institutional herding in the u.s. reit market introduction this study examines herding by...

TRANSCRIPT

Institutional Herding in the U.S. REIT Market

Vicky Lantushenko∗

Drexel University†

Edward Nelling‡

Drexel University

January 8, 2014

Abstract

This study explores whether institutional investors exhibit herding behav-ior by property type in real estate investment trusts (REITs). Our analysisof changes in institutional portfolio holdings suggests strong evidence of herd-ing behavior. Although momentum trading explains a small amount of thisherding, institutional property type demand is more strongly associated withlagged institutional demand than lagged returns. Most of the correlation indemand is attributed to institutional investors following trades of other institu-tional investors. The results reveal that correlated information signals seem todrive institutional property type herding, and institutional investors are likelyto infer information about REIT property types from each others’ trades.

Keywords: REITs, herding behavior

∗Email: [email protected]†LeBow College of Business. Mailing address: 3141 Chestnut St. Philadelphia, PA 19104‡Corresponding author. Email: [email protected]. Tel.: 215-895-2117

1

1 Introduction

This study examines herding by institutional investors in real estate investment trusts(REITs). Herding is usually interpreted as the tendency of investors to behave in asimilar or coordinated manner. It may arise due to investors reacting to common in-formation, reputational concerns by portfolio managers, or positive feedback trading.From a behavioral perspective, researchers attribute herding to the collective irra-tionality of investors, which can result in the mispricing of economic fundamentals(Shiller, 2005). Within the context of asset pricing, this mispricing due to herdingcan cause price momentum and excess volatility (Nofsinger and Sias, 1999).

Herding in REITs is of interest for three main reasons. First, institutional invest-ment in REITs has increased dramatically over the last twenty years, which is oftenreferred to as the ”modern” REIT era. This increase was facilitated by RevenueReconciliation Act of 1993. By imposing new tax-related provisions, this legislationmade it easier for institutions to make significant investments in REITs.1 The in-creased presence of institutions and the associated increase in investment companies(including real estate mutual funds) that specialize in REITs may have elevated rep-utational concerns by portfolio managers. It may have also increased informationproduction, and thus increased the ability of investors to react to common informa-tion.

Second, a number of studies have investigated the extent to which REIT returnsare correlated with the broader stock market. Herding by institutional investorsin REITs, as well as in stocks in general, may increase this correlation. A highercorrelation between REITs and stocks would reduce the ability of REITs to providediversification to broad equity portfolios. On a related note, portfolios that specializein real estate may find diversification within the sector desirable. If herding existswithin REITs, the potential to diversify is lessened.

Third, the asset pricing literature has documented the importance of a momentumfactor in stock returns (Carhart, 1997). One form of herding is the tendency of someinstitutional investors to follow the trades of others with a lag. If this type of herdingexists, momentum in stock returns may result.

Empirical research on herding has followed two main approaches. The first focuseson characteristics in security returns. This approach was developed by Christie and

1Certain REITs have gained a special tax advantage that allows avoiding federal income taxespayment. Moreover, the 1993 Act modifies ”five or fewer” rule that restricts a REIT from taxadvantages if 50% of its shares are held by five or fewer shareholders. Since REITs generally havesmall market capitalizations, it was difficult of large investors to gain significant positions in REITswithout violating the ”five and fewer” provision. For more information on the effect of the RevenueReconciliation Act of 1993 on equity REITs, refer to Crain, Cudd, and Brown (2000).

2

Huang (1995) and Chang, Cheng, and Khorana (2000). Zhou and Anderson (2011)apply the Chang, Cheng, and Khorana methodology to REITs, and find that herdingtends to occur during periods of high volatility. The second approach to testingfor herding uses portfolio holdings. Examples of this approach include Lakonishok,Shleifer, and Vishny (1992), Sias (2004), and Choi and Sias (2009).

Our examination of REIT herding uses data on portfolio holdings. In addition,we focus on herding at the property type level. We believe that a property-typefocus is appropriate because it is a fundamental characteristic that differs betweenindividual REITs. Furthermore, industry organizations such as the National Asso-ciation of Real Estate Investment Trusts (NAREIT) provide performance data onREITs by property type2. In the academic literature, Chiang (2010) notes that in-creased institutional investment in REITs has resulted in information transfers thathave increased the correlation of firm-level prices and property type common in-formation. In addition, a number of studies have examined the popularity of styleinvesting (Barberis and Shleifer, 2003). If style investing is popular in REITs andthe underlying nature of style is related to property type, herding may result.

This study contributes to the literature on institutional investing in REITs inseveral ways. First, we use a measure of herding behavior that directly estimatesthe degree of correlated trading arising from institutional investors following tradesof other investors. Second, we provide significant evidence of institutional herdingin REITs, and also describe the mechanism behind such behavior. Specifically, ourresults indicate that institutional investors are most likely to infer information signalsabout REIT property types from each other’s trades. Finally, existing research onherding in REITs focused on real estate mutual funds, and we examine the tradingbehavior of all institutional investors.

Our empirical tests produce significant evidence of herding in REIT propertytypes by institutional investors. We measure buying demand for each property typein each quarter. Demand is strongly and positively correlated over consecutive quar-ters, and approximately 75% of this correlation is due to institutional investors fol-lowing the lagged trades of others. We also find that institutional investors tend tofollow their own lagged trades into the same stocks. However, they are more likely tofollow lagged trades of other institutions into and out of different stocks in the sameproperty type. This suggests that herding behavior among REIT investors appearsto be at the property type level, rather than at the individual stock level. In addition,we find that REIT investors are positive-feedback traders, but momentum tradingdoes not seem to be the primary source of property type herding. We also examinereturns around changes in demand and find weak evidence of return reversals, which

2http://returns.reit.com/returns/prop.pdf

3

suggests that correlated information signals are likely to drive herding in REITs.The remainder of this paper is organized as follows. The literature review is

described in the next section. The data and methodology are discussed in Section3. We then document the results of tests for institutional property type herding. Asummary is presented in the final section.

2 Literature Review

This study is related to the literature on institutional trading in REITs, herdingbehavior, and momentum in stock returns. Ro and Gallimore (2013) find some evi-dence of herding in REITs by real estate mutual funds, but it is lower than herdingin other stocks. In addition, they find that investment strategies based on herdingor momentum do not generate abnormal returns. Ling and Naranjo (2006) docu-ment that REIT mutual fund flows are positively related to past returns measuredover up to two previous quarters, suggesting that retail investors may engage in mo-mentum trading strategies. Generally, a large body of literature provides supportfor the existence of momentum trading among various types of investors, includingmutual funds, pension funds, retail investors, and others. For example, Grinblattet al. (1995) argue that mutual funds appear to be momentum investors, and thisphenomenon is mostly pronounced for purchases: fund managers tend to buy pastwinners, but do not systematically sell past losers. However, the existing studies donot differentiate whether the momentum phenomenon is driven by feedback tradingor by the effect of investors’ herding behavior (Wermers, 1999).

