interim performance presentation - beranda · • rspo: to date, 155,045 ha of plantations...

TRANSCRIPT

0

12 November 2013

Interim Performance PresentationYTD Sep 2013 : nine-month period ended 30th September 2013

1

DisclaimerThis presentation has been prepared by Golden Agri-Resources Ltd. (“GAR” or “Company”) for informationalpurposes, and may contain projections and forward looking statements that reflect the Company’s currentviews with respect to future events and financial performance. These views are based on currentassumptions which are subject to various risks and which may change over time. No assurance can begiven that future events will occur, that projections will be achieved, or that the Company’s assumptions arecorrect. Actual results may differ materially from those projected. A prospective investor must make its ownindependent decision regarding investment in securities.

Opinions expressed herein reflect the judgement of the Company as of the date of this presentation andmay be subject to change without notice if the Company becomes aware of any information, whetherspecific to the Company, its business, or in general, which may have a material impact on any suchopinions.

The information is current only as of its date and shall not, under any circumstances, create any implicationthat the information contained therein is correct as of any time subsequent to the date thereof or that therehas been no change in the financial condition or affairs of GAR since such date. This presentation may beupdated from time to time and there is no undertaking by GAR to post any such amendments orsupplements on this presentation.

The Company will not be responsible for any consequences resulting from the use of this presentation aswell as the reliance upon any opinion or statement contained herein or for any omission.

© Golden Agri-Resources Ltd. All rights reserved.

2

Section 1 Executive Summary 3

Section 2 Financial Highlights 5

Section 3 Plantation Highlights 11

Section 4 Downstream Highlights 16

Section 5 Strategy and Outlook 19

Section 6 Appendix 24

Table of Contents

Section 1

Executive Summary

4

Executive Summary

• YTD Sep 2013 vs YTD Sep 2012 results

Revenue $4,683 mn 3%EBITDA $462 mn 28%Net Profit1 $188 mn 47%Palm product output 1.95 mn MT 5%CPO FOB price $786/MT 23%

• 3Q 2013 vs 2Q 2013 results

Revenue $1,571 mn 7%EBITDA $111 mn 21%Net Profit1 $30 mn 33%Palm product output 694,000 MT 17%CPO FOB price $769/MT 3%

Revenue for YTD Sep 2013 grew with expanded downstream operations, despite weaker CPO prices

EBITDA (US$ million)Price (US$/MT)

Output (‘000 MT)

Note:1. Net profit attributable to owners of the Company

100

200

300

400

500

600

700

800

9M09 9M10 9M11 9M12 9M13400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

EBITDACPO Price (FOB Belawan)Palm Products Output

Section 2

Financial Highlights

6

Financial Performance – YTD Sep 2013

Revenue 4,683 4,533 3%Gross Profit 938 1,250 -25%EBITDA 462 643 -28%

Interest on borrowings -73 -54 35%Depreciation and amortisation -99 -84 18%Foreign exchange loss, net -15 -12 26%

Net Profit attributable to owners of the Company 188 356 -47%

US$ million YTD Sep 2013 YTD Sep 2012 Change

Revenue increased by 3% mainly driven by the expansion of refinery capacity.Lower year-on-year performance mainly caused by the decrease in average CPO FOB prices by 23% to US$786 per tonne in YTD Sep 2013, from US$1,023 per tonne in the same period last year.

7

Financial Performance – 3Q 2013

3Q 2013 performance year-on-year:• Revenue declined by 6% due to weaker average CPO FOB prices by 19%.• Lower 3Q 2013 performance was mainly attributable to weaker selling prices and less palm product output

by 13%.

3Q 2013 performance quarter-on-quarter:• Lower revenue of 7% mainly impacted by lower average selling prices and higher inventory levels.• Weaker 3Q 2013 performance also affected by higher salary costs.

