intensive actuarial training for bulgaria january, 2007 lecture 2 – life annuity by michael sze,...

TRANSCRIPT

Intensive Actuarial Training for Bulgaria

January, 2007

Lecture 2 – Life Annuity

By Michael Sze, PhD, FSA, CFA

Overview of Lecture

• Different forms of annuities

• Pricing of annuities

• Life annuity reserves

• Minimum capital requirement

Different Forms of Annuities

• Immediate annuities– Single life

– Guarantee period

– Joint life

– Increasing annuities

• Accumulation annuities– Accumulation period

– Death benefits

– Ultimate distribution

Immediate Annuities

• These were covered in Basic Course 1– We shall only point out some key concepts

– Afternoon workshops will review some mathematics involved

• Joint life annuity, 100% payable when x is alive, and j% payable to survivor y– Joint and j% survivor annuity

– äx:j%y = äx + j% x äy\x

– If we know äx and äx:100%y , we are able to calculate all other factors

– Actuarial equivalent options provide benefits of the same present values

Immediate Annuities (continued)

• Three types of increasing annuities:– Increasing by a fixed amount each year

• PV calculated using Iäx

– Increasing by a fixed % (e.g. c%) each year• PV calculated using an adjusted interest rate: (1+i)/(1+c)

– Increasing according to an index (e.g. CPI) each year• PV calculated using the yield rate of real return bonds

• Real return = nominal return – inflation

Accumulation Annuities

• Example: State Accumulated Fund • During accumulation period:

– Individual account grows with investment return and additional contributions

– Typical death, termination, disability benefits: accumulated account balance – surrender charges

– Pre-distribution mortality, termination, disability assumptions: not important in calculation of PV

– Basically equal to a simple investment vehicle– However, there may be tax advantages– Some offer higher death benefits: premium charged

Accumulation Annuities (continued)

• Different forms of distribution– Annuitization on retirement, disability, or death

• With or without interest rate guarantee• Interest guarantee: risky for insurance company• No interest guarantee: risky for the individual

– Fixed period annuity (not life)• Individual takes the risk of outliving his wealth

– Flexible payout• Treating accumulated fund as savings account balance• Must impose maximum payout % to ensure covering life• Allow annuitization at a later date

Pricing of Annuities

• Pricing assumptions– Mortality rates– Interest and investment return – Expenses– Lapse rates and premium payment patterns

Mortality Assumptions

• For immediate annuities– Risk is individual lives a long time– Lower q are conservative– Need to reflect future mortality improvement– Anti-selection against insurance company:

• Purchasers of life annuities are usually healthier• Healthy lives selection single life• Less healthy lives selection joint life or guarantees

• For accumulation annuities– Not important during accumulation period, unless there is higher

death benefit guarantee– Annuitization usually based on same q as for immediate annuities

Interest and Investment Income Assumptions – For Accumulation

• Interest credit– Most visible marketing feature – Balance interest rate risk vs competitiveness

• Earnings based on spread between actual investment income and credited interest

• Possible interest rate risk– Credited rate guarantee: long, investment: short

– Liability may be short (lapses), investment: long

• Strategies:– Matching cash flows of assets and liabilities– Unpredictable lapse rates: lower interest credit, short investment

Expenses

• Usually predictable from past experience• Affected by sales and policy sizes• Expenses include:

– Administrative: issue checks, verify alive or not– Commissions on flexible premiums– Communications: statements, inquiries– Loan, withdrawal and surrender requests– Taxes

• Best to make explicit allowance for expenses, and offset them with expense loads

Lapses, Surrenders, Premium Payment Patterns

• Immediate annuities usually provide no cash surrender values

• Lapse: important assumption for accumulation– Affects investment decision: match cash flows– Lower for higher ages– Large policies especially interest sensitive– Rule: surrender charge + lapse rate = constant– Lapses spike when surrender charge goes to zero

• Flexible premium products sold as:– Single premium, or annual premium

Solvency Reserve for Immediate Annuities

• PV of benefits calculated on conservative interest and mortality basis

• May exceed gross single premium – acquisition cost: surplus strain

• If market interest declines or mortality improves: solvency reserve may be inadequate

Earnings Reserve for Immediate Annuities

• Equal to PV of future benefits – deferred acquisition costs, where– The interest rate i is determined from the initial

single premium P – P = PV of benefits – acquisition cost

• If actual return j > i, then investment gain appears– Investment gain = (j – i) x earnings reserve

Solvency Reserve for Accumulation Annuities

• Regulations often set cash surrender values: CSVn

for each accumulation year• These become minimum solvency reserves•

tVx = Maxn>t (PV at time x+t of CSVx+n)• Note: in this calculation, we assume that the lapse

happens at the worst possible year• Surrender charges typically decreases each year:

8%, 7%, … for years 1, 2, …– If interest spread + surrender charge > expenses each year

– CSV = solvency reserve each year

Earnings Reserves for Accumulation Annuities

• Earnings reserve = account value – deferred acquisition cost

• Deferred acquisition cost is amortized against stream of profit margins, especially the interest spread

Required Capital

• Many products pass on investment risk to the policyholder– Annuity buyers tend to watch interest credit

• Move money if credited rate low

– Need more capital to cover mismatch of assets and liability cash flows

– Usually ignored

• Mortality risk for higher death benefits– Technically risk for annuity offsets that for insurance– Usually ignored

Annuities• Annuities are just a stream of n payments,

of the same amount paid in each period

1 1 1 1 1 1 1

PV 1 v v2 v3 v4 vn-2 vn-1

Value of an annuity is just the sum of these present values.