Related to herding behavior of investors in the market overall, the literaturehas not reached a consensus as to whether such behavior exists. In an early study,Lakonishok, Shleifer, and Vishny (1992) did not find herding behavior among pensionfunds. Other studies (e.g. Grinblatt et al. (1995)) found statistically significantevidence of herding behavior, but noted that it was not economically large. Whilethe aforementioned studies use institutional holdings to construct their measure ofherding, others examine herding based on market-wide trading imbalances. Themarket-wide herding measure was first developed by Christie and Huang (1995) andthen extended by Chang et al. (2000). The basic idea behind these measures ofherding is in the relationship between cross-sectional dispersion of stock returns andthe overall market return. These two studies using return-based measures found noevidence of herding the broad U.S. equity market, but significant evidence of herdingin emerging markets. Specifically related to herding behavior in REITs, Zhou andAnderson (2011) use return-based measures and find evidence of herding. They notethat it is mostly pronounced during times of high market volatility.

4

3 Data and Methodology

We obtained data for this study from three resources. Data on prices and returnsfor equity REITs come from the Center for Research in Securities Prices (CRSP).REIT property type classifications come from NAREIT. All institutional investorswith at least $100 million under management are required to report to the Securitiesand Exchange Commission their equity positions greater than either 10,000 shares or$200,000 in market value. We obtained quarterly changes in holdings of institutionalinvestors for each REIT from the 13(f) report database maintained by ThomsonFinancial. Our sample consists of all institutional holdings reported during the periodof the first quarter of 1993 through the last quarter of 2011 (a total of 76 quarters).This particular time period was specifically chosen to capture the impact of theRevenue Reconciliation Act of 1993 that drove the potential to change the investmentclientele within REITs. By establishing a ”look-through” provision, this act madeinvestments in REITs more attractive to institutional investors. Chan et al. (1998)report that institutional ownership in REITs ranges from 12% to 14% between 1986and 1992 and increased to 17% in 1993, 26% in 1994, and 30% in 1995. In light ofthe increase in institutional ownership in real estate equity immediately after suchtax legislation, examining investors behavior across different REIT property typesduring this time period is particularly interesting.

We classify managers as buyers or sellers in property type k in quarter t basedon the product of prices at the beginning of the quarter and change in holdings heldby a manager n at the end of the quarter. A manager n is considered a buyer in theREIT property type k if:

Ik,t∑i=1

Pi,t−1(Holdingsn,i,t −Holdingsn,i,t−1) > 0 (1)

where Ik,t is the number of securities in the REIT property type k in quarter t, Pi,t−1

is the price of the REIT security at the beginning of quarter t, andHoldingsn,i,t−1 andHoldingsn,i,t are the number of shares of the REIT security i held by an institutionalinvestor n at the beginning and end of quarter t. Similarly, an institutional investor isdefined as a seller in the REIT property type k in quarter t if the term on the left sideof Equation (1) is negative. We further define institutional property type demand(∆k,t) as the number of institutional investors buying the REIT property type k inquarter t as a fraction of the total number of institutional traders in property typek in quarter t:

5

∆k,t =#buyers of property type k in quarter t

#buyers of property type k in quarter t+# sellers of property type k in quarter t(2)

Table 1 reports the descriptive statistics of our sample. On average, 1697 institu-tional investors traded individual REITs each quarter (varying from 844 to 2899) overthe chosen time period. The average institutional property type demand is 50.17%with a very small standard deviation of 1.43%, indicating that, on average, the num-ber of buyers does not substantially differ from the number of sellers in the marketfor REITs. Panel B shows that, on average, there are 44 firms in a property type(varying from a minimum of 19 in Healthcare to a maximum of 64 in Retail). PanelB also reports that, on average, the property type constitutes about 14% of the totalREIT market capitalization, and the largest company in the property type accountsfor about 27.73% of the property type capitalization. Panel C illustrates time-seriessummary statistics for all seven REIT property types, including the average numberof companies in the REIT property type, the property type’s market capitalizationweight, the mean, and standard deviation of institutional property type demand.

4 Institutional herding tests

4.1 Correlation between current and lag property type de-mand

Our tests for institutional herding are based on Choi and Sias (2009). Theysuggest that the herding behavior of institutional investors can be inferred fromthe cross-sectional correlation between investors’ demand for securities in a givenindustry in quarter t and quarter t − 1. Using 49 Fama and French industries overthe period of 1983 to 2005, they find strong evidence of institutional industry herding.Specifically, the correlation between institutional industry demand this quarter andlast quarter averages around 0.40, and is statistically significant at the 1% level.Moreover, they discover that correlation between institutional industry demand thisquarter and last quarter arises mostly from investors following other investors in andout of industries. We follow their approach, using REIT property types instead ofindustries. We partition the correlation between REIT property type demand thisquarter and last quarter as follows (see Choi and Sias (2009) for proof):

6

(3)

ρ(∆k,t,∆k,t−1)

=1

(K − 1)σ(∆k,t)σ(∆k,t−1)

K∑k=1

Nk,t∑n=1

(Dn,k,t −∆k,t

Nk,t

)(Dn,k,t−1 −∆k,t−1

Nk,t−1

) +

1

(K − 1)σ(∆k,t)σ(∆k,t−1)

K∑k=1

Nk,t∑n=1

Nk,t−1∑m=1,m6=n

(Dn,k,t −∆k,t

Nk,t

)(Dm,k,t−1 −∆k,t−1

Nk,t−1

)

where K is the number of REIT property types (seven), Nk,t is the number of in-stitutions trading property type k in quarter t, σ(∆k,t) and ∆k,t are cross-sectionalstandard deviation and average institutional demand in quarter t, respectively, Dn,k,t

equals to one if institution n purchases the REIT property type k in quarter t andzero if institution n sells the REIT property type i in quarter t. In Eq. (3), thecross-sectional correlation between institutional investors’ property type demand thisquarter and last quarter is partitioned into two components: the first term is a por-tion of the correlation that arises from institutional investors following their ownlag demand for property type k and the second component arises from institutionalinvestors following other institutional investors ′ lag demand for property type k.

