoreworkersareaddedtotheworkplaceasvariableinputsasthefirmexpandsoutputtheir averageproductivity falls becauseof overcrowding that causes them tobump intooneanother(“limitationsofplantspace”)andbecausetheincreaseinthenumberofworkerstobesupervised makes it more difficult for the employer to prevent workers from shirking(“management difficulties”). The resultant decline in labor productivity as output increasescausesAVCtorise.Inotherwords,Samuelson’sexplanationfortheU-shapedcostcurvewasthatariseinAVCoccursbecauseworkerscan’tworkandwon’twork.Moreover,thecostcurvegetsitsUshapewhentheriseinAVCissolargethatitoverwhelmsthefall inAFC.Theriseintotalunitcosts,reflectingdecliningproductivityasthefirmexpandsitsoutput,thenconstrainsthegrowthofthefirm,andratherthanconfront“limitationsofplantspace”and“managementdifficulties,”theneoclassicalemployerjustoptimizessubjecttothese“given”constraints.Insharpcontrast,theinnovativeenterprisewouldconfront“limitationsofplant space” by investing in more spacious plant and “management difficulties” by creatingincentivesforworkerstosupplyhigherlevelsofproductivity.Theseinvestmentsandincentiveswouldaddtothefirm’scosts,butiftheinnovatingfirmcanincreaseitsproductivitysufficientlybymaking theseexpenditures, it couldpossiblyoutcompete theoptimizing firm,as shown inFigure1.Somuchfortheneoclassicalidealofeconomicefficiency!Just a minute (I can hear the well-trained neoclassical economist saying). What about theneoclassicaltheoryofmonopolythatonecanalsofindinvirtuallyeveryintroductoryeconomicstextbook, with its demonstration that, compared with perfect competition, the monopolist,maximizingprofitssubjecttoadownward-slopingdemandcurve,restrictsoutputandraisestheproduct’sprice?Isn’tthatproofofperfectcompetitionastheidealofeconomicefficiency?No,itisnot.Thereisalogicalflawintheneoclassicalmonopolymodelthatyieldsthe“results”—restrictedoutput,higherprice—thatneoclassical ideologyrequires.AsshowninFigure2, it isassumedthatthemonopolistmaximizesprofitssubjecttothesamecoststructureastheperfectcompetitors.Butthenhowdidthemonopolistbecomeamonopolist?IntheTheoryofInnovativeEnterprise,thefirmgrowslarge,andoutcompetesperfectcompetitors,bytransformingthecoststructure—by,forexample,investinginmorespaciousplanttopreventovercrowding,creatingpositiveincentivesforemployeestoexpendmoreworkeffort,orlaunchinganR&Dinitiativethatmay yield a higher quality product. Compared with perfect competitors, who follow theneoclassical directive to optimize subject to given constraints, the innovating firm increasesoutputand,bydrivingdownAFCasitexpandsoutput,canlowerpricestoconsumerswhilestill

Lazonick:InnovativeEnterpriseandSustainableProsperity

11

increasingitsprofits.Fortheprosperityoftheeconomy,that’sabigplus.Forneoclassicaltheory,however,that’sabigminus.

Figure1:Theinnovatingfirmtransformsthecoststructurethat

theoptimizingfirmtakesasa“given”constraint

Figure2:Thelogicalflawintheneoclassicalmonopolymodelthat

seekstoprovethat“perfectcompetition”istheidealofeconomicefficiency

Comparing optimizing and innovating firms

q c

pc

pminc

qmax c

innovating firm

optimizing firm

averagecostmarginal cost

marginaland averagerevenue

Technological and market conditions are given by cost and revenue functions. The “good manager” optimizes subject to technological and market constraints. Through strategy, organization, & finance, innovating firm transforms technologies and markets to generate higher quality, lower cost products. There is no “optimal” output or “optimal” price.

p = price; q = output; c = perfect competitorpmin = minimum breakeven price; qmax = maximum breakeven output

output output

price,cost

How does the innovating firm transform high fixed costs into low unit costs?

Monopoly and competition: ILLOGICALCOMPARISON

pmininnovating firm

optimizing firmmarginal

cost

marginalrevenue

averagerevenue

Innovating and optimizing firms LOGICAL COMPARISON

pc

pm

qcqmqmin

pm= monopoly price; qm = monopoly outputPc = competitive price; qc = competitive output

The innovating firm transforms technological and market conditions that the optimizing firm accepts as “given” technological and market constraints.

pmin= lowest breakeven price, optimizing firmqmin= lowest breakeven output, optimizing firm

Lazonick:InnovativeEnterpriseandSustainableProsperity

12

Note also that, in his explanation of the U-shaped cost curve, Samuelson writes (with myemphasis)thatbecauseoflimitationsofplantspaceandmanagementdifficulties,“averagecostsfinallyturnup.”Samuelsoninserted(probablyinstinctively)theword“finally”becauseifaveragecostsdonotturnup,thefirmwillgrowlargeranddestroythepossibilityof“perfectcompetition”asanidealand“constrainedoptimization”asthedecisionruleforthe“profit-maximizing”firm.Samuelson’stheoryrequiresthatthefirmthatisthe“idealofeconomicefficiency”remainsmallandunproductive.Iftheeconomyisdominatedbyfirmsinwhich,touseSamuelson’sownwords,“largesizebreedssuccess,andsuccessbreedsfurthersuccess,”thenperfectcompetitionasthe“ideal of economic efficiency” disappears and “constrained optimization” may not be themanagementpracticethatachievessuperioreconomicperformance.YetevenPaulSamuelsonwasawarethat thereal-worldeconomycanbedominatedby largefirmsthatarehighlyproductive.InChapter2(“CentralProblemsofEveryEconomicSociety”)ofthefiftheditionofEconomics,Samuelsonfirstdiscusses“IncreasingCosts”and“TheFamousLawofDiminishingReturns”(bothsubheadings)andprovidesatablewithanumericalexamplethatbearstheheading“Diminishingreturnsisafundamentallawofeconomicsandtechnology”andthecaption“Returnsofcornwhenunitsof laborareaddedtofixed land.”Onthenextpage,however,hehasthesubheading“EconomiesofScaleandMassProduction:ADigression,”withtheexplanation:“Economiesofscaleareveryimportantinexplainingwhysomanyofthegoodswebuyareproducedbylargecompanies...Theyraisequestionstowhichweshallreturnagainandagaininlaterchapters.”Samuelsonmadehis“honorroleofAmericanbusiness”remark,citedabove,100pageslater.Butitwouldbeanexaggerationtosaythattheprofessorkepthispromiseto“return[tothiscentralproblem of every economic society] again and again.” After all, for Samuelson the actualimportanceofeconomiesofscaletotheproductiveeconomywasjust“adigression”fromhisobsessionwith“thefamouslawofdiminishingreturns”asa“fundamentallawofeconomicsandtechnology.”It may be, however, that, in the course of revising Economics in the early 1960s, ProfessorSamuelsongavethisglaringcontradictionbetweenneoclassical ideologyandeconomicrealitysomedeeperthoughtandcametorealizetheabsurdityofarguingthattheunproductivefirmisthe ideal of economic efficiency. If so, he resolved the problem, not by renouncing theneoclassical theory of the firm and calling for the construction of a theory of innovativeenterprise—drawingupon,forexample,EdithPenrose’sseminalcontribution,publishedin1959,andAlfredChandler’spioneeringhistoricalresearchdocumentedinhis1962bookStrategyandStructure20—butratherbysimplyexcisingfromthesixthandsubsequenteditionsofEconomicsthesentencesquotedaboveaboutoverheadbeingspreadthin, limitationsofplantspace,andmanagement difficulties. Henceforth, Samuelson would just refer to the “famous law ofdiminishingreturns”tojustifythenonsensethattheunproductivefirmistheidealofeconomicefficiency.And,overthesubsequentgenerations,economistssuchasN.GregoryMankiwandPaul Krugman, among other PhD economists, have published textbooks that reproduce this

