integrated gas and electricity markets in asia …some issues and observations mike thomas october...

TRANSCRIPT

Integrated gas and electricity markets in Asia…some issues and observations

Mike ThomasOctober 2008

2 Private and Confidential

Objective

• Characterise the landscape, in broad terms, in which gas and electricity markets in Asia, would need to operate

• Look at the issue from the perspective of security of energy supply (Malaysia)

• Look at the issue from the perspective of investor (Singapore)

3 Private and Confidential

Landscape

• Asia is diverse, economically, culturally, politically and geographically

• Independent, economic regulation is not common

• Infrastructure and economic development rather than investment optimisation

• Primary fuel resources are regionally abundant but generally concentrated

• End-user pricing is often regulated independently of costs and allocated risks

• Fuel supply security has been, and will remain, a major driver

Markets-based approaches have pre-requisites for success, many of which are not yet present

4 Private and Confidential

China’s challenge – relocating energy

Source: SP Info Network, BP, CRA’s research

Sichuan Basin10Tcf

East China Sea Basin

Junggar Basin 2Tcf

Qaidam Basin 3Tcf

Ordos Basin 2TcfTarim Basin 13Tcf

Major power consumption area

Major hydropower resources

Major wind field area

Major coalfield area

Major oil & gas fields

Bohai Bay Basin 5Tcf

Yinggehai Basin 6Tcf

Songliao Basin 2Tcf

Power flow direction

- 82% of coal deposits in north & southwest, 67% hydropower in southwest

- Over 70% energy consumption in central & coastal regions

- Mismatch of major load center & fuel resource locations

- Rely on major fuel delivery & power transmission networks

- Power flow WE, NS

5 Private and Confidential

China’s power generation-reference scenario (IEA, 2006)

dated

6 Private and Confidential

Elsewhere, in Asia, however, the story is very different

• Gas

– Australia (LNG)

– Indonesia (LNG and via pipe to Singapore

– Malaysia (LNG and via pipe to Singapore)

• Coal

– Australia

– Indonesia

– Vietnam

• Gas

– Japan (AP LNG)

– Singapore (ex Indonesia and Malaysia)

– S. Korea (AP LNG)

– Taiwan (AP LNG)

• Coal

– Japan

– Malaysia

– Philippines

– Singapore

– S. Korea

– Taiwan

Import Gas or Steam Coal for Power

Export Gas and Steam Coal for Power

The many depend on the few…

7 Private and Confidential

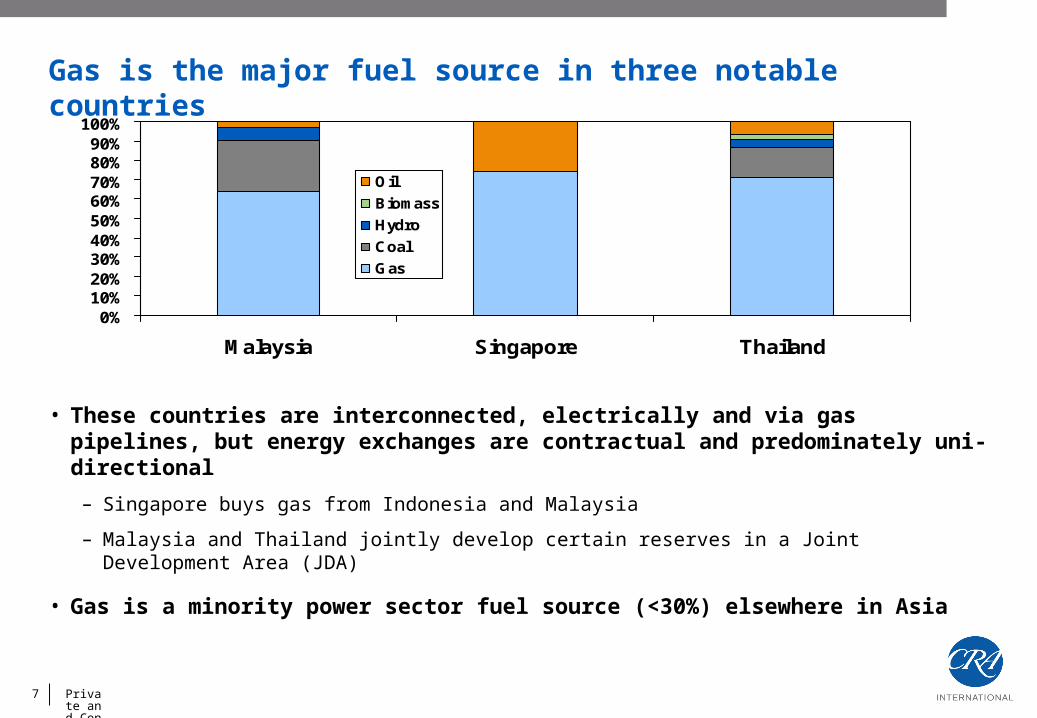

Gas is the major fuel source in three notable countries

• These countries are interconnected, electrically and via gas pipelines, but energy exchanges are contractual and predominately uni-directional

– Singapore buys gas from Indonesia and Malaysia

– Malaysia and Thailand jointly develop certain reserves in a Joint Development Area (JDA)

