insurance memaid 2008

TRANSCRIPT

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 1/32

San Beda College of Law2008 CENTRALIZED BAR OPERATIONS

INSURANCE CODEINSURANCE CODEPresidential Decree No. 612Presidential Decree No. 612

CONTRACT OF INSURANCE

CONTRACT OF INSURANCE An agreement whereby one undertakes for aconsideration to indemnify another againstloss, damage or liability arising from anunknown or contingent event (Sec.2, par.2,Insurance Code of the Philippines).

GOVERNING LAWS

1. Insurance Code; or, in its absence2. Civil Code; or, in the absence of both,3. General principles prevailing on the

subject in the United States, particularly inthe State of California where our Insurance Code was based.

ELEMENTS OF THE CONTRACT (RAPIS)

1. INSURABLE INTEREST – The insuredhas an insurable interest in the life or thinginsured, i.e. a pecuniary interest;

2. R ISK OF LOSS – The happening of

designated events, either unknown or contingent, past or future, will subject suchinterest to some kind of loss, whether inthe form of injury, damage or liability;

3. A SSUMPTION OF RISK – the insurer undertakes to assume the risk of such lossfor a consideration;

4. PAYMENT OF PREMIUM – theconsideration for the insurer’s promise toassume the risk and pay the losses fromsuch risk;

5. S CHEME TO DISTRIBUTE THE LOSSES – the assumption of risk is part of ageneral scheme to distribute the lossamong a large number of personsexposed to similar risks.

NATURE OF INSURANCE CONTRACT

(CAC-V- CUP2)

1. C ONSENSUAL – it is perfected by themeeting of the minds of the parties;

2. V OLUNTARY – the parties mayincorporate such terms or conditions asthey may deem convenient;

3. A LEATORY – the liability of the insurer isdependent on the happening of an event

which is uncertain, or though certain, is tooccur at some future undetermined time.(Article 2010, New Civil Code [NCC]).It is not, however, a gambling or wagering

EXECUTIVE COMMITTEE

VISMARCK UY over-all chair, APRIL CABEZA chair academics operations, ALDEAN LIMchair hotel operations, AYN SARSABA vice chair for operations, ANTHONY PURGANAN vicechair for academics,RONALD JOHN DECANO vice chair for secretariat, KARLA FUNTILA vice chair for finance, JEFFREY GALLARDO vice chair for edp, ULYSSES GONZALES vice chair for logistics

COMMERCIAL LAW

REINIER PAUL R. YEBRA subject chairANSON T. LAPUZ assistant chairFATIMA ANNE C. ZAMORA edpANSON T. LAPUZ code of commerce, JENNY VI H. MAGUGAT negotiable instruments law,CLARIBELLE S. BAUTISTA insurance, RALPH DAVID D. SO and MARA NADIA C. ELEFAÑOtransportation law, REXIE MAY E. MAGSANO corporation law, FRANCESCA LOURDES M.SENGA banking laws, BETHEENA C. DIZON law on intellectual property, PRINCESSITA M. YULDE special laws

MEMBERS: Colleen Infante, Andro Julio Quimpo, Jan Reyes, Anthony Menzon, Marife

Andal, Rayhanah Abubacar, Francis James Brillantes, , Jay Masangcay, Belle Salas,Charity Jimenez, Richardson Bassig, Leopoldo Aquino, Carlo Bautista, Raul Canon, KarlaFuntila, May Pandoy, Benedicto Claravall, Melanie Valenciano, Kring Carayugan, EvaNaparan, Paula Laureano, Kate Asilo, Ivy Galang, Masha Mariano, Diane Therese Dauz,Robert de Guzman, Jan Allyson Vitug, Agnes Pader, CJ Batalla, Leonardo Mendoza, JayCelzo, Maria Teresa Flaminiano, Rodrigo Melchor Jr., Jan Ale Fajardo, Joyce Maika Tolentino, Precious Lledo, Emilio Marañon III

4

9

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 2/32

MEMORY AID IN COMMERCIAL LAW

Insurance

contract where the risk is created by thecontract itself.

4. U NILATERAL – imposes legal duties only

on the insurer who promises to indemnifyanother in case of loss; executed as to theinsured after payment of premium, andexecutory on the part of the insurer untilpayment for a loss.

5. C ONDITIONAL – it is subject toconditions, the principal one of which isthe happening of the event insuredagainst.

6. C ONTRACT OF INDEMNITY – Except lifeand accident insurance where the result isdeath, a contract of insurance is a contract

of indemnity whereby the insurer promisesto make good only the loss of the insured.

7. P ERSONAL – each party having in viewthe character, credit and conduct of theother.

8. P ROPERTY – since an insurance is acontract, as such, it is property in legalcontemplation.

SURETY CONTRACT AS INSURANCE A contract of suretyship shall be deemed to bean insurance contract, within the meaning of

the Code, only if made by a surety who or which, as such, is doing an insurancebusiness.

“Doing an Insurance Business”:1. making or proposing to make, as insurer,

any insurance contract;2. making or proposing to make, as surety,

any contract of suretyship as a vocationand not as merely incidental to anylegitimate business or activity of thesurety;

3. doing any kind of business, including

reinsurance business, specificallyrecognized as constituting the doing of aninsurance business within the meaning of the Code;

4. doing or proposing to do any business insubstance equivalent to any of theforegoing in a manner designed to evadethe provisions of this Code (Sec.2, par.4).

Note: The fact that NO profit is derivedfrom the making of insurance contracts,agreements or transactions or that no

separate or direct consideration isreceived therefor, shall NOT be deemedconclusive to show that the making thereof does not constitute the doing or transacting of an insurance business.

FIVE CARDINAL PRINCIPLES IN INSURANCE(I-SIGA)

1. INSURABLE INTEREST – relation

between the insured and the event insuredagainst such that occurrence of the eventwill cause substantial loss or harm of some kind to the insured.

2. PRINCIPLE OF UTMOST GOOD FAITH(uberrimae fides) – Each party takes intoconsideration the character, conductand/or credit of the other and in makingthe contract, each is enjoined by law todeal with the other in utmost good faith. Aviolation of this duty gives the aggrievedparty the right to rescind the contract.

3. CONTRACT OF INDEMNITY – Theinsured who has insurable interest over aproperty is only entitled to recover theamount of actual loss sustained and theburden is upon him to establish theamount of such loss.

Note: A life insurance is NOT a contract of indemnity. It is considered an investment. A life policy constitutes, through theinsured’s savings, his investment and theearnings thereon, a measure of economicsecurity for the insured during his lifetimeand for his beneficiary after his death

(Insurance, Maria Clara L. Campos,1983ed).

Insurance contracts are not wageringcontracts or gambling contracts.

Reason: It is not a contract of chanceand it is not used for profit.

WAGERINGCONTRACT

CONTRACT OFINSURANCE

The partiescontemplate gain

through mere chance

The parties seek todistribute the possible

loss by reason of

mischanceGambler courts

misfortuneInsured seeks to avoid

misfortune

Tends to increase theinequality of fortune

Tends to equalizefortune

Essence of gambling isthat whatever one winsfrom a wager is lost by

the other wageringparty

The gains of the oneinsured are not at theexpense of another

insured

As soon as the partymakes a wager, he

creates a risk of loss tohimself where no such

risk existed previously

The purchase of insurance does not

create a new and non-existing risk of loss to

the purchaser

4. CONTRACT OF ADHESION (Fine Print Rule) – The policy is presented to theinsured already in its printed form, so that

50

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 3/32

San Beda College of Law2008 CENTRALIZED BAR OPERATIONS

he either “takes it or leaves it.” Most of theterms of the contract do not result frommutual negotiations between the partiesas they are prescribed by the insurer in

final printed form to which the insured may“adhere” if he chooses but which hecannot change (Rizal Surety andInsurance Co. vs. CA, GR No. 112360,336 SCRA 12, July 18, 2000). It is for this reason that any ambiguity therein isresolved in favor of the insured andagainst the insurer.

5. PRINCIPLE OF SUBROGATION – If theplaintiff’s property has been insured, andhe has received indemnity from theinsurance company for the injury or loss

arising out of wrong or breach of contractcomplained of, the insurance companyshall be subrogated to the rights of theinsured against the wrongdoer or theperson who has violated the contract.

If the amount paid by the insurancecompany does not fully cover the injury or loss, the aggrieved party shall be entitledto recover the deficiency from the personcausing the loss or injury (Article 2207NCC).

Note: The principle of subrogation is a

normal incident of indemnity insurance asa legal effect of payment; it inures to theinsurer without any formal assignment or any express stipulation to that effect in thepolicy. Said right is not dependent uponnor does it grow out of any privatecontract. Payment to the insured makesthe insurer a subrogee in equity (MalayanInsurance Co., Inc. vs. CA, GR No. L-36413, September 26, 1988).

