interim report / 2013 - admin.blacksheep.design report / 2013. palmerst 201 2. 03 ... cooper rapley...

TRANSCRIPT

PALMERSTON NORTH AIRPORT 2013 INTERIM REPORT 1

I N T E R I M R E P O R T / 2 0 1 3

PALMERSTON NORTH AIRPORT 2013 INTERIM REPORT 2

0 3

C O N T E N T S3 Joint Chairman & Chief Executive’s Report5 Statement of Service Performance6 Financial Statements11 Notes to the Financial Statements

0 4

DIRECTORS: D N Walker (Chairman) O B StockG F GillespieJ E NicholsJ M K B Adlam

MANAGEMENT:D R Cusack Chief ExecutiveR A Bodell Manager Transition & ProjectsL M J Macdonald Manager Business Services & Secretary to the BoardG W Pleasants Manager Aeronautical & Infrastructure

REGISTERED OFFICE:Palmerston North International AirportTerminal BuildingAirport DrivePALMERSTON NORTH 4442

Phone: +64 6 351 4415Fax: +64 6 355 2262e-mail: [email protected]: www.pnairport.co.nz

TRADING BANKERS:Bank of New Zealand

LEGAL ADVISOR:Cooper Rapley

AUDITORS:Audit New Zealand (on behalf of The Auditor-General)

PALMERSTON NORTH AIRPORT LIMITED

C O M P A N Y D I R E C T O R Y

0 5

The first six months of the 2013/14 financial year has been a positive period for Palmerston North Airport Ltd (PNAL) with a range of projects completed or underway and an improved financial result.

The Board and Management of PNAL continue to move forward with implementation of the Company’s strategy. The importance of growth across the region is essential for PNAL’s on-going growth and we continue to strive to achieve our vision to “grow shareholder and regional economic value by operating a safe, efficient, attractive and profitable airport that serves the Central Region”. The vision reflects the importance that the airport plays to the greater region and the need to work closely with a wide range of stakeholders both from a business and tourism perspective in identifying growth opportunities across the visitor and business sectors.

From a financial perspective, a net surplus after tax of $306,171 was achieved for the period. This is 43% above the same period last year. Revenue was up 7.5% on the same period last year as a result of increased passenger numbers which also flowed through to higher car park usage. In addition PNAL experienced growth in land & building rental as a result of moving to concession based charging for the terminal retail activity. EBITDA is up 17.9% on the same period last year.

Passenger numbers on scheduled commercial flights for the six months to 31 December 2013 were up 9% on the same period last year. The available seat capacity was 4% above the same six-month period last year which indicates higher load factors on flights with larger 68 seat aircraft being used more frequently on Auckland and Christchurch routes.

The company undertook a review of its debt structure with new arrangements being completed during 2012/13. The restructuring saw a review of arrangements, with the outcome being a more flexible debt facility for the business. As a result of this re-structure, PNAL reduced the cost of debt for the period by 10%.

PNAL have continued to work closely with Air New Zealand on a range of activities to support both inbound and outbound growth with a range of packages to bring visitors into the region. PNAL also continues to raise the profile of Palmerston North as an airport which is easy to access by road with cost effective car parking options supporting outbound travelers from the greater region. The importance of Palmerston North, Horowhenua, Rangitikei, Ruapehu, Manawatu and Tararua Districts collaborating on initiatives is key part of future success and we continue to refine our visitor strategy focusing on the fly market, however funding constraints restricts activities to support this.

In July we saw the launch of Nelson direct services with Air New Zealand. This has provided both important business and leisure connections for the wider regions of Tasman and Manawatu. Customer feedback has been very good with Air New Zealand now committing to this sector on a full time basis; the team continues to discuss other opportunities around new and existing routes.

Palmerston North also supported the response to natural seismic and weather events in the Wellington region, with diverted air traffic up on the previous year. PNAL’s ability to react positively and provide services for various aircraft diversions has highlighted the importance of PNAL as an emergency alternate. In addition, the strategic advantages of our central location for logistics/distribution businesses and 24/7 operation provide opportunities to grow our already important night freight market.

