institutional presentation - 2q14

TRANSCRIPT

Aug 8th, 2014

2

Company Defense & Security

Metallurgy & Plastics

Guidance Results Strategies

3

Company

Forjas Taurus S.A.

• LARGEST MANUFACTURER OF REVOLVERS

• LEADING NATIONAL HELMETS’ PRODUCTION

• BRAZILIAN COMPANY WITH METAL INJECTION

MOLDING TECHNOLOGY

4

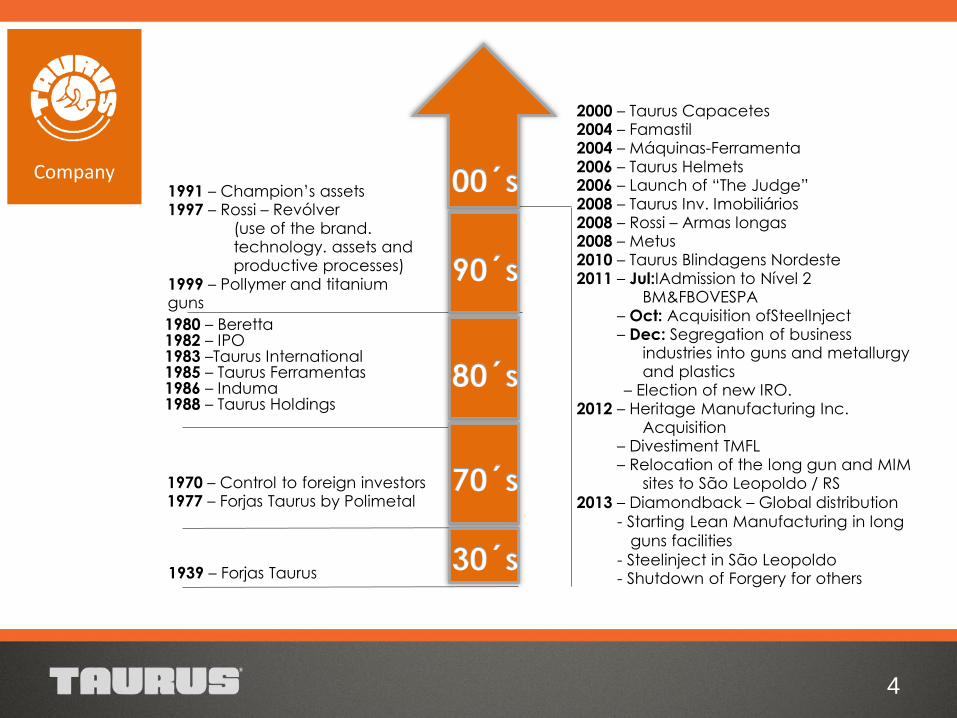

Company

1980 – Beretta 1982 – IPO 1983 –Taurus International 1985 – Taurus Ferramentas 1986 – Induma 1988 – Taurus Holdings

2000 – Taurus Capacetes 2004 – Famastil 2004 – Máquinas-Ferramenta 2006 – Taurus Helmets 2006 – Launch of “The Judge” 2008 – Taurus Inv. Imobiliários 2008 – Rossi – Armas longas 2008 – Metus 2010 – Taurus Blindagens Nordeste 2011 – Jul:IAdmission to Nível 2

BM&FBOVESPA – Oct: Acquisition ofSteelInject – Dec: Segregation of business

industries into guns and metallurgy and plastics

– Election of new IRO. 2012 – Heritage Manufacturing Inc.

Acquisition – Divestiment TMFL – Relocation of the long gun and MIM

sites to São Leopoldo / RS

2013 – Diamondback – Global distribution

- Starting Lean Manufacturing in long

guns facilities

- Steelinject in São Leopoldo - Shutdown of Forgery for others

00´s

30´s

70´s

80´s

90´s

1939 – Forjas Taurus

1970 – Control to foreign investors 1977 – Forjas Taurus by Polimetal

1991 – Champion’s assets 1997 – Rossi – Revólver

(use of the brand. technology. assets and productive processes)

1999 – Pollymer and titanium guns

2014 Facts

• Election of the Board of Directors by the multiple voting process at the

AGM realized on 06/27/14 and amend the Bylaw, increasing from 7 to 9

members with names linked to a strong experience in Corporate

Governance and Management;

• Tenure of the new Board of Directors on 07/17/14, elected Mr. Jório

Dauster and Mr. Ruy Lopes Filho as Chairman and Vice-Chairman,

respectively; also appointed the members of the Advisory Statutory

Committees of the Board: Audit and Risk, Remuneration and People

Development and Management and Corporate Governance Committee.

5

Company

• Actions for operational improvement: a process and products review in

order to reduce costs and expenses, measured by indicators that show a

reduction in staff and product portfolio (from 5,500 SKUS on Dec/13 to 400

on Dec/14);

• Actions for administrative improvemet: implementation of new ERP

modules, review of the entire value chain, balancing costs and the structure

of products and local and international sales, aiming to better internal

controls and compliance with market requirements;

6

Company

2014 Facts

• Trends and benefits of these transformations:

• Results-oriented strategic focus in the medium and long term;

• Resumption slow but gradual and continuos of the Company’s

perfomance, according to market conditions and productivity;

• Projects seeking greater productivity, quality and profitability;

• Recovery of margins and profitability;

• Continuos pursuit of maximazing shareholder value added; and

• Benefits will come through structural changes, causing the Company

to re-grow consistently and sustainably.

7

Company

2014 Facts

• Capital Increase

8

Company

• After two rounds of leftovers and period of review, 48,522,214

common shares and 85,703 preferred shares have been

subscribed, of the total of 48,528,020 common shares and

97,056,038 preferred shares, without par value, to be issued by

the Company;

• With the end of the review period, the subscribed shares

totaled BRL 67.078.925,46;

• The process of capital increase was completed and an

Extraordinay General Meeting has been convened for 08/20/14

in order to resolve their approval.

2014 Facts

9

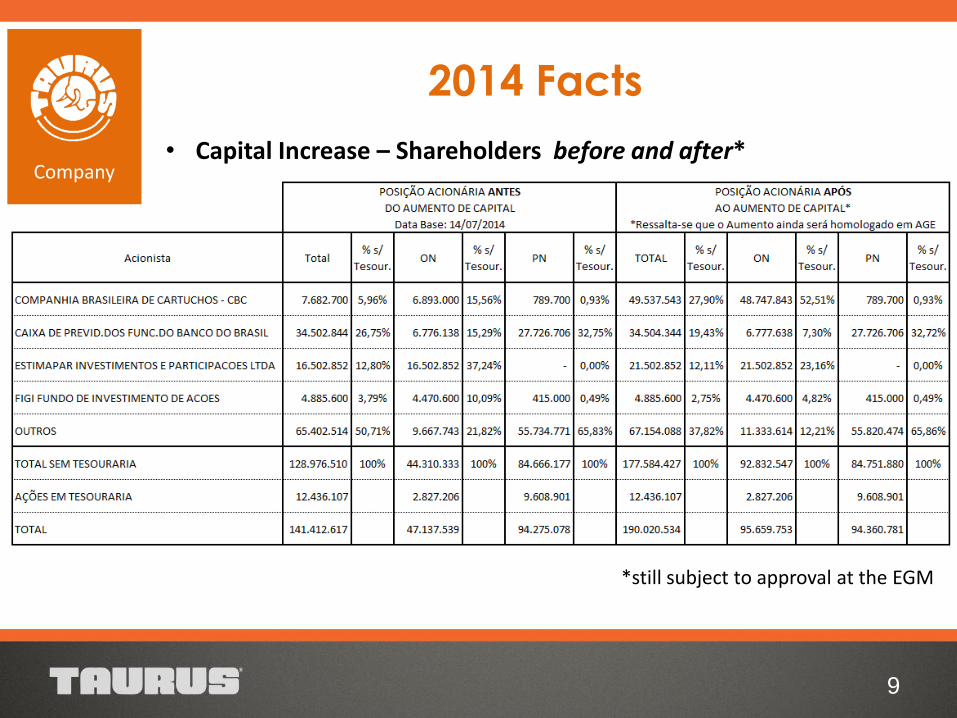

Company • Capital Increase – Shareholders before and after*

*still subject to approval at the EGM

2014 Facts

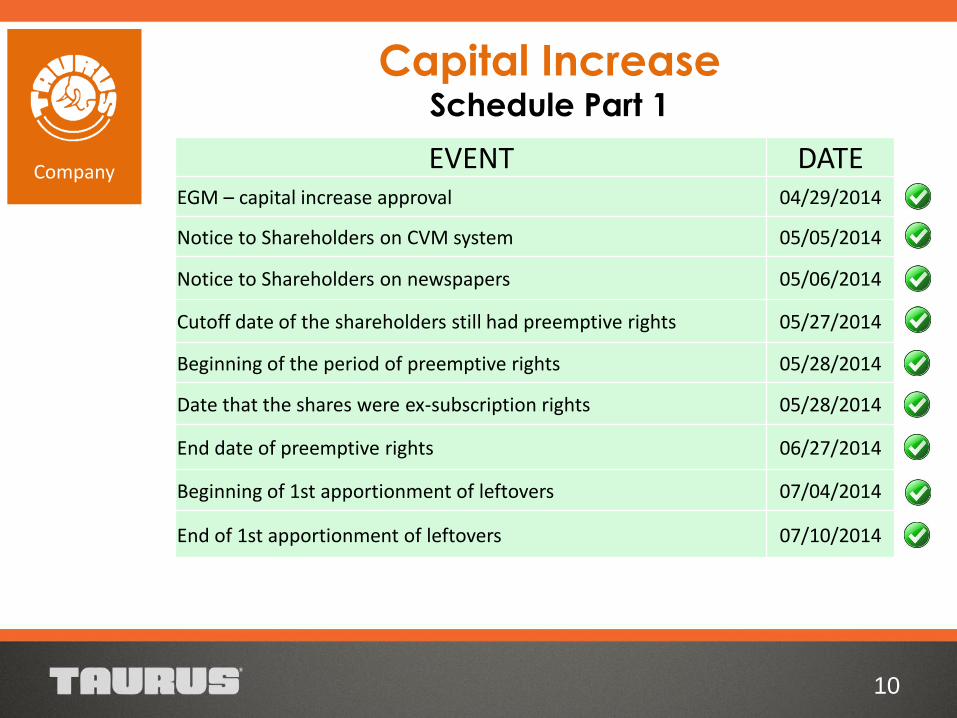

Capital Increase Schedule Part 1

10

Company EVENT DATE EGM – capital increase approval 04/29/2014

Notice to Shareholders on CVM system 05/05/2014

Notice to Shareholders on newspapers 05/06/2014

Cutoff date of the shareholders still had preemptive rights 05/27/2014

Beginning of the period of preemptive rights 05/28/2014

Date that the shares were ex-subscription rights 05/28/2014

End date of preemptive rights 06/27/2014

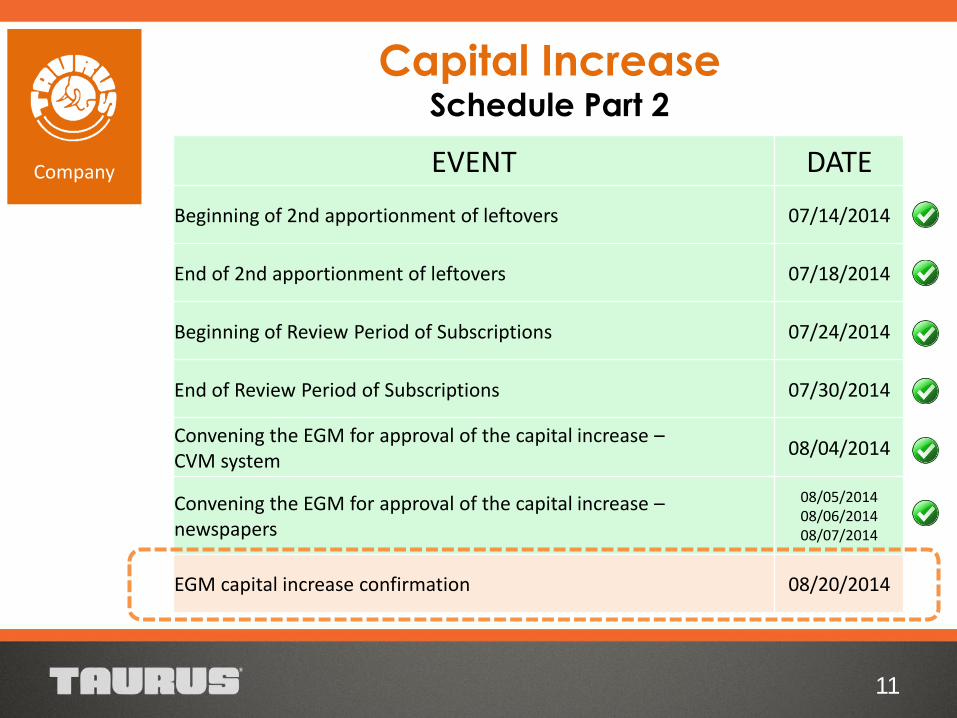

Beginning of 1st apportionment of leftovers 07/04/2014

End of 1st apportionment of leftovers 07/10/2014

11

Company EVENT DATE

Beginning of 2nd apportionment of leftovers 07/14/2014

End of 2nd apportionment of leftovers 07/18/2014

Beginning of Review Period of Subscriptions 07/24/2014

End of Review Period of Subscriptions 07/30/2014

Convening the EGM for approval of the capital increase – CVM system

08/04/2014

Convening the EGM for approval of the capital increase – newspapers

08/05/2014 08/06/2014 08/07/2014

EGM capital increase confirmation 08/20/2014

Capital Increase Schedule Part 2

Board of Directors

Chairman: Jorio Dauster Magalhães e Silva

Vice-Chairman: Ruy Lopes Filho

André Ricardo Balbi Cerviño

Durval José Soledade Santos

Fernando José Soares Estima

João Verner Juenemann

Luis Fernando Costa Estima

Luiz Felix de Freitas

Manuel Jeremias Leite Caldas

Tax Board

Amoreti Franco Gibbon

Alternate: Edgar Panceri

Juliano Puchalski Teixeira Alternate: Carlos Eduardo Bandeira de Mello Francesconi

