insurance community university homeowners problems and solutions 1 the webinar will begin shortly. ...

TRANSCRIPT

Insurance Community University

Homeowners Problems and Solutions

1

The webinar will begin shortly.

There is no audio at this time.

This presentation is being recorded for your viewing pleasure at a future date.

The attendance and proctor forms are available under ‘Materials’ in the Webinar’s Console to the right.

The PowerPoint presentation is also available under ‘Materials’.

You will receive the course number for your state near the end of class.

Use the ‘chat’ window for questions on the content.

100% Participation in Polling Questions is required to receive credit for this class. Even if you do not intend to receive credit, please participate in the polls.

Insurance Community University

Welcome to your Insurance Community University

• All of you are currently on mute – Un-mute your own system– Telephone Option

• Select Telephone on your screen• Dial in the PIN number so that your number becomes

active– Microphone and/or Speaker Option

• You can use this option if you have a headset that you use with your computer

Audio

2

Insurance Community University

Participation & Chat Window

• You will receive information from the monitor via the ‘Chat’ window. – Please locate window in the control panel

• Q & A is welcomed during the presentation and at the end of the presentation

• You will find the question box on your control panel– Write your question in that box

and send it to the presenter/organizer

• The presenter will take those• questions in the order submitted

3

Insurance Community University

DOI Requirements

• When you see a slide with the hand up symbol, touch the “hand” icon on your control panel– Click ONCE only

• If you do not raise your hand, the monitor will be in contact with you in the chat box

• If you are in a group, the designated proctor is responsible to make certain you are all in attendance at all times

4

= Hand is down

Insurance Community University

Polling

• Throughout the class we will be conducting periodic polls

• We need 100% participation on the polls• The polls are intended to check

participation but also to create discussion topics throughout the presentation

5

Insurance Community University

Forms To Complete for CE

• After class ends– Return attendance form– Proctors – return your form to email

address

• Email address is in chat window or in email sent to you today

6

Insurance Community University

DOI Requirements

• We will file your hours with the DOI after the completion of this webinar and we have received the attendance form.

• You have 48 hours to return the form• You will be sent a Certificate of

Attendance/Completion by email. Please retain this for your records for five years.

7

Insurance Community University

Internet Disruption

• If the presenter looses internet connection STAY ON THE LINE

• The administrators will communicate with you

Insurance Community University

Internet Failure

• If the internet fails and all participants are kicked off line by Go To Training or other source then the seminar will be terminated

• You will receive instructions by email as to how we will proceed

• This is a precautionary notice, only

9

Insurance Community University

This class is being recorded

• Available in the University• This course is approved for CE in CA Only

Insurance Community University

DisclaimerInsurance forms and endorsements vary based on insurance company;

changes in edition dates; regulations; court decisions; and state jurisdiction. This instructional materials provided by Insight is

intended as a general guideline and any interpretations provided by the instructor or the creator(s) of this material do not modify or

revise insurance policy language. In providing these materials, the authors assume neither liability nor responsibility to any person or

business with respect to any loss that is alleged to be caused directly or indirectly as a result of the instructional materials

provided. Copyright 2010 – 2013 All Rights Reserved

www.insurancecommunitycenter.com

11

Insurance Community University

Your Instructor Today

Mary A. LaPorte, CPCI, CIC, LIC, CPIALaPorte Consulting, LLC

[email protected] 623-8112

12

Insurance Community University

What This Course Will CoverSituations and Solutions1. Vacant and Occupied Homes2. Who is an insured?3. Loss Assessment and the Homeowner4. 13 year old children and Property

Damage Liability5. Vermin and Secretions—there is a

change

13

Insurance Community University

Vacant and Unoccupied Homes

14

Insurance Community University

Example

Joe and Sally Bergen have lived in their home for 8 years, and you have insured them the entire time. Joe’s employer down-sized and he lost his job six months ago. Both of them have not been able to find work since then. Sally’s brother in Arizona said there are plenty of jobs there, and invited them to stay with him for awhile. They have decided to do this and hope that once they get their finances in order they will return to their home. All of their furniture and contents are staying in their home. They let you know to temporarily change their mailing address.

