insurance community university installation floaters and contractor’s equipment 1 the webinar...

TRANSCRIPT

Insurance Community University

Installation Floaters and Contractor’s Equipment

1

The webinar will begin shortly.

There is no audio at this time.

This presentation is being recorded for your viewing pleasure at a future date.

The attendance and proctor forms are available under ‘Materials’ in the Webinar’s Console to the right.

The PowerPoint presentation is also available under ‘Materials’.

You will receive the course number for your state near the end of class.

Use the ‘chat’ window for questions on the content.

100% Participation in Polling Questions is required to receive credit for this class. Even if you do not intend to receive credit, please participate in the polls.

Insurance Community University

Disclaimer

Insurance forms and endorsements vary based on insurance company; changes in edition dates; regulations; court decisions; and state

jurisdiction. This instructional materials provided by Insight is intended as a general guideline and any interpretations provided by Insight do not

modify or revise insurance policy language. The authors of these materials, Insight Insurance Consultants is a division of Insight Consulting

and Management Inc. In providing these materials, Insight assumes neither liability nor responsibility to any person or business with respect to any loss that is alleged to be caused directly or indirectly as a result of

the instructional materials provided. Copyright 2010 – 2012 All Rights Reserved

www.insurancecommunitycenter.comLaurie: 714.803.5830 [email protected]

Marjorie: 714.206.9583 [email protected]

2

Insurance Community University

Your Instructor Today

Al Parizo, AFIS, CISC

In our last session:On Chautauqua Trail, Boulder CO we found a good Builder’s Risk

3

Insurance Community University

In Depth review

4

We now go deep into issues of Installation and Equipment floaters

Channel Islands CA

Insurance Community University

What This Class Will Cover

1. Reasons to purchase an Installation Floater

2. Covered Property/Excluded Property3. Coverage Locations/territory/valuation 4. Contractors Equipment eligible and

non-eligible property 5. Limits and Coverage Structure and

review

5

Insurance Community University

Inland Marine and Contractor’s Equipment

The rest of the project beyond Builders’ Risk

6

Insurance Community University

Inland Marine

• The client’s exposures should be reviewed and the insurance coverage specifications designed to meet those needs as effectively as possible

• Fit the coverage to the client – do NOT fit the client to the coverage

7

Insurance Community University

NAIC Definition of Installation Risk

8

Insurance Community University

Installation Floater

9

Insurance Community University

Coverages for Builders

10

Insurance Community University

Purpose of the Installation Floater

11

Insurance Community University

Comparison Installation Floater and Builder’s Risk

Project Begins

Builders Risk Policy Begins

Project Ends

Builders Risk

Policy Ends

Installation Begins

Installation Floater Coverage Begins

Installation Ends

Installation Floater

Coverage Ends

12

Insurance Community University

Why A Subcontractor Should Purchase An Installation Floater

13

Insurance Community University

Why A Subcontractor Should Purchase An Installation Floater

14

Insurance Community University

Commercial Property Policy

• Will not cover away from insured premises.

• Limited Transit coverage (if any).• Off site storage issues.

15

Insurance Community University

Covered Property

16

Insurance Community University

Excluded Or Limited Property

17

Insurance Community University

Excluded Or Limited Property

18

Insurance Community University

Museum Quality Installation

19

Museum of Fine Arts Job Site

Insurance Community University

Excluded Or Limited Property

20

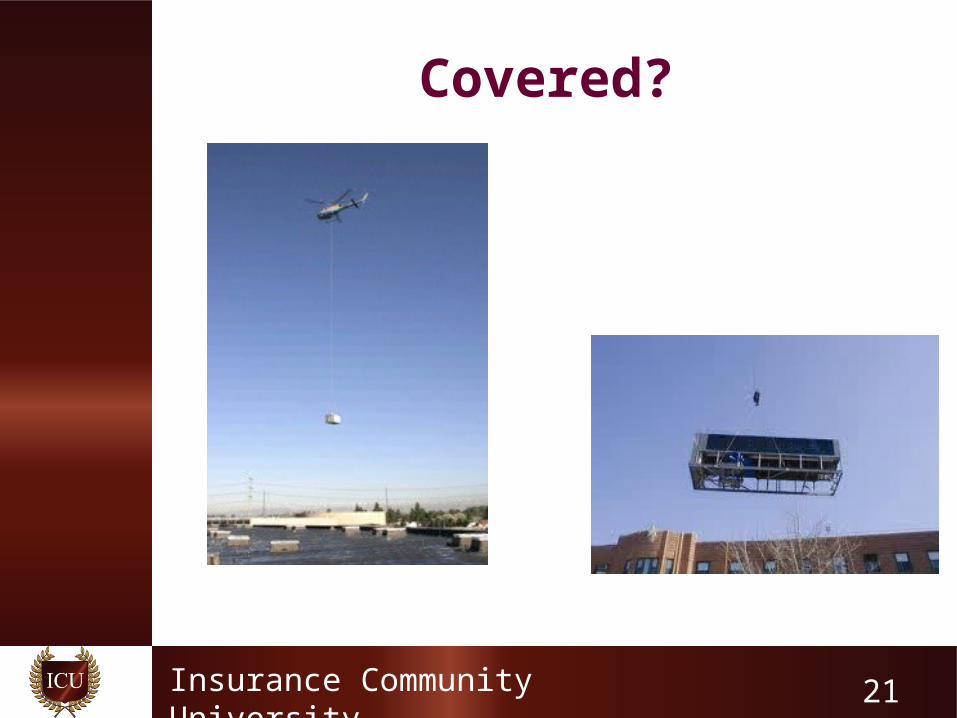

Insurance Community University

Covered?

