interest rate risk management - apb€¦ · mors software is delighted to share the results of our...

TRANSCRIPT

MONTH 1 MONTH 2 MONTH 3 MONTH 4 MONTH 5

INTEREST RATE RISK MANAGEMENT SURVEY 2017 ///

IRR

UP-TO-DATE ON ANALYSING AND

FORECASTING INTEREST RATE RISK?

� Internal Risk Management ranks higher than Regulatory Compliance as a driver for calculating IRR Scenarios & Stress testing

� Less than half of the banks have the ability to test sensitivities to key assumptions for IRRBB in intra-day or at end-of-day

� A third of banks are able to monitor & measure IRR only on a Monthly or Quarterly basis

� The majority of banks are not able to calculate the interaction of IRRBB with other risks, such as liquidity and credit risk

� Two out of three banks are able to calculate the standardized IRRBB framework

� Earnings at Risk (EaR) tops Economic Value of Equity (EVE) as the primary driver for managing IRRBB

KEY FINDINGS

TOWARDS A WIDER VIEW

MORS Software, a leading provider of intelligent real-time Treasury, Risk Management, Liquidity Management and ALM solutions for banks, conducted this first annual Interest Rate Risk Management Survey in January and February 2017.

Sixty-nine (69) banks participated from across the UK, Continental Europe, Asia, Africa and North America.

The following key findings emerged and are presented in greater detail in this Report:

2

MORS Software is delighted to share the results of our first Interest Rate Risk (IRR) Management Survey that was completed in February 2017. The IRR survey has been created to complement our annual Liquidity Risk Management survey that has been running for six years. The surveys support each other, to capture and present a more holistic picture of risk management trends within banks. As Interest Rate Risk in the Banking Book (IRRBB) regulation has continued to evolve lately, with the Basel IRRBB standards (BCBS 368) adopted for introduction by January 2018 and equally as the proposed amendment to EU’s Capital Requirements Directive (CRD) includes IRRBB, this offers a timely backdrop to introduce our new survey.

Government bond yields in key markets, such as the US and Germany have risen from their historic lows. Many key money market rates are still at historic (negative) lows but there are also signs of the ultra-loose monetary policy coming to an end, which has led to some regulatory concern. The operating environment of banks as expressed by Net Interest Income (NII) has been impacted negatively due to the low (negative) rate environment as well as margin compression in certain products. Having the ability to better analyse and manage performance and profitability drivers in the current and possibly changing operating environment will be key going forward and hence IRRBB will be in the spotlight for a good few years.

Our interest in IRR management has clear parallels with what we have been researching and surveying before on Liquidity Risk Management.

For us, as something of a pioneer in real-time Treasury & ALM systems, it is key to understand the technical readiness and capability banks have of calculating IRR overall as well as their readiness to meet regulatory requirements. We have also for quite some time been advocating an integrated and more holistic view of a bank’s risks.

The survey is highly motivated by the trend seen in banks to integrate the management of all financial resources as part of ALM, including interest rate and liquidity risk management, and to optimise all risks against internal and external constraints without silos. It will be interesting to follow-up how measurement and monitoring of interdependency between risks will improve during the coming years.

The survey questions fall into three categories: 1) capturing the bank's technical capabilities in terms of which risks can be measured and at what frequency 2) uncovering priorities and drivers for IRR management and 3) understanding specific readiness to meet IRRBB requirements.

We wish to extend our sincere thanks to all the participants in this year’s survey and are most grateful for the continued interest in our findings. We do hope you find the results in the booklet an interesting read, and look forward to continuing to provide you with annual surveys on both Liquidity and Interest Rate Risk Management.

Mika Mustakallio CEO, MORS Software

INTEREST RATE RISK MANAGEMENT IS DRIVEN BY INTERNAL NEEDS – REGULATION PAVING THE WAY FOR A MORE HOLISTIC APPROACH

THIS FIRST EDITION OF MORS INTEREST RATE RISK (IRR) MANAGEMENT SURVEY CONFIRMS INTERNAL RISK MANAGEMENT DRIVERS HAVING HIGHER PRIORITY IN MEASURING AND MONITORING IRR THAN REGULATORY REQUIREMENTS. HOWEVER, THE SURVEY ALSO SUGGESTS BANKS ARE MAKING PROGRESS ON MEASURING INTEREST RATE RISK ACCORDING TO RECENT IRRBB REGULATIONS.