FROM THE CHAIRMAN & CHIEF EXECUTIVE OFFICER FOR THE SIX MONTHS ENDING 31 DECEMBER 2013

J O I N T R E P O R T

0 6

We continue to seek growth opportunities both from an aeronautical and non-aeronautical perspective. A more commercial approach to various airport concessions and agreements has been followed through, with additional contractual changes planned in the second half of the financial year.

Operationally, we have continued capital upgrades on a variety of facilities with further car park upgrading and resurfacing complete. On airside, we have completed aircraft parking apron upgrades. We have also confirmed our runway capital plan for the next three years with stage one of the programmed runway resurfacing commencing in February 2014.

All statutory requirements relating to the airport have been met, including satisfactory independent audits by the Civil Aviation Authority, during the first six months of the year. These were also supported by continuing monthly internal audits and quality control checks undertaken by an independent body.

The following have been progressed over the last six months:-

• Forward capital program for airside runway pavements confirmed• Completion of stage one of a visitor strategy for the region • Aeronautical route development plans undertaken with the introduction of Nelson direct services and

additional capacity to Auckland and Christchurch • Completion of the café offering in terminal• A 2.6% increase in vehicles using the car park by comparison with the first 6 months of 2013, generated a

3.5% increase in revenue for the same period. • Completion of a new airside facility for Air BP• New airport retail concession with LS Travel (Relay) in the terminal building• Stage one of new car parking system at Palmerston North Airport • Successful negotiation and implementation of new terminal cleaning contract• Review of the air noise contour plan• Review of the Airport Masterplan underway

We watch with interest the performance of the local and global economy and how it impacts on the region in regard to growth opportunities. The domestic travel market has been consistent over the last 6 months, and upcoming airline alliances continue to be a feature of the Australia/New Zealand aviation market with recent announcements from Air New Zealand.

The importance of the wider region collaborating on a visitor strategy that supports opportunities continues to be high on priorities for the second half of the financial year. PNAL is committed to supporting the regions various visitor agencies to identify events and activities for promotion to the domestic and international markets, whilst building on iconic activities such as the Department of Conservation: “Great Walks” featuring the Tongariro Crossing and Whanganui River.

In closing PNAL continue to review its operations and opportunities to bring travelers into the region, we look forward to the stage one runaway project and upgrade of the car park system which continues the prudent capital investment plans for the airport; this also provides benefits to our customers and users.

Derek Walker Darin Cusack Chairman Chief Executive

0 7

• The Company’s Amended Statement of Intent is dated December 2013.• The Company has an interest in FreightGate Limited, a wholly owned subsidiary company which was

formed in October 2001and may be used for the management of non-operational property.• The ratio of consolidated shareholders’ funds to total assets has been maintained above 70%.• The Company is trading as Palmerston North Airport and FreightGate.• Palmerston North Airport has been maintained as an airport certificated pursuant to Civil Aviation Rule Part

139 and has achieved satisfactory audits during the period.• All obligations under the Resource Management Act and the District Plans of the Palmerston North City

Council and Manawatu District Council have been met.

PERFORMANCE MEASURES:

OBJECTIVE:“To grow the shareholder’s and regional economic value by operating a safe, efficient, attractive and profitable airport that serves the Central Region.”

STATEMENT OF SERVICE PERFORMANCE

S E R V I C E P E R F O R M A N C E

Dec 2013 Dec 2012 SOI Target % of target

6 Months 6 Months 12 Months achieved

1. Ratio of Net Surplus before interest and tax to Total Assets:

1.4% 1.2% 2.8% 51%

2. Ratio of Net Surplus after interest and tax to consolidated Shareholders funds:

0.9% 0.6% 1.7% 51%

3. Interest cover ratio of Net Surplus before interest tax and depreciation to interest, at or above :

5.2 2.4 ≥2.5 260%

4. Maintain a tangible net worth (of or above) 35.6 35.20 ≥$35m 100%

5. Total Passenger Throughput 250,284 229,767 475,000 53%

6. Maintain a high level of customer satisfaction 98% are either "Quite satisfied" or “very satisfied” - Customer Satisfaction Survey November 2013