Incapacity of the insured will not affect thecapacity of the subrogee because capacity

is personal to the holder (LorenzoShipping vs. Chubb and Sons, Inc,431 SCRA 266, June 8, 2004).

Purposes of Subrogation:1. To make the person who caused the

loss legally responsible for it;2. To prevent the insured from receiving

double recovery from the wrongdoer and the insurer; and

3. To prevent the tortfeasors from beingfree from liability and is thus foundedon considerations of public policy.

Rules on Subrogation:1. Applicable only to property insurance.

Reason: The value of human life isregarded as unlimited andtherefore, no recovery from a third

party can be deemed adequate tocompensate the insured’sbeneficiary.

2. The insurer can only recover from the

third person what the insured couldhave recovered.

NO SUBROGATION:1. Where the insured by his own act

releases the wrongdoer or third partyliable for the loss or damage;

2. Where the insurer pays the insuredthe value of the loss without notifyingthe carrier who has in good faithsettled the insured’s claim for loss;

3. Where the insurer pays the insured for a loss or risk not covered by the policy(Pan Malayan Insurance Company vs. CA, GR No. 77397 184 SCRA54, April 3, 1990);

4. In life insurance;5. For recovery of loss in excess of

insurance coverage;

Note: Should the insured, after receivingpayment from the insurer, release by hisown act the wrongdoer or third partyresponsible for the loss or damage fromliability, the insurer loses his rights againstthe wrongdoer since the insurer can onlybe subrogated to only such rights as theinsured may have (Manila Mahogany Mfg. Corp. vs. CA, GR No. L-52756,154 SCRA 668, October 12, 1987).

WHAT MAY BE INSURED AGAINST/ RISK:1. Any contingent or unknown event,

whether past or future, which may damnifya person having an insurable interest or creates a liability against him may beinsured against (Sec. 3).

2. A past event may be insured provided the

loss is unknown to both parties and theyexpressly stipulated that prior loss isinsured by the policy.

3. Contingent liability – E.g. Reinsurance

Note: Insurance for or against the drawingof any lottery, or for or against any chanceor ticket in a lottery drawing a price is notallowed (Sec. 4). It may result in profitwhich is not true in insurance which onlyseek to indemnify the insured againstlosses.

REQUISITES FOR RECOVERY UPONINSURANCE (CLIP)

1. The insured must have insurable interestin the subject matter;

2. That interest is covered by the policy;3. There must be a loss; and

51

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 4/32

MEMORY AID IN COMMERCIAL LAW

Insurance

4. The loss must be proximately caused bythe peril insured against.

CONSTRUCTION OF INSURANCE CONTRACT

1. The terms in an insurance policy which areambiguous, equivocal, or uncertain are tobe construed strictly and most stronglyagainst the insurer, and liberally in favor of the insured so as to effect the dominantpurpose of indemnity or payment to theinsured.

Reason: The insured usually has no voicein the selection or arrangement of thewords employed and that the language of the contract is selected with great careand deliberation by experts and legal

advisers employed by, and actingexclusively in the interest of, the insurancecompany (Calanoc v. Court of Appeals, et al., GR No. L-8218, 98SCRA 98, December 15, 1955). If theterms are clear, there is no room for interpretation.

2. “Intentional” as used in an accidentpolicy excepting intentional injuriesinflicted by the insured or any other person, etc. implies the exercise of reasoning, consciousness, and volition.Where a provision of the policy excludes

intentional injury, it is the intention of theperson inflicting the injury that iscontrolling (Biagtan v. The Insular Life Assurance Company, Ltd., GR No.25579, 44 SCRA 59, March 29, 1972).

3. The terms accident and accidental, asused in insurance contracts have notacquired any technical meaning, and areconstrued in their ordinary and commonacceptation. Thus, the terms mean thosethat which happen by chance or fortuitously, without intention or design,

and which is unexpected, unusual, andunforeseen.

An accident is an event that takes placewithout one’s foresight or expectation – anevent that proceeds from an unknowncause or is an unusual effect of a knowncause and therefore, not expected(Finman General Assurance Corp. v.Court of Appeals, GR No. 94588, 213SCRA 493, July 2, 1992).

4. An “Authorized Driver” clause limits theuse of the insured vehicle to two personsonly, namely: (1) the insured himself; or (2) any person on his (insured’s)permission.

The main purpose of the “authorizeddriver” clause is that a person other than

the insured owner, who drives the car onthe insured’s order, such as, his regular driver, or with his permission, such as afriend or member of the family or the

employees of a car service or repair shopmust be duly licensed drivers and have nodisqualification to drive a motor vehicle(Villacorta v. Insurance Commission,GR No. L-54171, 28 SCRA 467,October 28, 1980).

PERFECTION OF AN INSURANCE CONTRACT1. An insurance contract is a consensual

contract and is therefore perfected themoment there is a meeting of minds withrespect to the object and the cause or consideration.

2. Insurance contracts throughcorrespondence follow the “cognitiontheory” “an acceptance made by letter shall not bind the person making the offer except from the time it came to hisknowledge” (Enriquez vs. Sun Life Assurance Co. of Canada, GR No. L-15774, 41 Phil. 269, November 29,1920).

PARTIES TO THE CONTRACT

1. INSURER – the party who assumes or accepts the risk of loss and undertakes for a consideration to indemnify the insured or to pay him a certain sum on the happeningof a specified contingency or event. Every person, partnership, association, or corporation duly authorized to transact insurance business may be an insurer (Sec. 6).

Insurance Corporation – corporationformed or organized to save any person or other corporations harmless from loss,

damage, or liability arising from anyunknown or future or contingent event or to indemnify or to compensate any personor persons or other corporation for anysuch loss, damage, or liability or toguarantee the performance of or compliance with contractual obligations or the payment of debt of others. (Sec. 185)

a. It must have sufficient capital and assets required under theInsurance Code and the pertinentregulations issued by theCommission (Sec. 186);

b. It must have a certificate of authority to operate issued by theInsurance Commission whichshould be renewed every year.(Sec. 187).

52

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 5/32

San Beda College of Law2008 CENTRALIZED BAR OPERATIONS

Foreign Insurance Corporations – mayengage in insurance business in thePhilippines provided the followingrequirements are met:

a) The appointment of a resident of thePhilippines as a general agent onwhom any notice or proof of loss maybe served and on whom summonsand other processes may be served;

b) It must possess paid-up unimpairedassets or capital and reserve not lessthan that required of domesticcorporations;

c) It must deposit for the benefit andsecurity of policyholders, securitiessatisfactory to the Commission.

d) Its investments should not exceed20% of the net worth of foreigncorporation or 20% of the capital of theregistered enterprise.

2. INSURED – the person in whose favor thecontract is operative and who isindemnified against, or is to receive acertain sum upon the happening of aspecified contingency or event. Anyoneexcept a public enemy may be insured.(Sec. 7)

Public enemy – citizen or subject of anation at war with the Philippines anddoes not include robbers thieves andother criminals.

Reason: The purpose of war is to cripplethe power and exhaust the resources of the enemy, and it is inconsistent that onecountry should destroy its enemy’sproperty and repay in insurance the valueof what has been so destroyed, or that itshould in such manner increase theresources of the enemy, or render it aid(Filipinas Cia de Seguros v.

Christern Huenfeld & Co., Inc., GRNo. L-2294, 89 Phil., May 25, 1951).

Insurance by a minor (Sec. 3, par. 3)has been rendered moot and academic byRepublic Act 6809 which reduced themajority age from 21 to 18 years of age.Hence, a person who is 18 years or moremay enter into any kind of insurancecontract because he is already of legalage.

Insurance by a married woman A married woman may take out aninsurance on her life or that of her childrenwithout the consent of her husband (Sec.3 [2]), or that of her husband, having aninsurable interest in the latter (Sec. 10).

However, while either spouse mayexercise any legitimate profession,occupation, business or activity without theconsent of the other, the latter may object

on valid, serious and moral grounds (Art.73, Family Code).

3. CESTUI QUE VIE and BENEFICIARYCestui que vie is the person on whose lifethe insurance is written. The beneficiary isthe person designated to receive theproceeds of the policy when the riskattaches.

Illustration: A husband may take out apolicy on his wife’s life, proceeds payableto their son. The husband is the insured,the wife is the cestui que vie, and the sonis the beneficiary.

Kinds of Beneficiary:a) Insured himself;b) Third person who paid a

consideration; or c) Third person through mere bounty of

insured.

• In the second and third cases, the

beneficiary is not a party to thecontract. Art. 1311 (2 nd par.), NCC

allows the contracting parties toinclude a stipulation in favor of a thirdperson not a party to the contract.

Persons who cannot be named Beneficiary Any person who is forbidden fromreceiving any donation under Art. 739cannot be named beneficiary of a lifeinsurance policy by the person whocannot make any donation to him (Art.2012, NCC), to wit:a) Those who are guilty of adultery or

concubinage with the insured at the

time of designation;b) Those who were found guilty with theinsured of the same criminal offense,committed in consideration of thedesignation;

c) A public officer or his wife,descendants and ascendantsdesignated by reason of his office(Article 739, NCC).

