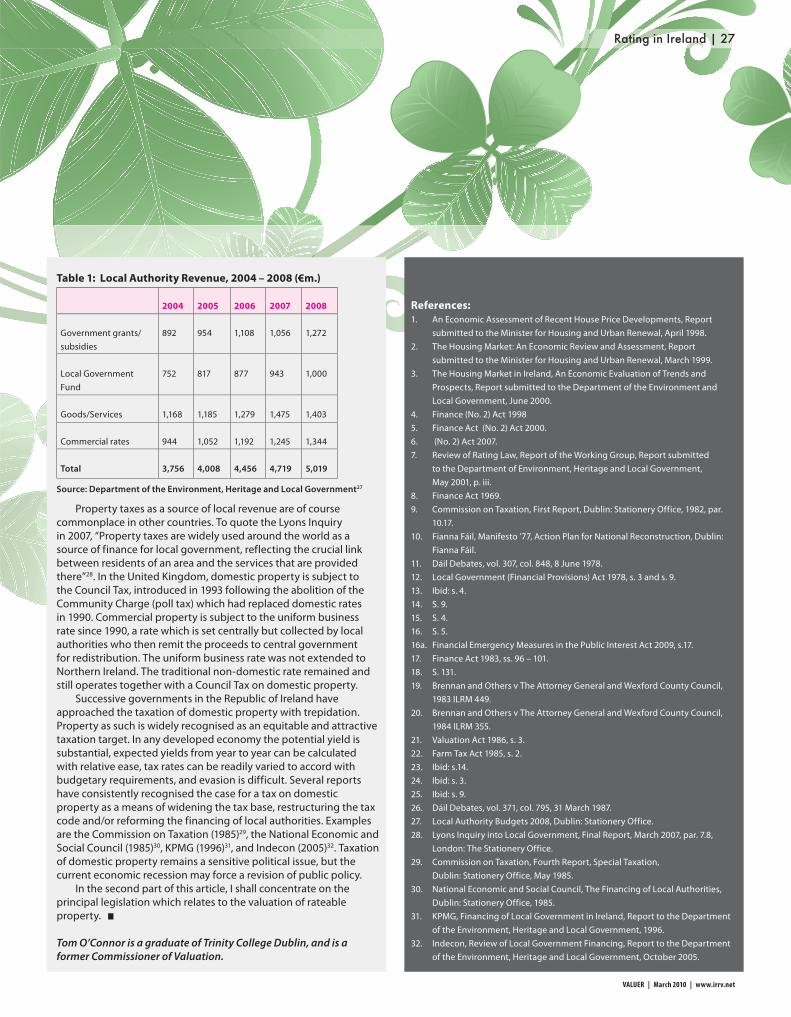

inside: rating in ireland | rics rating diploma holders | valuation in … · 2016-05-09 · •...

TRANSCRIPT

www.irrv.net

March 2010

ISSN: 1361-1305

VALUERInside: Rating in Ireland | RICS Rating Diploma Holders | Valuation in Europe | Legal Update | Member News

Visualising LandvaluescapeTony Vickers expounds his theories for the benefit of Valuer readers

�����������

������������ �������������

�������������������������� �����������������������

������������� �����������������������

����������������������������������������� ���� �������

� !��������"���#���#�#� �� ���!�"�������

������ !��������������� ���#�$%&������

$��������������������������#�$%&�����������'�$�&������

$������������������������� ������(�'�$�&������������)�*%&������

+���%�������%�$���������*���$,---.���*.��/.�0��������,�����!�(���(�!

+�����������1��������$���$������������,�����!�(���(�!

+���21�&�$���������$���$������������,���(���������

---.���*.��/.�0

�

Contents

cove

r im

age:

©iS

tock

phot

o.co

m/p

hoto

cana

l25

“

. . . a link between mapping land values and taxation

was established in my mind when I started

serious academic research

Editorial 04

VOA News 04

From the Trenches 05

RICS Rating Diploma Holders 07

Business Rates 11

Valuation in Europe 13

VOA Focus 16

Visualising Landvaluescape 17

Compulsory Purchase 20

Member News 24

Legal Update 24

Rating in Ireland 25

VTS Update 28

President Fisher s̓ Findings 29

Flotsam 30

IRRV VALUER

Managing Editor John Roberts

Designer Jamie Sowler

Publisher IRRV Publications

IRRV

Chief Executive David Magor, OBE

IRRV 41 Doughty Street

London WC1N 2LF

T 020 7831 3505

W www.irrv.net

EnquiriesMembership 020 7691 8980

Conferences 020 7691 8987

Subscriptions 020 7691 8980

Publications 020 7691 8975

Advertising IRRV Kate Hodder

T 020 7691 8996

EditorialJohn Roberts

T 07952 659 258

IRRV Valuer is produced by IRRV Publications

on behalf of the IRRV. Unless otherwise

indicated, copyright in this publication

belongs to the IRRV.

March 2010 ISSN 1361-1305

© IRRV 2010. Reproduction in whole or in part of any

article is prohibited without prior written consent. The

views expressed in this magazine do not necessarily

represent the views of the Institute. While all due care

is taken regarding the accuracy of information, no

responsibility can be accepted for errors. Any advice

given does not constitute a legal opinion.

IRRV Council: IRRV President Geoff Fisher FRICS (Dip

Rating) IRRV (Hons) REV; Senior Vice-President Kerry

Macdermott IRRV (Hons); Junior Vice-President Roger

Messenger BSc (Est Man) FRICS IRRV (Hons) MCIArb REV;

Phil Adlard Tech IRRV MInstLM MCMI; Alan Bronte FRICS

IRRV (Hons); David Chapman IRRV (Hons); Tracy Crowe

CPFA IRRV (Hons); Barbara Culverhouse IRRV (Hons)

CPFA; Carol Cutler IRRV (Hons); Tom Dixon RD BSc (Est

Man) FRICS IRRV (Hons); Pat Doherty CPFA IRRV (Hons);

Ian Ferguson IRRV (Hons); Richard Guy FRICS (Dip Rating)

IRRV (Hons) MCIArb; Richard Harbord MPhil CPFA FCCA

IRRV (Hons) FIDP FBIM FRSA; Mary Hardman IRRV (Hons)

FRICS MCMI; Gordon Heath BSc IRRV (Hons); Julie

Holden IRRV (Hons) MCMI CMg; Caroline Hopkins IRRV

(Hons); Brian Jeffrey IRRV (Hons); Graham Ryall FRICS

IRRV (Hons); Kevin Stewart IRRV (Hons) MAAT MCMI;

Angela Storey Tech IRRV MCMI; Bob Trahern IRRV (Hons);

Julie Trahern IRRV (Hons); Allan Traynor FCCA IRRV (Hons)

VALUER | March 2010 | www.irrv.net

David Magor

4 | Editorial/VOA news

Promoting

the European Valuation Standards

The Institute is leading a project to invest

resources in the preparation of detailed

guidance notes and information papers to

support European Valuation Standards and

to encourage best practice in valuation.

Within the sector, the publication of the

European Valuation Standards, the “Blue

Book”, has made a huge contribution to

European standards in valuation.

The specific objectives of the project are

to improve professional standards within

the sector, and to improve the general skill

levels of all people working in the valuation

profession across Europe. In the longer term,

it is envisaged that the project will result in

increased mobility of valuer professionals, so

that, subject to meeting local requirements,

people working in one Member State will be

able to offer advice and services in relation

to, and even in, another Member State

without hindrance.

The partnership as a whole is a

combination of:

• IRRV, a professional members’

association with educational

excellence;

• SNPI, a French trade association

which is a leader in its field;

• TEGoVA, the umbrella organisation

for European valuers’ associations;

• Polish Federation of Valuers

Association (PFVA);

• ANEVAR, the Romanian Valuers’

Association, and

• Registru Centras, The Lithuanian State

Register of Property.

