interim results fy2021 - seeking alpha

TRANSCRIPT

INTERIM RESULTS FY202125 February 2021

2IMPLATS

INTERIM RESULTS FY2021

FORWARD-LOOKING AND CAUTIONARY STATEMENT

Certain statements contained in this presentation, other than the statements of historical fact, contain forward-looking statements regarding Implats’

operations, economic performance or financial condition, including, without limitation, those concerning the economic outlook for the platinum

industry, expectations regarding metal prices, production, cash costs and other operating results, growth prospects and the outlook of Implats’

operations, including the completion and commencement of commercial operations of certain of Implats’ exploration and production projects, its

liquidity and capital resources and expenditure and the outcome and consequences of any pending litigation, regulatory approvals and/or legislative

frameworks currently in the process of amendment, or any enforcement proceedings. Although Implats believes that the expectations reflected in

such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to be correct. Accordingly, results

may differ materially from those set out in the forward-looking statements as a result of, among other factors, changes in economic and market

conditions, success of business and operating initiatives, changes in the regulatory environment and other government actions, fluctuations in metal

prices, levels of global demand and exchange rates and business and operational risk management. For a discussion on such factors, refer to the

risk management section of the company’s Integrated Annual Report. Implats is not obliged to update publicly or release any revisions to these

forward-looking statements to reflect events or circumstances after the dates of the Annual Report or to reflect the occurrence of unanticipated

events.

Disclaimer: This entire presentation and all subsequent written or oral forward-looking statements attributable to Implats or any person acting on its

behalf are qualified by caution. Recipients hereof are advised the presentation is prepared for general information purposes and not intended to

constitute a recommendation to buy- or offer to sell shares or securities in Implats or any other entity. Sections of this presentation are not defined

and assured under IFRS, but included to assist in demonstrating Implats’ underlying financial performance. Implats recommend you address any

doubts in this regard with an authorised independent financial advisor, stockbroker, tax advisor, accountant or suitably qualified professional.