There are several reasons why a positive correlation between institutional REITproperty type demand this quarter and last quarter may be detected. For instance,a positive correlation may originate when one institutional investor purchased (sold)the retail property type in both quarter t and quarter t− 1. Furthermore, a positivecorrelation may also arise when one institutional investor bought (sold) the retailproperty type this quarter and other institutional investors purchased (sold) the re-tail property type last quarter. Table 2 reports the time-series average cross-sectionalcorrelation coefficient between institutional REIT property type demand this quarterand last quarter. The average correlation coefficient of 0.5359, statistically signifi-cant at the 1% level, indicates that there is a strong correlation between institutionalREIT property type demand in quarter t and quarter t − 1. The second and thirdcolumns of Table 2 illustrate a portion of the correlation coefficient attributed toinstitutional investors following their own REIT property type demand (0.1337) anda portion of the correlation coefficient attributed to institutional investors followingother institutions’ lag REIT property type demand (0.4022), respectively (Eq. (3)).Both partitioned correlation coefficients are statistically significant at the 1% level,based on t-statistics calculated using Newey-West standard errors from the time-series of regression coefficient estimates. The partitioned regression coefficient thatarises from institutional investors following their own lag demand constitutes about25% of the total correlation, and the partitioned correlation coefficient attributed to

7

institutional investors following lag demand of other institutional investors consti-tutes other 75% of the total correlation, providing support for REIT property typeherding behavior among institutional investors.

4.2 REIT individual stock herding vs. REIT property typeherding

As reported in Panel B of Table 1, on average, the largest firm in a propertytype accounts for about 28% of the total property type capitalization, ranging froma minimum of 15.93% to a maximum of 98.75% (such a maximum is attributed toLodging/Resorts with a few companies in the beginning of the 1990’s, when Lodg-ing/Resorts was in its early stages as a REIT property type). Given such descriptivestatistics, it is plausible that institutional herding occurs in individual stocks, andnot at the broader property type level. To explore this issue in more detail, we use analternative measure to detect institutional REIT property type herding, defining theproperty type demand as weighted average demand for stocks in each REIT propertytype. Specifically, the institutional demand for each REIT security i in quarter t isdefined as a ratio of the number of institutional investors increasing their positionsin stock i to the total number of the REIT stock i traders:

∆i,t =#of buyers of stock i in quarter t

# of buyers of stock i in quarter t+# of sellers of stock i in quarter t(4)

The weighted institutional demand is, therefore, defined as the capitalization-weighted demand across stocks in property type k:

∆∗k,t =

Ik,t∑i=1

ωi,t∆i,t (5)

where ωi,t is stock i′s market capitalization weight in REIT property type k at theend of quarter t.

The weighted cross-sectional correlation between weighted institutional demandin quarter t and quarter t − 1 is then partitioned in the following four components(see Choi and Sias (2009) for proof):

8

ρ(∆∗k,t,∆∗k,t−1) =

1

(K − 1)σ(∆∗k,t)σ(∆∗k,t−1)

K∑k=1

Ik,t∑i=1

ωi,tωi,t−1

Ni,t∑n=1

(Dn,i,t −∆∗k,t

Ni,t•

Dn,i,t−1 −∆∗k,t−1Ni,t−1

)+1

(K − 1)σ(∆∗k,t)σ(∆∗k,t−1)×

×K∑

k=1

Ik,t∑n=i

ωi,tωi,t−1

Ni,t∑n=1

Ni,t−1∑m=1,m 6=n

Dn,i,t −∆∗k,tNi,t

•Dm,i,t−1 −∆∗k,t−1

Ni,t−1

+

1

(K − 1)σ(∆∗k,t)σ(∆∗k,t−1)

K∑k=1

Ik,t∑i=1

Ik,t−1∑j=1,j 6=i

ωi,tωj,t−1

Ni,t∑n=1

Dn,i,t −∆∗k,tNi,t

•Dn,j,t−1 −∆∗k,t−1

Nj,t−1

+1

(K − 1)σ(∆∗k,t)σ(∆∗k,t−1)×

×K∑

k=1

Ik,t∑i=1

Ik,t−1∑j=1,j 6=i

ωi,tωj,t−1

Ni,t∑n=1

Nj,t−1∑m=1,m 6=n

Dn,i,t −∆∗k,tNi,t

•

Dm,j,t−1 −∆∗k,t−1Nj,t−1

(6)

where Ni,t is the number of institutional investors trading the REIT stock i in quartert and Dn,i,t is a dummy variable that equals one if an institution purchases security iin quarter t and zero if an institution sells security i in quarter t. The first addendumof Eq. (6) is the component of the correlation coefficient attributed to institutionalinvestors following their own trades in the same REIT security. The second ad-dendum of Eq. (6) is the portion of the correlation coefficient that originates frominstitutional investors following other institutional investors into the same REITstock. The third term is the portion of the correlation coefficient that arises frominstitutional investors following their own trades into different securities within thesame REIT property type, and the last addendum of Eq. (6) is the component of theweighted correlation coefficient attributed to institutional investors following othersinto different REIT securities within the same property type.

Table 3 reports the partitioned correlation coefficients, given in Eq. (6), andtheir associated Newey-West t-statistics. The cross-sectional correlation betweenweighted institutional demand this quarter and last quarter averages 0.789. Theresults, reported in the first column, indicate that institutional investors are morelikely to follow their own lagged trades into the same stocks than to follow others’

9

lagged trades into the same stocks. In contrast, the second column of Table 3 providesevidence that investors tend to follow lagged trades of other institutional investorsinto and out of different stocks in the same property type, suggesting that herdingbehavior among REIT investors is more likely to occur at the property type levelthan at the individual stock level.

4.3 Alternative herding measure

Many existing studies of herding behavior among institutional investors employ aherding measure developed by Lakonishok, Shleifer, and Vishny (LSV) (1992). Thismeasure is designed to capture the disproportionate number of buyers and sellers of agiven stock in a given quarter. The basic intuition behind the LSV herding measureis illustrated in the following example. Assuming that in a given quarter, aggregatedacross the population of investors and securities, 50% of the changes in shares arepositive and 50% of the changes in shares are negative. If it happens that 50% ofinvestors are buyers and 50% of investors are sellers, the LSV herding measure wouldindicate that there is no herding observed in the market. On the other hand, assumethat for many securities, 70% of investors increased their holdings and the rest, 30%of investors, decreased their holdings. In this situation, more investors appear to beon one side of the market than on the other side of the market, and the measurewould signal of herding behavior observed among investors.

To gain additional insights about institutional herding in REITs, we use thismeasure to evaluate the average herding across every REIT property type everyquarter. The herding measure is defined as:

Hk,t =| ∆k,t − Pk,t | −AFk,t (7)

where ∆k,t is the fraction of the number of managers buying property type k tothe total number of active traders in property type k in quarter t, Pk,t is defined asthe expected proportion of institutions buying property type k in quarter t relativeto the number of active traders (the cross-sectional average ∆k,t), and AFk,t is theadjustment factor. The adjustment factor is the expected value of | ∆k,t−Pk,t | andaccounts for the fact that the absolute value of (∆k,t − Pk,t) is positive under thenull hypothesis of no herding. The adjustment factor, AFk,t, is calculated based onthe assumption that the number of investors in property type k in quarter t followsa binomial distribution with the probability of success, the probability of buying,equal to Pk,t.