15

Insurance Community University

Will Joe & Sally’s homeowner’s policy cover their home while

they are gone?16

Polling Question #1

Insurance Community University

Issues• If the home is located in a cold climate, the

insured will need to maintain heat or drain their water systems.

17

Insurance Community University

Exclusion in the ISO policy

Caused by:(1)Freezing of a plumbing, heating, air conditioning or

automatic fire protective sprinkler system or of a household appliance, or by discharge, leakage or overflow from within the system or appliance caused by freezing. This provision does not apply if you have used reasonable care to: (a) Maintain heat in the building; or(b) Shut off the water supply and drain the system and appliances of water.

18

Insurance Community University

Issues

• Vandalism if the home is vacant• Exclusion in the ISO policy:Caused by:(4) Vandalism and malicious mischief, and any ensuing loss caused

by any intentional and wrongful act committed in the course of the vandalism or malicious mischief, if the dwelling has been vacant for more than 60 consecutive days immediately before the loss.

19

Insurance Community University

Issues

• Breakage of glass if the home is vacant• Glass coverage exception in ISO policy:

We cover: a. The breakage of glass or safety glazing material

which is part of a covered building, storm door or storm window; ………This coverage does not include loss on the "residence premises" if the dwelling has been vacant for more than 30 consecutive days immediately before the loss.

20

Insurance Community University

Is the Home Considered Vacant?

• The homeowners policy is intended to insure owner-occupied homes

• Vacant homes create an “attractive nuisance”

21

Insurance Community University

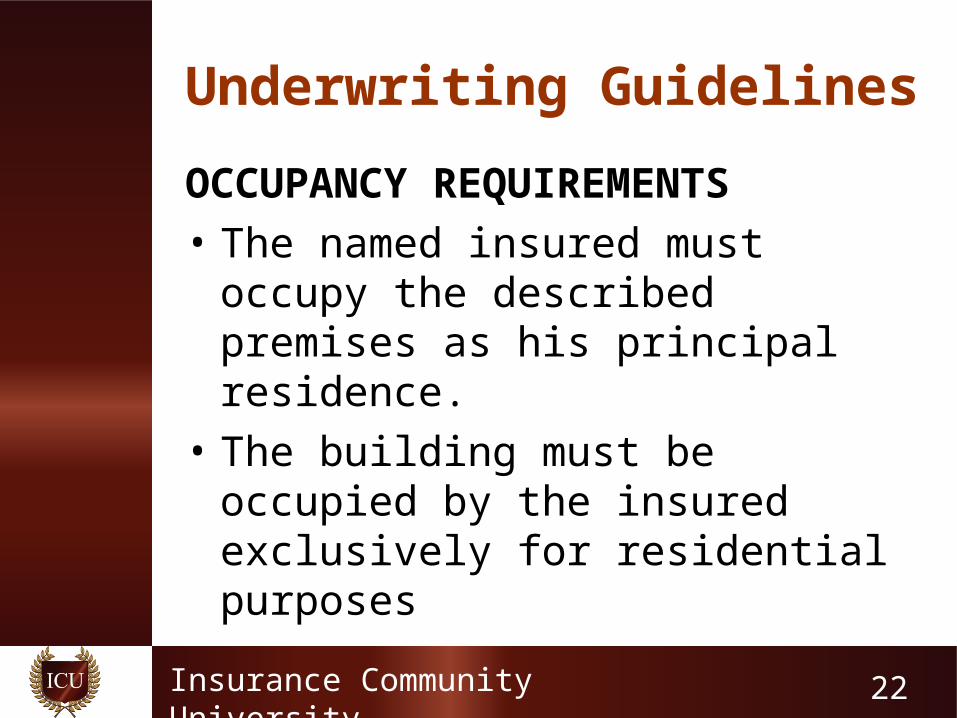

Underwriting Guidelines

OCCUPANCY REQUIREMENTS• The named insured must occupy the

described premises as his principal residence.

• The building must be occupied by the insured exclusively for residential purposes

22

Insurance Community University

ISO Homeowners Definition8."Residence premises" means:

a. The one family dwelling, other structures, and grounds; or

b. That part of any other building; where you reside and which is shown as the "residence premises" in the Declarations.