Denote value of an annuity with payments at the beginning of each period by Ab. As far as the value of money is concerned, to have Ab upfront is the same as having a stream of n payments of 1 paid at the beginning of each period, and vice versa. In symbols,

Ab = 1 + v + v2 + v3 + v4 +…+ vn-2 + vn-1. If periodic payments are made at the end of each period, the value Ae is given by:

Ae = v + v2 + v3 + v4 +…+ vn-1 + vn.

Life Annuities

• Similarity to annuities– Stream of payments, payable as long as the person lives

– Value of life annuity equals sum of present values of payments

• Difference from annuities– Payments only if the person survives

– Additional mortality discount

– Mortality discounts calculated from mortality tables

Explanation of Life Annuity

Value of life annuity for person age x with payments starting one year later, ax =

1pxv + 2pxv2 + 3pxv3 + 4pxv4 +…+ npxvn + …

1 1 1 1 1 1

v v2 v3 v4… vn vn+1…PVAnnuity

1px 2px 3px 4px npx n+1pxLifeAnnuity

Life Annuity with Payment at Beginning of Year

Value of life annuity for person age x with payments starting one year later, äx =

1+1pxv +2pxv2 + 3pxv3 + 4pxv4 +…+ npxvn + …

Deferred Life Annuity

Value of life annuity for person age x with payments starting t years later, t|

ax =

tpxvt + t+1pxvt+1 + t+2pxvt+2 + t+3pxvt+3 +…+ t+npxvt+n + …

Joint Life Annuity

Life Annuity Payable when both of two people x and y are alive axy =

1px.1pyv + 2px.2pyv2 + 3px.3pyv3 + 4px.4pyv4 +…+ npx.npyvn + …

Joint Life Annuity (continued)

Life Annuity Payable when either of two people x and y is alive ax:y = ax + ay - axy

It may also be regarded as sum of two annuities,ax and (ay – axy)

Joint and k% Survivor Annuity• (ay – axy) is annuity payable when y is alive,

but x is not, ay\x

• ax:y is annuity payable – when x is alive, and – 100% payable when a has died but y is alive

• ax:k%y is annuity payable – when x is alive, and – k% payable when a has died but y is alive

Joint and k% Survivor Annuity

ax:y = ax + (ay – axy ) = ax + ay\x

So, av\x = ax:y - ax

ax:k%y = ax + k% ay\x

= ax + k% (ax:y – ax)

= (ax – k% ax) + k% ax:y

= (1 – k%) ax + k% ax:y

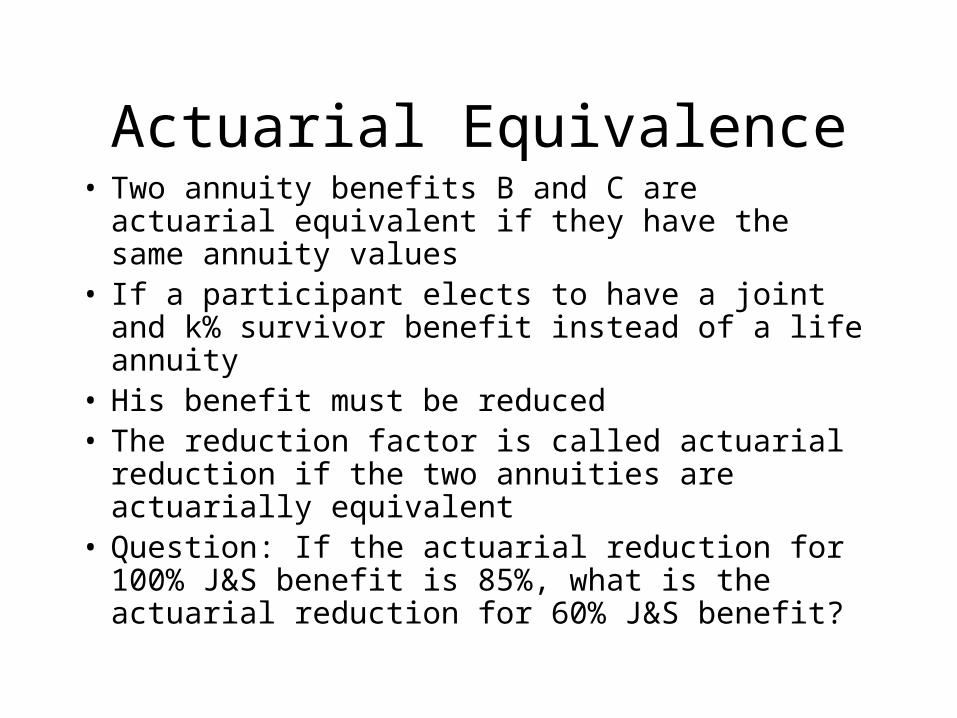

Actuarial Equivalence• Two annuity benefits B and C are actuarial

equivalent if they have the same annuity values• If a participant elects to have a joint and k%

survivor benefit instead of a life annuity• His benefit must be reduced• The reduction factor is called actuarial reduction if

the two annuities are actuarially equivalent• Question: If the actuarial reduction for 100% J&S

benefit is 85%, what is the actuarial reduction for 60% J&S benefit?