• Gas is a minority power sector fuel source (<30%) elsewhere in Asia

0%10%20%30%40%50%60%70%80%90%

100%

Malaysia Singapore Thailand

Oil

Biomass

Hydro

Coal

Gas

8 Private and Confidential

Thailand / Malaysia / Singapore / Indonesia

• Malaysia is a net gas and oil exporter, but via Sabah, not Peninsular Malaysia

– Peninsular-dedicated supplies are depleting / New reserves are smaller, more expensive

– Growth in non-power sector demand has forced a cap on gas to the power sector

– Imported coal is currently the main alternative fuel resource

• Singapore has no energy resources

– Imports gas via pipelines from Malaysia and Indonesia

– Malaysian source is depleting

– Energy resource security is a vital economic development consideration

– Plans to commission an LNG terminal in 2012 to enable LNG imports to supplement contracted piped gas supplies

– Proposals to build coal-fired capacity have been raised

9 Private and Confidential

Both power sectors are at a crossroads

• With limited domestic gas available, Malaysia can:

– Import coal

– Import LNG (from itself or globally)

– Develop massive interconnection to Sarawak and develop large scale hydro resources

– Develop nuclear power

• Singapore has an electricity market, but needs to ensure fuel supply security

– LNG terminal offers supply sourcing flexibility/storage

– Supplements connections with Malaysia/Thailand and Indonesia

– Support LNG uptake by imposing PNG import moratorium

– Completing with privatisation of gencos

10 Private and Confidential

The steam coal export market is highly concentrated

Actual (A); Projected (P)(millions of short tons) 2005A 2006A 2007P 2008P

Australia 123.1 124.8 127.4 128.6

China 73.2 64.9 59.5 55.1

Indonesia 127.7 181.8 180.9 183.4

Vietnam 14.1 25.9 21.6 17.4

Approximate Regional Steam Coal Exports 338.1 397.4 389.5 384.5

Percent Australia 36% 31% 33% 33%

Percent Indonesia 38% 46% 46% 48%

Percent Australia + Indonesia 74% 77% 79% 81%

Sources: Annual Energy Outlook 2008, Scenario aeo2008, d030208f, April 2008, DOE/EIA-0383(2008)

Plenty of coal in the ground, but not many countries to buy it from…

11 Private and Confidential

Pricing

Coal Import Prices in US Dollars/tonne

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

200.00

1987 1990 1993 1996 1999 2002 2005 2008

US

D/t

on

ne

Northwest Europe marker priceJapan steam coal import cif price

US Central Appalachian coal spot price index globalCoal RB Index (South Africa)

globalCoal NEWC Index (Australia)JPU

Platts Markers K1 (5900 GAR) (Indon)Platts Markers K2 (5000 GAR) (Indon)

Coal prices have moved similarly to other fossil fuels

12 Private and Confidential

With depleting peninsular reserves, Malaysia could utilise LNG

• Malaysia is a major Asia Pacific exporter of LNG, and so could always supply to itself

• But at what opportunity cost?

13 Private and Confidential

Singapore is an emerging champion of LNG importation

LNG Parity Pricing?PNG ONLY

???Constrained imported gas;

Increasing oil-basedgeneration

LNG available totop-up importedgas volumes and

support new entry

LNG+PNG

Commissioning of LNG terminal

End of existing imported gas contracts

TIME

2012Now

14 Private and Confidential

Impact of oil pricing on electricity asset value in Singapore (2)

Company Net Revenue: Gross Revenue - Fuel Cost - O&M ($m)

0

200

400

600

800

1,000

1,2002009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

$m

PowerSeraya SenokoPower TuasPowerWith limited gas, increasing demand requires more oil-fired generation. Gas-fired combined cycle units capture rent

LNG later displaces higher cost oil generation

LNG

High OilCase

Pro

fitab

ility

15 Private and Confidential

Impact of oil pricing on electricity asset value in Singapore (1)

Company Net Revenue: Gross Revenue - Fuel Cost - O&M ($m)

0

200

400

600

800

1,000

1,2002009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

$m

PowerSeraya SenokoPower TuasPowerIf oil prices are lower, then pre-LNG rents vanish!

Low OilCase

Pro

fitab

ility

LNG

16 Private and Confidential

Focusing on spreads….even if crude oil prices stay the same, spreads on crude products change

Company Net Revenue: Gross Revenue - Fuel Cost - O&M ($m)

0

200

400

600

800

1,000

1,200

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

$m

PowerSeraya SenokoPower TuasPower

HSFO p

ricin

g

rela

tions

hip

Versi

on A

17 Private and Confidential

Company Net Revenue: Gross Revenue - Fuel Cost - O&M ($m)

0

200

400

600

800

1,000

1,200

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

$m

PowerSeraya SenokoPower TuasPower

Focusing on spreads…HSFO

pric

ing

rela

tions

hip

Versi

on B

18 Private and Confidential

Summary

• China has the potential to benefit most from an integrated electricity and gas market, but has other challenges first…

• Uneven resource endowments elsewhere in Asia is beginning to spur interest in creative solutions

• LNG has selective, but important, prospective application in the power sector in Asia, particularly as smaller gas resources deplete

• The asset valuation and wealth transfer implications of gas/electricity integration are complex and easily overlooked

• Thailand/Malaysia/Singapore/Indonesia is an ideal corridor for gas/electricity sector development and trading, but net benefits are not yet sufficiently clear

19 Private and Confidential

Mike ThomasVice President

CRA International1902 A Tower Two Lippo Centre89 QueenswayAdmiralty, Hong Kong+852 9226 [email protected]