Requires residency of Named Insured

23

Insurance Community University

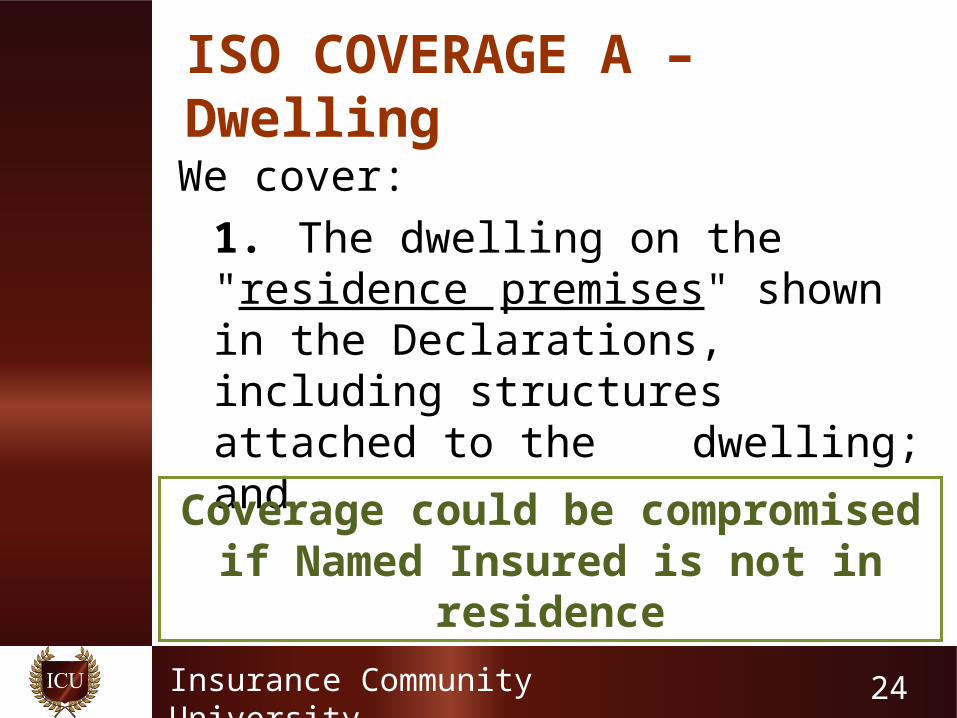

ISO COVERAGE A – Dwelling

We cover: 1. The dwelling on the "residence premises" shown in the Declarations, including structures attached to the dwelling; and

Coverage could be compromised if Named Insured is not in residence

24

Insurance Community University

ISO COVERAGE B – Other Structures

• We cover other structures on the "residence premises" set apart from the dwelling by clear space. This includes structures connected to the dwelling by only a fence, utility line, or similar connection.

Coverage could be compromised if Named Insured is not in residence

25

Insurance Community University

Solution• There is no endorsement that can be used

to assure continuation of coverage.• The best tactic is to notify the carrier of

the situation.• Most carrier’s will continue coverage for a

period of time. They would probably set up for non-renewal after that time.

• Counsel your customer and keep communication open.