Note: This prohibition will apply ONLYto life insurance policies (Art. 2012,NCC).

Right to change Beneficiary:GENERAL RULEThe insured shall have the right to changethe beneficiary he designated in the policy.

53

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 6/32

MEMORY AID IN COMMERCIAL LAW

Insurance

• The beneficiary acquires NO

vested right but only anexpectancy of receiving theproceeds under the insurance.

• The right may be exercised in themanner provided in the policy.

• The right ceases upon the

insured’s death. It may not beexercised by his representatives.

EXCEPTIONIf the right to change the beneficiary isEXPRESSLY WAIVED in the policy, thenthe insured has no power to make suchchange without the consent of thebeneficiary.

•The beneficiary acquires a vestedright in the policy. Suchbeneficiary, to whom a policy of insurance upon life or health haspassed by transfer, will or succession, may recover upon itwhatever the insured might haverecovered (Sec. 181, InsuranceCode).

• If the insured refuses to pay the

premiums, the designatedirrevocable beneficiary maycontinue the policy by paying

premiums that are due (Art.1236, NCC).

EXCEPTION TO THE EXCEPTIONUnder Articles 43(4), 50 and 64 of theFamily Code, the innocent spouse mayrevoke the designation of the other spouse who acted in bad faith asbeneficiary in any insurance policy,EVEN if such designation be stipulatedas irrevocable.

When the beneficiary dies before the insured:

1. Should the beneficiary predecease theinsured and such beneficiary isirrevocable, and hence has a vestedinterest in the policy, the legalrepresentatives of such beneficiary areentitled to the proceeds of theinsurance as assets of his or her estate, unless the proceeds weremade payable to the beneficiary only“if living”.

2. On the other hand, where thebeneficiary is revocable and thereforedoes not have vested interest in the

policy at the time of his death, hisestate or legal representatives deriveno interest from or through him, butthe proceeds passes to the estate of the insured.

3. In case of an insurance policy takenout by an original owner on the life or health of a minor , all rights, title andinterest in the policy shall

automatically vest in the minor uponthe death of the original owner, unlessotherwise provided for in the policy(Sec. 3, par. 5).

INSURABLE INTEREST

INSURABLE INTERESTThe relation between the insured and theevent insured against such that the occurrenceof the event will cause substantial loss or harmof some kind to the insured.

1. LIFE INSURANCE – Insurable interest inlife exists when there is reasonable groundfounded on the relation of the parties,either pecuniary or contractual or by bloodor affinity, to expect some benefit or advantage from the continuance of the lifeof the insured.

2. PROPERTY INSURANCE – Every interestin property, whether real or personal, or any relation thereto, or liability in respect

thereof, of such nature that acontemplated peril might directly damnifythe insured.

PURPOSES1. Based upon considerations which render

wager policies invalid. Without suchinsurable interest, the contract would ineffect be a mere wager or gamblingcontract which is void .

2. Measure of the upper limit of his provableloss under the contract.

INSURABLE INTEREST IN LIFEINSURANCE

1. Where the insured is also the cestui que vie(Insurance upon one’s life)

• A person has an insurable interest in

his own life and health (Sec. 10[a]).

• The insured can make it payable to

anyone he chooses, regardless of whether or not such beneficiary has aninsurable interest in his (insured’s) life.

• Upon the insured’s death, the

beneficiary shall be entitled to the full

face value of the policy.• It is assumed that the insured would

not designate as his beneficiary aperson whom he would not trust hislife.

54

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 7/32

San Beda College of Law2008 CENTRALIZED BAR OPERATIONS

2. Where the insured is not the cestui que viebut is the beneficiary (insurable interest inthe life of another)

• Where a person names himself

beneficiary in a policy he takes on thelife of another, he must have insurableinterest in the life of the latter.

• Sec. 10 specifies the person in whose

life the insured has an insurableinterest, to wit:

a) On himself, of his spouse, and of his children – the insured beneficiaryneed not prove insurable interestbecause he is presumed to have aninsurable interest on the life hisspouse or his children.

The husband and wife as well asparent and child do have somepecuniary interest in each other’s lifesince they are legally obliged tosupport each other.

b) Of any person on whom hedepends wholly or in part for education or support, or in whomhe has pecuniary interest – wherethe relationship is not as close asthose mentioned above, the insured-beneficiary will be like any other

stranger – i.e. he will have to provethat he has some pecuniary interest inthe life of the cestui que vie, otherwisethe policy will be void.

c) Of any person under legal obligation to him for the payment of money, or respecting property or services of which death or illnessmight delay or prevent performance.

d) Of any person upon whose life or estate vested in him depends.

3. Creditor of insured as beneficiary

• A creditor may name himself as

beneficiary in a policy he takes on thelife of his debtor. The death of thedebtor may either prevent payment if his estate is not sufficient to pay hisdebts or delay such payment if anadministrator has to be appointed tosettle his estate.

• Except Sec. 10 (par. a) of the ICP, an

insurance contract thereunder partakes the nature of a contact of

indemnity. Hence, the creditor’srecovery upon the death of the debtor should be limited to the amount of hisinterest, i.e. the amount owing to him.

• BUT if the debtor is the insured and

the creditor is named beneficiary, the

creditor will be entitled to the WHOLEproceeds of the policy upon thedebtor’s death, though his credit maybe much less.

4. Business associate or employer of insured

• A person may take a policy on the life

of his business partner because thelatter’s death may result in aninterruption of business operationswhich can in turn cause financial loss.

• A business firm can take out a policy

on the life of its officers or employeeswhose services proved valuable to thebusiness. The proceeds are nottaxable income but constitute

indemnity to the employer for the losswhich the business suffers because of the death of a valued officer or employee.

Consent of the Cestui que vie:1. First View – Consent is essential to the

validity of policy. It is believed that allsuch contracts (without the consent of theinsured) are contrary to public policy andvoid.

2. Second View – Under our law (Sec. 10),the consent of the person insured is not

essential to the validity of the policy. Solong as it could be proved that the assuredhas a legal insurable interest at theinception of the policy, the insurance isvalid even without such consent.

TIME OF EXISTENCE –GENERAL RULEInsurable interest in life or health must existwhen the insurance takes effect, but need notexist thereafter or when the loss occurs (Sec.19).

EXCEPTIONS1. When the insurance is taken by the

creditor on the life of the debtor, thecreditor is required to have an insurableinterest not only at the time of the contractbut also at the time of the debtor’s deathbecause in this case, it is considered as acontract of indemnity.

2. When the insurance is taken by theemployer on the life of the employee (ElOriente Fabrica de Tabacos, Inc. v.Posadas, GR No. 34774, September 21, 1931).

INSURABLE INTEREST IN PROPERTY

An insurable interest in property may consistin:

55

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 8/32

MEMORY AID IN COMMERCIAL LAW

Insurance

1. An existing interest – the existinginterest in the property may be legaltitle or equitable title.

Examples of insurable interest arising from legal title:a. Trustee, as in the case of the

seller of property not yet delivered;

b. Mortgagor of the property mortgaged;

c. Lessor of the property leased

Examples of insurable interest arising from equitable titlea. Purchaser of property before

delivery or before he has performed the conditions of the

sale;b. Mortgagee of property mortgaged;c. Mortgagor, after foreclosure but

before the expiration of the period within which redemption isallowed .

2. An inchoate interest founded on anexisting interestExample: A stockholder has aninchoate interest in the property of thecorporation of which he is astockholder, which is founded on an

existing interest arising from hisownership of shares in thecorporation.

3. An expectancy, coupled with anexisting interest in that out of which theexpectancy arises

• Expectancy to be insurable must be

coupled with an existing interest(Sec. 14) or founded on an actualright to the thing or upon any validcontract for it (Sec. 16).

MEASURE OF INSURABLE INTEREST INPROPERTY: The measure of insurable interestin property is the extent to which the insuredmight be damnified by loss or injury thereof (Sec. 17).

Insurable interest in property does notnecessarily imply a property interest in, or alien upon, or possession of, the subject matter of the insurance, and neither title nor abeneficial interest is requisite to the existencethereof. It is sufficient that the insured is sosituated with reference to the property that hewould be liable to loss should it be injured or destroyed by the peril against which it isinsured. Anyone has an insurable interest inproperty who derives a benefit from itsexistence or would suffer loss from its

destruction (Gaisano Cagayan, Inc. vs.Insurance Company of North America,GR No. 147839, June 8, 2006).

TIME OF EXISTENCE An interest in property insured must exist whenthe insurance takes effect AND when the lossoccurs, but need not exist in the meantime(Sec. 19).