Marcelo de Deus Saweryn Alternate: Lisiane Miguel Wilke

Mauro César Medeiros de Mello Alternate: Roberto Hesketh

Reinaldo Fujimoto

Alternate: José Airton Veras Carvalho

12

Company

Statutory Board

André Ricardo Balbi Cerviño

Eduardo Feldmann Costa

Eduardo Ermida Moretti

Dóris Beatriz França Wilhelm

Board

13

Company

Facilities

Co

rpo

rate

Go

ve

rna

nc

e

14

Company

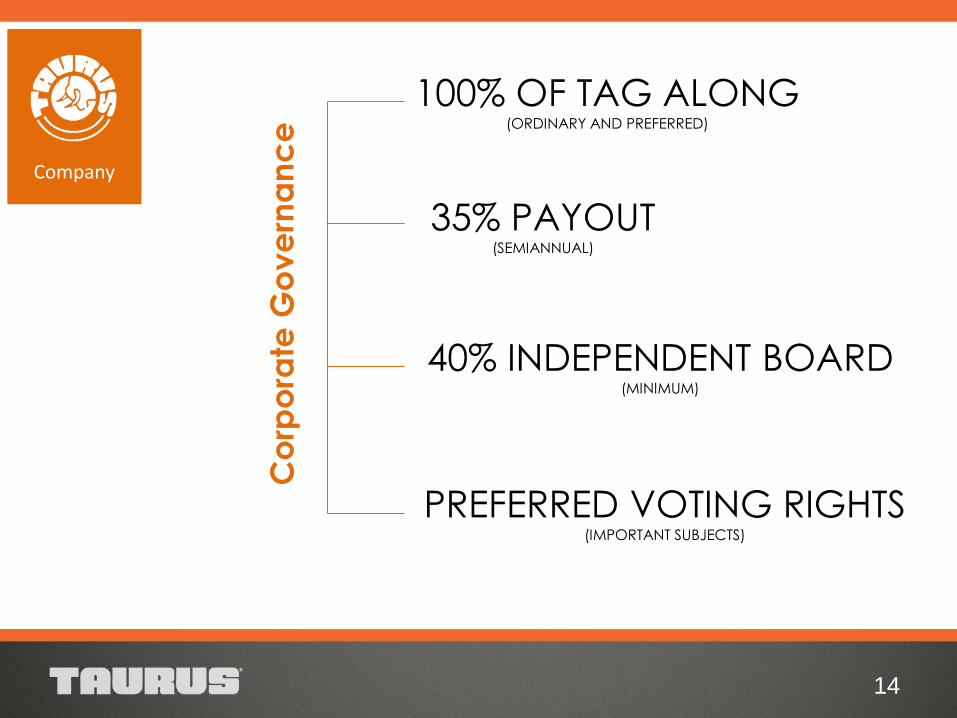

100% OF TAG ALONG (ORDINARY AND PREFERRED)

35% PAYOUT (SEMIANNUAL)

PREFERRED VOTING RIGHTS (IMPORTANT SUBJECTS)

40% INDEPENDENT BOARD (MINIMUM)

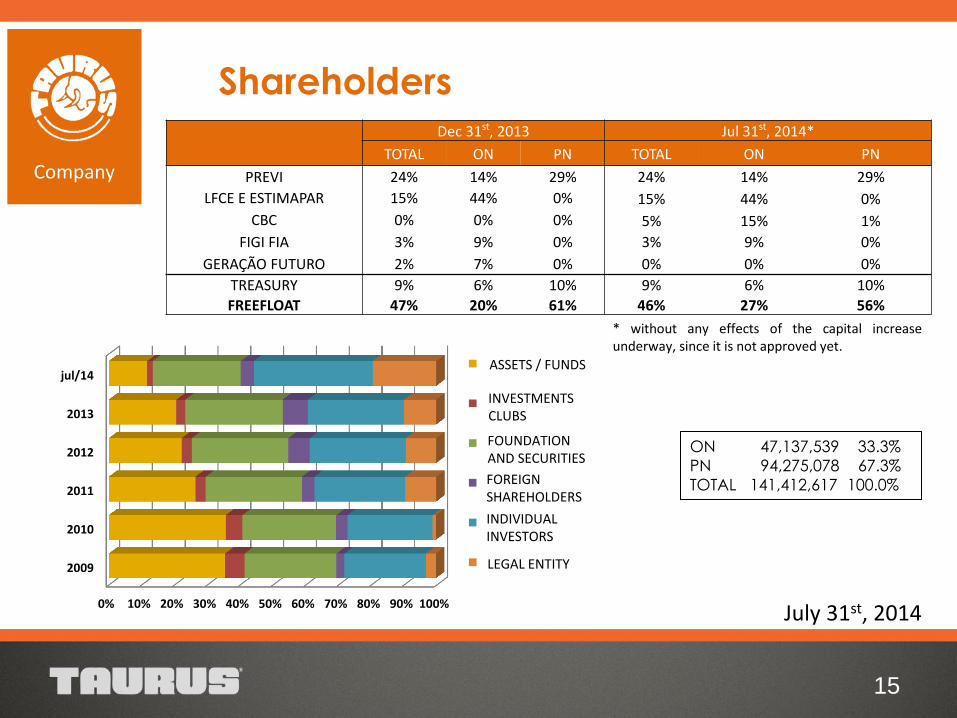

ON 47,137,539 33.3%

PN 94,275,078 67.3%

TOTAL 141,412,617 100.0%

Dec 31st, 2013 Jul 31st, 2014*

TOTAL ON PN TOTAL ON PN

PREVI 24% 14% 29% 24% 14% 29%

LFCE E ESTIMAPAR 15% 44% 0% 15% 44% 0%

CBC 0% 0% 0% 5% 15% 1%

FIGI FIA 3% 9% 0% 3% 9% 0%

GERAÇÃO FUTURO 2% 7% 0% 0% 0% 0%

TREASURY 9% 6% 10% 9% 6% 10%

FREEFLOAT 47% 20% 61% 46% 27% 56%

15

July 31st, 2014

Company

Shareholders

* without any effects of the capital increase underway, since it is not approved yet.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2009