26

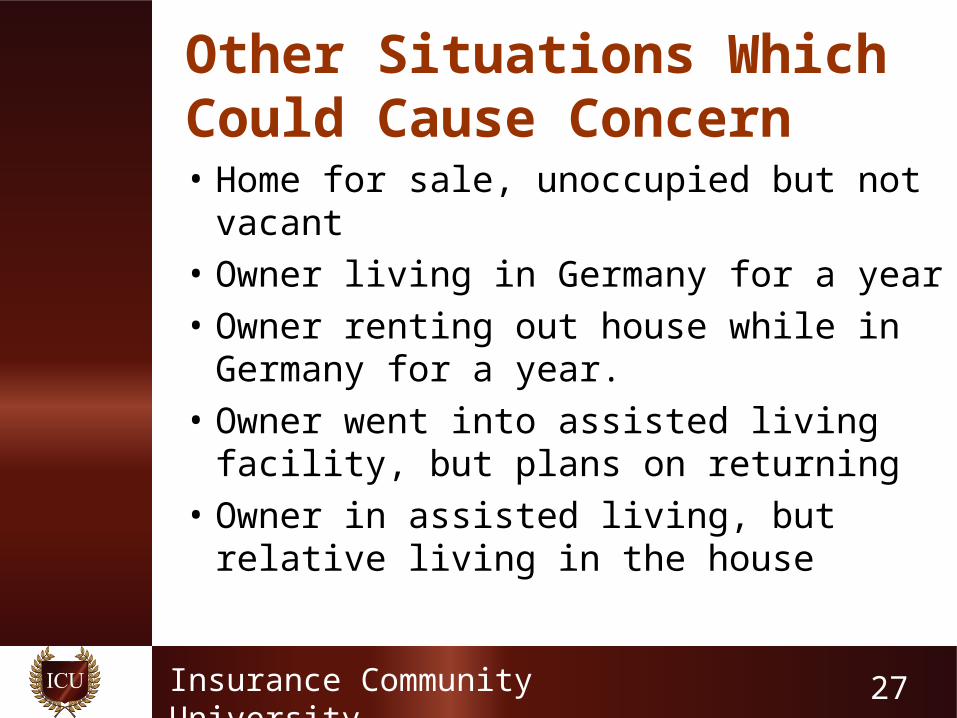

Insurance Community University

Other Situations Which Could Cause Concern• Home for sale, unoccupied but not vacant• Owner living in Germany for a year• Owner renting out house while in

Germany for a year.• Owner went into assisted living facility,

but plans on returning• Owner in assisted living, but relative living

in the house

27

Insurance Community University

Renting Out the Insured HomeBusiness Exclusion in the ISO policy: 2. "Business"

a. "Bodily injury" or "property damage" arising out of or in connection with a "business" conducted from an "insured location" or engaged in by an "insured", whether or not the "business" is owned or operated by an "insured" or employs an "insured".

This Exclusion E.2. applies but is not limited to an act or omission, regardless of its nature or circumstance, involving a service or duty rendered, promised, owed, or implied to be provided because of the nature of the "business".

b. This Exclusion E.2. does not apply to: (1) The rental or holding for rental of

an "insured location";

(a) On an occasional basis if used only as a residence;