Revenue 1,571 1,672 -6% 1,682 -7% Gross Profit 277 398 -30% 304 -9%EBITDA 111 190 -42% 140 -21%

Interest on borrowings -26 -21 28% -24 12%Depreciation and amortisation -35 -30 18% -33 6%Foreign exchange loss, net -6 -5 35% -14 -56%

Net Profit attributable to owners of the Company 30 86 -65% 45 -33%

US$ million 3Q 2013 3Q 2012 YoY 2Q 2013 QoQChange Change

8

Revenue 3,725 3,583 4% 959 950 1%

Gross Profit 884 1,227 -28% 54 23 140%

Gross Profit Margin 24% 34% -10% 6% 2% 4%

EBITDA 438 648 -32% 24 -5 n.m.

EBITDA Margin 12% 18% -6% 2% -1% 3%

Net Profitattributable to ownersof the Company 173 382 -55% 15 -26 n.m.

Segmental Results

While Indonesia Operations results were weaker, China Operations performance improved as a result of management team strengthening and more favourable business environment.

US$ million Indonesia Operations China OperationsYTD Sep 2013 YTD Sep 2012 Change YTD Sep 2013YTD Sep 2012 Change

9

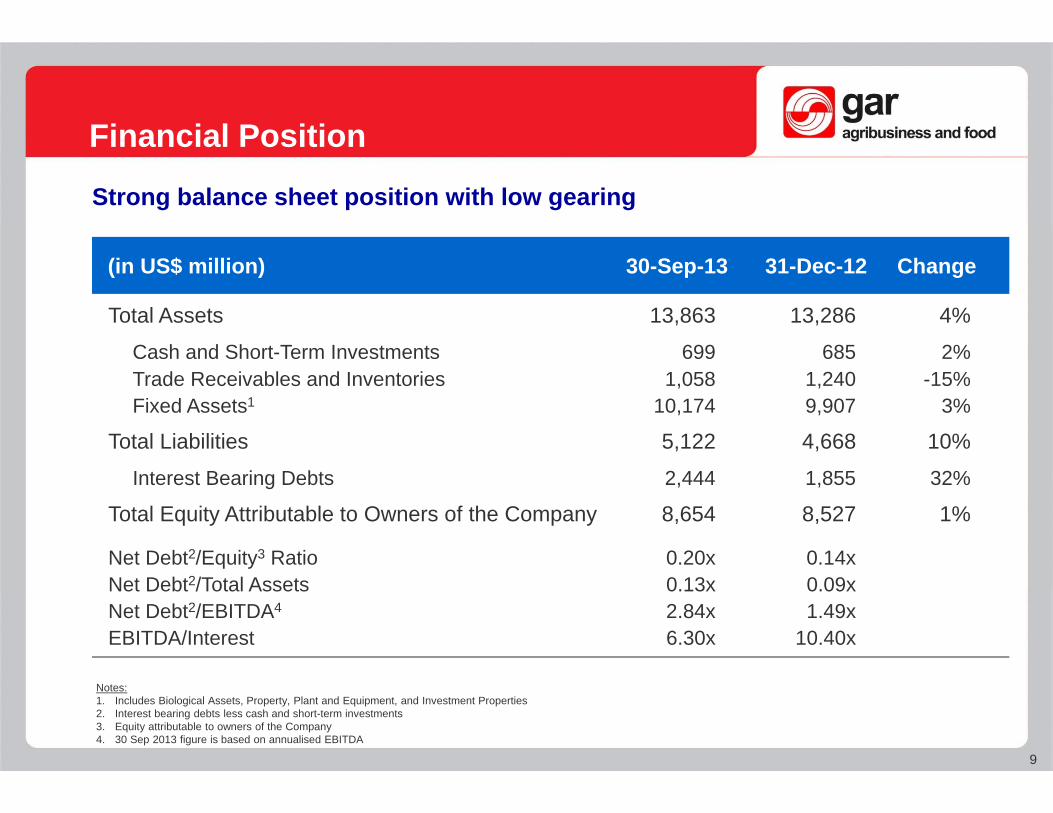

Financial Position

Strong balance sheet position with low gearing

(in US$ million) 30-Sep-13 31-Dec-12 Change

Total Assets 13,863 13,286 4%

Cash and Short-Term Investments 699 685 2%Trade Receivables and Inventories 1,058 1,240 -15%Fixed Assets1 10,174 9,907 3%

