intermarket divergencefree revised

TRANSCRIPT

7/24/2019 Intermarket DivergenceFree Revised

http://slidepdf.com/reader/full/intermarket-divergencefree-revised 1/10

Traders Management © 2014 All Rights Reserved Page 1

Inter Market Divergence Free

For TradeStation 9.X

7/24/2019 Intermarket DivergenceFree Revised

http://slidepdf.com/reader/full/intermarket-divergencefree-revised 2/10

Traders Management © 2014 All Rights Reserved Page 2

Overview of Inter‐market Analysis and Trading Systems

Over the past over 15 years, I have used inter-market analysis to develop trading systems

for many different markets. Examples include: the S&P500, Treasury bonds, Ten year note,

Eurodollars, gold, crude oil and more. Even with this said; I have done little on using inter-

market analysis with currencies. In this special report I will analyze inter-market analysis for

currency traders. Let’s first review the basics of inter-market analysis.

In John Murphy's first book, published in 1991 on Inter-market Analysis; he used the

crash of 1987 to lay out his Inter-market hypothesis. The problem is that until I built and

published Inter-market based trading systems in 1994, no one had confirmed his work in a public

forum. Many institutional traders used the concepts, but rules to mechanical trading systems,

which used Inter-market Analysis, were not generally publicly available. I developed a very

simple concept for an Inter-market Based system.

For positively correlated markets we have as follows:

If Inter-market is in an uptrend and traded market in a down trend then buy.

If Inter-market is in a down trend and traded market is in an uptrend then sell.

You can use various concepts to define an up and down trend. In most of my work I used prices

that were relative to a moving average.

For negatively correlated markets we have as follows:

If Inter-market is in an uptrend and traded market in an uptrend then sell.

If Inter-market is in a down trend and traded market is in a down trend then buy.

We define trend as the “Sign of price relative to a selected moving average length”. The traded

market and inter-market can have different length moving averages.

I developed this concept because most of my inter-market work was based on the futures

7/24/2019 Intermarket DivergenceFree Revised

http://slidepdf.com/reader/full/intermarket-divergencefree-revised 3/10

Traders Management © 2014 All Rights Reserved Page 3

market and using back adjusted futures contracts you can’t take ratios so this inter-market

divergence of price minus a moving average solved this issue.