INSURABLEINTEREST INPROPERTY

INSURABLEINTEREST IN LIFE

Extent

Insurable interest islimited to the actualvalue of the interest

thereon

Insurable interest in life isunlimited (save in life

insurance effected by acreditor on the life of the

debtor)

Existence of insurable interestMust exist when the

insurance takes effect AND when the lossoccurs, but need not

exist in the meantime.

It is enough that interestexist at the time the policytakes effect and need not

exist at the time of theloss.

Basis of expectation

There must be legalbasis

Expectation of the benefitderived need not have

legal basis

Insurable Interest

The beneficiary musthave an insurableinterest in the thing

insured.

If the insured secured thepolicy, the beneficiary

need not have insurableinterest over the life of theinsured; if secured by thebeneficiary, the latter musthave insurable interest in

the life of the insured.

SPECIAL CASES:1. In case of a carrier or depository

A carrier or depository of any kind has aninsurable interest in a thing held by him assuch, to the extent of his liability but not to

exceed the value thereof (Sec. 15). Reason: The loss of the thing by thecarrier or depository may cause liabilityagainst him to the extent of its value.

2. In case of a mortgaged propertyThe mortgagor and mortgagee each havean insurable interest in the propertymortgaged and this interest is separateand distinct from the other. Therefore,insurance taken by one in his name onlyand in his favor alone does not inure to thebenefit of the other.a) MORTGAGOR – As owner, has an

insurable interest therein to the extentof its value, even though the mortgagedebt equals such value.

56

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 9/32

San Beda College of Law2008 CENTRALIZED BAR OPERATIONS

Reason: The loss or destructionof the property insured will notextinguish the mortgage debt.

b) MORTGAGEE – His interest is only up

to the extent of the debt. Such interestcontinues until the mortgage debt isextinguished.

Reason: The property relied on asmortgaged is only a security. Ininsuring the property, he is notinsuring the property itself but hisinterest or lien thereon.

Note: In case of an insurance taken by themortgagee alone and for his benefit, themortgagee, after recovery from the insurer, isnot allowed to retain his claim against themortgagor but it passes by subrogation to theinsurer to the extent of the insurance moneypaid (Palileo vs. Cosio, GR No. L-7667,November 28, 1955).

The lessor cannot be validly a beneficiary of afire insurance policy taken by a lessee over hismerchandise, and the provision in the leasecontract providing for such automaticassignment is void for being contrary to lawand public policy (Cha vs. Court of Appeals, GR No. 124520, August 18,1997).

STANDARD ORUNION MORTGAGE

CLAUSE

OPEN OR LOSSPAYABLE

MORTGAGECLAUSE

Subsequent acts of themortgagor CANNOTaffect the rights of the

assignee.

Acts of the mortgagor affect the mortgagee.Reason: Mortgagor

does not cease to be aparty to the contract(Secs. 8 and 9).

Effects of Loss Payable Clause:1. The contract is deemed to be upon theinterest of the mortgagor; hence, he doesnot cease to be a party to the contract;

2. Any act of the mortgagor prior to the loss,which would otherwise avoid the insuranceaffects the mortgagee even if the propertyis in the hands of the mortgagee;

3. Any act, which under the contract of insurance is to be performed by themortgagor, may be performed by themortgagee with the same effect;

4. In case of loss, the mortgagee is entitled

to the proceeds to the extent of his credit;5. Upon recovery by the mortgagee to the

extent of his credit, the debt isextinguished.

• The rule on subrogation by the insurer

to the right of the mortgagee does notapply in this case.Reason: Premium payment has beenpaid by the mortgagor and not by themortgagee.

MORTGAGE REDEMPTION INSURANCE A life insurance taken pursuant to a groupmortgage redemption scheme by the lender of money on the life of a mortgagor, whomortgages the house constructed to the extentof the mortgage indebtedness, such that if themortgagor dies, the proceeds of his lifeinsurance will be used to pay for hisindebtedness and the deceased’s heirs willthereby be relieved from paying the unpaidbalance of the loan (Great Pacific Life Assurance Corp. vs. Court of Appeals, GRNo. 113899, 316 SCRA 677, October 13,1999).

TRANSFER OF INTEREST, POLICY, ORCLAIM

In Insurance, the following may be transferred or assigned:

a) The thing insured (See Sec. 20); b) The policy itself (See Sec. 58);

c) The claim itself (See Sec. 83).

1. CHANGE OF INTERESTGENERAL RULE A change of interest in any part of thething insured, unaccompanied by acorresponding change of interest in theinsurance, SUSPENDS the insurance toan equivalent extent, until the interest inthe thing and the interest in the insuranceare vested in the same person (Sec. 20).

EXCEPTIONSa. In cases of life, accident, and health

insurance (Sec. 20).Reason: They are not regarded ascontracts of indemnity and therefore,insurable interest need exist only at thetime the insurance is effected.

b. Change of interest in the thing insuredafter occurrence of an injury whichresults in a loss (Sec. 21).Reason: After the loss has happened,the liability of the insurer becomes fixed.Therefore, the insured has the right toassign his claim against the insurer as

any other money claim.c. Change in interest in one or more of

several distinct things separatelyinsured by one policy (Sec. 22).Reason: The contract is divisible.

57

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 10/32

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 11/32

San Beda College of Law2008 CENTRALIZED BAR OPERATIONS

or incorporated in it by proper reference,the untruth or non-fulfilment of which inany respect, and without reference towhether the insurer was in fact prejudiced

by such untruth or non-fulfilment render the policy voidable by the insurer. Thesame may be expressed, implied,affirmative or promissory.

4. E XCEPTION – Exceptions make moredefinite the coverage indicated by thegeneral description of the risk by excludingcertain specified risks that otherwise wouldbe included under the general languagedescribing the risks assumed.

5. C ONDITION – The insurer must alsoprotect himself against fraudulent claims of loss and this he attempts to do by insertingin the policy various conditions whichmake the form of either conditionsprecedent or subsequent.

CONCEALMENT

Requisites:1. A party knows a fact (a material fact)

which he neglects to communicate or disclose to the other party;

2. Such party concealing is duty bound todisclose such fact to the other;

3. Such party concealing makes no warrantyas to the fact concealed; and

4. The other party has no means of ascertaining the fact concealed.

Test of Materiality: Determined not by theevent, but solely by the probable andreasonable influence of the facts upon theparty to whom the communication is due, informing his estimate of the advantages of theproposed contract, or in making his inquiries(Sec. 31).

Distinguished from Materiality in MarineInsurance:Rules on concealment are stricter since theinsurer would have to depend almost entirelyon the matters communicated by the insured.

Thus, in addition to material facts, each partymust disclose ALL the information hepossesses which are material to theinformation of the belief or expectation of athird person, in reference to a material fact.

BUT a concealment in a marine insurance inany of the following matters enumerated under Sec. 110, ICP does NOT vitiate the entirecontract, but merely exonerates the insurer from a loss resulting from the risk concealed.

Effect of Concealment:a) If there is concealment under Sec. 27, the

remedy of the insurer is rescission.b) The party claiming the existence of

concealment must prove that there wasknowledge of the fact concealed on thepart of the party charged withconcealment.

c) Good faith is not a defense inconcealment. Concealment, whether intentional or unintentional entitles theinjured party to rescind the contract of insurance (Sec. 27).

d) The matter concealed need not be thecause of loss.

e) To be guilty of concealment, a party musthave knowledge of the fact concealed atthe time of the effectivity of the policy.

f) Failure to communicate informationacquired AFTER the effectivity of thepolicy will NOT be a ground to rescind thecontract.

Reason: Information is no longer material as it will no longer influencethe other party to enter into suchcontract.

Matters that need not be disclosed - Neither party to a contract of insurance isbound to communicate information of mattersfollowing, EXCEPT in answer to inquiries of the other: (WOKEE)

1. Those which the other knows;2. Those which, in the exercise of ordinary

care, the other ought to know and of which, the former has no reason tosuppose him ignorant;

3. Those of which the other waivescommunication;

4. Those which prove or tend to prove theexistence of a risk excluded by a warranty,and which are not otherwise material;

5. Those which relate to a risk excepted fromthe policy and which are not otherwisematerial.

Note: Neither party is bound tocommunicate, even upon inquiry ,information of his own judgment.

The parties are bound to know all thegeneral causes which are open to hisinquiry, equally with the other, and allgeneral usages of trade.

• The right to information of material

facts may be WAIVED:1. by the terms of the contract;2. by failure to make an inquiry as to

such facts, where they aredistinctly implied in other facts

59

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 12/32

MEMORY AID IN COMMERCIAL LAW

Insurance

from which information iscommunicated.

Matters that must be disclosed even in the

absence of inquiry: (M-No means-No war)1. Those material to

the contract (Secs. 31, 34, 35);2. Those which the

other has no means of ascertaining (Sec. 30, 32, 33);

3. Those as to whichthe party with the duty tocommunicate makes no war ranty(Secs. 67-76).

REPRESENTATIONS

Kinds of Representation:1. Affirmative – an affirmation of fact

existing when the contract begins;2. Promissory – statement by the insured

concerning what is to happen during theterm of the insurance.