As the project develops, more detail will

be published in this magazine and directly

to members of the partner organisations,

with the sole aim of enhancing the valuation

profession in Europe. █

David Magor OBE IRRV (Hons) is Institute Chief Executive

VOANEWS

New Year honour

Stephen Wright, the VOA’s Head of Business

Improvement and Support, has been awarded an OBE in the

2010 New Year Honours list.

Stephen joined the Valuation Office in 1968 as a clerical

assistant in Hereford. He learned the business from ‘the

shop floor’, soon becoming the Staff Officer in St Helens

before moving to Liverpool as the area’s first Regional Staff

Officer, responsible for operational issues across North West

England. He moved across the Pennines in 1985 to become

Regional Senior Executive Officer responsible for ensuring

the delivery of targets in the Yorkshire Region. Since 1990,

he has been based in the Chief Executive’s Office in London.

London Rent Maps launchedThe Mayor of London has launched the ‘London

Rent Maps’ website that uses information supplied by

the VOA (http://www.london.gov.uk/rents/).

The site shows median rents for privately rented

homes, and is designed to allow people living and working

in London to compare average rent levels. It is based

on information of passing rents collected from agents,

landlords and tenants by VOA Rent Officers for their

statutory roles in Housing Benefit and Fair Rents.

Tim Eden, Director of Council Tax and Housing

Allowances said, “I hope this initiative will lead to a better

understanding of the Private Rented Sector in London and

an even wider interest in contributing information to the

VOA’s Rent Officers. London has a diverse, complex and ever

changing market. Each and every example of a letting helps

to build a representative picture.”

Council tax scam

The VOA has been raising awareness of a council tax

scam targeting homeowners, through the local press.

Many households across the country have received

calls from crooks claiming to be VOA or council officials and

telling their victims that they are eligible for thousands of

pounds in council tax rebate. They are then asked for their

credit card or bank account details so the money can be

refunded. Others are asked for a one-off administration fee

to process the refund.

The VOA never asks for bank account information, and

is advising concerned customers to inform their local police

and their bank if they have given the scammers any details.

VOA News

is brought to

you by the

Agency’s

Communications

Team

www.irrv.net | March 2010 | VALUER

©iS

tock

phot

o.co

m/l

oops

7

VALUER | March 2010 | www.irrv.net

From the trenches | 5

The 2010 rating revaluation is likely

to prove the most controversial since

quinquennial re-assessment was re-

introduced in 1990. Although all four

revaluations since that date, and more

particularly their antecedent valuation

dates (AVD), have managed to catch

the peaks and troughs of the economic

cycle and the property market, the 2010

revaluation, with its antecedent valuation

date on the cusp of the economic collapse,

will inevitably brook major dissention.

The time line around April 2008

could not be more critical, with the

nationalisation of Northern Rock and

the first indications of the crumbling of

the finance industry having appeared in

the previous September, but the major

meltdown around Lehman Brothers and

the British clearing banks, Woolworths, MFI

and demolition of the bank rate was still

some months away. Inevitably, this means,

particularly in the peak aspects of the

2010 List for the retail industry and Central

London, that rental values when the List

comes into force may be significantly lower

than they were at the antecedent 1st April

2008. Of course, under s.19 of the General

Rate Act 1967, the assessment was the

lesser of the current rental value or the

tone of the list – those were the days!

Although the overall revaluation

outturn did not bring any major surprises,

it has certainly underlined some of the

dichotomies in the system. In terms of

re-distribution of value, the increases

in rents in supermarkets and Central

London, notably offices, have been

properly reflected, but the polarity

between the increases in these sectors

and the reductions elsewhere are perhaps

greater than have occurred in previous

revaluations. There is slight surprise

that the other geographical location for

increase is the South West region, but

this may only confirm the suspicion held

by some rating surveyors that the 2005

revaluation in that region was ‘under

done’. The polarisation of values also

means that the re-introduced transitional

scheme will have significant and longer

lasting effects. Quite how the government

intend to ‘sell’ the concept of London

ratepayers being subsidised by the rest

of the country through the withholding

of rates reductions, has yet to be seen.

There may be some grudging sympathy

because the 2p business rate supplement

to fund Crossrail only applies to the

Greater London area, and is not subject

to transitional relief. As a result, many

rates bills in the Greater London area will

increase in 2010 by far more than the

maximum 12.5% limit in the transitional

scheme – in the case of Central

London, premises in many cases by more

than double that percentage. The full

implications of this situation are unlikely to

hit ratepayers until they receive their new

rates bills.

Other likely conflicts in the 2010

Rating List revolve around the different

methods of valuation. One of these is the

contractors method, which has resulted

across the country in significant increases

of around 40% in rateable values, and

sometimes more, arising from the increase

in construction costs between 2003 and

2008. This raises the whole argument

of cost versus value in calculating

assessments, because outside London

and the South West other assessments

are likely to have fallen, and the Valuation

Office Agency (VOA) do not appear to have

adjusted the amortisation calculations to

reflect the reality of the property market at

the antecedent valuation date. There is a

further argument that the stage five ‘stand

back and look’ part of the calculation can

be applied to allow for a looking forward

at the antecedent valuation date at

anticipated future economic conditions,

being in the mind of the hypothetical

landlord and tenant on the day on which

the bargain is struck at 1st April 2008.

In that instance, it is readily arguable

that there would be some anticipation

of the future economic downturn,

and a consequential reduction of the

hypothetical rental bid.

Anticipation of economic events may

also be an issue in terms of the bulk class

properties valued on the rentals method.

Both contractors test and receipts and

expenditure valuations incorporate the

ability to look forward, but rental values

From the trenchesTom Dixon puts his own slant on preparations for the 2010 Revaluation

©iS

tock

phot

o.co

m/b

onat

hos

©iS

tock

phot

o.co

m/A

-Dig

it

©iS

tock

phot

o.co

m/d

anle

ap

©iS

tock

phot

o.co

m/p

akag

alla

rdo

www.irrv.net | March 2010 | VALUER

6 | From the trenches

adopted by the VOA are those on or

about 1st April 2008 (at least in an ideal

world). However, as these are rents for new

lettings as opposed to rent reviews, it is

likely that terms would have been agreed

several months prior to the lease being

signed and the rent coming into effect, so

it is arguable that a downward adjustment

should be applied to take account of the

rent which the landlord and tenant might

negotiate on the actual AVD. Whilst it is

already established that rents after the

AVD can be used as evidence to establish

a trend, the ‘catch 22’ situation is that due

to the economic circumstances there was

little or no rental market activity after the

April date.

In practical terms, this would be a

difficult case to argue, and it may also be

difficult to justify in terms of cost, because

given the greater impact of transition

for the 2010 revaluation, adjustments of

assessments when the List comes into

effect on 1st April 2010 will have restricted

financial effect.

Another contentious issue which is

now coming to a head following the recent

Lands Tribunal decision, in Sport England v Allan, where the President decided that

grant should not be taken into account in

calculating assessments by the contractors

method, is the taxing of many ‘not for

profit organisations’, whose assessments

are often calculated on this basis, and are

already facing disproportionate increases

in liability. Whatever the technical merits of

the Lands Tribunal decision, and they are

undoubtedly cogent, it must remain wholly

illogical for public money, such as lottery

funding, which is paid out to provide

facilities which a market economy would

not otherwise provide, to then be taxed at

a significant rate. Undoubtedly, the

completion of the Olympic developments

and the potential impact of rates liability

on the ODA funding will call this whole

issue further into question.