Total Liabilities 5,122 4,668 10%

Interest Bearing Debts 2,444 1,855 32%

Total Equity Attributable to Owners of the Company 8,654 8,527 1%

Net Debt2/Equity3 Ratio 0.20x 0.14xNet Debt2/Total Assets 0.13x 0.09xNet Debt2/EBITDA4 2.84x 1.49xEBITDA/Interest 6.30x 10.40x

Notes:1. Includes Biological Assets, Property, Plant and Equipment, and Investment Properties2. Interest bearing debts less cash and short-term investments3. Equity attributable to owners of the Company4. 30 Sep 2013 figure is based on annualised EBITDA

10

Dividend

The proposed dividend is in line with our dividend policy and takes into consideration our strategic expansion as well as potential value-creating acquisitions

The Company’s dividend policy is to distribute up to 30% of underlying profit

Cash DividendDividend per share (in S$ cents) 0.495 0.770 1.840 1.190 0.585Total Dividend (in S$ million) 60.09 93.47 223.35 152.77 75.10% to underlying profit 22% 18% 30% 30% 30%

Interim2009 2010 2011 2012 2013

The Board approves to distribute interim dividend of 0.585 Singapore cents per share, 30% of our underlying profit for YTD Sep 2013

Section 3

Plantation Highlights

12

(in ha) 30 Sep 30 Sep 30 Sep 2013/2012 31 Dec2013 2012 % increase 2012

Planted Area 467,014 459,502 1.6% 463,426Nucleus 368,476 363,586 1.3% 366,914Plasma 98,538 95,916 2.7% 96,512

Mature Area 431,612 418,137 3.2% 416,309Nucleus 339,601 330,187 2.9% 328,423Plasma 92,011 87,950 4.6% 87,886

GAR is the largest Indonesian plantation company with integrated operations

Plantation Area

• Total 8,600 hectares of new planting and replanting• In Dec 2012, we announced the acquisition of approximately 16,000 hectares of mature oil palm

plantations in Indonesia, of which completion is in progess.

13

41,365

91,953

211,932

94,851 19,401

35,402

79,597

224,322

107,369

20,324

Total Planted Area by Age Profile

GAR’s long-term growth is supported by favourable age profile of planted area underpinned by large immature and young plantations

Notes:1. Total planted area, including plasma 2. As of 30 Sep 2013, average age of plantations, including plasma, is 13 years

