inrs kingsley katahdin oct 2016 draft

TRANSCRIPT

Katahdin Revitalization Speaker SeriesThe Future of Maine’s Forest Economy

October 27, 2016Millinocket, Maine

Eric KingsleyInnovative Natural Resource Solutions LLC

[email protected] 207‐233‐9910

Innovative Natural Resource Solutions LLC• Founded in 1994• Offices in New Hampshire and Maine• Focus at the intersection of forest industry, energy and economic development

• Author of Maine Future Forest Economy Project (2005)• Services include:

‐ consulting in renewable energy‐ advocacy‐ forest management and protection‐ forest certification and sustainability

• Clients from the private, non‐profit and government sectors• Conducted work in all regions of North America• www.inrsllc.com

The Wood

The Markets

‐

1

2

3

4

5

6

7

8

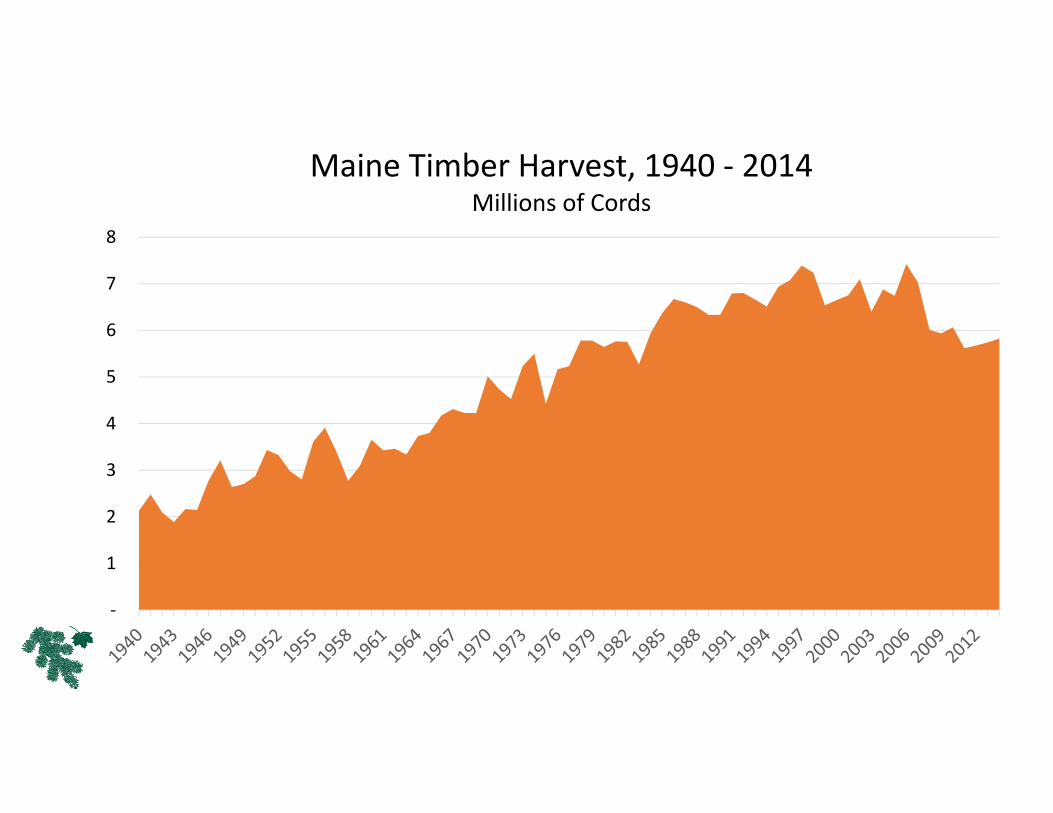

Maine Timber Harvest, 1940 ‐ 2014Millions of Cords

‐

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

2007 2008 2009 2010 2011 2012 2013 2014

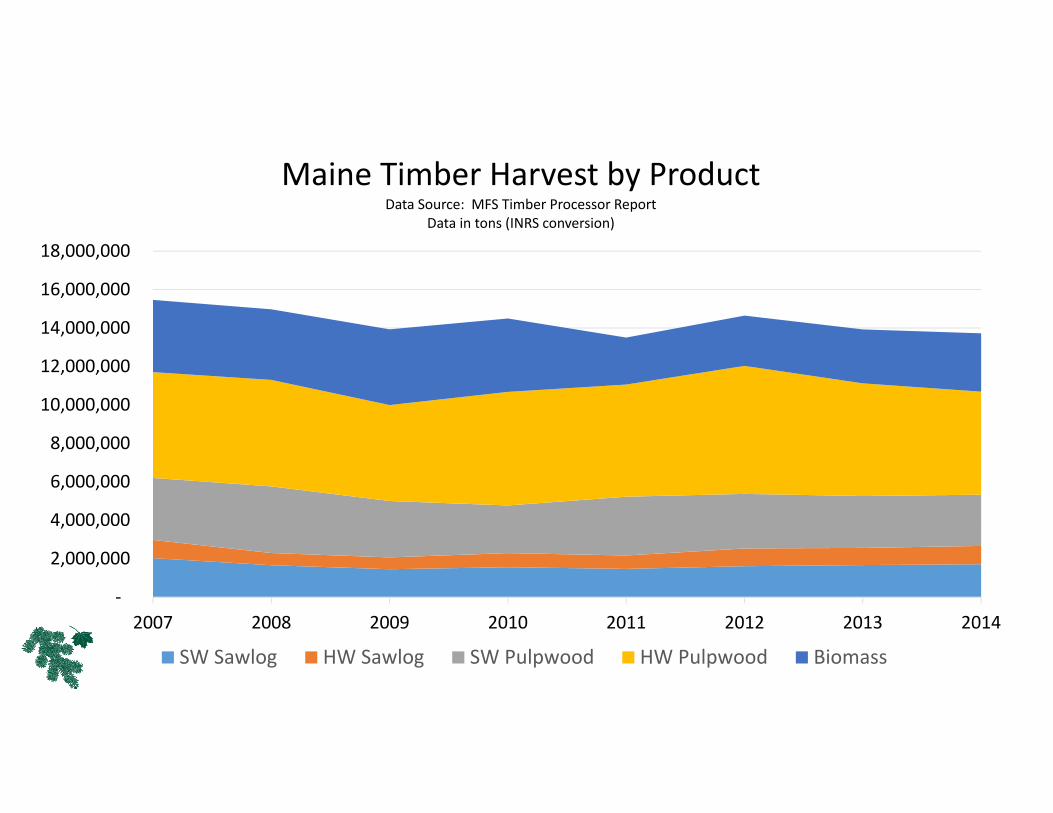

Maine Timber Harvest by ProductData Source: MFS Timber Processor Report

Data in tons (INRS conversion)