Requisites of a false representation(misrepresentation):1. The insured stated a fact which is untrue.2. Such fact was stated with knowledge that

it is untrue and with intent to deceive or which he states positively as true withoutknowing it to be true and which has atendency to mislead.

3. Such fact in either case is material to therisk.

Test of materiality – the same asconcealment (Sec. 31).

Effect of Misrepresentation:1. The injured party entitled to rescind from

the TIME when the representationbecomes false (Sec. 45).

2. When the insurer accepted the payment of premium with the knowledge of the groundfor rescission, there is a waiver of suchright.

3. There is no waiver of the right of rescission if the insurer had no knowledgeof the ground therefor at the time of acceptance of premium payment (Stokesvs. Malayan Insurance Co., Inc. GRNo. L-34768, February 24, 1984).

Characteristics:1. Not a part of the contract but merely a

collateral inducement to it;2. Oral or written;3. Made at the time of, or before issuing the

policy and not after;4. Altered or withdrawn before the insurance

is effected but not afterwards;

5. Refers to the date the contract goes intoeffect.

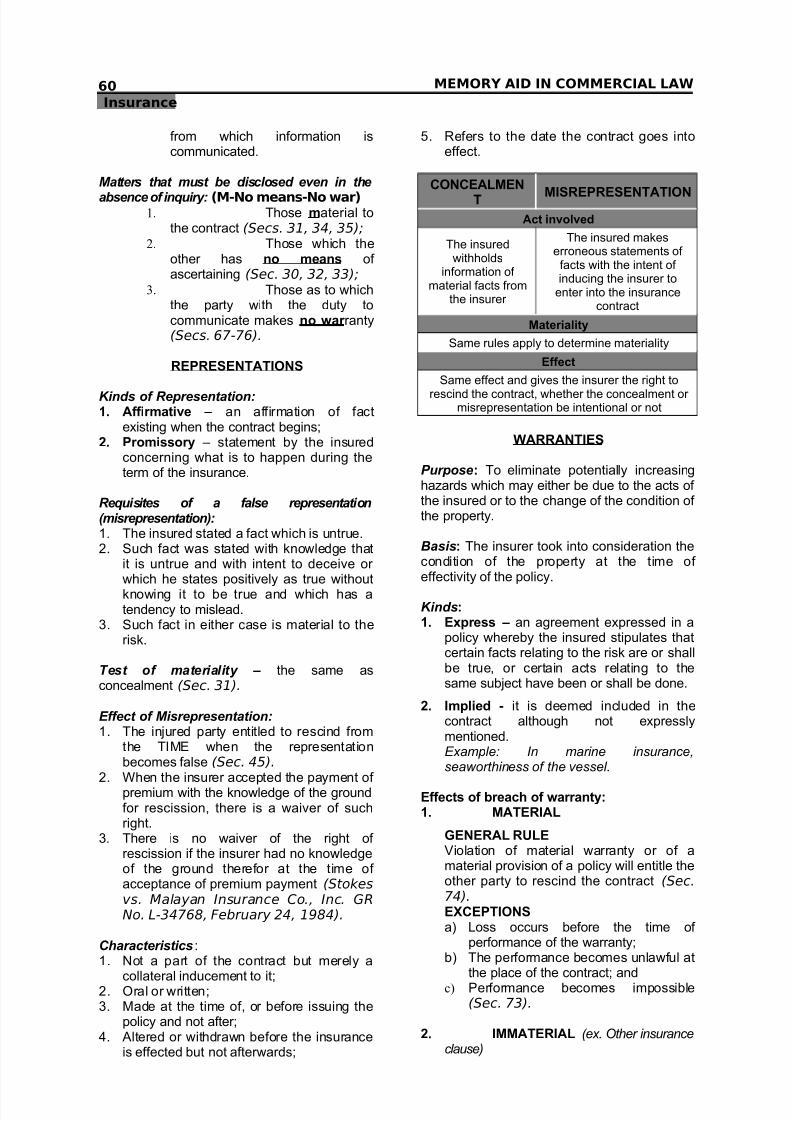

CONCEALMEN

T MISREPRESENTATION

Act involved

The insuredwithholds

information of material facts from

the insurer

The insured makeserroneous statements of facts with the intent of inducing the insurer to

enter into the insurancecontract

Materiality

Same rules apply to determine materiality

Effect

Same effect and gives the insurer the right to

rescind the contract, whether the concealment or misrepresentation be intentional or not

WARRANTIES

Purpose: To eliminate potentially increasinghazards which may either be due to the acts of the insured or to the change of the condition of the property.

Basis: The insurer took into consideration thecondition of the property at the time of effectivity of the policy.

Kinds:1. Express – an agreement expressed in a

policy whereby the insured stipulates thatcertain facts relating to the risk are or shallbe true, or certain acts relating to thesame subject have been or shall be done.

2. Implied - it is deemed included in thecontract although not expresslymentioned.Example: In marine insurance,seaworthiness of the vessel.

Effects of breach of warranty:1. MATERIAL

GENERAL RULEViolation of material warranty or of amaterial provision of a policy will entitle theother party to rescind the contract (Sec.74).EXCEPTIONSa) Loss occurs before the time of

performance of the warranty;b) The performance becomes unlawful at

the place of the contract; andc) Performance becomes impossible

(Sec. 73).

2. IMMATERIAL (ex. Other insuranceclause)

60

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 13/32

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 14/32

MEMORY AID IN COMMERCIAL LAW

Insurance

Requisites (2-LiP):

1. It must be a Life insurance policy;2. It must be Payable on the death of the

insured; and3. It must be in force during the lifetime of the

insured for at least 2 years from its date of issue or of its last reinstatement.

• The period of two years may be

shortened but it cannot be extendedby stipulation.

Defenses not barred by incontestability clause(FELT-Vicious-PMs):

1. That the person taking the insurancelacked insurable interest as required bylaw;

2. That the cause of the death of the insuredis an excepted risk;

3. That the premiums have not been paid;4. That the conditions of the policy relating to

military or naval service have beenviolated;

5. That the fraud is of a particular vicioustype;

6. That the beneficiary f ailed to furnish proof of death or to comply with any conditionsimposed by the policy after the loss hashappened;

7. That the action was not brought within thetime specified.

THE POLICY

POLICY OF INSURANCEThe written instrument in which a contract of insurance is set forth (Sec. 49). It is notnecessary for the perfection of the contract.

Note: An insurance contract may be verbal or in writing, or partly in writing and partly verbal.However, the law provides that no policy of

insurance shall be issued or delivered unlessin the form previously approved by theInsurance Commission (Sec. 226).

The approval of the Insurance Commissioner may be dispensed with upon the certificationof the president, vice-president, or generalmanager of the insurance company concernedthat the risk involved, the values of such risksand/ or the premiums therefor has notyet been determined or established, or such extension or renewal is not contraryto and is not for the purpose of violating

any provisions of the Insurance Code, or of any rulings, instructions, or circulars of theInsurance Commissioner (Ins. Memo Cir.No. 3-75, dated September 29, 1975,effective Oct. 21, 1976).

Contents of Policy (R2AP

2ID):

1. Parties;2. Amount of insurance, except in open or

running policies;

3. Rate of premium;4. Property or the life insured;5. Interest of the insured in the property if he

is NOT the absolute owner;

• BUT if he is the absolute owner,

information of the nature or amountof his interest need not becommunicated unless in answer toan inquiry (Sec. 34).

6. Risk insured against;7. Duration of the insurance.

RIDER An attachment to an insurance policy thatmodifies the conditions of the policy expandingor restricting its benefits or excluding certainconditions from the coverage.

Counter-signature of the insured on a rider,endorsement, clause, or warranty If the rider, endorsement, clause or warrantywas issued SIMULTANEOUSLY with thepolicy, the counter-signature of the insured isNOT necessary. However, the descriptive titleor name of the rider must be written on the

blank spaces provided in the policy.

The rider, endorsement, clause, or warrantywas issued AFTER the issuance of the policy:

• If the insured applied for the rider,

endorsement, clause, or warranty, hiscounter-signature is NOT necessary.

• If the same is not applied for by the

insured, riders and the like shall becountersigned by the insured or owner.

Note: When the requirements for a rider

are complied with, it is considered as partof the policy.

BINDING RECEIPT A mere acknowledgment on behalf of thecompany that its branch office had receivedfrom the applicant the insurance premium andhad accepted the application subject toprocessing by the head office.

COVER NOTE (AD INTERIM) A concise and temporary written contractissued by the insurer through its duly

authorized agent embodying the principalterms of an expected policy of insurance.