20Penrose,TheTheoryoftheGrowthoftheFirm;Chandler,StrategyandStructure.

Lazonick:InnovativeEnterpriseandSustainableProsperity

13

nonsense as a principle of economics, taught routinely to students and requiring neitherintrospectionnorexplanation.Theproblemwithperfectcompetitionastheidealofeconomicefficiencyisnotjustthatmillionsuponmillionsofeconomicsstudentshavebeenandcontinuetobemiseducatedabouttheroleofthebusinessenterprise intheeconomy.Thebiggerproblemisthatthe“well-trained”PhDeconomistswhoare supposed tobe theeducators (included those towhomso-calledNobelprizesineconomicshavebeenmetedout)spouttheinanitythattheunproductivefirmistheidealofeconomicefficiency,andinsodoingportraythe“ideal”firmasapowerlessentitythatdoesnot,andshouldnot,interferewiththemarketcoordinationoftheallocationofresources.In my own teaching, I call this view of the world “sweatshop economics” because theovercrowdedandunmotivatedfirmthatSamuelsondescribesasthemicrofoundationof idealefficiencyhas the characteristics of a sweatshop. Imake thepoint that if such firms actuallydominated the economy, we would, in a nation such as the United States, all be living inpoverty.21Meanwhile,the“well-trained”economistviewsthehighlyproductivefirmsthatgrowlarge,andperhapsevendominatetheindustriesinwhichtheyoperateasmassive“marketimperfections”thatimpedethepurportedefficiencyofmarketresourceallocation.Intherealeconomicworld,however,theinnovativeenterpriseisapowerfulentitythat,bytransformingthetechnological,market, and competitive conditions that it faces, succeeds in generating the higher-quality,lower-costgoodsandservicesthatraiseproductivity.Farfrombeingamarketimperfection,byconfrontingandtransformingthe“neoclassicalconstraints,”theinnovativeenterpriseprovidestheproductivefoundationsforachievingsustainableprosperity.AsIargueinthenextsectionofthisessay,throughtheveryprocessofdevelopingandutilizingproductive capabilities, the innovative enterprise tends to providemore stable employment,moreequitableincomes,andhigherproductivitythanthe“uninnovative”enterpriseswithwhichneoclassicaleconomistsareenamored.Forthesocietyasawhole,theinnovativeenterpriseisthe linchpinofthe investmenttriad,making itpossibleforhouseholdfamilies,throughstableandequitableemployment,tobesupportive,andforgovernmentagencies,throughaccesstotax revenues fromhouseholds andbusinesses andby servicing theneedsof households andbusinesses,tobedevelopmental.Forthesakeofsustainableprosperity,theacademicdisciplineknownaseconomicsneedstoriditselfofthemythofthemarketeconomy—fromtheSamuelson-cloneintroductorytextbookstotheubiquitousmathematicalmodelsthattypicallybearnorelationtoreality(andwhichoftenreflectutterignoranceofhowanactualeconomyfunctionsandperforms).ItishightimetotakeuptheSchumpeterianchallenge,andbuildausefulanalysisofeconomyandsocietyaroundatheory of innovative enterprise. We will then understand how and why the ideology thatcompaniesshouldberunto“maximizeshareholdervalue”subvertsinnovativeenterpriseand,withthatsubversion,ourquestforstableandequitableeconomicgrowth.

21Lazonick,“InnovativeEnterpriseorSweatshopEconomics?”.

Lazonick:InnovativeEnterpriseandSustainableProsperity

14

3. Fromretain-and-reinvesttodownsize-and-distributeTheTheoryofInnovativeEnterprise(TIE)thatIhaveconstructedthroughdecadesofresearchand teaching provides an analytical perspective on the microfoundations of sustainableprosperity.Thereisnowayinwhichaneconomycanattainstableandequitablegrowthunlessits major business enterprises focus on investing in productive capabilities for the sake ofgeneratinginnovativeproducts.Beginningwithacharacterizationoftheinnovationprocessasuncertain, collective, and cumulative, TIE articulates three “social conditions of innovativeenterprise”—strategiccontrol,organizationalintegration,andfinancialcommitment—thatcansupport the innovation process. Armed with TIE, we can then consider the impacts of theinnovationprocessonemploymentstability,incomeequity,andbusinessproductivity.Wecanaskwhetherthedominantcharacteristicsofthenation’smajorbusinessenterprisessupportorunderminetheattainmentofstableandequitablegrowthintheeconomyasawhole.

.TIE is an analytical framework for understanding how a business enterprise can generate aproductthatishigherqualityand/orlowercostthanproductspreviouslyavailable,andthusbea source of productivity growth. The innovation process that can generate a higher-quality,lower-costproductisuncertain,collective,andcumulative.22• Uncertain:Wheninvestmentsintransformingtechnologiesandaccessingmarketsaremade,

theproductandfinancialoutcomescannotbeknown;iftheywereitwouldnotbeinnovation.Hencetheneedforstrategy.

• Collective:Togeneratehigher-quality,lower-costproducts,theenterprisemustintegratetheskillsandeffortsoflargenumbersofpeoplewithdifferenthierarchicalresponsibilitiesandfunctionalcapabilitiesintothelearningprocessesthataretheessenceofinnovation.Hencetheneedfororganization.