0 8

Derek Walker Gerard GillespieChairman Director

The accompanying accounting policies and notes form part of and are to be read in conjunction with these financial statements

Date: 20 February 2014

STATEMENT OF FINANCIAL PERFORMANCE - PARENT & CONSOLIDATED FOR THE SIX MONTHS ENDED 31 DECEMBER 2013

31-Dec-13 31-Dec-12 30-Jun-14 30-Jun-13

Note 6 Months Unaudited

6 Months Unaudited

12 Months SOI

12 Months Audited

REVENUE 4 2,509,747 2,333,380 4,706,000 4,589,800

OPERATIONAL & MAINTENANCE COSTS

Airfield Services 246,752 246,752 493,500 493,503

Other Operating Expenses 5 575,680 645,430 1,004,000 1,180,906

TOTAL OPERATIONAL & MAINTENANCE COSTS 822,432 892,182 1,497,500 1,674,409

ADMINISTRATION

Audit Fees 14,000 13,583 28,000 27,083

Loss on Sale of Assets 2,812

Bad Debts Written Off 18,732 12,847 5,000 13,367

Changes in doubtful debt provision

Directors' Fees 38,250 38,250 76,500 76,500

Employee Expenses 6 347,243 384,508 825,253 700,649

General Administration 294,983 166,130 304,747 329,876

TOTAL ADMINISTRATION: 713,208 615,318 1,239,500 1,150,287

TOTAL OPERATING COSTS 1,535,640 1,507,500 2,737,000 2,824,696

Operating Surplus before interest, depreciation & taxation 974,107 825,880 1,969,000 1,765,104

FINANCE COSTS & DEPRECIATION

Finance costs 7 187,328 209,122 411,500 408,709

Depreciation 15 344,972 319,895 711,500 647,477

TOTAL FINANCE COSTS & DEPRECIATION: 532,300 529,017 1,123,000 1,056,186

Operating Surplus before taxation 441,807 296,863 846,000 708,918

Taxation Expense on operating surplus 8 135,636 83,122 236,500 217,035

NET SURPLUS AFTER TAXATION 306,171 213,741 609,500 491,883

For and on behalf of the Board

Date: 20 February 2014

0 9

31-Dec-13 31-Dec-12 30-Jun-14 30-Jun-13

Note 6 Months Unaudited

6 Months Unaudited

12 Months SOI

12 Months Audited

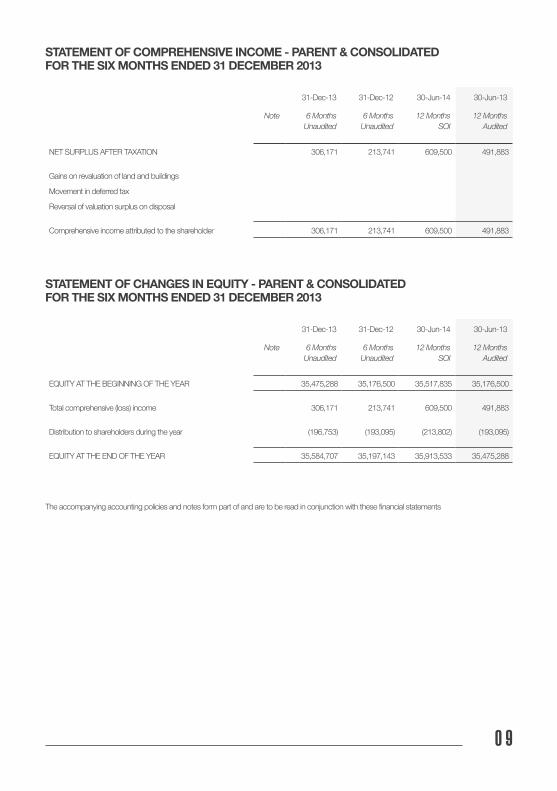

NET SURPLUS AFTER TAXATION 306,171 213,741 609,500 491,883

Gains on revaluation of land and buildings

Movement in deferred tax

Reversal of valuation surplus on disposal

Comprehensive income attributed to the shareholder 306,171 213,741 609,500 491,883