Last, but by no means least, there

are now major difficulties facing

ratepayers who wish to contest their new

assessments. The Valuation Tribunals in

England, which up to now have provided

a cost effective and acceptable facility for

ratepayers to challenge their assessments,

have been thrown into disarray by ill-

considered government intervention. A

new organisation, the Valuation Tribunal

for England, was produced somewhat like a

rabbit out of a hat on the 1st October 2009,

as a hopelessly flawed attempt to

shoehorn this highly specialised form for

valuation resolution into a ‘one size fits all’

social tribunal framework. It has quickly

become apparent that an almost total

lack of consultation by the government

and its agencies, which seem to have

little or no knowledge of the workings of

this particular and essential jurisdiction,

have resulted in regulations which are

now having to be revised, and practice

statements which are having to be

scrapped and re-written. In the meantime,

there is total confusion amongst all

parties concerned, including the Tribunal

themselves, as to how proposals against

entries in the Rating List should proceed.

Certainly, the considerably increased

complexity of the proposed procedures

can only result in increased costs to

ratepayers for a service which should be

available without financial inhibition.

However, on a more positive note, the

programming scheme for proposals to

alter the rating list served on the VOA,

which had fallen into such disrepute during

the 2005 List, due to its overzealous use by

the Agency to achieve internally imposed

clearance targets, is now the subject of

constructive discussion between the

interested parties, which will hopefully

produce a rational scheme to manage

proposals arising from the publication of

the Rating List on 1st April 2010.

Watch this space! █

Tom Dixon RD BSc (Est Man) FRICS IRRV (Hons) is an IRRV Past President, Council member and a senior partner with Sanderson Weatherall.

Last, but by no means least, there are now major difficulties facing ratepayers who wish to contest their new assessments.

““

There is slight surprise that the other geographical location for increase

is the South West region.

““

©iS

tock

phot

o.co

m/b

onat

hos

©iS

tock

phot

o.co

m/A

-Dig

it

©iS

tock

phot

o.co

m/d

anle

ap

©iS

tock

phot

o.co

m/p

akag

alla

rdo

The Tenant’s Share

In my first article, published in the December edition of Valuer, I explained something of the background to the receipts and

expenditure (R&E) method, used for the valuation of large utility

properties for rating purposes. I looked at what the courts had to

say on the matter of the tenant’s share before looking in more detail

at the first two of the four methods of how the “tenant’s share” has

normally been calculated by rating surveyors. These were:

1. Tenant’s Share as a percentage of gross receipts;

2. Tenant’s Share as a percentage of the divisible balance.

In this second article, I propose to look at the remaining two

methods in more detail:

3. “Spot figure” approachThe third method is to use the “spot figure” or intuitive method

of arriving at the “tenant’s share”. Included in this method is the

very common approach of splitting the divisible balance 50/50. This

is a common approach used for leisure properties. This approach

was adopted in the Bluebell Railway case, and one of the valuations

in Garton v Hunter, the holiday camp case, adopted the 50% of the

divisible balance approach. This default tenant’s share percentage

reflects the serious difficulty in estimating the value of the tenant’s

assets in circumstances where the tenant does not know how much

profit he will earn before the rent is fixed. In an amusement and

theme park valuation, for example, what part of a roller-coaster ride

is rateable, and even if you knew, what is its market value? What is

the market value of a couple of old elephants and a lion deemed to

be owned by the tenant in a zoo? Where would you go to get these

values for an R&E valuation?

4. Tenant’s share as a return on the market value of the tenant’s assets

This appears to be a straightforward exercise, and under perfect

conditions this is correct. However there are two significant

problems. The first one is to find the “market value” of the tenant’s

assets, and the second one is to find the percentage to be adopted.

i) Market value of tenant’s assetsThe market value of any asset is the present value of the right

to receive a future income. But this concept has to be applied to

the rating hypothesis. It seems to me that in the case of a tenanted

property, the right to receive a future income can be significantly

affected by the amount of rent that a tenant has to pay.

Take the example of a property where the business can produce

a profit of £2m before the payment of rent. If the rent paid by the

tenant was only £100, then he would have an income of just under

£2m. If however the rent was £1m, he would only have an income of

£1m. A tenant thinking of buying the assets needed in the business

would pay a lot more for them if they could earn him nearly £2

million per year than he would if they could only earn him £1m per

year.

This is unfortunately what rating valuers try to do in an R&E

valuation. They try to work out the rent of a property and make

various illogical assumptions regarding the value of the tenant’s

assets. The value of the assets depends on the future income earned

by the assets, but you cannot know that until the rent which a

The tenant’s share (part two)

Pat Brennan concludes his critical examination of ‘tenant’s share’, as he takes readers through this key aspect of valuation from the perspective of the rating valuer

RICS Rating Diploma Holders | 7

VALUER | March 2010 | www.irrv.net

The Tenant’s S

hare

tenant has to pay is known. It is all very circular and illogical.

Rating valuers sometimes get round this difficulty of finding the

market value of the assets required in rating valuations by starting

with the assumption that “cost equals market value”. Despite the

fact that it is unusual to find that “cost does not equal market value”,

particularly of assets which are a number of years old, rating valuers

generally adhere to this assumption both in their contractor’s

basis valuations, and to arrive at the value of the tenant’s assets

in their R&E valuation that cost equals value. They start with the

modern replacement cost, and adopt the mainly age-related

formulaic adjustments to arrive at what rating valuers think may

be their “market values”. Since the Monsanto Lands Tribunal case

(1998) RA 217 decision, the Lands Tribunal determined scales have

been adopted to adjust the replacement cost of items of plant and

machinery. These scales however do not seem to produce what

a normal businessman would regard as market values of items of

plant and machinery. According to the scales, the market value of an

eight year old piece of plant and machinery is the same as the value

of the item brand new. After the item plant gets to 30 years old, its

market value is 50% of its new replacement cost, but after that age

its market value stays the same.

If the “market values” of plant and machinery assets are

their replacement cost less Monsanto scale allowances for the

contractor’s basis valuations, the “market value” of the tenant’s

assets in an R&E valuation should be calculated in the same manner.

This is especially relevant for Class 1 electricity generation assets.

In a normal hereditament, the turbines and generators which

produce electricity to be consumed at the hereditament is rateable

under Class 1. In an electricity generating hereditament which

sells electricity and does not use it on the hereditament, the same

generator and turbine items are not rateable, and they will be

treated as “tenant’s assets” in an R&E valuation. Rather surprisingly,

the value of the tenant’s assets in some current R&E valuations

of electricity hereditaments in England and Wales have been

calculated not using the Monsanto scales allowances, but rather

using ‘straight line’ depreciation, thus producing lower amounts of

tenant’s capital and higher rateable values.

Another commonly adopted method of calculating the value

of the tenant’s assets is to use their net book value shown in the

company’s accounts. This is an even more unreliable method of

arriving at their market value, which relies on a historical twist

of fate, i.e. what were the prevailing costs when the assets were

acquired. In times when there was a buoyant market the price

would be high, but in times of oversupply the cost would be lower.

It also assumes that the company’s assets have not increased at all

and have gone down in value in line with their straight line book

depreciation methodology. None of these assumptions seem

logical.

A number of sales of utility properties have been analysed to

see whether the purchase price of the company is equal to the net

book value or regulatory asset value of its assets. In all cases this

has never been found to be the case. Apart from the electricity

power stations which sold at deep discounts to their asset values

around 2003, most utility companies’ properties have sold at prices

in excess of the net book value, adjusted appropriately for the

company debt.

(ii) Rate to be applied to the uncertain market value of these assets.

Rating surveyors have carried out the task of determining the

percentage to be applied to the value of the tenant’s capital since

at least 1926. However in 1994, parties to the appeal on China Light and Power v Commissioner of Rating and Valuation (Hong Kong) (1994) 1996 RA 475, an electricity property in Hong Kong, decided

that a rate to be applied to the value of the tenant’s assets was the

company’s WACC (Weighted Average Cost of Capital). Essentially

8 | RICS Rating Diploma Holders

www.irrv.net | March 2010 | VALUER

The Tenant’s Share

WACC is a fairly straightforward concept. If half the assets are

bought using borrowed money at a 5% interest rate and the rest of

the money to fund the purchase is funded by equity where a return

of 15% is obtained, the WACC of the company is 10%. The WACC

calculation is the province of economists. They make the simple

concept much more complicated, and spend hours talking about

betas, long term or short term risk free rates of return, equity risk

premiums, pre- or post-tax, cost of debt and financial gearing, real

or nominal. The problem is that WACC has nothing to do with the

return a tenant should receive on the value of his assets to arrive at

the “tenant’s share”.