• Cumulative: Collective learning today enables collective learning tomorrow, and theseorganizational learningprocessesmustbesustainedcontinuouslyovertimeuntil, throughthe sale of innovative products, financial returns can be generated. Hence the need forfinance.

TIEidentifiesthreesocialconditions—strategiccontrol,organizationalintegration,andfinancialcommitment—that can enable the firm tomanage the uncertain, collective, and cumulativecharacteroftheinnovationprocess.• Strategic control: For innovation to occur in the face of technological, market, and

competitiveuncertainties,executiveswhocontrolcorporateresourceallocationmusthavetheabilitiesandincentivestomakestrategicinvestmentsininnovation.Theirabilitiesdependon their knowledge of how strategic investments in new capabilities can enhance theenterprise’s existing capabilities. Their incentives depend on alignment of their personalinterestswiththecompany’spurposeofgeneratinginnovativeproducts.

22WilliamLazonick,“TheTheoryofInnovativeEnterprise:FoundationofEconomicAnalysis,”AIRWorkingPaper,August2015,

atwww.theAIRnet.org.

Lazonick:InnovativeEnterpriseandSustainableProsperity

15

• Organizational integration: The implementation of an innovation strategy requiresintegrationofpeopleworkinginacomplexdivisionoflaborintothecollectiveandcumulativelearning processes that are the essence of innovation. Work satisfaction, promotion,remuneration,andbenefitsareimportantinstrumentsinarewardsystemthatmotivatesandempowersemployeestoengageincollectivelearningoverasustainedperiodoftime.

• Financial commitment: For collective learning to cumulate over time, the sustainedcommitmentof“patientcapital”mustkeepthe learningorganization intact.Forastartupcompany,venturecapitalcanprovidefinancialcommitment.Foragoingconcern,retainedearnings(leveraged,ifneedbe,bydebtissues)arethefoundationoffinancialcommitment.

Theuncertaintyofaninnovativestrategyisembodiedinthefixed-costinvestmentsrequiredtodevelop the productive capabilities thatmay, if the strategy is successful, result in a higher-quality product. But an innovative strategy that can eventually enable the firm to developsuperiorproductivecapabilitiesmayplacetheinnovatingfirmatacompetitivedisadvantage(asindicatedforlowlevelsofoutputinFigure1above)becausesuchstrategiestendtoentailhigherfixed costs than the fixed costs incurred by rivals that choose to optimize subject to givenconstraints. As an essential part of the innovation process, the innovating firmmust accesssufficientmarketsforitsproductstotransformhighfixedcostsintolowunitcosts(seeFigure1),and, thereby, convert competitive disadvantage at low levels of output into competitiveadvantageathighlevelsofoutput.Thesehigherfixedcostsderivefromboththesizeandthedurationoftheinnovativeinvestmentstrategy.Theinnovatingfirmwillhavehigherfixedcoststhanthoseincurredbytheoptimizingfirmif,asistypicallythecase,theinnovationprocessrequiresthesimultaneousdevelopmentofproductive capabilities across abroader anddeeper rangeof integratedactivities than thoseundertakenbytheoptimizingfirm.Butinadditionto,andgenerallyindependentof,thesizeoftheinnovativeinvestmentstrategyatapointintime,highfixedcostswillbeincurredbecauseofthedurationoftimethat isrequiredtotransformtechnologiesandaccessmarketsuntil theyresultinproductsthataresufficientlyhighqualityand/orlowcosttogeneratereturns.Ifthesizeofinvestmentsinphysicalcapitaltendstoincreasethefixedcostsofaninnovativestrategy,sotoodoesthedurationoftheinvestmentrequiredforanorganizationofpeopletoengageinthecollective and cumulative—or organizational—learning that, to transform technologies andaccessmarkets,isthecentralcharacteristicoftheinnovationprocess.Thehighfixedcostsofaninnovativestrategycreatetheneedforthefirmtoattainahighlevelof utilization of the productive resources that it has developed—what are generally called“economiesofscale.”Giventheproductivecapabilitiesthatithasdeveloped,theinnovatingfirmmay experience increasing costs because of the problem of maintaining the productivity ofvariable inputs as it employs larger quantities of these inputs in theproductionprocess. Butratherthan,asinthecaseoftheoptimizingfirm,takeincreasingcostsasagivenconstraint,theinnovatingfirmattemptstotransformitsaccesstohigh-qualityproductivecapabilitiesathighlevels of output. To do so, it invests in the development of that productive capability, theutilizationofwhichasavariableinputhasbecomethesourceofincreasingcosts.Toovercomethe constraint on its innovative strategy posed by reliance on the market to supply it with

Lazonick:InnovativeEnterpriseandSustainableProsperity

16

inputs—whichiswhatavariablefactorofproductionentails—theinnovatingfirmintegratesthesupplyofthatfactorintoitsinternaloperations.Thedevelopmentoftheproductivecapabilityofthisnow-integratedfactorofproductionaddstothefixedcostsoftheinnovativestrategy.Previouslythisproductiveresourcewasutilizedasavariablefactorthatcouldbepurchasedincrementallyatthegoingfactorpriceonthemarketasextraunitsoftheinputwereneededtoexpandoutput.Havingaddedtoitsfixedcostsinorderto overcome the constraint on enterprise expansion posed by increasing variable costs, theinnovatingfirmisthenunderevenmorepressuretoexpanditssoldoutputinordertotransformhighfixedcostsintolowunitcosts.In effect, to restate Adam Smith’s first principle of economics enunciated in TheWealth ofNations,23economiesofscalearelimitedbytheextentofthemarket.Thefirm’shigher-qualityproductenablesittoaccessalargerextentofthemarketthanitscompetitors,althoughlearningaboutwhat potential buyerswant and convincingpotential buyers that the firm’s product isactually“higherquality”addtothefixedcostsoftheinnovationstrategy.Hencethefixedcostsoftheinnovativestrategydependoninvestmentsinnotonlytransformingtechnologybutalsoaccessingmarkets,withanincreaseinfixedcostsrequiringanevenlargerextentofthemarkettoconverthighfixedcostsintolowunitcosts.Apotentwayforaninnovatingfirmtoattainalargerextentof themarket is to share someof thegainsof this cost transformationwith itscustomersintheformoflowerprices.As, through the development and utilization of productive capabilities, the innovating firmsucceedsintheconversionofhighfixedcostsintolowunitcosts,itineffect“unbends”theU-shapedcostcurveratherthan,asinthetheoryoftheoptimizingfirm,takeinternaldiseconomiesofscaleasagivenconstraint(seeFigure1above).Byreshapingthecostcurveinthisway,theinnovatingfirmcreatesthepossibilityofsecuringcompetitiveadvantageover its“optimizing”rivalswhich,asinstructedbytheeconomicstextbooks,takeincreasingcostsasagivenconstraint.Tosumup:InmyelaborationofTIE,Iusethedistinctionbetweenfixedcostsandvariablecoststoarguethataninnovatingfirmthatexperiencesrisingvariablecostsasitseekstoexpandoutputwillrecognizetheneedtoexercisecontroloverthequalityofthevariableinput,theuseofwhichisdecreasingproductivity.Todosotheinnovatingfirmwillintegratetheproductionofthatinputintoitsinternaloperations,thusseekingtotransformvariablecostsintofixedcostsaspartofitsinnovative strategy. This strategic move will place the innovating firm at a competitivedisadvantageat lowlevelsofoutput(as inFigure1), increasingtheimperativethat itattainalarge market share to drive down unit costs. Moreover, there are often high fixed costs ofaccessingthatmarketshare(branding,advertising,distributionchannels,asalariedsalesforce,etc.),andindeedinsomeindustriesthefixedcostsofaccessingalargemarketsharearegreaterthanthefixedcostsofinvestinginthetransformationofproductiontechnologies.