STATEMENT OF COMPREHENSIVE INCOME - PARENT & CONSOLIDATED FOR THE SIX MONTHS ENDED 31 DECEMBER 2013

STATEMENT OF CHANGES IN EQUITY - PARENT & CONSOLIDATED FOR THE SIX MONTHS ENDED 31 DECEMBER 2013

31-Dec-13 31-Dec-12 30-Jun-14 30-Jun-13

Note 6 Months Unaudited

6 Months Unaudited

12 Months SOI

12 Months Audited

EQUITY AT THE BEGINNING OF THE YEAR 35,475,288 35,176,500 35,517,835 35,176,500

Total comprehensive (loss) income 306,171 213,741 609,500 491,883

Distribution to shareholders during the year (196,753) (193,095) (213,802) (193,095)

EQUITY AT THE END OF THE YEAR 35,584,707 35,197,143 35,913,533 35,475,288

The accompanying accounting policies and notes form part of and are to be read in conjunction with these financial statements

010

STATEMENT OF FINANCIAL POSITION - PARENT & CONSOLIDATED AS AT 31 DECEMBER 2013

31-Dec-13 31-Dec-12 30-Jun-14 30-Jun-13

Note 6 Months Unaudited

6 Months Unaudited

12 Months SOI

12 Months Audited

CURRENT ASSETS

Cash and Cash Equivalents 9 302,136 330,591 289,259 344,304

Trade Accounts Receivable 10 404,721 369,140 300,762 332,516

Inventory 11 133 2,066

Sundry Receivables and Prepayments 91,510 94,834 15,677 11,431

Tax Receivable

TOTAL CURRENT ASSETS 798,500 796,631 605,697 688,251

Less: CURRENT LIABILITIES

Income in Advance 105,745 95,987 90,000 79,380

Trade Accounts Payable 12 770,105 101,086 120,000 172,265

Other Creditors 17,212 70,727 150,000 70,892

Employee Benefit Liabilities 13 39,056 4,973 60,000 36,035

Tax Payable 27,255 19,479 86,054 17,362

Current Portion of Borrowings 14 700,000

TOTAL CURRENT LIABILITIES 959,373 992,252 506,054 375,934

WORKING CAPITAL (160,873) (195,621) 99,643 312,317

Add: NON CURRENT ASSETS

Property, Plant & Equipment 15 43,321,697 42,844,508 44,565,633 43,039,088

Less: NON CURRENT LIABILITIES

Deferred Tax Liability 16 2,876,117 2,751,744 2,751,744 2,876,117

Borrowings 14 4,700,000 4,700,000 6,000,000 5,000,000

TOTAL NON CURRENT LIABILITIES 7,576,117 7,451,744 8,751,744 7,876,117

NET ASSETS 35,584,707 35,197,143 35,913,533 35,475,288

Represented by:

SHAREHOLDERS' EQUITY

Paid in Capital 9,380,400 9,380,400 9,380,400 9,380,400

Retained Earnings 16,071,093 15,683,529 16,399,919 15,961,674

Asset Revaluation Reserve 10,133,214 10,133,214 10,133,214 10,133,214

TOTAL SHAREHOLDERS' EQUITY 35,584,707 35,197,143 35,913,533 35,475,288

The accompanying accounting policies and notes form part of and are to be read in conjunction with these financial statements

Derek Walker Gerard GillespieChairman DirectorDate: 20 February 2014

For and on behalf of the Board

Date: 20 February 2014

011

CASH FLOW STATEMENT - PARENT & CONSOLIDATED FOR THE SIX MONTHS ENDED 31 DECEMBER 2013

31-Dec-13 31-Dec-12 30-Jun-14 30-Jun-13

Note 6 Months Unaudited

6 Months Unaudited

12 Months SOI

12 Months Audited

CASH FLOWS FROM OPERATING ACTIVITIES

Cash was provided from:

Receipts from Customers 2,465,231 2,275,498 4,690,518 4,345,606

Interest Received 2,654 969 9,000 5,715

Tax Refund 201,579

2,467,885 2,276,467 4,699,518 4,552,900

Cash was disbursed to:

Payment to Suppliers and Employees 1,443,620 1,805,066 2,646,109 2,731,547

Net GST Movement 131,773

Payment of Income Tax 45,000 120,000 218,000 200,000

Interest Payments 189,364 209,122 411,585 408,709

1,677,984 2,134,188 3,275,694 3,472,029

Net Cash Flows from Operating Activities 17 789,901 142,279 1,423,824 1,080,871

CASH FLOWS FROM INVESTING ACTIVITIES

Cash was provided from:

Sale of Fixed Assets

Cash was applied to:

Purchase of Fixed Assets 335,316 125,489 1,667,290 650,368

Net Cash Flow from Investing Activities (335,316) (125,489) (1,667,290) (650,368)

CASH FLOW FROM FINANCING ACTIVITIES

Cash was provided from:

Borrowing 4,700,000 500,000 300,000

Cash was applied to:

Repayment of Borrowings 300,000 4,700,000 200,000 700,000

Payment of Dividends 196,753 193,095 213,802 193,095

Net Cash from Financing Activities (496,753) (193,095) 86,198 (593,095)

Net Increase/(Decrease) in Cash, Cash Equivalents and Bank Overdrafts

(42,168) (176,305) (157,268) (162,592)

Cash, Cash Equivalents and Bank Overdrafts at the beginning of the year

344,304 506,896 446,527 506,896

Cash, Cash Equivalents and Bank Overdrafts at the end of the year 9 302,136 330,591 289,259 344,304

Made up of:

Cash and Bank Balance 302,136 330,591 289,259 344,304

CLOSING CASH BALANCE 302,136 330,591 289,259 344,304

The accompanying accounting policies and notes form part of and are to be read in conjunction with these financial statements

1 2

CONSOLIDATED STATEMENT OF COMMITMENTS FOR THE SIX MONTHS ENDED 31 DECEMBER 2013

NON-CANCELLABLE COMMITMENTS - OPERATING LEASE COMMITMENTS

Not more than one year 18,306.00

One to two years 10,558.00

Two to five years 6,736.00

Over five years

35,600.0018

1 3

1. REPORTING ENTITY

Palmerston North Airport Limited is a New Zealand company registered under the Companies Act 1993.

The Company and its wholly owned subsidiary (FreightGate Limited) comprise the Palmerston North Airport Limited reporting entity.

The financial statements of Palmerston North Airport Limited are reported as parent and consolidated due to FreightGate Limited being a non-trading company during the six months to 31 December 2013.

2. BASIS OF PREPARATION

Statement of compliance The financial statements of Palmerston North Airport Limited have been prepared in accordance with the requirements of the Airport Authorities Act 1966, Airport Authorities Amendment Act 2000, the Local Government Act 2002, Airport Authorities (Airport Companies Information Disclosure) Regulations 1999 the Companies Act 1993, and the Financial Reporting Act 1993. The financial statements have been prepared in accordance with NZ GAAP. They comply with NZIFRS and other applicable Financial Reporting Standards as appropriate for public benefit entities.

Measurement base The financial statements have been prepared on a historical cost basis except where modified by the revaluation of land and buildings.

Functional and presentation currency The financial statements are presented in New Zealand dollars and all values are rounded to the nearest dollar. The functional currency of the company is New Zealand Dollars.

3. ACCOUNTING POLICIES

Changes in accounting policies There were no changes to accounting policies during the period being reported.

Specific accounting policies The accounting policies as published in the Annual Report to 30 June 2013 have been applied constantly to all periods presented in these financial statements.