21

Insurance Community University

Any waterborne exposure?

22

Insurance Community University

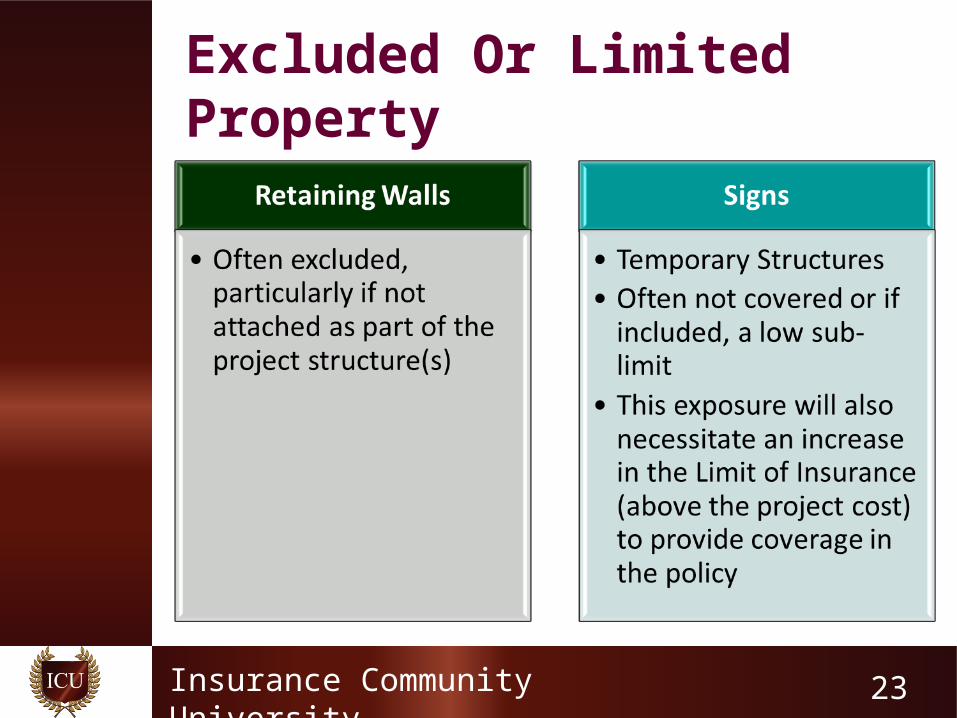

Excluded Or Limited Property

23

Insurance Community University

Coverage Locations

24

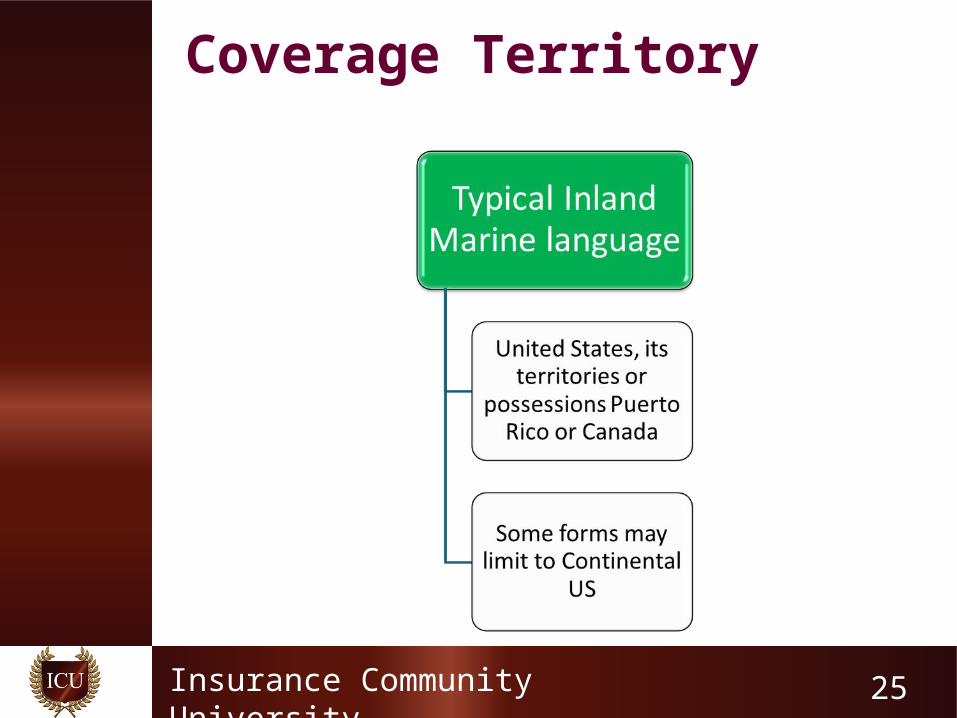

Insurance Community University

Coverage Territory

25

Insurance Community University

Valuation

26

Insurance Community University

When Coverage Begins and Ends

27

Insurance Community University

Covered Causes of Loss

• Typically Special Form perils• There are very few forms that use

named perils – this would be when the underwriter wants to exclude theft

• Equipment Breakdown coverage may be needed

• Earthquake, Flood, Wind (Tier 1) or Named Storms

28

Insurance Community University

Typical Exclusions

• Pollution Clean Up– Many policies have a limitation for

extraction or removal of pollutants from land or water at the coverage location only and will be limited to $10,000 or possibly $25,000

– This is clearly inadequate for most construction sites

– Review the need for Pollution Remediation Coverage

29

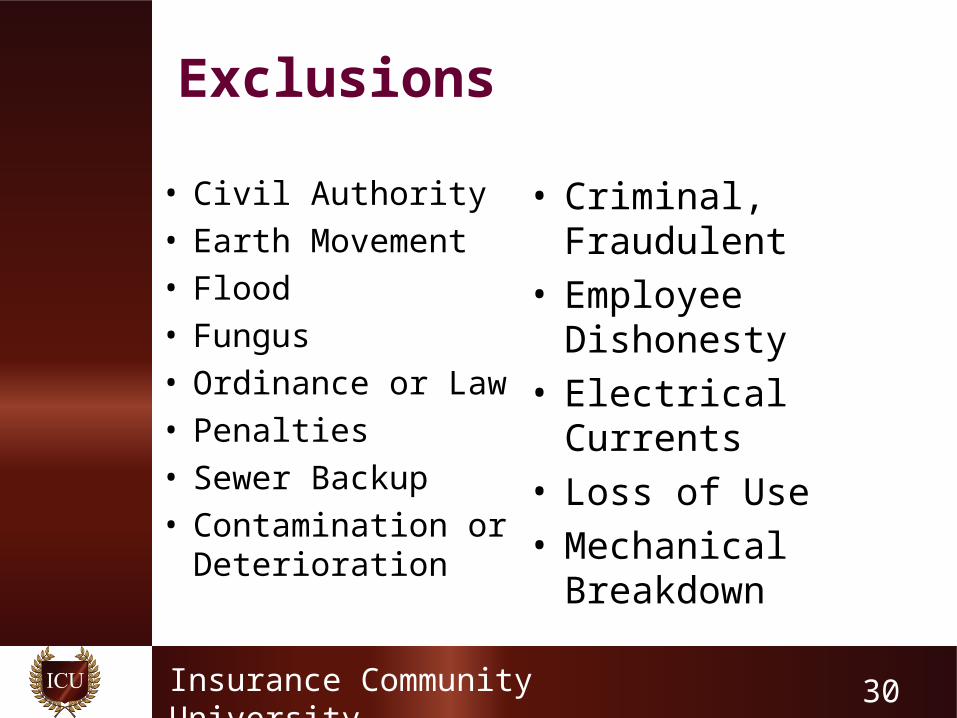

Insurance Community University

Exclusions

• Civil Authority• Earth Movement• Flood• Fungus• Ordinance or Law• Penalties• Sewer Backup• Contamination or

Deterioration

• Criminal, Fraudulent• Employee Dishonesty• Electrical Currents• Loss of Use• Mechanical Breakdown

30

Insurance Community University

Typical Exclusions

• Testing– Frequently excluded, either by specific

language or by removing any loss caused by Mechanical Breakdown, Explosion, Arcing (Artificially Generated Electrical Current), Steam Boiler or Pressure Vessel explosion

31

Insurance Community University

Typical Exclusions

• Error, omission or deficiency in design, specifications, workmanship or materials as respects the cost of making good such error, omission or deficiency– ALWAYS make sure that the policy contains an

exception to this exclusion, such as:– However, resulting physical loss or damage to the

insured property is covered

32

Insurance Community University

Typical Exclusions

• Terrorism– The coverage offer needs to be addressed

for both TRIA and other acts of terrorism, such as domestic

– Domestic terrorism could be a significant risk exposure, depending on the geographic siting of the project

– Domestic environmental groups have been known to destroy property while under construction