23AdamSmith,AnInquiryintotheNatureandCausesoftheWealthofNations,fifthedition(editedbyEdwinCannan),Methuen,1904,ch.1(“OntheDivisionofLabour”);originallypublishedin1776.

Lazonick:InnovativeEnterpriseandSustainableProsperity

17

Alongwith investments inplant andequipment, investment inproductive capabilitiesentailstrainingandretainingemployees.Itmayalsopossiblyentailsustaininglearningrelationshipswithfirmsthatactassuppliersofinputsanddistributorsofoutputsiftheseservicesareperformedbylegallyindependententerprises.Thetheoryoftheoptimizingfirmviewslaborasavariablecost;acommoditythatisaddedtoandsubtractedfromtheproductionprocessasrequiredbythe expansion or contraction of output. In fact, however, when a company enhances theproductive capability of an employee, either through formal or on-the-job training, thatemployee’scapabilitytakestheformofafixed-costassetthatbothcanenhancethequalityoftheproductthattheinnovatingfirmhastosellandincreasetheneedtoattainalargeextentofthemarkettotransformhighfixedcostsintolowunitcosts.Whenthefirmsucceedsinboth,itgeneratesahigher-quality,lower-costproductthanwaspreviouslyavailable.Innovationandthegrowthofthefirmgohandinhand.Investmentinproductivecapabilities,includingthoseofitslaborforce,driveinnovationandthegrowthofthefirm.Toretainandmotivatetheemployeesthatthefirmhashiredandtrained,the innovating firmgenerallyoffers theseemployeeshigherpay,moreemployment security,superiorbenefits,andmoreinterestingwork,allofwhichaddtothefixedcostoftheassetthatanemployee’slaborrepresents.Theinnovatingfirmmakesitsemployeesbetteroff,butitcanafford, and indeed profit from, the increased labor expense when that labor’s productivecapabilityenablesthefirmtogainacompetitiveadvantagebygeneratinghigh-quality,low-costproducts.Theinnovatingfirmsharesthegainsofinnovationwithitsemployeesbymakinginvestmentsinwhat I have called their “collective and cumulative careers.”24 Under such circumstances,increases in labor incomesand increases in laborproductivity tend to showahighlypositivecorrelation—aninterconnectionthat,Iargue,wasprevalentinU.S.businessenterprisesinthedecadesafterWorldWarIIwhen,forwhitemalesatleast,the“careerwithonecompany”wastheemploymentnorm.25Whensuccessful,the innovatingfirmmaycometodominate its industry,but itsoutput is farlargeranditsunitcosts,andhencepotentiallyitsproductprice,farlowerthantheywouldbeifalargenumberofsmallfirmshadcontinuedtopopulatetheindustry.Indeed,onemightevenfindthistransitionfromcompetitiontodominancemanifestedbythetransformationofalargenumber of overcrowded sweatshops with alienated labor into a small number of spaciousfactories with highlymotivated labor! The overall gains from innovationwill depend on therelationbetweentheinnovatingfirm’scoststructureandtheindustry’sdemandstructure,while

24WilliamLazonick,PhilipMoss,HalSalzman,andÖnerTulum“SkillDevelopmentandSustainableProsperity:CollectiveandCumulativeCareersversusSkill-BiasedTechnicalChange,”InstituteforNewEconomicThinkingWorkingGrouponthePoliticalEconomyofDistributionWorkingPaperNo.7,December2014,athttps://ineteconomics.org/ideas-papers/research-papers/skill-development-and-sustainable-prosperity-cumulative-and-collective-careers-versus-skill-biased-technical-change;MattHopkinsandWilliamLazonick,“WhoInvestsintheHigh-TechKnowledgeBase?”InstituteforNewEconomicThinkingWorkingGrouponthePoliticalEconomyofDistributionWorkingPaperNo.6,September2014(revisedDecember2014),athttp://ineteconomics.org/ideas-papers/research-papers/who-invests-in-the-high-tech-knowledge-base.

25WilliamLazonick,“LaborintheTwenty-FirstCentury:TheTop0.1%andtheDisappearingMiddleClass,”inChristianE.Weller,ed.,Inequality,Uncertainty,andOpportunity:TheVariedandGrowingRoleofFinanceinLaborRelations,CornellUniversityPress,2015:143-192.

Lazonick:InnovativeEnterpriseandSustainableProsperity

18

the distribution of those gains among the firm’s various “stakeholders”will depend on theirrelativepowertoappropriateportionsofthesegains.26Whatisimportantinthefirstinstanceisthat,asaresultofthetransformationoftechnologicaland market “constraints,” there are gains to innovative enterprise that can be shared. Inexpanding output and lowering costs, it is theoretically possible (although by no meansinevitable) for thegains to innovativeenterprise topermit, simultaneously,higherpay,morestableemployment,andbetterworkconditionsforemployees;astrongerbalancesheetforthefirm;moresecurepaperforcreditors;higherdividendsandstockpricesforshareholders;moretax revenues for governments; and higher-quality products at lower prices for consumers.

