insurance 101 the basics - insurance institute of kentucky

TRANSCRIPT

1

© 2010 Property Casualty Insurers Association of America

Insurance 101The Basics

2

© 2010 Property Casualty Insurers Association of America

What is Insurance?

Methods of addressing uncertain risk• Avoid (don’t purchase)• Keep (don’t insure)• Transfer (purchase insurance)

Insurance is the “transfer” of uncertain financial consequences for a certain financial cost (e.g., premium)

3

© 2010 Property Casualty Insurers Association of America

How does it work?

Policy is a legal “contract of adhesion”

Insurance is for accidental/“fortuitous” events

Insurance rates “shall not be excessive, inadequate, or unfairly discriminatory”

4

© 2010 Property Casualty Insurers Association of America

Why does it work? Risks are shared among a large group

of “similarly” classified insureds

Premiums are “conservatively” invested in “liquid” instruments

“Spread of risk”

Reinsurance

5

© 2010 Property Casualty Insurers Association of America

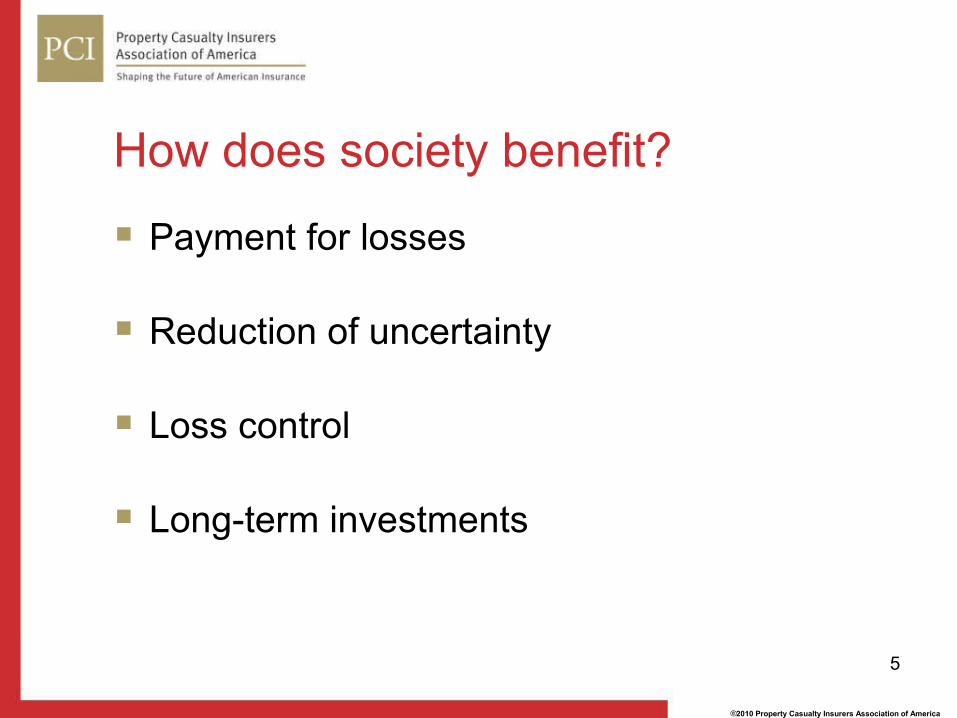

How does society benefit?

Payment for losses

Reduction of uncertainty

Loss control

Long-term investments

6

© 2010 Property Casualty Insurers Association of America

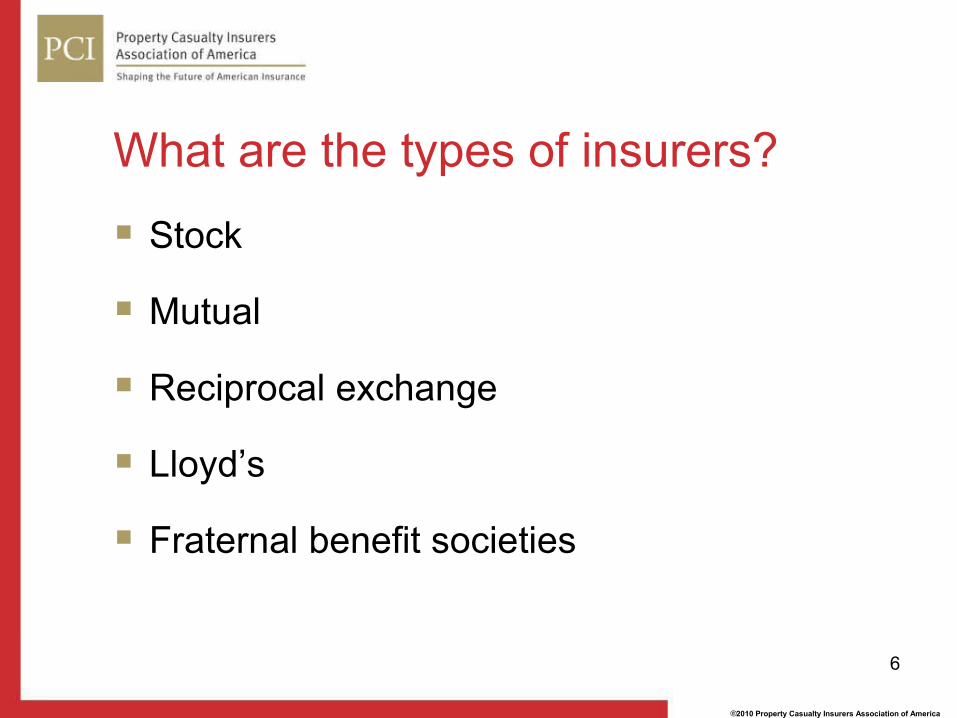

What are the types of insurers?