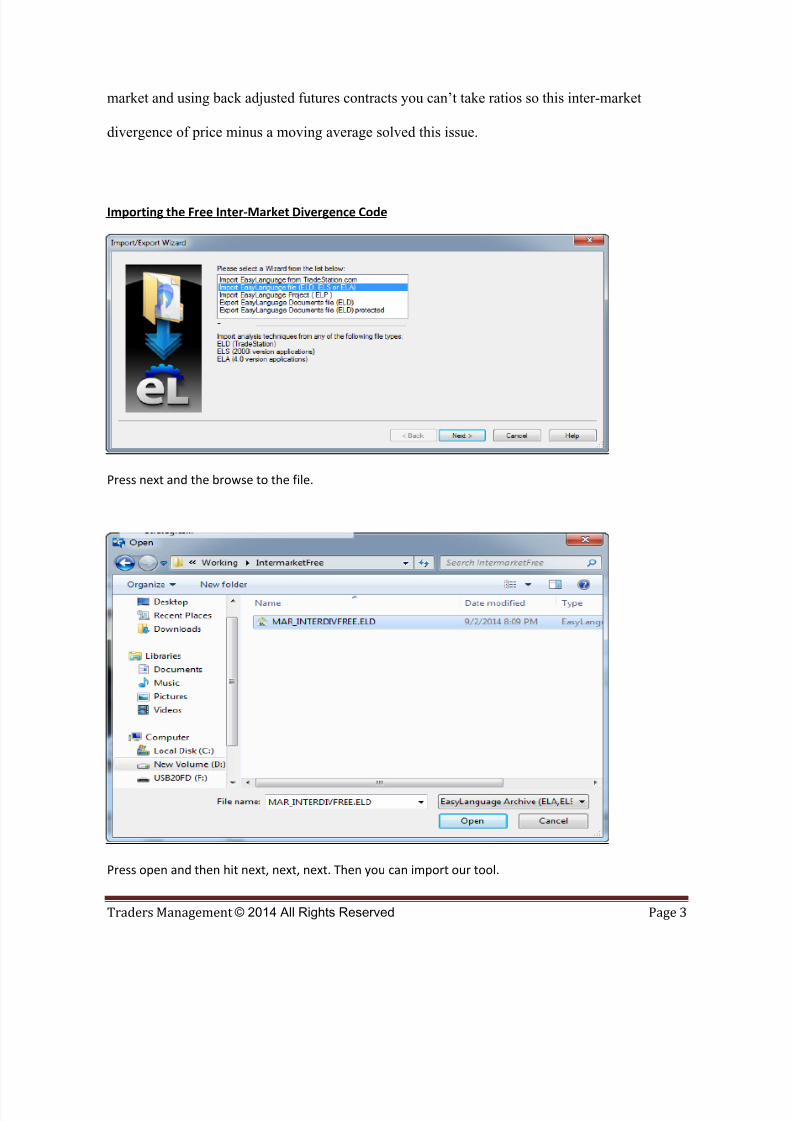

Importing the Free Inter‐Market Divergence Code

Press next and the browse to the file.

Press open and then hit next, next, next. Then you can import our tool.

7/24/2019 Intermarket DivergenceFree Revised

http://slidepdf.com/reader/full/intermarket-divergencefree-revised 4/10

Traders Management © 2014 All Rights Reserved Page 4

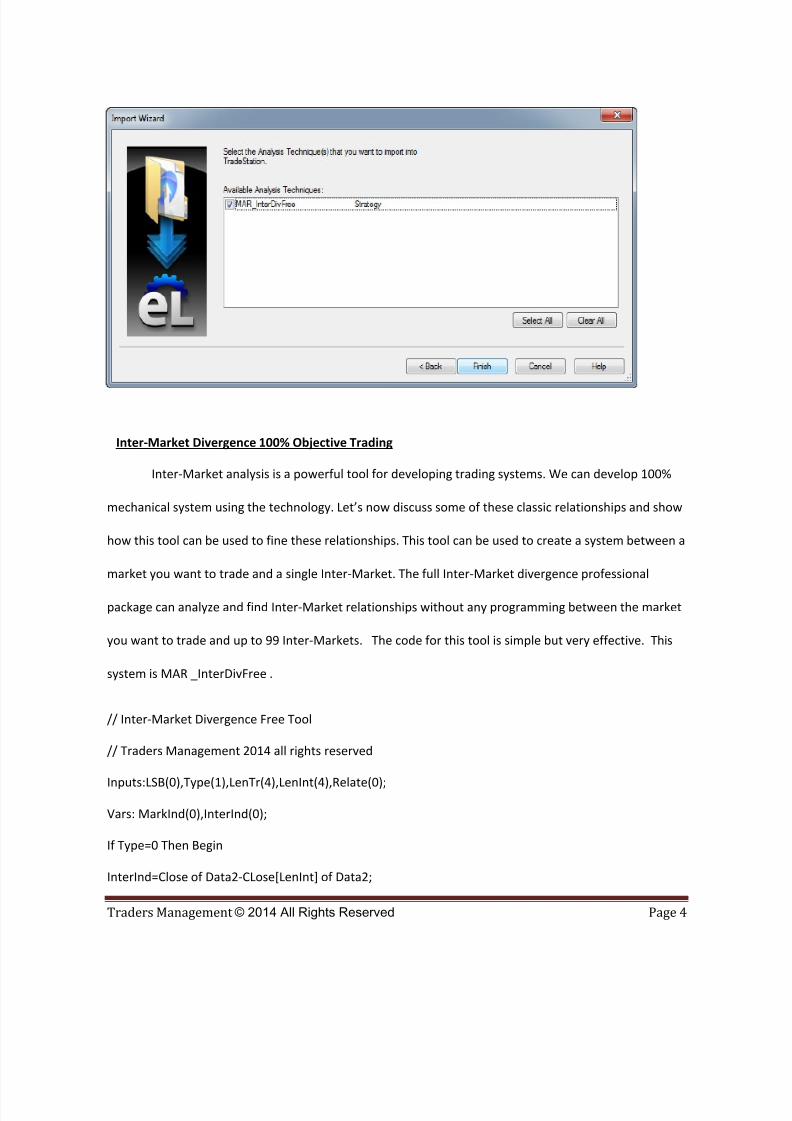

Inter‐Market Divergence 100% Objective Trading

Inter‐Market analysis is a powerful tool for developing trading systems. We can develop 100%