SW Sawlog HW Sawlog SW Pulpwood HW Pulpwood Biomass

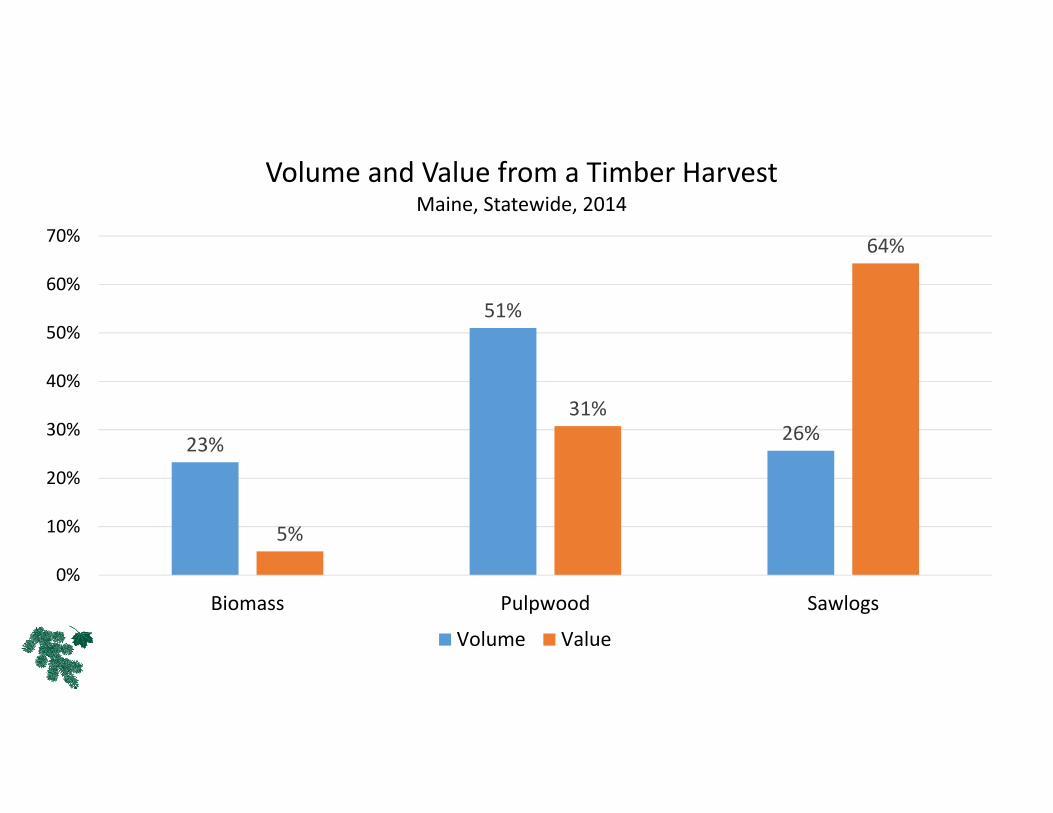

23%

51%

26%

5%

31%

64%

0%

10%

20%

30%

40%

50%

60%

70%

Biomass Pulpwood Sawlogs

Volume and Value from a Timber HarvestMaine, Statewide, 2014

Volume Value

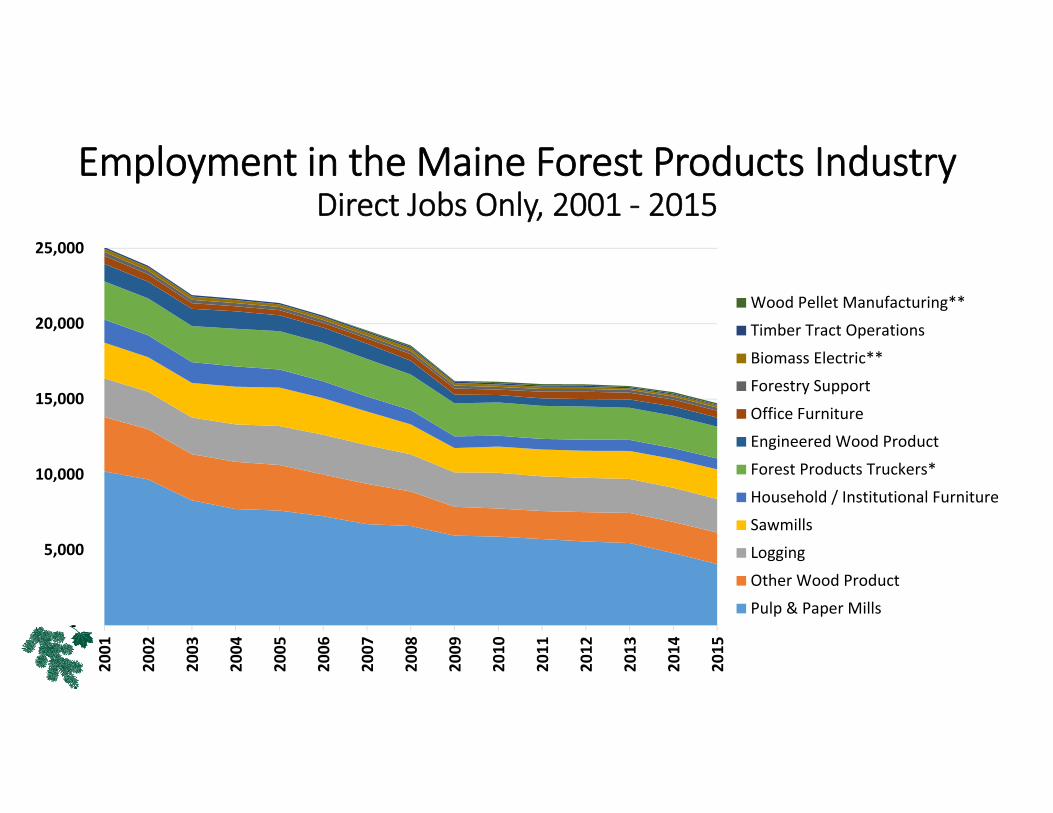

Employment in the Maine Forest Products IndustryDirect Jobs Only, 2001 ‐ 2015

‐

5,000

10,000

15,000

20,000

25,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Wood Pellet Manufacturing**

Timber Tract Operations

Biomass Electric**

Forestry Support

Office Furniture

Engineered Wood Product

Forest Products Truckers*

Household / Institutional Furniture

Sawmills

Logging

Other Wood Product

Pulp & Paper Mills

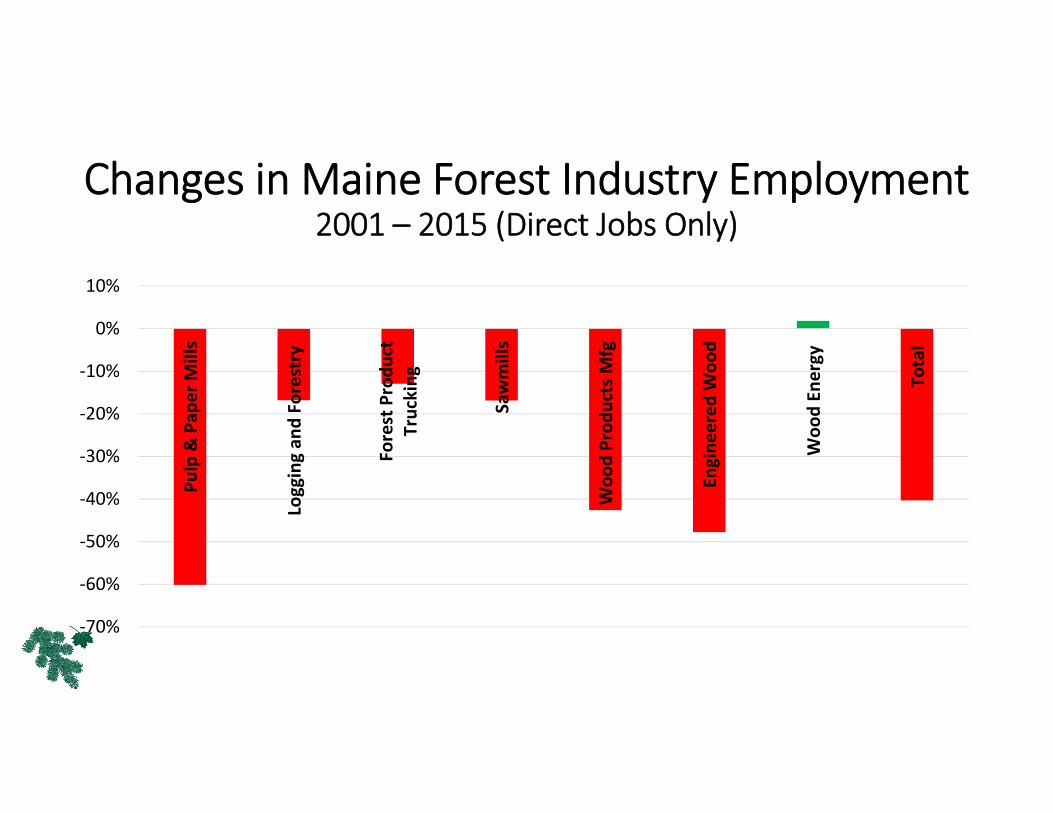

Changes in Maine Forest Industry Employment2001 – 2015 (Direct Jobs Only)