Stock

Mutual

Reciprocal exchange

Lloyd’s

Fraternal benefit societies

7

© 2010 Property Casualty Insurers Association of America

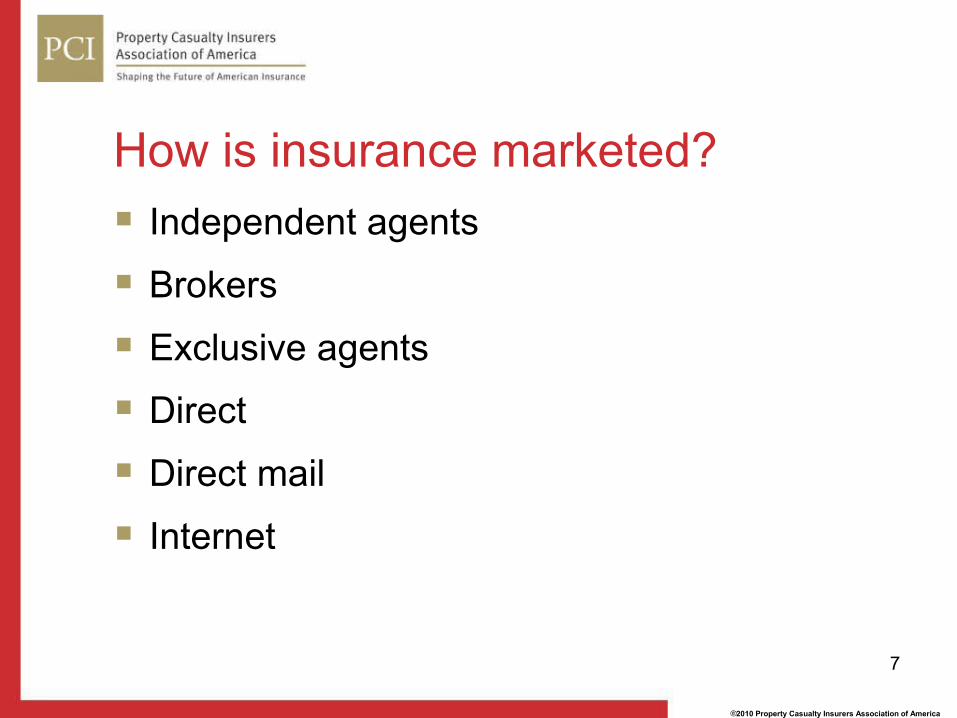

How is insurance marketed? Independent agents

Brokers

Exclusive agents

Direct

Direct mail

Internet

8

© 2010 Property Casualty Insurers Association of America

Why regulate insurance? Complex promise for future performance

Solidity

Equity and Fairness

Freedom from governmental restraint

Freedom of access to the market

9

© 2010 Property Casualty Insurers Association of America

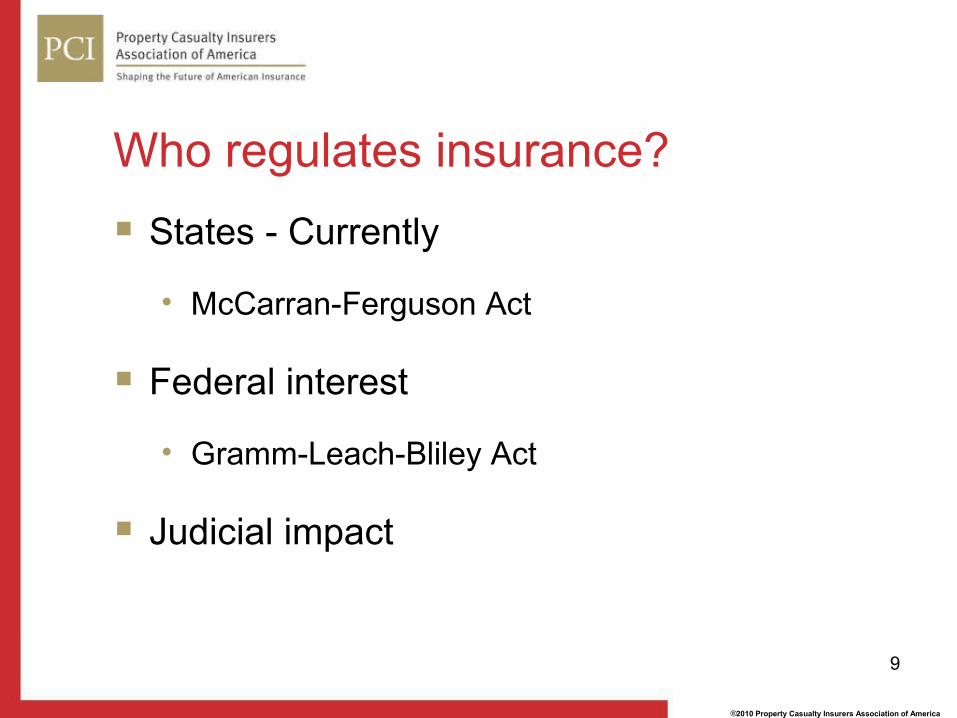

Who regulates insurance? States - Currently

• McCarran-Ferguson Act

Federal interest

• Gramm-Leach-Bliley Act

Judicial impact

10

© 2010 Property Casualty Insurers Association of America

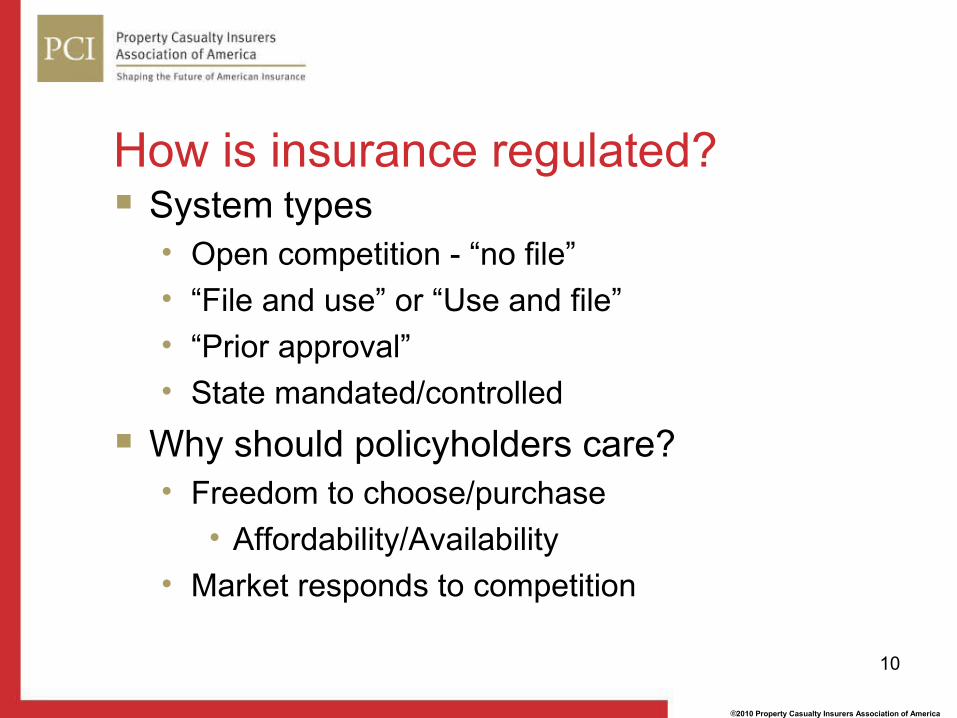

How is insurance regulated? System types

• Open competition - “no file”• “File and use” or “Use and file”• “Prior approval”• State mandated/controlled

Why should policyholders care?• Freedom to choose/purchase

• Affordability/Availability• Market responds to competition

11

© 2010 Property Casualty Insurers Association of America

So, what does all this mean? Complex and mature marketplace

• 3,100 insurers writing in the U.S.• 722 insurers writing in Kentucky

Intimate relationship with society• Delicate balance• Complex economic relationships

• Banking• Investments• Real Estate

12

© 2010 Property Casualty Insurers Association of America

What is the process? Company established Selection of market segment Development of product