mechanical system using the technology. Let’s now discuss some of these classic relationships and show

how this tool can be used to fine these relationships. This tool can be used to create a system between a

market you

want

to

trade

and

a single

Inter

‐Market.

The

full

Inter

‐Market

divergence

professional

package can analyze and find Inter‐Market relationships without any programming between the market

you want to trade and up to 99 Inter‐Markets. The code for this tool is simple but very effective. This

system is MAR _InterDivFree .

// Inter‐Market Divergence Free Tool

//

Traders

Management

2014

all

rights

reserved

Inputs:LSB(0),Type(1),LenTr(4),LenInt(4),Relate(0);

Vars: MarkInd(0),InterInd(0);

If Type=0 Then Begin

InterInd=Close of Data2‐CLose[LenInt] of Data2;

7/24/2019 Intermarket DivergenceFree Revised

http://slidepdf.com/reader/full/intermarket-divergencefree-revised 5/10

Traders Management © 2014 All Rights Reserved Page 5

MarkInd=CLose‐CLose[LenTr];

end;

If Type=1 Then Begin

InterInd=Close of

Data2

‐Average(CLose

of

Data2,LenInt);

MarkInd=CLose‐Average(CLose,LenTr);

end;

if Relate=1 then begin

If InterInd>0 and MarkInd<0 and LSB>=0 then Buy Next Bar at open;

If InterInd<0 and MarkInd>0 and LSB<=0 then Sell Short Next Bar at open;

If InterInd>0

and

MarkInd<0

then

Buy

to

Cover

Next

Bar

at

open;

If InterInd<0 and MarkInd>0 then Sell Next Bar at open;

end;

if Relate=0 then begin

If InterInd<0 and MarkInd<0 and LSB>=0 then Buy Next Bar at open;

If InterInd>0 and MarkInd>0 and LSB<=0 then Sell Short Next Bar at open;

If InterInd<0

and

MarkInd<0

then

Buy

to

Cover

Next

Bar

at

open;

If InterInd>0 and MarkInd>0 then Sell Next Bar at open;

end;

Let’s show how this simple Inter‐Market tool can be used to create a very effective 30 year

Treasury bond system. We will use the @US continuous contract to trade and $UTY which is the

Philadelphia electrical utility

average

as

our

Inter

‐Market.