3IMPLATS

INTERIM RESULTS FY2021

AGENDA

01 02 03 04 05Group overview

Operationaloverview

Financialreview

Marketreview

Businessoutlook

Nico Muller Mark Munroe

Gerhard Potgieter

Meroonisha Kerber Sifiso Sibiya Nico Muller

IMPLATS

INTERIM RESULTS FY2021

GROUP OVERVIEW Nico Muller

01

5IMPLATS

INTERIM RESULTS FY2021

6 Shaft 3.07 million

20 Shaft 2.93 million

16 Shaft 2.85 million

Mineral Processes 1.17 million

10 Shaft 1.09 million

E&F Shaft 1.03 million

GROUP SAFETY OVERVIEW

8

7

5 5

0

6.356.01

5.30

4.54 5.13

0

1

2

3

4

5

6

7

8

0

2

4

6

8

10

12

14

FY2017 FY2018 FY2019 FY2020 H1 FY2021

LTIFR**

FATALITIES

Rtb Services 13.74 million

Refineries 12.39 million

14 Shaft 5.43 million

9 Shaft 3.36 million

Zimplats 3.33 million

Marula 3.21 million

FATALITY FREE SHIFTS*

Implats reported no fatal incidents during the period

*as at 31 December 2020

**per million man hours worked

FATALITIES AND LOST-TIME INJURY FREQUENCY RATE

Description H1 FY2021 H1 FY2020 FY2020

Fatalities No. 0 3 5

FIFR pmmhw 0.000 0.055 0.050

LTIFR pmmhw 5.13 4.84 4.54

TIFR pmmhw 9.34 11.91 11.30

Impala Rustenburg 5.69 million Implats 7.83 million

6IMPLATS

INTERIM RESULTS FY2021

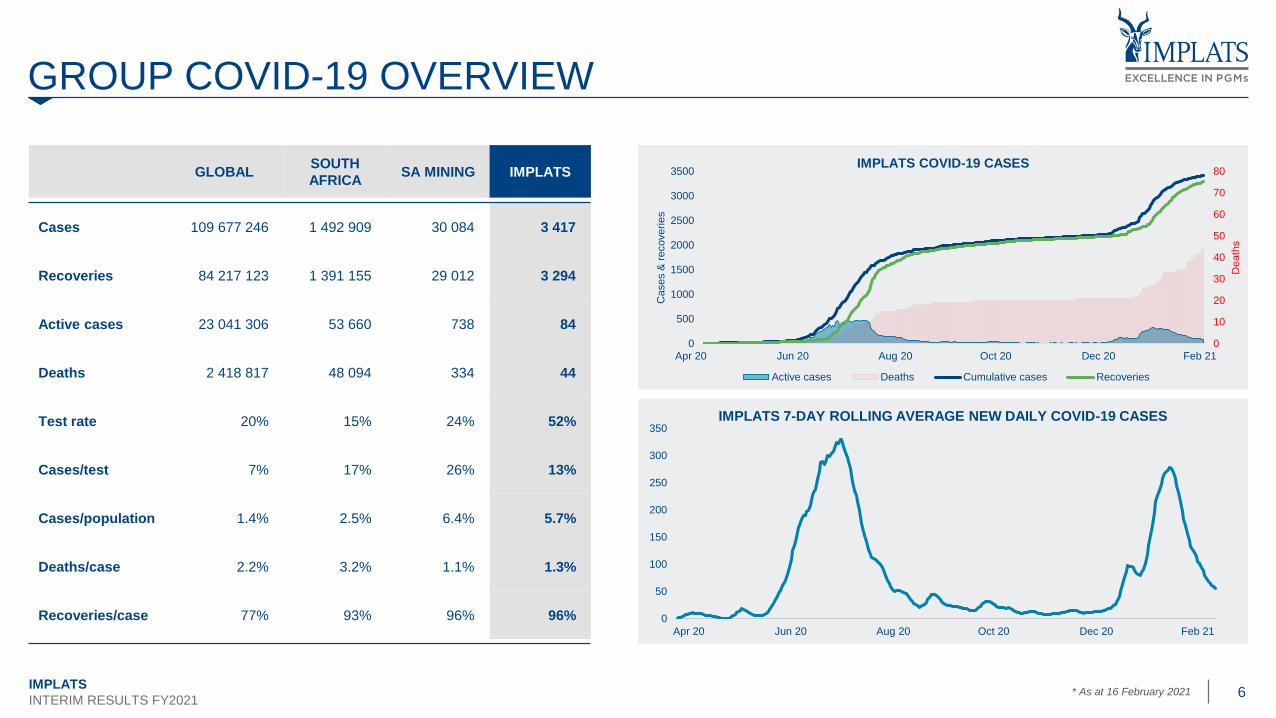

GROUP COVID-19 OVERVIEW

GLOBALSOUTH

AFRICASA MINING IMPLATS

Cases 109 677 246 1 492 909 30 084 3 417

Recoveries 84 217 123 1 391 155 29 012 3 294

Active cases 23 041 306 53 660 738 84

Deaths 2 418 817 48 094 334 44

Test rate 20% 15% 24% 52%

Cases/test 7% 17% 26% 13%

Cases/population 1.4% 2.5% 6.4% 5.7%

Deaths/case 2.2% 3.2% 1.1% 1.3%

Recoveries/case 77% 93% 96% 96%

* As at 16 February 2021

0

50

100

150

200

250

300

350IMPLATS 7-DAY ROLLING AVERAGE NEW DAILY COVID-19 CASES

0

10

20

30

40

50

60

70

80

0

500

1000

1500

2000

2500

3000

3500

Death

s

Cases &

recoverie

s

IMPLATS COVID-19 CASES

Active cases Deaths Cumulative cases Recoveries

Apr 20 Jun 20 Aug 20 Oct 20 Dec 20 Feb 21

Apr 20 Jun 20 Aug 20 Oct 20 Dec 20 Feb 21

7IMPLATS

INTERIM RESULTS FY2021

GROUP ESG OVERVIEW

Included for the

Bloomberg Gender-Equality Index

for the second year in a row

‘A’ rating for disclosures, awareness

and management of

water security risk

‘B’ rating for climate change

action and disclosures

IMPLATS

INTERIM RESULTS FY2021

Recognised by the

London Platinum and Palladium Market (LPPM)

for responsible sourcing of platinum and palladium

PLEASING PROGRESS ON OUR

SUSTAINABILITY EXCELLENCE

JOURNEY

• Zero Level 4 or 5 environmental

incidents

• 67% reduction in Level 3 incidents

• 18% increase in water recycled or

reused

• 11% reduction in scope 1 and 2

carbon emissions per tonne milled

• 26% increase in local procurement

spend to R1.8 billion

• R355 million spent on Covid-19

interventions across Group

operations in the period

8IMPLATS

INTERIM RESULTS FY2021

GROUP OPERATIONAL OVERVIEW

Description H1 FY2021 H1 FY2020 Var (%)

Tonnes Milled# kt 11 789 10 305 14%

Concentrate production 6E koz 1 684 1 539 9%

Managed operations 6E koz 1 205 1 090 11%

Impala 6E koz 660 653 1%

Zimplats 6E koz 297 299 (1%)

Marula 6E koz 121 124 (2%)

Impala Canada 6E koz 127 14 >100%

JV operations 6E koz 283 258 9%

Mimosa 6E koz 132 120 10%

Two Rivers 6E koz 150 138 9%

Third-party purchased 6E koz 196 190 3%

Refined production 6E koz 1 694 1 317 29%

Unit cost (to concentrate)# R/t 1 259 1 157 (9%)

Unit cost (refined stock-adjusted) R/oz 6E 14 292 13 157 (9%)

Capital expenditure# Rm 2 667 1 925 (39%)

Impala Rm 982 998 2%

Zimplats Rm 930 686 (36%)

Marula Rm 105 204 49%

Impala Canada Rm 640 37 (>100%)

#managed operations

1 5891 485

1 317

1 496

1 694

FY2019 FY2020 FY2021

6E

koz

REFINED PRODUCTION

11 41312 366

13 157 13 65714 292

FY2019 FY2020 FY2021

R/6

E o

z

UNIT COST

1 706

2 0801 925

2 5632 667

FY2019 FY2020 FY2021

Rm

CAPITAL EXPENDITURE

1 5611 449

1 539

1 311

1 684

FY2019 FY2020 FY2021

6E

koz

CONCENTRATE PRODUCTION

Managed JVs 3rd Party

9IMPLATS

INTERIM RESULTS FY2021

1 539

1 684

113

12 12

7 6

2 3

1 450

1 500

1 550

1 600

1 650

1 700

H1 FY20 Impala Canada Mimosa Two Rivers Impala 3rd party receipts Zimplats Marula H1 FY21

6E

koz

in c

oncentr

ate

MOVEMENT IN 6E CONCENTRATE PRODUCTION VS H1 FY2020

9

297(1%)

127>100%

1509%

6601%

1963%

121(2%)

13210%

koz 6E in concentrate

% variance from H1 FY2020

10IMPLATS

INTERIM RESULTS FY2021

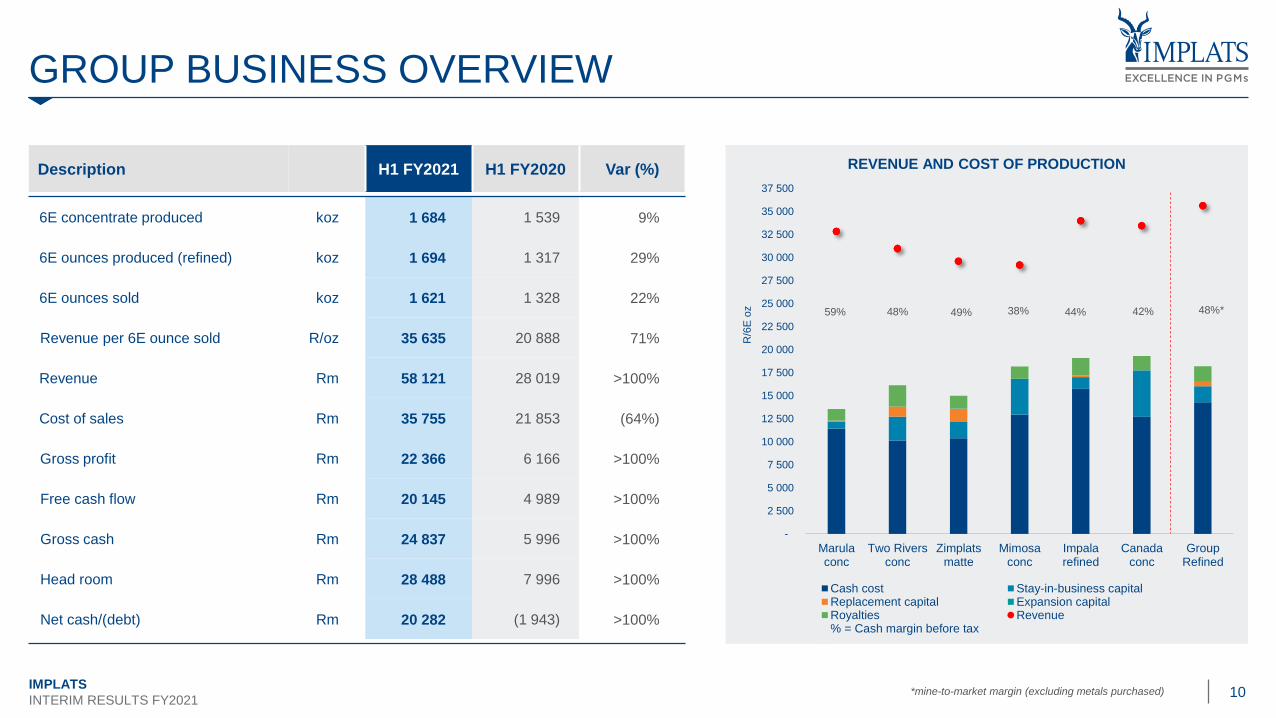

GROUP BUSINESS OVERVIEW

Description H1 FY2021 H1 FY2020 Var (%)