• Policy• Jurisdiction• Rating/Underwriting

Sale of product Claims Settlement

13

© 2010 Property Casualty Insurers Association of America

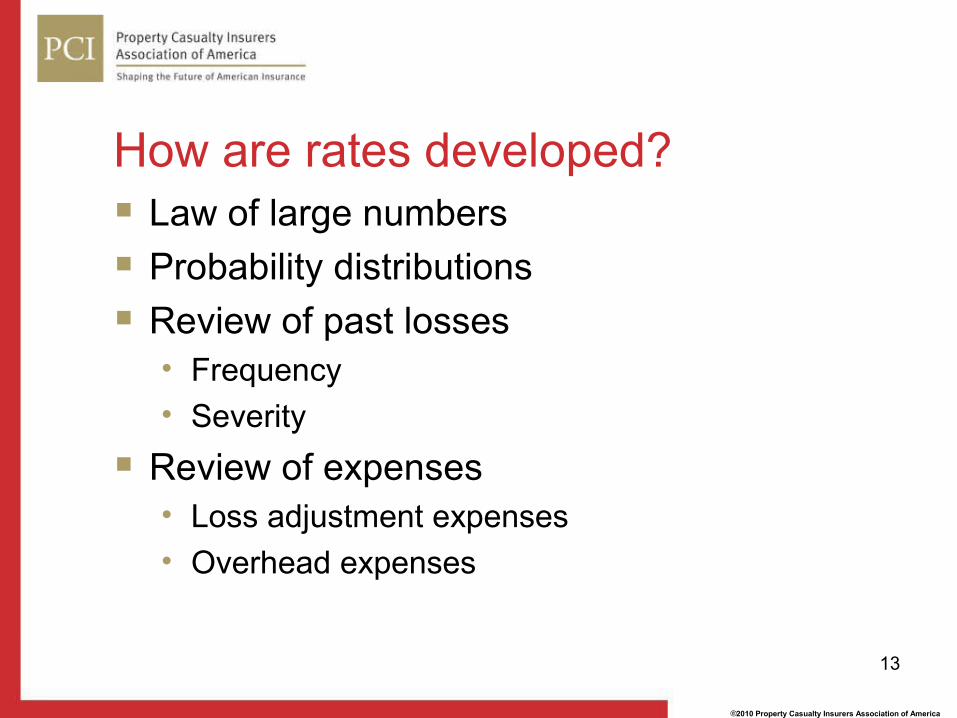

How are rates developed? Law of large numbers Probability distributions Review of past losses