7/24/2019 Intermarket DivergenceFree Revised

http://slidepdf.com/reader/full/intermarket-divergencefree-revised 6/10

Traders Management © 2014 All Rights Reserved Page 6

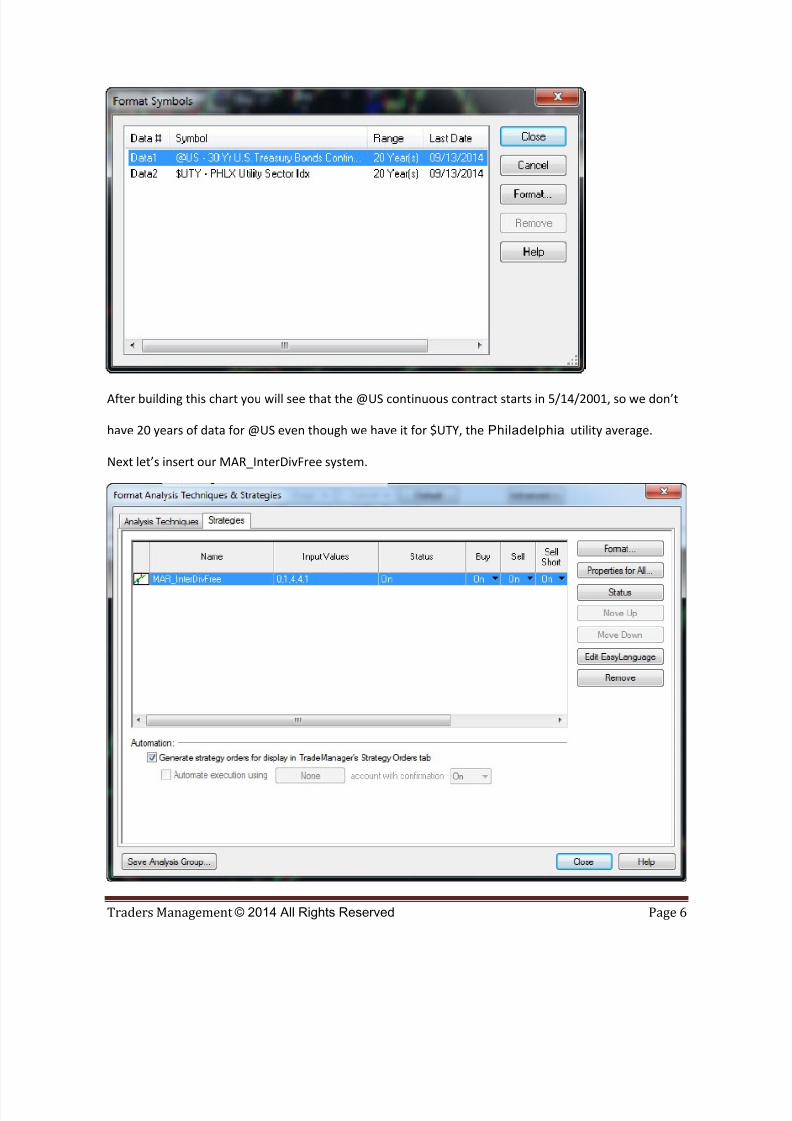

After building this chart you will see that the @US continuous contract starts in 5/14/2001, so we don’t

have 20 years of data for @US even though we have it for $UTY, the Philadelphia utility average.

Next let’s insert our MAR_InterDivFree system.