The “tenant’s share” is not just a return for investing in the

business. The “tenant’s share” is to reward “a person embarking

upon a commercial undertaking in which he is to sink his capital, in

which he takes all the risks of success or failure, and in which he has

not merely to be compensated by receiving a reasonable interest

upon the capital invested, but also to receive such a profit upon

his venture as reasonably to compensate him for the risk which it

involves and to induce him to embark upon its prosecution”.

The conventional WACC is the return investors expect for

interest on the capital they have invested, and a reward for the

risk they have taken in investing in the business. The “tenant’s

share” is also meant to reward the hypothetical tenant for another

aspect – namely “remuneration for his industry”. If that reward is not

included in the “tenant’s share” there is no incentive for the tenant

to strive to maximize profits or minimize losses, or even to take on

the tenancy of the property.

If all a tenant earns from running a business is a return

equivalent to his WACC, he will never have any spare capital to

improve or expand his business. This is an aim that all operators

of businesses will strive for, so unless he perceives that his “profit”

will be more than his WACC, he will not take on the tenancy of the

property.

There is another reason why adopting a company’s WACC is not

the appropriate percentage to apply to the value of the tenant’s

assets in an R&E valuation. Companies’ WACC are derived from an

analysis of their accounts, profits and share price. The actual WACC

is always of a company which does not have the same risk profile

as the hypothetical tenant. It is generally of an owner occupied

business. Sometimes it relates to a business operating from many

locations, not just at the property being valued. The risk profile of a

tenant of a property carrying out a business where he is deemed

to take all the risks of running the business, and pays a

predetermined

rent to occupy

the property, is

significantly

different from the

risk profile of an

owner occupier of

the same property

where he does not have a predetermined rent payable as a debt

before the tenant can take any profit. The differing risk profile

means that the WACC of the owner occupier must be different from

the hypothetical tenant.

It is not known why the VOA is so wedded to using a very low

WACC percentage of 8% or 9% for their 2005 list valuations when

the VOA adopted at least 30% more than BT’s WACC of 9.9% in 1995

when it settled the assessment of British Telecom at about 13.6%.

So if WACC is not the correct percentage to adopt when

calculating the “tenant’s share”, what should the percentage be?

Using the normal approach adopted by valuers when

justifying their valuation, the use of comparables, it is appropriate

to look at what happened in previous cases, and after analysis apply

the result to the property being valued. The courts have found the

following percentages appropriate:

What is the market value of a couple of old elephants and a lion deemed to be owned by the tenant in a zoo?

RICS Rating Diploma Holders | 9

VALUER | March 2010 | www.irrv.net

““

The Tenant’s S

hare

www.irrv.net | March 2010 | VALUER

Cairngorm Chairlift 18.0%

China Light and Power 25.0%

British Telecom 13.6%

Southern Railway (H of L) 15.0%

Brighton Marine Palace and Pier 15.0%

The one percentage that seems to be completely out of line

with previous cases is the VOA’s 2005 List percentage of 8% or 9%.

Leaving aside the 25% in the China Light and Power case in Hong

Kong, the percentage which seems appropriate is approximately

15%. This provides the tenant with a return which includes interest

on his capital invested, a reward for his risk (these two elements

comprise the normal WACC percentage) but also an additional

percentage to reward him for his enterprise, skill and remuneration

for industry.

(iii) Two stage calculation of the tenant’s share percentageTo ensure that all aspects of the tenant’s share have been fully

reflected, some valuers have approached the tenant’s share in two

stages. Firstly, the tenant is given a specific amount to provide

him with interest on the capital he has invested in the business.

The second stage is to provide him with a reward to reflect the risk

he takes operating the business from the property and his profit

for running the business. The second stage of the calculation is

sometimes related not to the value of the tenant’s assets, but rather

the turnover of the business or the amount of the divisible balance.

In Strand Hotels Ltd v Hampshire (VO) 1977 RA 265 this approach was

taken by the Lands Tribunal. The tenant was firstly awarded an

8% return on the value of his assets, and was given as his “share”

40% of the ‘divisible balance’ for his profit and risk. This two stage

calculation was also adopted in the Cross Harbour Tunnel (1978)

case in Hong Kong, where the tenant’s share was calculated giving

him an interest return of 8% on the value of his assets and a further

amount of 11% of the gross receipts. In the Cairngorm chairlift

case the two stage approach was also adopted. Again the tenant

was given an interest return of 8% on the value of his assets and a

further 10% for his risk and for operating the business.

ConclusionWhatever method is used to calculate the tenant’s share, the

important matter which valuers need to consider is that they are

tasked with finding the rental value of the property under

statutory rating

hypothesis. While

economists and

accountants can

inform Tribunals on

interest rates and

asset values used

in the “real world”

for accountancy

and investment

purposes, it is the job of rating valuers to determine the matters

which influence the parties to the “hypothetical” rental negotiations

assumed to have taken place to arrive at a rateable value. Most

of the utility properties in the UK were returned to conventional

assessment in the 2005 List. Their values are very significant, and

their assessments have generally been arrived at using the R&E

valuation method. It seems very likely that the Lands Tribunal will be

asked to consider some valuations in detail, and no doubt valuers

will put forward their views on how the tenant’s share should be

calculated at these hearings. Only after the Lands Tribunal have

given reasoned decisions on the tenant’s share element in R&E

valuations is there likely to be more of a consensus among rating

valuers on the correct approach to the calculation of the tenant’s

share. █

Pat Brennan FRICS Dip Rating is a consultant to Ruddle Merz Limited.

. . . the important matter which valuers need to consider is that they are tasked with finding the

rental value of the property under statutory rating hypothesis.

10 | RICS Rating Diploma Holders

““

themselves in the knowledge that their the knowledg

views informed the decision.he decision.

The English transitional scheme, sitional schem

ore inflation, limits ratebefore ate rises in

12.5% for hereditame2010 to 12 ments with

a rateable value of £18,000 or moa rateable va more,

and 5% for smaller hereditaments. Td 5% for sma s. This

is paid for by limiting reductions to d for by limitin

4.6% for large hereditaments and 20%large heredita

for small hereditaments. However, in reditaments. H

the first of various twists, an inflationous twists, an

factor has to be applied, and the RPI at plied, and thefa

eptember showed an annual reduction n annual reduSept

4% which makes the scheme morescheme moreof 1.4%

sgenerous.

face of it, taking inflatioation intoOn the fac

account, rate rises in 2010 will be limimitedount, rate rise

to 10.925% for large hereditaments25% for large

and 3.53% for small hereditaments. % for small her

Reductions will be limited to 5.9356% for will be limited

large hereditaments and 21.12% for small ents and 21.12

hereditaments. However, once again, thiswever, once aghe

ot quite the case because transition is ecause transitiis not

on the small business multiplier, and ss multiplier, abased on

so the 0.7p to pay for small business relief usiness relief so the 0.7p t

is outside transition. Also in Londodon, whereoutside trans

they apply, the 2p supplement for CroCrossrailapply, the 2p s

and the 0.4p premium in the City of Londndon 0.4p premium

are outside tratransition.

Worse still for some ratepayers will for some rate

be a reduction in small business relief, or asmall businesb

omplete loss of either small business relief er small busincom

ral rate relief. Like all changes to rate ll changes to ror rural

ese are not phased in by transition. in by transitiorelief, these

Although all reliefs have had the vhe variousAlthough all re

thresholds increased, this only worksorks if the esholds increas

rateable value increase at the revaluatiation is le value incre

near or below the average. Increases below the ave

in rateable value above theble value abo

national average can result average can r

in substantial losses of ntial losses of

relief.

