insurance dewas

TRANSCRIPT

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 1/16

1

³Impact of financial downturn on

insurance sector in India´

Dr. D.D. Bedia,

Reader ± Pt. Jawahar lal Nehru Institute of Business Management, Vikram University Ujjain

(M P )

Ms. Annada Padmawat.

Sr. lecturer & HR Manager- Mahakal Institute of Management, Ujjain

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 2/16

2

Abstract

This study is an attempt to find out the functions of

insurance company which are highly influenced by the

recession or financial crisis. The study is based on the

collecting information regarding impact measurement

of financial crisis on insurance sector. This paper

focuses how premium deposits are being affected by

financial downturn. In nut shell the impact of financial

crisis on insurance sector in India is not substantial.

Statistically there is no impact of financial crisis in

insurance sector and an average before crisis premium

deposits and during crisis premium deposits are same.

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 3/16

3

Introduction

In macroeconomics, recession is defined as a distinct

decline in any particular country's GDP (Gross DomesticProduct). In some other cases, when a country faces

negative real economic expansion, for two or more

successive quarters of a year, that¶s also termed as state of

recession. In general, recession affects a country¶s overalleconomic activities, including, investment, employment

rate, profits data of companies etc. Recession is almost

always accompanied by sharp increase in prices of

commodities. When recession continues for a longduration and with severe implications, it¶s termed as

economic depression whereas complete breakdown of

economy is referred as economic fall down.

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 4/16

4

This is true, Insurance Carriers in India are also struggling to

balance their funds. Top 100 companies have applied costcutting majors, giving a reason of economy slowdown, financial

crisis & Recession, giving pink slips to employees. The

slowdown in economic activities in India has lead to a sharp

reduction in asset creation in the Indian industries. This alongwith rigorous cost cutting measures in all businesses has directly

impacted the insurance industry in the country. The most

important reason for the go down in this business was that many

small and medium businesses either did not buy insurancecovers, or went for lower cover to save on premium expenditure.

Also the sharp drop in sales of commercial vehicles, tractors and

near stagnation in car sales led to a big drop in insurance

premium underwritten. Interestingly, despite the slowdown, the

insurance industry attracted many new players last year.

Introduction

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 5/16

5

Objective of the study

The main objectives of study are:

*To provide the overview of financial downturn.

*To measure the impact of financial downturn on

insurance sector.

*To study the impact of recession on premium deposits

in insurance sector.

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 6/16

6

Research Methodology

This study is an attempt to find out the functions of

insurance company which are highly influenced by therecession or financial crisis. We have taken all the data

from report, journal and website. Premium is the

important factor in various insurance companies in this

research paper, we are using secondary data for theanalysis of insurance sectors various private and public

insurance companies¶ premium. we have selected 4

insurance companies from the public sector and 3 private

life and general insurance companies from private sector and duration from 2006 to 2009.The statistical tool which

is appropriate to analyze the data to measure the impact of

financial crisis on insurance sector is paired µT µtest. With

the use of this technique, the inferences are drawn.