2010

2011

2012

2013

jul/14ASSETS / FUNDOS

CLUBES DEINVESTIMENTOS

FUNDAÇÕES ESEGURADORAS

ESTRANGEIROS

PESSOA FISÍCA

PESSOA JURÍDICA

ASSETS / FUNDS

INVESTMENTS CLUBS

FOUNDATION AND SECURITIES

FOREIGN SHAREHOLDERS

INDIVIDUAL INVESTORS

LEGAL ENTITY

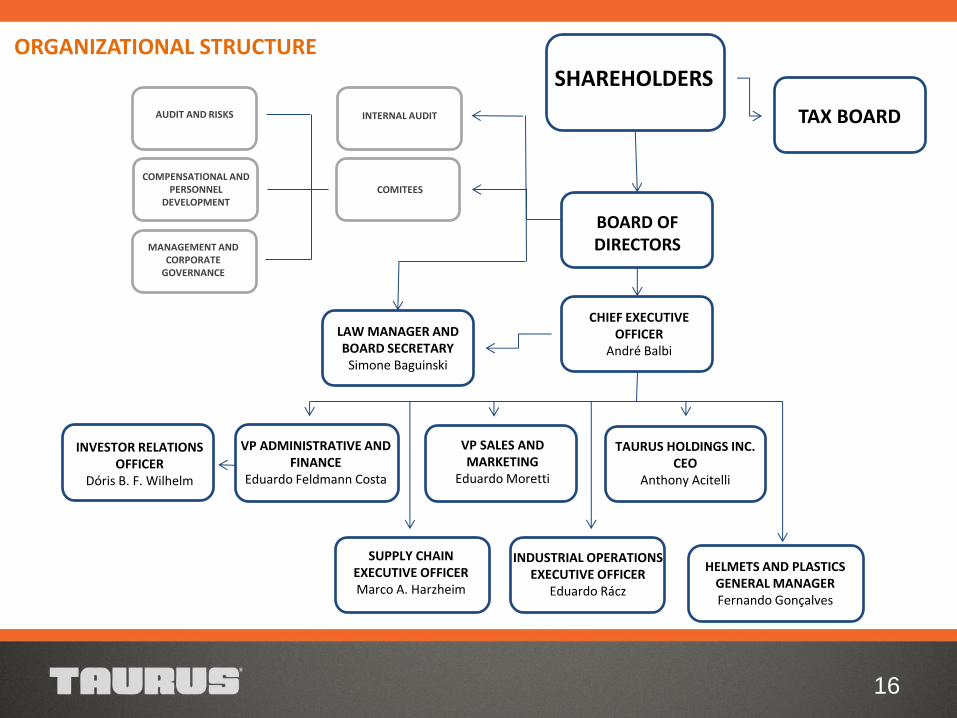

16

INVESTOR RELATIONS OFFICER

Dóris B. F. Wilhelm

VP ADMINISTRATIVE AND FINANCE

Eduardo Feldmann Costa

SHAREHOLDERS

BOARD OF DIRECTORS

CHIEF EXECUTIVE OFFICER

André Balbi

TAURUS HOLDINGS INC. CEO

Anthony Acitelli

INTERNAL AUDIT

COMITEES

LAW MANAGER AND BOARD SECRETARY

Simone Baguinski

COMPENSATIONAL AND PERSONNEL

DEVELOPMENT

AUDIT AND RISKS

MANAGEMENT AND CORPORATE

GOVERNANCE

VP SALES AND MARKETING

Eduardo Moretti

HELMETS AND PLASTICS GENERAL MANAGER Fernando Gonçalves

TAX BOARD

INDUSTRIAL OPERATIONS EXECUTIVE OFFICER

Eduardo Rácz

ORGANIZATIONAL STRUCTURE

SUPPLY CHAIN EXECUTIVE OFFICER Marco A. Harzheim

17

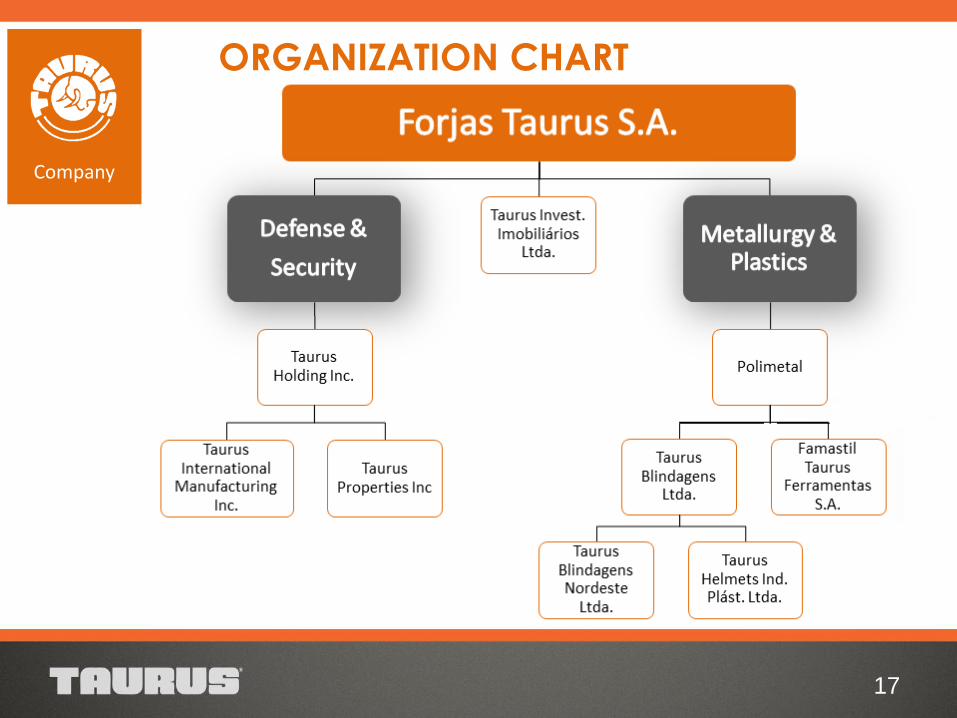

Company

ORGANIZATION CHART

18

SOCIAL COMMITMENT

Company

• Kids of the Future

• Library

• Digital Space

• Sign Language Course

• Educational Benefits

• Impulsor News

19

Company Defense & Security

Metallurgy & Plastics

Guidance Results Strategies

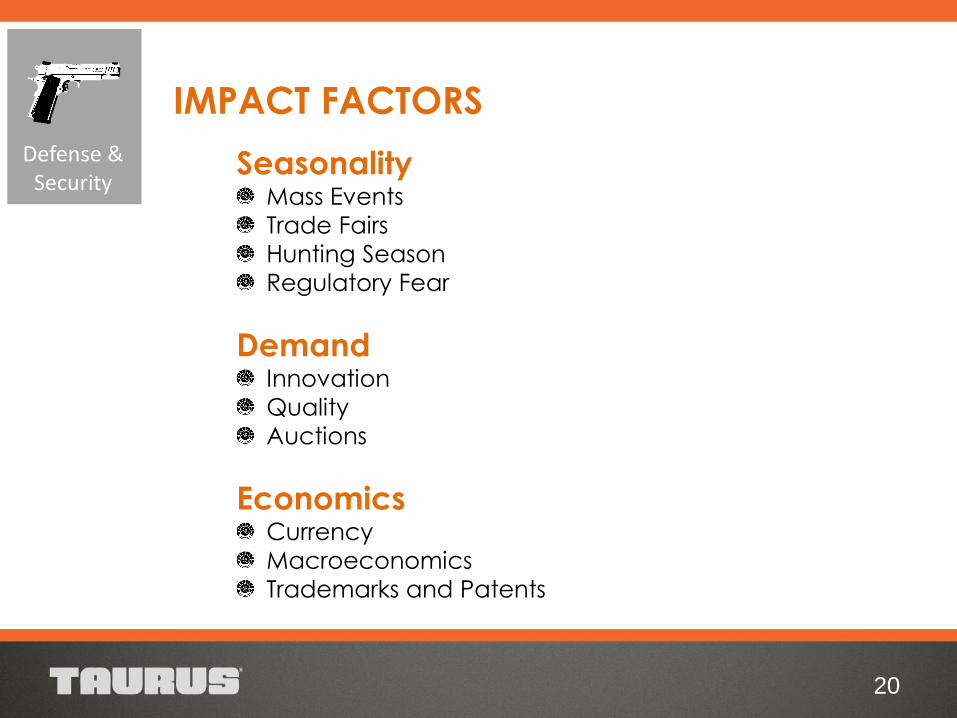

IMPACT FACTORS

20

Defense & Security

Seasonality Mass Events

Trade Fairs

Hunting Season

Regulatory Fear

Demand Innovation

Quality

Auctions

Economics Currency

Macroeconomics

Trademarks and Patents

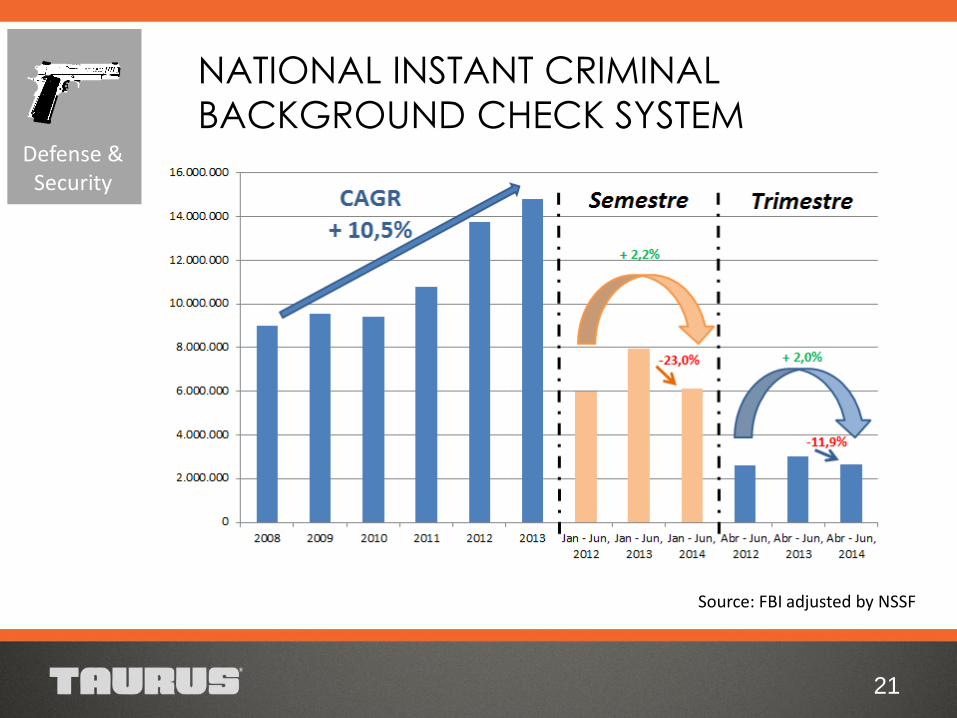

NATIONAL INSTANT CRIMINAL

BACKGROUND CHECK SYSTEM

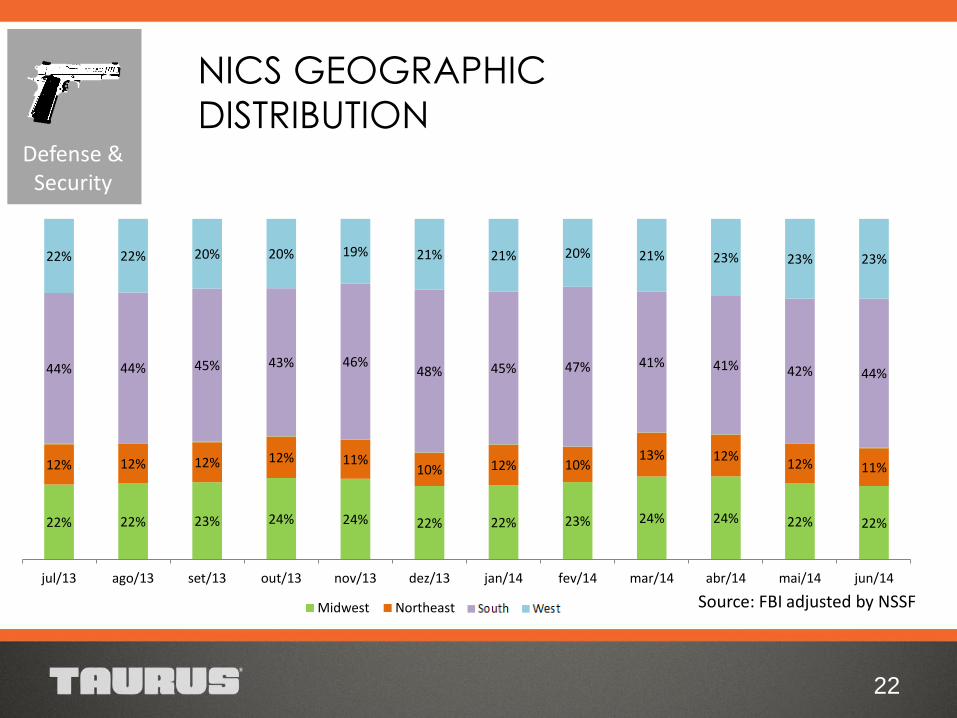

21

Defense & Security

Source: FBI adjusted by NSSF

22% 22% 23% 24% 24% 22% 22% 23% 24% 24% 22% 22%

12% 12% 12% 12% 11% 10% 12% 10%

13% 12% 12% 11%

44% 44% 45% 43% 46% 48% 45% 47% 41% 41% 42% 44%

22% 22% 20% 20% 19% 21% 21% 20% 21% 23% 23% 23%

jul/13 ago/13 set/13 out/13 nov/13 dez/13 jan/14 fev/14 mar/14 abr/14 mai/14 jun/14

Midwest Northeast Other South West

NICS GEOGRAPHIC

DISTRIBUTION

22

Defense & Security

Source: FBI adjusted by NSSF

PEERS

23

Defense & Security

PRODUCTION

24

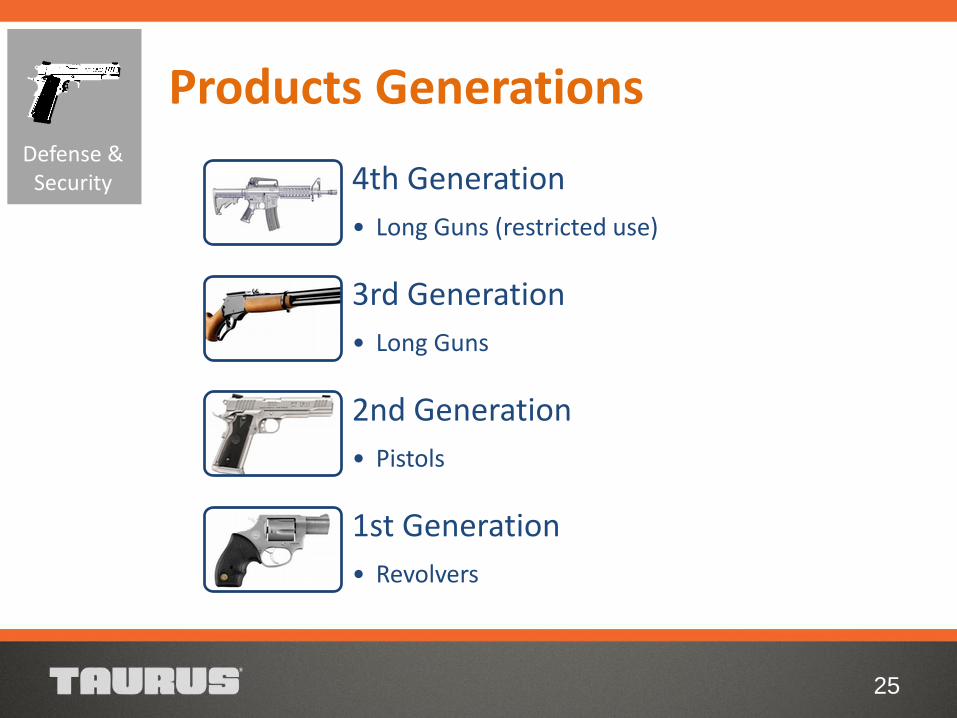

25

Defense & Security 4th Generation

• Long Guns (restricted use)

3rd Generation

• Long Guns

2nd Generation

• Pistols

1st Generation

• Revolvers

Products Generations

MARKETING &

SALES

26

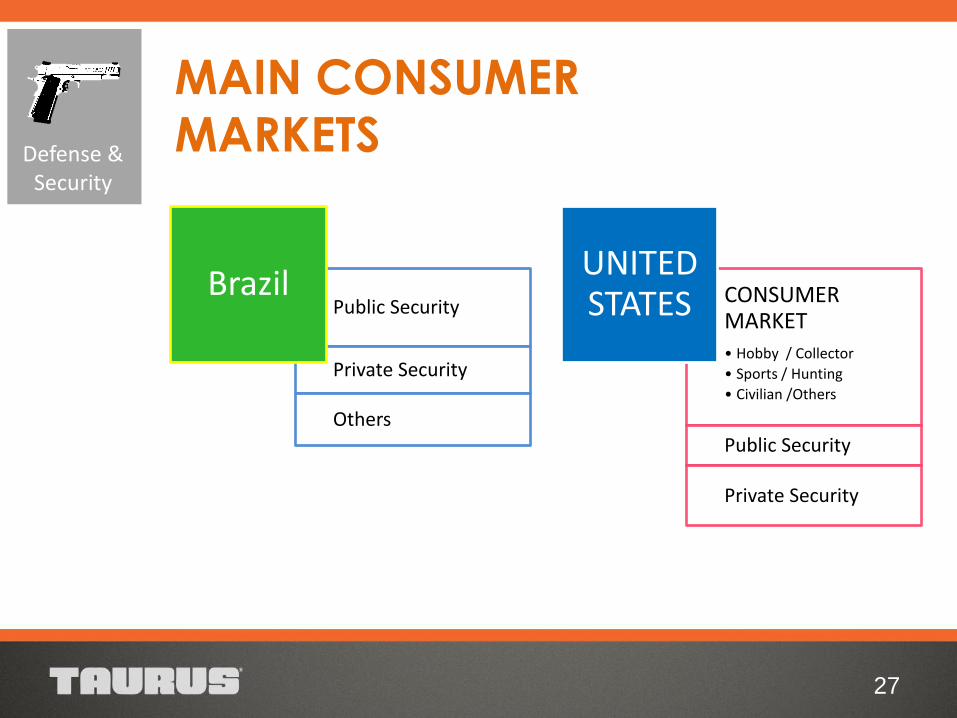

27

Public Security

Private Security

Others

Brazil CONSUMER MARKET

• Hobby / Collector

• Sports / Hunting

• Civilian /Others

Public Security

Private Security

UNITED STATES

MAIN CONSUMER

MARKETS Defense & Security

28

2012 FIELD & STREAM BEST OF THE BEST AWARD TAURUS TRACKER 992

2011 NRA: HANDGUN OF THE YEAR

PT 740 SLIM

2013 MANUFACTURER OF THE YEAR

TAURUS INTERNATIONAL MFG, INC.