‐70%

‐60%

‐50%

‐40%

‐30%

‐20%

‐10%

0%

10%

Pulp & Pap

er M

ills

Logging an

d Forestry

Forest Produ

ctTrucking

Sawmills

Woo

d Prod

ucts M

fg

Engine

ered

Woo

d

Woo

d En

ergy

Total

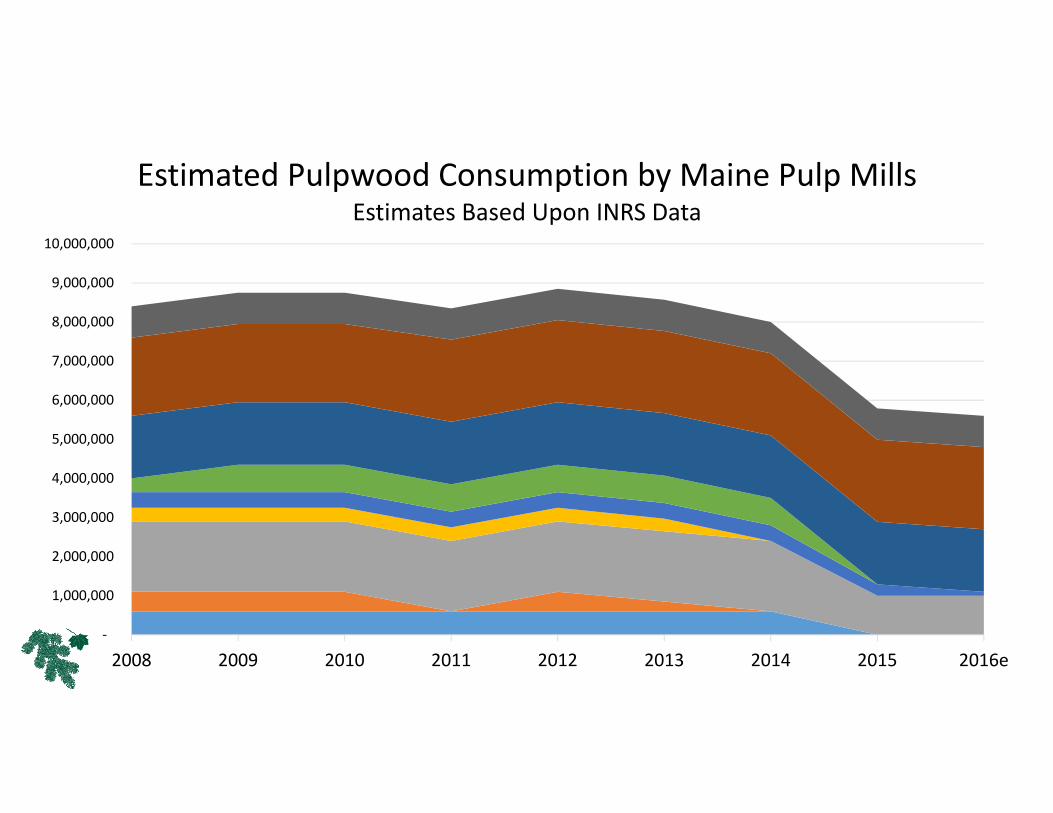

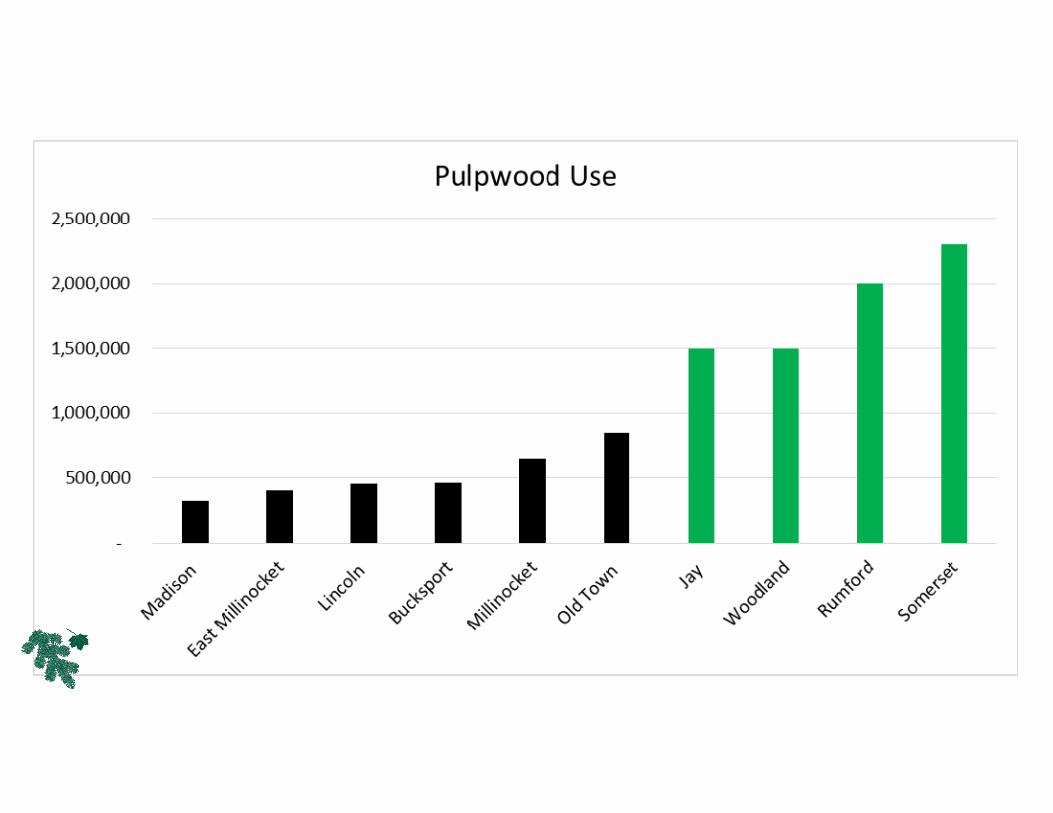

Markets for Low‐Grade

‐

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

2008 2009 2010 2011 2012 2013 2014 2015 2016e

Estimated Pulpwood Consumption by Maine Pulp MillsEstimates Based Upon INRS Data

‐

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

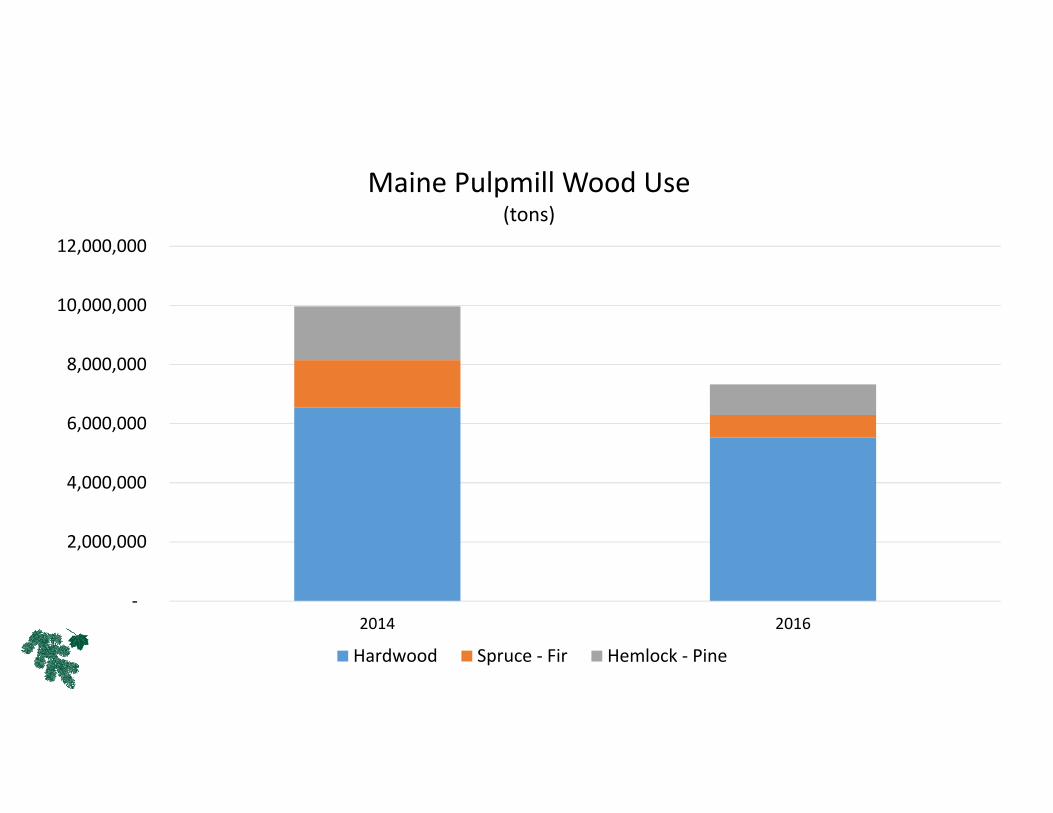

2014 2016

Maine Pulpmill Wood Use(tons)