• Frequency• Severity

Review of expenses• Loss adjustment expenses• Overhead expenses

14

© 2010 Property Casualty Insurers Association of America

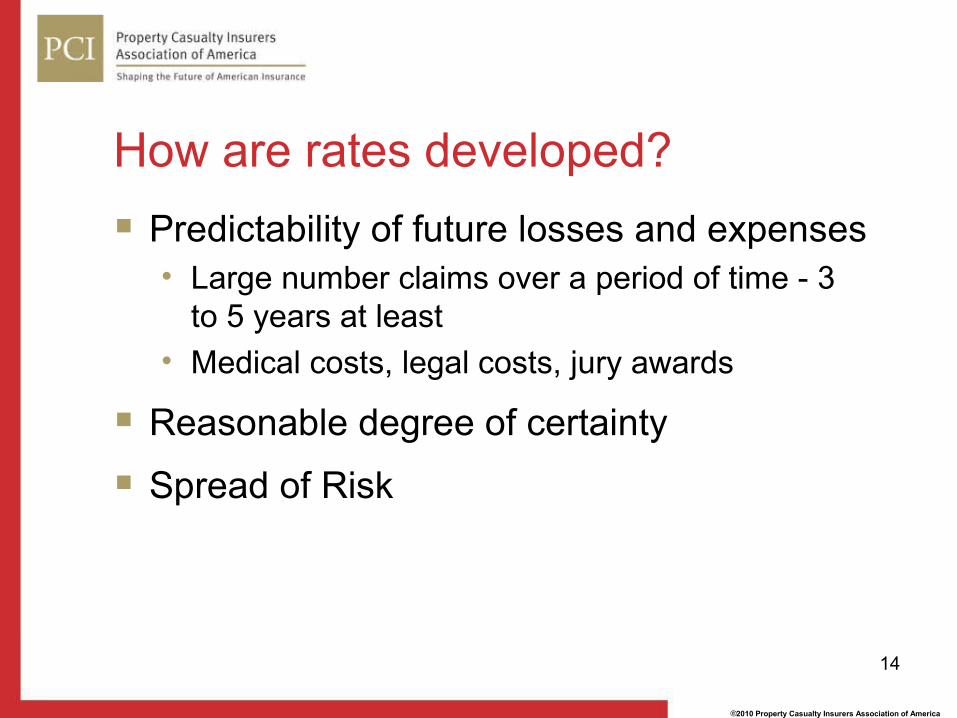

How are rates developed? Predictability of future losses and expenses

• Large number claims over a period of time - 3 to 5 years at least

• Medical costs, legal costs, jury awards

Reasonable degree of certainty

Spread of Risk

15

© 2010 Property Casualty Insurers Association of America

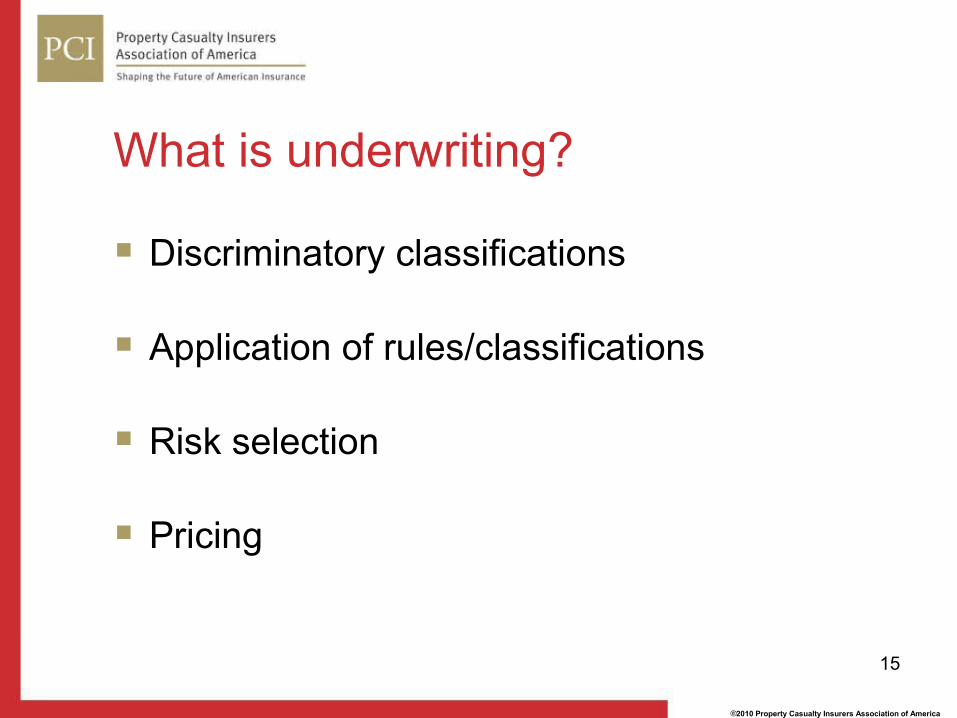

What is underwriting?

Discriminatory classifications

Application of rules/classifications

Risk selection

Pricing

16

© 2010 Property Casualty Insurers Association of America

How does it work? Agent/Company Representative

• Application/completion• Information - DMV report, etc.

Underwriters• Application/classifications• Additional info (financial, loss)• Risk Selection• Pricing