AWARDS

Defense & Security

29

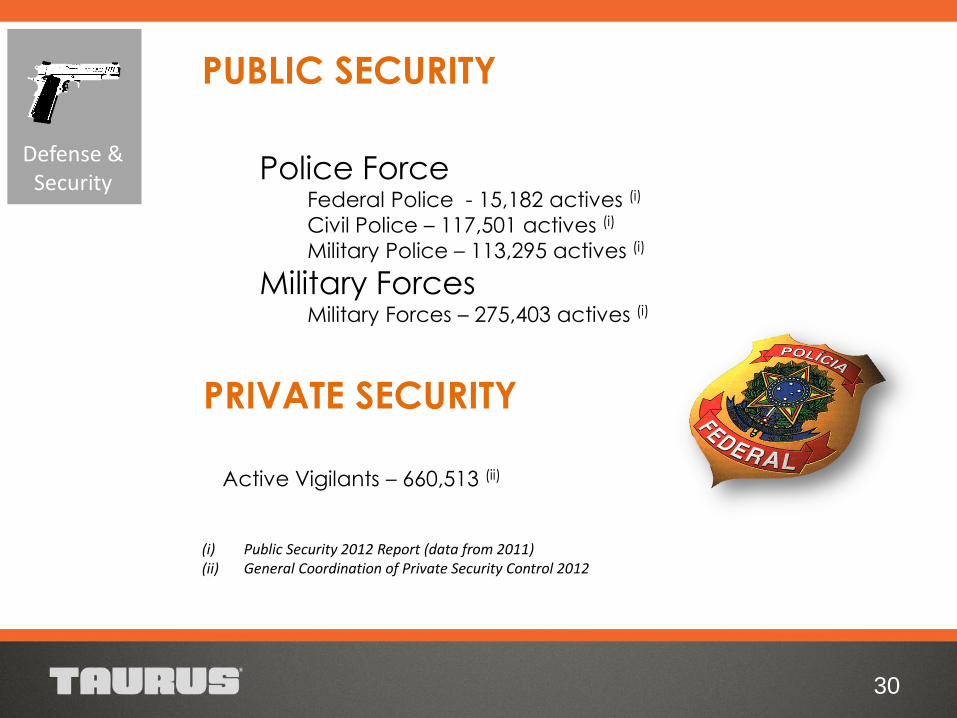

Police Force Federal Police - 15,182 actives (i)

Civil Police – 117,501 actives (i)

Military Police – 113,295 actives (i)

Military Forces Military Forces – 275,403 actives (i)

PUBLIC SECURITY

PRIVATE SECURITY

30

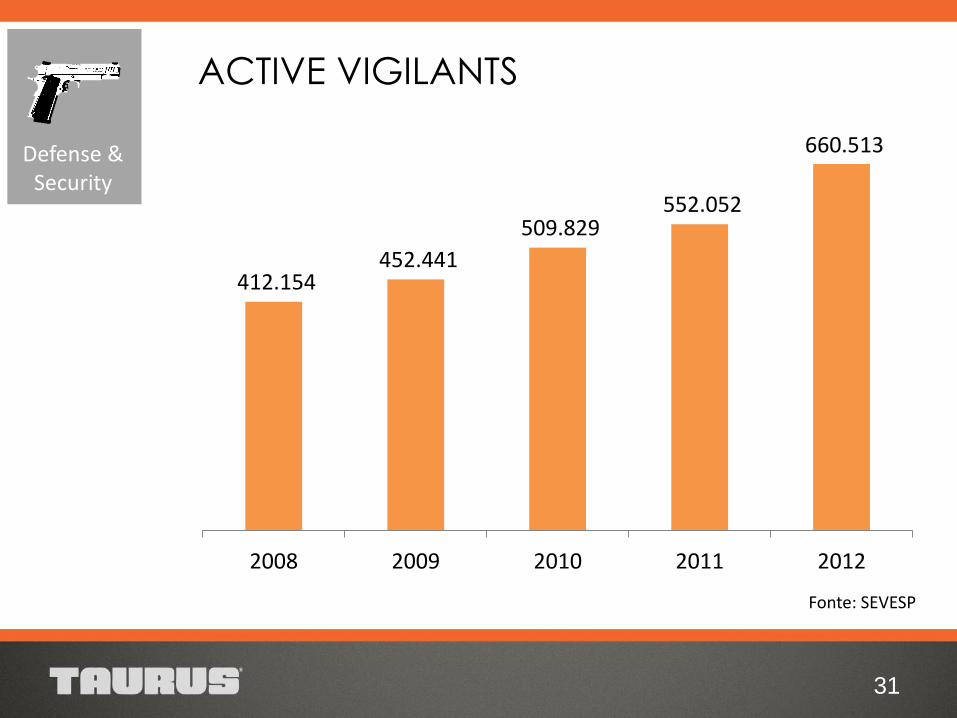

Active Vigilants – 660,513 (ii)

(i) Public Security 2012 Report (data from 2011) (ii) General Coordination of Private Security Control 2012

Defense & Security

31

412.154 452.441

509.829 552.052

660.513

2008 2009 2010 2011 2012

ACTIVE VIGILANTS

Defense & Security

Fonte: SEVESP

90% OF MARKET SHARE HANDGUNS IN

BRAZIL

PEERS: CBC AND IMBEL 10% OF MARKET

SHARE

32

Defense & Security

FOREIGN MARKET

33

34

CARRY ON MOVEMENT

World Champion

Speed Shooter 2013 Jessie Harrison Athlete – Taurus’ team leader

Taurus International Manufacturing Inc. initiative to

encourage the concealed carry guns and the shooting

sports.

Defense & Security

35

Considered a breakthrough in shooting sports, Alex Larch is the new member of Taurus team lead by Jessie Duff

Alex Larche

Taurus offers to its customers a new concept in packaging, providing greater security and perceived quality.

White Box

CARRY ON MOVEMENT

Defense & Security

Taurus cares about its consumers: new Customer Service

extended to all american territory.

36

CARRY ON MOVEMENT

Defense & Security

EXPORTS FOR

MORE THAN

70 COUNTRIES 37

Defense & Security

38

Company Defense & Security

Metallurgy & Plastics

Guidance Results Strategies

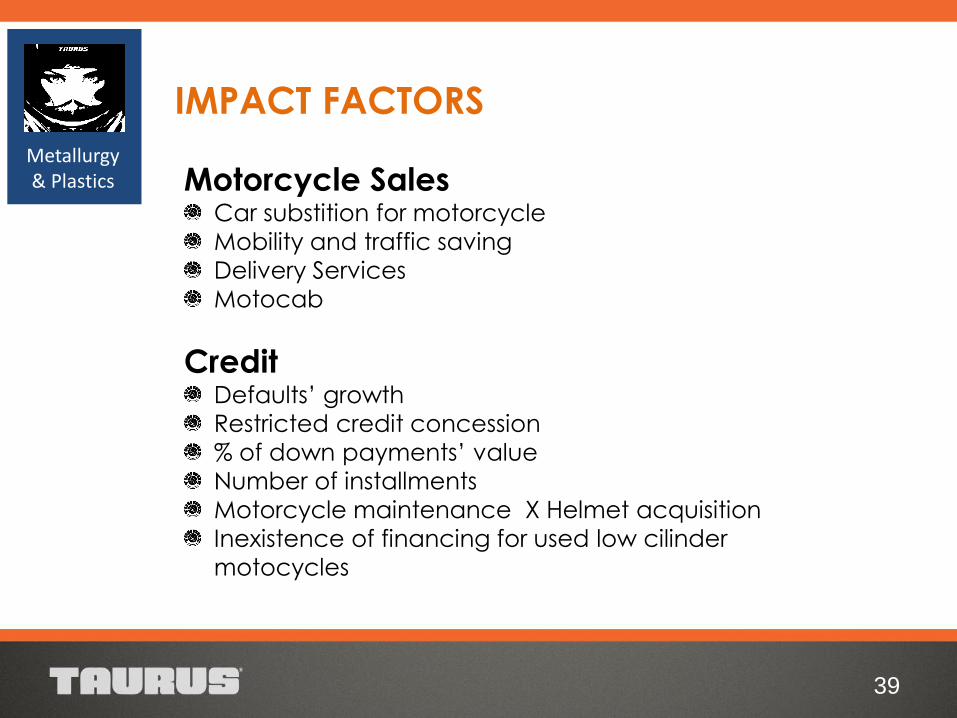

IMPACT FACTORS

39

Metallurgy & Plastics Motorcycle Sales

Car substition for motorcycle

Mobility and traffic saving

Delivery Services

Motocab

Credit Defaults’ growth

Restricted credit concession

% of down payments’ value

Number of installments

Motorcycle maintenance X Helmet acquisition

Inexistence of financing for used low cilinder

motocycles

0

5.000.000

10.000.000

15.000.000

20.000.000

25.000.000

0

50.000

100.000

150.000

200.000

250.000

300.000

dez

/02

abr/

03

ago

/03

dez

/03

abr/

04

ago

/04

dez

/04

abr/

05

ago

/05

dez

/05

abr/

06

ago

/06

dez

/06

abr/

07

ago

/07

dez

/07

abr/

08

ago

/08

dez

/08

abr/

09

ago

/09

dez

/09

abr/

10

ago

/10

dez

/10

abr/

11

ago

/11

dez

/11

abr/

12

ago

/12

dez

/12

abr/

13

ago

/13

dez

/13

abr/

14

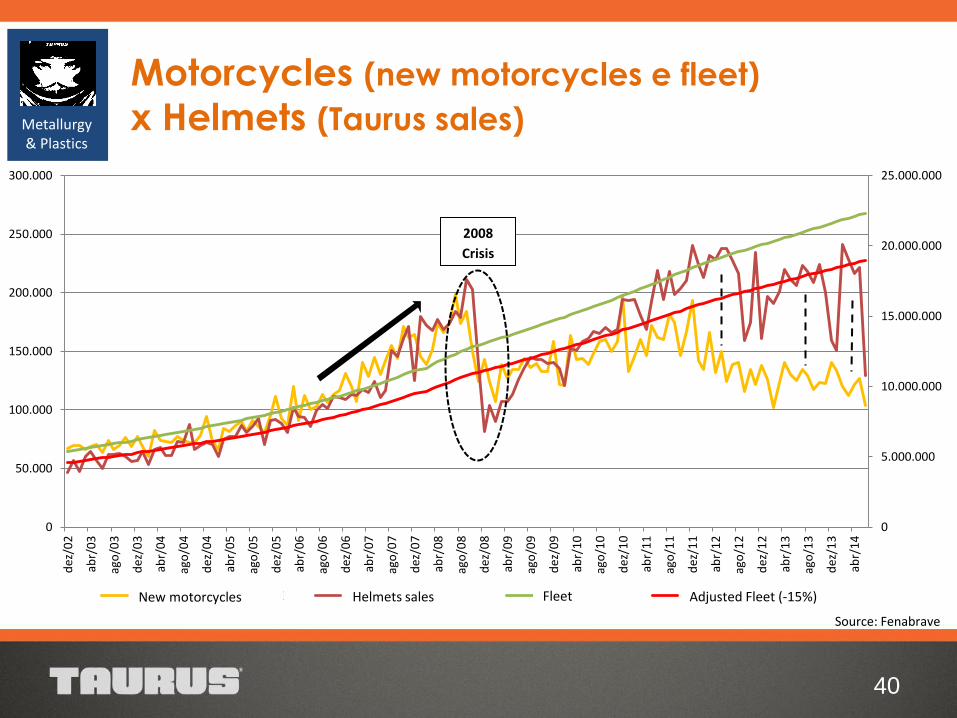

Emplacamentos FENABRAVE Venda Capacetes Taurus Frota Circulante Frota Circulante Ajustada (-15%)

2008

Crisis

40

Motorcycles (new motorcycles e fleet)

x Helmets (Taurus sales)

Source: Fenabrave

Metallurgy & Plastics

New motorcycles Helmets sales Fleet Adjusted Fleet (-15%)