33

Insurance Community University

Waiver of Subrogation

• Contracts often require a waiver of subrogation

• Not all forms allow a waiver and can void coverage

34

Insurance Community University

Contractor’s Equipment Floater

35

Tools of the trade

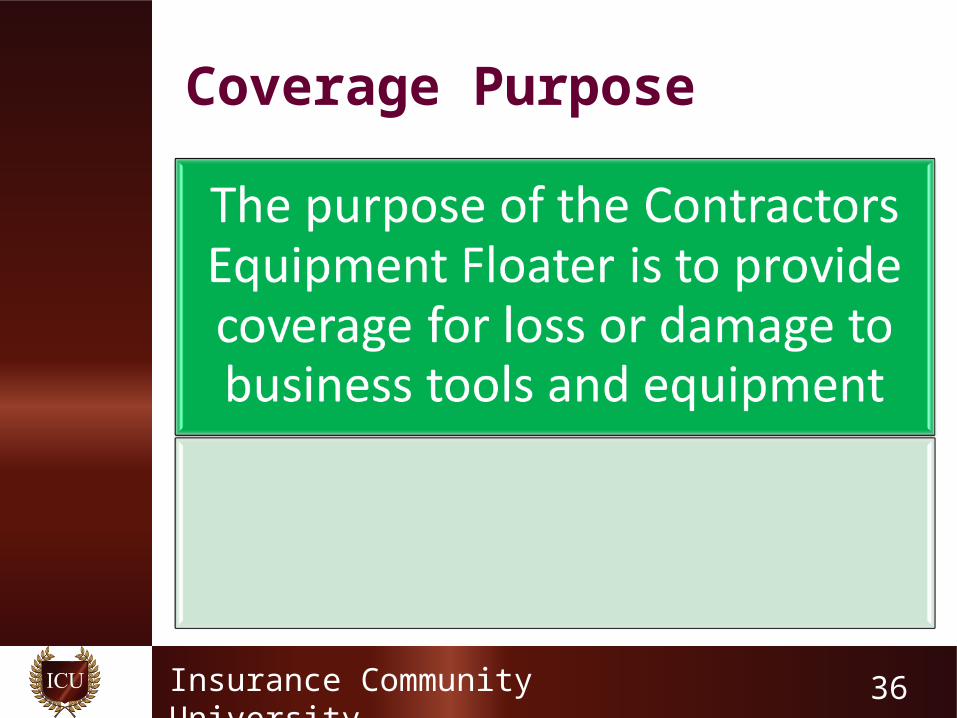

Insurance Community University

Coverage Purpose

36

Insurance Community University

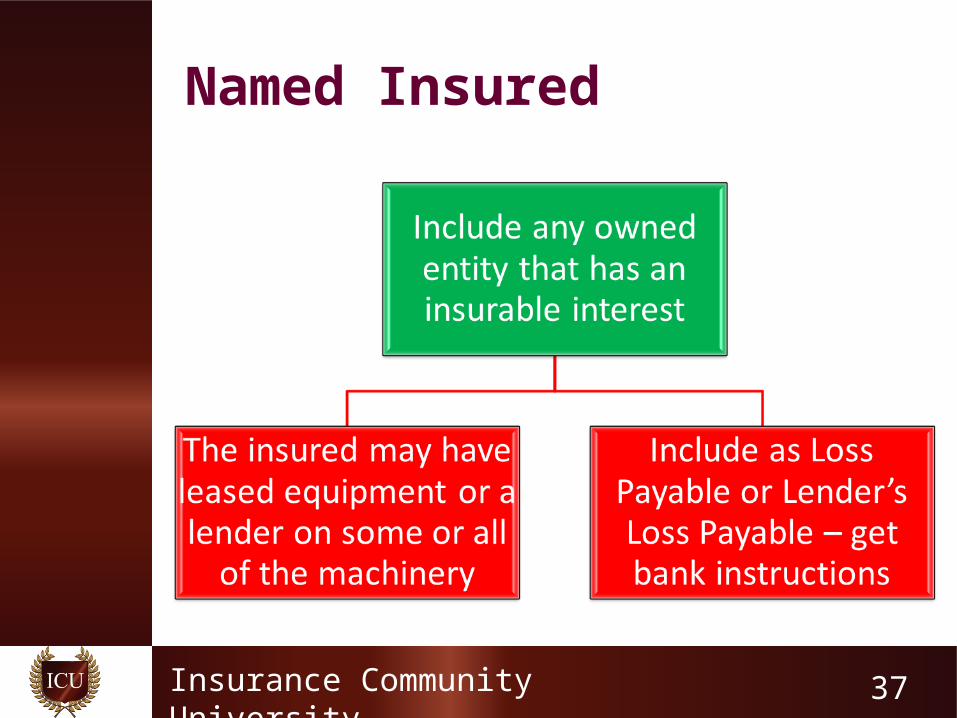

Named Insured

37

Insurance Community University

Eligible Property

Everything to get the job done

38

Insurance Community University

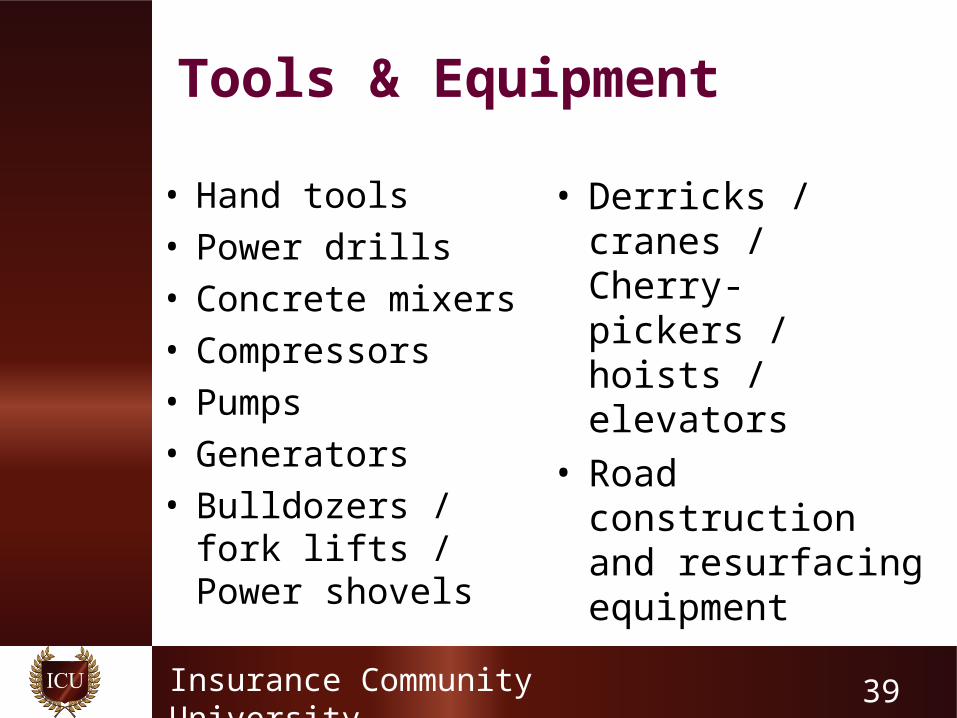

Tools & Equipment

• Hand tools• Power drills• Concrete mixers• Compressors• Pumps• Generators• Bulldozers / fork

lifts / Power shovels

• Derricks / cranes / Cherry-pickers / hoists / elevators

• Road construction and resurfacing equipment

39

Insurance Community University

Covered Property

Broad Definition

40