28

Insurance Community University

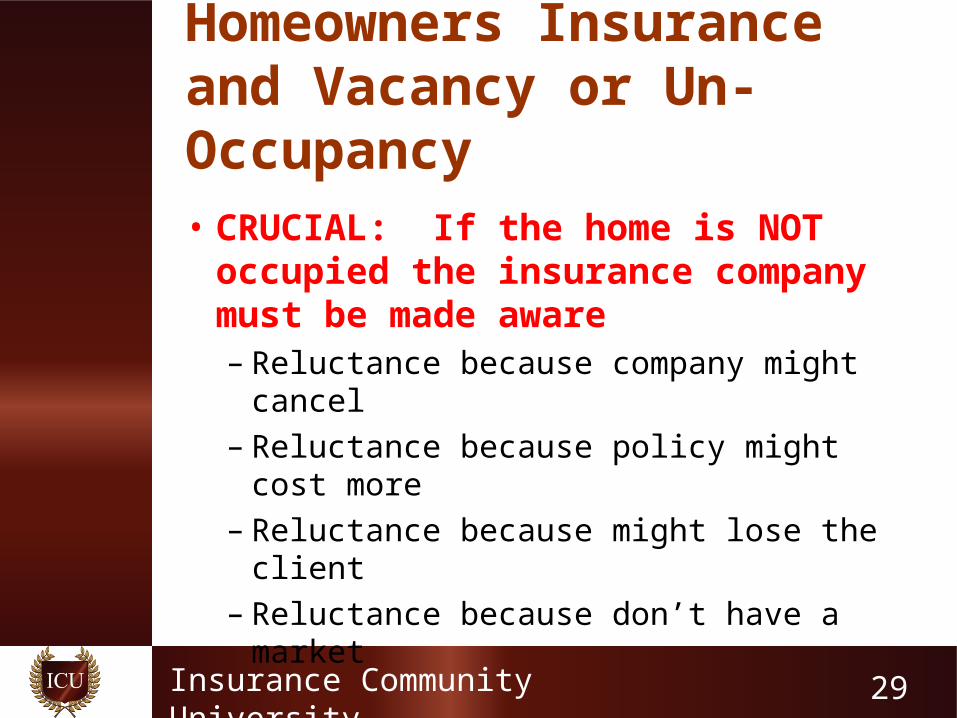

Homeowners Insurance and Vacancy or Un-Occupancy

• CRUCIAL: If the home is NOT occupied the insurance company must be made aware– Reluctance because company might cancel– Reluctance because policy might cost more– Reluctance because might lose the client– Reluctance because don’t have a market

29

Insurance Community University

Who is an insured?

30

Insurance Community University

Example #1 Steve and Lisa Davis have lived in Texas for three years with their two sons, Bobby who is 8 and Jacob who is 6. Because of financial and employment problems, they have decided to move back to Oregon, their home state. They ask Steve’s parents, Bob & Gina if they can stay with them at their home in Portland OR until they are able to find a place of their own. Bob & Gina are excited to have them moving back to the area, and agree to the arrangement. A short time after moving in, Jacob was playing with matches and started a fire that burned a portion of a neighbor’s home which resulted in the neighbor suing Steve & Lisa for negligence.

31

Insurance Community University

Are Steve and Lisa “insureds” under Bob & Gina’s (Steve’s

parents) homeowner’s policy?32

Polling Question #2

Insurance Community University

ISO Homeowner’s Policy• Definition of “Insured”:5. “Insured” means:a. You and residents of your household who are:(1) Your relatives; or(2) Other persons under the age of 21 and in your care or

the care of a resident of your household who is your relative;

33

Two part test:1.Resident2.Relative

Insurance Community University

Courts will evaluate a number of criteria when determining residency:• Drivers license• Voter’s registration• Tax records• Location of bank accounts• Location of employment• Location of furnishings/stuff• Length of time there

34

Insurance Community University

Are you sure you want to be an insured?• Circumstances often help you decide.• If 6 yr old Jacob had fallen from grandpa’s

rickety ladder, and wanted Medical payments or Liability coverage under grandpa’s policy, he could not collect if he were an “insured”.

35

Insurance Community University

ISO Homeowner’s Policy• Liability Exclusion6. "Bodily injury" to you or an "insured" as defined under Definition

5.a. or b. This exclusion also applies to any claim made or suit brought against

you or an "insured" to:a. Repay; orb. Share damages with;another person who may be obligated to pay damages because of

"bodily injury" to an "insured".

36

No Liability or Medical Coverage for an “Insured”.

Insurance Community University

Example #3 Peter and Deb Johnson have an 18 year old son, Caleb, who is just entered college. He is attending a university which is over 200 miles from home, and has decided to share an apartment with two other students.

He has taken a lot of stuff from home to furnish the apartment, plus all of his electronics and other personal items.

Peter and Deb contact you and are concerned about all of the personal property as well as liability.

37

Insurance Community University

Is Caleb an “insured” under the homeowner’s policy?

38

Polling Question #3

Insurance Community University

ISO Homeowner’s Policy• Definition of “Insured” (continued):

5. “Insured” means:b. A student enrolled in school full time, as

defined by the school, who was a resident of your household before moving out to attend school, provided the student is under the age of:

(1) 24 and your relative; or(2) 21 and in your care or the care of a

resident of your household who is your relative;

39

Insurance Community University

Full Time Student• If the student drops classes and becomes less

than full time, then they are no longer an “insured”

40

CAUTION: Parents may not always be made aware of status changes their student makes!

Insurance Community University

Under the Age of 24• They are an “insured” up to their 24th birthday (not

24 years old).• When they reach 24 they will no longer be an

“insured” if they are away at school.

41

CAUTION: Parents may need to take action before the 24th birthday.