3

Participant's Pro�le

Participant's Pro�le merged 2017 2

SURVEY DEMOGRAPHICS

69 SENIOR AND MID-LEVEL EXECUTIVES IN 33 COUNTRIES RESPONDED TO THE 2017 MORS SOFTWARE INTEREST RATE RISK SURVEY

REGIONAL PARTICIPATION

PARTICIPANT'S PROFILE

26% Central Europe

22% Nordic countries

19% Southern Europe

18% Eastern Europe

6% UK

4% North America

3% Africa

2% Asia

Regional Participation data 2017

Regional Participation merged 2017 2

48% Treasury & ALM

29% Risk management

19% Executive management

3% Liquidity management

1% Consultancy

4

A third of banks are able to monitor & measure IRR only on a Monthly or Quarterly basis, whilst the majority can do it at End-of-Day, or more frequently

The results of nearly a third, (29%), of respondents relying on Monthly or even Quarterly monitoring and measurement of IRR suggests that there still remains important further work to be completed for a significant number of banks in order to have timely IRR monitoring and measurement in place. This relatively large number of respondents (29%) opted for the “Other” category. Reviewing the provided further detail in the “Other” responses reveals that these respondents state Monthly and a few even Quarterly.

On the other hand, a majority of respondents (57%) are able to monitor and measure IRR on an End-of-Day basis, or more frequently. This 57% is composed of 43% of respondents who state their ability to monitor and measure IRR on an End-of Day basis, 7% who are able to monitor and measure in real-time and 6% who can do so on an intraday basis.

14% of respondents have stated that they are able to monitor and measure IRR on a Weekly basis.

Real-time // 7,3%

Intra-day // 5,8%

End-of-day // 43,4%

Weekly // 14,5%

Other // 29,0%

How frequently are you able to monitor and measure IRR (Interest Rate Risk) limits and sub-limits by currency, product etc.?

RESULTS AN INTEREST RATE RISK BANKING SECTOR SURVEY

SPONSORED BY MORS SOFTWARE – 2017

1

5

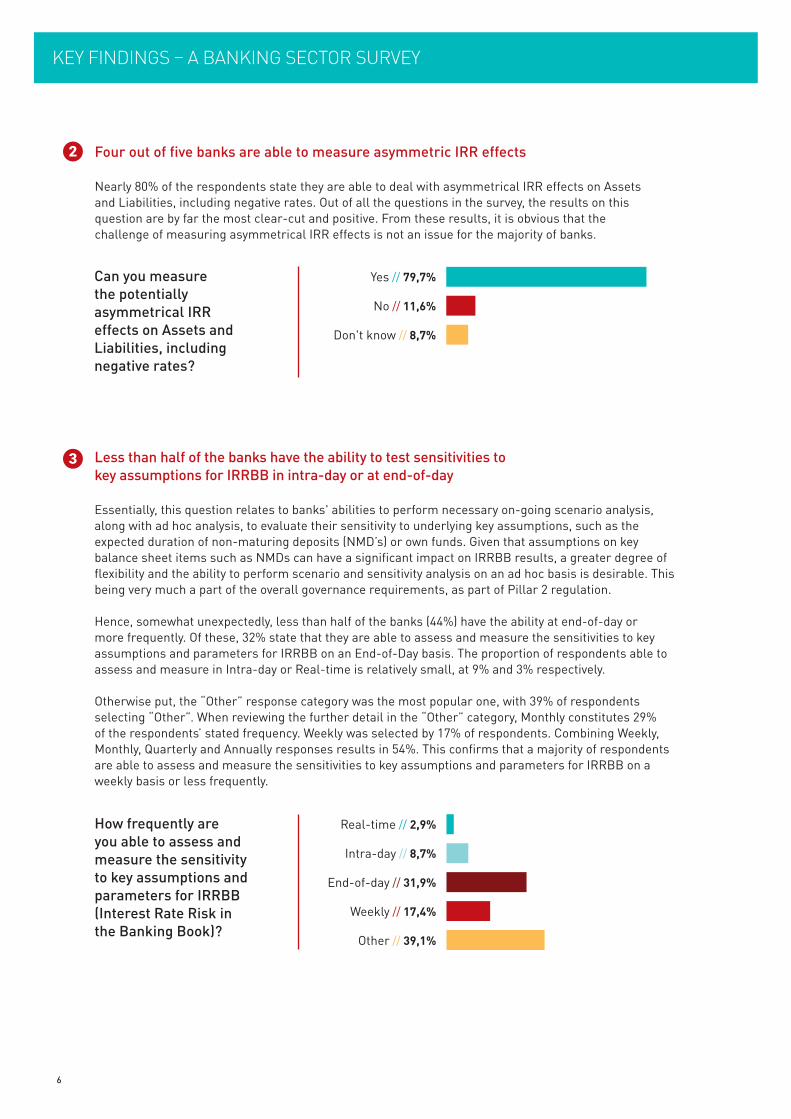

Less than half of the banks have the ability to test sensitivities to key assumptions for IRRBB in intra-day or at end-of-day