7/24/2019 Intermarket DivergenceFree Revised

http://slidepdf.com/reader/full/intermarket-divergencefree-revised 7/10

Traders Management © 2014 All Rights Reserved Page 7

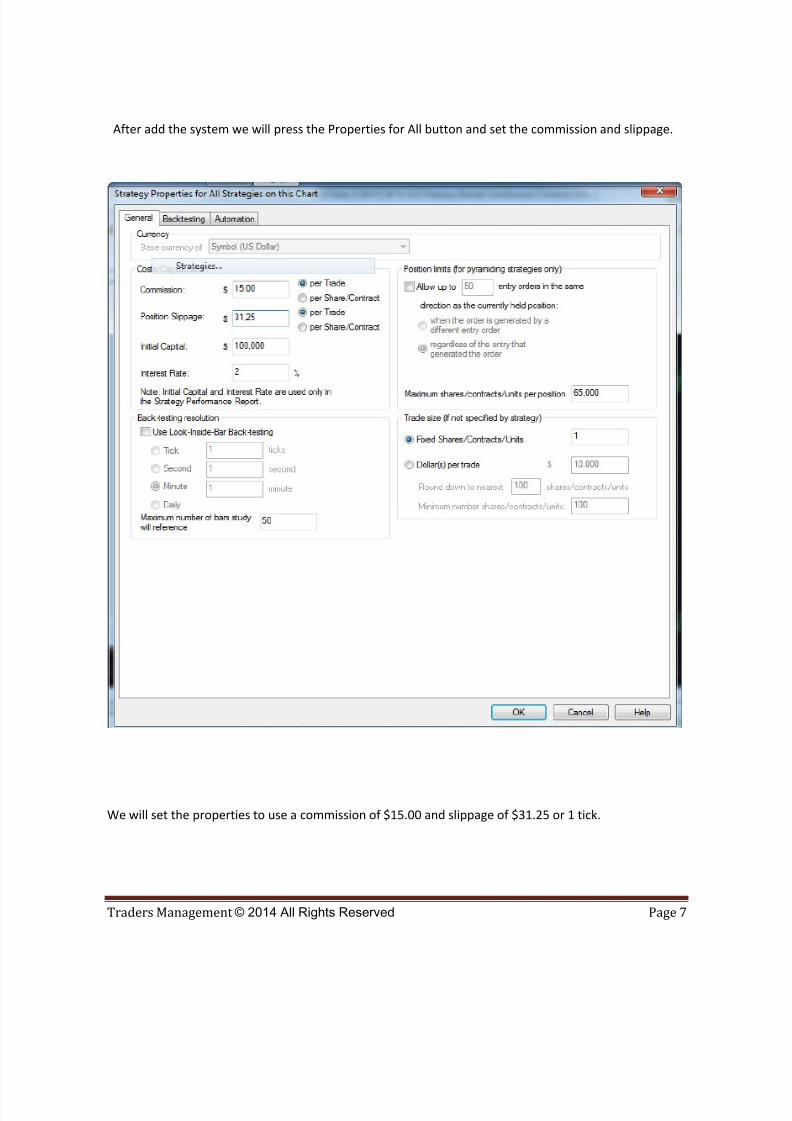

After add the system we will press the Properties for All button and set the commission and slippage.

We will set the properties to use a commission of $15.00 and slippage of $31.25 or 1 tick.

7/24/2019 Intermarket DivergenceFree Revised

http://slidepdf.com/reader/full/intermarket-divergencefree-revised 8/10

Traders Management © 2014 All Rights Reserved Page 8

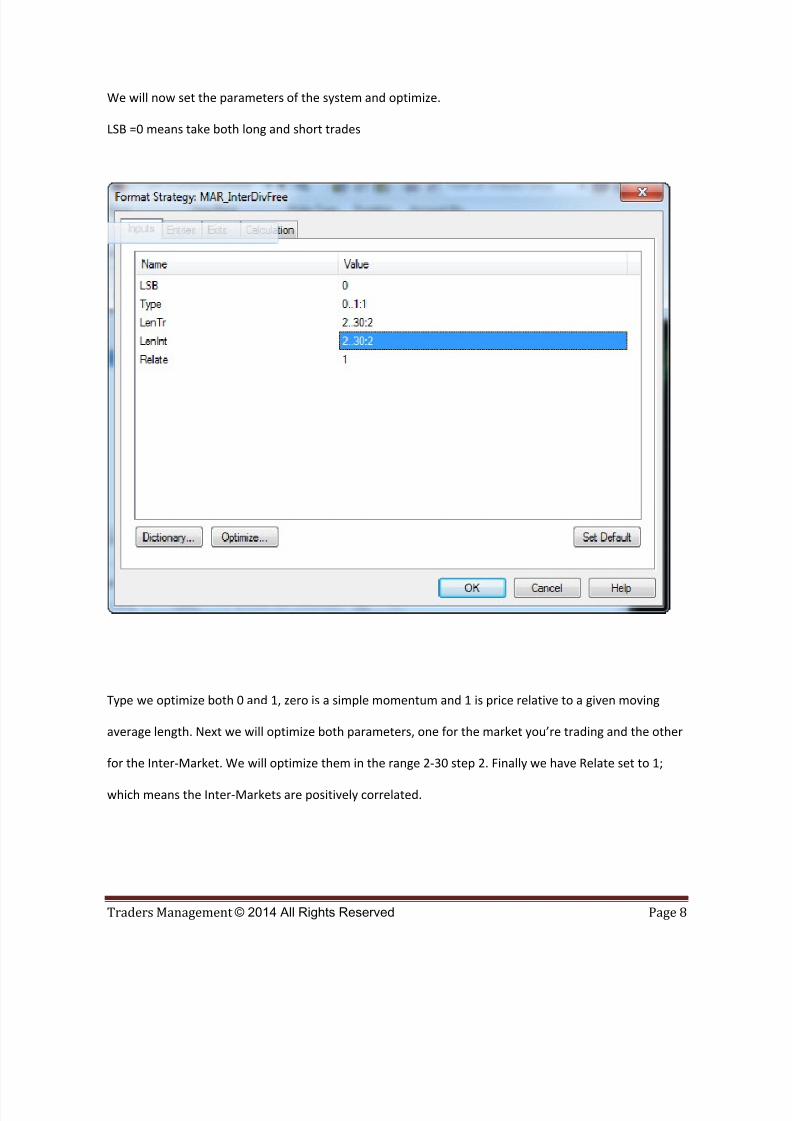

We will now set the parameters of the system and optimize.