Insurance Community University

Policy Limitations• A student’s personal property is only covered up to 10% of the

insured’s personal property limit.• There is no coverage for theft of personal property if the student

has not been there for 90 days.– Some carriers may limit the time to 30 or 60 days.

42

This “automatic” coverage may not be sufficient for most students at school.

Insurance Community University

Solutions

43

Insurance Community University

HO 05 27 – Additional Insured – Student Living Away from the Residence Premises

• Added to parent’s homeowner’s policy for an additional premium• Schedules location where student resides• Can cover student age 24 and over• Can cover student who is not enrolled full-time

44

Insurance Community University

Will Charlie's dog bite injury be covered under Nancy's homeowner's policy?

45

Polling Question #4

Insurance Community University

Select Answer:1. No, Charlie needs to make a claim under

his parent’s homeowners policy.2. No, Charlie was in the “business” of dog

walking, and there is no business coverage.

3. Yes, Nancy’s policy will cover him only if he wasn’t getting paid.

4. Nancy’s policy will cover him regardless if he was getting paid or not.

46

Insurance Community University

ISO Homeowner’s Policy• Definition of “Insured” (continued):

5. “Insured” means:c. Under Section II:

(1) With respect to animals or watercraft to which this policy applies, any person or organization legally responsible for these animals or watercraft which

are owned by you or any person described in 5. a. or b. “Insured” does not mean a person or organization

using or having custody of these animals or watercraft in the course of any “business” or without consent of the owner.

47

Insurance Community University

Example #5• While walking Buster in the park one day,

Buster pulled the leash out of Charlie’s hands to chase another dog. Charlie caught up with Buster and while attempting to break up the dog fight, was bitten by Buster. His injury required twelve stitches.

48

Insurance Community University

Will Nancy’s homeowners policy also provide liability coverage

for Charlie? 49

Polling Question #5

Insurance Community University

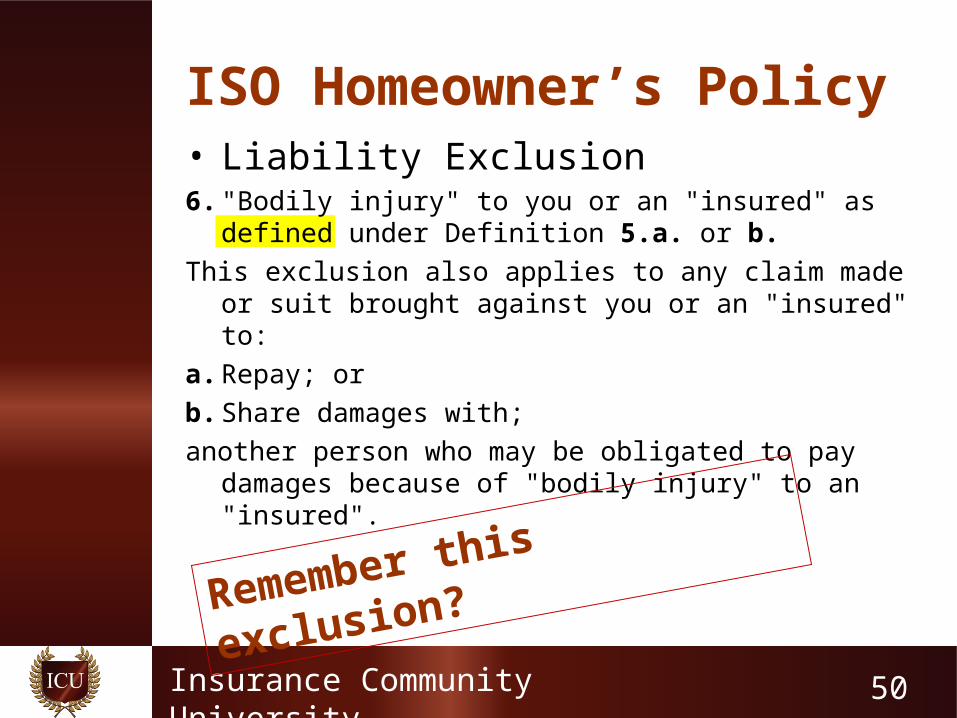

ISO Homeowner’s Policy• Liability Exclusion6. "Bodily injury" to you or an "insured" as defined under Definition

5.a. or b. This exclusion also applies to any claim made or suit brought against

you or an "insured" to:a. Repay; orb. Share damages with;another person who may be obligated to pay damages because of

"bodily injury" to an "insured".