Hardwood Spruce ‐ Fir Hemlock ‐ Pine

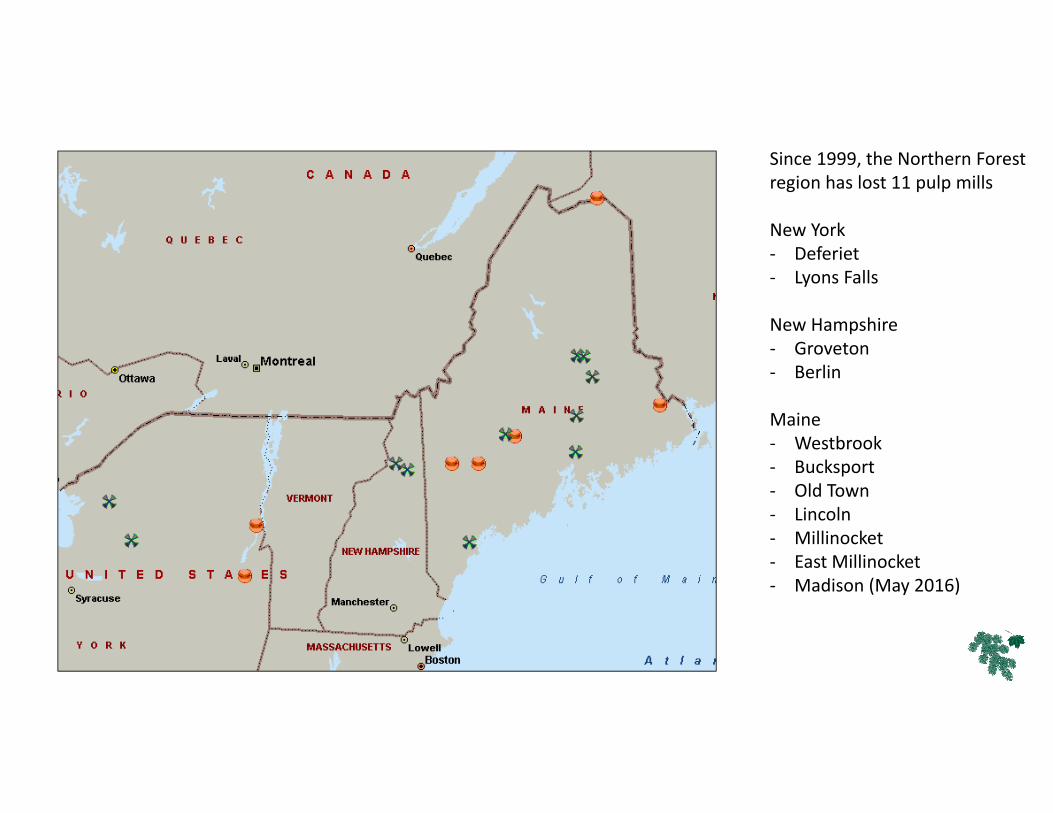

Since 1999, the Northern Forest region has lost 11 pulp mills

New York‐ Deferiet‐ Lyons Falls

New Hampshire‐ Groveton‐ Berlin

Maine‐ Westbrook‐ Bucksport‐ Old Town‐ Lincoln‐ Millinocket‐ East Millinocket‐ Madison (May 2016)

Emails you ne

ver e

xpected…

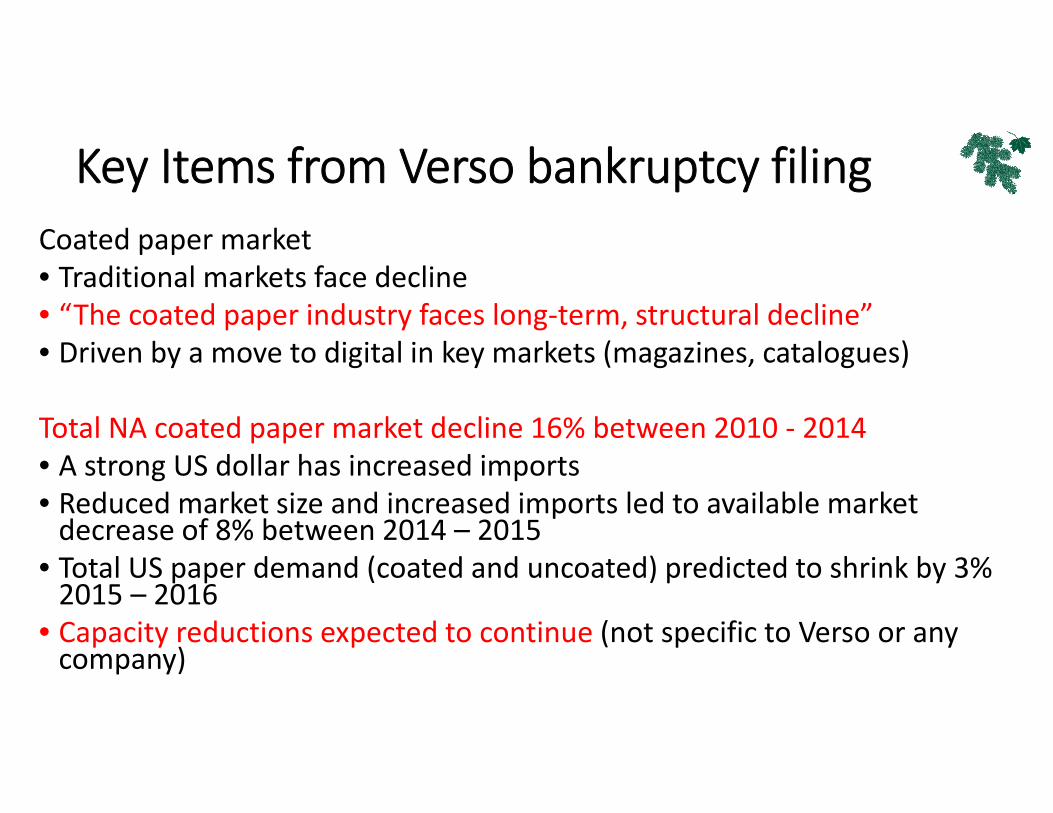

Key Items from Verso bankruptcy filingCoated paper market• Traditional markets face decline• “The coated paper industry faces long‐term, structural decline” • Driven by a move to digital in key markets (magazines, catalogues)

Total NA coated paper market decline 16% between 2010 ‐ 2014• A strong US dollar has increased imports• Reduced market size and increased imports led to available market decrease of 8% between 2014 – 2015

• Total US paper demand (coated and uncoated) predicted to shrink by 3% 2015 – 2016

• Capacity reductions expected to continue (not specific to Verso or any company)