Innovativeenterpriseprovidesafoundationforachievingsustainableprosperity.TIE explains how, in the rise of the United States to global industrial leadership during thetwentiethcentury,a“retain-and-reinvest”allocationregimeenabledarelativelysmallnumberofbusinessenterprisesinawiderangeofindustriestogrowtoemploytens,orevenhundreds,of thousands of people and attain dominant product-market shares. Companies retainedcorporateprofits and reinvested them inproductive capabilities, including first and foremostcollective and cumulative learning. Companies integrated personnel into learning processesthroughcareeremployment.Intothe1980s,thenormofacareer-with-one-companyprevailedatmajorU.S.corporations.Asteadystreamofdividendincomeandtheprospectofhigherfuturestockpricesbasedoninnovativeproductsgaveshareholdersaninterestin“retain-and-reinvest.”Intheimmediatepost-WorldWarIIdecades,thebeneficiariesofaretain-and-reinvestcorporateresource-allocationregimeweremainlywhitemales.Forminoritiesandwomen,accesstomorestableemploymentandmoreequitableincomewasbolsteredbytheCivilRightsActof1964andtheEqualEmploymentOpportunityCommissionlaunchedthefollowingyear.Asabellwetherofprogressinupwardmobility,bythe1970shundredsofthousandsofblackswithnomorethanhigh-schooldiplomaswereattainingmiddle-classstatusthroughemploymentinunionizedsemi-skilledoperativejobsinmass-productionindustriessuchasautomobiles,steel,andelectronicsmanufacturing.27 White males, however, maintained privileged access to intergenerationalupwardmobility fromblue-collar jobs towhite-collar jobs as the sons of blue-collarworkersobtainedhighereducations followedby “careerwithone company”employment inbusinesscorporations. In the 1970s, females (disproportionately white) with college educations alsogainedsignificantlyincreasedaccesstocareeremploymentinbusinesscorporations,althoughtheir upward mobility was impeded by the persistence of the ideology that, when childrenarrived,theywouldgiveuporinterrupttheircareerstoassumethetraditionalmiddle-class“stay-at-home-mother”role.Then,however, fromthe late1970s,andcontinuingtothepresent, formassesofAmericans,includingwhitemales,thequantityandqualityofemploymentopportunitythatcouldsupportupwardmobilityeroded,whilethedistributionofincomegrewincreasinglyunequal.Thatdespite26Lazonick,CompetitiveAdvantageontheShopFloor;Lazonick,“TheTheoryofInnovativeEnterprise”27WilliamLazonick,PhilipMoss,andJoshuaWeitz,“TheEqualEmploymentOpportunityOmission,”InstituteforNewEconomicThinkingWorkingPaperNo.53,December5,2016,athttps://www.ineteconomics.org/research/research-papers/the-equal-employment-opportunity-omission.

Lazonick:InnovativeEnterpriseandSustainableProsperity

19

thefactthatoverthepastfortyyearsorso,realgrossdomesticproductpercapitahasdoubledin the United States.28 By the first half of the 1980s, some acute observers of blue-collaremployment perceived that the U.S. income distribution was taking a “great U-turn.”29 Inhistoricalretrospect,wenowknowthat,sincethatchangeindirectionintheearly1980s,theUnitedStateshascontinueddownthe road toextreme income inequalityand theerosionofmiddle-class employment opportunities. TIE provides a framework for analyzing this historicchangeindirectionofU.S.economicperformance—essentiallytheendofthenationalquestforsustainableprosperity—byfocusingonthetransformationofthedominantregimeofcorporateresourceallocationfromretain-and-reinvesttodownsize-and-distribute.Underretain-and-reinvest,thecorporationretainsearningsandreinveststhemintheproductivecapabilitiesembodiedinitslaborforce.Underdownsize-and-distribute,thecorporationlaysoffexperienced, and often more expensive, workers and distributes corporate cash toshareholders.30 Since the beginning of the 1980s, employment relations in U.S. industrialcorporationshaveundergonethreemajorstructuralchanges,summarizedas“rationalization,”“marketization,” and “globalization,” that have eliminated existing middle-class jobs in theUnited States. The failure of the U.S. economy to replace these jobs with newmiddle-classemployment opportunities cannot, however, be attributed to these changes in employmentrelations alone. Exacerbating the rate of job loss and limiting investment in new careeremploymentopportunitieshasbeenthefinancializationofthebusinesscorporation,manifestedbymassivedistributionsofcorporatecashtoshareholders.From theearly 1980s, rationalization, characterizedbyplant closings, terminated the jobsofhigh-school educated blue-collarworkers,most of themwell-paid unionmembers. From theearly 1990s,marketization, characterized by the end of a career with one company as anemploymentnorm,placedthejobsecurityofmiddle-agedwhite-collarworkers,manyofthemcollege educated, in jeopardy. From the early 2000s, globalization, characterized by theacceleratedmovementofemploymentoffshoretolower-wagenations,leftallmembersoftheU.S. labor forcevulnerable todisplacement,whatever theireducational credentialsandworkexperience.Initially, thesestructuralchanges inemploymentcouldbeexplainedasbusinessresponsestochangesintechnologies,markets,andcompetition.Duringtheonsetoftherationalizationphaseintheearly1980s,theplantclosingswereareactiontothesuperiorproductivecapabilitiesofJapanesecompetitorsinconsumer-durableandrelatedcapital-goodsindustriesthatemployedsignificantnumbersofunionizedblue-collarworkers.Duringtheonsetofthemarketizationphaseintheearly1990s,theerosionoftheone-company-careernormamongwhite-collarworkerswasaresponsetothedramatictechnologicalshiftfromproprietarysystemstoopensystems,integraltothemicroelectronicsrevolution;ashiftthatfavoredyoungerworkerswiththelatestcomputerskills,acquiredinhighereducationandtransferableacrosscompanies,overolderworkerswithmanyyearsofcompany-specificexperience.Duringtheonsetoftheglobalizationphaseinthe28https://fred.stlouisfed.org/series/A939RX0Q048SBEA29BennettHarrisonandBarryBluestone,CorporateRestructuringandthePolarizingofAmerica,BasicBooks,1986;BennettHarrison,ChrisTilly,andBarryBluestone,“WageInequalityTakesaGreatU-Turn,”Challenge,29,1,1986:26-32.

30LazonickandO’Sullivan,“MaximizingShareholderValue.”