10

In our analysis of herding behavior across REIT property types, the Lakonishok,Shleifer, and Vishny (1992) herding measure averages 0.64% for 525 property-type-quarter observations (75 quarters × 7 property types) and is statistically differentfrom zero (t-statistics is 2.69). The basic interpretation of this result is that given theaverage institutional property type demand of 50.17% (as reported in Table 1), in anyrandomly selected property-type-quarter, we would expect 50.81% (50.17%+0.64%)of traders on one side of the market (buying or selling), and 49.19% of traders onthe other. In summary, both the Choi and Sias (2009) and Lakonishok, Shleifer,and Vishny (1992) measures reveal evidence of herding by institutional investors inREITs.

4.4 Herding and reputation

Research on herding behavior among investors suggests that institutions maybe motivated to herd for reputational purposes. For instance, Sias (2004) proposesthat if institutions herd due to reputational motives, they should be more likely tofollow institutions of the same type, rather than institutions of a different type (e.g.,banks will tend to follow the trades of other banks, instead of insurance companies).Moreover, since different types of institutions may operate under different aspectsof regulatory pressure, have differences in financial or other constraints, or be moresensitive to the influence of competitive environment, there is a reason to expectdifferent degrees of a herding tendency across various types of institutional investors.For example, changes in mutual fund reputation will most likely to be reflectedin their net flows. Alternatively, changes in the reputational aspect of insurancecompanies may not affect their net flows as much as they do for investment companiesor financial advisors. Therefore, since the functionality of investment companies, aswell as financial advisors, is more prone to reputational factors than it is for otherinstitutional investor types, one would expect the tendency of herding to be morepronounced among investment companies and financial advisors than among others.

Thomson Financial assigns all institutional investors into five major classifica-tions: advisors, banks, insurance companies, investment companies, and other (pen-sion funds, endowments, etc). We follow Choi and Sias (2009) to measure eachinvestor type’s propensity to herd in two ways: 1) as their average contribution fromfollowing institutions of a similar type and 2) their average contribution from follow-ing institutions of a different type. For example, each quarter, the average same-typeherding contribution for banks is defined as following (see Choi and Sias (2009) forproof):

11

(8)Same− typeBankst =

1

7

7∑k=1

Bk,t∑b=1

B∗k,t−1∑

m=1,m 6=b,m∈B

(Db,k,t −∆k,t)(Dm,k,t−1 −∆k,t−1)

Bk,tB∗k,t−1

where Bk,t is the number of banks trading property type k in quarter t and B∗k,t isthe number of different banks trading property type k in quarter t− 1. Analogically,the average different-type herding contribution for banks is the following (see Choiand Sias (2009) for proof):

Different− typeBankst =

1

7

7∑k=1

Bk,t∑b=1

Nk,t−1−Bk,t−1∑m=1,m/∈B

(Db,k,t −∆k,t)(Dm,k,t−1 −∆k,t−1)

Bk,t(Nk,t−1 −Bk,t−1)

(9)

where Nk,t−1−Bk,t−1 is the number of non-banks trading property type k in quartert− 1. Average same-type and different-type herding contributions are computed foreach of the five institutional investor types. Using Equation (3), we compute theaverage contribution from following their own lagged trades for each investor typeand the average contribution from following other investors’ trades across all othertrader types.

Table 4 documents mixed results for the reputational herding hypothesis. Thefirst column reports the average contribution from investors following their owntrades, and the second column shows the average contribution from following otherinstitutional investors’ trades into and out of property types. All contribution co-efficients in both columns are positive and statistically significant at the 1% levelfor each investor type, except for investment companies’ contribution from followingothers. The third column reports the average contribution from following similarlyclassified investors, and the fourth column documents the average contribution fromfollowing differently classified investors. As shown, investment advisors tend to fol-low lagged trades of other institutional investors, regardless of their classificationtypes. The results also reveal that banks tend to follow other banks; and in contrast,insurance companies seem to mimic lagged trades of differently classified investors.Moreover, investment companies, on average, do not appear to engage in herdingbehavior. The last column of Table 4 documents the difference between the thirdand fourth columns. This is a test whether each investor type is more likely to herdafter similarly classified investors or differently classified investors.

Overall, the herding behavior of financial advisors and banks is consistent withthe reputational herding hypothesis. As expected, the nature of the competitiveenvironment where financial advisors operate can explain why this type of institutions

12

tends to mimic the same-type investors at the significantly higher extent than adifferent-type of institutions. Surprisingly, this is not found to hold for investmentcompanies (e.g. mutual funds), institutions for whom reputation is at the heart oftheir existence and operation in the market. The reputational hypothesis also holdsfor the case of banks. This finding seems intuitive, since bank trust departments’flows may also be driven by their past performance. In addition, it is reasonableto find that the reputational hypothesis does not hold for insurance companies andunclassified investors, since these types of institutional investors are less likely toexperience changes in flows due to fluctuations in their reputation levels.

4.5 Herding and property type momentum

Institutional investors may herd in and out of REIT property types becauseproperty type demand is positively associated with lagged property type returns,i.e., momentum can drive institutional herding. To examine this possibility, we runcross-sectional regressions of institutional property type demand on lagged propertytype returns, measured over the previous quarter, six months, or a year. Propertytype returns are value-weighted. In addition, we also estimate regressions of contem-poraneous institutional demand on the lagged institutional property type demandover the previous quarter, six months, and a year. To facilitate the interpretationof the coefficient estimates, we standardize both institutional demand and propertytype returns by subtracting their cross-sectional mean and dividing them by theircross-sectional standard deviation.

Table 5 presents the results of the cross-sectional regressions of institutional de-mand on lagged institutional demand and lagged property type returns. Consistentwith the results, reported in Table 2, the cross-sectional regression of institutionalproperty type demand on the lagged property type demand produces a coefficientthat averages at 0.5359. To obtain the lagged six-month property type demand andthe lagged yearly property type demand, we define a manager as a buyer or a sellerbased on changes in holdings (Eq. (1)) over the previous six months or one year,respectively. The fourth and seventh columns of Table 5 indicate that institutionalproperty type demand is strongly and positively associated with demand measuredover the previous six months or a year. The second, fifth, and eighth columns ofTable 5 report that institutional demand is positively correlated with property typereturns measured over the previous quarter or six months and negatively correlatedwith property type returns measured over the previous year. These findings suggestthat REIT investors appear to engage in momentum trading at the property type

13

level.The third and sixth columns of Table 5 reveal that contemporaneous REIT prop-

erty type demand is positively associated with both the lagged demand and laggedproperty type return measured over the previous quarter and the previous six months,respectively. However, the last column of Table 5 indicates that contemporaneousdemand is positively correlated with the lagged demand and negatively correlatedwith the lagged return, measured over the previous year. This finding reveals the ev-idence that positive-feedback trading affects REIT investors’ property type demandover short-term horizons.