41

Source: Denatran and FENABRAVE

Motorcycles (new motorcycles e fleet) Metallurgy & Plastics

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

0

5.000.000

10.000.000

15.000.000

20.000.000

25.000.000

Motorcycles Fleet x New Motorcycles

Frota Circulante Emplacamentos FENABRAVE

7%

15%

25%

33%

13%

-16%

12% 8%

-16%

-7% -2%

14% 14% 16% 18% 17%

12% 12% 12% 9% 8%

3%

-20%

-10%

0%

10%

20%

30%

40%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

Growth Rates New Motorcycles x Fleet

Crescimento de Emplacamentos Crescimento da Frota

*2014 new motorcycles LTM until June/2014

New Motorcycles Fleet Motorcycles Growth Rate Fleet Growth Rate

42

Source: Taurus

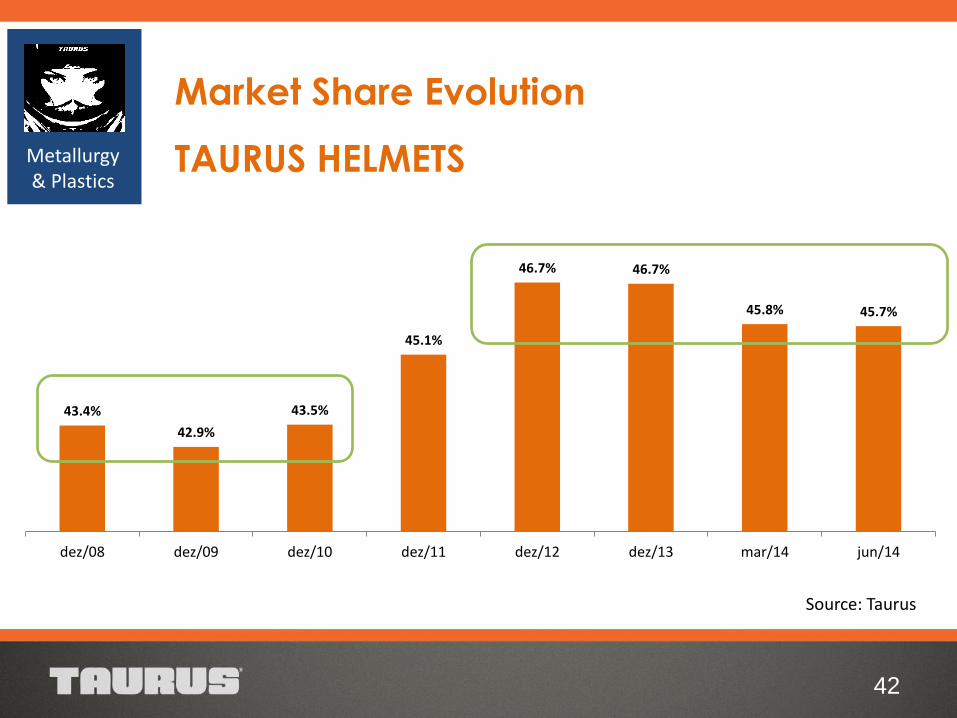

Market Share Evolution

TAURUS HELMETS Metallurgy & Plastics

43.4%

42.9%

43.5%

45.1%

46.7% 46.7%

45.8% 45.7%

dez/08 dez/09 dez/10 dez/11 dez/12 dez/13 mar/14 jun/14

IN BRAZIL, ON AVERAGE, ARE

1.5 HELMETS

PER MOTORCYCLE FLEET

WITH REPLACEMENT

EVERY 6 YEARS

43

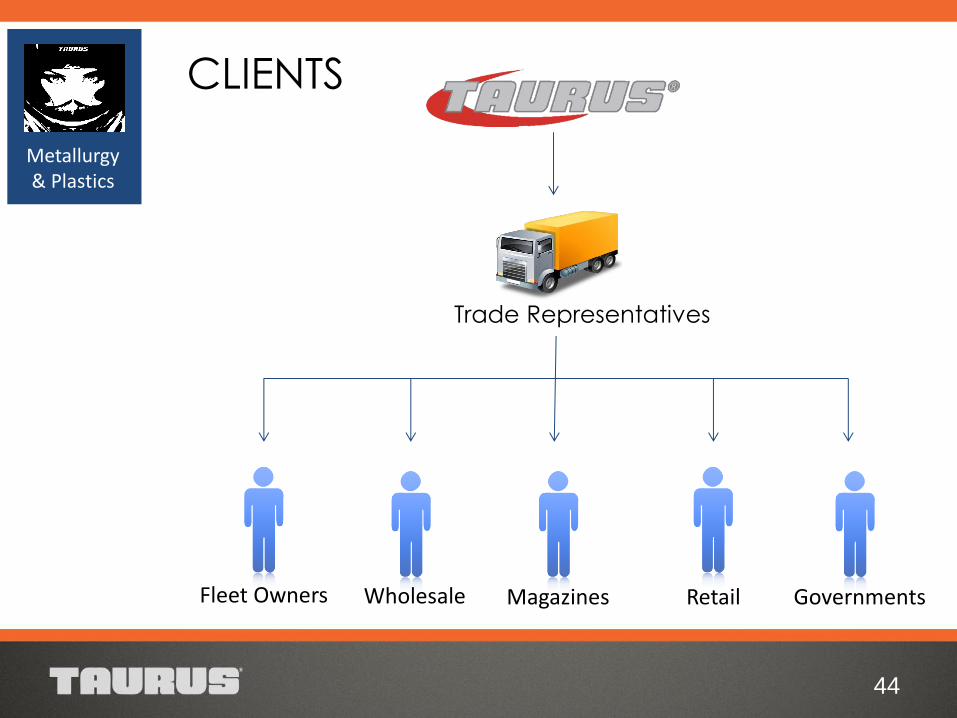

Metallurgy & Plastics

Retail Wholesale Magazines Fleet Owners Governments

Trade Representatives

CLIENTS

44

Metallurgy & Plastics

45

Metallurgy & Plastics

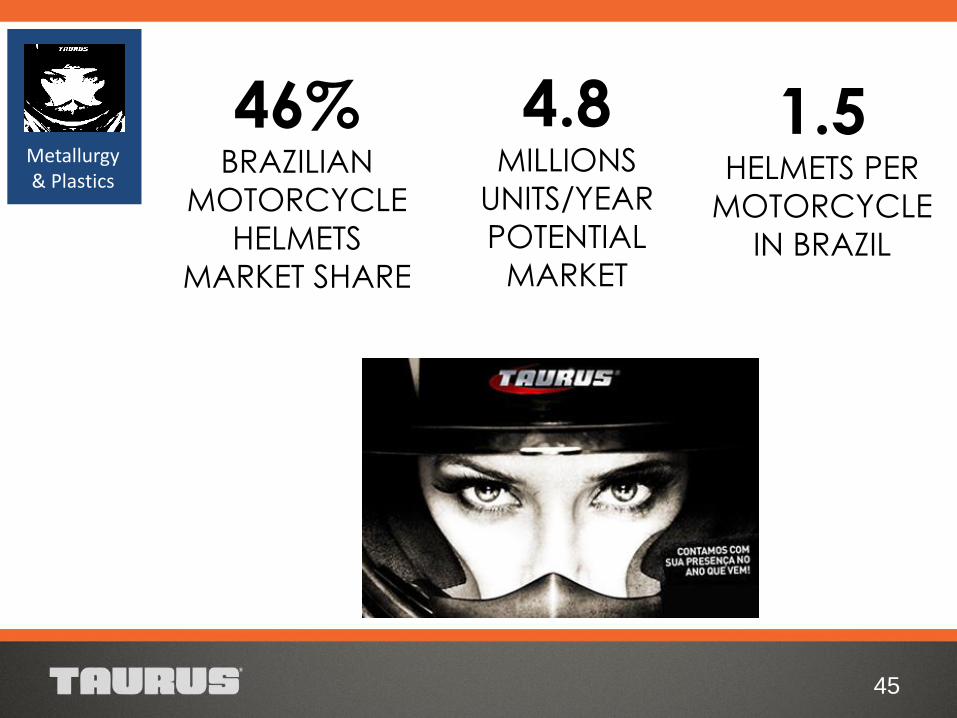

46%

BRAZILIAN

MOTORCYCLE

HELMETS

MARKET SHARE

1.5 HELMETS PER

MOTORCYCLE

IN BRAZIL

4.8 MILLIONS

UNITS/YEAR

POTENTIAL

MARKET

Redesign the helmet

sales success:

SAN MARINO,

the model is smaller,

lighter,

with better aerodynamics,

maintaining the large peripheral vision.

46

Metallurgy & Plastics

TAURUS HELMETS

FOR CYCLING

47

Metallurgy & Plastics

Urban Mobility

Environmental Consciousness

NEW!

48

NEW!

“Brazilian leader in helmets manufacturing, Taurus

expands its portfolio with the launchof new features for

motorcycles medium and high displacement. By now,

the brand offers a complete TOP line of helmets

developed in partnership with

Italian company Caberg ”

- MOTO.com.br

Metallurgy & Plastics

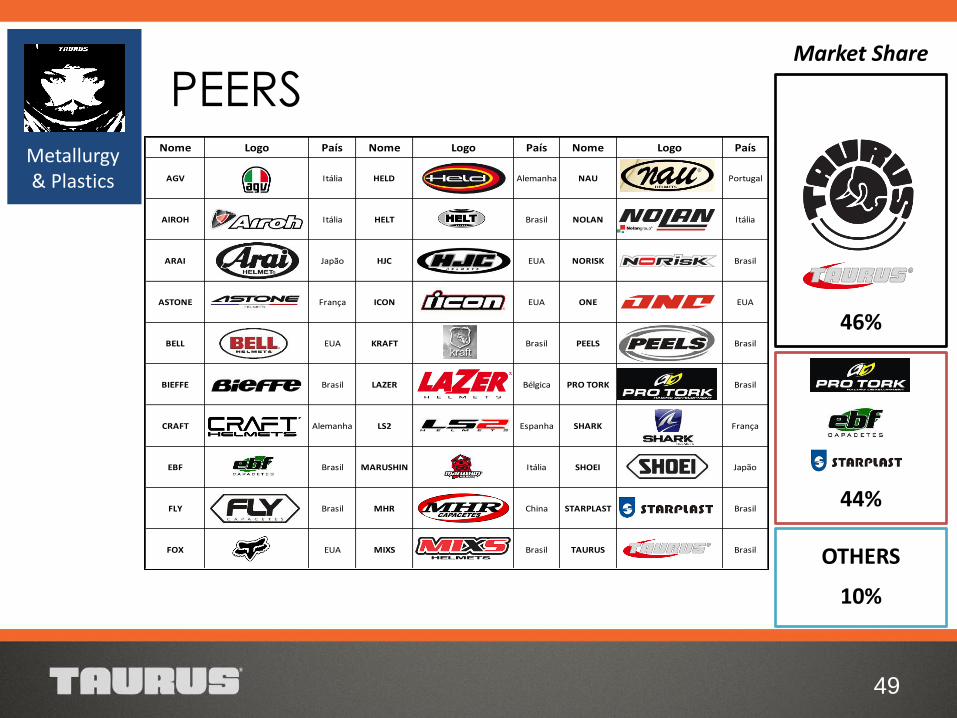

PEERS

49

Metallurgy & Plastics

46%

44%

10%

OTHERS

Market Share

Nome Logo País Nome Logo País Nome Logo País

AGV Itália HELD Alemanha NAU Portugal

AIROH Itália HELT Brasil NOLAN Itália

ARAI Japão HJC EUA NORISK Brasil

ASTONE França ICON EUA ONE EUA

BELL EUA KRAFT Brasil PEELS Brasil

BIEFFE Brasil LAZER Bélgica PRO TORK Brasil

CRAFT Alemanha LS2 Espanha SHARK França

EBF Brasil MARUSHIN Itália SHOEI Japão

FLY Brasil MHR China STARPLAST Brasil

FOX EUA MIXS Brasil TAURUS Brasil

HARLEY-

DAVIDSONEUA MT Espanha VAZ Brasil

COMPETITIVE ADVANTAGES

Quality

Raw material from recognized suppliers

Compliance with brazilian quality standard (NBR 7471/2001)