© 2010 Property Casualty Insurers Association of America

Part II

Countrywide and State Industry Results

18

© 2010 Property Casualty Insurers Association of America

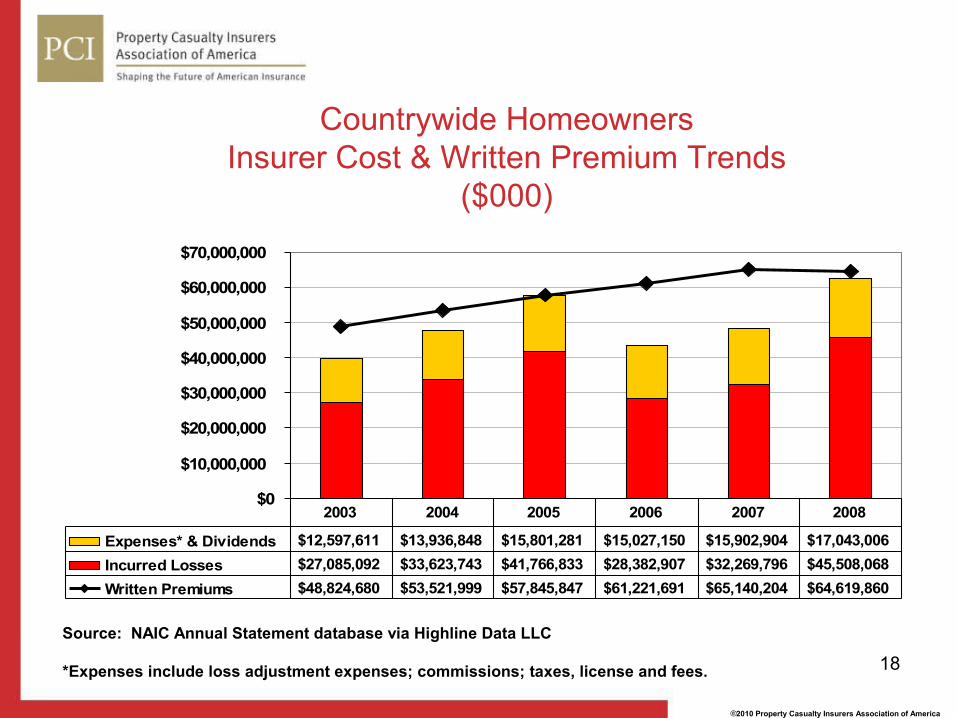

Countrywide HomeownersInsurer Cost & Written Premium Trends

($000)

$0

$10,000,000

$20,000,000

$30,000,000

$40,000,000

$50,000,000

$60,000,000

$70,000,000

Expenses* & Dividends $12,597,611 $13,936,848 $15,801,281 $15,027,150 $15,902,904 $17,043,006Incurred Losses $27,085,092 $33,623,743 $41,766,833 $28,382,907 $32,269,796 $45,508,068Written Premiums $48,824,680 $53,521,999 $57,845,847 $61,221,691 $65,140,204 $64,619,860

2003 2004 2005 2006 2007 2008

Source: NAIC Annual Statement database via Highline Data LLC

*Expenses include loss adjustment expenses; commissions; taxes, license and fees.