Essentially, this question relates to banks' abilities to perform necessary on-going scenario analysis, along with ad hoc analysis, to evaluate their sensitivity to underlying key assumptions, such as the expected duration of non-maturing deposits (NMD’s) or own funds. Given that assumptions on key balance sheet items such as NMDs can have a significant impact on IRRBB results, a greater degree of flexibility and the ability to perform scenario and sensitivity analysis on an ad hoc basis is desirable. This being very much a part of the overall governance requirements, as part of Pillar 2 regulation.

Hence, somewhat unexpectedly, less than half of the banks (44%) have the ability at end-of-day or more frequently. Of these, 32% state that they are able to assess and measure the sensitivities to key assumptions and parameters for IRRBB on an End-of-Day basis. The proportion of respondents able to assess and measure in Intra-day or Real-time is relatively small, at 9% and 3% respectively.

Otherwise put, the “Other” response category was the most popular one, with 39% of respondents selecting “Other”. When reviewing the further detail in the “Other” category, Monthly constitutes 29% of the respondents’ stated frequency. Weekly was selected by 17% of respondents. Combining Weekly, Monthly, Quarterly and Annually responses results in 54%. This confirms that a majority of respondents are able to assess and measure the sensitivities to key assumptions and parameters for IRRBB on a weekly basis or less frequently.

KEY FINDINGS – A BANKING SECTOR SURVEY

Four out of five banks are able to measure asymmetric IRR effects

Nearly 80% of the respondents state they are able to deal with asymmetrical IRR effects on Assets and Liabilities, including negative rates. Out of all the questions in the survey, the results on this question are by far the most clear-cut and positive. From these results, it is obvious that the challenge of measuring asymmetrical IRR effects is not an issue for the majority of banks.

2

3

Yes // 79,7%

No // 11,6%

Don't know // 8,7%

Can you measure the potentially asymmetrical IRR effects on Assets and Liabilities, including negative rates?

Real-time // 2,9%

Intra-day // 8,7%

End-of-day // 31,9%

Weekly // 17,4%

Other // 39,1%

How frequently are you able to assess and measure the sensitivity to key assumptions and parameters for IRRBB (Interest Rate Risk in the Banking Book)?

6

Earnings at Risk (EaR) tops Economic Value of Equity (EVE) as the primary driver for managing IRRBB

Close to 51% of respondents selected Earnings at Risk as the primary driver for managing IRRBB, whilst 38% of respondents consider Economic Value of Equity to be the primary driver. This is consistent with our understanding and results published by different trade bodies, and is also in line with the Basel consultation on IRRBB. In the “Other” category, both EVE and EaR had an equal weighting as the most common response.

Internal Risk Management ranks higher than Regulatory Compliance as a driver for calculating IRR Scenarios & Stress testing

With an average score of 4.4 on a scale of 1 to 5, Internal Risk Management emerges as the most important driver for calculating IRR scenarios and stress testing. Regulatory compliance with a score of 4.2 ranks as a fairly close second and Internal Planning Processes third with a score of 3.8.

Managing IRR in the banking book has always been the main task for ALM. With all the recent regulatory development in the area, we were unsure though how regulatory compliance would be seen as a driver.

4

Please rank the importance of the below drivers for calculating IRR scenarios and stress testing. 1 not important – 5 very important.

Regulatory compliance e.g. IRRBB

Internal planning process

Internal risk management

Other

5,8% 1,5% 13,0% 29,0% 47,8% 2,9%

2,9% 11,6% 21,7% 30,4% 31,9% 1,5%

2,9% 4,4% 7,2% 24,6% 59,4% 1,5%

1,4% 2,9% 4,3% 1,4% 1,4% 88,6%

1 2 3 4 5 Do not know Average

4,2

3,8

4,4

2,9

5

EVE // 37,7% (Economic Value of Equity

EaR // 50,7%(Earnings at Risk)

Other // 11,6%

Which metric would you consider as the primary driver in managing IRRBB, for your internal steering purposes?

7

Only 13% of the banks are capable of performing intra-day IRRBB calculations

Only 13% of the respondents state that they are able to calculate and measure on an intraday basis all the IRRBB disclosure scenarios and to explain the material changes. While this result is low, it is in line with the results of questions 1 and 3, which also address frequency of calculating, measuring and explaining variances for IRR and IRRBB.