LSB =0 means take both long and short trades

Type we optimize both 0 and 1, zero is a simple momentum and 1 is price relative to a given moving

average length. Next we will optimize both parameters, one for the market you’re trading and the other

for the

Inter

‐Market.

We

will

optimize

them

in

the

range

2‐30

step

2.

Finally

we

have

Relate

set

to

1;

which means the Inter‐Markets are positively correlated.

7/24/2019 Intermarket DivergenceFree Revised

http://slidepdf.com/reader/full/intermarket-divergencefree-revised 9/10

Traders Management © 2014 All Rights Reserved Page 9

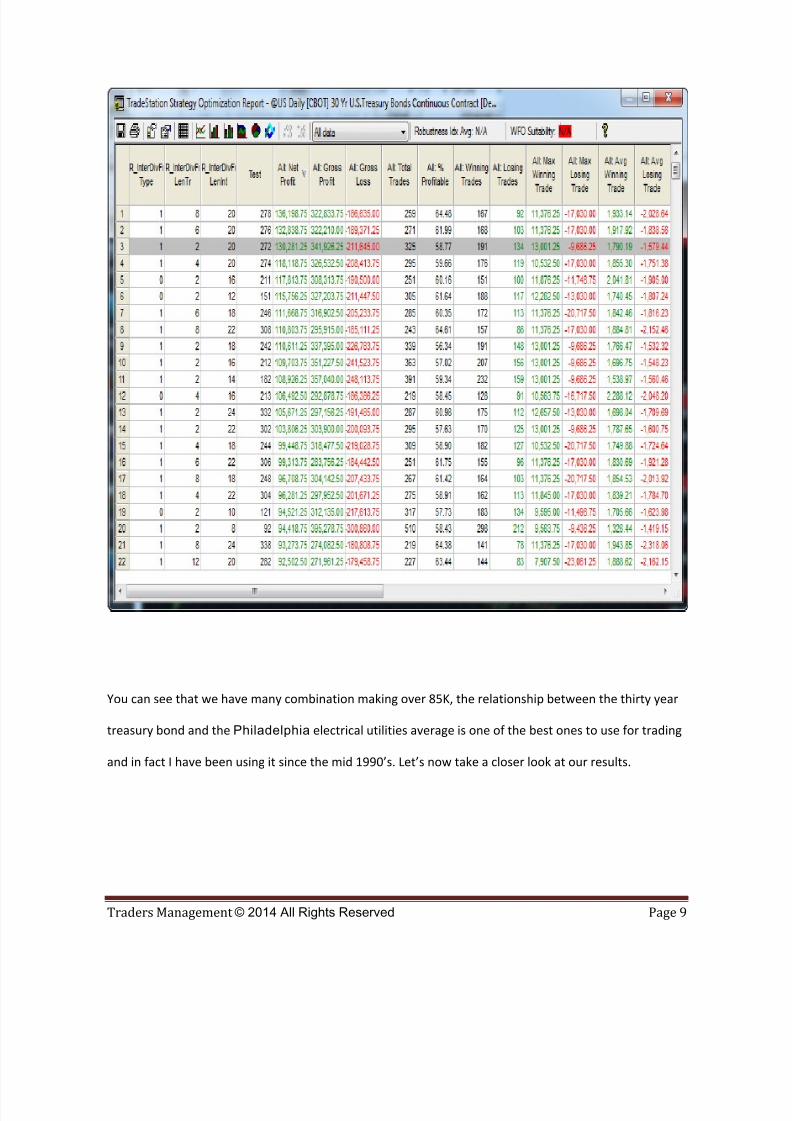

You can see that we have many combination making over 85K, the relationship between the thirty year

treasury bond and the Philadelphia electrical utilities average is one of the best ones to use for trading

and in

fact

I have

been

using

it

since

the

mid

1990’s.