Purpose: It is intended to give temporaryinsurance protection coverage to theapplicant pending the acceptance or rejection of his application.

62

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 15/32

San Beda College of Law2008 CENTRALIZED BAR OPERATIONS

Rules on Cover Notes:a. The cover note is valid for 60 days, after

which the policy must be issued.

b. The period may be extended or renewedbeyond 60 days with the written approvalof the Commissioner if he determines thatsuch extension is not contrary to and is notfor the purpose of violating any provisionsof the Code.

c. No separate premiums are intended or required to be paid on a cover notebecause cover notes do not containparticulars of the property insured thatwould serve as basis for the computationof premiums. Thus, no premium could befixed and paid on the cover note. Cover notes should not be treated as separatepolicies but should be integrated to theregular policies subsequently issued sothat the premiums on the regular policiesinclude the consideration for the cover notes (Pacific Timber Export Corporation vs. Court of Appeals, GRNo. L-38613, 112 SCRA 199,February 25, 1982).

KINDS OF POLICY:1. OPEN POLICY – one in which the value of

the thing insured is not agreed upon, but isleft to be ascertained in case of loss (Sec.60).

2. VALUED POLICY – one which expresseson its face agreement that the thinginsured shall be valued at a specified sum(Sec. 61).

3. RUNNING POLICY – one whichcontemplates successive insurances andwhich provides that the object of the policymay be from time to time defined,especially as to the subjects of insurance,

by additional statements or endorsements(Sec. 62).

GENERAL RULEThe insurance proceeds shall be appliedexclusively to the proper interest of the personin whose name or for whose benefit it is made. A third person may not sue the insurer directly.

EXCEPTIONIf the insurance contract was intended tobenefit third persons (Art. 1311, CivilCode), the latter may directly claim from the

insurer. Thus,1. If the insurance contract contain some

stipulation in favor of a third person(stipulation pour autrui), the latter although not a party to the contract mayenforce the stipulation in his favour before

it is revoked by the contracting parties(Coquia v. Fieldmen’s Ins. Co., et al,GR No. L-23276, November 29,1968).

2. A third person has no right in law or equityto the proceeds of an insurance unlessthere is a contract or trust, express or implied, between the insured and thirdperson (Bonifacio Bros., Inc. v. Mora,GR No. L-20853, May 29, 1967).

3. Where the contract insurance provides for indemnity against liability to thirdpersons, then third persons, to whom theinsured is liable, can sue the insurer (Guingon v. del Monte, et al., GR No.L-21806, 20 SCRA 1043, August 17,1967).

INSURANCE PROCURED BY AN AGENTThe insurance inures to the benefit of theprincipal.Requisites:1. agent must be authorized;2. must act within the scope of his authority;3. must disclose his principal;4. indicate by appropriate words that he is

acting in a representative capacity.

TEST TO DETERMINE WHETHER A THIRD

PERSON MAY DIRECTLY SUE THE INSUREROF THE WRONGDOERWhere the contract provides for indemnity against liability to third persons, then thelatter to whom the insured is liable, can directlysue the insurer.

On the other hand, where the insurance is for indemnity against actual loss or payment ,then third persons cannot proceed against theinsurer, the contract being solely to reimbursethe insured for liability actually discharged byhim through payment to third persons, saidthird person’s recourse being, thus limited to

the insured alone (Guingon v. Del Monte,Ibid).

CANCELLATION OF NON-LIFE POLICYRequisites (WANG):1. prior notice of cancellation to the insured;2. notice must be based on the occurrence

after the effective date of the policy of oneor more of the grounds mentioned;

3. notice must be in writing, mailed or delivered to the insured at the addressshown in the policy;

4. notice must state the grounds relied upon

provided in Section 64 of the InsuranceCode and upon request of the insured tofurnish facts on which cancellation ismade.

Grounds (VP- FrANC):

63

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 16/32

MEMORY AID IN COMMERCIAL LAW

Insurance

1. non-payment of premiums;2. conviction of a crime out of acts increasing

the hazard insured against;3. fr aud or material misrepresentation;

4. wilLful or reckless acts or omissionsincreasing the risk insured against;

5. physical changes in the property insuredmaking it uninsurable;

6. determination by the InsuranceCommissioner that the policy would violatethe Insurance Code.

PREMIUM

GENERAL RULECASH AND CARRY RULE - No insurance

policy issued or renewal is valid and bindinguntil actual payment of the premium. Anyagreement to the contrary is void (Sec. 77).

EXCEPTIONS (LACIE)

1. In case of life and industrial life whenever the grace period provision applies (Sec.77).

2. Where there is an acknowledgment inthe contract or policy of insurance that thepremium had already been paid (Sec.78).

3. If the parties have agreed to the payment

of the premium in installments and partialpayment has been made at the time of theloss (Makati Tuscany Condominium v.Court of Appeals, GR No. 95546,November 6, 1992).

4. Where a credit term was agreed upon(UCPB General Insurance, Inc. v.Masagana Telemart, GR No. 13717, April 4, 2001).

5. Where the parties are barred by estoppel.

Note: Sec. 77 merely precludes the partiesfrom stipulating that the policy is valid even if

the premiums are not paid (Makati Tuscany Condominium Corp. vs. CA, GR No.95546, November 6, 1992).

Effect of Acknowledgment of Receipt of Premium in Policy:Conclusive evidence of its payment, in so far as to make the policy binding, notwithstandingany stipulation therein that it shall not bebinding until the premium is actually paid(Sec. 78).

Reason: When the policy contains suchwritten acknowledgement, it is presumed

that the insurer has waived the conditionof prepayment. It hereby creates a legalfiction of payment.

Note: The conclusive presumptionextends only to the question on the

binding effect of the policy. As far as thepayment of the premium itself isconcerned, the acknowledgment is only a prima facie evidence of the fact of such

payment. The insurer may still disputeits acknowledgment but only for thepurpose of receiving the premium dueand unpaid (The Insurance Code of the Philippines Annotated, De Leon,H., 2006ed).

Effect of acceptance of premium: Acceptance of premium within the stipulatedperiod for payment thereof, including theagreed grace period, merely assurescontinued effectivity of the insurance policy inaccordance with its terms.

Where an insurer authorizes an insuranceagent or broker to deliver a policy to theinsured, it is deemed to have authorized saidagent to receive the premium in its behalf.The insurer is bound by its agent’sacknowledgment of the receipt of payment of premium.

Payment of the premium by post-datedcheck.Delivery of a promissory note or a check willnot be sufficient to make the policy binding

until the said note or check has beenconverted into cash. This is consistent with Article 1249 of the Civil Code.

NOTE: Payment by means of a check or note,accepted by the insurer, bearing a date PRIORto the loss, assuming availability of the fundsthereof, would be sufficient even if it remainsunencashed at the time of the loss. Thesubsequent effects of encashment wouldretroact to the date of the instrument and itsacceptance by the creditor (Pandect of Commercial Law and Jurisprudence,Vitug, 2006ed).

Entitlement of insured to return of premiumspaid:1. WHOLE

a. If the thing insured was never exposedto the risks insured against (Sec. 79);

b. If contract is voidable due to fraud or misrepresentation of the insurer or hisagents (Sec. 81);

c. If contract is voidable because of theexistence of facts of which the insured

was ignorant without his fault(Sec.

81);d. When by any default of the insured

other than actual fraud, the insurer never incurred liability (Sec. 81); and

64

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 17/32

San Beda College of Law2008 CENTRALIZED BAR OPERATIONS

e. When rescission is granted due to theinsurer’s breach of contract (Sec.74).

2. PRO RATAa. When the insurance is for a definite

period and the insured surrenders hispolicy before the termination thereof;Exceptions:

1. policy not made for a definiteperiod of time;

2. short period rate is agreedupon;

3. life insurance policy

b. When there is over-insurance1. In case of over-insurance by

double insurance, the insurer isnot liable for the total amount of the insurance taken, his liabilitybeing limited to the propertyinsured. Hence, the insurer is notentitled to that portion of thepremium corresponding to theexcess of the insurance over theinsurable interest of the insured.

2. In case of over-insurance by several insurers, the insured isentitled to a ratable return of thepremium, proportioned to theamount by which the aggregatesum insured in all the policiesexceeds the insurable value of thething at risk (Sec. 82).

DEVICES USED TO PREVENT THEFORFEITURE OF A LIFE INSURANCE AFTERTHE PAYMENT OF THE FIRST PREMIUM:1. GRACE PERIOD – after the payment of

the first premium, the insured is entitled toa grace period of thirty days within whichto pay the succeeding premiums.

2. CASH SURRENDER VALUE – theamount the insurer agrees to pay to theholder of the policy if he surrenders it andreleases his claim upon it.

3. EXTENDED INSURANCE – where theinsurance originally contracted for iscontinued for such period as the amountavailable therefor will pay when it willterminate. In such a case, the insurancewill be for the same amount as the originalpolicy but for a period shorter than theperiod in the original contract.