6E concentrate produced koz 1 684 1 539 9%

6E ounces produced (refined) koz 1 694 1 317 29%

6E ounces sold koz 1 621 1 328 22%

Revenue per 6E ounce sold R/oz 35 635 20 888 71%

Revenue Rm 58 121 28 019 >100%

Cost of sales Rm 35 755 21 853 (64%)

Gross profit Rm 22 366 6 166 >100%

Free cash flow Rm 20 145 4 989 >100%

Gross cash Rm 24 837 5 996 >100%

Head room Rm 28 488 7 996 >100%

Net cash/(debt) Rm 20 282 (1 943) >100%

59% 48% 49% 38% 44% 42%

-

2 500

5 000

7 500

10 000

12 500

15 000

17 500

20 000

22 500

25 000

27 500

30 000

32 500

35 000

37 500

Marulaconc

Two Riversconc

Zimplatsmatte

Mimosaconc

Impalarefined

Canadaconc

GroupRefined

R/6

E o

z

REVENUE AND COST OF PRODUCTION

Cash cost Stay-in-business capitalReplacement capital Expansion capitalRoyalties Revenue% = Cash margin before tax

48%*

*mine-to-market margin (excluding metals purchased)

IMPLATS

INTERIM RESULTS FY2021

OPERATIONS REVIEW Mark Munroe

02

12IMPLATS

INTERIM RESULTS FY2021

IMPALA

12

Description H1 FY2021 H1 FY2020 Var (%) Remarks

Tonnes milled kt 5 577 5 739 (3%) • Effective Covid-19 protocols; 9 Shaft closure

6E head grade g/t 4.03 3.91 3% • Reduced waste from 16 Shaft

6E in concentrate koz 660 653 1% • Higher yields

6E refined (Stock

adjusted)koz 670 645 4% • Improved recoveries

6E refined koz 729 761 (4%) • Previous year benefitted from IRS re-allocation

Cash cost Rm 10 560 9 358 (13%)• Covid-related expenditure and costs incurred on

development and asset integrity

Cost per 6E oz (Stock adjusted)

R/oz 15 754 14 515 (9%) • Volume benefits offset cost inflation

Capital expenditure Rm 982 998 2%

Free cash flow Rm 10 656 7 083 50%• Previous period benefitted from metal prepayment

and stock reallocation

*6E refined production (stock-adjusted)

**Cost per 6E ounce (stock-adjusted)

682617 645

470

670

FY2019 FY2020 FY2021

koz

PRODUCTION*

12 461 13 868 14 515 15 735 15 754

FY2019 FY2020 FY2021

R/o

z

COST**

2 228

-352

7 083

1 363

10 656

FY2019 FY2020 FY2021

Rm

FREE CASH FLOW

13IMPLATS

INTERIM RESULTS FY2021

6E OUNCES STOCK-ADJUSTED – H1 FY2021 / H1 FY2020

*costs including SIB capital**cash profit (after tax) after replacement capital

1includes the treatment of dumps, slag and sludge

Production 6E koz 37 45 120 104 7 102 68 66 20 62 27 13

Revenue R/6E oz 34 074 32 053 32 741 25 901 32 996 30 713 35 164 35 556 34 571 35 582 35 556

Cost* R/6E oz 19 075 17 068 17 068 12 626 20 621 20 393 15 814 13 650 18 707 15 266 17 187

Cash Profit / (Loss)** Rm 435 1 171 1 063 72 723 391 845 292 648 289 155

645

670

22

10

5

4 2

1

0 0 0 1

2

15

620

630

640

650

660

670

680

690

H1 FY2020 Other 1# 14# 11# Re-mining 16# 20# 12# E&F 10# 6# 9# H1 FY20211

IMPLATS

INTERIM RESULTS FY2021

OPERATIONS REVIEW Gerhard Potgieter

02

15IMPLATS

INTERIM RESULTS FY2021

MARULA

Description H1 FY2021 H1 FY2020 Var (%) Remarks

Tonnes milled kt 934 970 (4%)• Weak Q2 FY2021 due to Covid-related staffing

challenges

6E head grade g/t 4.40 4.60 (4%) • Negative variance in ratio of stoping to development

6E in concentrate koz 121 124 (2%) • Benefitted from higher recoveries

Cash Cost Rm 1 388 1 276 (9%) • Covid-19 expenditure including shift changes

Cost per 6E oz R/oz 11 433 10 265 (11%)

Capital expenditure Rm 105 204 49% • Slowing spend as TSF project nears completion

Free cash flow Rm 897 431 >100%• Higher basket price partially offset by impact of IRS

contractual payment lag

*6E concentrate production

**Cost per 6E ounce in concentrate

118 99

124

86

121

FY2019 FY2020 FY2021

koz

PRODUCTION*

9 779

11 493

10 265

11 354 11 433

FY2019 FY2020 FY2021

R/o

z

COST**

162 218 431

1 721

897

FY2019 FY2020 FY2021

Rm

FREE CASH FLOW

16IMPLATS

INTERIM RESULTS FY2021

TWO RIVERS

Description H1 FY2021 H1 FY2020 Var (%) Remarks

Tonnes milled kt 1 631 1 646 (1%)• Resolution of milling challenges offset by delayed

return of foreign employees

6E head grade g/t 3.37 3.45 (2%) • Mining from lower grade areas

6E in concentrate koz 150 138 9% • Improved plant performance

Cash Cost Rm 1 526 1 329 (15%) • Mining volumes increased to build ROM stockpile

Cost per 6E oz R/oz 10 153 9 616 (6%)

Capital expenditure Rm 552 391 (41%) • Acceleration of project spend

Free cash flow Rm 721 154 >100%• Higher basket price partially offset by impact of