Adaptation to european standards

Production scale

Design

Updated and innovative design

Artwork with excellent finishing

50

Metallurgy & Plastics

Safety traffic campaign

Participation in associations

like APAE, ABAI and

others

Recycling events and

adaptation to Environmental

Institute of Paraná

ENVIRONMENTAL CONSCIOUSNESS

51

Metallurgy & Plastics

A NEW CONSCIOUSNESS

IN COLLECTION

52

Metallurgy & Plastics

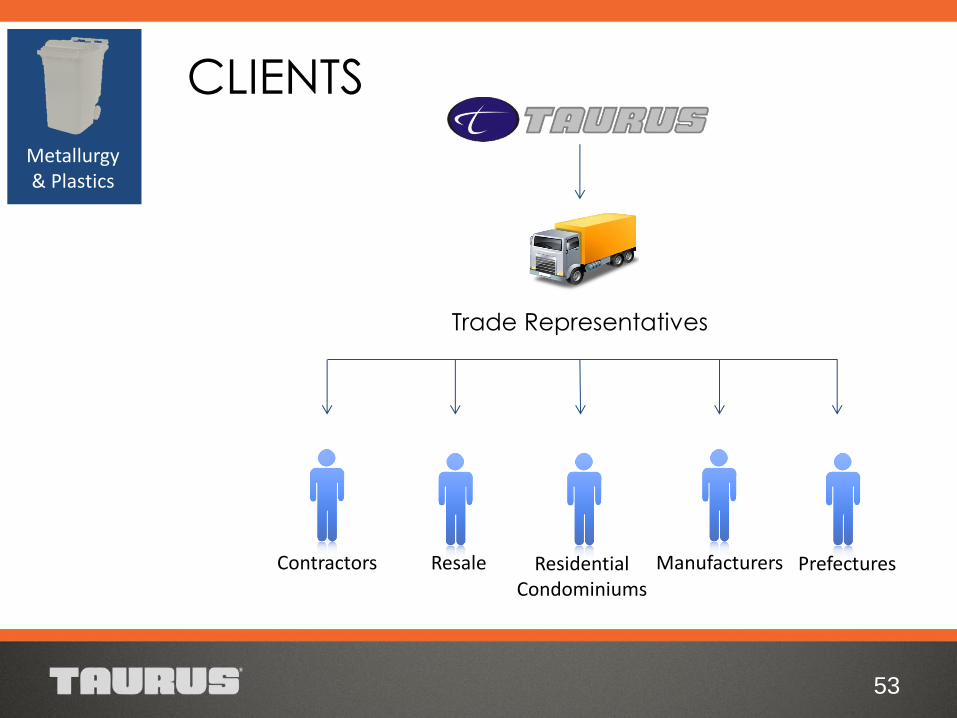

CLIENTS

Trade Representatives

Contractors Resale Residential Condominiums

Manufacturers Prefectures

53

Metallurgy & Plastics

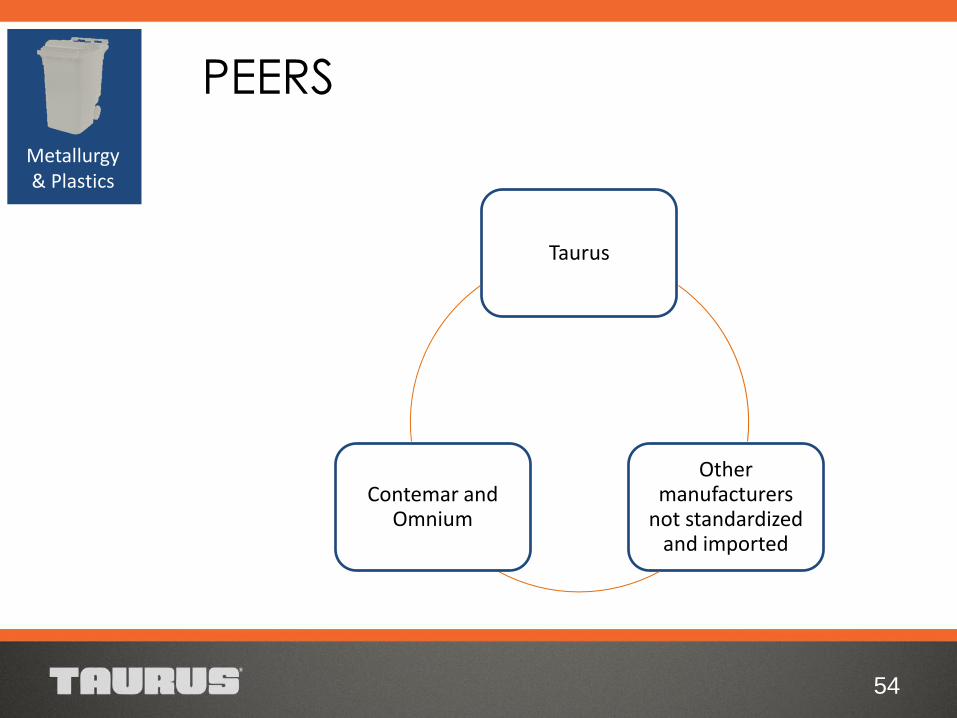

Taurus

Other manufacturers

not standardized and imported

Contemar and Omnium

PEERS

54

Metallurgy & Plastics

TO PROTECT YOUR LIFE,

COUNT ON TAURUS

BULLETPROOF VESTS

55

Metallurgy & Plastics

M.I.M. (METAL INJECTION MOLDING) IS TECHNOLOGY

ON TAURUS’ PRODUCTS

56

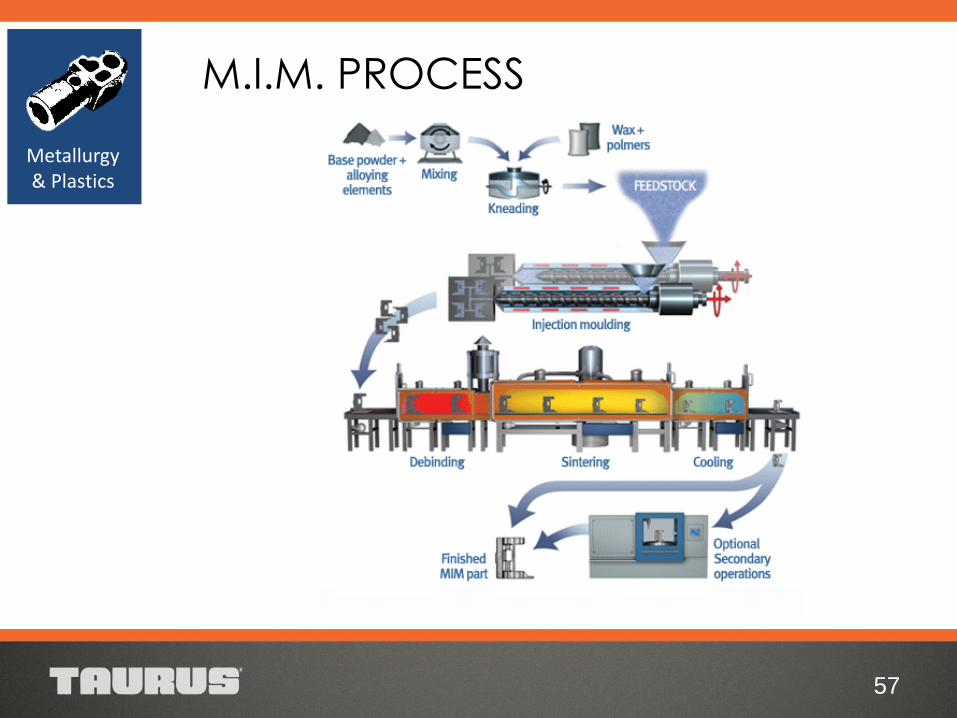

Metallurgy & Plastics

M.I.M. PROCESS

57

Metallurgy & Plastics

58

MAIN M.I.M. CLIENTS

DEFENSE & SECURITY

OTHERS

Metallurgy & Plastics

TAURUS TOOLS PREMIUM

LINE.

QUALITY AND INNOVATION

PARTICIPATION OF 35% IN

ASSOCIATED

59

Metallurgy & Plastics

60

Company Defense & Security

Metallurgy & Plastics

Guidance Results Strategies

ECONOMIC AND FINANCIAL

INDICATORS

61

Results

In BRL millions

Variation %

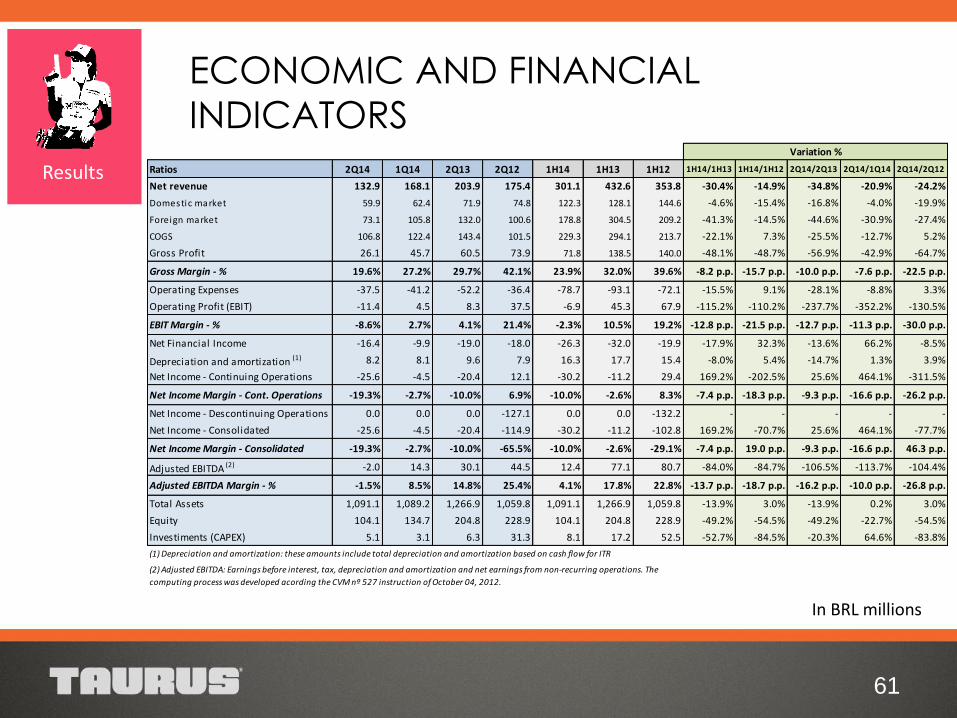

Ratios 2Q14 1Q14 2Q13 2Q12 1H14 1H13 1H12 1H14/1H13 1H14/1H12 2Q14/2Q13 2Q14/1Q14 2Q14/2Q12

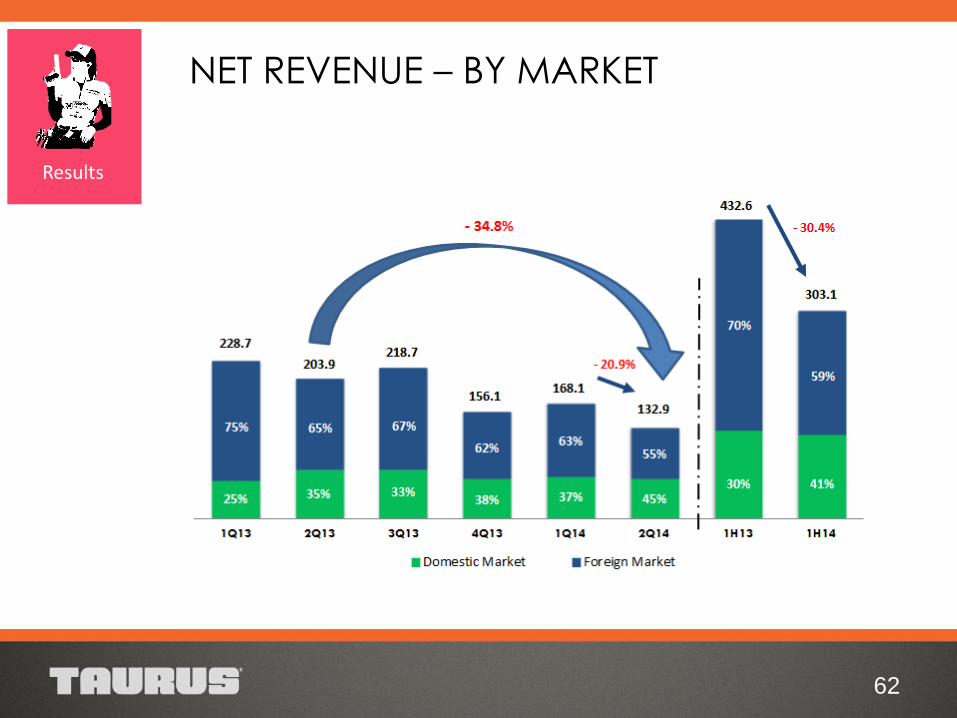

Net revenue 132.9 168.1 203.9 175.4 301.1 432.6 353.8 -30.4% -14.9% -34.8% -20.9% -24.2%

Domestic market 59.9 62.4 71.9 74.8 122.3 128.1 144.6 -4.6% -15.4% -16.8% -4.0% -19.9%

Foreign market 73.1 105.8 132.0 100.6 178.8 304.5 209.2 -41.3% -14.5% -44.6% -30.9% -27.4%

COGS 106.8 122.4 143.4 101.5 229.3 294.1 213.7 -22.1% 7.3% -25.5% -12.7% 5.2%

Gross Profit 26.1 45.7 60.5 73.9 71.8 138.5 140.0 -48.1% -48.7% -56.9% -42.9% -64.7%

Gross Margin - % 19.6% 27.2% 29.7% 42.1% 23.9% 32.0% 39.6% -8.2 p.p. -15.7 p.p. -10.0 p.p. -7.6 p.p. -22.5 p.p.

Operating Expenses -37.5 -41.2 -52.2 -36.4 -78.7 -93.1 -72.1 -15.5% 9.1% -28.1% -8.8% 3.3%

Operating Profit (EBIT) -11.4 4.5 8.3 37.5 -6.9 45.3 67.9 -115.2% -110.2% -237.7% -352.2% -130.5%

EBIT Margin - % -8.6% 2.7% 4.1% 21.4% -2.3% 10.5% 19.2% -12.8 p.p. -21.5 p.p. -12.7 p.p. -11.3 p.p. -30.0 p.p.

Net Financial Income -16.4 -9.9 -19.0 -18.0 -26.3 -32.0 -19.9 -17.9% 32.3% -13.6% 66.2% -8.5%

Depreciation and amortization (1) 8.2 8.1 9.6 7.9 16.3 17.7 15.4 -8.0% 5.4% -14.7% 1.3% 3.9%

Net Income - Continuing Operations -25.6 -4.5 -20.4 12.1 -30.2 -11.2 29.4 169.2% -202.5% 25.6% 464.1% -311.5%

Net Income Margin - Cont. Operations -19.3% -2.7% -10.0% 6.9% -10.0% -2.6% 8.3% -7.4 p.p. -18.3 p.p. -9.3 p.p. -16.6 p.p. -26.2 p.p.

Net Income - Descontinuing Operations 0.0 0.0 0.0 -127.1 0.0 0.0 -132.2 - - - - -

Net Income - Consolidated -25.6 -4.5 -20.4 -114.9 -30.2 -11.2 -102.8 169.2% -70.7% 25.6% 464.1% -77.7%

Net Income Margin - Consolidated -19.3% -2.7% -10.0% -65.5% -10.0% -2.6% -29.1% -7.4 p.p. 19.0 p.p. -9.3 p.p. -16.6 p.p. 46.3 p.p.