50

Remember this exclusion?

Insurance Community University

ISO Homeowner’s Policy• Definition of “Insured” (continued):

5. “Insured” means:c. Under Section II:

(1) With respect to animals or watercraft to which this policy applies, any person or organization legally responsible for these animals or watercraft which

are owned by you or any person described in 5. a. or b. “Insured” does not mean a person or organization using or having custody of these animals or watercraft

in the course of any “business” or without consent of the owner.

51

An “insured” under 5.c. is not excluded for injury (only 5.a. and 5.b.)

Insurance Community University

Others who may be an insured:• Someone using a covered watercraft• Someone using a motor vehicle on premises

Others you may wish to add as an insured:

• Trusts• Land Contract Holders• Co-owners• Other co-inhabitants

52

Insurance Community University

• Additional Insured – Residence Premises• HO 04 41

Solution

31

Insurance Community University

• Trust Endorsement• HO 06 15

Solution

31

Insurance Community University

• Other Members of Your Household• HO 04 58• Extends liability coverage and

personal property to a co-resident

Solution

31

Insurance Community University

Loss Assessment and the Homeowner

56

Insurance Community University

ExampleTom and Penny have had their homeowner’s insurance coverage written through your agency for six years. They live in a very upscale suburb of the city and you have had an opportunity to do a complete coverage review with them every couple of years.They have just notified you that they are being assessed by their home association. Apparently, a dog owned by another association member has bitten a child. The association was sued for “not enforcing the leash law”. The association carried $1,000,000 liability, but the settlement was for $1,250,000. Your insured’s share is $2,600 and they want to make a claim.

57

Insurance Community University

Will Tom & Penny’s homeowners policy provide any

coverage?58

Polling Question #6

Insurance Community University

ISO Homeowner’s Policy• Liability Exclusion:

Coverage E does not apply to: 1. Liability:

a. For any loss assessment charged against you as a member of an association, corporation or

community of property owners, except as provided in D. Loss Assessment under

Section II – Additional Coverages;

59

Insurance Community University

ISO Homeowner’s PolicyD. Loss Assessment

1. We will pay up to $1,000 for your share of loss assessment charged against you, as owner or tenant of the "residence premises", during the policy period by a corporation or

association of property owners, when the assessment is made as a result of:

a. "Bodily injury" or "property damage" not excluded from coverage under Section II – Exclusions; or

b. Liability for an act of a director, officer or trustee in the capacity as a director, officer or trustee, provided such person: (1) Is elected by the members of a corporation or

association of property owners; and (2) Serves without deriving any income from the

exercise of duties which are solely on behalf of a corporation or association of property owners.

60

Insurance Community University

ISO Homeowner’s PolicyD. Loss Assessment

1. We will pay up to $1,000 for your share of loss assessment charged against you, as owner or tenant of the "residence premises", during the policy period by a corporation or

association of property owners, when the assessment is made as a result of:

a. "Bodily injury" or "property damage" not excluded from coverage under Section II – Exclusions; or

b. Liability for an act of a director, officer or trustee in the capacity as a director, officer or trustee, provided such person:

(1) Is elected by the members of a corporation or association of property owners; and

(2) Serves without deriving any income from the exercise of duties which are solely on behalf of a corporation or association of property owners.