4. PAID UP INSURANCE – no more

payments are required, and consists of insurance for life in such an amount as thesum available therefor, considered as asingle and final premium, will purchase. Itresults to a reduction of the original

amount of insurance, but for the sameperiod originally stipulated.

5. AUTOMATIC LOAN CLAUSE – astipulation in the policy providing that upon

default in payment of premium, the sameshall be paid from the loan value of thepolicy until that value is consumed. Insuch a case, the policy is continued inforce as fully and effectively as though thepremiums had been paid by the insuredfrom funds derived from other sources.

6. REINSTATEMENT – provision that theholder of the policy shall be entitled toreinstatement of the contract at any timewithin three years from the date of defaultin the payment of premium, unless thecash surrender value has been paid, or the extension period expired, uponproduction of evidence of insurabilitysatisfactory to the company and thepayment of all overdue premiums and anyindebtedness to the company upon saidpolicy (Reviewer on Insurance,Insolvency and Code of Commerce,Perez H., 2000ed).

DOUBLE INSURANCE

Double insurance exists where the sameperson is insured by several insurersseparately, in respect to the same subject andinterest (Sec. 93).

Requisites (2- same IRIS):1. same insured person;2. same subject matter;3. same interest insured;4. same r isk or peril insured against; and5. 2 or more insurers insuring separately.

OVER-INSURANCE

Exists when the insured insures the sameproperty for an amount GREATER than thevalue of that property.

Effect in case of loss:1. The insurer is bound only to pay the

extent of the real value of the propertylost;

2. The insured is entitled to recover theamount of premium corresponding tothe excess in value of the property.

EFFECTS OF OVER INSURANCE BYDOUBLE INSURANCE (Sec. 94)1. The insured, unless the policy otherwise

provides, may claim payment from theinsurers in such order as he may select,up to the amount for which the insurers

65

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 18/32

MEMORY AID IN COMMERCIAL LAW

Insurance

are severally liable under their respectivecontracts;

2. Where the policy under which the insuredclaims is a valued policy , the insured must

give credit as against the valuation for anysum received by him under any other policy without regard to the actual value of the subject matter insured;

3. Where the policy under which the insuredclaims is an unvalued policy, he must givecredit, as against the full insurable value,for any sum received by him under anypolicy;

4. Where the insured receives any sum inexcess of the valuation in the case of valued policies, or of the insurable value inthe case of unvalued policies, he must

hold such sum in trust for the insurers,according to their right of contributionamong themselves;

5. Each insurer is bound, as between himself and the other insurers, to contributeratably to the loss in proportion to theamount for which he is liable under hiscontract.

• Under the “Principle of Contribution” or

“Contribution Clause” it is required thateach insurer contribute ratably to theloss or damage considering that theseveral insurances cover the samesubject matter and interest against thesame peril.

ADDITIONAL OR OTHER INSURANCE CLAUSE A condition in the policy requiring the insuredto inform the insurer of any other insurancecoverage of the property insured. It is lawfuland specifically allowed under Sec. 75 whichprovides that “(a) policy may declare that aviolation of a specified provision thereof shall avoid it, otherwise the breach of an immaterial provision does not avoid it.”

Purposes:1. To prevent an increase in the moral

hazard; and2. To prevent over-insurance and fraud.

OVER-INSURANCEDOUBLE

INSURANCE

Amount of insurance

When the amount of the insurance is

beyond the value of

the insured’s insurableinterest

There may be no over-insurance as when the

sum total of the amounts

of the policies issueddoes not exceed the

insurable interest of theinsured

Number of insurers

There may only be There are always several

one insurer involved insurers

REINSURANCE A contract by which the insurer procures athird person to insure him against loss or liability by reason of an original insurance(Sec. 95) also known as “ReinsuranceCession” .

In every reinsurance, the original contract of insurance and the contract of reinsurance arecovered by separate policies.

LIMIT OF SINGLE RISKNo insurance company other than life,shall retain any risk on any one subject of insurance in an amount exceeding 20% of its net worth (Sec. 215).

DOUBLEINSURANCE

REINSURANCE

Interest

Involves the sameinterest

Involves differentinterest

Subject

Subject of insurance isproperty

Subject of insurance isthe original insurer’s

risk

Insurer

Insurer remains insuch capacity

Insurer becomes theinsured in relation to

reinsurer

Insured

Insured is the party ininterest in the 2

contracts

Original insured has nointerest in the

reinsurance contract(Sec. 98)

Insured’s consent

Insured has to give hisconsent

Insured’s consent notnecessary

Other Terms:1. Reinsurance treaty – Merely an

agreement between two insurancecompanies whereby one agrees to cedeand the other to accept reinsurancebusiness pursuant to provisions specifiedin the treaty.

2. Automatic reinsurance – The reinsuredis bound to cede and the reinsurer isobligated to accept a fixed share of therisk which has to be reinsured under thecontract.

3. Facultative reinsurance – There is noobligation to cede or accept participation inthe risk each party having a free choice.But once the share is accepted, theobligation is absolute and the liabilitythereunder can be discharged only by

66

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 19/32

San Beda College of Law2008 CENTRALIZED BAR OPERATIONS

payment (Equitable Ins. & Casualty Co. vs. Rural Ins. & Surety Co., Inc.,GR No. L-17436, 4 SCRA 343, January 31, 1962).

4. Retrocession – A transaction wherebythe reinsurer, in turn, passes to another insurer a portion of the risk reinsured. It isreally the reinsurance of reinsurance (TheInsurance Code of the Philippines Annotated, Hector de Leon, 2002ed).

LOSS

LOSS IN INSURANCEThe injury, damage or liability sustained by the

insured in consequence of the happening of one or more of the perils against which theinsurer, in consideration of the premium, hasundertaken to indemnify the insured. It may betotal, partial, or constructive.

LOSS IS SATISFIED BY (RPR)

a) Payment of loss;b) Reinstatement (repair or restoration)

of the property lost or damaged;c) Replacement (substitution) with

another or similar property.

WHEN INSURER IS LIABLE FOR LOSS1. Loss the proximate cause of which is the

peril insured against (Sec. 84);2. Loss the immediate cause of which is the

peril insured against except where theproximate cause is an excepted peril(Sec. 86);

3. Loss through the negligence of the insuredexcept where there was gross negligenceamounting to willful act (Sec. 87);

4. Loss caused by efforts to rescue the thinginsured from a peril insured against (Sec.85);

5. Loss caused by a peril NOT insuredagainst to which the thing insured wasexposed in the course of rescuing thesame from the peril insured against (Sec.85).

WHEN THE INSURER IS NOT LIABLE1. Loss by the insured’s willful act or gross

negligence;2. Loss due to the connivance of the insured

(Sec. 87); and

3. Loss where the excepted peril is the

proximate cause.

PROXIMATE CAUSEThat which in a natural and continuoussequence, unbroken by any newindependent cause, produces an event

and without which the event would nothave occurred.

NOTICE OF LOSS

Purposes:1. To give the insurer information by which

he may determine the extent of his liability;2. To afford the insurer a means of detecting

any fraud that may have been practicedupon him;

3. To operate as a check upon extravagantclaims.

In fireinsurance

In other types of insurance

Required Not required

Effect of failure to furnish

Failure to givenotice will defeatthe right of the

insured to recover.

Failure to give notice willnot exonerate the insurer,

unless there is astipulation in the policy

requiring the insured to doso.

Defects in the notice or proof of loss arewaived when the insurer:1. Writes to the insured that he considers the

policy null and void as the furnishing of notice or proof of loss would be useless;

2. Recognizes his liability to pay the claim;3. Denies all liability under the policy;4. Joins in the proceedings for determining

the amount of the loss by arbitration,making no objections on account of noticeand preliminary proof; or

5. Makes objection on any ground other thanformal defect in the preliminary proof.

CLAIMS SETTLEMENTThe indemnification of the loss of the insured.

In case of an unreasonable delay/denial in the

payment of the insured’s claim by the insurer,the insured can recover:

i. attorney’s fees;ii. expenses incurred by reason of the

unreasonable withholding;iii. interest at double the legal interest

rate fixed by the Monetary Board; andiv. amount of the claim (Zenith

Insurance Corp. vs. CA, GR No.85296, 185 SCRA 398, May 14,1990; Sec. 244).

TIME FOR PAYMENT OF CLAIMS

67

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 20/32

MEMORY AID IN COMMERCIAL LAW

Insurance

LIFE POLICIES NON-LIFE POLICIES

a. Maturing upon theexpiration of the term – The proceeds are

immediately payable tothe insured, except if proceeds are payable

in installments or annuities, which shall

be paid as theybecome due.

b. Maturing at thedeath of the insured,occurring prior to theexpiration of the term

stipulated – Theproceeds are payable

to the beneficiarieswithin 60 days after:presentation of claimand filing of proof of death (Sec. 242).