As illustrated by Table 5, in the regression of institutional demand on the laggeddemand and property type returns measured over the previous quarter, the coef-ficient associated with lag standardized returns averages 0.1709 and is statisticallysignificant at the 1% level. Because the variables are standardized, this result is in-terpreted as a one standard deviation increase in last quarter’s return leads to 0.1709standard deviation greater in contemporaneous property type demand. However, in-stitutional momentum trading constitutes a smaller portion of institutional herding.More specifically, adding a lag return to the regression has a very little influence onthe average coefficient on the previous quarter’s property type demand. As supportedby Table 5, the average coefficient associated with the lagged demand measured overthe previous quarter decreases from 0.5359 to 0.5022, when lagged return is addedto the model. Since all variables are standardized, the coefficients are directly com-parable - the average coefficient on the lagged demand is about 200% larger than theaverage coefficient associated with lagged property type return. The suggests that aone standard deviation change in lagged demand predicts a 200% greater change inthe following quarter’s demand than a one standard deviation change in lag return.In addition, adding lagged returns increases the explanatory power of the model byonly a small amount, as evidenced by the marginal increase in adjusted R2.

Overall, the findings reveal substantial evidence that REIT investors engage inpositive-feedback trading over short-term horizons. However, the relation betweencontemporaneous property type demand and lagged demand does not change muchafter accounting for past property type returns. Hence, momentum trading does notappear to be the primary driver of institutional herding among REIT investors.

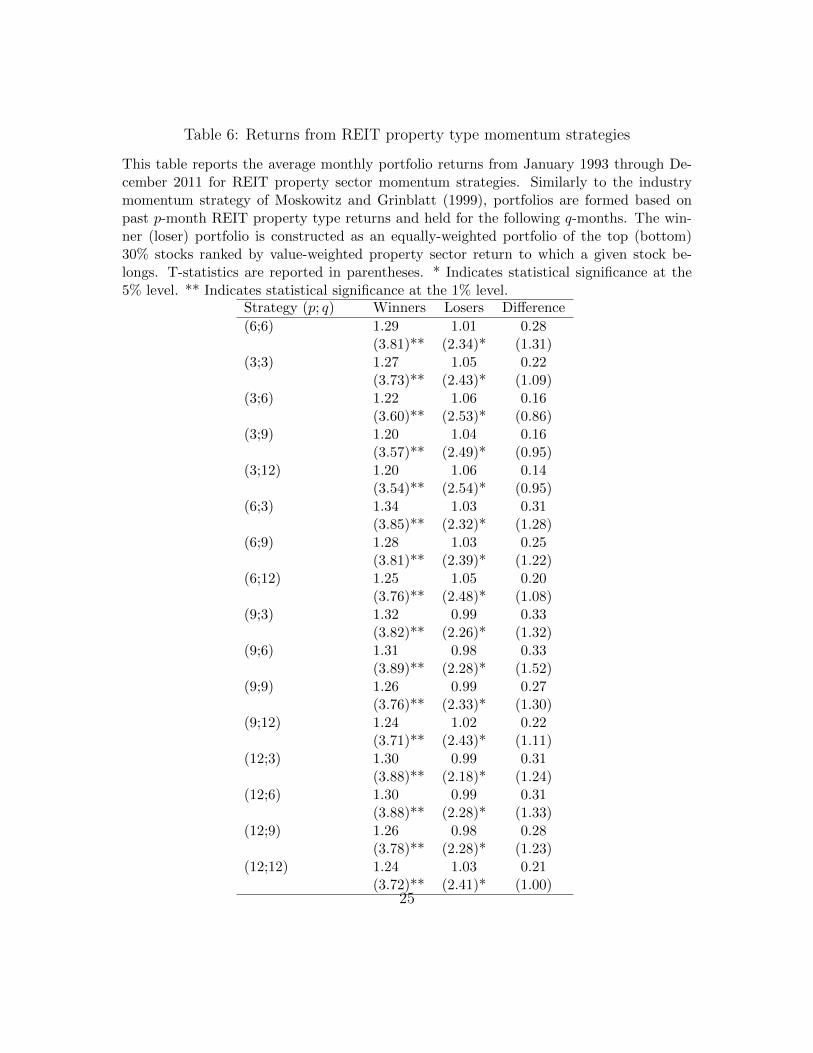

To further investigate institutional investors’ tendency to engage in momentumtrading, we analyze if various property type momentum strategies appear to beprofitable. Similar to the industry momentum strategy of Moskowitz and Grin-blatt (1999), we experiment with possible REIT property type momentum strategiesfor various formation and holding periods. To start, we calculate monthly value-weighted REIT property type returns from January 1993 through December 2011.

14

Each month, all REITs are ranked based on their property sectors’ past performanceover the p-month horizon. The number of months in the formation period, p, includes3, 6, 9, and 12 months. Stocks in the top 30% of property types form the winnerportfolio, and stocks in the bottom 30% of property type returns constitute the loserportfolio. The winner and loser portfolios are equally-weighted. The winner andloser portfolios are held for the following q months. The number of months in theholding period, q, includes 3, 6, 9, and 12 months. For example, in a given month of a(9;6) REIT property type momentum strategy, the return from winners is computedas the equally-weighted return of all six winner portfolios that were consecutivelyconstructed over previous nine months. Similarly, we calculate the return from theloser portfolio. The return to the REIT property type momentum strategy in thismonth is the difference between returns for the winner and loser portfolios.

Table 6 reports the returns for the REIT property type strategies for variousformation and holding periods. None of the considered strategies seem to promisesignificant profitability. Both the winner and loser portfolios do appear to generatesignificant positive returns regardless of the choice of the formation and holdingperiods. However, going long with the winners and going short with the losers doesnot seem to produce returns statistically indistinguishable from zero. As these resultssuggest, it would not be profitable for institutional investors to implement any of theconsidered strategies. Therefore, consistent with the evidence reported in Table 5,property type momentum is most likely to be an insufficient source of institutionalproperty type herding.