First,

take the

Business Improvement Districts (BIDs). Business Improvement Districts (BIDs).

Does anyone recall that in 1989 we oes anyone recall that in 1989 we

were looking forward to the Uniformlooking forward to the Unifo

Business Rate? Will anyone still usingsiness Rate? Will anyone still using

this term, kindly desist immediatelythis term, kindly desist immediately!

In Scotland, they have decidedd, they hav

to match the English multipliers,to match the English m

and have already set theirs at 40.7pand have already set their

and 41.4p respectively, which is and 41.4p respectively, which

an interesting interpretation of nteresting interpretation of

devolution. Presumably, the same ution. Presumably, the same

multipliers are required so that Scottishultipliers are required so that Scotti

ratepayers have a level playing fieldratepayers have a level playing field

with their English competitors. Goodwith their English compe

heavens, if this idea catches on we could heavens, if this idea catches on we could

have uniform business taxes acrosshave uniform business tax

Europe! Where are the people who think urope! Where are the people who thi

that we should have lower taxes and a we should have lower taxes and

devalued pound in order to give Britain aued pound in order to give Bri

competitive advantage?mpetitive adv

In Wales, they have a singleIn Wales, they have a sin

provisional multiplier of 40.9p. It seemsprovisional multiplier of 4

that the Welsh Assembly Government justthat the Welsh Assembly Government justtt

don’t understand that rates are supposeddon’t understand that rates are supposed

to be complicated! There is still only onee complicated! There is still only on

BID in Wales, and I have detected little Wales, and I have detected lit

enthusiasm for adopting the provisions forusiasm for adopting the provisio r

a Business Rate Supplement. Consultation Business Rate Supplement. Consultatio

was held in England over the summer for awas held in England over the summer for aaa

new transition scheme for the 2010 rating new transition scheme for the 2010 rating

list. The choices revolved around four or list. The choices revolved around four or

five years and having transitional reliefve years and having transitional relief

as before, either paid for by transitionalfore, either paid for by transitiona

surcharge or a supplement on the multipliege or a supplement on the m err.

The government stated its preferred optionovernment stated its preferred op nn

was five years, with transitional relief paidas five years, with transitional relief paid

for by transitional surcharge, as in previousfor by transitional surcharge, as in previous

chemes. Guess what - that’s what the schemes. Guess what - th

government chose. Everyone, myself government chose. Everyone, myself

included, who thought that aincluded, who thought th

supplement on the multipliersupplement on the multiplier

would share the burden would share the burden

more fairly, can more fairly, can

consolecon

The revaluation has resultedas result

in new rating lists in England, gland

Scotland and Wales with overalld a

increases in value but a crop of ases in v

gainers and losers from the changes.and

After the resulting reductions in thections

multipliers and increases in the relief es in the

thresholds, there are still substantialsubs

gainers and losers. Ironically, ins and lo

England with its sophisticatednd with i

transition scheme, there will still ben sch

some surprisingly large changes in change

rate bills to individual ratepayers.tepayers

At the time of writing, we are we a

still waiting for the proposed rate ting for

multipliers for England to be confirmeders for E d

at 40.7p for properties that benefitor pr

from small business relief and 41.4p for and 41

everything else. Well almost, because ost, beca

in London, it is anticipated that Boris that

Johnson and the GLA will set a business nd t

rate supplement of 2p to pay for Crossraiplement il.

That would effectively increase the d effe

multiplier to 43.4p for all properties in roperti

the Greater London area that are above ahat are a

rateable value of £50,000. Of course, by the cou he

time that you read this, if a snap Generalyou rea

Election has taken place, then whateveras taken

the result, an incoming government couldn inc m d

be planning an emergency budget in budget

which Crossrail is delayed again, or even w gain, or

abandoned, despite the works already e s alre

taking place.

So that’s three multipliers then? No, no’s three ot t

quite because the City of London sets its owe the n wnwnwn

multipliers and if it follows the form of recene form nntntnt

years in setting a premium of 0.4p, there ye f 0.4p, th

would be three more multipliers of 41.1p,e iers

41.8p and 43.8p applying in the Citynd 43.8

of London only. Then there areondon o

some ratepayers in various me ra ri

parts of the countryntry

who are also

paying for

Business rates | 11

VALUER | March 2010 | www.irrv.net

Business ratesAs the business rate revaluation lies just around the corner, Gordon Heath explores the knotty problem of transition and the new list

©iS

tock

phot

o.co

m/m

ikem

cd

12 | Business rates

After the resulting reductions in the multipliers and increases

in the relief thresholds, there are still substantial gainers and losers.

““

It seems that the Welsh Assembly Government just donʼt

understand that rates are supposed to be complicated!

““

©iS

tock

phot

o.co

m/m

ikem

cd

anticipated 3.53%53%.

This is not the most extreme casee most extrem

possible. A rateable value increase that pos value increase

es a property out of rural rate relief takes a rural rate relie

only be a little above the national might onl e the national

average rateable value increase, average ratea se, but the

bill will more than double. This coul will more th ould

also apply to some of the larger increaspply to some o eases

on properties currently receiving small erties currently

business reliefef.

By way of balance, I could set outalance, I could

examples where a rateable value fall at therateable valueex

valuation might reduce the ratepayer’s uce the ratepareval

y over 50%, by combinibining the bill by ov

f transition and rate rerelief. The effects of t

big questions are how many ratepaepayers ig questions a

will be facing large increases and whawhatbe facing large

sectors or areas are affected? The or areas are a

government line is that it is a comparativelyelynt line is that i

small number of ratepayers overall. Myof ratepayers

discussions with various people around the various people

ountry suggest that small pubs and smallt small pubs ancou

ol stations are two types of propertytypes of propepetrol s

be facing large increareases.likely to be

nal thought is that, however bad a however bad aOne final

“comparatively small” number of ratratepayer mparatively s

facing increases of up to just over 100%0% might increases of u

be, it is nowhere near the outrageous 44,904,900%owhere near th

and 22,400% increases that were allegedly% increases tha

claimed on 10 January 2010 by an over-exciteddanuary 2010 by

Liberal-Democrat intern in a press releasentern in a presLib

ce rapidly withdrawn). It seems thatwn). It seems th(since

ver cuts the incoming government mustng governmenwhatever

make, we need more expenditure on educationiture on educmake, we nee

in mathematics! mathematics █

Gordon Heath BSc IRRV (Hons) is anandon Heath BScindependent revenues consultant. Thedent revenues

views expressed here are purely pressed here apersonal.

Gordon on can be contacted at at gordon.

surcharge of £9,069.47 above e 9 e

the £41,400 that they would pay 400 ld p

without transition. This equates tran uate

to a reduction of 5.4%, except in ct p

London where the Business Rate Lon e Bu

Supplement for Crossrail is likely to Sup rossr

add £2,000 to the bill, reducing theird bil

gain to only 1.65%.nly

However, I think that most large ever, most l

ratepayers will accept the transitions w an

scheme – it is the small ratepayers che ma

where there will be major problems. wher e ma

For most small hereditaments where or m dit

no rate reliefs apply, the increases ef ea

will be close to 4% and the reductions se to educ

around 20%, but changes to relief can %, b rel

have dramatic effects.ve s.

Take the example of a property witTa ple of ith

small business relief and a rateable value mall f and ue

of £4,500 in the 2005 list and £9,000 in th 9

the 2010 listt.

In 2010/11, the full bill would be:the f be:

£9,000 x 41.4p = £3,7260 6

Using the small multiplier:ing t iplie

Notional Chargeable amount = £9,000 x otion amo x

40.7p = £3,663p

In 2009/10, with 50% small business relief, with sine

the bill would have been:ld ha

(£4,500 x 48.1p)/2 = £1,082.25p)

Using the small multiplier:g t plier

Base liability BL = £4,500 x 48.1p = £2,164.50e liab 500 x 64.5000

Appropriate Fraction AF = 1.0353op F =

The transitional limit = BL x AF = £2,240.91al = £

Transitional relief = £3,663 - £2,240.91 = elief 240.