Disclosure has been an integral part of the debate surrounding IRRBB lately. There is particular concern that the disclosed figures will be miss-interpreted and not understood correctly. As EVE calculations and disclosures can be performed, based on the “internal” view discounted by a risk-free rate, or the “external” view (containing margins) discounted by a risky rate, figures may differ substantially among banks. With ALM and IRRBB not being that well understood, different stakeholders, ranging from regulators and equity analysts to rating agencies, might draw false conclusions from the disclosures. Hence the importance of having the ability to explain all material movement.

The majority of banks are not able to calculate the interaction between IRRBB and other risks

The majority of respondents (54%) state that they are not able to measure the interaction of IRRBB with other risks, such as liquidity and credit risk. In accordance with the results, the multi-dimensional optimisation challenge of having the ability to integrate all financial resources is often cited as a major challenge by many banks.

However, as integrated stress-testing is already a reality in some jurisdictions, such as Comprehensive Capital Analysis and Review (CCAR) in the US, and as it is a part of the governance requirements within EU legislation, there will be some regulatory pressure going forward. More importantly, perhaps, we see it as a necessity to have the ability to measure and manage all constraints in an integrated way.

KEY FINDINGS – A BANKING SECTOR SURVEY

6

7

Yes // 13,0%

No // 81,2%

Don't know // 5,8%

Yes // 34,8%

No // 53,6%

Don't know // 11,6%

Are you able to calculate and measure on an intraday basis all the IRRBB disclosure scenarios as well as explain the material changes?

Can you measure the interaction of IRRBB with other risks such as liquidity and credit?

8

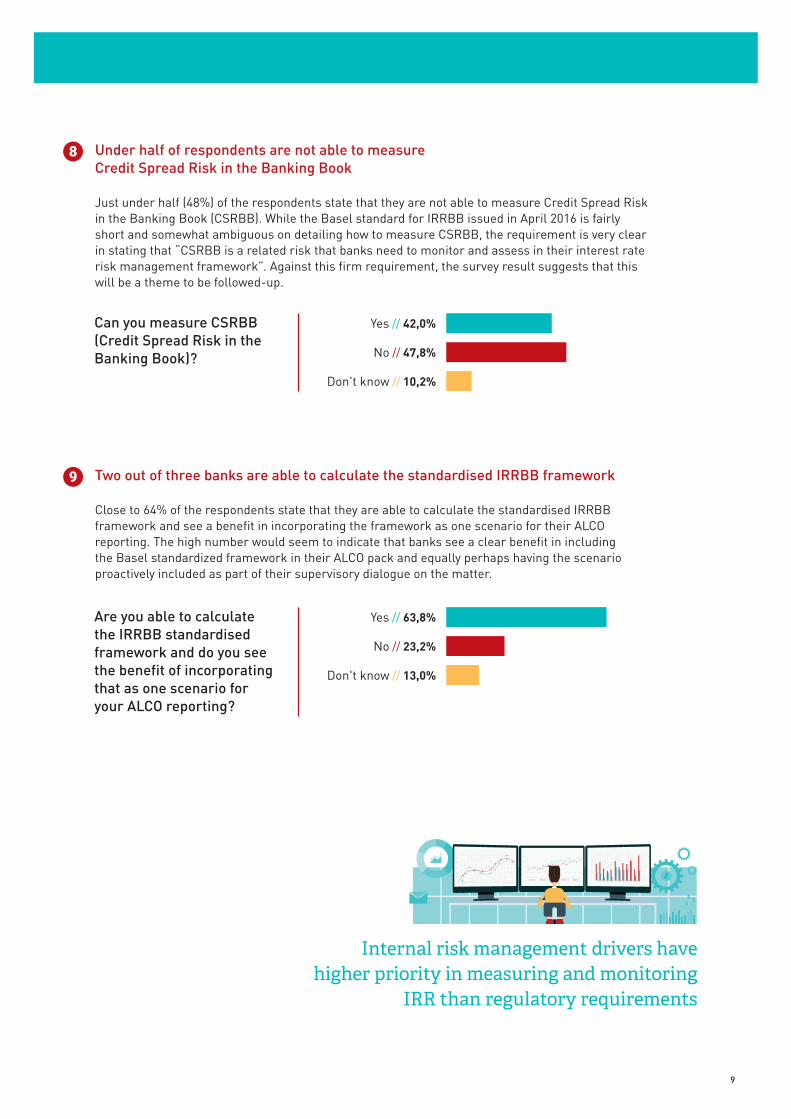

Under half of respondents are not able to measure Credit Spread Risk in the Banking Book

Just under half (48%) of the respondents state that they are not able to measure Credit Spread Risk in the Banking Book (CSRBB). While the Basel standard for IRRBB issued in April 2016 is fairly short and somewhat ambiguous on detailing how to measure CSRBB, the requirement is very clear in stating that “CSRBB is a related risk that banks need to monitor and assess in their interest rate risk management framework”. Against this firm requirement, the survey result suggests that this will be a theme to be followed-up.