4.6 REIT property type demand and returns

One possible explanation for herding behavior suggests that investors may tradein the same direction as a result of reacting to correlated information signals. There-fore, herding may contribute to the process of a correct price adjustment (Wermers,1999). In contrast, recent research also suggests that herding may drive prices fur-ther away from fundamentals (Gutierrez and Kelley, 2009; Sias, Starks, and Titman,2006).

In this section, we attempt to differentiate between the correlated signals explana-tion from alternative explanations by studying the relationship between institutionaldemand and lagged, contemporaneous, and subsequent returns. If herding behav-ior among investors reflects correlated signals being incorporated into prices, theninstitutional demand should be positively associated with current property type re-turns and not negatively associated with subsequent returns, as institutions engage

15

in the price correction process. On the other hand, if herding tends to move pricesaway from their intrinsic values, then institutional demand should be positively cor-related with contemporaneous property type returns and negatively associated withsubsequent returns.

We start examining this hypothesis by identifying property types with highestexcess demand and lowest excess demand relative to the quarterly cross-sectionalaverage demand. Each quarter, excess demand is computed as the difference betweenthe demand in a given property type and average cross-sectional demand aggregatedacross all seven property types. We next calculate value-weighted returns of theidentified property types with the highest and lowest excess demands starting twoquarters prior to the formation period and up to three quarters following formation.In addition, having the time-series of quarterly returns, we estimate abnormal returnsfollowing Fama and French (1993):

Rp,t −Rf,t = αp + βp(Rm,t −Rf,t) + βSMBRSMB,t + βHMLRHML,t + εp,t (10)

where Rp,t is the quarterly return of property type with highest (lowest) excessdemand, Rf,t is the risk-free rate, and Rm,t, RSMB,t, and RHML,t are the Fama-French market, size, and value factors, respectively 3.

Table 7 reports average value-weighted returns (the first two columns) , as wellas Fama-French three-factor model alphas (the fourth and fifth columns), for prop-erty types with highest and lowest excess demands from two quarters prior to theformation quarter and up to three quarters following formation. The third columnreveals the difference between returns of property types with highest and lowest ex-cess demands and their associated t-statistics. The last column of Table 7 reportsthe difference in alphas (based on Eq. (10)), obtained from time-series regressions ofreturns of property types with highest and lowest excess demands.

The results, reported in Table 7, provide the support for the hypothesis thatinstitutional demand impacts prices. In the formation quarter and up to two quartersprior to formation, property types with highest excess demands outperform thosewith lowest excess demands by 2.60%, 4.01%, and 4.38% per quarter, respectively.The differences in alphas between portfolios with highest excess demand and lowestexcess demand are 3.41%, 3.91%, and 4.83% (all are statistically significant at the 1%level) during the formation period, one quarter prior to formation, and two quartersprior to formation, respectively. However, while the results indicate a strong positiverelation between property type demand and contemporaneous returns and returnsup to two quarters prior to formation, there is no evidence of subsequent return

3Quarterly market, size, and value factors were obtained from Ken French’s web site

16

reversals. Overall, the findings in Table 7 reveal that correlated information signalsdrive institutional property type herding.

5 Conclusion

This study documents that institutional investors exhibit herding behavior inREIT property types. We demonstrate that property type demand this quarter isstrongly and positively correlated with property type demand the previous quarter,and approximately 75% of this correlation is attributed to institutional investorsfollowing lagged trades of other institutional investors. The evidence indicates thatinstitutional investors tend to follow their own lagged trades into the same stocks;however, the analysis also shows that investors are more likely to follow lagged tradesof other institutional investors into and out of different stocks in the same propertytype, suggesting that herding behavior among REIT investors appears to be at theproperty type level rather than at the individual stock level. In addition, the re-sults reveal that REIT investors are positive-feedback traders; however, momentumtrading does not seem to be the primary source of herding among REIT institu-tional investors. Moreover, because evidence of return reversals is weak, our findingsare consistent with the hypothesis that the correlated informational signals seem todrive institutional property type herding, and institutional investors are likely toinfer REIT property type signals from each others’ trades.

17

References

[1] Barberis, Nicholas, and Andrei Shleifer, 2003. Style investing. Journal of Finan-cial Economics 68, 161-199.

[2] Carhart, Mark, 1997. On persistence in mutual fund performance. Journal ofFinance 52, 57-82.

[3] Chan, Su, Wai Leung, and Ko Wang, 1998. Institutional investment in REITs:Evidence and Implications. Journal of Real Estate Research 16, 357-374.

[4] Chang, Eric, Joseph Cheng, and Ajay Khorana, 2000. An examination of herdbehavior in equity markets: An international perspective. Journal of Bankingand Finance 24, 1651-1679.

[5] Chiang, Kevin, 2010. On the comovement of REIT prices. Journal of Real EstateResearch 32, 187-199.

[6] Choi, Nicole, and Richard Sias, 2009. Institutional industry herding. Journal ofFinancial Economics 94, 469-491.

[7] Christie, William, and Roger Huang, 1995. Following the pied piper: Do individ-ual returns herd around the market? Financial Analysts Journal 51, 31-37.

[8] Crain, John, Mike Cudd, and Christopher Brown, 2000. The impact of the Rev-enue Reconciliation Act of 1993 on the pricing structure of equity REITs. Journalof Real Estate Research 19, 275-285.

[9] Fama, Eugene, and Kenneth French, 1993. Common risk factors in the returnson stocks and bonds. Journal of Financial Economics 33, 3-56.

[10] Grinblatt, Mark, Sheridan Titman, and Russ Wermers, 1995. Momentum in-vestment strategies, portfolio performance, and herding: A study of mutual fundbehavior. The American Economic Review 85, 1088-1105.

[11] Gutierrez, Roberto, and Eric Kelley, 2009. Institutional herding and future stockreturns. Working paper.

[12] Jegadeesh, Narasimhan, and Sheridan Titman, 1993. Returns to buying winnersand selling losers: Implications for stock market efficiency. Journal of Finance48, 65-91.

18

[13] Lakonishok, Josef, Andrei Shleifer, and Robert Vishny, 1992. The impact ofinstitutional trading on stock prices. Journal of Financial Economics 32, 23-43.

[14] Ling, David, and Andy Naranjo, 2003. The dynamics of REIT capital flows andreturns. Real Estate Economics 31, 405-434.

[15] Moskowitz, Tobias, and Mark Grinblatt, 1999. Do industries explain momen-tum? Journal of Finance 54, 1249-1290.

[16] Newey, Whitney, and Kenneth West, 1987. A simple, positive, semi-definite, het-eroskedasticity and autocorrelation consistent covariance matrix. Econometrica55, 703-708.

[17] Nofsinger, John, and Richard Sias, 1999. Herding and feedback trading by in-stitutional and individual investors. Journal of Finance 54, 2263-2295.