IRS contractual payment lag

*6E concentrate production

**Cost per 6E ounce in concentrate

161 152 138

123150

FY2019 FY2020 FY2021

koz

PRODUCTION*

7 727 8 568

9 616 9 403 10 153

FY2019 FY2020 FY2021

R/o

z

COST**

64

382

154

1 131

721

FY2019 FY2020 FY2021

Rm

FREE CASH FLOW

17IMPLATS

INTERIM RESULTS FY2021

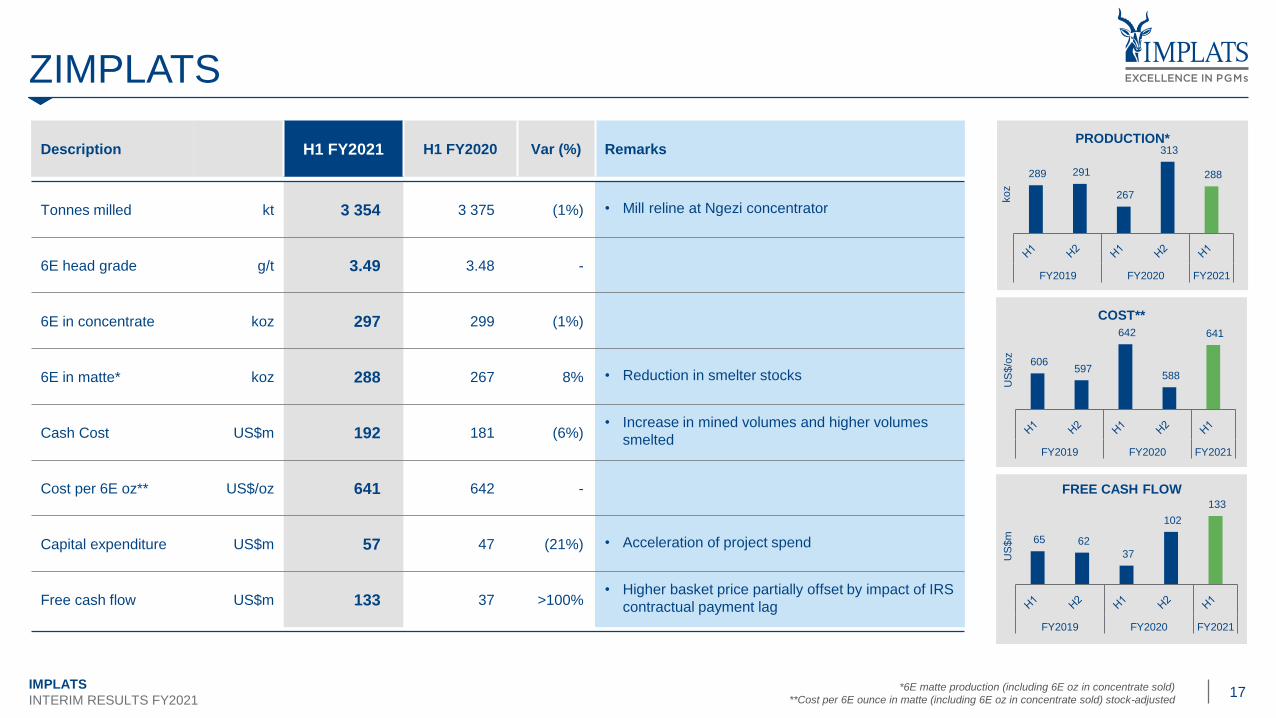

ZIMPLATS

17

Description H1 FY2021 H1 FY2020 Var (%) Remarks

Tonnes milled kt 3 354 3 375 (1%) • Mill reline at Ngezi concentrator

6E head grade g/t 3.49 3.48 -

6E in concentrate koz 297 299 (1%)

6E in matte* koz 288 267 8% • Reduction in smelter stocks

Cash Cost US$m 192 181 (6%)• Increase in mined volumes and higher volumes

smelted

Cost per 6E oz** US$/oz 641 642 -

Capital expenditure US$m 57 47 (21%) • Acceleration of project spend

Free cash flow US$m 133 37 >100%• Higher basket price partially offset by impact of IRS

contractual payment lag

*6E matte production (including 6E oz in concentrate sold)

**Cost per 6E ounce in matte (including 6E oz in concentrate sold) stock-adjusted

606 597

642

588

641

FY2019 FY2020 FY2021

US

$/o

z

COST**

65 62

37

102

133

FY2019 FY2020 FY2021

US

$m

FREE CASH FLOW

289 291

267

313

288

FY2019 FY2020 FY2021

koz

PRODUCTION*

18IMPLATS

INTERIM RESULTS FY2021

MIMOSA

Description H1 FY2021 H1 FY2020 Var (%) Remarks

Tonnes milled kt 1 433 1 306 10% • Prior period impacted by mill breakdown

6E head grade g/t 3.89 3.84 1%

6E in concentrate koz 132 120 10%

Cash Cost US$m 106 100 (6%) • Higher mined, milled and sold volumes

Cost per 6E oz US$/oz 798 830 4%

Capital expenditure US$m 32 25 (29%) • Plant optimisation

Free cash flow US$m 29 9 >100%• Higher sales and basket price partially offset by

impact of IRS contractual payment lag

*6E concentrate production

**Cost per 6E ounce in concentrate

132 129

120

128

132

FY2019 FY2020 FY2021

koz

PRODUCTION*

741

802 830

709

798

FY2019 FY2020 FY2021

US

$/o

z

COST**

-5

-

9

15

29

FY2019 FY2020 FY2021

US

$m

FREE CASH FLOW

19IMPLATS

INTERIM RESULTS FY2021

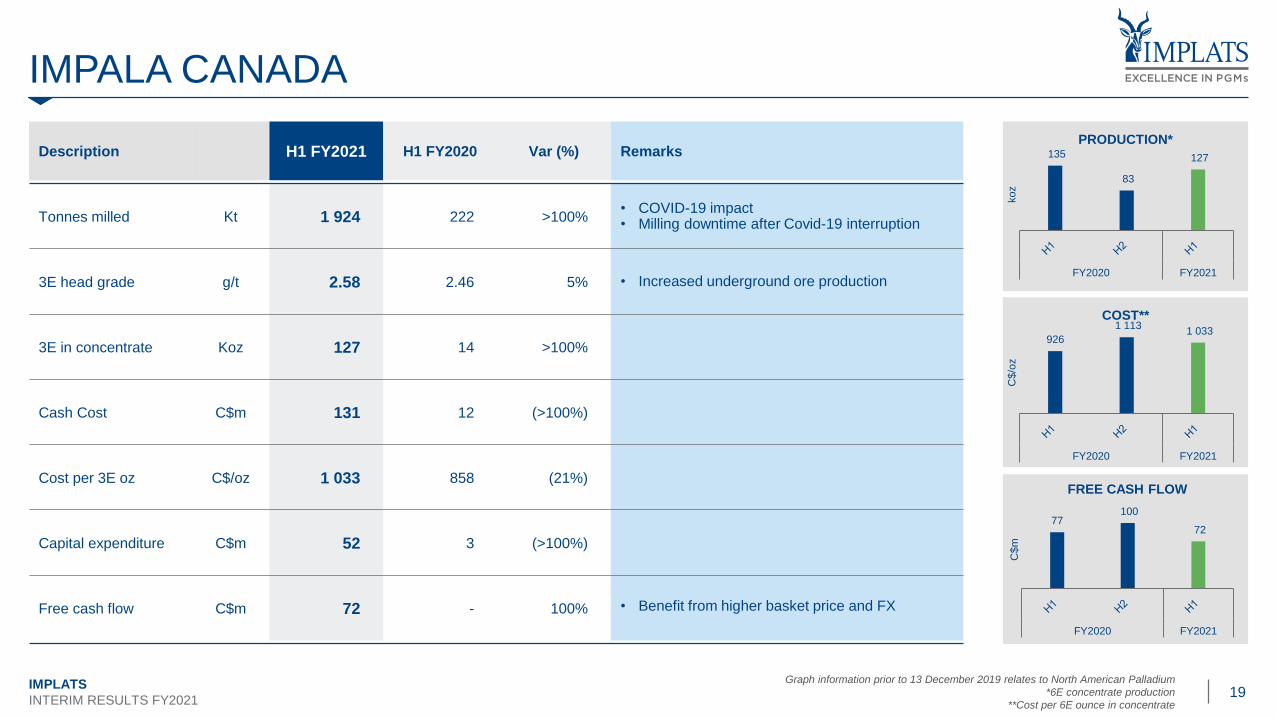

IMPALA CANADA

Description H1 FY2021 H1 FY2020 Var (%) Remarks

Tonnes milled Kt 1 924 222 >100%• COVID-19 impact• Milling downtime after Covid-19 interruption