61

Insurance Community University

Important points:• The ISO policy automatically includes $1,000

loss assessment coverage• This includes assessments for property losses

as well as liability losses• The policy must not exclude that type of loss

in order for coverage to apply• The coverage is based on the date of the

assessment, not the date of loss• Other policies may have higher coverage or

even no coverage at all

62

Insurance Community University

Solution• HO 04 35 Supplemental Loss

Assessment Coverage• The $1,000 limit may be increased up to

$50,000• Pays for property or liability assessments

charged by a home association• Coverage is based on the date of the

assessment

63

Insurance Community University

Children under 13 years of age and Property Damage Liability

64

Insurance Community University

ExampleIt was summertime and the neighborhood kids were bored. Kevin French is twelve and the other kids range in age from eight to thirteen.It was one of the other kids who had the idea. They had been watching the construction crew working all week. They waited until the workers had left for the night, then snuck into the construction site and shoveled gravel into all of the fuel tanks of the bulldozers, graders and loaders. When the workers returned in the morning, they realized what had happened when each of the heavy equipment stopped running.One of them remembered Kevin watching them and went to his parents. Kevin was quick to blame the other kids and gave out all of their names.

65

Insurance Community University

Will the homeowner’s policy for Kevin’s parents cover this

damage?66

Polling Question #7

Insurance Community University

ISO Homeowner’s Policy• Liability Exclusion:

E. Coverages E and F do not apply to the following: 1. Expected Or Intended Injury

"Bodily injury" or "property damage" which is expected or intended by an "insured" even if the resulting "bodily injury" or "property damage":a. Is of a different kind, quality or degree than initially expected or intended; orb. Is sustained by a different person, entity or property than initially expected or intended.

However, this Exclusion E.1. does not apply to "bodily injury" or “property damage” resulting from the use of reasonable force by an "insured" to protect persons or property;

67

Insurance Community University

ISO Homeowner’s Policy• Additional Coverages – Section II

3. C. Damage To Property Of Others1. We will pay, at replacement cost, up to $1,000 per

"occurrence" for "property damage" to property of others caused by an "insured".

2. We will not pay for "property damage": a. To the extent of any amount recoverable under

Section I; b. Caused intentionally by an "insured" who is 13

years or older;

68

Insurance Community University

Conclusion:• Intentional acts are not covered under

liability.• Additional Coverages provides $1,000

coverage • It will not cover intentional damage

unless caused by someone under the age of 13.

• The parents of the 8-12 year old boys would have coverage.

69

Insurance Community University

Vermin and SecretionsThere is a change

70

Insurance Community University

ExampleWhen Kristin Jacobs pulled in her driveway after work, the first thing she noticed was the broken glass on the deck, which she realized was from the French door. She entered the house cautiously, and was overwhelmed by what she saw. It was a disaster! At first she thought it was a burglar in a bad mood, but then she saw the blood. There was blood and urine everywhere, especially at the door. She called 911 and the police were there in minutes. The officers were reassuring, and it was pretty obvious. A deer had broken into her rural home, and caused a lot of damage. Holes in walls, urine and blood on carpeting and furniture, broken TV, dented appliances. What a mess!

71

Insurance Community University

Will Kristin’s homeowner’s policy pay for this damage?

72

Polling Question #8

Insurance Community University

A History Lesson on Vermin• Previous ISO Exclusions:

(g) Birds, vermin, rodents, or insects; or(h) Animals owned or kept by an “insured”

• Exclusions revised in the ISO 2011 edition:(g) Birds, rodents, or insects; (h) Nesting or infestation, or discharge or

release of waste products or secretions, by any animals; or

(i) Animals owned or kept by an "insured".

73

In lieu of “vermin”, the policy now excludes nesting, infestation, release of waste products secretions………

Insurance Community University

Conclusion:• The ISO policy has removed significant

coverage for damage done by release of waste products and secretions by any animals

• Not all carriers have adopted the 2011 version of the ISO homeowner’s policy

• Some carriers may choose not to adopt the new policy language

• Familiarize yourself with the forms being used by your carriers

74

Insurance Community University

Upcoming ClassesUpcoming University/Paid CE ClassesCyber Liability and the Personal Lines Account

FREE to University Members$50.00/charge for non university members

10/10 Manufacturers - Insurance Coverages that are Unique and Essential to Consider

10/15 Voluntary Benefits

10/17 Agricultural Equipment Breakdown

75

Join the University TODAY. www.insurancecommunitycenter.comClick Join University at the top of the bar

Upcoming Community Classes FREE to University Members$25.00/charge for non university members

10/22 Cyber Liability and the Personal Lines Account