[18] Ro, SeungHan, and Paul Gallimore, 2013. Real estate mutual funds: Herding,mometum trading and performance. Real Estate Economics 42, 1-33.

[19] Shiller, Robert, 2005. Irrational exuberance. Princeton University Press.

[20] Sias, Richard, 2004. Institutional herding. Review of Financial Studies 17, 165-206.

[21] Sias, Richard, Laura Starks, and Sheridan Titman, 2006. Changes in institu-tional ownership and stock returns: Assessment and methodology. Journal ofBusiness 79, 2869-2910.

[22] Wermers, Russ, 1999. Mutual fund trading and the impact on stock prices.Journal of Finance 54, 581-622.

[23] Zhou, Jian, and Randy Anderson, 2011. An empirical investigation of herdingbehavior in the U.S. REIT market. The Journal of Real Estate Finance andEconomics 47, 83-108.

19

Table 1: Institutional investors and REIT property type characteristics

Panel A reports the quarterly cross-sectional summary statistics of the number of in-

stitutional investors trading in each property type and institutional property type demand

each quarter. Panel B displays the time-series average of the quarterly cross-sectional

summary statistics for the number of firms in each property type, property type market

capitalization, and the portion of property type capitalization attributed to the largest

firm of the property type. Panel C of the table reports time-series descriptive statistics for

all seven REIT property types: the average number of companies in the property type,

the property type’s market capitalization weight, and the mean and standard deviation

of institutional demand for each REIT property type. The institutional demand for each

REIT property type quarter is defined as the ratio of the number of institutional buyers

to the total number of institutional buyers and sellers in the property type over one quarter.

Panel A: Institutional investor statistics

Mean Median Minimum Maximum Std.dev.

# of institutions trading in a REIT type 1697 1478 844 2899 739# of advisors trading 757 666 374 1315 335# of banks trading 269 244 140 443 112# of insurance companies trading 125 107 56 221 60# of investment companies trading 151 126 74 272 72# of unclassified investors trading 395 343 199 653 165# buyers/(# buyers+# sellers) 50.17% 49.62% 48.54% 52.39% 1.43%

Panel B: Property type statistics statistics

Mean Median Minimum Maximum Std.dev.

Number of firms in property type 44 48 19 64 17Property type capitalization 14.29% 14.55% 7.11% 21.75% 3.54%Largest firm in property type 27.73% 23.48% 15.96% 98.75% 12.27%

Panel C: Statistics by property type

Property type Property type demand%Market Auto-

# of Firms cap. Mean Std. dev. correlationDiversified 54 10.73% 0.4958 0.1246 0.72Healthcare 19 8.67% 0.5063 0.1324 0.67Lodging/Resorts 27 7.78% 0.5239 0.1658 0.79Office/Industrial 59 22.40% 0.5160 0.1380 0.75Other 38 10.76% 0.4854 0.1211 0.71Residential 48 16.44% 0.4962 0.1265 0.77Retail 64 23.22% 0.4886 0.1260 0.72

20

Table 2: Tests for property type herding

The institutional demand for each REIT property type quarter is defined as the ratioof the number of institutional buyers to the total number of institutional buyers and sellersin the property type over one quarter. The first column reports the time-series averagecorrelation coefficient between institutional property type demand in quarter t and quartert − 1. The second column displays a portion of the correlation coefficient attributed toinstitutional investors following their own lag demand, and the third column reports aportion of the correlation coefficient attributed to institutional investors following lagdemand of other institutional investors. T-statistics is calculated using Newey-West (1987)standard errors from the time-series of regression coefficient estimates. *** Indicatesstatistical significance at the 1% level.

Partitioned correlation coefficientAverage correlation Institutions following Institutions following

coefficient their own lag property other instutions’ lag

type demand property type demand

Property type 0.5359 0.1337 0.4022demand (10.81)*** (2.81)*** (5.22)***

21

Table 3: Regression of weighted institutional property type demand on lag weightedinstitutional property type demand

Weighted institutional demand is defined as a cross-sectional weighted average demandfor all stocks in property type k. The table reports the time-series average correlationcoefficient between weighted institutional property type demand in quarter t and quartert− 1. Based on Eq. (6), this correlation coefficient is partitioned into four terms. The topleft-hand cell of the table represents a portion of correlation attributed to institutionalinvestors following themselves into the same stock. The left-hand cell in the middle rowcontains a portion of correlation attributed to institutional investors following others intothe same stock. The middle cell in the top row displays a portion of correlation that arisesfrom institutional investors following themselves into different REIT securities in the sameproperty type, and the middle cell in the middle row illustrates a portion of correlationattributed to institutional investors following other institutions into different stocks in thesame REIT property type. The right-hand side column represents totals with respect towhat portion of the average correlation is attributed to institutions following themselvesand what portion of the average correlation is attributed to institutions following others.The bottom row of the table contains totals with respect to what portion of the averagecorrelation is attributed to institutional investors following into the same stock and whatportion of the average correlation is attributed to investors following into different stocksin the same property type. ***, ** and * indicate statistical significance at the 1%, 5%and 10% level, respectively.

Partitioned correlation coefficientInto different stocks

in the sameInto the same stock property type Total

Following themselves 0.0154 0.0680 0.0834(2.84)*** (1.82)* (1.96)**

Following others 0.0216 0.6846 0.7062(1.27) (11.39)*** (10.18)***

Total 0.0370 0.7526 0.7896(2.37)** (23.22)*** (21.88)***

22

Table 4: Property type herding analysis by investor type

This table reports the average contribution for the cross-sectional correlation between in-stitutional demand this quarter and last quarter by investor type.The first column presentseach investor type’s propensity to follow their own lagged property type demand and thesecond column presents investors’ propensity to follow other institutional investors intoand out of the same property type. The third column reports the average contributionto the correlation from different investor types following similarly classified institutions,e.g. insurance companies following other insurance companies. The average contributionthat arises from investors following other investors of a different type is reported in thefourth column. The last column reports the difference between the average contributionfrom following same-type traders and the average contribution from following different-typetraders. All t-statistics are calculated based on Newey and West (1987) standard errors.* Indicates statistical significance at the 10% level. ** Indicates statistical significance atthe 5 % level. *** Indicates statistical significance at the 1% level.