Insurance Community University

Owned

41

Insurance Community University

Scheduled

42

Insurance Community University

Blanket

43

Insurance Community University

Combination

44

Insurance Community University

Newly Acquired

45

Insurance Community University

Non-Owned

• NEVER assume that coverage is automatic

• Leased• Hired• Rented• Borrowed from others• Loaned to others

46

Insurance Community University

Excluded or Limited Property

Where is it covered?

47

Insurance Community University

Tools or Equipment Loaned or Rented to Others

48

Insurance Community University

Employee Tools

49

Insurance Community University

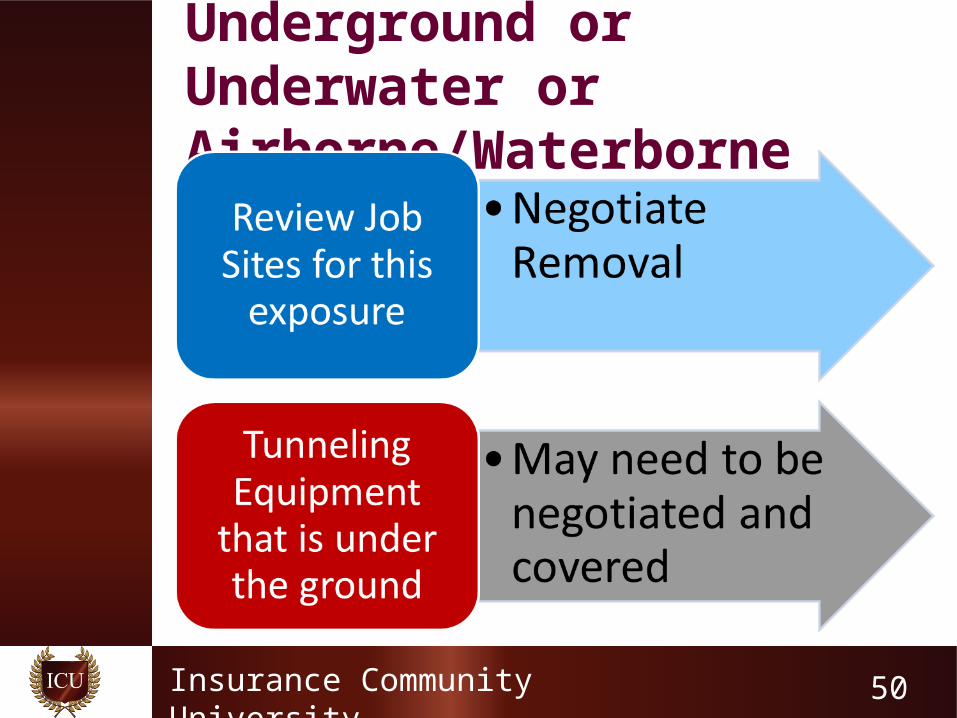

Underground or Underwater or Airborne/Waterborne

50

Insurance Community University

Vehicles Designed for Highway Use

51

Insurance Community University

BAP vs. Marine

• Highway exposure vs. job site. Don’t depend on BAP Physical Damage.