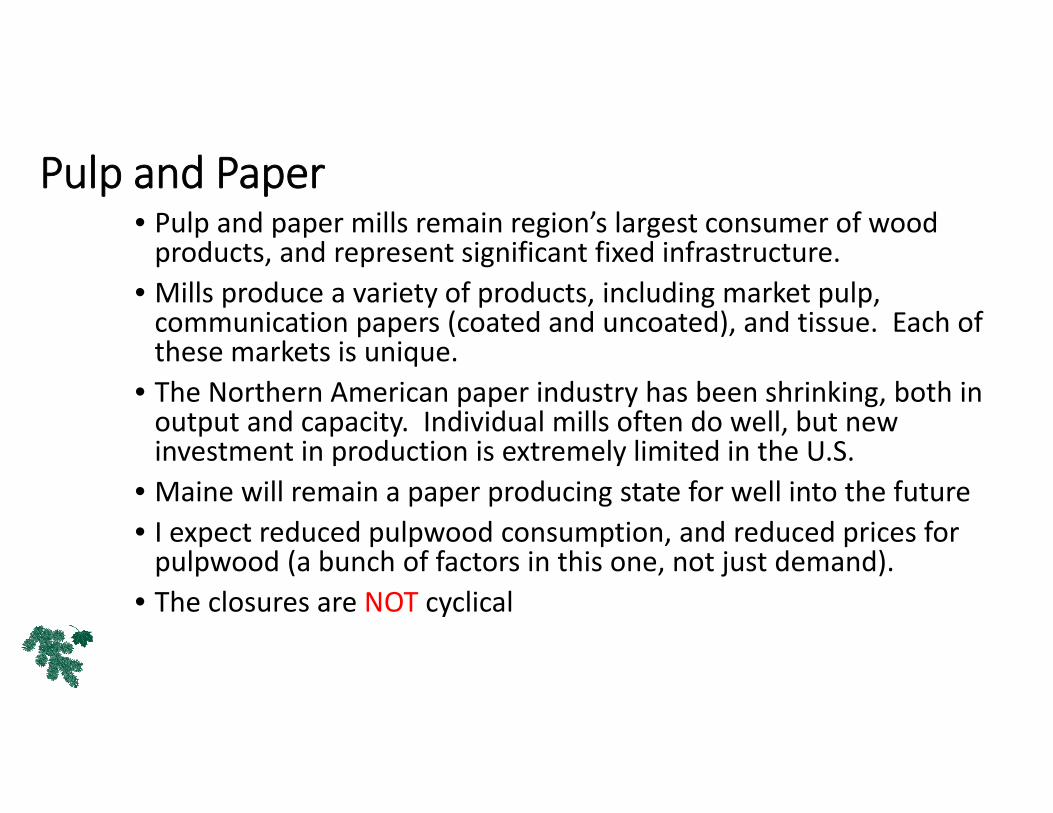

Pulp and Paper• Pulp and paper mills remain region’s largest consumer of wood products, and represent significant fixed infrastructure.

• Mills produce a variety of products, including market pulp, communication papers (coated and uncoated), and tissue. Each of these markets is unique.

• The Northern American paper industry has been shrinking, both in output and capacity. Individual mills often do well, but new investment in production is extremely limited in the U.S.

• Maine will remain a paper producing state for well into the future• I expect reduced pulpwood consumption, and reduced prices for pulpwood (a bunch of factors in this one, not just demand).

• The closures are NOT cyclical

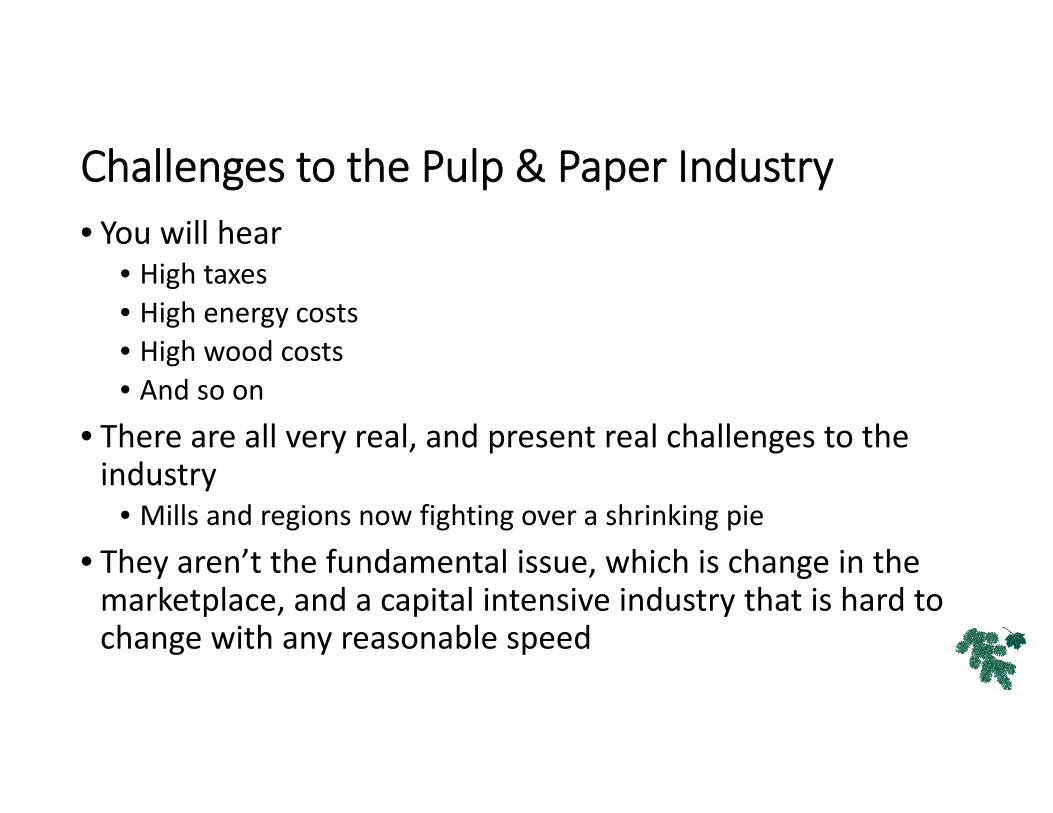

Challenges to the Pulp & Paper Industry• You will hear

• High taxes• High energy costs• High wood costs• And so on

• There are all very real, and present real challenges to the industry

• Mills and regions now fighting over a shrinking pie• They aren’t the fundamental issue, which is change in the marketplace, and a capital intensive industry that is hard to change with any reasonable speed