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 7/16

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 8/16

8

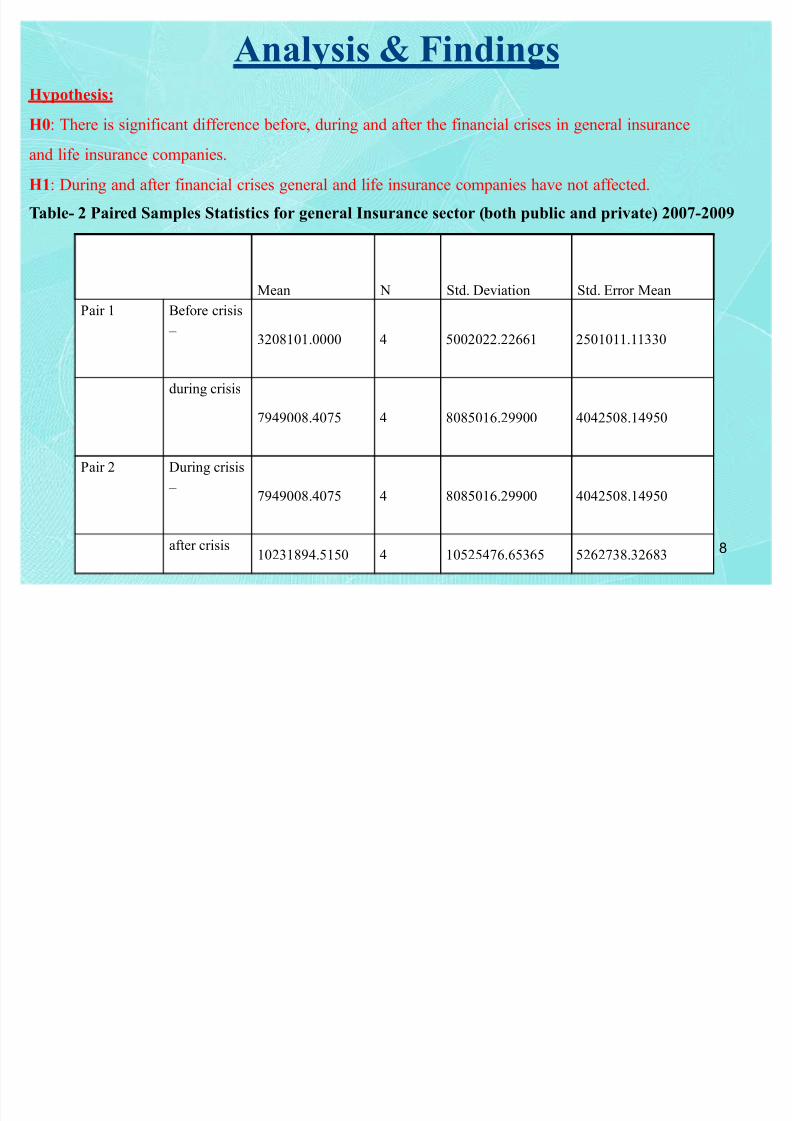

Analysis & FindingsHypothesis:

H0: There is significant difference before, during and after the financial crises in general insurance

and life insurance companies.

H1: During and after financial crises general and life insurance companies have not affected.

Table- 2 Paired Samples Statistics for general Insurance sector (both public and private) 2007-2009

Mean N Std. Deviation Std. Error Mean

Pair 1 Before crisis

± 3208101.0000 4 5002022.22661 2501011.11330

during crisis

7949008.4075 4 8085016.29900 4042508.14950

Pair 2 During crisis

± 7949008.4075 4 8085016.29900 4042508.14950

after crisis10231894.5150 4 10525476.65365 5262738.32683

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 9/16

9

Analysis & Findings

Table -3 Paired Samples Test for general Insurance sector (both public and private) 2007-2009

Paired Differences

Mean

Std.

Deviation

Std. Error

Mean

95% Confidence Interval

of the Difference t df

Sig.

(2-

tailed)

Lower Upper

Pair 1 Before crisis

± during

crisis-

4740907.407

50

6724630.61

145

3362315.305

72

-

15441295.32

940

5959480.5

1440

-

1.4103 .253

Pair2

During

crisis ± after

crisis-

2282886.107

50

2476004.74

779

1238002.373

90

-

6222762.188

24

1656989.9

7324

-

1.8443 .162

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 10/16

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 11/16

11

Analysis & Findings

Table -5 Paired Samples Test for Life Insurance (both public and private sector) 2007-2009

Paired Differences t df

Sig.

(2-

tailed)

Mean Std. Deviation

Std.Error

Mean

95% ConfidenceInterval of the

Difference

Lower Upper

Pair 1 P

Pair1

Before

crisis -

during

crisis

-30170688.83250

25163271.06939

12581635.53469

-

7021106

8.35431

9869690.68931

-2.398 3 .096

Pair 2P

Pair2

During

crisis ±

after crisis -8508125.240007396974.8091

5

3698487.

40457

-

2027836

2.81582

3262112.

33582-2.300 3 .105

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 12/16

12

Analysis & Findings

Hypothesis:

H0: There is significant difference before, during and after the financial crises in overall banking both

sectors.

H1: During and after financial crises in overall banking both sectors have not affected.

Table -6 Lives and general Insurance 2007-2009 Paired Samples Statistics

Mean N Std. Deviation Std. Error Mean

Pair 1 Before crisis

24820043.8943 7 30824081.59230 11650407.75503

-during crisis

42748664.3171 7 54260718.57226 20508623.90027

Pair 2 During crisis

42748664.3171 7 54260718.57226 20508623.90027

-after crisis

48235201.9443 7 60661817.11550 22928011.73784

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 13/16

13

Analysis & Findings

Table -7 Insurance sector (public and private both) 2007-2009 Paired Samples Test

Paired Differences t df

Sig. (2-

tailed)

MeanStd.Deviation

Std.

Error Mean

95% Confidence Interval of the Difference

Lower Upper

Pair 1 Before

crisis ±

during

crisis

-

17928620.

42286

23509078.

94792

8885596

.63548

-

39670892.1

3472

3813651.2890

0-2.018 6 .090

Pair 2 During

crisis ±

after crisis

-

5486537.6

2714

6577495.0

9441

2486059

.46708

-

11569705.9

9979

596630.74551 -2.207 6 .069

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 14/16

14

Conclusion

When we see in comparative analysis of public and private insurance

sector, even both have face the crises but in public sector there was

not the condition of jobless situation, cost cutting situation and people

had faith on LIC on that time also, but because of financial meltdown

people might be not able to invest the money even in LIC, but in

private sector there was worst situation in inside of the companies,

very much pressure on employees to sale the products, cost cutting

situation have faced by many private insurance sector, there old

products were not in running position and new one were almost

failed.

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 15/16

15

Conclusion

In conclusion, the impact of financial crisis on insurance sector in

India is not substantial. Statistically there is no impact of financial

crisis in insurance sector and an average before crisis premium

deposits and during crisis premium deposits are same. There is no

difference between average premium deposits during the crisis and

after the financial crisis. Thus it is clear that there is no effect of

financial crisis in insurance sector both in life insurance and general

insurance.

8/6/2019 Insurance Dewas

http://slidepdf.com/reader/full/insurance-dewas 16/16

16

Dr. D.D. Bedia

Ms. Annada Padmawat