Sep 2013 Sep 2012

48%

8%4%

23% 17%

46%

20%

9%4%

21%

14

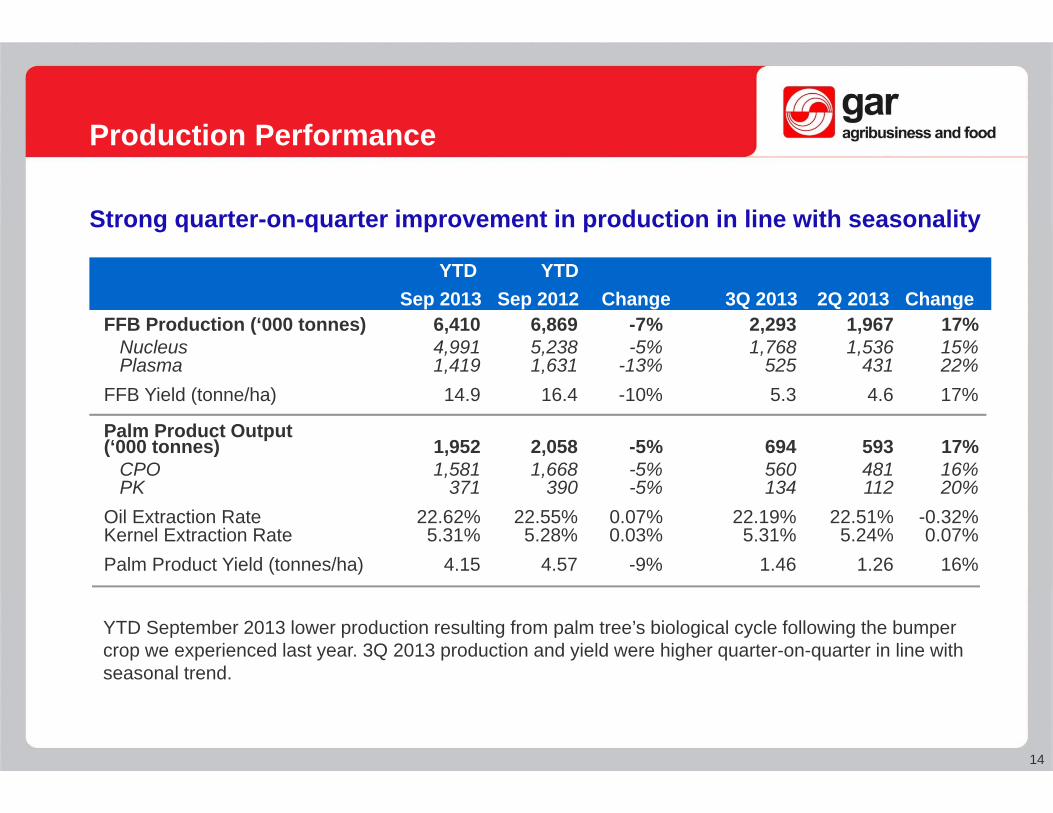

YTD September 2013 lower production resulting from palm tree’s biological cycle following the bumper crop we experienced last year. 3Q 2013 production and yield were higher quarter-on-quarter in line with seasonal trend.

Strong quarter-on-quarter improvement in production in line with seasonality

Production Performance

FFB Production (‘000 tonnes) 6,410 6,869 -7% 2,293 1,967 17%Nucleus 4,991 5,238 -5% 1,768 1,536 15%Plasma 1,419 1,631 -13% 525 431 22%

FFB Yield (tonne/ha) 14.9 16.4 -10% 5.3 4.6 17%

Palm Product Output(‘000 tonnes) 1,952 2,058 -5% 694 593 17%

CPO 1,581 1,668 -5% 560 481 16%PK 371 390 -5% 134 112 20%

Oil Extraction Rate 22.62% 22.55% 0.07% 22.19% 22.51% -0.32%Kernel Extraction Rate 5.31% 5.28% 0.03% 5.31% 5.24% 0.07%Palm Product Yield (tonnes/ha) 4.15 4.57 -9% 1.46 1.26 16%