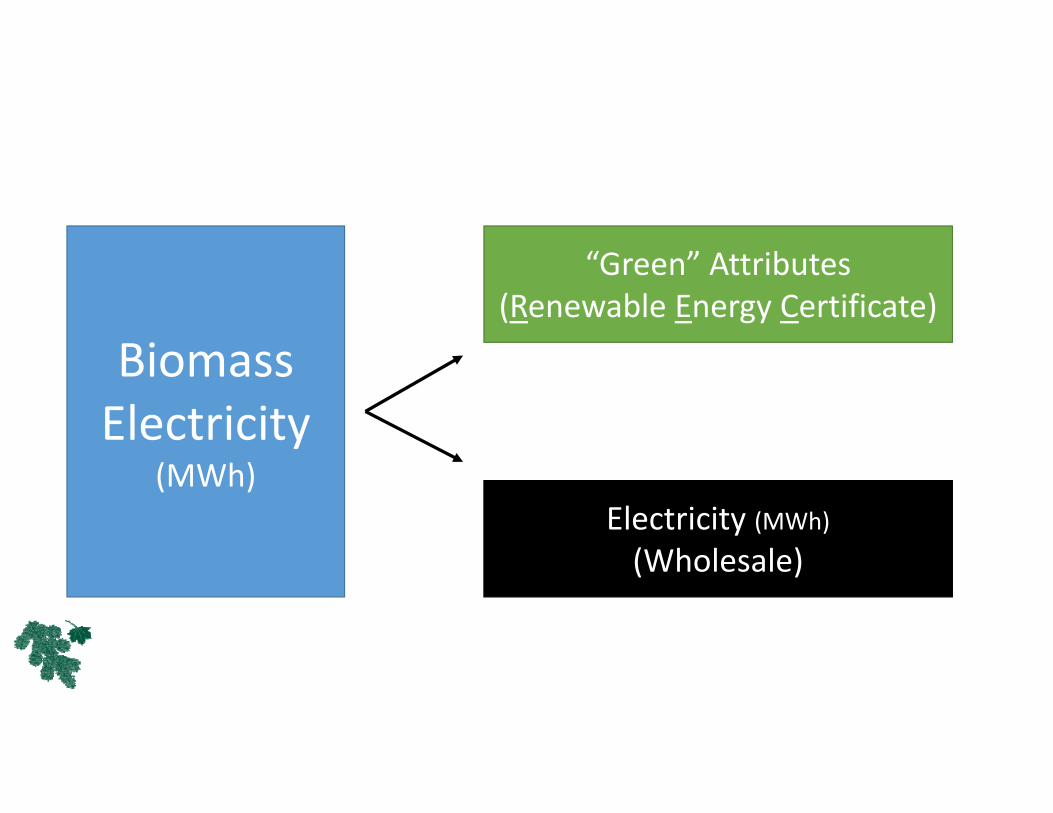

Biom

ass

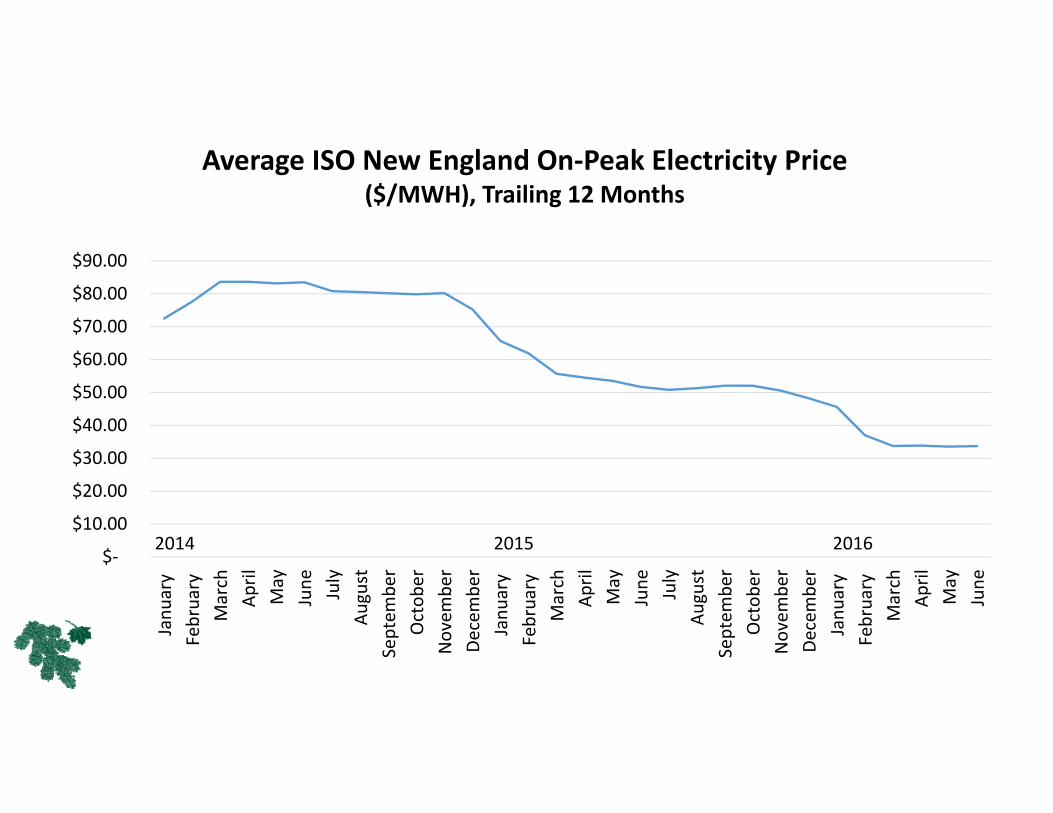

Biomass Electricity

(MWh)

“Green” Attributes(Renewable Energy Certificate)

Electricity (MWh)

(Wholesale)

$‐

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

$90.00

Janu

ary

February

March

April

May

June July

August

Septem

ber

Octob

erNovem

ber

Decembe

rJanu

ary

February

March

April

May

June July

August

Septem

ber

Octob

erNovem

ber

Decembe

rJanu

ary

February

March

April

May

June

2014 2015 2016

Average ISO New England On‐Peak Electricity Price ($/MWH), Trailing 12 Months

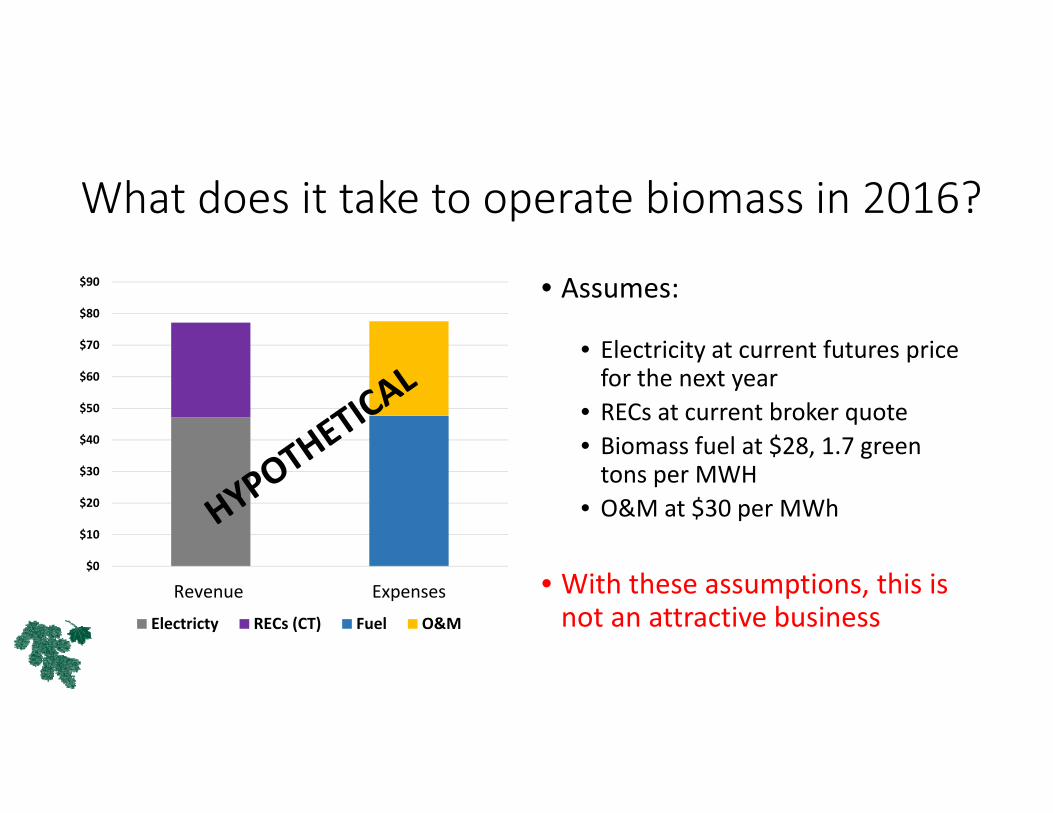

What does it take to operate biomass in 2016?