19

© 2010 Property Casualty Insurers Association of America

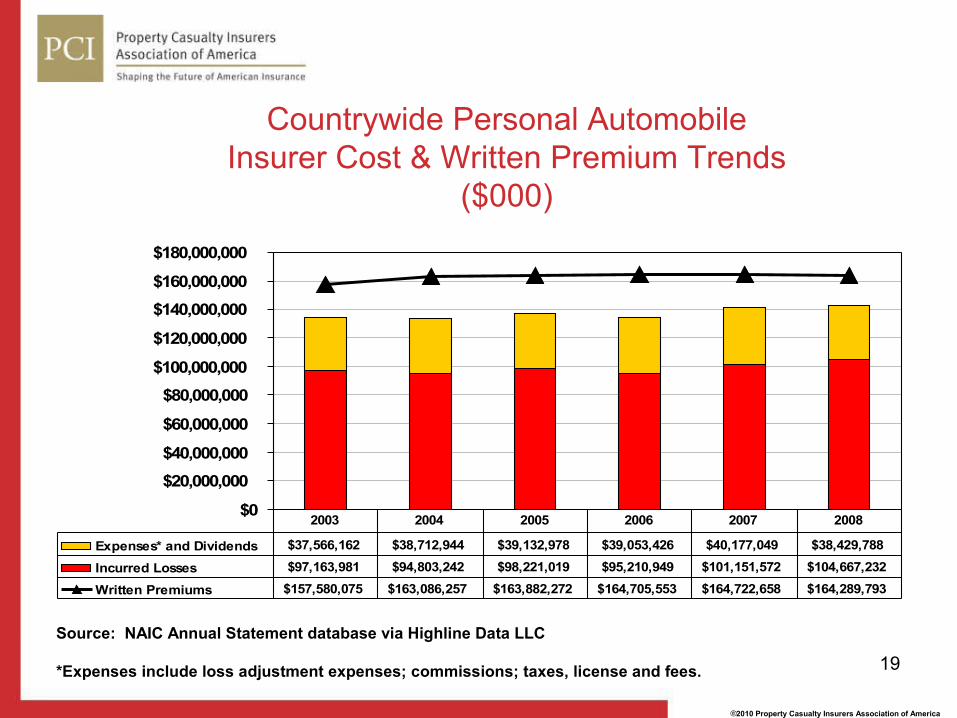

Countrywide Personal AutomobileInsurer Cost & Written Premium Trends

($000)

$0

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

$140,000,000

$160,000,000

$180,000,000

Expenses* and Dividends $37,566,162 $38,712,944 $39,132,978 $39,053,426 $40,177,049 $38,429,788

Incurred Losses $97,163,981 $94,803,242 $98,221,019 $95,210,949 $101,151,572 $104,667,232

Written Premiums $157,580,075 $163,086,257 $163,882,272 $164,705,553 $164,722,658 $164,289,793

2003 2004 2005 2006 2007 2008

Source: NAIC Annual Statement database via Highline Data LLC

*Expenses include loss adjustment expenses; commissions; taxes, license and fees.

20

© 2010 Property Casualty Insurers Association of America

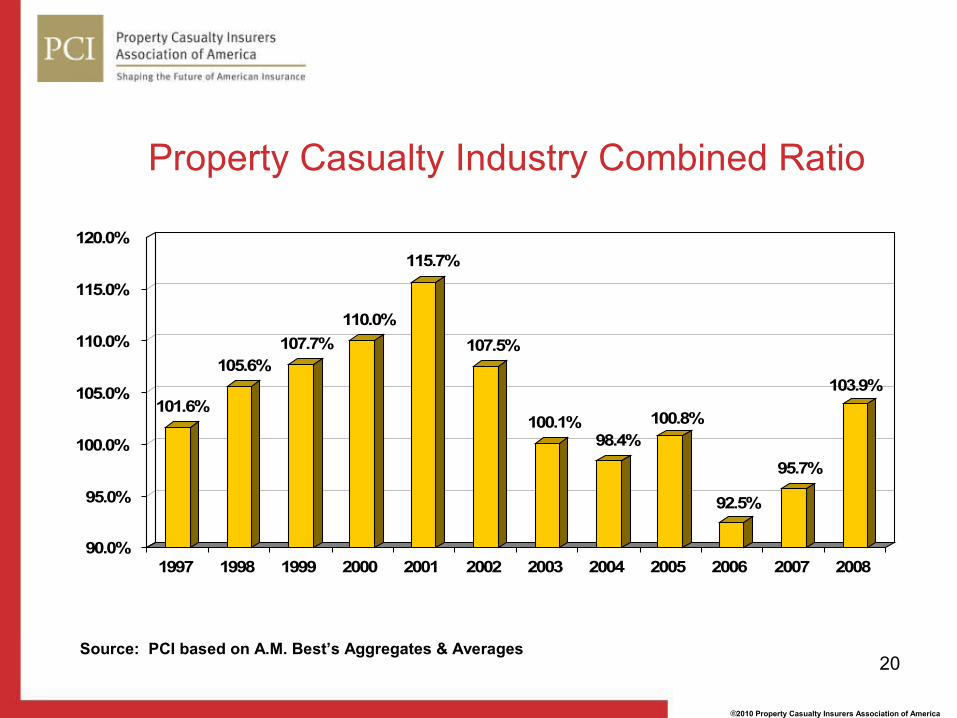

Property Casualty Industry Combined Ratio

101.6%

105.6%107.7%

110.0%

115.7%

107.5%

100.1%98.4%

100.8%

92.5%

95.7%

103.9%

90.0%

95.0%

100.0%

105.0%

110.0%

115.0%

120.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Source: PCI based on A.M. Best’s Aggregates & Averages