Lazonick:InnovativeEnterpriseandSustainableProsperity

20

early2000s,thesharpaccelerationintheoffshoringofjobswasaresponsetotheemergenceoflargesuppliesofhighlycapable,andlowerwage,laborindevelopingnationssuchasChinaandIndiawhich,linkedtotheUnitedStatesthroughinexpensivecommunicationandtransportationsystems,couldtakeoverU.S.employmentactivitiesthathadbecomeroutine.OnceU.S.corporationstransformedtheiremploymentrelations,however,theyoftenpursuedrationalization,marketization,andglobalization tocutcurrentcosts rather than to repositiontheirorganizationstoproduceinnovativeproducts.Definingsuperiorcorporateperformanceasever-higherquarterlyearningspershare(EPS),companiesturnedtomassivestockrepurchasesto“manage”theirowncorporations’stockprices.TrillionsofdollarsthatcouldhavebeenspentoninvestmentinproductivecapabilitiesintheU.S.economyoverthepastthreedecadeshaveinsteadbeenusedtobuybackstockforthepurposeofmanipulatingstockprices.Figure3showsnetequityissues(newstockissueslessstocktakenoffthemarketthroughstockrepurchasesandM&Aactivity)ofU.S.nonfinancialcorporationsfrom1946through2016.Overthedecade2007-2016netequityissuesofnonfinancialcorporationsaveraged-$412billionperyear. In2016netequity issueswere-$586billion.Overthepastthreedecades, inaggregate,dividendshavetendedtoincreaseasaproportionofcorporateprofits.Yetin1997buybacksfirstsurpasseddividendsintheU.S.corporateeconomyand,evenwithdividendsincreasing,havefarexceededtheminrecentstock-marketbooms.31

Figure3.Netequityissues,U.S.nonfinancialcorporations,1946-2016

Source:BoardofGovernorsoftheFederalReserveSystem,FederalReserveStatisticalRelease

Z.1,“FinancialAccountsoftheUnitedStates:FlowofFunds,BalanceSheets,andIntegratedMacroeconomicAccounts,”TableF-223:CorporateEquities,June8,2017,athttps://www.federalreserve.gov/releases/z1/current/

31WilliamLazonick,“StockBuybacks:FromRetain-and-ReinvesttoDownsize-and-Distribute,”CenterforEffectivePublicManagement,BrookingsInstitution,April2015,pp.10-11,athttp://www.brookings.edu/research/papers/2015/04/17-stock-buybacks-lazonick;Lazonick,“TheValue-ExtractingCEO.”

Lazonick:InnovativeEnterpriseandSustainableProsperity

21

UsingthedatainFigure3,thefirstdatacolumnofTable1showstheamountsofnetequityissuesbynonfinancialcorporations,decadebydecade,from1946to2015,in2015dollars.ForthefirstthreedecadesafterWorldWarII,netequityissuesweremoderatelypositiveinthecorporateeconomyasawhole.Inthefollowingdecades,however,netequityissuesbecameincreasinglynegative (even after adjusting for inflation). As a gauge of their growing importance in theeconomy,theseconddatacolumnofTable1showsnetequityissuesasaproportionofGDP.

Table1.Netequityissuesbynon-financialcorporationsintheU.S.economy,

bydecadein2015dollars,andasapercentofGDP Netequityissues,

U.S.non-financialcorporations2015$billions

Netequityissuesas%ofGDP

1946-1955 143.2 0.561956-1965 110.9 0.301966-1975 316.0 0.581976-1985 -290.9 -0.401986-1995 -1,002.5 -1.001996-2005 -1,524.4 -1.092006-2015 -4,466.6 -2.65

Sources:NetequityissuesdataisthesameasinFigure4,adjustedto2015U.S.dollars,usingtheconsumerpriceindexinCouncilofEconomicAdvisors,Economic Report of the President 2017, January 2017, Table B-10, athttp://www.presidency.ucsb.edu/economic_reports/2017.pdf.

AsshowninFigure4,sincetheearly1980s,majorU.S.businesscorporationshavebeendoingstockbuybacksontopof(andnotinsteadof)makingdividendpaymentstoshareholders.Figure4showsdividendsandbuybacksfor236companiesthatwereintheS&P500IndexinJanuary2016thatwerepubliclylistedfrom1981through2015.Atthebeginningofthe1980s,buybackswereminimal,andfrom1981through1983buybacksforthese236companiesabsorbedonly4.3percentofnetincome,withdividendsrepresenting49.5percent.Thebuybackproportionofnet income increased to 18.8 percent in 1984 and 30.8 percent in 1985,while the dividendproportionswere42.5percentand52.4percent.Thereafter,byten-yearperiods,thebuybackproportionsofnetincomeincreasedfrom25.8percentin1986-1995to42.9percentin1996-2005and49.5percentin2006-2015,whiledividendpayoutsoverthesedecadalperiodswere50.7percent,39.0percent,and39.1percent,respectively.Eventhoughdividendpayoutratioswerelowerin1996-2005and2006-2015thanin1986-1995,totalpayoutratiostoshareholdersrosefrom76.5percentto81.9percentto88.6percentoverthesethreeperiods.Mostrecently,thetotalpayoutratiosforthese236companieswere97.0percentin2014and106.2percentin2015.

Lazonick:InnovativeEnterpriseandSustainableProsperity

22

Figure4.Meancash-dividendandstock-buybackdistributionsin2015dollarsfor236companies in theS&P500 Index in January2016 thatwerepublicly listedfrom1981through2015

Source:StandardandPoor’sCompustatdatabase;calculationsbyMustafaErdemSakinçandEmreGomeçof

theAcademic-IndustryResearchNetwork.Overthepastthreedecades,U.S.stockmarkets,ofwhichtheNewYorkStockExchangeandtheNationalAssociationofSecuritiesDealersAutomatedQuotation(NASDAQ)exchangearebyfarthemostimportant,haveenabledtheextractionoftrillionsofdollarsfrombusinesscorporationsintheformofstockbuybacks.Ofcourse,somecompaniesdoraisefundsonthestockmarket,particularlywhen theyaredoing initialpublicofferings (IPOs).But theseamounts tend toberelativelysmall,swampedoverallbystockrepurchases,whichhavebeenmainlyresponsibleforthehugelynegativenetequityissuesofnonfinancialcorporationsshowninFigure1.Moreover,whenthemostsuccessfulstartupsbecomemajorenterprises,oftenemployingtensofthousandsofpeople,theytootendtobecomemajorrepurchasersoftheirownshares.Whyare companiesdoing thesemassivedistributions to shareholders? In anarticle “ProfitsWithoutProsperity”thatIpublishedinHarvardBusinessReviewin2014,32Iarguethatthestock-basedremunerationofseniorexecutiveswhoexercisestrategiccontroloverresourceallocationin these U.S. business corporations incentivizes them to manipulate their companies’ stockprices.Thatistheonlylogicalexplanationforthisbuybackactivity.Standard&Poor’sExecuCompdatabase provides the numbers needed to determine how much money the highest-paidcorporateexecutivesintheUnitedStatestakehomeintotalandtheproportionoftheirtotalcompensationwhichisstockbased.Figure5showstheaveragetotalcompensationofthe500highest-paidexecutives intheExecuCompdatabaseforeachyearfrom2006through2015. Itranges froma lowof$15.9million in2009,whenthestockmarketshadcrashed,withstock-32WilliamLazonick,“ProfitsWithoutProsperity:StockBuybacksManipulatetheMarketandLeaveMostAmericansWorseOff,”HarvardBusinessReview,September2014,46-55.