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

Revenue Expenses

Electricty RECs (CT) Fuel O&M

• Assumes:

• Electricity at current futures price for the next year

• RECs at current broker quote• Biomass fuel at $28, 1.7 green tons per MWH

• O&M at $30 per MWh

• With these assumptions, this is not an attractive business

23

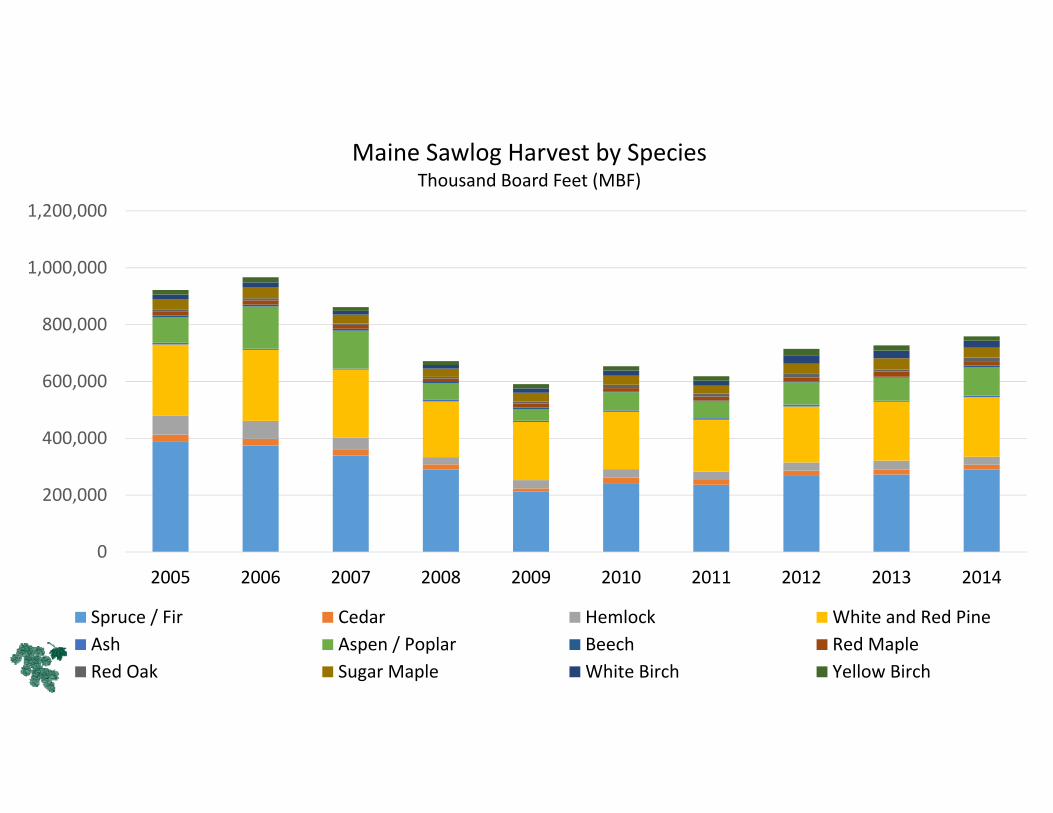

Sawlog Markets

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Maine Sawlog Harvest by SpeciesThousand Board Feet (MBF)

Spruce / Fir Cedar Hemlock White and Red PineAsh Aspen / Poplar Beech Red MapleRed Oak Sugar Maple White Birch Yellow Birch

0

20

40

60

80

100

120

140

160

180

200

0

50

100

150

200

250

300

350

400

450

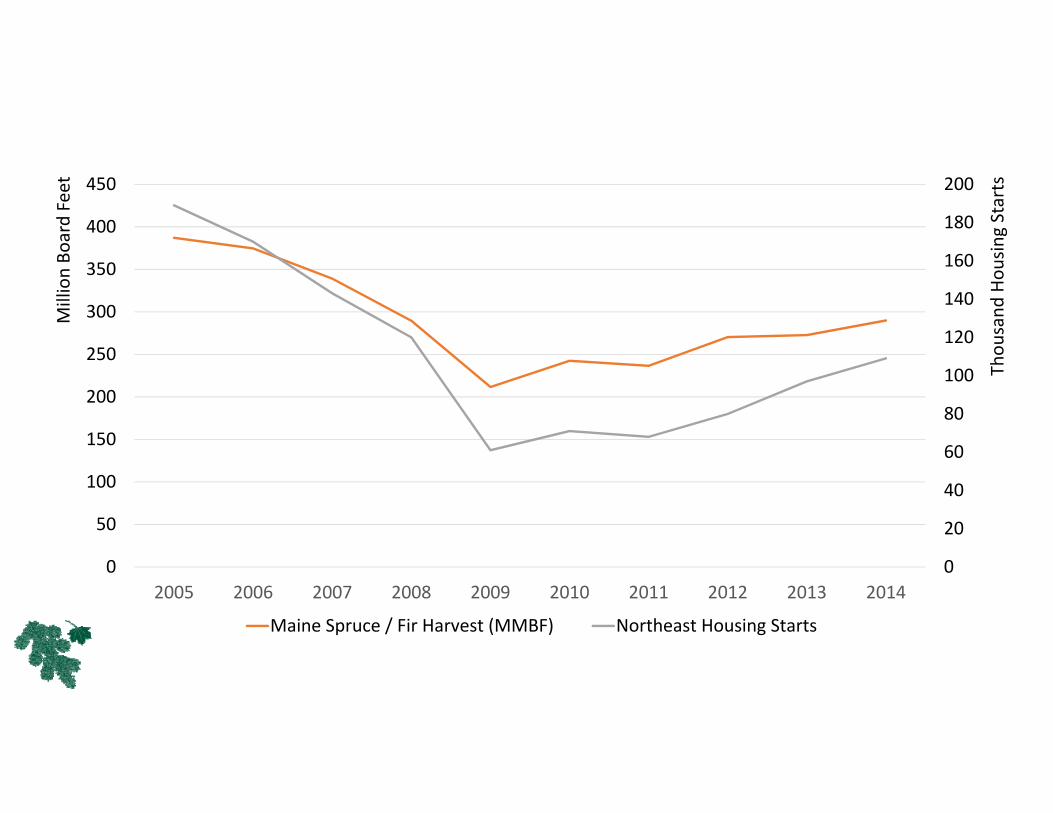

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Maine Spruce / Fir Harvest (MMBF) Northeast Housing Starts

Million Bo

ard Feet

Thou

sand

Hou

sing Starts

Emerging Products

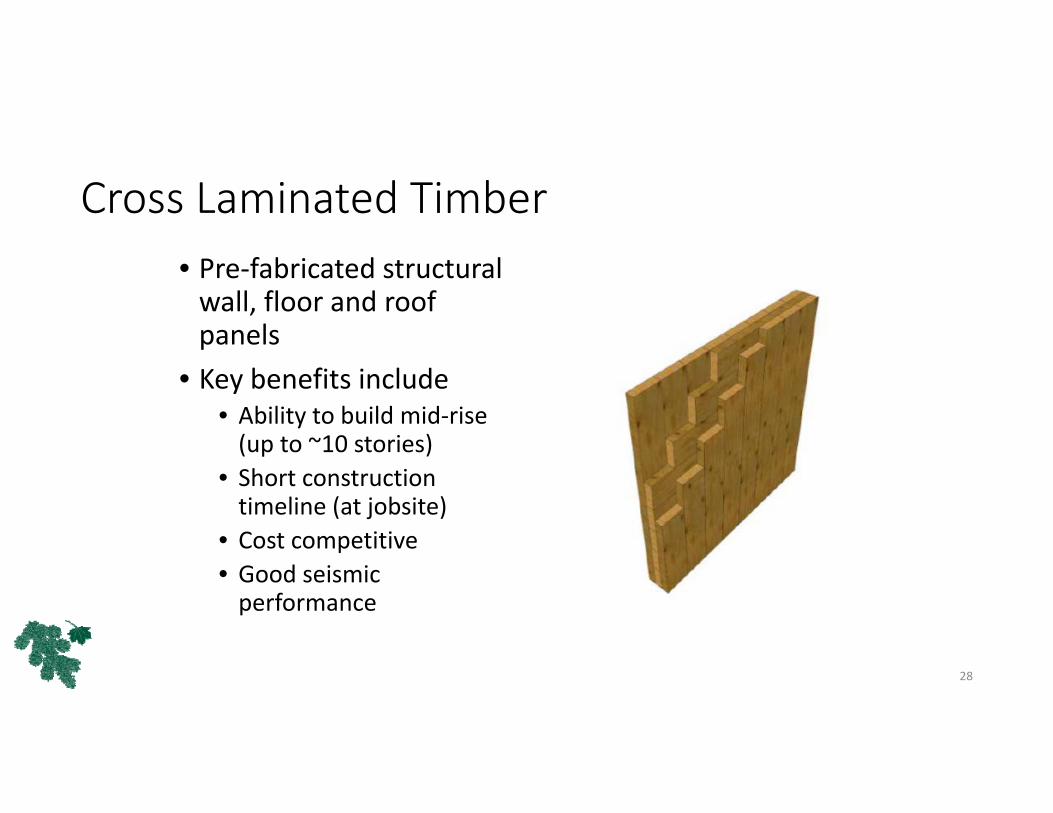

Cross Laminated Timber• Pre‐fabricated structural wall, floor and roof panels

• Key benefits include• Ability to build mid‐rise (up to ~10 stories)