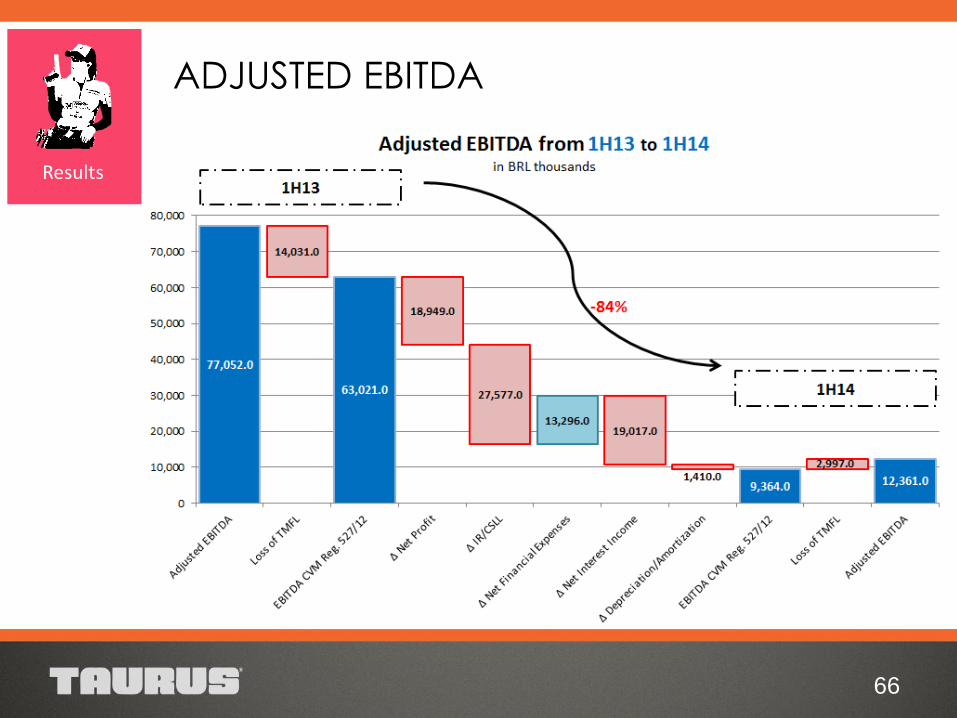

Adjusted EBITDA (2) -2.0 14.3 30.1 44.5 12.4 77.1 80.7 -84.0% -84.7% -106.5% -113.7% -104.4%

Adjusted EBITDA Margin - % -1.5% 8.5% 14.8% 25.4% 4.1% 17.8% 22.8% -13.7 p.p. -18.7 p.p. -16.2 p.p. -10.0 p.p. -26.8 p.p.

Total Assets 1,091.1 1,089.2 1,266.9 1,059.8 1,091.1 1,266.9 1,059.8 -13.9% 3.0% -13.9% 0.2% 3.0%

Equity 104.1 134.7 204.8 228.9 104.1 204.8 228.9 -49.2% -54.5% -49.2% -22.7% -54.5%

Investiments (CAPEX) 5.1 3.1 6.3 31.3 8.1 17.2 52.5 -52.7% -84.5% -20.3% 64.6% -83.8%

(1) Depreciation and amortization: these amounts include total depreciation and amortization based on cash flow for ITR

(2) Adjusted EBITDA: Earnings before interest, tax, depreciation and amortization and net earnings from non-recurring operations. The

computing process was developed acording the CVM nº 527 instruction of October 04, 2012.

NET REVENUE – BY MARKET

62

Results

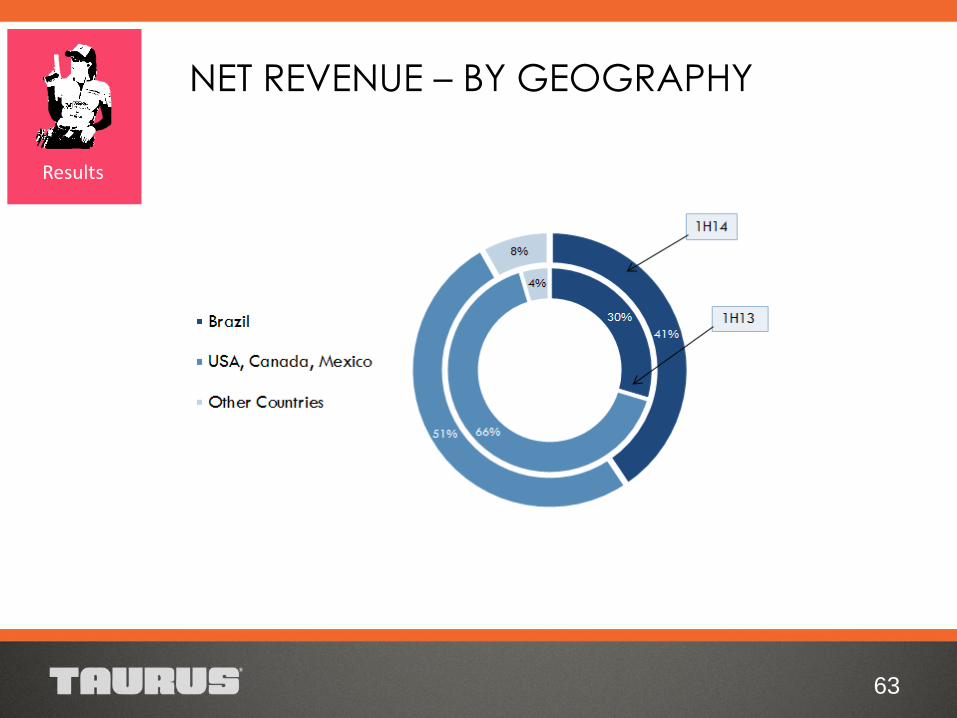

NET REVENUE – BY GEOGRAPHY

63

Results

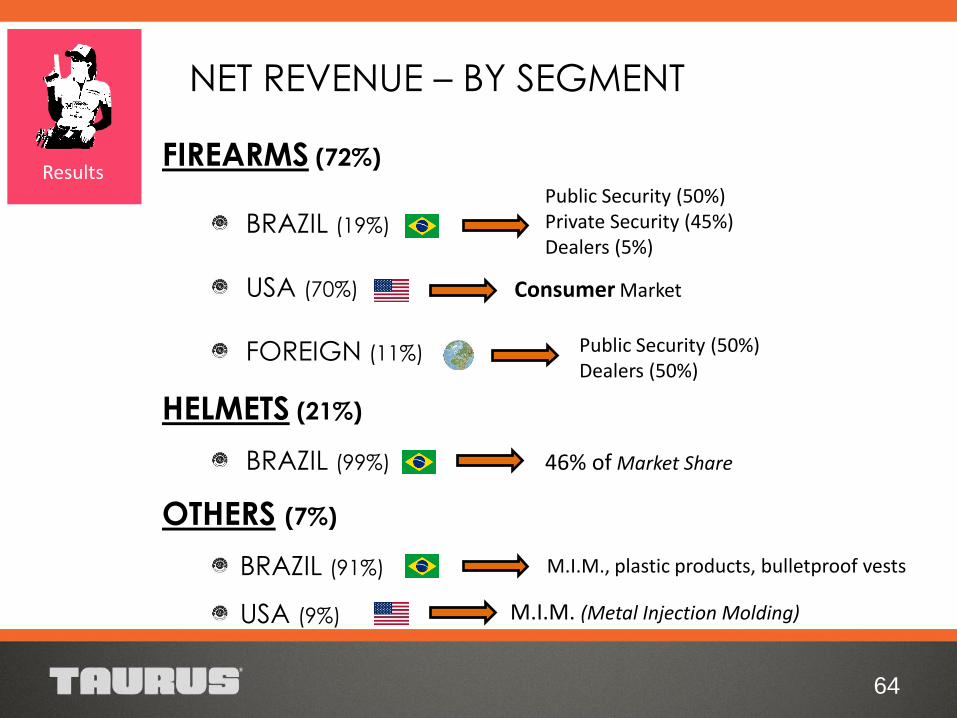

64

FIREARMS (72%)

BRAZIL (19%)

USA (70%)

FOREIGN (11%)

HELMETS (21%)

BRAZIL (99%)

OTHERS (7%)

BRAZIL (91%)

USA (9%)

Public Security (50%) Private Security (45%) Dealers (5%)

Consumer Market

Public Security (50%) Dealers (50%)

46% of Market Share

NET REVENUE – BY SEGMENT

Results

M.I.M. (Metal Injection Molding)

M.I.M., plastic products, bulletproof vests

65

Results

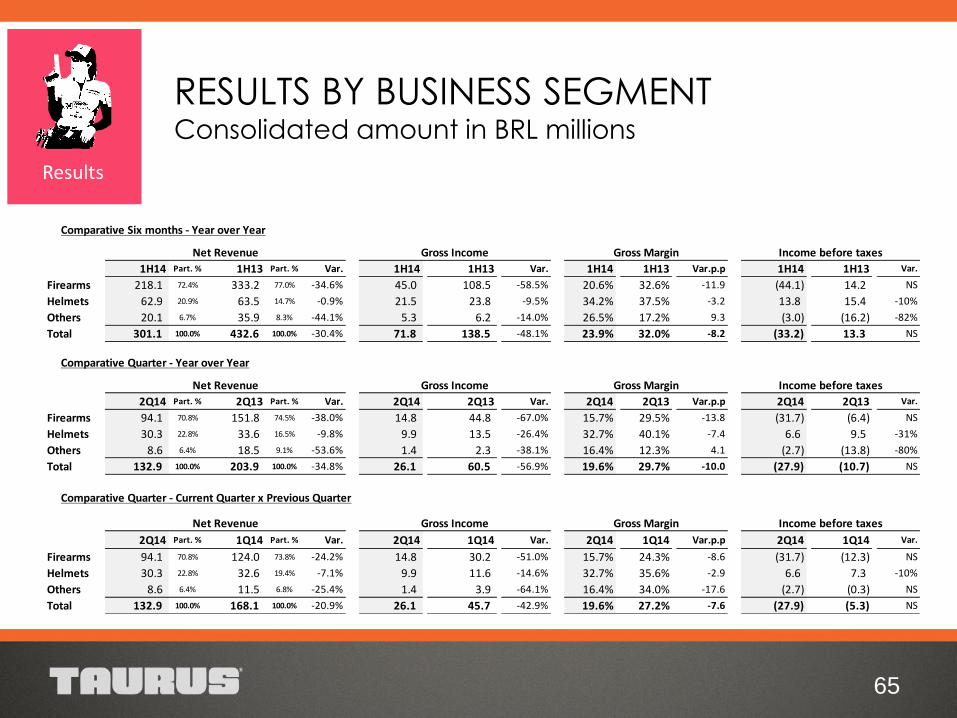

RESULTS BY BUSINESS SEGMENT Consolidated amount in BRL millions

1H14 Part. % 1H13 Part. % Var. 1H14 1H13 Var. 1H14 1H13 Var.p.p 1H14 1H13 Var.

Firearms 218.1 72.4% 333.2 77.0% -34.6% 45.0 108.5 -58.5% 20.6% 32.6% -11.9 (44.1) 14.2 NS

Helmets 62.9 20.9% 63.5 14.7% -0.9% 21.5 23.8 -9.5% 34.2% 37.5% -3.2 13.8 15.4 -10%

Others 20.1 6.7% 35.9 8.3% -44.1% 5.3 6.2 -14.0% 26.5% 17.2% 9.3 (3.0) (16.2) -82%

Total 301.1 100.0% 432.6 100.0% -30.4% 71.8 138.5 -48.1% 23.9% 32.0% -8.2 (33.2) 13.3 NS

2Q14 Part. % 2Q13 Part. % Var. 2Q14 2Q13 Var. 2Q14 2Q13 Var.p.p 2Q14 2Q13 Var.

Firearms 94.1 70.8% 151.8 74.5% -38.0% 14.8 44.8 -67.0% 15.7% 29.5% -13.8 (31.7) (6.4) NS

Helmets 30.3 22.8% 33.6 16.5% -9.8% 9.9 13.5 -26.4% 32.7% 40.1% -7.4 6.6 9.5 -31%

Others 8.6 6.4% 18.5 9.1% -53.6% 1.4 2.3 -38.1% 16.4% 12.3% 4.1 (2.7) (13.8) -80%

Total 132.9 100.0% 203.9 100.0% -34.8% 26.1 60.5 -56.9% 19.6% 29.7% -10.0 (27.9) (10.7) NS

2Q14 Part. % 1Q14 Part. % Var. 2Q14 1Q14 Var. 2Q14 1Q14 Var.p.p 2Q14 1Q14 Var.