Two out of three banks are able to calculate the standardised IRRBB framework Close to 64% of the respondents state that they are able to calculate the standardised IRRBB framework and see a benefit in incorporating the framework as one scenario for their ALCO reporting. The high number would seem to indicate that banks see a clear benefit in including the Basel standardized framework in their ALCO pack and equally perhaps having the scenario proactively included as part of their supervisory dialogue on the matter.

8

9

Yes // 42,0%

No // 47,8%

Don't know // 10,2%

Yes // 63,8%

No // 23,2%

Don't know // 13,0%

Can you measure CSRBB (Credit Spread Risk in the Banking Book)?

Are you able to calculate the IRRBB standardised framework and do you see the benefit of incorporating that as one scenario for your ALCO reporting?

Internal risk management drivers have higher priority in measuring and monitoring

IRR than regulatory requirements

MONTH 1 MONTH 2 MONTH 3 MONTH 4 MONTH 5

9

This first edition of the MORS Interest Rate Risk (IRR) Management Survey confirms internal risk management drivers having higher priority in measuring and monitoring IRR than regulatory requirements. However, the survey also suggests banks are making progress on measuring interest rate risk according to recent IRRBB regulations.

The highlights worth noting seem to relate to performance and capacity issues. Firstly, the majority of banks lack the ability to test the sensitivity to key assumptions, and as such to explain the potential changes, on a daily level. Secondly, the survey results reveal a third of banks being able to monitor & measure IRR only on a Monthly, or less frequent basis. Thirdly, multi-dimensional optimisation, that is the ability to measure the interaction of different risks, certainly seems to be a challenge.

In terms of results suggesting room for further improvement we would raise the three highlights noted above as the key features and functionalities to improve. We realise that there are many challenges related to the aforementioned, but we also believe that they have already moved quite some time ago from nice-to-haves to outright necessities. We note that these are major challenges and are eager to follow-up on the topics, as we expect to see quite some progress in the coming years.

We look forward to renewing the survey in one year’s time to measure progress.

THE 1ST ANNUAL INTEREST RATE RISK MANAGEMENT SURVEY

� Internal Risk Management ranks higher than Regulatory Compliance as a driver for calculating IRR Scenarios & Stress testing

� Less than half of the banks have the ability to test sensitivities to key assumptions for IRRBB in intra-day or at end-of-day

� A third of banks are able to monitor & measure IRR only on a Monthly or Quarterly basis

� The majority of banks are not able to calculate the interaction of IRRBB with other risks, such as liquidity and credit risk

� Two out of three banks are able to calculate the standardized IRRBB framework

� Earnings at Risk (EaR) tops Economic Value of Equity (EVE) as the primary driver for managing IRRBB

KEY FINDINGS

CONCLUSION

10

ABOUT MORS SOFTWARE

MORS SOFTWARE IS A LEADING PROVIDER OF INTELLIGENT REAL-TIME TREASURY AND RISK MANAGEMENT SOLUTIONS FOR BANKS

MORS Solutions can quickly ADAPT to an existing business and IT environment and produce

benefits without requiring major changes to business processes or IT systems

The fast delivery and COST EFFICIENCY make MORS unique and appreciated by

many leading Banks worldwide

MORS Balance Sheet Manager enables users to analyse IRR and margins at cash-flow and transaction levels, ensuring a continuous oversight of profitability within given constraints.

The solution incorporates static and dynamic models for:

� Interest rate risk management, including: Repricing Risk, Yield Curve Risk, Basis Risk and Option Risk

� Net Interest Income (NII) and Net Interest Margin (NIM): Analysis, Forecasting and Stress-testing

� Managing Interest Rate Risk in the Banking Book (IRRBB): All risk components can be expressed as Economic Value of Equity (EVE) and Earnings at Risk (EaR) numbers

MORS BALANCE SHEET MANAGER A REAL-TIME ALM SOLUTION FOR FINANCIAL INSTITUTIONS

adapt cost efficient

€

BALANCESHEET

MANAGER

11

“IR

R S

urve

y 20

17”

Des

ign:

gat

tade

sign

.fr

MORS Software Aleksanterinkatu 48 A00100 HelsinkiFinland tel +358 9 6829 650

[email protected] [email protected]

www.morssoftware.com

www.morssoftware.com