3E head grade g/t 2.58 2.46 5% • Increased underground ore production

3E in concentrate Koz 127 14 >100%

Cash Cost C$m 131 12 (>100%)

Cost per 3E oz C$/oz 1 033 858 (21%)

Capital expenditure C$m 52 3 (>100%)

Free cash flow C$m 72 - 100% • Benefit from higher basket price and FX

Graph information prior to 13 December 2019 relates to North American Palladium

*6E concentrate production

**Cost per 6E ounce in concentrate

135

83

127

FY2020 FY2021

koz

PRODUCTION*

926

1 113 1 033

FY2020 FY2021

C$/o

z

COST**

77100

72

FY2020 FY2021

C$m

FREE CASH FLOW

20IMPLATS

INTERIM RESULTS FY2021

Description H1 FY2021 H1 FY2020 Var (%) Remarks

Receipts 6Ekoz 943 822 15%• High deliveries from Mimosa, Two Rivers and

Zimplats

Mine-to-market

3rd Party

6Ekoz

6Ekoz

747

196

631

190

18%

3%

Refined output 6Ekoz 845 549 54%• Prior period impacted by IRS/Impala stock

reallocation

Refined metal returned 6Ekoz 0.2 0.6 (67%) • No major toll refining contracts

Free cash flow Rm 4 762 (3 381) >100%• Prior period impacted by metal reallocation

(R5bn)

IRS

696 657 631 582

747

FY2019 FY2020 FY2021

koz

MINE-TO-MARKET RECEIPTS

184 175 190

136

196

FY2019 FY2020 FY2021

koz

THIRD PARTY RECEIPTS

743

2 632

-3 381

3 265 4 762

FY2019 FY2020 FY2021

Rm

FREE CASH FLOW

IMPLATS

INTERIM RESULTS FY2021

FINANCIAL REVIEW Meroonisha Kerber

03

22IMPLATS

INTERIM RESULTS FY2021

INCOME STATEMENT

• Revenue up 107% to R58 billion on higher sales volumes and rand pricing

• 22% increase in 6E sales volumes: ~R6.4 billion

• 55% increased in dollar revenue basket: ~R18.2 billion

• 10% weaker rand exchange rate: ~R5.4 billion

• Cost of sales increased by 64% to R35.8 billion

• Increase in cost of metals purchased ~R7.7 billion

on higher receipts and rand PGM pricing

• Inclusion of Impala Canada cost of sales ~R2.3 billion

• Higher royalties on improved ~R1.5 billion

profitability and revenue

• Impairment reversal of R14.7 billion included in basic earnings

• PPE ~R10.4 billion

• Prepaid royalties ~R4.3 billion

• Other net expenses includes R1.5 billion Marula IFRS 2 BEE non-cash charge.

• No tax impact and included in both EBITDA and headline earnings (-194cps)

• EBITDA > 3x to R25 billion at EBITDA margin of 43%

• Headline earnings improved from 436 to 1 855 cps

R MILLION H1 FY2021 H1 FY2020VARIANCE

(%)

Revenue 58 121 28 019 >100

Cost of sales (35 755) (21 853) (64)

Cash costs (17 648) (14 268) (24)

Royalties (2 021) (488) >100

Metals purchased (16 055) (8 364) (92)

Change in stock 3 519 3 613 3

Other cost of sales (3 550) (2 346) (51)

Gross profit 22 366 6 166 >100

Impairment reversal 14 728 - -

Net foreign exchange (losses)/gains (521) (222) >100

Other net (expenses)/income (1 534) (1 066) (44)

Net finance costs (155) (346) 55

Share of associates income 1 003 247 >100

Profit before tax 35 887 4 779 >100

Tax (10 470) (1 312) >100

Profit after tax 25 417 3 467 >100

GP margin (%) 38 22 75

EBITDA 25 064 7 569 >100

Headline earnings 14 441 3 378 >100

23IMPLATS

INTERIM RESULTS FY2021

STOCK-ADJUSTED UNIT COSTS

Stock adjusted unit costs increased by 9% to R14 292 per ounce

• Overall Implats mining inflation of 6.7%

• SA +5.9%

• Zimbabwe (US$) +0.7%

• Weaker rand on the translation of Zimplats US dollar costs

• Covid-19 related direct expenditure of R283 million

Implats incurred additional spend on:

• Higher production bonuses in line with above-budget volume achievements

at all operations

• Additional development at Impala to improve mining flexibility, and

• Targeted spend on asset integrity

23

13 157

14 292

633

248

237

16

H1 FY2020 Inflation TranslationZimplats USdollar costs

Covid-19 costs Other H1 FY2021

(R/6

E o

z)

STOCK-ADJUSTED UNIT COST

24IMPLATS

INTERIM RESULTS FY2021

EXCESS INVENTORY

• Excess in-process 6E stock of 100 000 oz 6E unchanged from June 2020

• Material stockpiled in Zimbabwe in FY2020 due to force majeure was delivered

to the refineries

• All excess IRS pre-smelter stock was treated

• BMR processing impacted in December 2020 due to impurities in the feed

• Planned furnace maintenance at Zimplats and Rustenburg in Q3 FY2020

• All excess stock is expected to be refined by the end of FY2021

• Financial impact of excess stock at period-end metal prices:

• Gross profit c.R2.1 billion

• Cash flow c.R2.6 billion 215

350

100 100

0

0

50

100

150

200

250

300

350

FY2019 H1 FY2020 FY2020 H1 FY2021 FY2021

000 o

z 6

E

EXCESS WORK IN PROCESS STOCK AT PERIOD END

25IMPLATS

INTERIM RESULTS FY2021

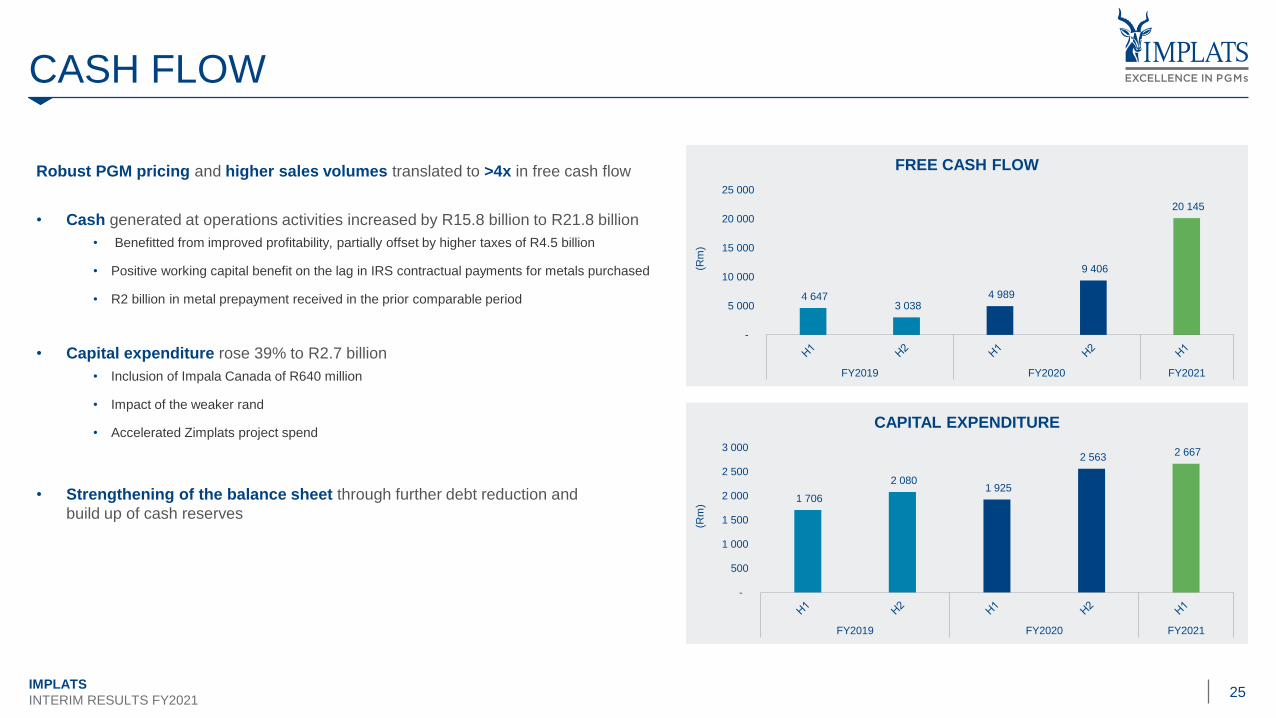

CASH FLOW

Robust PGM pricing and higher sales volumes translated to >4x in free cash flow

• Cash generated at operations activities increased by R15.8 billion to R21.8 billion

• Benefitted from improved profitability, partially offset by higher taxes of R4.5 billion

• Positive working capital benefit on the lag in IRS contractual payments for metals purchased

• R2 billion in metal prepayment received in the prior comparable period

• Capital expenditure rose 39% to R2.7 billion

• Inclusion of Impala Canada of R640 million

• Impact of the weaker rand

• Accelerated Zimplats project spend

• Strengthening of the balance sheet through further debt reduction and

build up of cash reserves

4 647 3 038

4 989

9 406

20 145

-

5 000

10 000

15 000

20 000

25 000

FY2019 FY2020 FY2021

(Rm

)

FREE CASH FLOW

1 706

2 080 1 925

2 563 2 667

-

500

1 000

1 500

2 000

2 500

3 000

FY2019 FY2020 FY2021

(Rm

)

CAPITAL EXPENDITURE

26IMPLATS

INTERIM RESULTS FY2021

CASH NET OF DEBT

• Cash net of debt of R20.3 billion

• Reduction in debt:

• Expedited repayment of Impala Canada term loan of R1.4 billion

• Scheduled payment of Marula BEE debt of R885 million

• Reduced carrying value of ZAR convertible bond following repurchase

and conversion

• Group headroom at period end of R28.5 billion:

• R24.8 billion cash, excluding restricted cash R349 million

• Undrawn RCF of R4 billion in place until June 2021

• RCF successfully refinanced post period-end:

• R6 billion and US$125m

• Group of domestic and international banks

• Effective increase in headroom to c.R32.3 billion

2

6

R MILLION H1 FY2021 H1 FY2020 FY2020

South African cash 20 713 5 256 9 689

Offshore cash 4 124 740 3 642

Gross cash 24 837 5 996 13 331

ZAR Convertible bond (2 533) (2 838) (2 914)

Marula BEE debt - (886) (885)

Zimplats overdraft (174) - (126)

Impala Canada term loan (1 848) (4 215) (3 658)

Gross debt (excluding leases) (4 555) (7 939) (7 583)

Net cash / (debt) excluding leases 20 282 (1 943) 5 748

(976)

1 075

(1 943)

5 748

20 282

-5 000

0

5 000

10 000

15 000

20 000

25 000

FY2019 FY2020 FY2021

(Rm

)

NET CASH / (DEBT)

27IMPLATS

INTERIM RESULTS FY2021

CAPITAL ALLOCATION FRAMEWORK AND H1 FY2021 DIVIDEND

BALANCE SHEET STRENGTH

• Repayment of Marula BEE loan (R0.9 billion)

• Repayment of borrowings (R1.5 billion)

• Repurchase of ZAR bonds liability portion (R0.2 billion)

• Provision for future rehabilitation obligations (R1.0

billion)

• Retained cash (R5.7 billion)

RETURNS TO SHAREHOLDERS

• Interim dividend – proposed (R7.9 billion)

• Zimplats minorities (R0.1 billion)

• Repurchase of ZAR bonds equity portion (R0.8 billion)

GROWTH AND INVESTMENT

• Investment in AP Ventures (R0.1 billion)

R9.3bn

R8.8bn

R0.1bn

FR

EE

CA

SH

FL

OW

* O

F R

18.2

BIL

LIO

N

DISCIPLINED AND TRANSPARENT CAPITAL ALLOCATION TO ENSURE A SUSTAINABLE BUSINESS AND CREATE VALUE FOR ALL STAKEHOLDERS

STAY-IN-BUSINESS CAPEX

• Required infrastructure

replacement investment

• Required spend on regulatory

capitalCash from operations of

R27.0bn

R 2.5bn outflowOTHER NET INCOME

• Interest received of +R0.4bn

• Dividends of +R0.5bn

R0.9bn inflow

TAXES PAID

R 5.0bn outflow

INTEREST PAID

R 0.3bn outflow

OTHER OUTFLOWS*

• Share scheme - R1.3bn

• FX cash adjustment –R0.6bn

R 1.9bn outflow

* Free cash flow adjusted for outflows/impacts relating to foreign exchange translation adjustment on

cash and cost of purchasing of shares for the Implats share schemes (included under “other outflows”