21

© 2010 Property Casualty Insurers Association of America

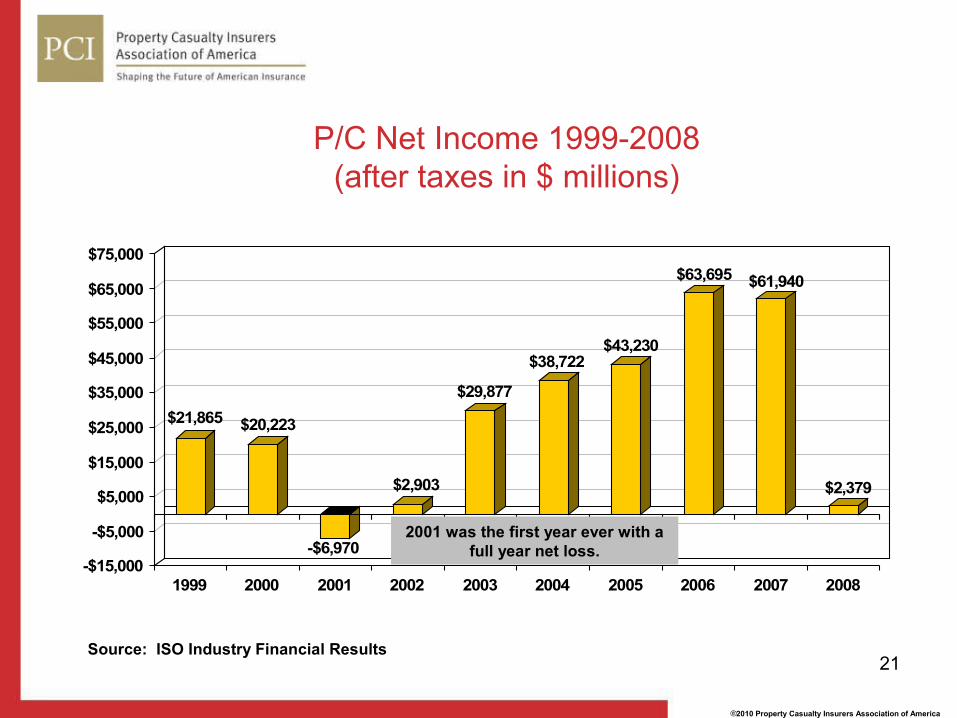

P/C Net Income 1999-2008(after taxes in $ millions)

$21,865 $20,223

-$6,970

$2,903

$29,877

$38,722$43,230

$63,695 $61,940

$2,379

-$15,000

-$5,000

$5,000

$15,000

$25,000

$35,000

$45,000

$55,000

$65,000

$75,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

2001 was the first year ever with afull year net loss.

Source: ISO Industry Financial Results

22

© 2010 Property Casualty Insurers Association of America

Kentucky HomeownersInsurer Cost & Written Premium Trends

($000)

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

Expenses* & Dividends $106,590 $114,303 $125,950 $122,957 $125,012 $130,611Incurred Losses $351,430 $320,708 $274,367 $372,044 $434,458 $826,860Written Premiums $546,557 $608,089 $643,306 $668,344 $691,137 $725,705

2003 2004 2005 2006 2007 2008

Source: NAIC Annual Statement database via Highline Data LLC

*Expenses include loss adjustment expenses; commissions; taxes, license and fees.