Let’s

now

take

a closer

look

at

our

results.

7/24/2019 Intermarket DivergenceFree Revised

http://slidepdf.com/reader/full/intermarket-divergencefree-revised 10/10

Traders Management © 2014 All Rights Reserved Page 10

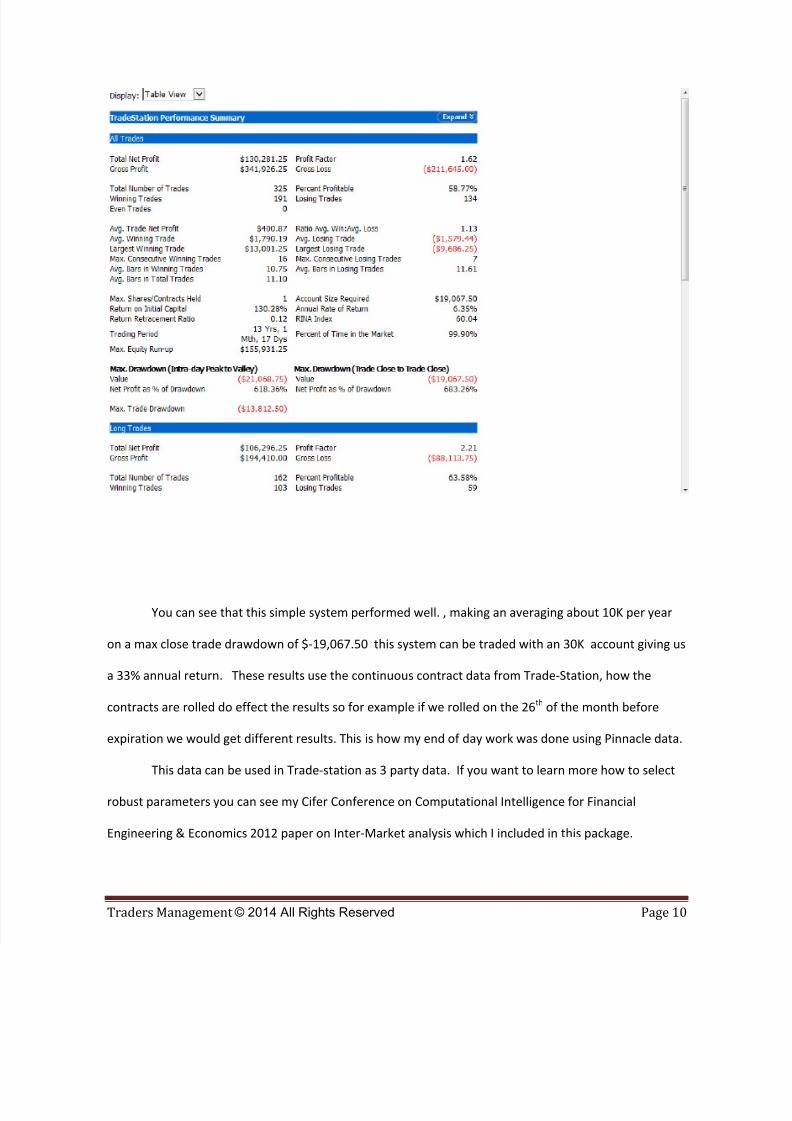

You can see that this simple system performed well. , making an averaging about 10K per year

on a max close trade drawdown of $‐19,067.50 this system can be traded with an 30K account giving us

a 33% annual return. These results use the continuous contract data from Trade‐Station, how the

contracts are rolled do effect the results so for example if we rolled on the 26th of the month before

expiration we would get different results. This is how my end of day work was done using Pinnacle data.

This data can be used in Trade‐station as 3 party data. If you want to learn more how to select

robust parameters you can see my Cifer Conference on Computational Intelligence for Financial

Engineering & Economics 2012 paper on Inter‐Market analysis which I included in this package.