£1,422.09

The small business relief is now only 25% andma f is andd

therefore:efore

Amount payable = £2,240.91/1.333 = oun ,24

£1,681.10

Hence, the amount payableence, paya

has increased by a massive incr ssiv

55.33%, compared m

with the headlinee he

5% or the or th

example of a property with a xa p of pr e w h a

rateable value of £65,000 in theat bl al o 65 00 n t

2005 list and £100,000 in the 2010 00 is n 10 00 in e 10

list.st.

In 2010/11, the full bill would be:2 0/ t fu bi wo d

£100,000 x 41.4p = £41,4000 00 4 4p £4 40

Using the small multiplier, asin th m m lti e s

required in transition:qu ed t si n

Notional Chargeable amount = oti a ha ea e mo t

£100,000 x 40.7p = £40,70000 00 40 p £4 70

In 2009/10, the bill would have been:20 9/1 th bi wo d ve ee

£65,000 x 48.5p = £31,52£ 5,0 0 x 8. = 31 5

Using the small multiplieU ng he ma m ip r:

Base liability BL = £65,000 x 48.1p = B e bi y B = 5, 0 8 =

£31,265£ ,2

Appropriate Fraction AF = 1.10925A pro ria F ti A = 09

The transitional limit = BL x AF =T tr si n im = x F =

34,680.70£ 6 70

Transitional relief = £40,700 - £34,680.70Tr si n e f = 40 00 £3 68 70

= £6,019.30= ,0 3

Supplement for small business relief =Su ple e fo m b n r ef

£100,000 x 0.7p = £700£1 ,0 x 7p £ 0

Amount payable = £34,680.70 + £700 =Am un pa b = 4,6 0. + 00

£35,380.703 8 0

Hence, the amount payable hase e, e o t ya e h s

increased by 12.23%, not the headline nc as b 2 % o he ea ne

12.5% or the anticipated 10.925%. 2. o he nt pa d .9 %

However, as it is close to the headlineow ve as is os o e h ad e

12.5%, it is probably not going to worry th2.5 , i p ba y t g n o or the

ratepayer too much. Unless of course, it is te y to m h. nle o ou e, s inn

London, where there will be a Business Ratn n he t re ll a us es atte

Supplement which is likely to be £100,000 xp em nt hi is el o £ 0, 0 x

2p = £2,000 which in this example increase= 2,0 0 w ic n s am le cr seess

the bill to £37,380.70. This is an increase ofe b to 37 80 0. is an nc as f

18.57%, which might just worry the ratepay57 , w ic mi t j t w rr he at ayyeer.

Conversely, take the example of aC nv se ta t e m e o

ratepayer benefiting from a rateableep ye en fit g f m ra b

value reduction from £110,000 in the va e du o ro £ 0,0 0 i he

old list to £100,000 in the new list. d t t £1 0 in he ew st

The annual bill will only fallT e a nu bi wi n al

from £53,350 in 2009/10 ro £ 35 in 00 10

to £50,469.47 in£ 4 47 n

0010/112 10 ,

which is a wh h i

www.irrv.net | March 2010 | VALUER

Valuation in Europe | 13

VALUER | March 2010 | www.irrv.net

In this first in a series on European valuation issues, my

purpose is to give the big picture and address the key question

– why are there European valuation issues when property is such

a local thing requiring very local knowledge? And if there’s been

some globalisation of real estate investment and valuation, then

surely international standards are what are needed, not European.

Why Europe?

In this article, I’ll explain why, in my view, the European Union

is the new frontier for property investment, how the opening up

of that frontier is going to help us emerge from the crisis, and how

valuation, and very specifically The European Group of Valuers’

Association’s (TEGoVA) European Valuation Standards (EVS) and

Recognised European Valuer (REV) scheme, are a central part of the

whole process.

What’s European about real estate?I know that for many readers of this magazine, it’s not obvious.

Most people take pan-European property investment for granted,

as if it were some kind of automatic fallout from

‘globalisation’. And yet,

current events are making

it clear that, in a world of

sovereign states, where

treaties and ‘open markets’

are here today and gone

tomorrow, nothing is guaranteed, especially concerning the right

to buy land and buildings. Witness, even before the crisis, China’s

crackdown on foreign property investment, about which nobody

can do anything.

The only place cross-border property investment is guaranteed

is the EU, because it’s not a trading bloc, it is a union of European

citizens founded on real political institutions and a real Court of

Justice that guarantee the right for everybody to buy and sell

property wherever they want, without obstacle.

The very meaning of ‘freedom to invest in property’ varies

from night to day depending on whether you’re talking global or

European. Globally, it means, at best, that there’s no law formally

forbidding foreigners from buying local real estate. Beyond that,

there can be any amount of controls, and foreign investors are

often a captive market for all local real estate service providers. In

the EU, freedom to invest means the whole package. Investors can

not only buy wherever they want, they can use their own estate

agents, valuers, architects and contractors, from the investor’s home

country or from anywhere else in the Union. And above all, the EU

means security – these freedoms can never be repealed.

This was not done in a day. It took more than thirty years just to

get free movement of capital, the basic building block of cross-

border property investment.

Then there’s the great penchant of national governments to

obstruct. The European Court of Justice had to build up case law

neutralising governments that paid lip service to the principle of

freedom to buy property, but kept inventing niggling administrative

requirements for foreigners only. Only the EU can overcome that

kind of bureaucratic interference, and it does.

New entrants to the Union often have land purchase fears. In the

last big accession wave, several candidate member states tried to

retain controls on property investment for ‘transition periods’ of up

to 18 years. The European Property Federation, with which TEGoVA

now works closely, explained to the European Commission that this

would undermine the whole foundation of the EU Internal Market,

mortgage lending in particular, not to mention the damage to local

people deprived of a competitive property market. The Commission

took this point and stood firm.

Recently, there was an attempt to exclude real estate services,

including valuation, from the scope of the Services Directive. That,

too, was defeated, but it shows how resistant local privilege and

captive markets are.

On any market, the health of valuers’ clients, property investors,

Valuation in EuropeRoger Messenger explores the ‘new dawn’ for European Property Markets, putting valuation at the centre of EU real estate policy

. . . the European Union is the new frontier

for property investment.“

“

©iS

tock

phot

o.co

m/L

azar

ev

www.irrv.net | March 2010 | VALUER

14 | Valuation in Europe

The second fundamental impact of the EU on real estate is the fight against climate warming.

““

depends not just on the services investors offer, but on those

they receive. The EU competition authorities have a long tradition

of uncovering and dismantling European cartels of companies

that provide goods and services to building owners. Valuation

services have never been a problem, but contractors and building

component suppliers have, and recently, lift and escalator cartels

were fined a record €992 million, and property companies can seek

damages on top of that.

The new wave of EU regulationThus, free movement of capital, freedom to provide services

and free competition are the bedrock of property investment

across the EU. It took decades to achieve that, but now Europe has

entered a new period of political and economic integration which

is helping property markets and at the same time, supervisory

legislation regulating property fund managers and the

dismantling of the last obstacles to cross-border property

investment are making a substantial contribution in their own

right to a stronger and safer European economy. On top of that, EU

energy and environment policy targeting buildings is opening up

new property investment and valuation opportunity.

Looking first at the EU internal market, if there’s one thing

now obvious to everyone, it’s how dependent real estate is on the

financial system. Imagine what would have happened without the

euro. A number of Eurozone countries could have seen their local

currency collapse, and the local economy and real estate could

have gone down with them. Think what would have happened if

Eurozone leaders hadn’t led in stemming the financial blow-out. We

can now face a future where the economy and the property markets

that emerge from this will be shaped by the European Union and its

priorities – a unified market underpinned by a dynamic, low-carbon

economy.