FOR THE SIX MONTHS ENDED 31 DECEMBER 2013

N O T E S T O T H E F I N A N C I A L S T A T E M E N T S

1 4

4. ANALYSIS OF OPERATING REVENUE

31-Dec-13 31-Dec-12 30-Jun-14 30-Jun-13

6 Months Unaudited

6 Months Unaudited

12 Months SOI

12 Months Audited

Landing, departure & facility fees 1,359,358 1,291,066 2,567,629 2,508,860

Car park, rent and advertising 1,058,044 982,572 2,064,308 1,968,249

Other 89,691 58,774 65,063 106,976

Interest 2,654 968 9,000 5,715

2,509,747 2,333,380 4,706,000 4,589,800

5. OTHER OPERATING EXPENSES

Rates 181,062 154,513 318,000 337,402

Power and Insurance 164,319 143,886 282,505 288,614

Repairs and maintenance 230,299 347,031 403,495 554,890

575,680 645,430 1,004,000 1,180,906

6. EMPLOYEE EXPENSES

Salaries and wages 386,299 419,806 830,000 688,195

Employer Contribution to Kiwi Saver 9,432

Movement in employee entitlements (39,056) (35,298) (4,747) 3,022

347,243 384,508 825,253 700,649

7. FINANCE COST

Interest on term loans 187,328 209,122 411,500 408,709

Interest on overdraft

187,328 209,122 411,500 408,709

8. TAXATION

Current year tax payable 135,636 83,122 236,500 179,112

Prior year adjustments (86,450)

Movement in deferred tax 124,373

Total 135,636 83,122 236,500 217,035

Tax payable is exclusive of any tax–loss offset with Palmerston North City Council.

1 5

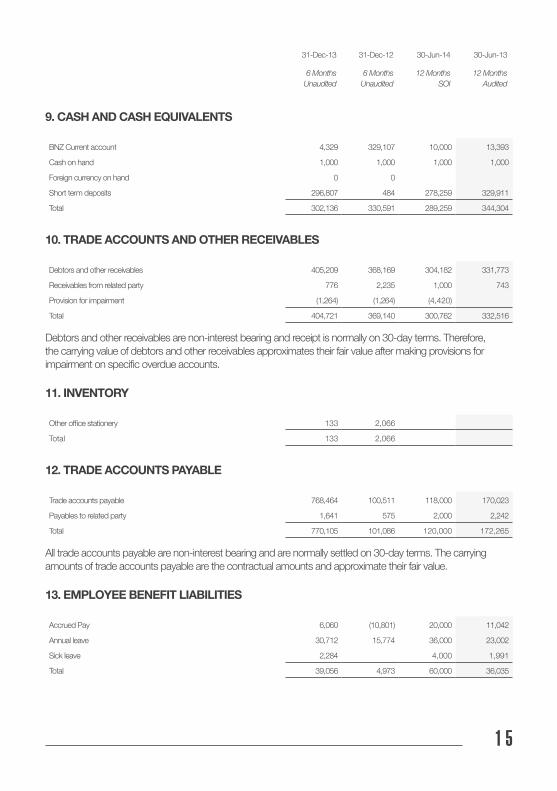

9. CASH AND CASH EQUIVALENTS

31-Dec-13 31-Dec-12 30-Jun-14 30-Jun-13

6 Months Unaudited

6 Months Unaudited

12 Months SOI

12 Months Audited

BNZ Current account 4,329 329,107 10,000 13,393

Cash on hand 1,000 1,000 1,000 1,000

Foreign currency on hand 0 0

Short term deposits 296,807 484 278,259 329,911

Total 302,136 330,591 289,259 344,304

10. TRADE ACCOUNTS AND OTHER RECEIVABLES

Debtors and other receivables 405,209 368,169 304,182 331,773

Receivables from related party 776 2,235 1,000 743

Provision for impairment (1,264) (1,264) (4,420)

Total 404,721 369,140 300,762 332,516

Debtors and other receivables are non-interest bearing and receipt is normally on 30-day terms. Therefore, the carrying value of debtors and other receivables approximates their fair value after making provisions for impairment on specific overdue accounts.

13. EMPLOYEE BENEFIT LIABILITIES

Accrued Pay 6,060 (10,801) 20,000 11,042

Annual leave 30,712 15,774 36,000 23,002

Sick leave 2,284 4,000 1,991

Total 39,056 4,973 60,000 36,035

11. INVENTORY

Other office stationery 133 2,066

Total 133 2,066

12. TRADE ACCOUNTS PAYABLE

Trade accounts payable 768,464 100,511 118,000 170,023

Payables to related party 1,641 575 2,000 2,242

Total 770,105 101,086 120,000 172,265

All trade accounts payable are non-interest bearing and are normally settled on 30-day terms. The carrying amounts of trade accounts payable are the contractual amounts and approximate their fair value.