23

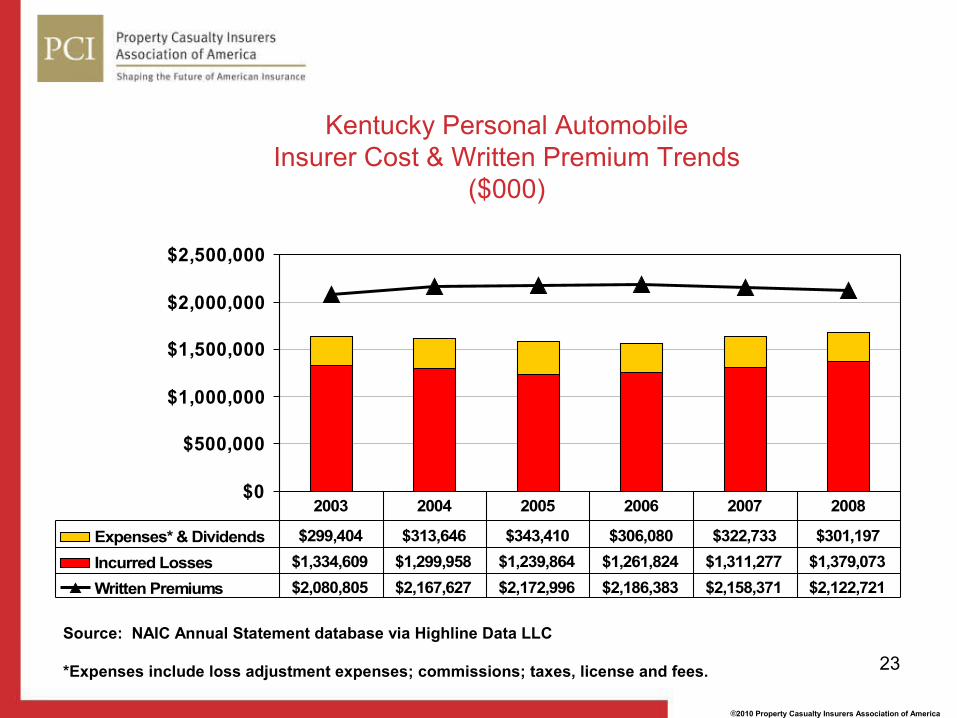

© 2010 Property Casualty Insurers Association of America

Kentucky Personal AutomobileInsurer Cost & Written Premium Trends

($000)

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

Expenses* & Dividends $299,404 $313,646 $343,410 $306,080 $322,733 $301,197Incurred Losses $1,334,609 $1,299,958 $1,239,864 $1,261,824 $1,311,277 $1,379,073Written Premiums $2,080,805 $2,167,627 $2,172,996 $2,186,383 $2,158,371 $2,122,721

2003 2004 2005 2006 2007 2008

Source: NAIC Annual Statement database via Highline Data LLC

*Expenses include loss adjustment expenses; commissions; taxes, license and fees.

24

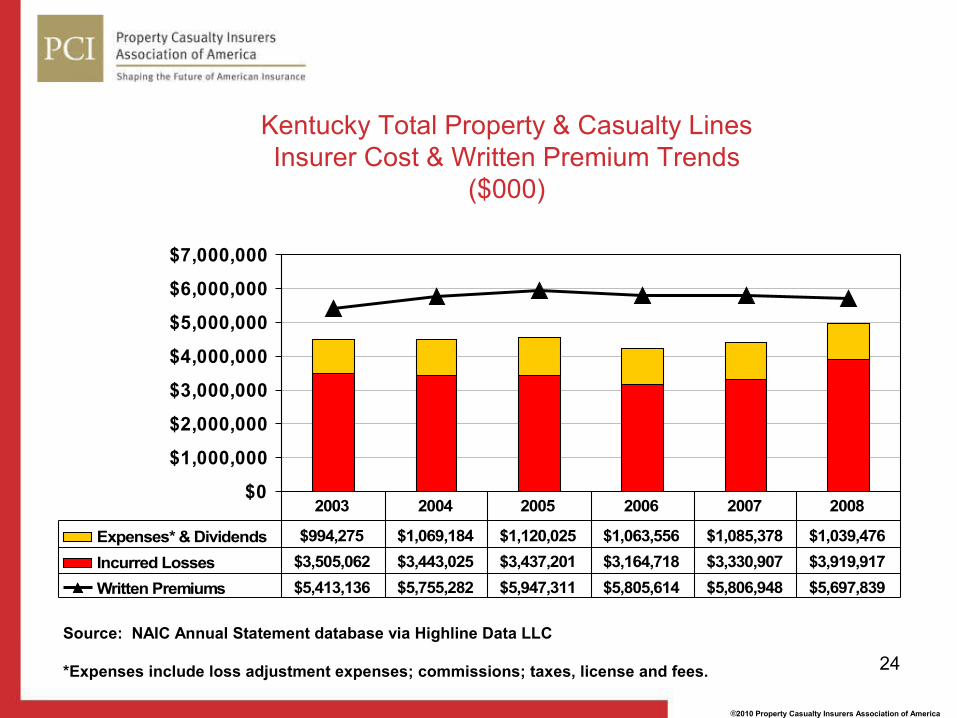

© 2010 Property Casualty Insurers Association of America

Kentucky Total Property & Casualty LinesInsurer Cost & Written Premium Trends

($000)

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$7,000,000

Expenses* & Dividends $994,275 $1,069,184 $1,120,025 $1,063,556 $1,085,378 $1,039,476Incurred Losses $3,505,062 $3,443,025 $3,437,201 $3,164,718 $3,330,907 $3,919,917Written Premiums $5,413,136 $5,755,282 $5,947,311 $5,805,614 $5,806,948 $5,697,839

2003 2004 2005 2006 2007 2008

Source: NAIC Annual Statement database via Highline Data LLC

*Expenses include loss adjustment expenses; commissions; taxes, license and fees.

© 2010 Property Casualty Insurers Association of America

Questions?

Thank you!