On this macro level, first, real estate will benefit along with the

rest of the economy from extension of the Eurozone to cover almost

the entire Union, with the power of the euro felt well beyond its

borders.

Second, before this year is out, there will be true European

oversight of the solvency and liquidity of credit institutions. To what

extent this will be done by a centralised European authority alone,

or in collaboration with national regulators, remains to be decided,

and as ever in European integration, there will be trial, error and

gradual improvement, but the political will is now there. In the

current context, it’s hard to overestimate the importance for the

property industry of stronger, safer financial markets.

But equally essential for the whole economy is the safety and

security of the property markets themselves, and crucial to that are

two fundamentals:

1) new EU supervisory rules directly targeting real estate fund

managers and their valuation practices, and

2) removing the final obstacles to cross-border property

investment and mortgage lending.

That’s why TEGoVA is working with the European authorities

on the valuation aspects of the supervisory rules and why TEGoVA,

the European Property Federation (EPF) and their allies are leading

the effort to get EU legislation facilitating cross-border investment

by real estate investment trusts, or REITs, and by open ended real

estate funds.

The second fundamental impact of the EU on real estate is

the fight against climate warming. Buildings are key – 40% of CO2

emissions come from buildings – and the EU, working with us, has

produced a raft of legislation that could make European real estate

the world leader in carbon reduction and in overall environmental

performance. Energy performance renovation and certification

requirements for buildings are being increased, including

renewable energy, and also extended to water performance of the

building. Also, in response to a two-year effort by TEGoVA, EPF and ©iS

tock

phot

o.co

m/L

azar

ev

allies, there will be harmonisation of the certification categories of

commercial buildings so that investors and developers can market

their environmentally cutting edge buildings globally, and valuers

can start integrating the EU energy grades into their reports. The

EU ‘Ecolabel’ is being extended to buildings, EU green public

procurement is prioritising construction, and construction products

will have to be more environmentally friendly to earn the EU CE

mark facilitating cross-border trade. EU flood management rules

are keeping property above water and EU money is repairing the

damage already done, for instance in the UK.

It all means a sea change to planning, construction and

investment culture for half a billion people, a massive challenge and

opportunity for investors and valuers.

TEGoVA at the heart of the processAll these events have placed valuation issues at the centre of

EU policy and TEGoVA at the heart of the legislative process:

• The Energy Performance of Buildings Directive imposes

energy performance certificates (EPCs) for all buildings in

Europe, but it won’t realise its full potential until valuers

actually factor into their valuations the EPC and the grade it

gives the building. TEGoVA is working on that, adapting EVS

and REV accordingly;

• On the Alternative Investment Fund Managers Directive,

TEGoVA is working with the European Commission, the

European Parliament and the Council of Ministers to ensure

independent valuation of real estate assets and valuation

frequencies adapted to real estate;

• In the work on an EU passport for open ended real estate

funds, TEGoVA is working with the Commission on

harmonised rules on frequency of valuation, valuation and

the sale and purchase price, notification of the valuer to

the regulator and minimum professional indemnity

insurance cover for the valuer;

• The European Commission wants to free up the mortgage

credit market so that people can use their own home banks

to buy secondary residences wherever they want – valuation

is crucial here. The Commission’s draft recommendation

suggests that member states promote the use of TEGoVA’s

European Valuation Standards and that member states

should ensure that minimum professional qualifications for

property valuers “such as those set by TEGoVA” exist and are

adhered to within their territory.

But perhaps the most exciting aspect of all this is the extent to

which the success of cross-border property investment depends,

not just on EU law, but on the rules and safeguards set and policed

by the valuation profession itself. That’s because common European

valuation practice is truly market-led. In a cross-border context,

first-time investors on a new and strange property market need

reliable local valuation more than anybody else. They’re more

dependent on valuation than they would be in their home

countries, which is why they need the assurance that their local

valuer works according to the same core European valuation

standards as in the investor’s home country. Just as important,

the investor needs to be sure that the local valuer is qualified to a

recognised high European standard. That’s why TEGoVA’s European

Valuation Standards and its REV scheme have become central to

the whole European cross-border property investment and

valuation process, a cornerstone in a process of political, economic

and business practice integration that could see Europe emerge

from this crisis with the most efficient property market in the

world. █

Roger Messenger BSc FRICS IRRV (Hons) MCIArb REV, Chairman of TEGoVA, is Junior Vice President of the IRRV and Senior Partner with Wilks Head and Eve.

VALUER | March 2010 | www.irrv.net

Valuation in Europe | 15

. . . the investor needs to be sure that the local valuer is qualified to

a recognised high European standard.

““

16 | VOA focus

Philip Evans tackles the valuation of property of mixed age

Many properties change over time. This is particularly true of

large industrial properties that may have evolved over the decades,

with each part having its own character and qualities. It has often

been of concern to valuers how to assess those parts in the context

of the hereditament as a whole. A recent decision in the Lands

Tribunal concerning a rating appeal on a large industrial property

has helped shed light on this potentially troublesome area.

How can valuations reflect the age, constructional and quality

differences in a hereditament?

• Does one value overall, reflecting the age of the majority?

• Does one value each part of different age at different rates?

• Does one then make an end allowance to reflect those

differences?

• How should that be quantified?

Using the first method may fail to take account of the added

value the newer parts bring, whereas valuing using the second

method may value the property as though each part of a different

age is, in effect, a different property and any end adjustment may

be difficult to quantify.

In Allen (VO) v. Freemans PLC the Lands Tribunal preferred

the approach of applying higher values to the more modern

accommodation rather than the overall approach as adopted by

the respondent. The differences between the rates applied were

significant and drawn from the industrial levels in the locality for

that particular age group. This evidence was preferred to that of the

actual rent on the property, which was disregarded by the tribunal

as having no merit as it was, essentially, a surrender and renewal

arrangement.

The property in question is large – a warehouse and premises

of nearly 105,000 metres squared, located in Peterborough and

used for the storage and distribution of catalogue goods. It was

originally built in the 1960s, but extended in the 1980s and

1990s. The 2005 compiled list rateable value (RV) was

£1,770,000, and the Valuation Officer (VO) asked for

£1,760,000 RV at the Valuation Tribunal (VT) hearing,

relying on comparable evidence. Agents for Freemans

asked for £850,000 RV, based upon the rent passing

on the property. The VT decided the assessment

should be £850,000 RV based on that rent. The VO

appealed to the Lands Tribunal and Freemans appeared as

respondents. The Lands Tribunal have now decided that the RV

should be £1,675,000. 76% of the property is of 1960s generation,

and the remainder was composed of 22% 1980s and 2% 1990s.

On the valuation of the mixed age hereditament the

respondent’s valuer adopted values that reflected the age of the

hereditament as a whole, rather than an amalgam of three different

aged buildings/extensions. He stood back and looked at the overall

nature of the hereditament, which he claimed was dominated by

the 1960s warehousing.

In the decision, the tribunal considered there was no

comparable evidence to support the respondent's approach – ''I

do not accept this approach and I prefer Mr Allen's method of

valuation, which places a higher value upon the more modern

Freemans accommodation.'' The VO was able to demonstrate this

approach had been accepted elsewhere.

There was also some difficulty with the use

of evidence

of smaller

standalone

buildings to

value the later

1980s and 1990s

accommodation

forming part of

the hereditament. This was because such comparables reflected

a different market to that of the larger building. However the

Lands Tribunal accepted that it was correct to use such evidence,

providing it was coupled with an appropriate end allowance to

reflect the mixed age characteristics.

In judging the quantum of the end allowance, which

covered not only mixed age but a cramped site and a piecemeal

development, the tribunal adopted the use of base prices of

comparable properties which they accepted reflected similar

disabilities and therefore did not require further adjustment.