• Contractor’s equipment policy covers anywhere in policy territory.

• Can go broader than collision and other than collision coverage in BAP in tailoring consequential loss and rental reimbursement.

52

Insurance Community University

Limits and Coverage Structure

Non controlled form gives you flexibility

53

Insurance Community University

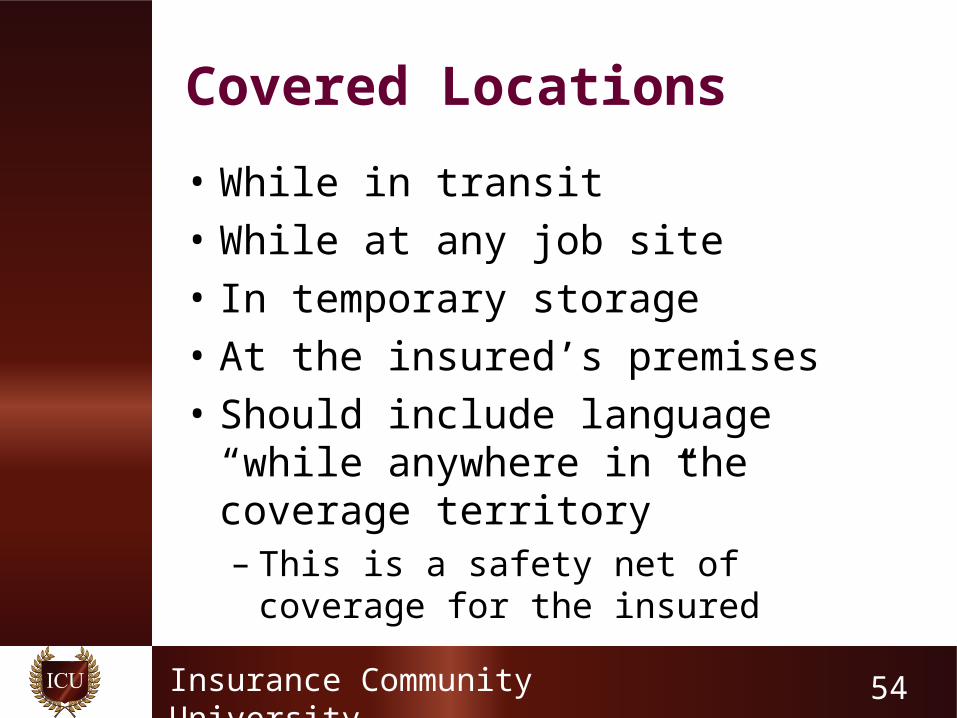

Covered Locations

• While in transit• While at any job site• In temporary storage• At the insured’s premises• Should include language “while

anywhere in the coverage territory”– This is a safety net of coverage for the

insured

54

Insurance Community University

Covered Territory

55

Insurance Community University

Coinsurance

• Most companies use coinsurance: 80%, 90%, 100%– Used to ensure that the limits of insurance