Lazonick:InnovativeEnterpriseandSustainableProsperity

23

basedpay(realizedgainsfromstockoptionsandstockawards)makingup60percentofthetotal,toahighof$32.6millionin2015,withstock-basedgainsmakingup82percentofthetotal.U.S.corporate executives are incentivized to boost their companies’ stock prices and are amplyrewardedfordoingso.InSEC-approvedstockbuybacks,theyhaveattheirdisposalaninstrumenttoenrichthemselves.Intheirmassive,widespread,andubiquitoususeofthisinstrument,theyhavebeenparticipatinginthelegalizedlootingoftheU.S.businesscorporation.

Figure 5. Mean total direct compensation, 500 highest-paid namedexecutivesintheUnitedStates,foreachyear,2006-2015

Source:Standard&Poor’sExecuCompdatabase,retrievedOctober11,2016.CalculationsbyMattHopkins

oftheAcademic-IndustryResearchNetworkNote:Thefollowingextraordinarilyhighlypaidoutliers,with$1billionormoreintotalcompensation,have

beenremoved:2012,RichardKinder,KinderMorgan,$1.1billion,andMarkZuckerberg,Facebook,$2.3billion;2013,MarkZuckerberg,$3.3billion.

Thisstock-basedpayofU.S.corporateexecutivesisamajorreasonfortheextremeconcentrationofincomethathasoccurredsincethe1980samongtherichesthouseholdsintheUnitedStates.Basedaswellondatafromhouseholdfederaltaxfilings,Figure6showstheshareofincomeinthehandsofthe0.1percentofallhouseholdswiththehighestincomes,includingcapitalgains,from1916through2011.In1975,theshareofthetop0.1percentwas2.56percentofallU.S.incomes,thelowestproportionovertheentire96-yearperiod.Thehighestproportionwas12.28percent in2007, justbefore the financialcrisis. In thecrisis, theshareof the top0.1percentdeclined,butwiththerecoverybouncedback.In2012(notincludedinFigure6),theshareofthetop0.1percentwas11.33percent,thefourth-highestproportionrecorded.33Clearly,fromthe

33TheWorldWealthandIncomeDatabase,athttp://topincomes.parisschoolofeconomics.eu/#Database:UnitedStates,P99.9incomethreshold.Forthelatestdataonthepre-taxshareofthetop0.1%notincludingcapitalgains,seehttp://wid.world/world/#sptinc_p99.9p100_z/US/last/eu/k/p/yearly/s/false/2.9295/12.5/curve/false

Lazonick:InnovativeEnterpriseandSustainableProsperity

24

late1970s,onadramaticscale,therewasareversalinthetrendtowardasomewhatfallingshareofincomeofthetop0.1percentthathadoccurredinthedecadesafterWorldWarII.

Figure6:ShareoftotalU.S.incomesofthetop0.1%ofhouseholdsintheU.S.income

distributionanditscomponents,1916-2011

Source:http://topincomes.parisschoolofeconomics.eu/#Database:UnitedStates,Top0.1%income

composition.Note:Thecategory“salaries”includescompensationfromtherealizedgainsonexercisingstock

optionsandthevestingofstockawards.NotethatinFigure6,alargepartoftheexplosionoftheshareofthetop0.1percenthasbeenintheformof“salaries.”Asindicated,these“salaries”includerealizedgainsfromstock-basedpay—stockoptionsandstockawards—thatshowupinthesummarystatisticsofanexecutive’sForm 1040 tax returns (the source of these data) as “Wages, salaries, tips, etc.” Since 1976virtuallyalloftherealizedgainsfromstock-basedpayhasbeentaxedattheordinaryincome-taxratesandhenceisnotincludedinthe“capitalgains”portionoftheincomesofthetop0.1percentasshowninFigure6.Federal tax returns include information on a filer’s occupation and, through an employeridentificationnumber(EIN)onFormW-2,thetypeofbusinesssectorthatprovidesthetaxpayerwithhisorherprimaryemploymentincome.JonBakija,AdamColeandBradleyHeimaccessedfederaltaxreturndataforselectedyearsfrom1979to2005toanalyzetheoccupationsoffederaltaxpayers at the topof theU.S. incomedistribution. They found that “executives,managers,supervisors,andfinancialprofessionalsaccountforabout60percentofthetop0.1%ofincomeearnersinrecentyears,andcanaccountfor70percentoftheincreaseintheshareofnationalincomegoingtothetop0.1%oftheincomedistributionbetween1979and2005.”3434JonBakija,AdamCole,andBradleyT.Heim,“JobsandIncomeGrowthofTopEarnersandtheCausesofChangingIncomeInequality:EvidencefromU.S.TaxReturnData,”workingpaper,April,2012,at

Lazonick:InnovativeEnterpriseandSustainableProsperity

25

For2005,theyfoundthat,oftaxpayerswhoseincomes(includingcapitalgains)placedtheminthe top0.1%,executives,managers,andsupervisors innon-financebusinessesmadeup41.3percentof the total,while financialprofessionals (includingmanagement)wereanother17.7percent.Ofthe41.3percentwhowerenon-financeexecutives,managersorsupervisors,19.8percentweresalariedandtherestwereincloselyheldbusinesses.35Besidesthe6.2percentofthetop0.1%whowere“notworkingordeceased,”thenextlargestoccupationalgroupswerelawyerswith5.8percent,realestatewith5.1percent,andmedicalwith4.1percent.WecanusetheStandard&Poor’sExecuCompdatabase,whichcompilesdataonexecutivepaythatisinSECFormDEF14A—theproxystatementthatacompanyfilespriortoitsannualgeneralmeetingofshareholders—togetanideaoftherepresentationofhigh-paidcorporateexecutivesamongthetop0.1%ofhouseholdsintheincomedistribution.In2012,forexample,thethresholdincome including capital gains for inclusion in the top 0.1% of the income distribution was$1,906,047.36FromtheExecuCompproxystatementdataon“named”topexecutives(theCEO,CFO, and three other highest-paid executives), in 2012, 4,339 executives (41 percent of theexecutives in the ExecuComp database that year) had total compensation greater than thisthreshold amount,with an average incomeof $7,524,168.Of that amount, 64 percentwererealized gains from stock-based compensation,with 32 percent derived from the exercise ofstockoptionsandtheother32percentfromthevestingofstockawards.Thenumberof corporateexecutiveswho, in2012,weremembersof the top0.1%clubwas,however,farhigherthan4,339fortworeasons.First,totalcorporatecompensationofthenamedexecutivesdoesnotincludeothernon-compensationincome(fromsecurities,property,feesforsitting on the boards of other corporations, etc.) thatwould be included in their federal taxreturns. Ifwe assume that namedexecutiveswhose corporate compensationwasbelow the$1.91million thresholdwereable toaugment that incomeby25percent (topickaplausiblenumber)fromothersources,thenthenumberofnamedexecutivesinthetop0.1%in2012wouldhavebeen5,095.Second, included inthetop0.1%oftheU.S. incomedistributionwereapotentially large,butunknown,numberofU.S.corporateexecutiveswhosepaywasabovethe$1.91millionthreshold,butwhowerenotnamedinproxystatementsbecausetheywerenottheCEO,CFOoroneofthethreeotherhighest-paidexecutives,asrequiredbySECregulations.Forexample,ofthehighest-paidIBMexecutives in2012namedinthecompany’sproxystatement,thelowestpaidhadatotalcompensationof$9,177,663.TherewerepresumablymanyotherIBMexecutiveswhosetotalcompensationwasbetweenthisamountandthe$1.91millionthresholdforinclusioninthetop0.1%.These “unnamed”executiveswouldhavebeenamong the top0.1% in the incomedistribution.