In conclusion, the key point in the judgement of how to value

mixed age properties lies in the establishment of evidence. As

the Lands Tribunal demonstrated, it prefers to value mixed age

properties at values geared to the local evidence for the age of each

part, and then make an allowance for the fact that they form part of

a larger hereditament. The quantum of that allowance should also

be established by evidence. To value on an overall rate reflecting

the majority floor space of the hereditament fails to take account of

the added value the newer parts bring. █

Philip Evans is Specialist Adviser (Industrial) with the Valuation Office Agency’s Rating Directorate Valuation and Policy Team.

In the decision, the tribunal considered there was no

comparable evidence to support the respondent s̓ approach.

“

www.irrv.net | March 2010 | VALUER

©iS

tock

phot

o.co

m/S

tura

inis

Cover story: visualising landvaluescape | 17

When I retired from the Survey Branch

of the Royal Engineers in 1994, having

acted as a kind of ‘internal consultant’

to UK defence forces on how to use

computer modelling of the physical

landscape, I became interested in how the

same techniques could be applied to the

economic landscape: Landvaluescape.

I had been lucky enough to spend

over half my 14 years in military surveying

in a pseudo-civilian capacity – first with

Ordnance Survey’s Development Branch in

Southampton in the early years of digital

mapping, seeing how local authorities,

the property industry and public utilities

in particular could use map data, and then

with the Australian Army, mapping their

‘outback’….and finally with the Hong Kong

government, helping prepare for British

withdrawal.

Australia and Hong Kong have more of

their tax revenue raised from land values

than anywhere else in the world. It seemed

to me no coincidence that they also

have among the finest ‘fiscal cadastres’

– property databases. So a link between

mapping land values and taxation was

established in my mind when I started

serious academic research on the subject

at Kingston University in 2002.

The hypothesis for my doctoral

thesis1, completed last year, was that the

concept of Visualising Landvaluescape now

offers discernable public and commercial

benefits for Britain, sufficient to justify

immediate and coherent steps to be taken

to overcome any institutional, technical

and policy (including tax policy) barriers

that might be exposed.

This article summarises, for British

professional valuers, what my research

found. It draws on four strands of research

work:

• the experience of selected other

countries;

• the views of a multi-disciplinary

British-based ‘virtual committee’ of

experts;

• an attempt to map land values

assessed by a professional valuer for

a trial of Land Value Taxation (LVT)

in part of Oxfordshire; and

• a thorough literature review.

Surveys I carried out in 2002 and

2005 of members of the World Congress

of Surveyors (FIG) showed that national

property tax systems invariably underpin

any nation-wide comprehensive, detailed

value mapping. In those systems, use of

computer-aided mass assessment (CAMA)

together with geographic information

system (GIS) techniques is becoming de rigour in all developed countries.

Five countries where such systems

have recently been modernised to take

advantage of latest technologies were

studied in detail: Denmark, Sweden,

Lithuania, Australia and the USA – the

The principle of land value mapping has many uses, and the UK should be listening. Tony Vickers expounds his theories for the benefit of Valuer readers

©iS

tock

phot

o.co

m/p

hoto

cana

l25

VALUER | March 2010 | www.irrv.net

Visualising Landvaluescape

18 | Cover story: visualising landvaluescape

latter exhibiting a cross-section of

systems generally run at county or state

level, from the most advanced to some

relatively arcane property tax assessments.

Visits were made to the three European

comparator countries.

Whereas their value mapping is

invariably designed purely to meet the

needs of tax authorities – more often for

internal quality control than for public

viewing – some property professionals

in many countries are now anticipating

potential uses in other areas, spatial

planning decision making (by both public

and private sectors) and insurance risk

assessment being the most interesting. The

EU itself used the word ‘landvaluescape’

in 2004 in a study of the economic impact

of sea-level rises that might result from

climate change.

Probably because Britain does not

have a comprehensive property tax

system, the 29 experts and value mapping

stakeholders2 who participated in three

rounds of questionnaire in a controlled

Policy Delphi in 2003–4 accepted fairly

readily that the novel concept of mapping

Landvaluescape was potentially useful. At

the outset of the study, it was of little or no

concern to them. Yet they were prepared

to engage with the subject.

The Delphi research technique was

chosen because it allows people with a

wide variety of professions and interests

to cross-fertilise views and ideas and

approach consensus on complex policy-

related matters. By taking full advantage of

internet technology, so as not to actually

meet at all, the Delphi participants’

collective pool of knowledge is enhanced,

in a way which minimises costs to all

concerned and pressure from dominant

individuals. My PhD supervisors monitored

my moderation of the Value Mapping

Delphi Process throughout, from selection

of participants through to final analysis and

feedback of results at a workshop in 2005.

The Delphi Group concluded by

broadly accepting an indicative Action

Plan for British Value Mapping (see

Figure 1)3. This broke down the concept

into three ‘scales’ of mapping and two

indicative programmes of action to take

the concept forward – one “market led”

and the other “tax reform led”. At each

scale, for the products to be of general

use, some leadership from government in

developing standards for property-related

geographic information (GI) is needed: a

“GI Champion” to pull together disparate

initiatives from various UK government

departments.

At the crudest level, it is possible now

to map categories of land value such as

‘house prices’ at local authority level.

Intermediate scale mapping, roughly at

postcode sector level, is less feasible, but

has been attempted for major transport

infrastructure project feasibility studies4.

‘Full’ value mapping requires

discrete site valuations or assessment of

neighbourhoods with no more than a few

hundred properties each, linked carefully

to detailed land use patterns and defined

‘break lines’ such as roads and rivers. This

can only be expected to happen if there

is a comprehensive modernisation of

property taxes, preferably recognising

the different ‘dynamic’ of land values as

distinct to the value of built property.

In North America, even when land and

buildings are taxed at the same rate,

assessments must distinguish these two

elements in tax/rating lists, which allows

value maps to be derived much more easily

than in the UK.

The pilot ‘desk study’ of LVT by

Oxfordshire County Council and Vale of

White Horse DC proved conclusively that

site valuations can be carried out with no

more difficulty than in other countries,

providing the definitive property market

transaction data and planning constraint

. . . a link between mapping land values and taxation was

established in my mind when I started serious academic research.

““

www.irrv.net | March 2010 | VALUER

©iS

tock

phot

o.co

m/p

hoto

cana

l25

Cover story: visualising landvaluescape | 19

data are

made available. The

trial used a former VOA valuer who

had to rely entirely on locally sourced

market data. The GIS officer of the rating

authority, which had already produced a

land parcel map of the district, mapped the

site values for use in a variety of theoretical

revenue yield calculations for ‘winners and

losers’ under LVT. Delays caused by lack of

staff and appropriate software in the local

authorities meant that the ‘landvaluescape

model’ wasn’t ready in time to present to

the Delphi Group. The literature review

revealed that the use of automated

valuation methods (AVMs) generally and

CAMA for tax assessment specifically is set

to grow rapidly worldwide, at least where

property markets are mature or being

developed. The technology is mature and

GIS/CAMA systems are easily adapted

to different national property datasets.

International agencies and professional

bodies invariably recommend that land

value is part of national land information

‘cadastres’.

The almost unique nature of British

land policies – lack of both a cadastre and

of comprehensive property taxation –

means

that property

professionals, especially valuers, are

unfamiliar with these new technologies.

In addition, the extremely commercial

attitude taken by Ordnance Survey

towards preserving its revenue from base

mapping data – a ‘low volume, high price’

business model – has acted as a brake on

the spread of applications using definitive

GI. Although a Parliamentary Inquiry

20 years ago found no good reason to

withhold VOA source data from public use,

this secrecy continues to be an obstacle to

research.

Perhaps the most interesting

conclusion from my research is that,

despite these apparently poor prospects,

Britain could yet see the most extensive,

up-to-date, detailed and accessible Value

Mapping system in the world within ten

years, given the political will to allow

increased sharing of publicly funded

datasets. The quality of our data is very