• Short construction timeline (at jobsite)

• Cost competitive• Good seismic performance

28

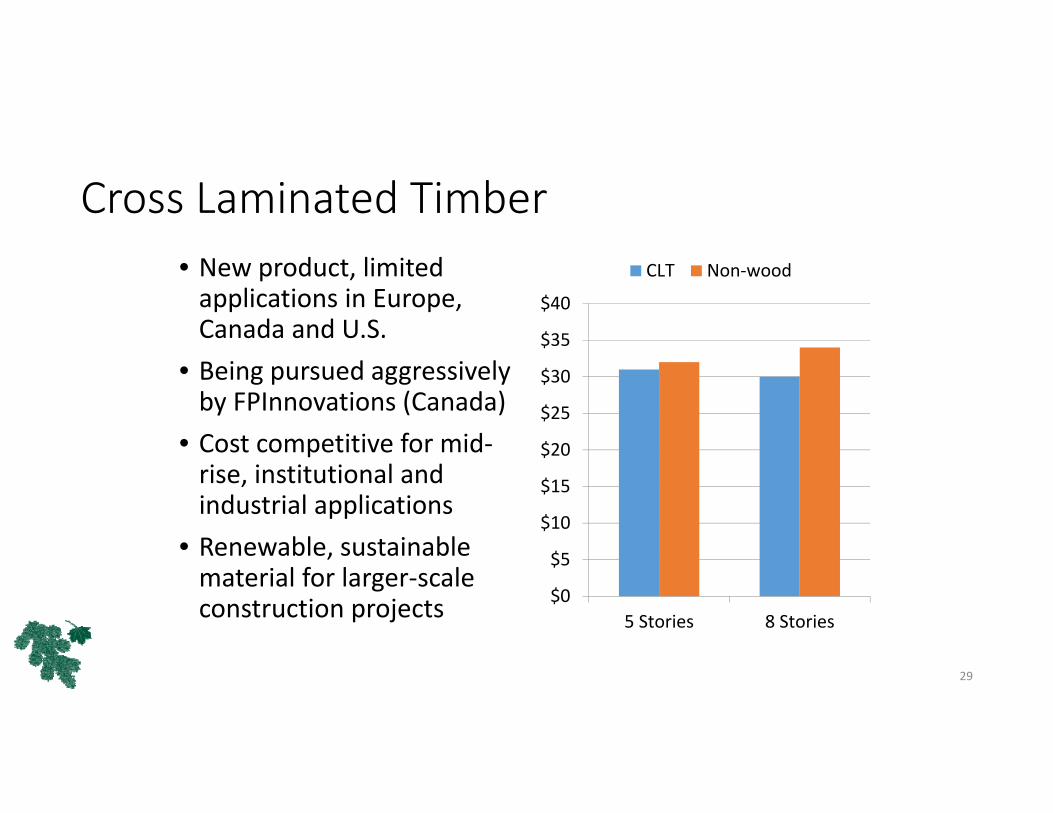

Cross Laminated Timber• New product, limited applications in Europe, Canada and U.S.

• Being pursued aggressively by FPInnovations (Canada)

• Cost competitive for mid‐rise, institutional and industrial applications

• Renewable, sustainable material for larger‐scale construction projects $0

$5

$10

$15

$20

$25

$30

$35

$40

5 Stories 8 Stories

CLT Non‐wood

29

Photos of CLT Under ConstructionExcerpted from FPInnovations Presentations

30

Bio‐Based Material

• Significant opportunities to replace fossil‐fuel based products with wood‐based

• Fuels, chemicals, plastics, etc. – a field limited only by economics• To date, that has been a big limitation

• Bio‐Based Maine received funding to pursue this opportunity as a spin‐off of federal economic development efforts

• Easier said than done, but the state is well positioned, and UMO in a significant leadership role

The glass is half full…

• We have markets, and are incredibly well positioned compared to other parts of the country

• We have the forest resource and supply infrastructure (landowners, loggers, entire forest industry ecosystem) that would make other regions jealous

• We live in close proximity to (and are part of) the greatest collection of consumers in the history of the world

• There may never be a better time to be develop a project or technology that uses low‐grade, particularly softwood

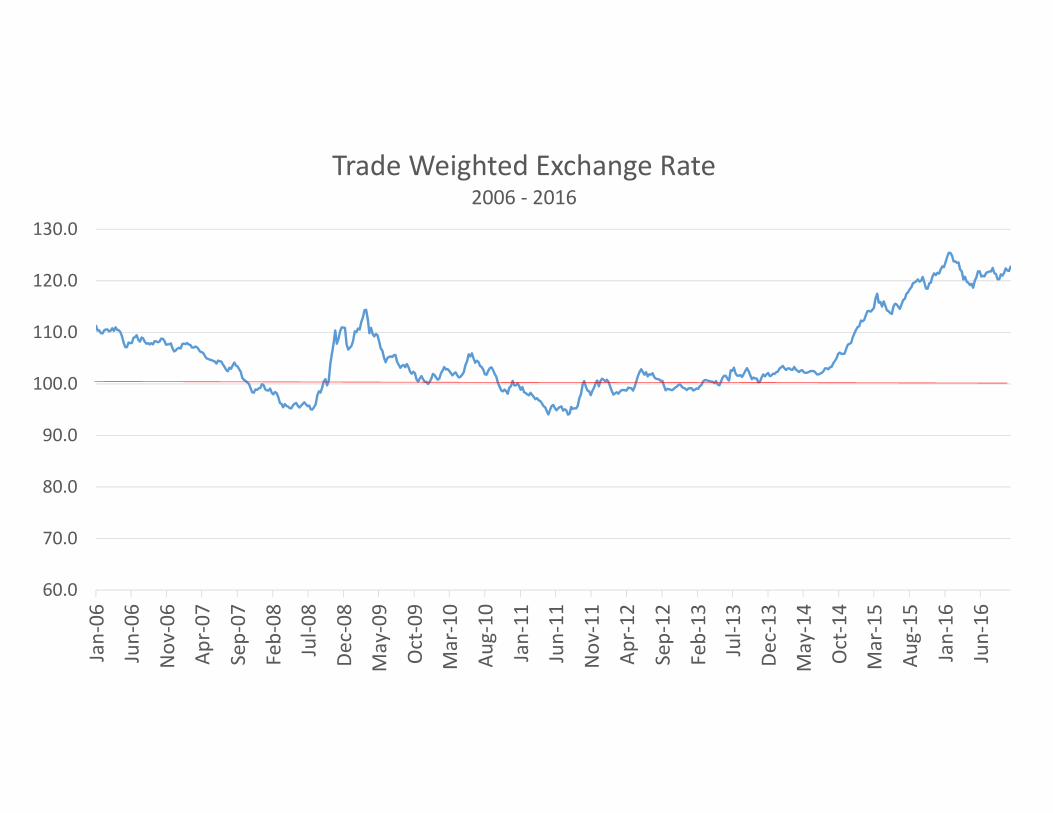

60.0

70.0

80.0

90.0

100.0

110.0

120.0

130.0

Jan‐06

Jun‐06

Nov

‐06

Apr‐07

Sep‐07

Feb‐08

Jul‐0

8

Dec‐08

May‐09

Oct‐09

Mar‐10

Aug‐10

Jan‐11

Jun‐11

Nov

‐11

Apr‐12

Sep‐12

Feb‐13

Jul‐1

3

Dec‐13

May‐14

Oct‐14

Mar‐15

Aug‐15

Jan‐16

Jun‐16

Trade Weighted Exchange Rate 2006 ‐ 2016