IMPLATS

INTERIM RESULTS FY2021

MARKET REVIEW Sifiso Sibiya

04

29IMPLATS

INTERIM RESULTS FY2021

METAL PRICE PERFORMANCE - MARKET

Description H1 FY2021 H1 FY2020 Var (%)

Platinum US$/oz 921 895 3%

Palladium US$/oz 2 258 1 666 35%

Rhodium US$/oz 12 824 4 849 164%

Nickel US$/t 15 086 15 489 (3%)

Exchange rate US$/oz 16.26 14.69 11%

Basket price index R/6E oz 34 305 20 409 68%

Revenue per oz sold R/6E oz 35 635 20 888 71%

20 000

25 000

30 000

35 000

40 000

45 000

1 200

1 400

1 600

1 800

2 000

2 200

2 400

2 600

2 800

3 000

Rands

US

$/o

z

IMPALA BASKET PRICE PER 6E OUNCE

US$ Basket/6E oz Rand Basket/6E oz

30IMPLATS

INTERIM RESULTS FY2021

21%

29%

44%

6%

IMPALA

18%

35%

36%

3%8%

IRS

18%

37%

36%

2%7%

IMPLATS

14%

34%40%

1%9%

2%

MARULA

18%

25%

44%

1%10%

2%

TWO RIVERS

17%

36%20%

4%

17%

6%

ZIMPLATS

20%

38%

17%

9%

11%

5%

MIMOSA

2%

88%

3%7%

IMPALA CANADA

PGM REVENUE BASKETS H1 FY2021

REVENUE CONTRIBUTION BY METAL

Platinum OtherFV pricesNickelRhodiumPalladium

Revenue of

R23.1bn

Revenue of

R4.5bnRevenue of

R5.3bn

Revenue of

R10.7bn

Revenue of

R58.1bnRevenue of

R5.3bn

Revenue of

R4.4bn

Revenue of

R30.4bn

31IMPLATS

INTERIM RESULTS FY2021

MARKET DEVELOPMENT

Anticipate and

respond to

medium and

longer term

market forces

ANTICIPATE

1

Defend markets

or metals where

fundamental

support is

waning

DEFEND

2

De-risk expected

growth to ensure

successful

adoption of

PGM bearing

technologies and

uses

DE-RISK

3

Target spend and

seek

collaboration

across peer

group and

customer base

TARGET

4

Support

sustainable

patterns of

demand for our

primary products

SUPPORT

5

Harness the

benefits of PGM

demand growth

for all our

stakeholders

HARNESS

6

In December 2020 Implats announced its investment in AP Ventures

- Limited Partner and Advisory Board Member

- Total commitment of US$61m with 1H 2021 spend of R130m

- Core linkages and strong developmental commitment to South Africa

32IMPLATS

INTERIM RESULTS FY2021

SUPPLY AND DEMAND BALANCES

2021 platinum market to return to surplus

- Demand expected to rebound by 17%

• European automotive production recovery

• Catalyst loadings to rise on HDD legislation, initial switching

• Jewellery rebound on pent-up demand, Indian recovery and ‘reboot’ in China

• Industrial recovery bolstered by investment in capacity

- Supply to grow by 28% on South African recovery and de-stocking of producer inventory

- Continued momentum in physical investment demand could tighten market

2021 palladium market to remain in deficit

- Demand estimated to rise by 12%

• Automotive production in excess of sales to replenish inventories

• Thrifting on loadings ahead of next phase of legislative tightening

• Industrial demand reflects ongoing price elasticity of demand

• Further clarity on rate and scope of switching

- Supply to grow by 18% with rebound in secondary flows and South African recovery

- Deficit despite destocking of peer group inventory

2021 rhodium market balanced by inventory release

- Demand growth of 12% on automotive production growth

- South African supplies temporarily elevated on inventory release

- Supply side concerns likely to lead to opportunistic accumulation of metal where possible

-1 500

-1 000

-500

0

500

1 000

1 500

2019 2020 2021

koz

SUPPLY/DEMAND BALANCES*

Platinum Palladium Rhodium

* 2019 balance includes 1.15Moz of Pt investment and 75koz of Pd disinvestment

* 2020 balance includes 1.18Moz of Pt investment and 90koz Pd disinvestment

33IMPLATS

INTERIM RESULTS FY2021

Platinum fundamentals set to improve in the medium-term - price

will be dictated by investor sentiment

Our supply outlook is largely unaltered

Palladium and rhodium demand underpinned by resurgent

automotive production in excess of sales

Iridium and ruthenium demand growth from industrial application

and strong linkages to hydrogen economy

The impact of Covid-19 will be cyclical rather than structural

PGM MARKET OUTLOOK

Ir

Ru

Pt

Pd

Rh

IMPLATS

INTERIM RESULTS FY2021

BUSINESS OUTLOOK Nico Muller

05

35IMPLATS

INTERIM RESULTS FY2021

GROUP OUTLOOK

ACTUAL PREV GUIDANCE NEW GUIDANCE

Business area Unit FY2020 FY2021 FY2021

REFINED PRODUCTION:

Group6E koz 2 813 2 800 – 3400 3 200 – 3 460

CONCENTRATE PRODUCTION:

Impala 6E koz 1 109 1 100 – 1 270 1 200 – 1 300

Zimplats 6E koz 597 570 – 600 580 – 600

Two Rivers 6E koz 261 260 – 300 280 – 300

Mimosa 6E koz 248 230 – 260 250 – 270

Marula 6E koz 210 220 – 260 220 – 260

Impala Canada 6E koz 97 250 – 280 260 – 280

IRS (third party) 6E koz 327 300 – 380 360 – 400

GROUP UNIT COST* R/oz 6E 13 345 14 500 – 15 500 14 600 – 15 100

GROUP CAPITAL EXPENDITURE* Rm 4 488 6 000 – 6 750 5 800 – 6 200

* guidance premised on R/US$ 15.62 and R/C$ 12.00

INTERIM RESULTS FY202125 February 2021

37IMPLATS

INTERIM RESULTS FY2021

16 SHAFT

16 SHAFT

Description H1 FY2021 H1 FY2020

Project completion % 97.6 94.3

Estimated completion date date Nov 21 Nov 21

Approved capital Rm 7 899 7 939

Estimate at completion Rm 7 899 7 939

Expenditure to date Rm 7 707 7 484

Estimated steady-state achievement date Oct 22 Jun 22

Design production (6E at steady state) koz per annum 330 330

6E production koz 102 101

Mineable face length (31 Dec) m 4 813 3 879

Stoping teams (31 Dec) teams 122 120

Panel Ratio (31 Dec)* panels/team 1.67 1.45

Average Productivity (full year)* ca/team/month 240 283

Unit cost (excl. project capital) R/6E oz 20 621 17 012

* Based on producing stoping teams and 25 m panel

38IMPLATS

INTERIM RESULTS FY2021

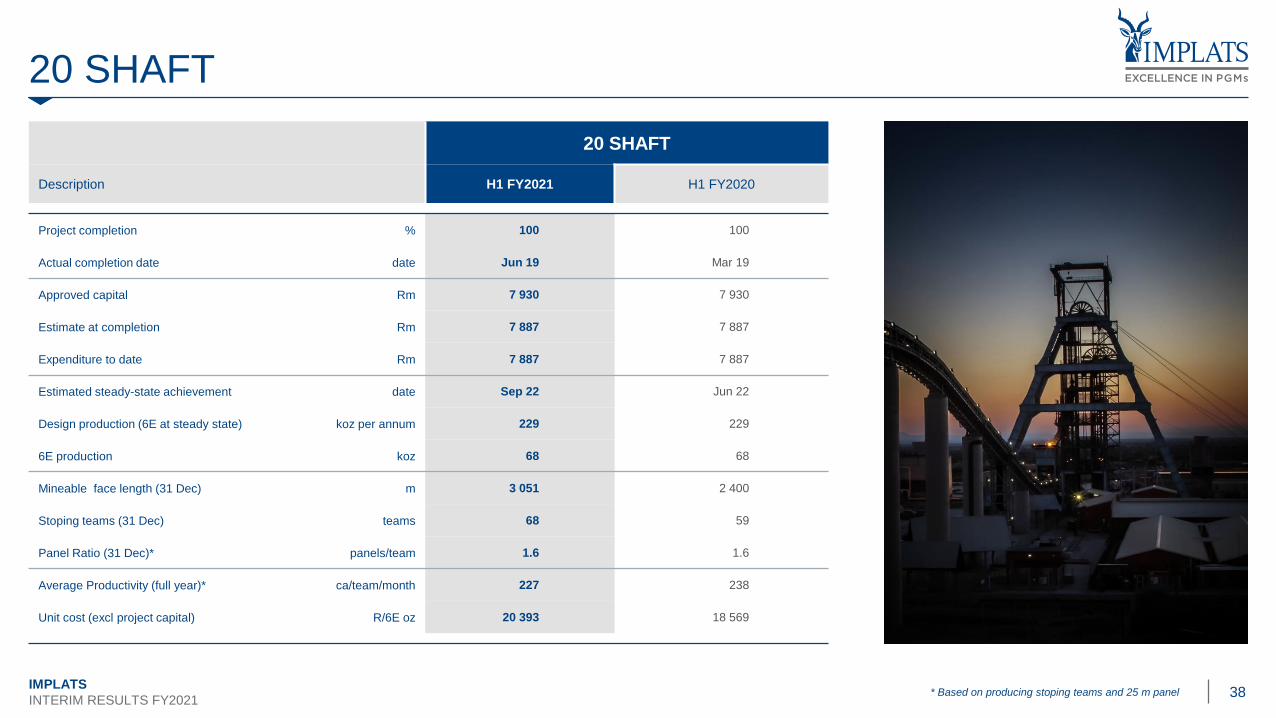

20 SHAFT

20 SHAFT

Description H1 FY2021 H1 FY2020

Project completion % 100 100

Actual completion date date Jun 19 Mar 19

Approved capital Rm 7 930 7 930

Estimate at completion Rm 7 887 7 887

Expenditure to date Rm 7 887 7 887

Estimated steady-state achievement date Sep 22 Jun 22

Design production (6E at steady state) koz per annum 229 229

6E production koz 68 68

Mineable face length (31 Dec) m 3 051 2 400

Stoping teams (31 Dec) teams 68 59

Panel Ratio (31 Dec)* panels/team 1.6 1.6

Average Productivity (full year)* ca/team/month 227 238

Unit cost (excl project capital) R/6E oz 20 393 18 569

Photo: Jacques McCarthy* Based on producing stoping teams and 25 m panel

39IMPLATS

INTERIM RESULTS FY2021

MUPANI

MUPANI

Description H1 FY2021 H1 FY2020

Project completion % 47 39

Estimated completion date date Jul-24 Jul-24

Approved capital US$m 264 264

Estimate at completion US$m 260 258

Expenditure to date US$m 123 80

Design production (nominal 6E value

in matte at steady state )

koz per

annum192 192

Estimated steady-state achievement date Sep-24 Jul-24

Planned 6E production (in ore) koz 8.8 7.4

40IMPLATS

INTERIM RESULTS FY2021

ESG INDICATORS

H1

FY2021 H1 FY2020 Var (%) Remarks

Level 4 or 5

environmental incidentscount 0 0 0% • Maintained

Level 3 environmental

incidentsCount 3 9 67%

• Group-wide environmental awareness

initiatives continue to be rolled-out at all

operations

Water recycled or

reused% 47 40 18%

• Above 44% target (2021)

• Inclusion of Impala Canada (higher recycling

rates (>70%))

Energy consumption GJ/t milled 0.81 0.83 3%• Load shedding and curtailments from Eskom

• Benefit of inclusion of tonnage from Impala

Canada and hydro power electricity supplyScope 1 and 2 carbon

emissionsCO2 t/t milled 0.17 0.19 11%

Local procurement

spendRm 1 836 1 459 26%

• Increase in expenditure to direct production-

related suppliers (predominantly local

Tier 1 and 2).

ESG

• Marula, Impala Refineries and Zimplats operations were recertified ISO 14001:2015 compliant (Canada developing a

gap analysis)

• Refineries, Marula and Zimplats were certified ISO 45001:2018 (safety management systems standard) compliant

• Ongoing initiatives to support host communities during the Covid-19 pandemic

• Additional R10 million donated to Gift of the Givers Foundation to assist host communities and labour-sending areas

41IMPLATS

INTERIM RESULTS FY2021

ITEMS IMPLATS IMPALA ZIMPLATSIMPALA

CANADAMARULA MIMOSA TWO RIVERS TOTAL

Rm Rm US$000 C$000 Rm US$000 Rm Rm

1. Isolation facilities - 50.9 1 460 - 1.4 151 0.3 78.8

2. Employee related costs - 50.8 108 326 13.8 89 6.0 77.8

3. Medical equipment / medicine - 35.7 87 1 0.0 202 1.0 41.4

4. Protective clothing and equipment - 14.9 48 78 0.6 1 350 0.9 40.0

5. Donations 10.0 5.0 111 - 2.1 1 004 0.3 35.5

6. Cleaning consumables / services - 8.0 247 536 1.0 188 1.6 24.3

7. Expenses for staff in quarantine - 7.2 352 67 1.8 43 5.0 21.2

8. Awareness campaigns - 5.4 40 142 0.5 99 0.2 10.1

9. Other - 12.6 293 - 2.3 337 0.2 25.5

TOTAL 10.0 190.6 2 745 1 150 23.5 3 463 15.5

R354.8mTOTAL RAND MILLION 10.0 190.6 44.6 14.1 23.5 56.6 15.5

COVID-19 RELATED COST (H1 FY2021)

41