YTD YTDSep 2013 Sep 2012 Change 3Q 2013 2Q 2013 Change

15

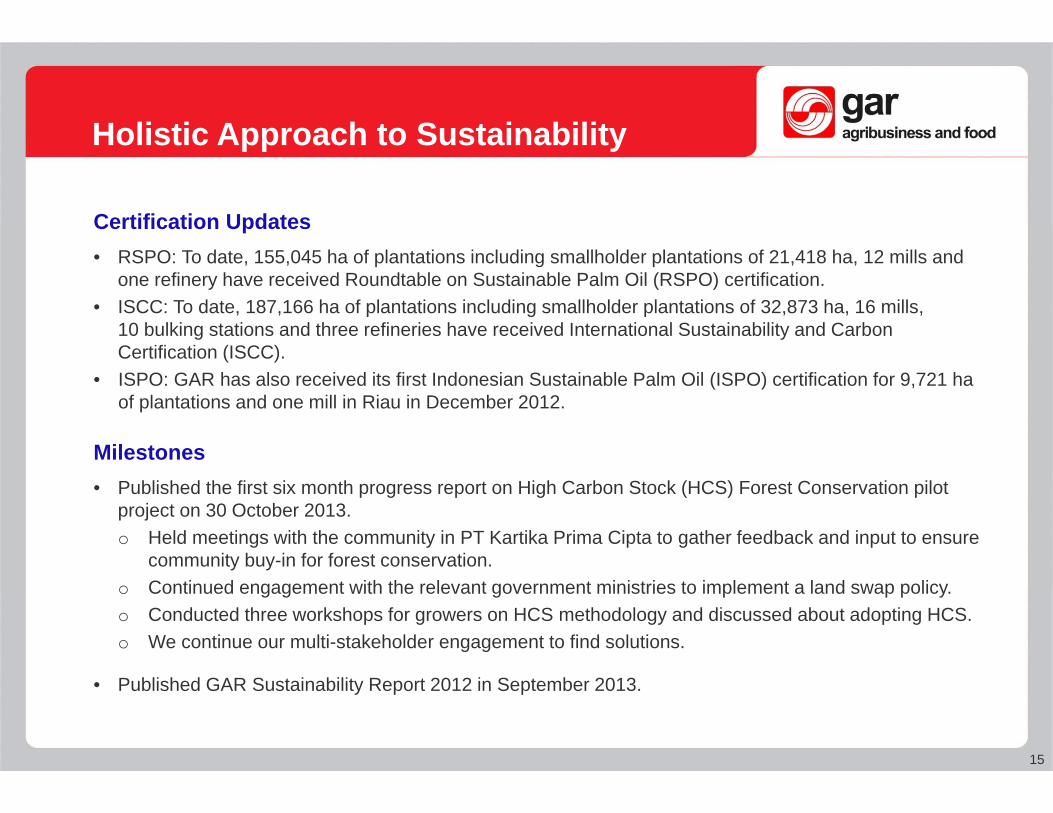

Holistic Approach to Sustainability

Certification Updates• RSPO: To date, 155,045 ha of plantations including smallholder plantations of 21,418 ha, 12 mills and

one refinery have received Roundtable on Sustainable Palm Oil (RSPO) certification.• ISCC: To date, 187,166 ha of plantations including smallholder plantations of 32,873 ha, 16 mills,

10 bulking stations and three refineries have received International Sustainability and Carbon Certification (ISCC).

• ISPO: GAR has also received its first Indonesian Sustainable Palm Oil (ISPO) certification for 9,721 ha of plantations and one mill in Riau in December 2012.

Milestones• Published the first six month progress report on High Carbon Stock (HCS) Forest Conservation pilot

project on 30 October 2013.o Held meetings with the community in PT Kartika Prima Cipta to gather feedback and input to ensure

community buy-in for forest conservation.o Continued engagement with the relevant government ministries to implement a land swap policy.o Conducted three workshops for growers on HCS methodology and discussed about adopting HCS.o We continue our multi-stakeholder engagement to find solutions.

• Published GAR Sustainability Report 2012 in September 2013.

Section 4

Downstream Highlights

17

Our Brands

Expanding Downstream Capacity in Indonesia

• YTD Sep 2013 sales volume of refined products grew by 58% year-on-year

• Refining capacity expansion supported by:• Growing palm products output from our plantations• Export tax scheme favouring refined products• Government target to allow only packaged cooking oil in Indonesia by 2015

• Improved logistics infrastructure through increased bulking and warehousing capacity as well as owned port and jetties

• Our prominent cooking oil brands, Filma and Kunci Mas, are among the leaders in Indonesia supported by nation-wide coverage with hundreds of distributors and thousands of retailers

Expanding Indonesia downstream production base for global exports

0200400600800

100012001400160018002000

2009 2010 2011 2012 Sep-13

Annu

al C

apac

ity ('

000

MT)

Kernel crushingcapacity

Refinery capacity

Expanded annual capacity by 180k MT in Q3 2013

18

ZhuhaiNingbo

Tianjin

Strengthening Downstream Business in China

Strengthening of the management team showing positive impact in China as one of the largest and fastest growing edible oils consumers

GAR strategically strengthen its presence in China by:• Developing distribution channels to enter new areas in

China• Achieve competitive raw material cost by exploring

strategic sourcing opportunities• Enhance relationships with end customers by providing

additional services• Actively manage flexible production to optimise profits• Pursuing value-added products such as specialty fats

Facilities Annual CapacityRefining 776,000 MT

Crushing 2.3 million MT

Noodle Manufacturing 5 billion packets

Oilseeds facilitiesFood facilities

19

Section 5

Strategy and Outlook

20

Strategic Priorities

Build on core competitive strengths and leverage scale to maximize long-term shareholder returns