Average Average Average Average Averagecontribution contribution contribution contribution ”same

from from from following from following contribution”

following following same- different- lesstheir own others’ type type ”different

trades trades traders traders contribution”

Advisors 0.00024 0.00011 0.00118 0.00003 0.00115(6.01)*** (3.51)*** (3.27)*** (2.24)** (3.27)***

Banks 0.00091 0.00005 0.00251 0.00002 0.00249(2.44)** (1.78)* (3.70)*** (1.53) (3.72)***

Insurance 0.00090 0.00002 0.00096 0.00001 0.00095companies (2.94)*** (3.09)*** (1.07) (2.34)** (1.06)

Investment 0.00247 0.00000 -0.00018 0.00000 -0.00018companies (2.83)*** (0.05) (-0.34) (0.38) (-0.34)

Other 0.00189 0.00004 0.00129 0.00001 0.00128(3.25)*** (3.35)*** (1.64) (1.89)* (1.63)

23

Tab

le5:

Tes

tsfo

rR

EIT

pro

per

tyty

pe

her

din

gan

dm

omen

tum

trad

ing

Each

colu

mn

inth

ista

ble

rep

orts

the

tim

e-se

ries

aver

age

coeffi

cien

tfr

om74

cross

-sec

tion

al

regre

ssio

ns

(fro

mS

epte

m-

ber

198

3to

Dec

emb

er2011

)of

stan

dar

diz

edin

stit

uti

onal

pro

per

tyty

pe

dem

and

this

qu

arte

ron

:(1

)st

an

dar

diz

edla

gin

stit

uti

onal

pro

per

tyty

pe

dem

and

over

the

pre

vio

us

qu

arte

r,si

xm

onth

s,or

yea

r(fi

rst,

fou

rth

,an

dse

venth

colu

mn

s),

(2)

stan

dard

ized

pro

per

tyty

pe

retu

rns

the

pre

vio

us

qu

arte

r,si

xm

onth

s,or

year

(sec

on

d,

fift

h,

an

dei

ghth

colu

mn

s),

(3)

stan

dard

ized

pro

per

tyty

pe

retu

rns

and

stan

dar

diz

edin

stit

uti

onal

pro

per

tyty

pe

dem

an

dov

erth

ep

re-

vio

us

qu

art

er,

six

mon

ths,

orye

ar(t

hir

d,

sixth

,an

dla

stco

lum

ns)

.A

llt-

stat

isti

csar

ead

just

edb

ase

don

New

eyan

dW

est

(1987)

stan

dard

erro

rs,

com

pu

ted

from

the

tim

e-se

ries

ofco

effici

ent

esti

mate

s,an

dare

rep

ort

edin

pare

nth

eses

.**

Ind

icate

sst

ati

stic

alsi

gnifi

can

ceat

the

1%le

vel

;*

atth

e5%

level

.M

easu

red

over

pre

vio

us

Mea

sure

dov

erp

revio

us

Mea

sure

dov

erp

revio

us

qu

arte

rsi

xm

onth

sye

ar

Lag

inst

itu

tion

al

0.53

59

0.50

220.

5015

0.469

40.3

927

0.392

3d

eman

d(1

0.8

1)**

(8.4

9)**

(12.

76)*

*(1

1.09)

**

(8.7

5)**

(6.5

6)*

*

Lag

retu

rn0.

1873

0.17

090.

2721

0.239

2-0

.1665

-0.1

829

(3.4

1)**

(3.8

5)**

(4.2

5)**

(5.9

3)*

*(-

2.21)

*(-

2.9

2)*

*

Ad

just

edR

226.6

9%5.

21%

26.8

0%23

.02%

7.37

%26

.02%

33.

59%

20.

95%

16.6

9%

24

Table 6: Returns from REIT property type momentum strategies

This table reports the average monthly portfolio returns from January 1993 through De-cember 2011 for REIT property sector momentum strategies. Similarly to the industrymomentum strategy of Moskowitz and Grinblatt (1999), portfolios are formed based onpast p-month REIT property type returns and held for the following q-months. The win-ner (loser) portfolio is constructed as an equally-weighted portfolio of the top (bottom)30% stocks ranked by value-weighted property sector return to which a given stock be-longs. T-statistics are reported in parentheses. * Indicates statistical significance at the5% level. ** Indicates statistical significance at the 1% level.

Strategy (p; q) Winners Losers Difference

(6;6) 1.29 1.01 0.28(3.81)** (2.34)* (1.31)

(3;3) 1.27 1.05 0.22(3.73)** (2.43)* (1.09)

(3;6) 1.22 1.06 0.16(3.60)** (2.53)* (0.86)

(3;9) 1.20 1.04 0.16(3.57)** (2.49)* (0.95)

(3;12) 1.20 1.06 0.14(3.54)** (2.54)* (0.95)

(6;3) 1.34 1.03 0.31(3.85)** (2.32)* (1.28)

(6;9) 1.28 1.03 0.25(3.81)** (2.39)* (1.22)

(6;12) 1.25 1.05 0.20(3.76)** (2.48)* (1.08)

(9;3) 1.32 0.99 0.33(3.82)** (2.26)* (1.32)

(9;6) 1.31 0.98 0.33(3.89)** (2.28)* (1.52)

(9;9) 1.26 0.99 0.27(3.76)** (2.33)* (1.30)

(9;12) 1.24 1.02 0.22(3.71)** (2.43)* (1.11)

(12;3) 1.30 0.99 0.31(3.88)** (2.18)* (1.24)

(12;6) 1.30 0.99 0.31(3.88)** (2.28)* (1.33)

(12;9) 1.26 0.98 0.28(3.78)** (2.28)* (1.23)

(12;12) 1.24 1.03 0.21(3.72)** (2.41)* (1.00)

25

Table 7: Herding and subsequent returns

This table reports quarterly value-weighted returns and abnormal returns for propertytypes with highest and lowest excess demands over the formation quarter (Quarter 0),up to two quarters prior to formation, and up to three quarter after formation. Excessdemand is defined as the difference between the demand in a given property type andaverage cross-sectional demand aggregated across all seven property types each quarter.T-statistics (reported in parentheses) are based on Newey-West standard errors (1987). *Indicates statistical significance at the 10% level. *** Indicates statistical significance atthe 1% level.

Property type value-weighted Fama-French three-factorreturns model alphas

Highest Lowest Highest Lowest

excess exccess excess exccess

demand demand Difference demand demand Difference

Quarter -2 0.0690 0.0252 0.0438 0.0649 0.0166 0.0483(3.74)*** (3.85)***

Quarter -1 0.0548 0.0147 0.0401 0.0496 0.0105 0.0391(3.45)*** (3.09)***

Quarter 0 0.0585 0.0325 0.0260 0.0294 -0.0047 0.0341(2.66)*** (2.72)***

Quarter 1 0.0462 0.0345 0.0117 0.0282 0.0208 0.0074(1.34) (0.56)

Quarter 2 0.0375 0.0516 -0.0141 0.0283 0.0520 -0.0237(-1.12) (-1.72)*

Quarter 3 0.0461 0.0589 -0.0128 0.0413 0.0590 -0.0177(-0.99) (-1.27)

26