submitted are at value– Penalties will apply if the limits do not meet

or exceed the coinsurance percentage selected

• Signed statement of values• Attempt to waive coinsurance

56

Insurance Community University

Valuation

57

Insurance Community University

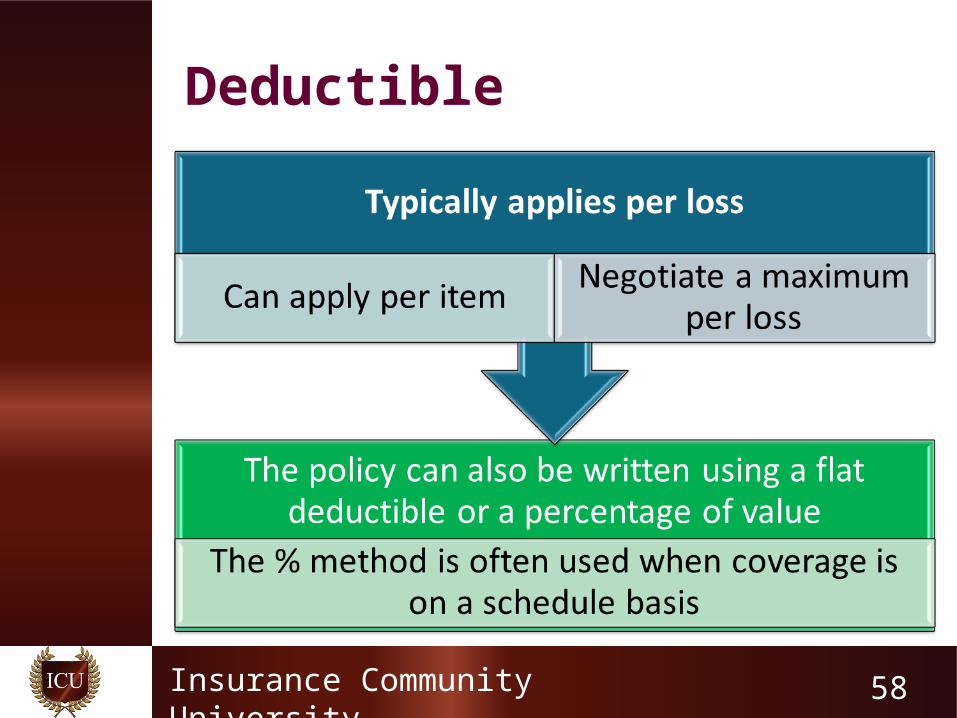

Deductible

58

Insurance Community University

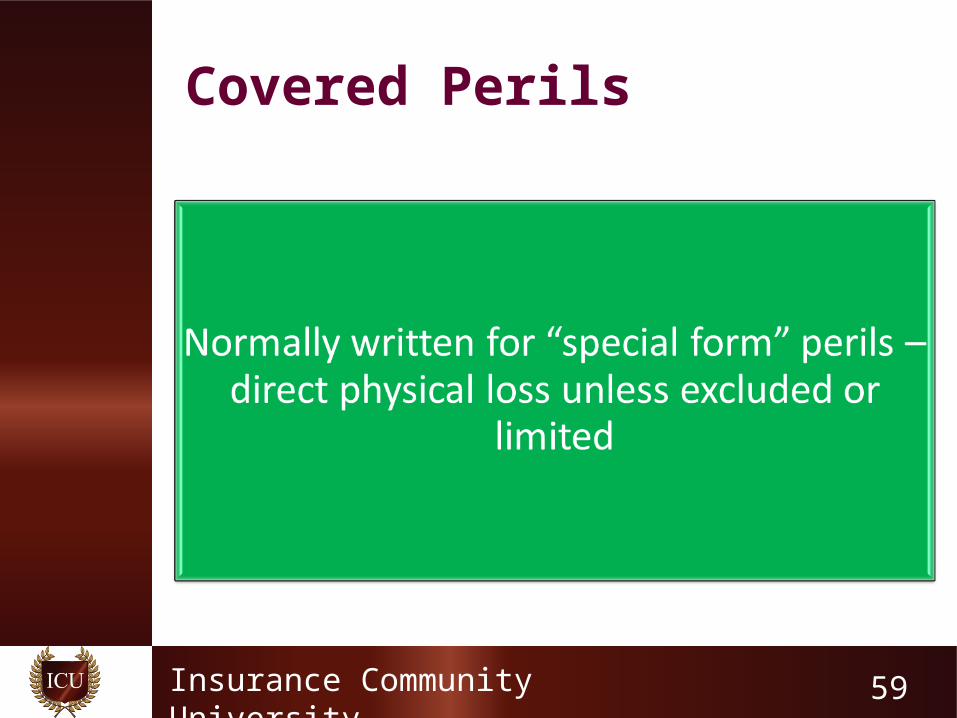

Covered Perils

59

Insurance Community University

Commonly Excluded Perils

• Inventory shortage• Dishonesty of insured, employees• Wear and tear• Gradual deterioration / Hidden or latent

defect / inherent vice• Rust, dampness, or dryness

60

Insurance Community University

Commonly Excluded Perils

• Mechanical breakdown or failure / electrical arcing

• War and nuclear• Loss to crane or derrick

– Specified perils are often covered as an exception to the exclusion

– Attempt to negotiate elimination or modification of this exclusion

61

Insurance Community University

Commonly Excluded Perils

• Weight of a load exceeding lifting capacity– Attempt to negotiate elimination or