Objective: Sustained Growth and Profitability

Upstream

• To become the world largest oil palm plantation company in terms of planted area through green field and acquisitions

• Sustain cost leadership through operational excellence, best-in-class plantation management and highest yielding seeds

Downstream• Optimise value throughout the chain supported

by prudent risk management• Grow destination business by extending

distribution and processing reach to key consuming countries

• Shift product mix to higher value-added products, including oleochemicals, through innovation and customer solutions

Continued strong commitment to environmental and social responsibility

21

Downstream Value Chain Optimisation

CANADA

PAKISTAN

TURKEY

UKNETHERLANDGERMANY

EGYPT

46

5

9

10

128

11

Capitalise on our unique advantage of having own large CPO production and close access to third party plantations …

… to grow our globally diversified customer base via distribution, branding, merchandising, destination processing and shipping

East Asia

South Asia

EUUS

Africa

Middle East

CPO inputTrade flows

22

Downstream Value Chain Optimisation

Commercially manage our plantation output and downstream assets to capitalise on value chain optimisation opportunities

Efficient logistics• Own large CPO

output base• Close access to

3rd party plantations

Sourcing of raw materials

• Strategic locations provide logistics advantage

• Refining, shortenings, specialty fats, and oleochemicals facilities

Processing

Margin optimisation through large product portfolio -specifications, quality and sustainability certification

Product customisation

Broad geographic footprint - distribution, branding, merchandising, destination processing, shipping and logistics

Sales and distribution

23

Growth Strategy and Outlook

Growth Strategy• Expanding palm oil plantations by 25,000-30,000 hectares in 2013 through organic growth and

acquisition• Building milling capacity in line with the growth in fruits production• Constructing additional downstream processing capacity in strategic locations • Extending distribution coverage and global market reach as well as logistic facilities to enhance

our integrated operations

Projected capex for FY 2013 growth strategy: approximately US$550 million

Industry OutlookIn the long term, GAR remains to believe in the robust demand growth of palm oil:• As edible oil from both emerging markets and developed countries• As substitute and alternative uses such as oleochemicals and biodiesel• Supported by limited supply growth of other vegetable oils, especially soybean

GAR continues to expand its integrated operation capabilities in order to capitalise on the firm industry long-term outlook, best-in-class plantation

management and solid financial position

24

Section 6

Appendix

25

Revenue Details

CPO38%

Unbranded Refined Palm

Products35%

Branded Products

7%

Soybean Meal8%

Soybean Oil3%

Soybean 4% Others5%

YTD Sep 2013 revenue of US$4.7 billion mainly from CPO and refined palm oil based products

By CountryBy Product

Indonesia Local11%

Indonesia Export

69%

China Local20%

26

Age Profile

GAR’s long-term growth is supported by favourable age profile of planted area underpinned by large immature and young plantations

30 September 2013Nucleus 28,875 69,494 173,434 76,349 20,324 368,476Plasma 6,527 10,103 50,888 31,020 - 98,538Total Area 35,402 79,597 224,322 107,369 20,324 467,014% of total planted area 8% 17% 48% 23% 4% 100%

Immature Young Prime Old 1 Old 2 Total(in ha) (0-3 years) (4-6 years) (7-18 years) (19-25 years) (>25 years)

Note:Average age of plantations as of 30 September 2013 is 13 years

30 September 2012Nucleus 33,399 83,920 153,839 73,027 19,401 363,586Plasma 7,966 8,033 58,093 21,824 - 95,916Total Area 41,365 91,953 211,932 94,851 19,401 459,502% of total planted area 9% 20% 46% 21% 4% 100%

27

Contact Us

If you need further information, please contact:

Golden Agri-Resources Ltdc/o 108 Pasir Panjang Road#06-00 Golden Agri PlazaSingapore 118535

Telephone : +65 65900800Facsimile : +65 65900887

www.goldenagri.com.sg

Contact Person : Richard Fung ([email protected])