1 6

14. BORROWINGS

31-Dec-13 31-Dec-12 30-Jun-14 30-Jun-13

6 Months Unaudited

6 Months Unaudited

12 Months SOI

12 Months Audited

Borrowings 4,700,000 4,700,000 6,000,000 5,000,000

Current portion of borrowings 700,000

Total 4,700,000 5,400,000 6,000,000 5,000,000

15. PROPERTY, PLANT AND EQUIPMENT

30-Jun-13 31-Dec-13

Carrying Amount

Additions Disposals Depreciation Carrying Amount

Land 21,351,000 21,351,000

Buildings 10,977,012 40,699 115,606 10,902,105

Infrastructure 9,738,925 592,482 17,946 174,871 10,138,590

Plant & Equipment 664,768 9,999 26,812 647,955

Furniture & Fittings 257,920 1,291 19,496 239,715

Computer Equipment 25,022 1,720 5,421 21,321

Motor Vehicles

Intangibles 23,777 2,765 21,012

43,038,424 646,191 17,946 344,972 43,321,697

A registered first debenture and mortgage secure the $4.7 million borrowings from Bank of New Zealand over assets and property of the Company.

The carrying value of borrowings is materially consistent with their fair value.

16. DEFERRED TAX ASSETS/(LIABILITIES)

Property, plant and equipment

Employee entitlements

Other provisions

Total

Balance at 30 June 2013 2,885,746 (9,629) 2,876,117

Change to profit and loss

Balance at 31 December 2013 2,885,746 (9,629) 2,876,117

1 7

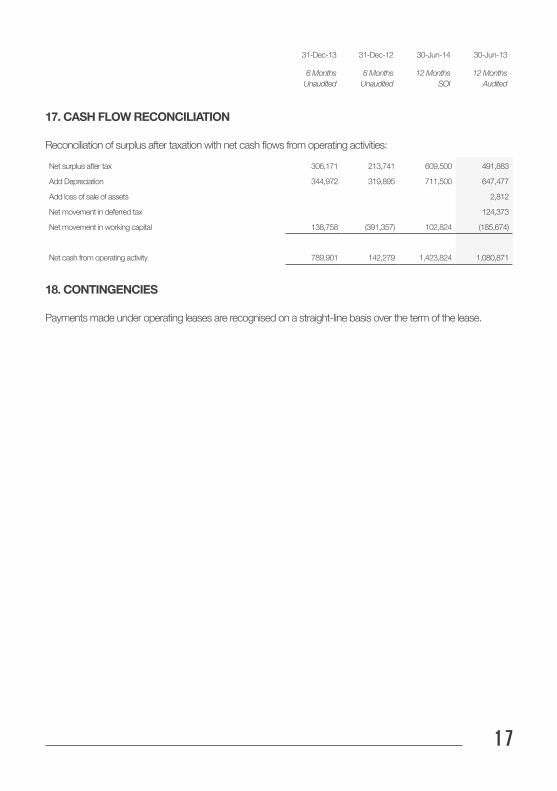

17. CASH FLOW RECONCILIATION

31-Dec-13 31-Dec-12 30-Jun-14 30-Jun-13

6 Months Unaudited

6 Months Unaudited

12 Months SOI

12 Months Audited

Net surplus after tax 306,171 213,741 609,500 491,883

Add Depreciation 344,972 319,895 711,500 647,477

Add loss of sale of assets 2,812

Net movement in deferred tax 124,373

Net movement in working capital 138,758 (391,357) 102,824 (185,674)

Net cash from operating activity 789,901 142,279 1,423,824 1,080,871

Reconciliation of surplus after taxation with net cash flows from operating activities:

18. CONTINGENCIES

Payments made under operating leases are recognised on a straight-line basis over the term of the lease.

1 8

PALMERSTON NORTH AIRPORT 2013 INTERIM REPORT 19

PALMERSTON NORTH AIRPORT 2013 INTERIM REPORT 20

P N A I R P O R T. C O . N ZF B . C O M / P N A I R P O R T