modification of this exclusion

• Upset or overturn– This is a variation on the weight of load or

loss to crane or derrick– Attempt to negotiate elimination or

modification of this exclusion

62

Insurance Community University

Crane Considerations

63

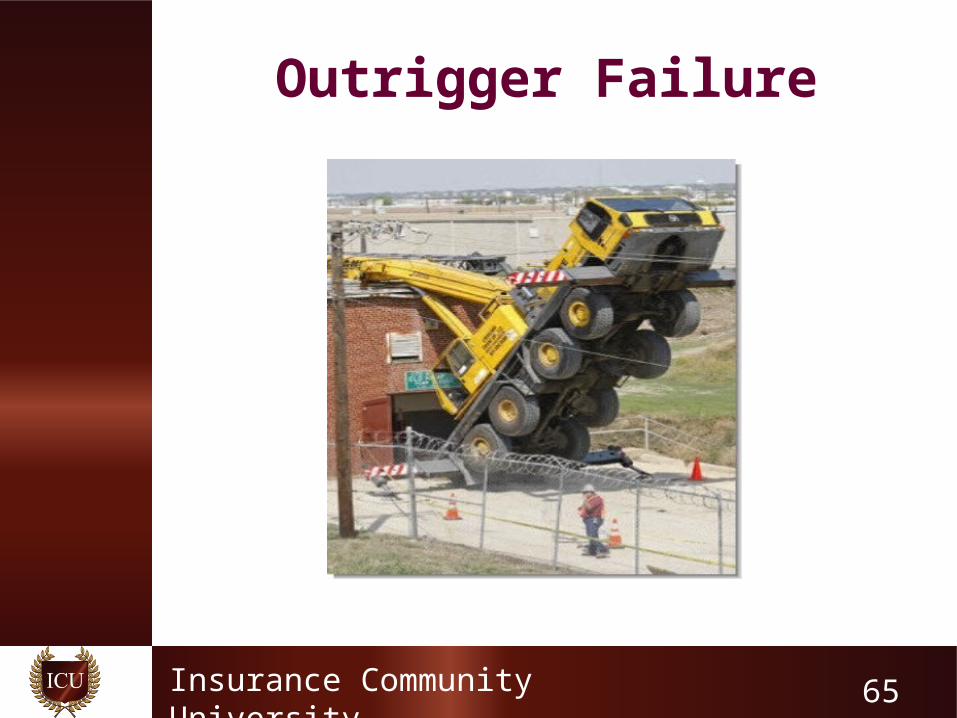

Insurance Community University

Outriggers add stability

Operator failure can have a bad outcome

64

Insurance Community University

Outrigger Failure

65

Insurance Community University

Boom goes the Crane

66

Insurance Community University

Operator training and supervision

67

Insurance Community University

Exceeded Lifting Capacity

68

Insurance Community University

Boom goes the Boom

69

Insurance Community University

Wind Damage

70

Insurance Community University

Endorsements

• Boom coverage– Removes the boom limitation– The underwriter will want to know job supervision,

operator training and experience before adding the coverage, which will often still be limited, depending on the length of the extension.

• Overload coverage– Removes the exclusion wherever possible.

71

Insurance Community University

Endorsements

• Rented, Leased or Borrowed From Others Equipment– Provides coverage for equipment that belongs to

others while in the care, custody or control of the insured

– Often limited to the type of owned property already insured

• Property loaned to others– Removes the exclusion when the insured’s own

property is in the care, custody or control of others

72

Insurance Community University

Endorsements

• Rigger’s Liability– This endorsement provides coverage for damaging

another person’s property while in the insured’s care custody or control.

– If not available on the Equipment form, check with the Inland Marine underwriter for stand alone or cross check to the CGL and ask the underwriter to consider removing or modifying the exclusion for care, custody or control in that form.

73

Insurance Community University

Low tech submission, Rigger

74

Sometimes all you need is a good dog and some rope

Insurance Community University

Consequential Losses and Optional Coverages

Loss of use issues

75

Insurance Community University

Loss of Income

• Covers loss of income arising out of a covered loss to covered property

• A time deductible may apply• This coverage may be critical, especially if the

insured has specialized or customized equipment

• Loss of the equipment may cost the insured a job

• This coverage is not widely available

76

Insurance Community University

Extra Expenses

• Time deductible may apply• Coverage applies if a consequence of

covered loss to covered property• Additional costs to repair, restore or rent

equipment• Less widely available than Rental

Reimbursement

77

Insurance Community University

Rental Reimbursement

• Limit per day with a maximum for all rental costs

• Can sometimes apply using a time deductible, such as first 24 or 48 hours

• Loss must be a consequence of a covered peril to covered property

• This coverage endorsement is often available

78

Insurance Community University

Underwriting Considerations

The more information provided with the submission, the more leeway the

underwriter will have to modify coverage

79

Insurance Community University

Underwriting Considerations

• Type of work performed and where• Type of equipment and inherent

exposures• Assists in establishing exposures and

rates.• Total values at risk• Maximum values at job sites• Employee tools

80

Insurance Community University

Underwriting Considerations

• Method of transporting equipment• Maintenance records and mechanic

qualifications• Security• At the job site and at insured’s yard or

storage facility• Where and how garaged when not in

use

81

Insurance Community University

Underwriting Considerations

• Experience of personnel• Loss history• Loss control / prevention measures• Union status and labor relations• Financial condition of insured

– Insured in poor financial condition will often skip routine maintenance, training, security, etc. thereby increasing loss potential

82

Insurance Community University

Good Supplemental Information

83

Insurance Community University

Summary

• No standard form in the industry• MUST review the form to verify it

responds for risk exposures of the insured– Not as easy as it may seem

84

Insurance Community University

The Rest Is Up To You

• A good Marine Underwriter is your best asset to tailor appropriate coverage.

• There is insurable interest during the life cycle of construction for everyone in the project.

• Help your client identify and cover theirs as an installer or contractor.

85