Firearms 94.1 70.8% 124.0 73.8% -24.2% 14.8 30.2 -51.0% 15.7% 24.3% -8.6 (31.7) (12.3) NS

Helmets 30.3 22.8% 32.6 19.4% -7.1% 9.9 11.6 -14.6% 32.7% 35.6% -2.9 6.6 7.3 -10%

Others 8.6 6.4% 11.5 6.8% -25.4% 1.4 3.9 -64.1% 16.4% 34.0% -17.6 (2.7) (0.3) NS

Total 132.9 100.0% 168.1 100.0% -20.9% 26.1 45.7 -42.9% 19.6% 27.2% -7.6 (27.9) (5.3) NS

Net Revenue Gross Income Gross Margin Income before taxes

Comparative Quarter - Year over Year

Net Revenue Gross Income Gross Margin Income before taxes

Comparative Quarter - Current Quarter x Previous Quarter

Comparative Six months - Year over Year

Net Revenue Gross Income Gross Margin Income before taxes

66

Results

ADJUSTED EBITDA

67

Results

WORKING CAPITAL

68

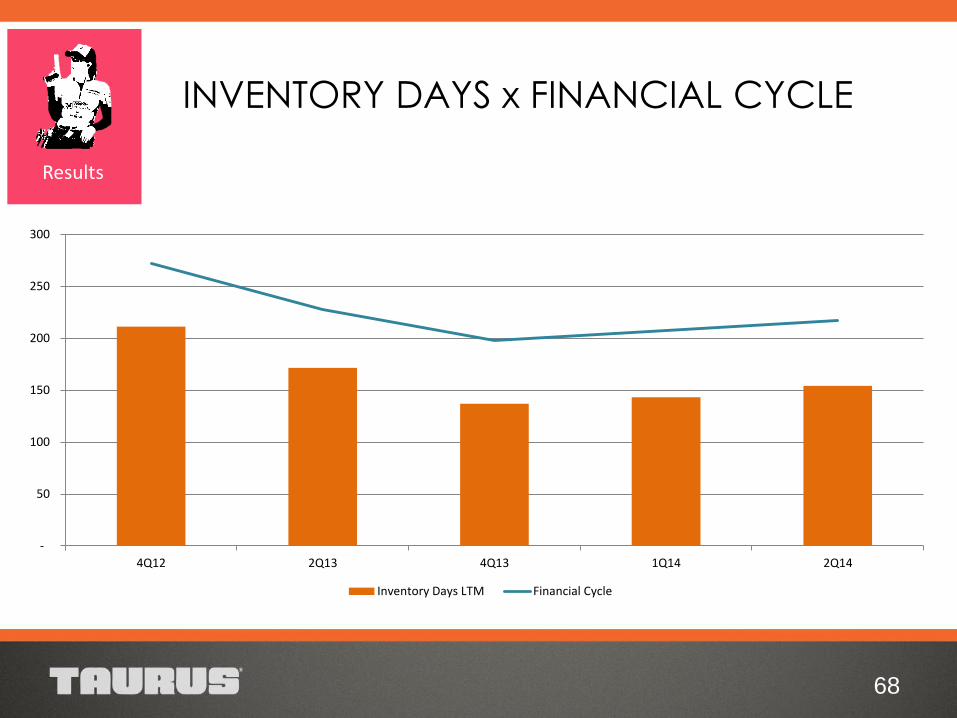

INVENTORY DAYS x FINANCIAL CYCLE

Results

-

50

100

150

200

250

300

4Q12 2Q13 4Q13 1Q14 2Q14

Inventory Days LTM Financial Cycle

69

WORKING CAPITAL NEEDS

Results

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

400.000

2011 2012 2013 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

70

Results

DEBT

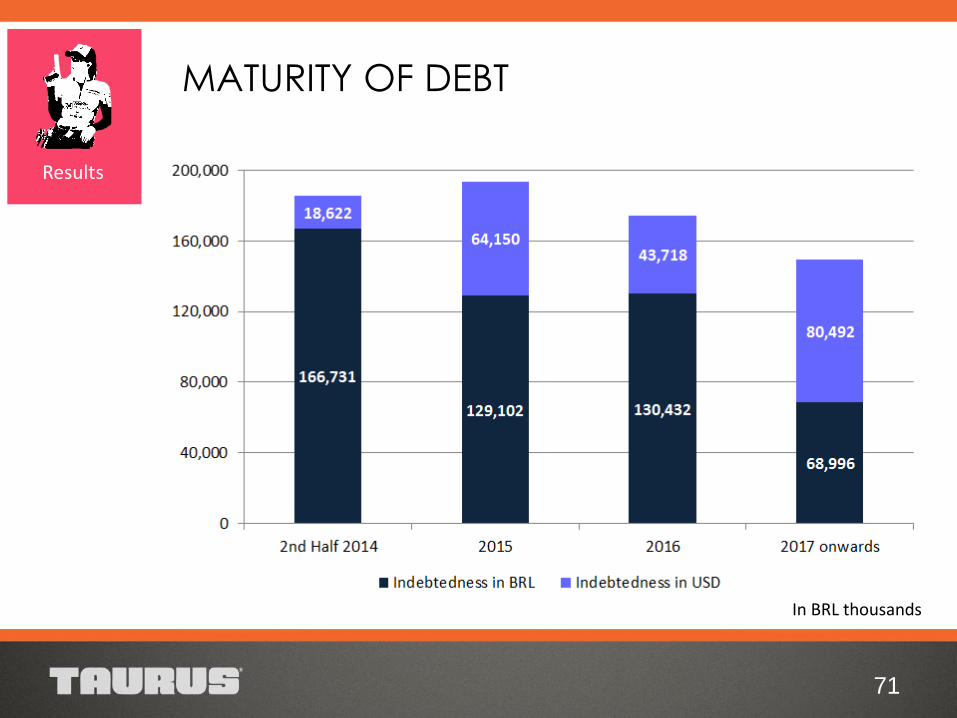

MATURITY OF DEBT

71

Results

In BRL thousands

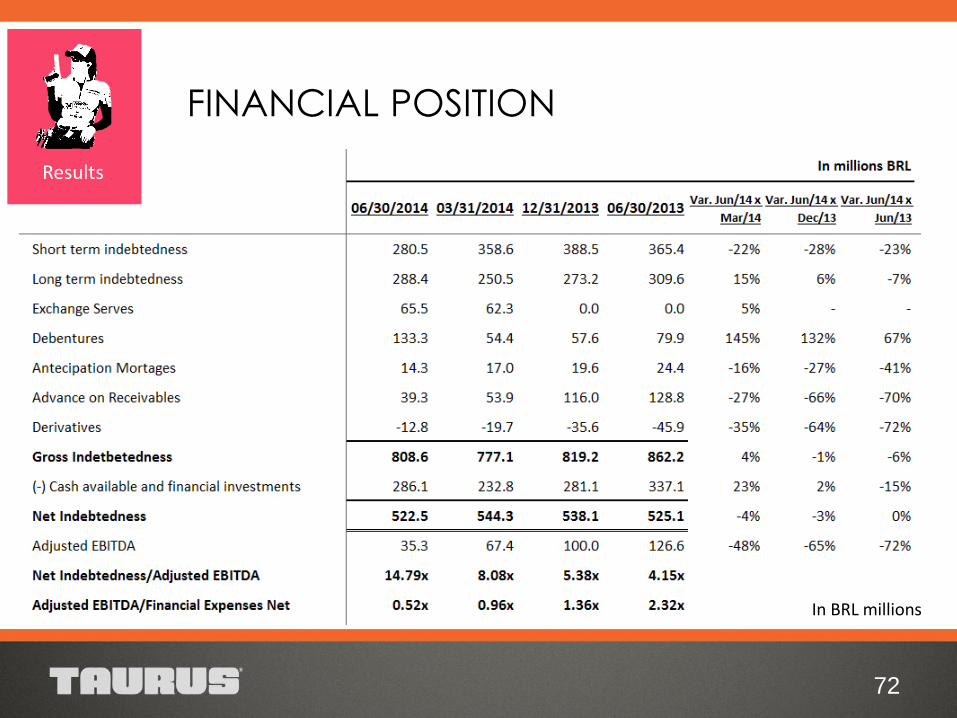

FINANCIAL POSITION

72

Results

In BRL millions

73

Results

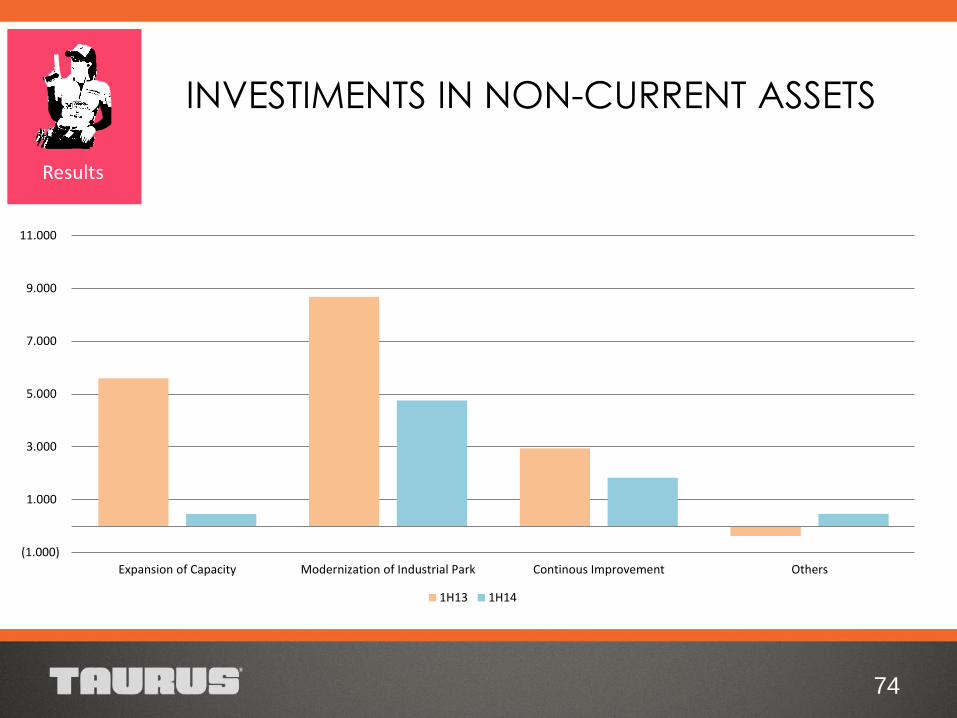

INVESTIMENTS

INVESTIMENTS IN NON-CURRENT ASSETS

74

Results

(1.000)

1.000

3.000

5.000

7.000

9.000

11.000

Expansion of Capacity Modernization of Industrial Park Continous Improvement Others

1H13 1H14

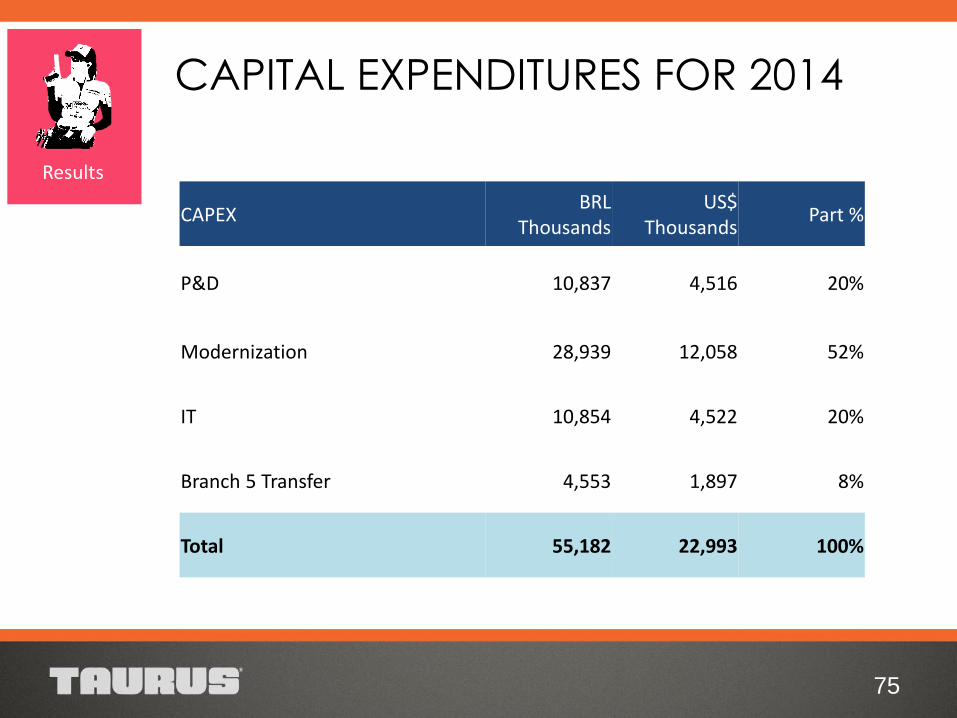

CAPITAL EXPENDITURES FOR 2014

75

Results

CAPEX BRL

Thousands US$

Thousands Part %

P&D 10,837 4,516 20%

Modernization 28,939 12,058 52%

IT 10,854 4,522 20%

Branch 5 Transfer 4,553 1,897 8%

Total 55,182 22,993 100%

76

Company Defense & Security

Metallurgy & Plastics

Guidance Results Strategies

GUIDANCE 2014

77

Guidance

The Management chose to not provide Net Revenue

and EBITDA for 2014;

CAPEX: the capital expenditures for 2014 approved in

AGM is BRL 55,2 millions, 14,7% have been done

until 1H14.

78

Company Defense & Security

Metallurgy & Plastics

Guidance Results Strategies

79

Stop selling forged to other companies: completed in

November/2013;

Transfer the long guns production to Polimetal (São

Leopoldo) in Lean concept;

Reduce the number of models (SKUs);

REESTRUCTUING ACTIONS IN PROGRESS

80

Reimplementation the Management of Manufacturing System;

Reduced costs and resources used in production;

Structuring the Supply Chain department;

Review of the entire logistics chain (use of new modes and

reducing inventories).

REESTRUCTUING ACTIONS IN PROGRESS

81

Update and introduce new modules on ERP system,

improving internal controls and management reports;

Integrate the operations between Brazil and the USA;

Expand M.I.M. markets to other markets, promoting

profitability increase of the segment;

MAIN ACTIONS FOR 2014

82

Reduce dependence on the american market by increasing

the volume of exports to other countries;

Expand supply the armed forces, taking advantage of our

condition of Strategic Defense Company;

Preparing the Company to provide services of products

maintanance.

MAIN ACTIONS FOR 2014

FELIPE G. OLIVEIRA

Investor Relations Analyst

DORIS B. F. WILHELM

Investor Relations Officer

83

EDUARDO F. COSTA

Vice-President Administrative & CFO

FORJAS TAURUS S.A. 55 51 3021 3001

www.taurusri.com.br