https://web.williams.edu/Economics/wp/BakijaColeHeimJobsIncomeGrowthTopEarners.pdf.Thequoteisfromthepaper’sabstract.

35Ibid.,p.38.36TheWorldWealthandIncomeDatabase,athttp://topincomes.parisschoolofeconomics.eu/#Database:UnitedStates,P99.9incomethreshold.

Lazonick:InnovativeEnterpriseandSustainableProsperity

26

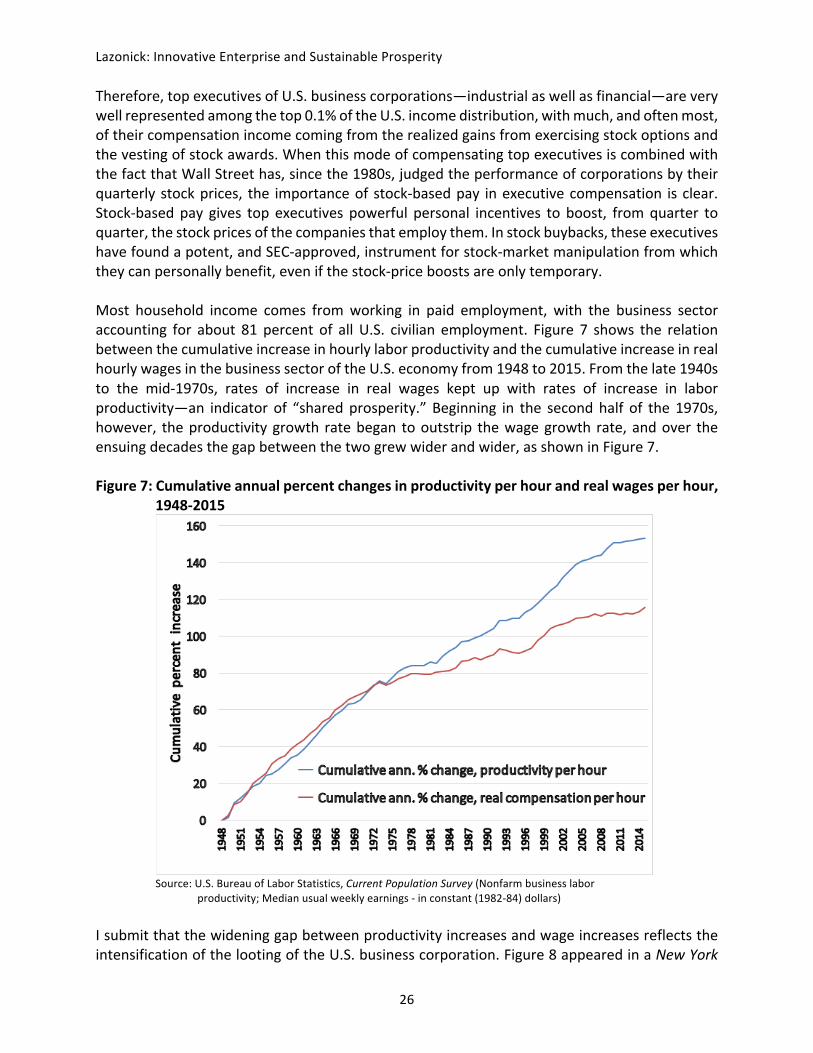

Therefore,topexecutivesofU.S.businesscorporations—industrialaswellasfinancial—areverywellrepresentedamongthetop0.1%oftheU.S.incomedistribution,withmuch,andoftenmost,oftheircompensationincomecomingfromtherealizedgainsfromexercisingstockoptionsandthevestingofstockawards.WhenthismodeofcompensatingtopexecutivesiscombinedwiththefactthatWallStreethas,sincethe1980s,judgedtheperformanceofcorporationsbytheirquarterly stockprices, the importanceof stock-basedpay inexecutivecompensation is clear.Stock-basedpay gives top executives powerful personal incentives to boost, fromquarter toquarter,thestockpricesofthecompaniesthatemploythem.Instockbuybacks,theseexecutiveshavefoundapotent,andSEC-approved,instrumentforstock-marketmanipulationfromwhichtheycanpersonallybenefit,evenifthestock-priceboostsareonlytemporary.Most household income comes fromworking in paid employment, with the business sectoraccounting for about 81 percent of all U.S. civilian employment. Figure 7 shows the relationbetweenthecumulativeincreaseinhourlylaborproductivityandthecumulativeincreaseinrealhourlywagesinthebusinesssectoroftheU.S.economyfrom1948to2015.Fromthelate1940sto the mid-1970s, rates of increase in real wages kept up with rates of increase in laborproductivity—an indicator of “sharedprosperity.” Beginning in the secondhalf of the 1970s,however, theproductivitygrowth ratebegan tooutstrip thewagegrowth rate,andover theensuingdecadesthegapbetweenthetwogrewwiderandwider,asshowninFigure7.Figure7:Cumulativeannualpercentchangesinproductivityperhourandrealwagesperhour,

1948-2015

Source:U.S.BureauofLaborStatistics,CurrentPopulationSurvey(Nonfarmbusinesslabor

productivity;Medianusualweeklyearnings-inconstant(1982-84)dollars)IsubmitthatthewideninggapbetweenproductivityincreasesandwageincreasesreflectstheintensificationofthelootingoftheU.S.businesscorporation.Figure8appearedinaNewYork

Lazonick:InnovativeEnterpriseandSustainableProsperity

27