The proceeds shall bepaid within 30 days after the receipt by the insurer

of proof of loss, andascertainment of the loss

or damage byagreement of the partiesor by arbitration but notlater than 90 days fromsuch receipt of proof of

loss, whether or notascertainment is had or

made (Sec. 243).

EFFECT OF REFUSAL OR FAILURE TO PAYTHE CLAIM WITHIN THE TIME PRESCRIBEDSections 242, 243 and 244 of the InsuranceCode provide that the insurer shall be liable topay interest “twice the ceiling prescribed bythe Monetary Board” which means twice

12% per annum (legal rate of interestprescribed in CB No. 416) or 24% per annuminterest on the proceeds of the insurance fromthe date following the time prescribed in Secs.242 or 243, until the claim is fully satisfied(Prudential Guarantee and Assurance,Inc v. Trans-Asia Shipping Lines, Inc. GRNo. 151890, June 20, 2006).

EXCEPTIONRefusal or failure to pay the loss or damage will entitle the assured to collectinterest UNLESS such refusal or failure to

pay is based on the ground that the claimis fraudulent (Ibid; Secs. 242, 243).

PRESCRIPTIVE PERIOD(Secs. 63 & 384)

RULES1. The parties to a contract of insurance may

validly agree that an action on the policyshould be brought within a limited periodof time, provided such period is NOT lessthan 1 year from the time the cause of action accrues. If the period agreed uponis less than 1 year from the time the causeof action accrues, such agreement is void.(Sec. 63)

a. The stipulated prescriptive periodshall begin to run from the date of theinsurer’s rejection of the claim filedby the insured or beneficiary and not

from the time of the loss.b. In case the claim was denied by the

insurer but the insured filed a petitionfor reconsideration, the prescriptiveperiod should be counted from thedate the claim was denied at the firstinstance and not from the denial of the reconsideration (Sun LifeOffice, Ltd. v. Court of Appeals,GR No. 89741, 195 SCRA 193,March 13, 1991).

2. If there is no stipulation or the stipulation isvoid, the insured may bring the action

within the prescriptive period provided for in the Civil Code, which is 10 years incase the contract is written.

3. In CMVLI, the written notice of claim mustbe filed within 6 months from the date of the accident; otherwise, the claim isdeemed waived even if the same isbrought within one year from its rejection(Vda. De Gabriel vs. CA, GR No.103883, 264 SCRA 137, November 14, 1996).

4. The suit for damages, either with theproper court or with the InsuranceCommissioner, should be filed within 1year from the date of the denial of theclaim by the insurer; otherwise, claimant’sright of action shall prescribe (Sec. 384).

SPECIAL KINDS OFINSURANCE

MARINE INSURANCE

Insurance against risks connected withnavigation, to which a ship, cargo, freightage,profits or other insurable interest in movableproperty, may be exposed during a certainvoyage or a fixed period of time (Sec. 99).

Coverage:

1. Insurance against loss or damage to:

a. Vessels, goods, freight, cargo,merchandise, profits, money, valuablepapers, bottomry and respondentia,and interest in respect to all risks or

perils of navigation;b. Persons or property in connection with

marine insurance;

68

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 21/32

San Beda College of Law2008 CENTRALIZED BAR OPERATIONS

c. Precious stones, jewels, jewelry andprecious metals whether in the courseof transportation or otherwise; and

d.Bridges, tunnels, piers, docks andother aids to navigation andtransportation (Sec. 99).

• Cargo can be the subject of marine

insurance, and once it is enteredinto, the implied warranty of seaworthiness immediatelyattaches to whoever is insuring thecargo, whether he be the shipowner or not (Roque vs. IAC, GR No. L-66935, November 11, 1985).

2. Marine Protection and IndemnityInsurance

Measure of Indemnity:1. Valued policy – The parties are bound by

the valuation, if the insured had someinterest at risk and there is no fraud (Sec.156).

2. Open policy – The following rules shallapply in estimating a loss:a. value of the ship – value at the

beginning of the risk ;b. value of the cargo – actual cost when

laden on board or market value at thetime and place of lading ;

c. value of freightage – gross freightageexclusive of primage;

d. cost of insurance – in each case, to beadded to the estimated value (Sec.161).

Major divisions of transportation insurance:1. Ocean Marine Insurance

Scope:a. ships or hullsb. goods or cargoesc. earnings such as freightd. liability incurred by reason of maritime

perils2. Inland Marine Insurance

Classes:a. Property in transit –

provides protection to propertyfrequently exposed to loss while it isbeing transported from one location toanother.

b. Bailee liability – insurancefor those who have temporary custody

of the goods.c. Fixed transportation property – they are so insuredbecause they are held to be anessential part of the transportationsystem such as bridges, tunnels, etc.

d. Floater – providesinsurance to follow the insuredproperty wherever it may be located,subject always to the territorial limits of

the contract.

INSURABLE INTEREST1. SHIPOWNER

a) Over the vessel to the extent of itsvalue, provided that if chartered, therecovery is only up to the amount notrecoverable from the charterer.

b) He also has an insurable interest onexpected freightage (Sec. 103).

c) No insurable interest if he will becompensated by charterer for thevalue of the vessel, in case of loss.

2. CARGO OWNER

• Over the cargo and expected

profits (Sec. 105).

3. CHARTERER

• Over the amount he is liable to the

shipowner, if the ship is lost or damaged during the voyage (Sec.106).

4. OWNER/ DEBTOR (where the vessel or cargo is hypothecated by bottomry or respondentia)

• Difference between the value of vesselor goods and the amount of loan(Sec. 101).

• In loans on bottomry and

respondentia, repayment of the loan issubject to the condition that the vesselor goods, respectively, given as asecurity, shall arrive safely at the portof destination.

• If a vessel is hypothecated by

bottomry, only the excess is insurable,since a loan on bottomry partakes of the nature of an insurance coverage tothe extent of the loan accommodation.The same rule would apply to thehypothecation of the cargo byrespondentia (Pandect of Commercial Law and Jurisprudence, Vitug, 2006ed).

5. CREDITOR/ LENDER

• Amount of the loan

RISK INSURED AGAINSTIt is only perils of the sea which may beinsured against unless perils of the ship are

covered by an all-risk policy.

PERILS OF THESEA

PERILS OF THE SHIP

69

7/27/2019 Insurance Memaid 2008

http://slidepdf.com/reader/full/insurance-memaid-2008 22/32

MEMORY AID IN COMMERCIAL LAW

Insurance

Includes onlythose casualtiesdue to the:

1. unusualviolence; or

2. extraordinaryaction of windand wave; or

3. other extraordinarycausesconnected withnavigation.

A loss which in theordinary course of events, results from the:1. natural and

inevitable action of thesea;2. ordinary wear

and tear of the ship; or 3. negligent failure

of the ship’s owner toprovide the vesselwith proper equipmentto convey the cargounder ordinaryconditions.

SPECIAL MARINE INSURANCE CONTRACTS

AND CLAUSES1. ALL-RISKS POLICY – insurance against

all causes of conceivable loss or damage.

Except:

a. as otherwise excluded in the policy; or

b. due to fraud or intentional misconducton the part of the insured (Choa Tiek Seng vs. CA, GR No. 84507, 183SCRA 223, March 15, 1990).

The insured has the initial burden of proving that the cargo was in goodcondition when the policy attached andthat the cargo was damaged whenunloaded from the vessel; thereafter, theburden shifts to the insurer to show theexception to the coverage (FilipinoMerchants Insurance vs. Court of Appeals, GR No. 85141, 179 SCRA638, November 28, 1989).

2. BARRATRY CLAUSE A clause which provides that there can beno recovery on the policy in case of anywillful misconduct on the part of the master or crew in pursuance of some unlawful or

fraudulent purpose without consent of owners, and to the prejudice of theowner’s interest (Roque vs. IAC, Ibid).

3. INCHAMAREE CLAUSE A clause which makes the insurer liable for loss or damage to the hull or machineryarising from the:a. Negligence of the captain, engineers,

etc.b. Explosions, breakage of shafts; andc. Latent defect of machinery or hull

(Bar Review Materials inCommercial Law, Jorge Miravite,

2007ed).

4. SUE AND LABOR CLAUSE A clause under which the insurer maybecome liable to pay the insured, inaddition to the loss actually suffered, such

expenses as he may have incurred in hisefforts to protect the property against aperil for which the insurer would havebeen liable (Sec. 163).

Note: Such clause constitutes anexception to the principle that aninsurance contract is one of indemnity(where the insurer promises to makegood only the loss of the insured)since the insurer is liable to payadditional expenses for the protectionof the property against an insuredperil.

Matters, although concealed, will NOT vitiate thecontract except when they caused the loss

(Sec. 110)1. National character of the insured;2. Liability of the thing insured to capture or

detention;3. Liability to seizure from breach of foreign